Market Definition

The 3D Printing (Additive Manufacturing) market comprises a comprehensive ecosystem of hardware, materials, software, and services used to manufacture components layer-by-layer from digital design files. The market includes industrial 3D printers, desktop and professional systems, metal and polymer additive manufacturing equipment, specialty materials (powders, filaments, resins), design and simulation software, and contract manufacturing/service bureaus.

3D printing forms a critical pillar of modern advanced manufacturing by enabling rapid prototyping, part consolidation, mass customization, lightweighting, and decentralized production. It serves key sectors including aerospace, automotive, healthcare, consumer electronics, construction, defense, and industrial machinery.

Over the past two years, the global 3D printing industry has undergone structural transformation driven by the transition from prototyping to end-use part production, expansion in metal additive manufacturing, supply chain localization initiatives, and rising demand for lightweight and high-performance components. The sector has also been influenced by raw material price volatility (metal powders and specialty polymers), semiconductor shortages affecting printer electronics, and increasing enterprise adoption of digital manufacturing workflows.

Market Insights

Global demand for 3D printing has been strongly shaped by industrial digitalization, supply chain resilience strategies, and the push toward localized manufacturing. The years 2021–2022 saw strong momentum as manufacturers adopted additive manufacturing to mitigate supply chain disruptions, reduce inventory risks, and accelerate product development cycles. Aerospace and medical sectors led adoption of certified metal additive manufacturing, while automotive expanded tooling and lightweight applications.

In 2023–2025, adoption shifted toward production-grade applications, particularly in aerospace engine components, EV battery housing systems, customized medical implants, and industrial spare parts. Metal additive manufacturing and high-performance polymer systems experienced faster growth compared to entry-level desktop systems.

The industry is increasingly shaped by sustainability imperatives such as material waste reduction, lightweight design for fuel efficiency, distributed manufacturing to lower logistics emissions, and development of recyclable or bio-based printing materials. Digital twins, AI-enabled generative design, topology optimization, and automated post-processing technologies are enhancing efficiency, scalability, and repeatability.

Industry projections indicate that the global 3D printing market will expand at a CAGR of approximately 18.67% between 2026 and 2031, driven by North America, Europe, and Asia-Pacific. Emerging markets in the Middle East and Latin America are witnessing rising adoption in construction printing, defense applications, and industrial prototyping.

Regulatory and certification requirements, particularly in aerospace, medical devices, and automotive safety components, are shaping adoption rates. Standards bodies are increasingly defining qualification frameworks for printed parts, pushing manufacturers toward traceability, material consistency, and repeatability. However, the market remains sensitive to high capital expenditure, slow certification cycles, material cost premiums, and workforce skill gaps in design-for-additive manufacturing (DfAM).

Market Dynamics: Drivers

Rapid prototyping acceleration, supply chain localization, customization demand, and lightweight engineering are key drivers of global 3D printing adoption. Aerospace and defense investments in fuel-efficient, lightweight components significantly boost metal additive manufacturing. Healthcare demand for patient-specific implants, prosthetics, and surgical guides continues to grow.

Automotive electrification is driving tooling, jigs, fixtures, and EV component printing. Additionally, Industry 4.0 initiatives, digital thread integration, generative design software, and on-demand spare part manufacturing are enabling decentralized production models. Construction-scale 3D printing, bio-printing research, and polymer innovations further contribute to long-term market expansion.

Market Dynamics: Challenges

The 3D printing industry faces several structural challenges including high equipment costs, expensive certified metal powders, slow certification cycles for aerospace and medical parts, and limited standardization across materials and processes. Print speed constraints and post-processing requirements can limit scalability for high-volume production.

Material qualification complexity, lack of skilled additive design engineers, and competition from conventional manufacturing methods also impact adoption rates. Furthermore, economic downturns can delay capital investment in industrial-grade printers. As additive manufacturing shifts toward production, ensuring repeatability, quality assurance, and cost competitiveness remains critical.

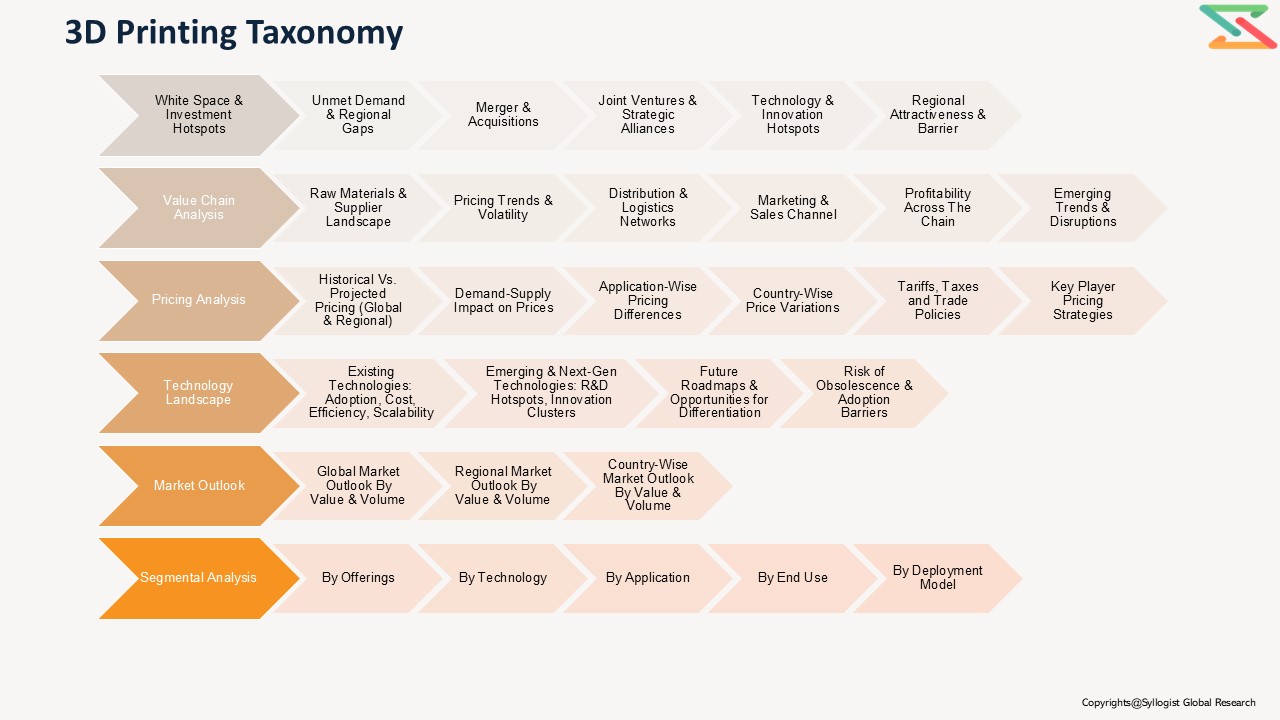

Market Segmentation

- By Offerings

- Hardware

- Metal Printers

- Desktop Printers

- Industrial Printers

- Large-Format Printers

- Construction Printers

- Materials

- Plastic Powders

- Polyamides

- Thermoplastic Polyurethanes (TPU)

- Ether ketones

- Others

- Plastic Filaments

- Polylactic Acid (PLA)

- Polycarbonate (PC) and Blends

- Acrylonitrile Butadiene Styrene (ABS)

- Others

- Photopolymers

- Epoxies and Hybrids

- Acrylics

- Polyurethanes (PU)

- Others

- Metals

- Plastic Powders

- Software

- CAD & Design Software

- Simulation & Optimization

- Blockchain-enabled file security

- Workflow Management

- Service

- On-demand printing

- Post-processing Services

- Design Consulting

- Maintenance & AMC

- Prototyping Services

- By Technology

- PolyJet / Material Jetting

- Multi Jet Fusion (MJF)

- Selective Laser Sintering (SLS)

- Digital Light Processing (DLP)

- Fused Deposition Modelling

- Stereolithography (SLA)

- Binder Jetting (Metal)

- Directed Energy Deposition (DED)

- Electron Beam Melting (EBM)

- Direct Metal Laser Sintering (DMLS)

- Selective Laser Melting (SLM)

- Others

- By End Use

- Aerospace & Defense

- Automotive

- Healthcare

- Industrial Machinery

- Construction

- Consumer Goods

- Energy

- By Deployment Model

- Service Bureau Model

- In-house Manufacturing

- Distributed Manufacturing Networks

- Manufacturing-as-a-Service Platforms

- Hardware

All market revenues are presented in USD, with production volumes expressed in units shipped, installed base, and material consumption (metric tons).

Historical Year: 2021–2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027–2031

Key Questions this Study Will Answer

- What are the key market statistics and forecasts (market size by value, unit shipments, material consumption, segment growth trends) for the Global 3D Printing Market?

- What are the region-wise market dynamics, industrial adoption patterns, and production maturity shifts?

- What technology innovations, certification trends, and sustainability drivers are shaping additive manufacturing?

- Who are the leading competitors, and how do they benchmark across hardware capability, material portfolio, software ecosystem, and production scalability?

- What insights emerge from interviews with OEMs, material suppliers, service bureaus, aerospace engineers, and industrial buyers conducted during the market assessment?

- Market Foundations & Dynamics

- Introduction

- Product Overview (Definition & Scope of 3D Printing: Polymer, Metal, Ceramic, Bio-Printing, Construction Printing)

- 3D Printing Value Chain Overview (Design → Material Supply → Printing → Post-Processing → End-Use Integration)

- Research Methodology

- Executive Summary

- Major Trends Shaping the Market (Industry 4.0, Distributed Manufacturing, Lightweighting, Customization, Digital Supply Chains)

- Short-Term vs. Long-Term Opportunities

- Comparison of Key 3D Printing Technologies (FDM, SLA, SLS, DMLS, Binder Jetting, MJF, DED)

- Scenario Planning (Base, Optimistic, Conservative Adoption Scenarios)

- Sensitivity Analysis (Material Costs, Printer CAPEX, Energy Prices, Adoption Rates)

- Identification of Regional Growth Hotspots

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Introduction

- Market Ecosystem & Value Chain

- Overview of Value Chain Participants

- Hardware Manufacturers (Desktop, Industrial, Metal, Large-Format Printers)

- Material Suppliers (Polymers, Metals, Resins, Powders, Filaments)

- Software Providers (CAD, Simulation, Workflow Management)

- Service Providers (On-Demand Printing, Post-Processing, Design Consulting)

- System Integrators & Automation Providers

- End-Users (Aerospace, Automotive, Healthcare, Industrial, Consumer)

- Flow of Value & Material Through the Chain

- Value Addition & Margins at Each Stage

- Design & Prototyping

- Printing & Production

- Post-Processing & Finishing

- Integration into Final Assemblies

- Impact of Vertical Integration

- Mapping of Roles & Interdependencies

- Market Trends & Developments

- White Space Analysis

- Demand Supply Analysis

- Demand–Supply Gaps (Material Shortages, Skilled Labor, Industrial Printer Availability)

- Unmet Needs (High-Speed Printing, Multi-Material Printing, Sustainable Materials)

- Risk Assessment Framework

- Political / Geopolitical Risk (Trade Barriers, Technology Export Controls)

- Operational Risk (Print Failures, Material Defects, Quality Control)

- Environmental Risk (Waste Management, Energy Consumption)

- Financial Risk (High CAPEX, ROI Uncertainty)

- Regulatory Framework & Standards

- Global Regulatory Overview

- Industry Standards (ISO/ASTM Additive Manufacturing Standards)

- Aerospace & Automotive Certification Requirements

- Medical & Healthcare Regulations (FDA, CE, MDR)

- Material & Safety Compliance

- Construction & Structural Printing Regulations

- Intellectual Property & Digital File Protection

- Environmental Compliance & Sustainability Mandates

- Liability & Insurance Requirements

- Digital Traceability & Quality Documentation

- Technology Landscape

- Polymer-Based Technologies (FDM, SLA, SLS, MJF)

- Metal-Based Technologies (DMLS, SLM, EBM, Binder Jetting, DED)

- Construction & Large-Scale Printing

- Bioprinting & Healthcare Innovations

- Automation & AI-Driven Optimization

- Future Outlook (Mass Customization, Distributed Manufacturing, Digital Warehousing)

- Global, Regional & Country Forecasts, 2021-2031

- Global 3D Printing Market Outlook (Value & Volume)

- Market Share by Offerings

- Hardware

- Metal Printers

- Desktop Printers

- Industrial Printers

- Large-Format Printers

- Construction Printers

- Materials

- Plastic Powders

- Polyamides

- Thermoplastic Polyurethanes (TPU)

- Ether ketones

- Others

- Plastic Filaments

- Polylactic Acid (PLA)

- Polycarbonate (PC) and Blends

- Acrylonitrile Butadiene Styrene (ABS)

- Others

- Photopolymers

- Epoxies and Hybrids

- Acrylics

- Polyurethanes (PU)

- Others

- Metals

- Plastic Powders

- Software

- CAD & Design Software

- Simulation & Optimization

- Blockchain-enabled file security

- Workflow Management

- Service

- On-demand printing

- Post-processing Services

- Design Consulting

- Maintenance & AMC

- Prototyping Services

- Market Share & Forecast by Technology

- PolyJet / Material Jetting

- Multi Jet Fusion (MJF)

- Selective Laser Sintering (SLS)

- Digital Light Processing (DLP)

- Fused Deposition Modelling

- Stereolithography (SLA)

- Binder Jetting (Metal)

- Directed Energy Deposition (DED)

- Electron Beam Melting (EBM)

- Direct Metal Laser Sintering (DMLS)

- Selective Laser Melting (SLM)

- Others

- Market Share & Forecast by End Use

- Aerospace & Defense

- Automotive

- Healthcare

- Industrial Machinery

- Construction

- Consumer Goods

- Energy

- Market Share & Forecast by End Use

- Aerospace & Defense

- Automotive

- Healthcare

- Industrial Machinery

- Construction

- Consumer Goods

- Energy

- Market Share & Forecast by Deployment Model

- Service Bureau Model

- In-house Manufacturing

- Distributed Manufacturing Networks

- Manufacturing-as-a-Service Platforms

- By Competition

- Hardware

Note: Similar level of information will be provided for all regions, Asia-Pacific, North America, Europe, Latin America and Middle East & Africa and for 40 countries. List of countries is available on slide

- Pricing Analysis

- Overview of Pricing Structures (Printer Cost, Material Cost per Kg, Service Cost per Part)

- Price Trends by Offering (Hardware, Materials, Software, Services)

- Cost Benchmark

- Hardware vs Material Cost Split

- Polymer vs Metal Printing Cost Comparison

- Price Sensitivity (Powder Costs, Resin Costs, Energy Costs)

- Historical & Forecasted Pricing

- Forecast Pricing

- Factors Influencing Price

- Raw Material Availability

- Energy Costs

- Technology Innovation

- Regulatory Burden

- R&D & Software Costs

- Regional Pricing Differentiation

- Impact of Sustainability Transition

- Competition Outlook

- Market Concentration vs Fragmentation

- Company Market Shares

- Competitive Strategies

- Technology Innovation

- Material Portfolio Expansion

- Geographic Expansion

- Strategic Partnerships & M&A

- Benchmarking Matrix (Scale vs Technology Depth vs Application Breadth)

- Recent Developments (New Product Launches, Capacity Expansions, Partnerships)

- Cost Structure & Margin Analysis

- Detailed Cost Breakdown

- Average Cost per Printing Stage

- Profitability & Margin Distribution

- Sensitivity Analysis (Material Cost, Machine Cost, Production Volume)

- Cost Reduction Opportunities (Automation, Digital Workflow Optimization)

- Business Models & Strategic Insights

- Service Bureau Model

- In-House Manufacturing Model

- Distributed Manufacturing Platforms

- Manufacturing-as-a-Service (MaaS)

- Hybrid Models

- SWOT of Leading Business Models

- Sales & Distribution Channel Analysis

- GTM Channels (Direct Sales, Channel Partners, Online Platforms)

- Channel Share by Region

- Typical Channel Flow Diagram (OEM → Distributor → End-User)

- Sales Process & Customer Engagement

- Distribution Strategy of Leading Players

- Emerging Trends (Subscription Models, Digital Marketplaces)

- Strategic Recommendations & Roadmap

- Competitor Strategic Initiatives

- Future Outlook

- Strategic Recommendations for Stakeholders

- Adoption Roadmap for Industrial-Scale 3D Printing

- Tailored Recommendations (OEMs, Material Suppliers, Service Providers, Investors)

- Key Success Factors (Material Quality, Process Reliability, Certification, Ecosystem Integration)