Market Definition

The Global Space Debris Removal Technologies Market refers to the aggregate ecosystem of systems, services, platforms, and enabling technologies purposefully designed to detect, characterize, track, capture, deorbit, and ultimately mitigate the accumulation of defunct satellites, spent rocket bodies, fragmentation debris, and other non-operational man-made objects orbiting the Earth. The market encompasses both active debris removal (ADR) solutions, which involve physical interaction with and controlled disposal of resident space objects, and passive debris mitigation technologies, which are integrated into spacecraft and launch vehicles at the design stage to reduce end-of-life residual lifetime in orbit. This includes a broad spectrum of technological approaches such as robotic capture systems, harpoon and net mechanisms, ion beam shepherding, laser ablation, electrodynamic tethers, drag augmentation devices, and on-orbit servicing platforms capable of performing deorbit maneuvers on targeted objects. The market further incorporates space situational awareness (SSA) and space traffic management (STM) infrastructure, including ground-based and space-based sensor networks, advanced tracking software, conjunction analysis platforms, and collision avoidance systems, all of which constitute critical enabling layers within the broader debris removal and mitigation value chain. Stakeholders operating across this market include national space agencies, commercial launch operators, satellite constellation operators, defense organizations, specialized aerospace technology developers, and international standards bodies, collectively representing a rapidly maturing industry at the intersection of orbital sustainability, commercial space operations, and national security policy.

Market Insights

The global space debris removal technologies market is entering a phase of accelerated commercial and institutional maturation, driven by the convergence of a rapidly expanding orbital population, heightened international regulatory attention, and the emergence of technically credible removal and servicing mission architectures. As of 2026, the number of active satellites in low Earth orbit has grown substantially, reflecting the proliferation of large and mega-constellations deployed by commercial operators across multiple geographies. This densification of the orbital environment has correspondingly elevated the probability of on-orbit collisions and conjunction events, generating an unprecedented level of urgency among space operators, insurers, and government bodies. The market is transitioning from a largely research-and-demonstration phase toward the initial phases of commercial service deployment, with several mission frameworks advancing through final regulatory clearance and pre-launch preparation. Market revenues are being generated across a combination of government-contracted demonstration missions, commercial pilot programs, and in-orbit servicing contracts, with the aftermarket for debris-related SSA software and data services constituting a significant and near-term revenue component.

A defining structural shift currently reshaping the market landscape is the progressive entry of commercial operators into mission segments previously dominated exclusively by national space agencies. Venture-backed and strategically funded technology developers are advancing proprietary capture mechanism designs, proximity operations algorithms, and debris rendezvous guidance systems toward operational readiness. Several companies have demonstrated proximity operations and docking capabilities in low Earth orbit through technology demonstration missions, validating core competencies necessary for full active debris removal mission execution. This commercial momentum is being reinforced by the emergence of public-private partnership frameworks through which space agencies provide anchor contracts, orbital safety data access, and regulatory facilitation to de-risk early commercial missions. The resulting ecosystem is progressively lowering the technical and financial barriers to scalable debris removal service delivery.

The convergence of active debris removal with the broader on-orbit servicing and manufacturing sector represents one of the most strategically significant market developments of the current period. Platforms originally designed for satellite life extension, in-orbit refueling, and inspection missions are increasingly being configured with modular debris capture payloads, enabling multi-mission operational architectures that substantially improve mission economics. This dual-use capability is attracting investment from satellite operators seeking both asset life extension services and environmental liability management for end-of-life platforms. The resulting technology overlap between servicing and removal missions is compressing development timelines, enabling operators to amortize platform development costs across multiple revenue streams, and accelerating the overall commercial viability of the active debris removal market segment.

From a regional perspective, the market is characterized by a well-defined multi-polar structure in which the United States, European Union member states through the European Space Agency, Japan, and China are simultaneously the largest contributors to the orbital debris problem and the primary sources of institutional investment in debris removal technology development. The United States maintains its position as the largest single market by funding volume and technology development activity, with defense and civilian agency programs constituting a significant proportion of contracted R&D. Europe has established a distinct commercial mission profile through dedicated debris removal program commitments, with active removal missions progressing toward operational execution. Japan has invested in electrodynamic tether technology and is advancing commercial deorbit service offerings targeted at constellation operators. Emerging space-faring nations, including India and the United Arab Emirates, are investing in domestic SSA capabilities and beginning to participate in the international policy frameworks that will define future debris removal obligations and commercial market access rights.

Key Drivers

Exponential Growth of Orbital Populations and the Escalating Kessler Syndrome Risk

The foundational driver of the global space debris removal technologies market is the exponential growth in the number of objects resident in Earth orbit, driven primarily by the accelerating deployment of commercial mega-constellations and the legacy accumulation of defunct satellites and rocket bodies from decades of space activity. The densification of critical orbital shells, particularly in low Earth orbit between 400 and 1,200 kilometers altitude, has materially elevated the risk of cascade collision events through the mechanism commonly referred to as the Kessler Syndrome, wherein collisions generate additional debris that triggers further collisions in a self-sustaining chain. Space agencies, satellite operators, and government bodies are increasingly treating the management of orbital debris not as an optional environmental commitment but as a fundamental precondition for the long-term commercial viability of the space economy. This shift in institutional and commercial risk perception is translating directly into contracted programs, regulatory mandates, and investment in technologies capable of actively reducing the resident space object population in the most congested orbital regimes.

Regulatory Mandates and the Global Harmonization of End-of-Life Disposal Requirements

A second major driver is the progressive tightening of national and international regulatory frameworks governing satellite end-of-life disposal and post-mission orbital lifetime. Leading space regulatory bodies have adopted or are in the process of adopting stricter requirements for post-mission disposal timelines, compelling satellite operators to integrate deorbit propulsion and drag augmentation devices into spacecraft design at the outset of a mission. The emergence of extended producer responsibility frameworks in the space domain, in which operators are held financially and legally accountable for end-of-life disposal compliance, is creating a structural market pull for both passive mitigation hardware and contracted active removal services. Multilateral policy coordination through forums such as the United Nations Committee on the Peaceful Uses of Outer Space and the Inter-Agency Space Debris Coordination Committee is contributing to the progressive convergence of national regulatory standards, which is in turn expanding the addressable market for compliance-oriented debris mitigation and removal technologies globally.

Commercial Space Economy Expansion and the Rising Economic Stakes of Orbital Sustainability

The third primary driver is the accelerating economic integration of low Earth orbit and geostationary orbit into commercial infrastructure, encompassing satellite broadband connectivity, Earth observation, precision agriculture, financial services, and emerging space-based manufacturing and pharmaceutical applications. The aggregate economic value of in-orbit assets and the downstream services they enable has reached a scale at which orbital congestion and collision risk represent financially material threats to commercial balance sheets, insurance underwriting viability, and long-term investor confidence in the space sector. Satellite fleet operators, insurance underwriters, launch service providers, and institutional investors are collectively developing a more sophisticated understanding of debris-related risk pricing, generating demand for SSA data services, conjunction analysis platforms, and collision avoidance optimization tools. This commercial risk management imperative is constituting an independent and growing demand vector for space debris removal and mitigation technologies, distinct from and complementary to the regulatory compliance driver described above.

Key Challenges

Technical Complexity of Rendezvous, Proximity Operations, and Non-Cooperative Object Capture

The most significant technical challenge confronting the space debris removal market is the inherent difficulty of designing and operating systems capable of safely rendezvousing with, capturing, and deorbiting non-cooperative space objects, meaning objects that were not designed to be serviced and that may be tumbling, structurally degraded, or geometrically complex. Unlike servicing missions targeting cooperative satellites equipped with standardized docking interfaces, active debris removal requires the development of highly adaptive guidance, navigation, and control algorithms capable of operating in close proximity to unpredictable target objects without generating secondary fragmentation events. Capture mechanisms including robotic arms, nets, harpoons, and adhesive systems must function reliably across a wide range of target geometries, material properties, and rotational states. The qualification and certification of these systems for operational missions requires extensive ground testing, analog demonstration, and in-orbit technology validation campaigns, each representing substantial programmatic cost and schedule risk that constrains the pace at which the market can scale from demonstration to commercial service delivery.

Absence of a Mature Commercial Business Model and the Challenges of Mission Cost Recovery

A structural challenge facing the commercial segment of the space debris removal market is the absence of a fully established and financially self-sustaining business model capable of supporting the high per-mission development and operational costs associated with active debris removal without sustained government subsidy or anchor contracting. The primary beneficiaries of debris removal activity, namely satellite constellation operators and the broader space economy, do not currently bear direct financial liability proportional to their contribution to the orbital debris environment, creating a market externality that limits the willingness of commercial operators to independently procure removal services at cost-reflective prices. Mission economics are further challenged by the single-use nature of most early capture and deorbit architectures, which prevent cost amortization across multiple targets. Until regulatory frameworks evolve to impose direct financial accountability for orbital debris contributions, or until multi-target mission architectures are validated operationally, the commercial business case for large-scale active debris removal will remain contingent on sustained public sector funding and policy support.

Jurisdictional Ambiguity and the Absence of International Legal Frameworks Governing Debris Removal

A third and distinctly structural challenge is the absence of a clear, internationally agreed legal and liability framework governing the physical interaction with, capture of, and disposal of space objects registered to sovereign nations or commercial operators under national licensing regimes. Under the current Outer Space Treaty framework, space objects remain the property of their launching state or registering operator, creating potential jurisdictional complications for third-party debris removal missions, particularly those operating across national licensing boundaries. The lack of clarity on liability attribution in the event of a removal mission generating secondary debris or damaging an adjacent space object introduces significant legal and insurance risk for commercial debris removal operators. Progress toward internationally harmonized legal frameworks is advancing through multilateral deliberation, but the pace of policy development has to date lagged the pace of commercial and technical progress, creating a regulatory uncertainty that constrains mission planning, investor confidence, and the ability to structure bankable long-term service contracts for debris removal operations.

Market Segmentation

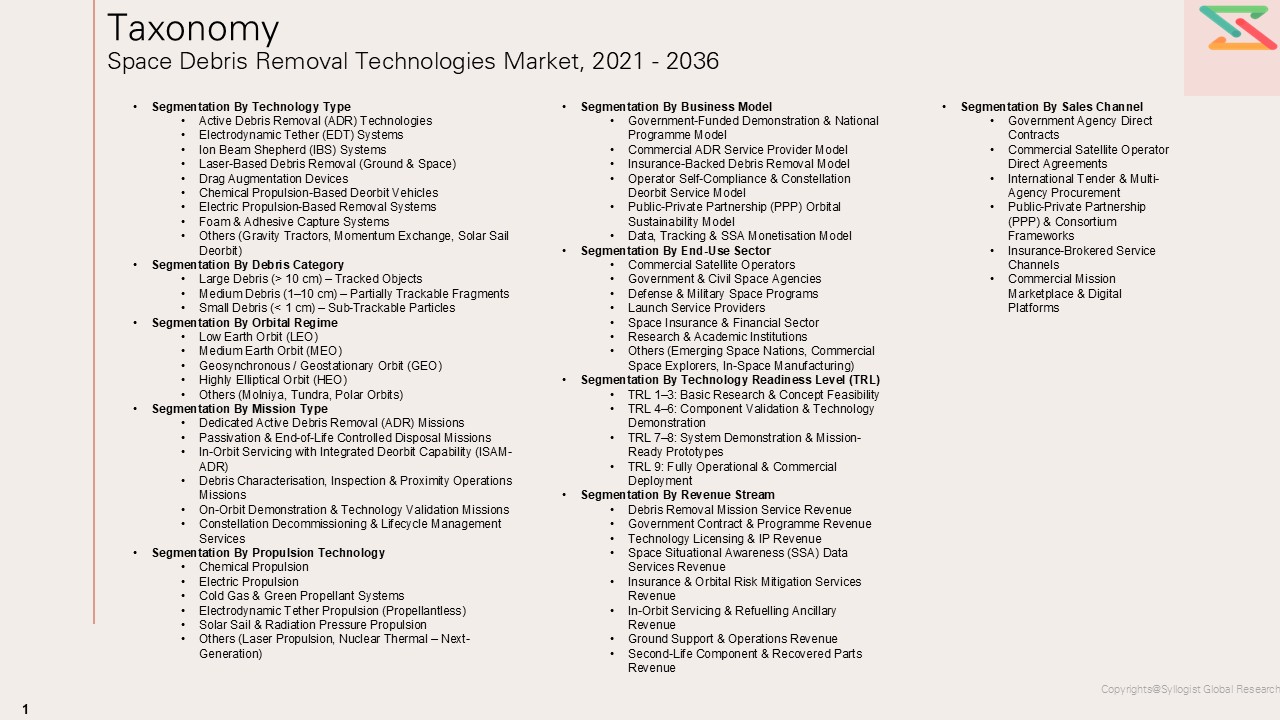

- Segmentation By Technology Type

- Active Debris Removal (ADR) Technologies

- Robotic Arm Capture Systems

- Net-Based Capture Mechanisms

- Harpoon and Tether Systems

- Ion Beam Shepherding

- Laser Ablation and Photon Pressure Systems

- Electrodynamic Tether Deorbit Systems

- Drag Augmentation Devices

- Adhesive and Gecko-Grip Capture Technologies

- Passive Debris Mitigation Technologies

- Post-Mission Disposal Propulsion Systems

- Deployable Drag Sails

- Passivation Systems

- Others

- Segmentation By Service Type

- Active Debris Removal Services

- In-Orbit Servicing and Life Extension

- End-of-Life Deorbit Services

- Space Situational Awareness (SSA) Data Services

- Conjunction Analysis and Collision Avoidance Services

- Space Traffic Management (STM) Services

- On-Orbit Inspection and Characterization Services

- Others

- Segmentation By Orbit Type

- Low Earth Orbit (LEO)

- Medium Earth Orbit (MEO)

- Geostationary Earth Orbit (GEO)

- Graveyard and Disposal Orbits

- Others

- Segmentation By Target Object Type

- Defunct Satellites

- Spent Rocket Bodies and Upper Stages

- Fragmentation Debris

- Mission-Related Objects (MLOs)

- Micro-Debris and Sub-Centimeter Particles

- Others

- Segmentation By Mission Architecture

- Single-Target Dedicated Removal Missions

- Multi-Target Sequential Removal Missions

- On-Orbit Servicing Platform with Modular Removal Payloads

- Tug-and-Deorbit Architecture

- Autonomous Swarm Removal Missions

- Others

- Segmentation By Propulsion System

- Chemical Propulsion

- Electric Propulsion (Ion and Hall-Effect Thrusters)

- Electrodynamic Tether Propulsion

- Cold Gas Propulsion

- Hybrid Propulsion Systems

- Propellantless Propulsion (Photon Pressure, Drag)

- Others

- Segmentation By Platform

- Dedicated Debris Removal Spacecraft

- On-Orbit Servicing and Logistics Vehicles

- Hosted Payload on Commercial Satellites

- Ground-Based Laser and Tracking Systems

- Space-Based SSA Sensor Networks

- Others

- Segmentation By End User

- National Space Agencies

- Commercial Satellite Operators

- Commercial Launch Service Providers

- Defense and Intelligence Organizations

- Space Insurance Underwriters

- International Space Stations and Crewed Platform Operators

- Others

- Segmentation By Application

- Orbital Congestion Mitigation

- Critical Infrastructure Protection

- Crewed Spaceflight Safety

- Regulatory Compliance and Liability Management

- Commercial Asset Protection and Insurance

- National Security and Defense Applications

- Sustainable Space Environment Preservation

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021–2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027–2036

Key Questions this Study Will Answer

- What is the projected global market valuation for space debris removal technologies through 2036, segmented by technology type, service category, and orbit regime? This analysis provides the quantitative foundation required for strategic investment planning, technology portfolio prioritization, and long-term commercial mission planning across the debris removal value chain.

- Which active debris removal technology architectures, including robotic capture systems, net and harpoon mechanisms, ion beam shepherding, and electrodynamic tether systems, are expected to achieve the earliest commercial operational status, and what are the key technical readiness milestones that will determine the pace of commercial service deployment within the forecast period?

- How will the evolving international regulatory landscape, including post-mission disposal mandates, extended producer responsibility frameworks, and space traffic management requirements, reshape procurement behavior among satellite constellation operators and launch service providers, and to what extent will regulatory compliance drive demand for passive mitigation versus active removal technologies?

- What commercial business model frameworks, including government anchor contracting, multi-target mission architecture, debris removal as a service, and insurance-integrated liability management structures, are best positioned to deliver financial viability for commercial active debris removal operators in the absence of universally mandated removal obligations?

- Who are the leading technology developers, mission operators, SSA data providers, and institutional investors currently defining the competitive landscape of the global space debris removal market, and what are their respective technology differentiation strategies, regulatory engagement approaches, and geographic market expansion priorities through the forecast horizon?

- Product Definition

- Scope of the Study

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Industry Publications, Space Agency Reports & Press Releases

- Government Space Agency Data (NASA, ESA, JAXA, ISRO, Roscosmos, etc.)

- Space Debris Monitoring, Cataloguing & Collision Avoidance Statistics

- Defense & Dual-Use Space Programme Databases

- Primary Research Design & Execution

- In-depth Interviews with Satellite Operators, Space Agencies & Mission Planners

- Surveys with Debris Removal Technology Developers & Launch Service Providers

- Expert Panel Validation

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Bottom-Up & Top-Down Reconciliation

- Orbital Debris Population & Removal Mission Demand Model

- Mission Economics & Cost-Per-Object Removal Model

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Technology & Innovation Highlights

- Mission Economics & Unit Economics Summary

- Average Mission CAPEX & OPEX Benchmarks

- Removal Efficiency & Objects-Per-Mission Analysis

- Active Debris Removal (ADR) Revenue Model Summary

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Geographic & Regional Trends

- Risk Assessment Framework

- Geopolitical & Political Risk

- Orbital Congestion & Kessler Syndrome Risk

- Environmental & Regulatory Risk

- Financial / Market Risk

- Technology Maturity & Mission Failure Risk

- Regulatory Framework & Policy Standards

- Space Debris Removal Technology Economics

- Mission Economics & Unit Economics Framework

- Capital Expenditure (CAPEX) Structure

- Operating Expenditure (OPEX) Structure

- Revenue Model & Monetisation Levers

- Mission Frequency & Objects-Removed-Per-Year Economics

- Payback Period & Return on Investment (ROI) Analysis

- Total Cost of Removal (TCR) vs Debris Shielding & Avoidance Alternatives

- Global Space Debris Removal Technologies Market Outlook

- Market Size & Forecast by Value (USD Billion, 2021–2036)

- Market Size & Forecast by Technology Type

- Active Debris Removal (ADR) Technologies

- Robotic Arm & Tentacle Capture Systems

- Net Capture & Deorbit Systems

- Harpoon & Tethered Deorbit Systems

- Electrodynamic Tether (EDT) Systems

- Propellantless EDT Deorbit Devices

- Tethered Satellite Active Drag Systems

- Ion Beam Shepherd (IBS) Systems

- Laser-Based Debris Removal (Ground & Space)

- Ground-Based High-Power Laser Ablation Systems

- Space-Based Laser Push / Ablation Systems

- Drag Augmentation Devices

- Deployable Drag Sails & Ballutes

- Inflatable Deorbit Modules

- Chemical Propulsion-Based Deorbit Vehicles

- Dedicated Deorbit Tug Spacecraft

- Servicer / Refuelling-Integrated Deorbit Platforms

- Electric Propulsion-Based Removal Systems

- Hall-Effect Thruster Deorbit Vehicles

- Ion Thruster Rendezvous & Deorbit Missions

- Foam & Adhesive Capture Systems

- Others (Gravity Tractors, Momentum Exchange, Solar Sail Deorbit)

- Market Size & Forecast by Debris Category

- Large Debris (> 10 cm) – Tracked Objects

- Defunct Satellites

- Spent Rocket Bodies & Upper Stages

- Mission-Related Debris (Fairings, Adapters, Lens Covers)

- Medium Debris (1–10 cm) – Partially Trackable Fragments

- Small Debris (< 1 cm) – Sub-Trackable Particles

- Fragmentation Debris from Explosions & Collisions

- Ejecta & Surface Degradation Particles

- Market Size & Forecast by Orbital Regime

- Low Earth Orbit (LEO)

- Sun-Synchronous Orbit (SSO) – 600–900 km

- Very Low Earth Orbit (VLEO) – Below 450 km

- Mega-Constellation Orbital Shells (550–1,200 km)

- Medium Earth Orbit (MEO)

- GPS & Navigation Satellite Orbital Band (~20,200 km)

- Semi-Synchronous MEO (4,000–10,000 km)

- Geosynchronous / Geostationary Orbit (GEO)

- Active GEO Belt (35,786 km)

- Graveyard / Disposal Orbit Band

- Highly Elliptical Orbit (HEO)

- Others (Molniya, Tundra, Polar Orbits)

- Low Earth Orbit (LEO)

- Market Size & Forecast by Mission Type

- Dedicated Active Debris Removal (ADR) Missions

- Single-Target High-Value Debris Removal

- Multi-Object Removal Per Mission

- Passivation & End-of-Life Controlled Disposal Missions

- In-Orbit Servicing with Integrated Deorbit Capability (ISAM-ADR)

- Debris Characterisation, Inspection & Proximity Operations Missions

- On-Orbit Demonstration & Technology Validation Missions

- Constellation Decommissioning & Lifecycle Management Services

- Dedicated Active Debris Removal (ADR) Missions

- Market Size & Forecast by Propulsion Technology

- Chemical Propulsion (Monopropellant & Bipropellant)

- Electric Propulsion (Hall-Effect Thruster, Ion Engine, FEEP)

- Cold Gas & Green Propellant Systems

- Electrodynamic Tether Propulsion (Propellantless)

- Solar Sail & Radiation Pressure Propulsion

- Others (Laser Propulsion, Nuclear Thermal – Next-Generation)

- Market Size & Forecast by Business Model

- Government-Funded Demonstration & National Programme Model

- Agency-Funded ADR Demonstration & In-Orbit Validation Contracts

- National Space Debris Removal Mandates & Procurement Programs

- Commercial ADR Service Provider Model

- Per-Object Removal Service (Pay-Per-Deorbit)

- Annual Debris Management Subscription

- Insurance-Backed Debris Removal Model

- Insurer-Sponsored Removal for High-Risk Objects

- Satellite Operator Deorbit Assurance Contracts

- Operator Self-Compliance & Constellation Deorbit Service Model

- Mega-Constellation End-of-Life Deorbit Services

- Fleet Deorbit-as-a-Service (DaaS)

- Public-Private Partnership (PPP) Orbital Sustainability Model

- Space Agency + Commercial Operator Co-Funded ADR Programmes

- International Multi-Stakeholder Debris Clearance Consortia

- Data, Tracking & SSA Monetisation Model

- Space Situational Awareness (SSA) Data-as-a-Service

- Debris Catalogue Licensing & Analytics Platforms

- Market Size & Forecast by End-Use Sector

- Commercial Satellite Operators

- Large GEO Telecom Operators

- LEO Broadband Mega-Constellation Operators (SpaceX Starlink, OneWeb, Amazon Kuiper, etc.)

- Earth Observation & Remote Sensing Operators

- Government & Civil Space Agencies

- NASA (United States)

- ESA (Europe)

- JAXA (Japan)

- Other National Space Agencies

- Defense & Military Space Programs

- National Reconnaissance & Military Satellite Operators

- Defense Space Command & Situational Awareness Programs

- Launch Service Providers

- Orbital Debris Liability Mitigation Services

- Spent Upper Stage Deorbit Compliance Services

- Space Insurance & Financial Sector

- Satellite Hull & Liability Underwriters

- ESG-Focused Space Asset Investors & Asset Managers

- Research & Academic Institutions

- Others (Emerging Space Nations, Commercial Space Explorers, In-Space Manufacturing)

- Commercial Satellite Operators

- Market Size & Forecast by Technology Readiness Level (TRL)

- TRL 1–3: Basic Research & Concept Feasibility

- TRL 4–6: Component Validation & Technology Demonstration

- TRL 7–8: System Demonstration & Mission-Ready Prototypes

- TRL 9: Fully Operational & Commercial Deployment

- Market Size & Forecast by Revenue Stream

- Debris Removal Mission Service Revenue

- Government Contract & Programme Revenue

- Technology Licensing & IP Revenue

- Space Situational Awareness (SSA) Data Services Revenue

- Insurance & Orbital Risk Mitigation Services Revenue

- In-Orbit Servicing & Refuelling Ancillary Revenue

- Ground Support & Operations Revenue

- Second-Life Component & Recovered Parts Revenue

- Market Size & Forecast by Sales Channel

- Government Agency Direct Contracts

- Commercial Satellite Operator Direct Agreements

- International Tender & Multi-Agency Procurement

- Public-Private Partnership (PPP) & Consortium Frameworks

- Insurance-Brokered Service Channels

- Commercial Mission Marketplace & Digital Platforms

- Asia-Pacific Space Debris Removal Technologies Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Technology Type

- By Debris Category

- By Orbital Regime

- By Mission Type

- By Business Model

- By End-Use Sector

- By Revenue Stream

- By Technology Readiness Level

- Key Demand Drivers (APAC-Specific)

- Competitive Landscape (APAC)

- Europe Space Debris Removal Technologies Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Technology Type

- By Debris Category

- By Orbital Regime

- By Mission Type

- By Business Model

- By End-Use Sector

- By Revenue Stream

- By Technology Readiness Level

- Key Demand Drivers (Europe-Specific)

- Competitive Landscape (Europe)

- North America Space Debris Removal Technologies Market Outlook

- Market Overview & Strategic Importance

- Market Size & Forecast

- By Value (2020–2035)

- By Technology Type

- By Debris Category

- By Orbital Regime

- By Mission Type

- By Business Model

- By End-Use Sector

- By Revenue Stream

- By Technology Readiness Level

- Key Demand Drivers (North America-Specific)

- Competitive Landscape (North America)

- Latin America Space Debris Removal Technologies Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Technology Type

- By Debris Category

- By Orbital Regime

- By Mission Type

- By Business Model

- By End-Use Sector

- By Revenue Stream

- By Technology Readiness Level

- Key Demand Drivers (LATAM-Specific)

- Competitive Landscape (Latin America)

- Middle East & Africa Space Debris Removal Technologies Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Technology Type

- By Debris Category

- By Orbital Regime

- By Mission Type

- By Business Model

- By End-Use Sector

- By Revenue Stream

- By Technology Readiness Level

- Key Demand Drivers (MEA-Specific)

- Competitive Landscape (MEA)

- Country-Wise Space Debris Removal Technologies Market Outlook

- Market Size & Forecast by Country

- By Value

- By Technology Type

- By Debris Category

- By Orbital Regime

- By Mission Type

- By Business Model

- By End-Use Sector

- By Revenue Stream

- By Technology Readiness Level

- Market Size & Forecast by Country

- Market Size & Forecast

- Market Size & Forecast

- Market Size & Forecast

- Market Size & Forecast

- Government-Funded Demonstration & National Programme Model

- Large Debris (> 10 cm) – Tracked Objects

- Mission Economics & Unit Economics Framework

- Countries Covered: United States, Canada, Germany, United Kingdom, France, Italy, Spain, Netherlands, Switzerland, China, Japan, India, South Korea, Australia, Singapore, Brazil, Mexico, Saudi Arabia, United Arab Emirates, South Africa

- Technology Landscape & Innovation Analysis

- Debris Removal Technology Maturity Assessment

- Emerging & Disruptive Technologies in Space Debris Removal

- Digital Technologies in Mission Operations & Space Traffic Management

- Technology Readiness Level (TRL) Matrix – Key ADR Technologies

- Patent Landscape Analysis

- R&D Investment Benchmarking

- Value Chain & Supply Chain Analysis

- Space Debris Removal Value Chain Mapping

- Supply Chain Concentration & Dependency Analysis

- Key Supplier Mapping by Technology Programme

- Supplier Risk Heat Map

- Make vs Buy Strategy Trends Among Debris Removal Technology Developers

- Pricing Analysis

- Debris Removal Service Pricing Dynamics & Mechanisms

- Pricing by Debris Category & Orbital Regime

- Total Cost of Removal (TCR) Analysis

- ADR Service Contract Pricing Trends & Benchmarks

- Sustainability & Orbital Stewardship

- Long-Term Orbital Sustainability Landscape

- Kessler Syndrome Risk Assessment & Debris Population Benchmarking

- Space Sustainability Ratings & ESG Frameworks for Orbital Operations

- Debris Second-Life Recovery & Circular Space Economy Impact Assessment

- Net-Zero Launch & Orbital Sustainability Pathway

- ESG Reporting & Lifecycle Assessment (LCA) in Debris Removal Operations

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level: Government-Dominated vs Emerging Commercial Players

- Top 5 Space Debris Removal Companies Market Revenue Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis by Technology Segment

- Competitive Intensity Map by Segment & Region

- Player Classification

- Tier-1 Dedicated ADR Technology Developers

- Tier-1 In-Orbit Servicing & ISAM Players with Debris Removal Capability

- Government Agency-Led Debris Removal Programmes

- Emerging & Disruptive Players

- Competitive Analysis Frameworks

- Market Share Analysis by Technology Type & Geography

- R&D Intensity Benchmarking

- Government Contract Revenue & Mission Portfolio Comparison

- Geographic Revenue Exposure Comparison

- Company Profiles

- Company Overview, HQ & Organisational Structure

- Technology Products & Mission Services Portfolio

- Revenue Breakdown

- Key Debris Removal Programmes & Mission Deployments

- Manufacturing Footprint & Key Facilities

- Recent Developments (M&A, Partnerships, New Programmes, Financial Results)

- SWOT Analysis

- Strategic Focus: Technology Maturation, Government Contracts, Commercial ADR Scale-Up

- Strategic Output

- Market Opportunity Matrix

- High-Value Opportunity Quadrant Analysis

- Addressable Market by Segment & Region

- Time-to-Revenue Assessment by Opportunity

- White Space Opportunity Analysis

- Underserved Orbital Regime & Business Model Gaps

- Geographic Markets with Low Penetration

- Technology Gaps with High Commercialisation Potential

- Customer Segment Unmet Needs

- Strategic Recommendations

- Technology Development & Mission Portfolio Strategy

- Digitalization & Space Traffic Management Strategy

- Mission Lifecycle & Spacecraft Asset Management Strategy

- Service Offering & Commercial ADR Scale-Up Strategy

- Pricing & Commercial Strategy

- Sustainability & Regulatory Compliance Strategy

- Supply Chain & Component Sourcing Strategy

- Partnership, M&A & International Collaboration Strategy

- Regional Growth Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-Term (2025–2028)

- Mid-Term (2029–2032)

- Long-Term (2033–2036)

- Market Opportunity Matrix

- Market Structure & Concentration