Market Definition

The Global Aircraft Engine Market encompasses the design, development, manufacturing, maintenance, and commercial deployment of propulsion systems installed across civil, commercial, military, and general aviation platforms. Aircraft engines serve as the core mechanical and thermodynamic systems that convert chemical energy into thrust, enabling the safe and efficient movement of passengers, cargo, and defense assets across both subsonic and supersonic flight profiles. The market includes a spectrum of engine architectures, most notably turbofan, turboprop, turboshaft, turbojet, and piston engines, each engineered for distinct performance envelopes, altitude requirements, and fuel efficiency objectives. Commercially, the turbofan engine segment constitutes the dominant propulsion technology for large commercial transport aircraft, owing to its superior bypass ratios and significantly improved specific fuel consumption relative to older turbojet designs. Beyond conventional thermal propulsion, the market is increasingly incorporating emerging propulsion technologies, including electric, hybrid-electric, and hydrogen-based systems, which are projected to establish a meaningful commercial presence over the coming decade. This market encompasses original equipment manufacturers (OEMs), tier-one and tier-two component suppliers, MRO (maintenance, repair, and overhaul) service providers, and aftermarket parts distributors operating across a deeply integrated global aerospace supply chain.

Market Insights

The global aircraft engine market is currently navigating one of the most consequential structural transitions in its history, driven simultaneously by a robust post-pandemic recovery in commercial aviation, accelerating defense modernization programs, and a technology inflection toward next-generation propulsion architectures. As of 2026, global commercial air passenger traffic has surpassed pre-2020 levels across all major regions, compelling airlines to aggressively expand and renew their fleets. This fleet renewal activity directly drives demand for new-generation turbofan engines characterized by higher bypass ratios, advanced combustor designs, and ceramic matrix composite (CMC) hot-section components. Leading OEMs are consequently operating at near-peak production rates, with engine delivery backlogs extending well beyond five years for certain narrow-body aircraft programs. The market valuation has demonstrated consistent upward momentum, underpinned by both new engine deliveries and the growing contribution of the high-margin aftermarket segment.

A defining trend shaping the market landscape in 2026 is the accelerating convergence of digital engineering and advanced manufacturing technologies within the engine production ecosystem. Leading OEMs and their supply chain partners are deploying additive manufacturing at scale for the production of complex hot-section components, including fuel nozzles, turbine blades, and heat exchanger cores, thereby reducing part counts, lowering manufacturing lead times, and achieving geometries previously unattainable through conventional machining. Simultaneously, the widespread adoption of digital twin platforms is transforming both engine design validation and in-service monitoring. By creating high-fidelity virtual replicas of physical engines that are continuously updated with real-time operational data, manufacturers and MRO operators are achieving unprecedented accuracy in predictive maintenance, significantly reducing unplanned aircraft-on-ground events and extending time-on-wing for revenue-generating assets.

The aftermarket and MRO segment represents a structurally significant and rapidly growing component of the total aircraft engine market. As the global installed base of commercial turbofan engines continues to expand, and as older-generation engines remain in active service particularly in emerging aviation markets across Asia-Pacific, the Middle East, and Latin America, demand for engine overhauls, life-limited part replacements, and performance restoration services is exhibiting strong and durable growth. MRO providers are increasingly investing in automated borescope inspection systems, robotic component processing, and data-driven shop visit planning to optimize turnaround times and reduce labor-intensive manual inspection requirements. Furthermore, the introduction of power-by-the-hour and outcome-based service agreements by OEMs has effectively shifted MRO revenue from episodic to recurring, providing greater earnings visibility and transforming the aftermarket into a long-cycle, high-margin business.

From a regional standpoint, the Asia-Pacific region has emerged as the largest and fastest-growing geographic market for aircraft engines, a position underpinned by the sustained expansion of low-cost and full-service carriers across China, India, Southeast Asia, and the broader Pacific Rim. Domestic fleet expansion programs in these markets are generating substantial engine procurement volumes, while the simultaneous build-out of indigenous MRO infrastructure is creating new service revenue opportunities. North America maintains its position as the global epicenter of aircraft engine R&D and OEM manufacturing, housing the principal production and engineering facilities of the world’s largest propulsion system developers. Europe remains a critical market driven by both commercial aviation demand and a robust defense procurement cycle, with significant engine programs underpinning NATO interoperability modernization efforts. The Middle East, while a comparatively smaller volume market, commands strategic importance as a high-value hub for widebody aircraft operations and associated long-haul engine MRO activity.

Key Drivers

Global Commercial Aviation Recovery and Unprecedented Fleet Renewal Activity

The most consequential demand driver for the aircraft engine market is the structural recovery and sustained capacity expansion of the global commercial aviation industry following the disruptions of the early 2020s. Airlines worldwide are accelerating new aircraft deliveries to retire aging, fuel-inefficient platforms, driven by both economic imperatives around fuel cost reduction and mounting regulatory pressure to lower per-seat carbon emissions. New-generation single-aisle and twin-aisle aircraft programs are commanding record order backlogs at airframe OEMs, each unit representing a paired order for the most advanced turbofan engines currently in production. This fleet renewal supercycle is generating a multi-year demand pipeline for propulsion system deliveries that is structurally independent of near-term macroeconomic fluctuations, as airline capital commitments are contractually secured years in advance. The compounding effect of this delivery ramp on the future installed base of new engines further amplifies the long-term aftermarket opportunity for both OEMs and independent MRO operators.

Defense Modernization and the Expansion of Military Propulsion Programs

Escalating geopolitical tensions across multiple regions and the resulting increase in national defense budgets are providing a powerful and durable secondary driver for the global aircraft engine market. Governments across North America, Europe, and the Indo-Pacific are committing to the modernization of their tactical fighter fleets, transport aviation assets, and rotary-wing platforms, all of which require advanced engine systems with enhanced thrust-to-weight ratios, survivability characteristics, and reduced infrared signatures. The development of sixth-generation combat aircraft programs in key defense markets is catalyzing significant investment in adaptive cycle engine technologies, which offer variable bypass ratios capable of optimizing performance across a wider range of mission profiles. Parallel investments in unmanned aerial system (UAS) propulsion, including small turbofan and turboprop engines for surveillance and strike platforms, are creating an entirely new and rapidly expanding product category within the military engine segment that was nascent as recently as five years prior.

Advancing Sustainable Aviation and the Emergence of Next-Generation Propulsion Technologies

The aviation industry’s commitment to achieving net-zero carbon emissions by 2050, reinforced by binding national and international regulatory frameworks, is directly stimulating R&D investment and early commercialization activity in alternative propulsion architectures. Hybrid-electric propulsion systems are advancing from laboratory and demonstrator phases toward regional aircraft applications, with multiple certified programs anticipated to enter commercial service within the forecast period. Concurrently, hydrogen combustion turbine technology is receiving substantial investment from both established OEMs and well-capitalized technology entrants, supported by government co-funding programs across Europe, North America, and East Asia. The development of sustainable aviation fuel (SAF)-compatible engine variants, capable of operating on blends of up to 100% SAF, represents an interim yet commercially significant driver that is enabling airlines to meet near-term decarbonization targets without requiring radical propulsion architecture changes. These converging technological threads are collectively expanding the addressable market for propulsion systems beyond conventional applications.

Key Challenges

Supply Chain Fragility and Critical Material Constraints in Engine Manufacturing

The aircraft engine manufacturing ecosystem operates through one of the most complex and geographically concentrated supply chains in global industry, creating a structural vulnerability that constitutes a significant near-to-medium-term market challenge. The production of high-performance turbine components demands precisely formulated nickel-based superalloys, single-crystal casting capabilities, advanced thermal barrier coatings, and, increasingly, specialized ceramic matrix composite materials. The refining and processing capacity for several of these critical materials is concentrated in a limited number of geographies, exposing OEMs and tier-one suppliers to supply disruption risk from geopolitical events, trade policy shifts, and mine-level production interruptions. In 2026, the industry continues to grapple with persistent delivery bottlenecks in specific engine sub-systems, driven by a combination of skilled labor shortages in precision machining and inspection disciplines, extended qualification lead times for new suppliers, and the challenge of simultaneously ramping production across multiple concurrent new engine programs.

Intensifying Regulatory Stringency and the Rising Cost of Certification Compliance

The pathway to commercial certification for new aircraft engine designs and propulsion technologies has become progressively more demanding, time-consuming, and capital-intensive. Aviation safety authorities are applying heightened scrutiny to all aspects of propulsion system certification, encompassing structural integrity under extreme thermal and mechanical loading, foreign object damage tolerance, containment capability, and emissions conformance under the latest ICAO CAEP standards. For novel propulsion architectures, including hybrid-electric systems and hydrogen combustion engines, regulatory frameworks are still being developed and standardized, creating inherent certification timeline uncertainty that increases program risk and challenges investor confidence. The cumulative cost of ground test campaigns, flight test programs, and documentation packages required to achieve type certification for a new engine family represents a multi-billion dollar financial commitment that effectively serves as a formidable barrier to entry and constrains the number of credible new market participants.

Workforce Capability Gaps and the Challenge of Knowledge Transfer in a Maturing Industry

The aircraft engine industry faces a structural human capital challenge that is emerging as a binding constraint on both production ramp-up velocity and engineering innovation capacity. A significant cohort of experienced engineers, test pilots, manufacturing specialists, and overhaul technicians who accumulated decades of domain-specific expertise are approaching retirement across the major OEM and MRO organizations simultaneously. The transfer of tacit engineering knowledge, particularly in disciplines such as combustor aerodynamics, hot-section materials behavior, and fan blade aeroelastic design, is inherently difficult to systematize and accelerate. Concurrently, the industry faces intensifying competition from adjacent high-technology sectors for graduates with expertise in computational fluid dynamics, materials science, and systems engineering. This talent acquisition pressure is compounded by the geographic specificity of engine manufacturing and testing infrastructure, which limits workforce flexibility and necessitates sustained investment in regional technical training programs and apprenticeship pipelines to meet projected demand.

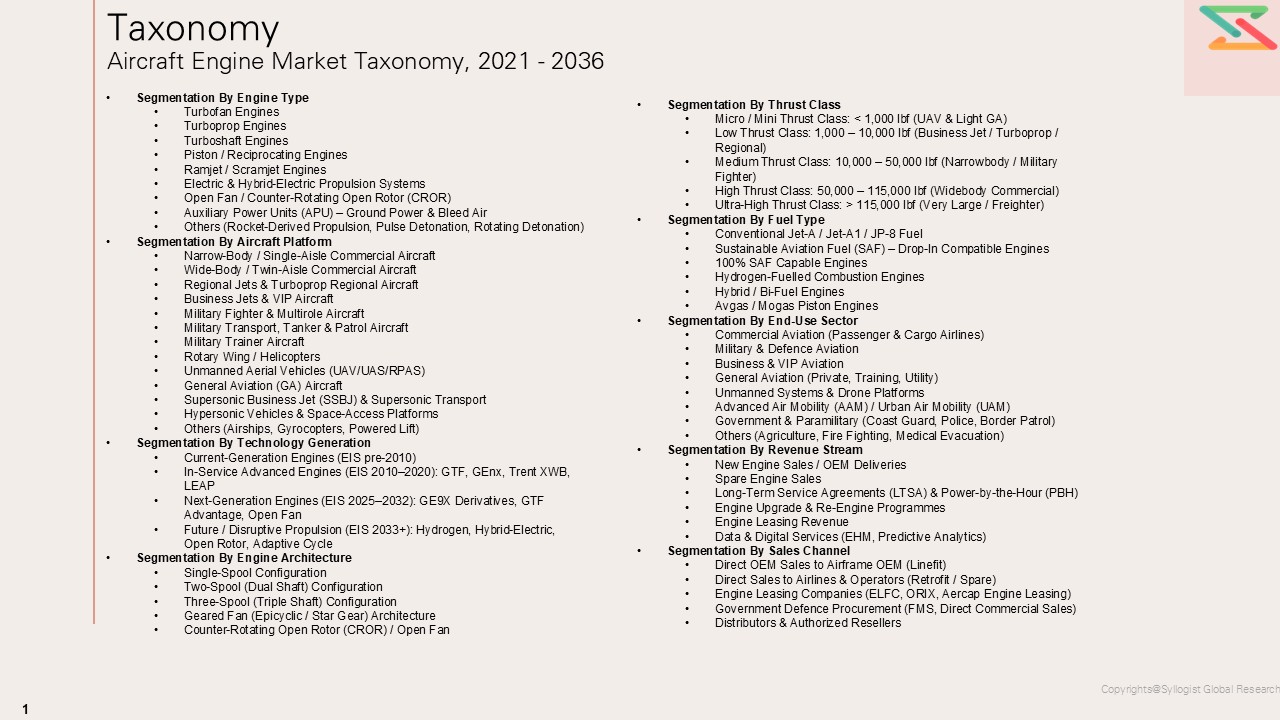

Market Segmentation

- Segmentation By Engine Type

- Turbofan Engine

- Turboprop Engine

- Turboshaft Engine

- Turbojet Engine

- Piston / Reciprocating Engine

- Electric and Hybrid-Electric Propulsion Systems

- Hydrogen Combustion Engine

- Others

- Segmentation By Platform

- Commercial Aviation

- Military Aviation

- General Aviation

- Business and Corporate Aviation

- Unmanned Aerial Vehicles (UAVs) / Unmanned Combat Aerial Vehicles (UCAVs)

- Rotary-Wing Aircraft (Helicopters)

- Supersonic and Hypersonic Platforms

- Others

- Segmentation By Aircraft Type

- Narrow-Body Aircraft

- Wide-Body Aircraft

- Regional Jets

- Turboprop Commuter Aircraft

- Fighter and Multirole Combat Aircraft

- Strategic Transport Aircraft

- Maritime Patrol Aircraft

- Unmanned Systems

- Others

- Segmentation By Application

- Commercial Passenger Transport

- Commercial Cargo and Freight

- Defense and Tactical Operations

- Intelligence, Surveillance, and Reconnaissance (ISR)

- Aerial Firefighting and Emergency Services

- Agricultural Aviation

- Training and Flight Simulation Support

- Others

- Segmentation By Thrust Rating

- Below 25,000 lbf

- 25,000 lbf to 75,000 lbf

- Above 75,000 lbf

- Segmentation By Component

- Fan and Compressor Assembly

- Combustion Chamber and Combustor Liner

- Turbine Section (High-Pressure and Low-Pressure)

- Exhaust System and Thrust Reverser

- Engine Control Systems (FADEC)

- Fuel System Components

- Nacelle and Inlet Assembly

- Gearbox and Accessory Drive System

- Bearings and Seals

- Others

- Segmentation By Material Type

- Nickel-Based Superalloys

- Titanium Alloys

- Ceramic Matrix Composites (CMC)

- Carbon Fiber Reinforced Polymer (CFRP) Composites

- Aluminum Alloys

- Refractory Metals

- Others

- Segmentation By Technology

- Conventional Turbofan Architecture

- Geared Turbofan (GTF) Technology

- Open Rotor / Open Fan Architecture

- Adaptive Cycle Engine Technology

- Hybrid-Electric Propulsion Integration

- Hydrogen Combustion Propulsion

- Distributed Electric Propulsion

- Others

- Segmentation By Sales Channel

- Original Equipment Manufacturer (OEM) Direct Delivery

- Aftermarket and Spare Parts Sales

- Power-by-the-Hour and Performance-Based Logistics Contracts

- Government and Defense Procurement Programs

- Others

- Segmentation By MRO Service Type

- Engine Overhaul and Heavy Maintenance

- On-Wing Support and Line Maintenance

- Component Repair and Life-Limited Part Replacement

- Borescope Inspection and Non-Destructive Testing

- Engine Leasing and Asset Management Services

- Others

- Segmentation By End User

- Commercial Airlines and Leasing Companies

- Defense Ministries and Armed Forces

- General and Business Aviation Operators

- Government and Para-Military Agencies

- MRO Independents and Third-Party Service Providers

- Others

All market revenues are presented in USD

Historical Year: 2021–2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027–2036

Key Questions this Study Will Answer

- What is the projected global market valuation and unit delivery volume for aircraft engines through 2036, segmented by engine type and platform? This provides the quantitative foundation necessary for long-term capacity planning, capital allocation decisions, and competitive positioning strategies across the propulsion value chain.

- How will the accelerating adoption of geared turbofan and adaptive cycle engine technologies reshape the competitive dynamics among established OEMs, and which next-generation engine platforms are expected to capture the largest share of the narrow-body and wide-body aircraft engine replacement cycle over the forecast period?

- To what extent will military engine procurement programs across North America, Europe, and the Indo-Pacific contribute to total market revenue growth through 2036, and which defense platform categories, including sixth-generation fighter programs, unmanned combat systems, and advanced rotary-wing platforms, are expected to generate the highest incremental propulsion demand?

- What is the projected revenue contribution and CAGR of the aircraft engine MRO and aftermarket segment relative to the new engine delivery segment, and how are power-by-the-hour and performance-based service contract structures transforming the revenue mix, margin profiles, and long-term customer relationships of leading OEMs and independent MRO operators?

- Who are the leading OEMs, tier-one component suppliers, and independent MRO service providers currently defining the competitive landscape of the global aircraft engine market, and what are their respective strategic priorities in terms of technology investment, supply chain localization, sustainability commitments, and geographic market expansion through the forecast horizon?

- Product Definition

- Scope of the Study

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Industry Publications, Aviation Authority Reports & Press Releases

- Government Aviation & Defense Authority Data (FAA, EASA, ICAO, DGCA, etc.)

- IATA, ICAO & Boeing/Airbus Commercial Market Outlook Statistics

- Defense Procurement & Aerospace Finance Databases

- Primary Research Design & Execution

- In-depth Interviews with Engine OEM Executives, MRO Operators & Aviation Investors

- Surveys with Airlines, Aircraft Lessors & Defense Procurement Officials

- Expert Panel Validation

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Bottom-Up & Top-Down Reconciliation

- Aircraft Fleet Demand & Engine Attachment Rate Model

- MRO Cycle & Aftermarket Revenue Model

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Technology & Innovation Highlights

- Engine Economics & Unit Economics Summary

- Average Engine CAPEX & MRO Cost Benchmarks

- Fuel Efficiency & Specific Fuel Consumption (SFC) Analysis

- Power-by-the-Hour (PBH) Revenue Model Summary

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Geographic & Regional Trends

- Risk Assessment Framework

- Geopolitical & Political Risk

- Fuel Price & Energy Transition Risk

- Environmental & Regulatory Risk

- Financial / Market Risk

- Technology Obsolescence & Certification Risk

- Regulatory Framework & Policy Standards

- Aircraft Engine Economics

- Engine Economics & Unit Economics Framework

- Capital Expenditure (CAPEX) Structure

- Operating & Maintenance Expenditure (OPEX) Structure

- Revenue Model & Monetisation Levers

- Engine Utilisation Rate & Flight Cycle Economics

- Payback Period & Return on Investment (ROI) Analysis

- Total Cost of Ownership (TCO) vs Alternative Propulsion

- Engine Component & Lifecycle Cost Analysis

- Engine Unit Cost Trends (USD/Engine, 2021–2035)

- Component Degradation & Time-Between-Overhaul (TBO) Economics

- Engine Reconditioning, Second-Life & Parts-Out Value Chain Economics

- Spare Engine Inventory Optimisation Models

- Engine Insurance & Warranty Economics

- Impact of Next-Generation & Hydrogen Propulsion on Engine Economics

- MRO & Aftermarket Economics

- MRO Cost Structure by Engine Type & Geography

- Power-by-the-Hour (PBH) & Flight-Hour Agreement (FHA) Economics

- Digital MRO & Predictive Maintenance Cost Savings

- Shop Visit Frequency & Workscope Economics

- Aftermarket Parts Pricing Dynamics: OEM vs PMA vs Used Serviceable Material (USM)

- Financing Structures & Capital Markets

- Equity Financing: VC, PE & Strategic Corporate Investment

- Debt Financing: Export Credit, Project Finance & ECA-Backed Loans

- Government Grants, R&D Subsidies & Defense Procurement Funding

- Sale-Leaseback & Operating Lease Structures

- Asset-Backed Financing & Engine Pool Securitisation

- Carbon Credit & SAF-Linked ESG Financing

- Certification & Regulatory Compliance Economics

- FAA & EASA Type Certification Cost Benchmarks

- Economic Impact of ICAO CORSIA & Emissions Compliance

- Noise & Emissions Standards Compliance Costs

- Maintenance Programme Approval (MPA) Costs

- Global Aircraft Engines Market Outlook

- Market Size & Forecast by Value (USD Billion, 2021–2036)

- Market Size & Forecast by Engine Type

- Turbofan Engines

- High-Bypass Turbofan (HBTF)

- Low-Bypass Turbofan (LBTF)

- Geared Turbofan (GTF)

- Turboprop Engines

- Single-Turbine Turboprop

- Free-Turbine Turboprop

- Turbojet Engines

- Turboshaft Engines

- Piston / Reciprocating Engines

- Electric & Hybrid-Electric Propulsion Systems

- All-Electric Propulsion

- Series Hybrid Propulsion

- Parallel Hybrid Propulsion

- Hydrogen Propulsion – Next-Generation Applications

- Others (Ramjet, Scramjet, Auxiliary Power Units)

- Turbofan Engines

- Market Size & Forecast by Application

- Commercial Aviation

- Narrowbody Aircraft (Single-Aisle)

- Widebody Aircraft (Twin-Aisle)

- Regional Jets & Turboprops

- Business Jets & VIP Aircraft

- Military & Defense Aviation

- Fighter & Combat Aircraft

- Military Transport & Tanker Aircraft

- Military Helicopter & Rotorcraft

- Unmanned Aerial Vehicles (UAVs / Drones)

- General Aviation

- Private Piston Aircraft

- Light Sport Aircraft

- Experimental & Kit-Built Aircraft

- Rotorcraft & Helicopters

- Civil Utility Helicopters

- Offshore & SAR Helicopters

- Military Attack & Transport Helicopters

- Urban Air Mobility (UAM) & Advanced Air Mobility (AAM)

- eVTOL Aircraft

- Electric Air Taxis

- Regional Electric Commuters

- Supersonic & Hypersonic Platforms

- Space Launch & Rocket Propulsion

- Others (Agriculture, Fire-Fighting, Experimental)

- Commercial Aviation

- Market Size & Forecast by Engine Technology

- Conventional Kerosene-Fuelled Turbine Engines

- SAF (Sustainable Aviation Fuel)-Compatible Engines

- Open Rotor & Ultra-High Bypass Ratio (UHBR) Engines

- Ceramic Matrix Composite (CMC)-Enabled Engines

- Additive Manufactured Component Engines

- Distributed Electric Propulsion (DEP) Systems

- Hydrogen-Fuelled Combustion Engines

- Hydrogen Fuel Cell & Hybrid Systems

- Others (Hybrid Thermodynamic Cycles, Advanced Cooling Systems)

- Market Size & Forecast by Thrust Class

- Ultra-Low Thrust: < 2,000 lbf (Micro-UAVs, Light Sport Aircraft)

- Low Thrust: 2,000 – 10,000 lbf (Regional Jets, Business Jets)

- Medium Thrust: 10,000 – 30,000 lbf (Narrowbody Commercial Aircraft)

- High Thrust: 30,000 – 70,000 lbf (Widebody Commercial Aircraft)

- Very High Thrust: 70,000 – 120,000 lbf (Large Widebody & Freighters)

- Ultra-High Thrust: > 120,000 lbf (Jumbo & Military Airlifters)

- Market Size & Forecast by Business Model

- OEM Direct Sales (New Engine Supply)

- Power-by-the-Hour (PBH) / Flight-Hour Agreement (FHA) – OEM-Led

- Independent MRO Service Provider Model

- Airline-Owned MRO (In-House)

- Third-Party MRO Providers

- Engine Leasing & Asset Management Model

- Operating Lease Model (Short & Long-Term)

- Engine Pooling & Asset Sharing

- Fleet-Focused B2B Engine Supply & Service Contracts

- Long-Term Engine Supply Agreements with Airlines

- Defense Procurement & Government Service Agreements

- Parts Manufacturer Approval (PMA) & Aftermarket Parts Model

- Hybrid & Multi-Revenue Model

- OEM + Aftermarket Services + Data Analytics Integrated Model

- Engine Leasing + MRO + Second-Life Parts Model

- Market Size & Forecast by End-Use Sector

- Commercial Airlines & Flag Carriers

- Full-Service Network Carriers (FSNCs)

- Low-Cost Carriers (LCCs) & Ultra-Low-Cost Carriers (ULCCs)

- Regional & Commuter Airlines

- Defense & Military

- Air Force Jet & Turboprop Procurement

- Naval Aviation

- Army Aviation & UAV Programs

- Aircraft Leasing & Asset Management

- Operating Lessors (AerCap, Air Lease, SMBC Aviation, etc.)

- Engine Leasing Specialists (ORIX, BBAM, Willis Lease, etc.)

- Business Aviation & Charter

- Corporate Flight Departments

- Charter & Fractional Ownership Operators

- General Aviation & Flight Training

- Flight Schools & Training Academies

- Private & Recreational Pilots

- Emergency & Special Mission Aviation

- Air Ambulance & Medical Evacuation

- Fire-Fighting & Aerial Application

- Law Enforcement & Surveillance

- Others (Space, Agriculture, Research & Experimental)

- Commercial Airlines & Flag Carriers

- Market Size & Forecast by Technology Generation

- First-Generation Jet Engines (Pre-1960): Straight-Turbojet, Early Military Applications

- Second-Generation Turbofan Engines (1960–1990): High-Bypass Commercial Entry

- Third-Generation Advanced Turbofan (1990–2015): FADEC, Composite Fan Blades, Advanced Alloys

- Fourth-Generation Next-Gen Engines (2015–2030): GTF, GE9X, LEAP, CMC Components

- Next-Generation Propulsion Systems (2030+): Open Rotor, Hybrid-Electric, Hydrogen, SAF-Optimised

- Market Size & Forecast by MRO Service Type

- Shop Visits & Heavy Engine Overhaul

- On-Wing & Line Maintenance

- Component & Module Repair

- Engine Test Cell Services

- Predictive Maintenance & Digital MRO Services

- Engine Teardown & Parts-Out Services

- Market Size & Forecast by Revenue Stream

- New Engine Sales Revenue

- Engine Aftermarket & Spare Parts Revenue

- Power-by-the-Hour (PBH) & Service Contract Revenue

- Engine Leasing Revenue

- MRO & Overhaul Revenue

- Defense & Government Contract Revenue

- Data Analytics & Digital Services Revenue

- Second-Life Parts & Engine Teardown Revenue

- Market Size & Forecast by Sales Channel

- OEM Direct-to-Airline / Operator Sales

- Aircraft OEM-Bundled Engine Supply

- Independent Engine Distributors & Brokers

- Government / Defense Procurement Channels

- Operating Lessors & Finance Partners

- Aftermarket Parts Distributors

- Asia-Pacific Aircraft Engines Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Engine Type

- By Application

- By Engine Technology

- By Business Model

- By End-Use Sector

- By Revenue Stream

- By Technology Generation

- By MRO Service Type

- Key Demand Drivers (APAC-Specific)

- Competitive Landscape (APAC)

- Europe Aircraft Engines Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Engine Type

- By Application

- By Engine Technology

- By Business Model

- By End-Use Sector

- By Revenue Stream

- By Technology Generation

- By MRO Service Type

- Key Demand Drivers (Europe-Specific)

- Competitive Landscape (Europe)

- North America Aircraft Engines Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Engine Type

- By Application

- By Engine Technology

- By Business Model

- By End-Use Sector

- By Revenue Stream

- By Technology Generation

- By MRO Service Type

- Key Demand Drivers (North America-Specific)

- Competitive Landscape (North America)

- Latin America Aircraft Engines Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Engine Type

- By Application

- By Engine Technology

- By Business Model

- By End-Use Sector

- By Revenue Stream

- By Technology Generation

- By MRO Service Type

- Key Demand Drivers (LATAM-Specific)

- Competitive Landscape (Latin America)

- Middle East & Africa Aircraft Engines Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Engine Type

- By Application

- By Engine Technology

- By Business Model

- By End-Use Sector

- By Revenue Stream

- By Technology Generation

- By MRO Service Type

- Key Demand Drivers (MEA-Specific)

- Competitive Landscape (MEA)

- Country-Wise Aircraft Engines Market Outlook

- Market Size & Forecast by Country

- By Value

- By Engine Type

- By Application

- By Engine Technology

- By Business Model

- By End-Use Sector

- By Revenue Stream

- By Technology Generation

- By MRO Service Type

- Market Size & Forecast by Country

- Market Size & Forecast

- Market Size & Forecast

- Market Size & Forecast

- Market Size & Forecast

- Market Size & Forecast

- Engine Economics & Unit Economics Framework

Countries Covered: United States, Canada, Germany, United Kingdom, France, Italy, Spain, Netherlands, Switzerland, China, Japan, India, South Korea, Australia, Singapore, Brazil, Mexico, Saudi Arabia, United Arab Emirates, South Africa

- Technology Landscape & Innovation Analysis

- Engine Technology Maturity Assessment

- Emerging & Disruptive Technologies in Aircraft Propulsion

- Digital Technologies in Engine Operations & Fleet Management

- Technology Readiness Level (TRL) Matrix – Key Propulsion Technologies

- Patent Landscape Analysis

- R&D Investment Benchmarking

- Value Chain & Supply Chain Analysis

- Aircraft Engine Value Chain Mapping

- Supply Chain Concentration & Dependency Analysis

- Key Supplier Mapping by Engine Programme

- Supplier Risk Heat Map

- Make vs Buy Strategy Trends Among Engine OEMs

- Pricing Analysis

- Engine Pricing Dynamics & Mechanisms

- Pricing by Engine Type & Thrust Class

- Total Cost of Ownership (TCO) Analysis

- PBH & MRO Pricing Trends & Benchmarks

- Sustainability & Energy Efficiency

- Energy & Environmental Sustainability Landscape

- Carbon Footprint Benchmarking of Engine Generations

- SAF Integration Roadmap for Engine Manufacturers

- Hydrogen Propulsion Transition & Circular Economy Impact Assessment

- Net-Zero Aviation Pathway & Engine OEM Commitments

- ESG Reporting & Lifecycle Assessment (LCA) in Engine Operations

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level: Duopoly-Led (CFM/GE) vs Emerging Players

- Top 5 Aircraft Engine OEMs Market Revenue Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis by Engine Segment

- Competitive Intensity Map by Segment & Region

- Player Classification

- Tier-1 Commercial Engine OEMs

- Tier-1 Military & Defense Engine Manufacturers

- Regional & Business Aviation Engine Manufacturers

- Emerging & Disruptive Players

- Competitive Analysis Frameworks

- Market Share Analysis by Engine Type & Geography

- R&D Intensity Benchmarking

- Airline Customer Revenue & Long-Term Contract Portfolio Comparison

- Geographic Revenue Exposure Comparison

- Company Profiles

- Company Overview, HQ & Organisational Structure

- Engine Products & Services Portfolio

- Revenue Breakdown

- Key Engine Programmes & Fleet Deployments

- Manufacturing Footprint & Key Facilities

- Recent Developments (M&A, Partnerships, New Programmes, Financial Results)

- SWOT Analysis

- Strategic Focus: Next-Gen Propulsion, Aftermarket Expansion, SAF Integration

- Strategic Output

- Market Opportunity Matrix

- High-Value Opportunity Quadrant Analysis

- Addressable Market by Segment & Region

- Time-to-Revenue Assessment by Opportunity

- White Space Opportunity Analysis

- Underserved Aircraft Segment & Business Model Gaps

- Geographic Markets with Low Penetration

- Technology Gaps with High Commercialisation Potential

- Customer Segment Unmet Needs

- Strategic Recommendations

- Engine Programme & Product Portfolio Strategy

- Technology & Digitalization Strategy

- Engine Lifecycle & Aftermarket Management Strategy

- MRO Service Offering & Expansion Strategy

- Pricing & Commercial Strategy

- Sustainability & Regulatory Compliance Strategy

- Supply Chain & Materials Sourcing Strategy

- Partnership, M&A & Expansion Strategy

- Regional Growth Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-Term (2025–2028)

- Mid-Term (2029–2032)

- Long-Term (2033–2036)

- Market Opportunity Matrix

- Market Structure & Concentration