Market Definition

The Global Automotive Glass Market encompasses the design, manufacturing, processing, distribution, and aftermarket replacement of all glass-based components integrated into passenger vehicles, commercial vehicles, off-highway equipment, and specialty automotive platforms. Automotive glass serves as a structurally integral, safety-critical, and increasingly multi-functional system component that performs a range of concurrent functions including occupant protection, structural rigidity contribution, aerodynamic optimization, acoustic insulation, and the enabling of a progressively expanding portfolio of advanced driver assistance, connectivity, and human-machine interface technologies. The primary product categories within this market include windshields, side windows, rear windows, sunroofs and panoramic roof systems, rear-view mirror glass, and specialized glazing solutions for electric vehicle platforms and autonomous driving applications. From a manufacturing technology standpoint, the market spans laminated safety glass, tempered glass, acoustic glass, heated glass, heads-up display-compatible glass, electrochromic and smart glass, and solar control glass, each engineered to satisfy distinct performance, regulatory, and application-specific requirements across different vehicle segments. The value chain of this market encompasses raw float glass producers, automotive glass processors and fabricators, tier-one automotive suppliers, original equipment manufacturers, independent aftermarket distributors, and professional installation service networks. The market is shaped by the intersection of automotive design trends, vehicle safety regulations, consumer technology expectations, sustainability mandates, and the structural transformation of the automotive industry toward electrification and autonomous mobility.

Market Insights

The global automotive glass market is experiencing a period of significant structural evolution, driven by the convergence of accelerating vehicle electrification, the proliferation of advanced driver assistance systems, and the increasing architectural and aesthetic ambitions of vehicle designers who are repositioning glass surfaces as expansive, multi-functional canvases rather than passive transparency elements. As of 2026, the market is characterized by sustained volume growth in the original equipment segment, underpinned by recovering global vehicle production across key manufacturing hubs in Asia-Pacific, Europe, and North America, alongside a robust and structurally expanding aftermarket segment driven by the growing global parc of vehicles requiring periodic windshield repair and replacement. The progressive integration of high-value functional technologies into glass components, including embedded heating elements, antenna systems, acoustic interlayers, heads-up display projection zones, and electrochromic dimming capabilities, is driving a meaningful upward shift in average selling prices per vehicle unit that is outpacing volume growth and contributing disproportionately to overall market revenue expansion.

A defining trend reshaping the product and technology landscape of the automotive glass market is the rapid proliferation of panoramic and full-roof glazing systems across vehicle platforms spanning from premium passenger cars to mass-market electric vehicles. The design language of battery electric vehicles, unconstrained by the packaging requirements of conventional powertrain architecture, has strongly favored expansive glass roof surfaces that enhance the perception of interior space, reinforce premium brand positioning, and satisfy consumer demand for open, light-filled cabin environments. This trend is substantially increasing the total glazed area per vehicle, expanding the revenue opportunity per unit for glass suppliers, and driving investment in solar control and thermal management glass technologies that mitigate the heat load and occupant comfort challenges associated with large glazed roof panels. Concurrently, the integration of advanced driver assistance system sensor suites including cameras, LiDAR, and radar directly into windshield and glazing assemblies is requiring glass manufacturers to develop new coating, interlayer, and substrate technologies that maintain optical clarity and sensor transmission performance across a demanding range of environmental conditions.

The automotive glass aftermarket represents a structurally distinct and commercially significant segment of the overall market, operating through dedicated distribution networks, insurance-integrated repair and replacement channels, and professional installation service providers. The aftermarket is supported by the fundamental characteristic that windshields and automotive glass components are subject to damage from road debris, environmental stress, and collision events throughout a vehicle’s operational life, generating a recurring demand stream that is largely independent of new vehicle production cycles. The growing complexity and cost of original equipment glazing assemblies, particularly windshields incorporating heads-up display zones, advanced driver assistance system sensor windows, and acoustic interlayers, is significantly increasing the average transaction value per replacement event and elevating the technical skill requirements for professional installation. The expansion of mobile glass repair and replacement services, enabled by advances in adhesive technology and portable installation equipment, is broadening service channel coverage and improving customer convenience, while the progressive integration of windshield recalibration requirements for advanced driver assistance systems following replacement is creating a new and growing revenue stream for aftermarket service operators.

From a regional perspective, Asia-Pacific dominates the global automotive glass market in both volume and production capacity terms, underpinned by the concentration of global vehicle manufacturing activity in China, Japan, South Korea, and India and the presence of major float glass and automotive glass processing facilities serving both regional and export markets. China in particular is central to global market dynamics both as the world’s largest vehicle production and sales market and as the home market of the fastest-growing electric vehicle segment globally, which is driving disproportionate demand for panoramic glass, smart glass, and high-specification windshield assemblies. Europe maintains a structurally important position in the market through its concentration of premium automotive brands, its leading role in vehicle safety regulation, and its active legislative agenda on automotive sustainability and end-of-life vehicle glass recyclability. North America is characterized by a high-value aftermarket driven by a large vehicle parc, high per-vehicle glazed area in the popular light truck and sport utility vehicle segments, and an advanced insurance-integrated replacement channel. Emerging markets across South Asia, Southeast Asia, the Middle East, and Latin America are exhibiting early-stage growth driven by rising vehicle ownership rates and improving access to organized aftermarket service infrastructure.

Key Drivers

Accelerating Vehicle Electrification and the Transformation of Glazing Architecture in Battery Electric Vehicles

The global transition toward battery electric vehicles is constituting one of the most consequential demand drivers for advanced automotive glass technologies and is reshaping the product mix, average content per vehicle, and technology investment priorities of glass manufacturers and their tier-one supply chain partners. The design architecture of battery electric vehicles, freed from the structural and thermal constraints imposed by conventional internal combustion engine layouts, has systematically migrated toward larger, more integrated, and more technologically sophisticated glazing systems. Panoramic and full-length glass roof assemblies are appearing across a broadening range of electric vehicle platforms at multiple price points, substantially increasing the square footage of glass content per vehicle. Simultaneously, the high thermal sensitivity of lithium-ion battery systems to solar heat gain is accelerating the adoption of advanced solar control glass incorporating low-emissivity coatings, infrared-reflective interlayers, and spectrally selective substrates that manage cabin temperature and reduce air-conditioning load without compromising visible light transmission. These technology requirements are commanding significant premium pricing relative to conventional automotive glass and are positioning advanced glazing as a high-value differentiation lever for electric vehicle OEMs competing on range efficiency, thermal management performance, and perceived interior quality.

Tightening Global Vehicle Safety Regulations and the Expanding Role of Glass in Passive Safety Systems

The progressive strengthening of vehicle safety regulations across major automotive markets is serving as a structural driver for the adoption of higher-specification laminated and safety-engineered glass technologies throughout the vehicle. Regulatory frameworks governing windshield performance, side glazing penetration resistance, roof crush strength contribution, and pedestrian head impact protection are creating mandatory minimum performance thresholds that are effectively phasing out lower-specification glass products and elevating the technical and cost requirements for compliant automotive glass across all vehicle segments. The expanding mandates for advanced driver assistance systems including autonomous emergency braking, lane keeping assistance, and automatic high-beam control, all of which rely on vision-based sensors mounted in or adjacent to the windshield, are additionally driving requirements for glass products with certified optical homogeneity, controlled distortion characteristics, and dedicated sensor aperture zones. These regulatory imperatives are translating into sustained demand for the most advanced laminated glass formulations, and the ongoing evolution of safety testing protocols toward more comprehensive and stringent performance standards across major regulatory jurisdictions is expected to further elevate the technical content requirements for automotive glass over the forecast period.

Growth in Heads-Up Display Adoption and the Integration of Connectivity and Human-Machine Interface Technologies in Glazing

The rapid mainstream proliferation of windshield-projected heads-up display systems, transitioning from a feature historically confined to premium luxury segments toward mid-market and volume vehicle applications, is constituting a significant and growing technology-driven demand driver for specialized automotive glass. Augmented reality heads-up display systems, which project navigation, speed, collision warning, and advanced driver assistance information directly onto the windshield in the driver’s natural line of sight, require windshield glass manufactured to exacting optical specifications including precisely controlled wedge angle across the projection zone, certified optical distortion limits, and compatibility with p-polarized light projection sources. The technical requirements for augmented reality heads-up display-compatible windshields represent a substantial advancement over conventional laminated glass specifications, commanding a meaningful price premium and requiring significant capital investment in precision manufacturing process control. Beyond heads-up display functionality, the embedding of antenna arrays for vehicle-to-everything communication, heated wiper park zones, and light-sensing elements directly into glass assemblies is progressively transforming automotive glazing from a passive structural component into an active electronic subsystem, further elevating its average selling price and strategic importance within the vehicle architecture.

Key Challenges

Raw Material Cost Volatility and Energy Intensity of Float Glass and Automotive Glass Processing Operations

A significant structural challenge confronting the global automotive glass market is the exposure of both upstream float glass production and downstream automotive glass processing operations to sustained volatility in raw material input costs and energy tariffs, both of which constitute major components of the total manufacturing cost base. Float glass production is an energy-intensive continuous melting process requiring sustained high-temperature furnace operation, making production economics highly sensitive to natural gas, electricity, and fuel oil price movements that can vary substantially across geographies and time periods. The principal raw material inputs including silica sand, soda ash, dolomite, and limestone are subject to supply concentration risks and logistics cost exposure that can amplify price volatility at the furnace level. Automotive glass processors additionally face cost pressure from specialty interlayer materials, coating precursors, and encapsulation compounds required for advanced laminated and functional glass products, many of which involve specialized chemical inputs with limited supply bases. Managing these input cost dynamics while maintaining the price competitiveness required by automotive OEM procurement processes, which operate through long-term supply agreements with structured cost reduction expectations, represents a persistent margin management challenge for glass manufacturers across the value chain.

Technical Complexity of Integrating Functional Technologies and the Challenge of Maintaining Optical and Structural Performance

The increasing demand for multi-functional automotive glass incorporating heads-up display compatibility, embedded heating elements, antenna systems, electrochromic capabilities, and advanced solar control coatings within a single integrated glazing assembly is presenting substantial technical development and manufacturing quality challenges for glass producers and their technology partners. Each functional layer introduced into a laminated glass assembly, whether a conductive coating, a printed silver busbar network, a photochromic interlayer, or an embedded LED light guide, introduces new requirements for thermal expansion compatibility, inter-layer adhesion integrity, edge seal durability, and optical interference management that must be satisfied simultaneously across the full operational temperature and humidity range of the vehicle. The qualification of complex multi-functional glazing assemblies through automotive OEM validation programs requires extensive environmental cycling, durability testing, and optical performance verification under conditions that reflect the full range of global climatic environments, adding substantial time and cost to development programs. Manufacturing yield management for high-specification functional glazing, particularly for large panoramic roof panels and curved windshields incorporating augmented reality heads-up display zones, remains a technical challenge that constrains production scalability and contributes to cost structures that are significantly above those of conventional automotive glass.

End-of-Life Glass Recyclability Challenges and the Growing Sustainability Accountability Requirements of the Automotive Supply Chain

The automotive glass industry faces a growing and structurally important challenge related to the recyclability and circular economy performance of advanced laminated glass products at end of vehicle life, an issue that is receiving increasing regulatory and corporate sustainability scrutiny across major automotive markets. Conventional automotive laminated windshields and complex functional glazing assemblies present significant recycling difficulties due to the permanent bonding of glass laminates with polyvinyl butyral or thermoplastic polyurethane interlayer films, which are challenging to separate at end of life without specialized processing infrastructure. The addition of functional layers including conductive coatings, encapsulated wiring, and embedded electronic components further complicates the material recovery process and reduces the purity and economic value of cullet recovered from end-of-life automotive glass. Evolving extended producer responsibility regulations in Europe and other jurisdictions are progressively increasing the recycled content and end-of-life recyclability requirements applied to automotive materials including glass, creating compliance obligations for vehicle manufacturers that cascade into design and material specification requirements for their glass supply chains. Developing commercially viable separation, cullet purification, and closed-loop recycling pathways for complex laminated automotive glass, while maintaining the structural and optical performance specifications demanded by safety regulations and OEM quality standards, represents a priority technical and investment challenge for the industry over the forecast period.

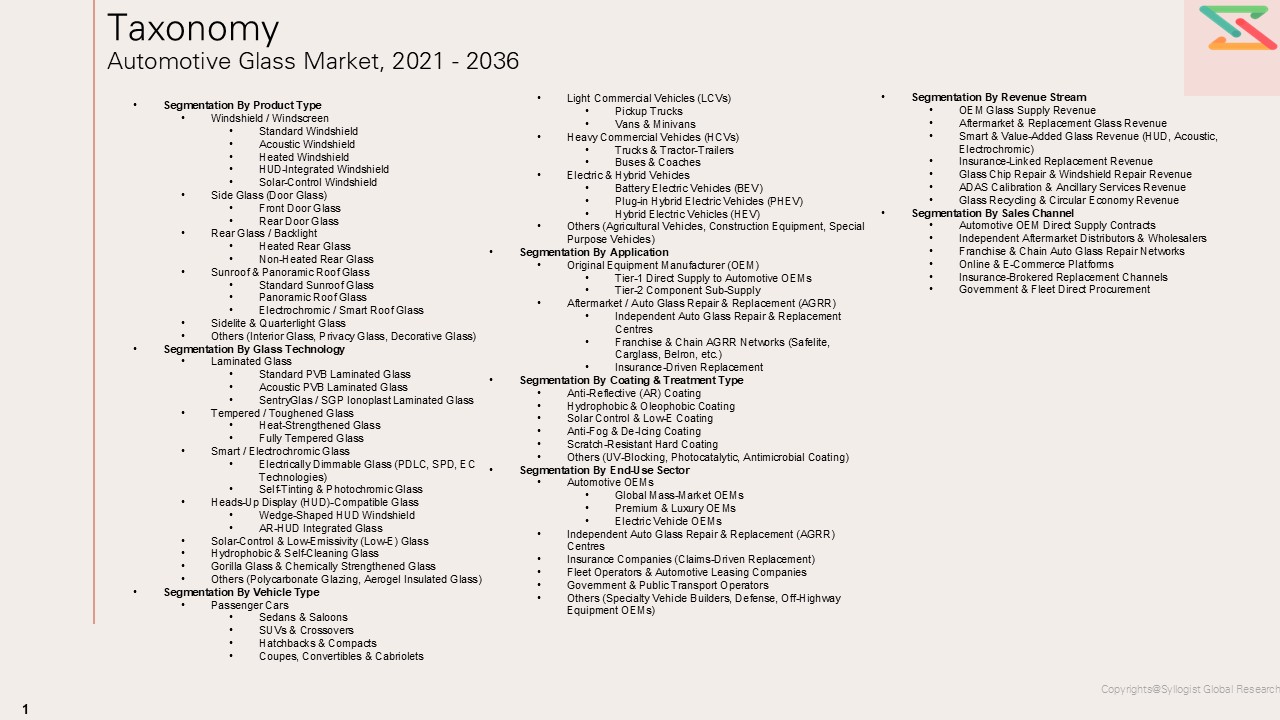

Market Segmentation

- Segmentation By Product Type

- Windshield

- Side Windows

- Rear Window

- Sunroof and Panoramic Roof Glass

- Quarter Glass

- Rear-View Mirror Glass

- Vent Glass

- Others

- Segmentation By Glass Type

- Laminated Glass

- Tempered Glass

- Acoustic Glass

- Heated Glass

- Solar Control and Low-Emissivity Glass

- Heads-Up Display Compatible Glass

- Electrochromic and Smart Glass

- Chemically Strengthened Glass

- Others

- Segmentation By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles and Trucks

- Buses and Coaches

- Off-Highway and Agricultural Vehicles

- Electric Vehicles

- Autonomous and Connected Vehicles

- Others

- Segmentation By Technology and Functional Feature

- Heads-Up Display Compatible Glazing

- Augmented Reality Windshields

- Embedded Antenna Glass

- Heated Windshield and Rear Window

- ADAS Sensor-Integrated Glazing

- Electrochromic Dimming Glass

- Photovoltaic Integrated Glass

- Privacy and Switchable Glass

- Acoustic Interlayer Glass

- Others

- Segmentation By Coating Type

- Anti-Reflective Coating

- Hydrophobic and Self-Cleaning Coating

- Solar Control Coating

- Low-Emissivity Coating

- Conductive and Heating Coating

- Anti-Fog Coating

- Others

- Segmentation By Sales Channel

- Original Equipment Manufacturer (OEM) Channel

- Independent Aftermarket

- Insurance-Integrated Repair and Replacement Channel

- Mobile Glass Repair and Replacement Service

- Dealer and Authorized Service Network

- Others

- Segmentation By Application

- Structural and Safety Glazing

- Thermal and Solar Management

- Driver Information and Display Integration

- Acoustic Comfort and Noise Reduction

- Connectivity and Communication

- Aesthetic and Design Differentiation

- Others

- Segmentation By Interlayer Material

- Polyvinyl Butyral (PVB)

- Thermoplastic Polyurethane (TPU)

- Ethylene-Vinyl Acetate (EVA)

- Acoustic PVB

- Others

- Segmentation By End User

- Automotive OEMs

- Fleet and Commercial Operators

- Individual Vehicle Owners

- Insurance Companies

- Aftermarket Service Providers

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021–2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027–2036

Key Questions this Study Will Answer

- What is the projected global market valuation for automotive glass through 2036, segmented by product type, glass technology, vehicle type, and region, and which product and technology segments are expected to generate the highest incremental revenue growth over the forecast period? This analysis provides the quantitative foundation required for strategic investment planning, product portfolio prioritization, and competitive positioning across the automotive glass value chain.

- How is the accelerating global transition toward battery electric vehicles reshaping the product mix, average glass content per vehicle, and technology investment priorities of automotive glass manufacturers, and which advanced glazing technologies including panoramic roof systems, solar control glass, and electrochromic smart glass are expected to achieve the most rapid adoption rate expansion within electric vehicle platforms across the forecast horizon?

- What is the projected revenue contribution and growth trajectory of heads-up display compatible and augmented reality windshield glass, and how will the mainstream proliferation of these technologies across mid-market and volume vehicle segments alter the competitive dynamics, manufacturing investment requirements, and average selling price structures within the windshield product category?

- How are evolving end-of-life recyclability regulations, extended producer responsibility frameworks, and automotive supply chain sustainability commitments reshaping material specification requirements and capital investment priorities for glass manufacturers, and which circular economy and closed-loop recycling technologies are expected to achieve commercial viability within the forecast period?

- Who are the leading automotive glass manufacturers, tier-one functional glazing technology developers, interlayer material suppliers, and aftermarket distribution network operators currently defining the competitive landscape of the global automotive glass market, and what are their respective technology differentiation strategies, regional capacity investment plans, and partnership and acquisition priorities through the forecast horizon?

- Product Definition

- Scope of the Study

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Industry Publications, Automotive OEM Reports & Press Releases

- Government Automotive & Safety Authority Data (NHTSA, EURO NCAP, BIS, etc.)

- Automotive Glass Production, Trade & Replacement Market Statistics

- OEM Procurement & Automotive Supply Chain Databases

- Primary Research Design & Execution

- In-depth Interviews with Automotive Glass Manufacturers, OEM Procurement Heads & Aftermarket Distributors

- Surveys with Automotive OEMs, Independent Glass Retailers & Insurance Companies

- Expert Panel Validation

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Bottom-Up & Top-Down Reconciliation

- Vehicle Production & Parc Model for OEM & Aftermarket Demand

- Replacement Rate, Insurance Claims & AGRR Market Sizing Model

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Technology & Innovation Highlights

- Manufacturing Economics & Unit Economics Summary

- Average Plant CAPEX & OPEX Benchmarks

- OEM vs Aftermarket Margin & Profitability Analysis

- Smart Glass & Value-Added Glass Revenue Model Summary

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Geographic & Regional Trends

- Risk Assessment Framework

- Geopolitical & Trade Policy Risk

- Raw Material Price Volatility (Soda Ash, Float Glass, PVB) Risk

- Environmental & Regulatory Risk

- Financial / Market Risk

- Technology Substitution & EV Transition Risk

- Regulatory Framework & Policy Standards

- Automotive Glass Market Economics

- Manufacturing Economics & Unit Economics Framework

- Capital Expenditure (CAPEX) Structure

- Operating Expenditure (OPEX) Structure

- Revenue Model & Monetisation Levers

- Capacity Utilisation & Throughput Economics

- Payback Period & Return on Investment (ROI) Analysis

- Total Cost of Production vs Alternative Glazing Material Technologies

- Raw Material & Input Cost Analysis

- Float Glass & Soda Ash Price Trends (USD/tonne, 2021–2035)

- PVB Interlayer & Encapsulant Cost Dynamics

- Rare Earth & Specialty Chemical Costs for Smart Glass Coatings

- Energy Cost Structure in Glass Manufacturing

- Scrap, Cullet & Glass Recycling Value Chain Economics

- Impact of Next-Generation Smart & Lightweight Glass on Product Economics

- Aftermarket & Replacement (AGRR) Economics

- AGRR Cost Structure by Geography & Service Channel

- Insurance-Linked Replacement Rate & Claim Economics

- Mobile vs In-Shop Service Delivery Cost Comparison

- ADAS Recalibration Cost & Revenue Opportunity Post-Replacement

- Warranty & Guarantee Economics in OEM vs Aftermarket Glass

- Regulatory & Standards Compliance Economics

- ECE R43 & FMVSS 205 Safety Standard Compliance Cost Benchmarks

- ADAS Integration & Windshield Calibration Compliance Economics

- Noise, Vibration & Harshness (NVH) Regulation Compliance Costs

- Environmental & Emissions Regulation Compliance Costs (CO2, VOC, Recyclability)

- Global Automotive Glass Market Outlook

- Market Size & Forecast by Value (USD Billion, 2021–2036)

- Market Size & Forecast by Product Type

- Windshield / Windscreen

- Standard Windshield

- Acoustic Windshield

- Heated Windshield

- HUD-Integrated Windshield

- Solar-Control Windshield

- Side Glass (Door Glass)

- Front Door Glass

- Rear Door Glass

- Rear Glass / Backlight

- Heated Rear Glass

- Non-Heated Rear Glass

- Sunroof & Panoramic Roof Glass

- Standard Sunroof Glass

- Panoramic Roof Glass

- Electrochromic / Smart Roof Glass

- Sidelite & Quarterlight Glass

- Others (Interior Glass, Privacy Glass, Decorative Glass)

- Market Size & Forecast by Glass Technology

- Laminated Glass

- Standard PVB Laminated Glass

- Acoustic PVB Laminated Glass

- SentryGlas / SGP Ionoplast Laminated Glass

- Tempered / Toughened Glass

- Heat-Strengthened Glass

- Fully Tempered Glass

- Smart / Electrochromic Glass

- Electrically Dimmable Glass (PDLC, SPD, EC Technologies)

- Self-Tinting & Photochromic Glass

- Heads-Up Display (HUD)-Compatible Glass

- Wedge-Shaped HUD Windshield

- AR-HUD Integrated Glass

- Solar-Control & Low-Emissivity (Low-E) Glass

- Hydrophobic & Self-Cleaning Glass

- Gorilla Glass & Chemically Strengthened Glass

- Others (Polycarbonate Glazing, Aerogel Insulated Glass)

- Laminated Glass

- Market Size & Forecast by Vehicle Type

- Passenger Cars

- Sedans & Saloons

- SUVs & Crossovers

- Hatchbacks & Compacts

- Coupes, Convertibles & Cabriolets

- Light Commercial Vehicles (LCVs)

- Pickup Trucks

- Vans & Minivans

- Heavy Commercial Vehicles (HCVs)

- Trucks & Tractor-Trailers

- Buses & Coaches

- Electric & Hybrid Vehicles

- Battery Electric Vehicles (BEV)

- Plug-in Hybrid Electric Vehicles (PHEV)

- Hybrid Electric Vehicles (HEV)

- Others (Agricultural Vehicles, Construction Equipment, Special Purpose Vehicles)

- Passenger Cars

- Market Size & Forecast by Application

- Original Equipment Manufacturer (OEM)

- Tier-1 Direct Supply to Automotive OEMs

- Tier-2 Component Sub-Supply

- Aftermarket / Auto Glass Repair & Replacement (AGRR)

- Independent Auto Glass Repair & Replacement Centres

- Franchise & Chain AGRR Networks (Safelite, Carglass, Belron, etc.)

- Insurance-Driven Replacement

- Market Size & Forecast by Coating & Treatment Type

- Anti-Reflective (AR) Coating

- Hydrophobic & Oleophobic Coating

- Solar Control & Low-E Coating

- Anti-Fog & De-Icing Coating

- Scratch-Resistant Hard Coating

- Others (UV-Blocking, Photocatalytic, Antimicrobial Coating)

- Market Size & Forecast by End-Use Sector

- Automotive OEMs

- Global Mass-Market OEMs

- Premium & Luxury OEMs

- Electric Vehicle OEMs

- Independent Auto Glass Repair & Replacement (AGRR) Centres

- Insurance Companies (Claims-Driven Replacement)

- Fleet Operators & Automotive Leasing Companies

- Government & Public Transport Operators

- Others (Specialty Vehicle Builders, Defense, Off-Highway Equipment OEMs)

- Automotive OEMs

- Market Size & Forecast by Revenue Stream

- OEM Glass Supply Revenue

- Aftermarket & Replacement Glass Revenue

- Smart & Value-Added Glass Revenue (HUD, Acoustic, Electrochromic)

- Insurance-Linked Replacement Revenue

- Glass Chip Repair & Windshield Repair Revenue

- ADAS Calibration & Ancillary Services Revenue

- Glass Recycling & Circular Economy Revenue

- Market Size & Forecast by Sales Channel

- Automotive OEM Direct Supply Contracts

- Independent Aftermarket Distributors & Wholesalers

- Franchise & Chain Auto Glass Repair Networks

- Online & E-Commerce Platforms

- Insurance-Brokered Replacement Channels

- Government & Fleet Direct Procurement

- Asia-Pacific Automotive Glass Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Product Type

- By Glass Technology

- By Vehicle Type

- By Application

- By End-Use Sector

- By Revenue Stream

- By Sales Channel

- Key Demand Drivers (APAC-Specific)

- Competitive Landscape (APAC)

- Europe Automotive Glass Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Product Type

- By Glass Technology

- By Vehicle Type

- By Application

- By End-Use Sector

- By Revenue Stream

- By Sales Channel

- Key Demand Drivers (Europe-Specific)

- Competitive Landscape (Europe)

- North America Automotive Glass Market Outlook

- Market Overview & Strategic Importance

- Market Size & Forecast

- By Value (2020–2035)

- By Product Type

- By Glass Technology

- By Vehicle Type

- By Application

- By End-Use Sector

- By Revenue Stream

- By Sales Channel

- Key Demand Drivers (North America-Specific)

- Competitive Landscape (North America)

- Latin America Automotive Glass Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Product Type

- By Glass Technology

- By Vehicle Type

- By Application

- By End-Use Sector

- By Revenue Stream

- By Sales Channel

- Key Demand Drivers (LATAM-Specific)

- Competitive Landscape (Latin America)

- Middle East & Africa Automotive Glass Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Product Type

- By Glass Technology

- By Vehicle Type

- By Application

- By End-Use Sector

- By Revenue Stream

- By Sales Channel

- Key Demand Drivers (MEA-Specific)

- Competitive Landscape (MEA)

- Country-Wise Automotive Glass Market Outlook

- Market Size & Forecast by Country

- By Value

- By Product Type

- By Glass Technology

- By Vehicle Type

- By Application

- By End-Use Sector

- By Revenue Stream

- By Sales Channel

- Market Size & Forecast by Country

- Market Size & Forecast

- Market Size & Forecast

- Market Size & Forecast

- Market Size & Forecast

- Original Equipment Manufacturer (OEM)

- Manufacturing Economics & Unit Economics Framework

Countries Covered: United States, Canada, Germany, United Kingdom, France, Italy, Spain, Netherlands, Switzerland, China, Japan, India, South Korea, Australia, Singapore, Brazil, Mexico, Saudi Arabia, United Arab Emirates, South Africa

- Technology Landscape & Innovation Analysis

- Automotive Glass Technology Maturity Assessment

- Emerging & Disruptive Technologies in Automotive Glazing

- Digital Technologies in Manufacturing Operations & Quality Control

- Technology Readiness & Commercialisation Matrix – Key Automotive Glass Technologies

- Patent Landscape Analysis

- R&D Investment Benchmarking

- Value Chain & Supply Chain Analysis

- Automotive Glass Value Chain Mapping

- Supply Chain Concentration & Dependency Analysis

- Key Supplier Mapping by Product & Technology Programme

- Supplier Risk Heat Map

- Make vs Buy Strategy Trends Among Automotive Glass Manufacturers

- Pricing Analysis

- Automotive Glass Pricing Dynamics & Mechanisms

- Pricing by Product Type & Vehicle Segment

- Total Cost of Ownership (TCO) Analysis

- OEM vs Aftermarket Pricing Trends & Benchmarks

- Sustainability & Environmental Stewardship

- Environmental & Sustainability Landscape in Automotive Glass Manufacturing

- Carbon Footprint Benchmarking Across Glass Production Technologies

- Recycled Content & Cullet Integration Roadmap for Glass Manufacturers

- Glass Recyclability & End-of-Life Vehicle (ELV) Circular Economy Assessment

- Lightweighting & CO2 Reduction Pathway for Automotive OEMs

- ESG Reporting & Lifecycle Assessment (LCA) in Automotive Glass Operations

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level: Oligopoly-Led (AGC, NSG/Pilkington, Saint-Gobain, Fuyao) vs Regional Players

- Top 5 Automotive Glass Manufacturers Market Revenue Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis by Product & Application Segment

- Competitive Intensity Map by Segment & Region

- Player Classification

- Tier-1 Global Integrated Automotive Glass Manufacturers

- Tier-2 Regional & Specialist Glass Manufacturers

- Aftermarket & AGRR Service Network Players

- Emerging & Disruptive Players

- Competitive Analysis Frameworks

- Market Share Analysis by Product Type & Geography

- R&D Intensity Benchmarking

- OEM Customer Revenue & Long-Term Supply Contract Portfolio Comparison

- Geographic Revenue Exposure Comparison

- Company Profiles

- Company Overview, HQ & Organisational Structure

- Automotive Glass Products & Services Portfolio

- Revenue Breakdown

- Key OEM Supply Programmes & Platform Deployments

- Manufacturing Footprint & Key Facilities

- Recent Developments (M&A, Partnerships, New Products, Financial Results)

- SWOT Analysis

- Strategic Focus: Smart Glass Innovation, OEM Platform Wins, Aftermarket Expansion

- Strategic Output

- Market Opportunity Matrix

- High-Value Opportunity Quadrant Analysis

- Addressable Market by Segment & Region

- Time-to-Revenue Assessment by Opportunity

- White Space Opportunity Analysis

- Underserved Vehicle Segment & Product Type Gaps

- Geographic Markets with Low Penetration

- Technology Gaps with High Commercialisation Potential

- Customer Segment Unmet Needs

- Strategic Recommendations

- Product Portfolio & Innovation Strategy

- Technology & Digitalization Strategy

- Manufacturing Footprint & Capacity Expansion Strategy

- Aftermarket & AGRR Channel Growth Strategy

- Pricing & Commercial Strategy

- Sustainability & Regulatory Compliance Strategy

- Supply Chain & Raw Material Sourcing Strategy

- Partnership, M&A & Expansion Strategy

- Regional Growth Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-Term (2025–2028)

- Mid-Term (2029–2032)

- Long-Term (2033–2036)

- Market Opportunity Matrix

- Market Structure & Concentration