Market Definition

The Global Two-Wheeler Tire Market encompasses the design, manufacturing, distribution, and sale of tires specifically engineered for motorcycles, scooters, mopeds, electric two-wheelers, and performance and off-road two-wheeled vehicles across both original equipment and replacement channels worldwide. Two-wheeler tires constitute a safety-critical consumable component that directly governs vehicle dynamics, handling stability, braking performance, ride comfort, fuel efficiency, and all-weather operational capability across the diverse terrain and climatic conditions in which two-wheelers are deployed globally. The product landscape spans a broad spectrum of tire constructions, including radial, bias-ply, and belted bias configurations, as well as a wide range of tread pattern designs, rubber compound formulations, and dimensional specifications tailored to the specific performance requirements of commuter motorcycles, sport and supersport motorcycles, touring motorcycles, dual-sport and adventure motorcycles, scooters and maxi-scooters, electric two-wheelers, and off-road and motocross platforms. The value chain of this market extends from raw material suppliers of natural rubber, synthetic elastomers, carbon black, steel cord, and specialty chemicals through to tire manufacturers, authorized distributors, dealer networks, roadside fitment service providers, and organized replacement retail chains. The market is defined by the intersection of two-wheeler vehicle production trends, the evolving needs of an increasingly diverse global rider population, the rapid growth of electric two-wheeler platforms, advancing tire material science and engineering capabilities, and the regulatory and consumer safety standards that govern tire performance certification and fitment compliance across jurisdictions.

Market Insights

The global two-wheeler tire market is operating in a period of robust and structurally driven growth, underpinned by the continued expansion of two-wheeler vehicle ownership across emerging economies in Asia-Pacific, South Asia, Southeast Asia, Latin America, and Sub-Saharan Africa, where the two-wheeler remains the primary mode of personal and commercial mobility for hundreds of millions of consumers. As of 2026, the market is exhibiting resilient volume growth across both the original equipment and replacement segments, with the replacement tire segment constituting the larger share of total revenue owing to the high replacement frequency characteristic of two-wheeler tires relative to passenger vehicle tires, the large and continuously expanding global parc of in-use two-wheelers, and the growing consumer awareness of tire safety and performance in both mature and developing markets. The market is simultaneously experiencing a meaningful product mix upgrade, with consumers across a broadening range of geographies demonstrating increasing willingness to trade up to premium and performance-oriented tire products that offer superior grip, handling precision, wet-weather safety performance, and extended service life, driving favorable average selling price trends that are amplifying the revenue growth rate beyond volume growth alone.

A structurally significant development reshaping the product and technology landscape of the two-wheeler tire market is the rapid scaling of electric two-wheeler platforms across multiple vehicle categories and geographies, which is generating distinct and demanding new tire performance requirements that are creating both product development opportunities and technology differentiation imperatives for tire manufacturers. Electric two-wheelers are characterized by instantaneous torque delivery profiles, elevated vehicle curb weights attributable to battery pack mass, regenerative braking deceleration dynamics, and operational noise environments that differ fundamentally from those of conventional internal combustion engine two-wheelers, collectively imposing more demanding requirements on tire compound durability, traction management, load-carrying capacity, and rolling resistance optimization. Tire manufacturers are investing in the development of dedicated electric two-wheeler tire product lines engineered with reinforced carcass constructions to manage elevated load ratings, specifically formulated tread compounds optimized for low rolling resistance to maximize battery range while maintaining wet grip performance, and tread patterns designed for the noise sensitivity characteristics of electric powertrain platforms. The commercial scaling of these dedicated products represents one of the most consequential product portfolio evolution opportunities within the market over the forecast period.

The premiumisation of the two-wheeler tire market is being advanced by the concurrent growth of the sport, adventure touring, and premium commuter motorcycle segments, particularly in North America, Europe, Japan, and the rapidly evolving premium motorcycle markets of China, India, and Southeast Asia. Riders investing in higher-displacement and higher-value motorcycles are exhibiting a correspondingly elevated propensity to specify premium and ultra-high-performance original equipment and replacement tires, driving demand for products incorporating the most advanced silica compound technologies, multi-radius profile designs, construction innovations including zero-degree steel belt applications, and category-specific compounds engineered for track-day, touring, or all-season performance profiles. Simultaneously, the growing penetration of tubeless tire technology into the mass-market scooter and commuter motorcycle segments, particularly in urban markets where puncture resistance and convenience are primary purchasing considerations, is driving a structural shift in the product mix toward higher-value tubeless constructions that offer improved safety and serviceability relative to tube-type alternatives and support a favorable price and margin premium for manufacturers and distributors operating in these channels.

From a regional perspective, Asia-Pacific overwhelmingly dominates the global two-wheeler tire market in volume terms, with India, China, Indonesia, Vietnam, and Thailand collectively accounting for the majority of global two-wheeler production and in-use vehicle parc, and consequently representing the largest and most strategically consequential markets for both original equipment and replacement tire volumes. India in particular is emerging as the single most important market for the global two-wheeler tire industry, combining the world’s largest two-wheeler production base with a rapidly growing electric two-wheeler segment, a large and increasingly organized replacement market, and a consumer base exhibiting progressive premiumisation across urban mobility categories. Europe and North America represent high-value markets characterized by a premium and performance-oriented product mix, strong aftermarket dynamics driven by the large and active sport and touring motorcycle communities, and advanced retail and fitment service channel structures. Latin America, the Middle East, and Sub-Saharan Africa represent developing but structurally attractive markets where expanding two-wheeler ownership rates, improving road infrastructure, and growing consumer access to organized tire retail channels are collectively supporting above-average volume growth trajectories relative to more mature geographies.

Key Drivers

Expanding Two-Wheeler Ownership in Emerging and Developing Economies Driven by Urbanization and Mobility Demand

The most foundational demand driver for the global two-wheeler tire market is the sustained and structurally driven expansion of two-wheeler vehicle ownership across the populous emerging and developing economies of Asia, Africa, and Latin America, where rapid urbanization, rising disposable incomes, and the economic efficiency of two-wheelers as a primary mobility solution are collectively supporting consistent growth in new vehicle registrations and the expansion of the in-use vehicle parc. In densely populated urban environments across South and Southeast Asia, the two-wheeler serves not only as a personal commuter vehicle but as the primary commercial platform for last-mile delivery, courier services, food delivery logistics, and small goods transport, generating high-intensity daily utilization patterns that translate into elevated tire replacement frequencies and durable recurring demand throughout the vehicle lifecycle. The formalization and growth of organized motorcycle taxi, ride-hailing, and delivery platform ecosystems across these markets is additionally creating a fleet purchasing channel for replacement tires that operates on accelerated replacement cycles relative to individual consumer purchasing, providing a structurally growing and commercially accessible demand stream for tire manufacturers and their distribution partners. The continued expansion of road network coverage in developing economies is progressively extending the effective operational range of two-wheelers and broadening the geographic footprint of the replacement tire market in regions where organized fitment service infrastructure has historically been limited to urban centers.

Rapid Growth of Electric Two-Wheelers and the Creation of a New High-Value Tire Product Category

The accelerating global adoption of electric two-wheelers, progressing from government-incentivized early deployment toward increasingly market-driven mainstream consumer adoption across a growing range of vehicle categories and price segments, is establishing a new and commercially significant product category within the two-wheeler tire market that is characterized by elevated performance requirements, differentiated engineering specifications, and the potential for premium pricing relative to equivalent conventional tire products. The policy environments of the major electric two-wheeler markets, including China, India, and several European economies, continue to provide fiscal incentives, registration benefits, and regulatory tailwinds that are sustaining strong electric two-wheeler sales momentum and rapidly expanding the installed base of vehicles that will generate replacement tire demand over the forecast period. For tire manufacturers, the electric two-wheeler opportunity represents not merely a volume extension of existing product lines but a genuine technology development and product differentiation opportunity, as the distinct dynamic and load characteristics of electric platforms demand purpose-engineered solutions that cannot be fully satisfied by conventional tire designs. Early movers in the development of credentialed and OEM-validated electric two-wheeler tire product lines are establishing technology and commercial positions that are expected to translate into durable competitive advantages as the electric two-wheeler installed base scales and replacement demand accelerates.

Increasing Consumer Safety Awareness and the Growing Adoption of Premium Radial and Tubeless Tire Technologies

A demand driver of progressively increasing commercial significance is the growing awareness among two-wheeler riders globally of the direct causal relationship between tire quality, maintenance, and fitment practices and road safety outcomes, which is translating into measurable consumer behavior changes that favor the adoption of higher-specification radial, tubeless, and advanced compound tire products over lower-cost bias-ply or tube-type alternatives. Road safety campaigns, insurance premium differentiation, and the increasing availability of digital consumer information are collectively educating riders on the performance advantages of premium tire technologies in terms of wet and dry braking distances, stability under emergency maneuver conditions, and resistance to sudden pressure loss events. Regulatory initiatives in several key markets are additionally mandating minimum tire performance standards for newly registered two-wheelers and strengthening enforcement of roadworthy tire condition requirements for in-service vehicles, creating a compliance-driven upgrade dynamic within the replacement market. Tire manufacturers are amplifying these demand dynamics through investment in consumer-facing brand building, performance certification communication, and dealer technical training programs designed to reinforce the safety and performance value proposition of premium tire products relative to unbranded or counterfeit alternatives that remain prevalent in price-sensitive market segments.

Key Challenges

Volatility in Natural Rubber and Petrochemical Raw Material Costs and the Challenge of Margin Management

The global two-wheeler tire industry is structurally exposed to significant and persistent volatility in the prices of its principal raw material inputs, most notably natural rubber, synthetic rubber derived from petrochemical feedstocks, carbon black, and specialty processing chemicals, collectively representing the dominant component of the total manufacturing cost base for tire production. Natural rubber prices are subject to supply-side dynamics including weather-related yield disruptions in major producing regions, disease pressures, replanting cycle lags, and geopolitical developments that can create substantial price movements across relatively short time horizons. Synthetic rubber and carbon black prices are correlated with crude oil and natural gas market cycles, exposing tire manufacturers to the additional volatility layer introduced by global energy market dynamics. Managing these input cost fluctuations within the context of competitive market pricing structures, long-term supply agreements with OEM customers that incorporate cost reduction expectations, and price-sensitive replacement market consumer behavior represents a persistent and technically demanding margin management challenge. Tire manufacturers are responding through investment in natural rubber supply chain integration, synthetic rubber compound development programs aimed at reducing dependency on specific petrochemical derivatives, and advanced procurement hedging strategies, but the fundamental raw material cost exposure remains a structural feature of the industry’s financial profile that constrains profitability visibility across the business cycle.

Proliferation of Low-Cost and Counterfeit Tire Products and the Challenge of Protecting Market Position in Price-Sensitive Segments

A persistent and commercially significant challenge facing established tire manufacturers in the global two-wheeler market is the widespread availability and consumer adoption of low-cost and counterfeit tire products in price-sensitive replacement market segments across emerging economies, where a meaningful share of replacement tire demand is served by unbranded, substandard, or fraudulently labeled products that compete primarily on the basis of price rather than certified performance or safety compliance. The fragmented and informally structured nature of the replacement tire distribution and fitment channel in many high-volume markets in South and Southeast Asia, Latin America, and Sub-Saharan Africa creates an environment in which quality verification and brand authentication are difficult to enforce at the point of sale, enabling the circulation of non-compliant products that expose riders to elevated safety risks while simultaneously eroding the volume and pricing power of compliant manufacturers. Counterfeit products bearing fraudulent brand markings of established tire manufacturers are a documented presence in several major markets, undermining consumer trust and imposing enforcement costs on brand owners. Addressing this challenge requires sustained investment in distribution channel development and oversight, consumer education on tire identification and quality verification, engagement with regulatory authorities on counterfeit enforcement, and the development of entry-tier branded product lines that offer a credible quality-differentiated alternative to unbranded products at accessible price points in volume segments.

Technological Adaptation Requirements for Electric Two-Wheeler Tire Development and the Pace of OEM Validation

The transition of the two-wheeler vehicle market toward electric powertrains, while representing a significant commercial opportunity for tire manufacturers, also constitutes a near-term technical and commercial challenge arising from the investment requirements, development lead times, and OEM validation cycles associated with bringing purpose-engineered electric two-wheeler tire products to market at competitive cost structures and sufficient scale. The differentiated performance requirements of electric two-wheelers demand compound formulations, carcass architectures, and tread designs that deviate meaningfully from the proven product platforms and manufacturing process parameters of existing conventional two-wheeler tire lines, necessitating dedicated research and development investment, pilot production trials, and extensive validation testing before products can be submitted for OEM evaluation. The OEM qualification and fitment homologation process for new tire products on electric platforms involves time-consuming vehicle dynamics, endurance, and safety testing programs that can extend development-to-market timelines significantly. Tire manufacturers that are slower to complete this development and validation cycle risk being excluded from the original equipment fitment positions on rapidly scaling electric two-wheeler platforms, which in turn determines replacement market brand familiarity and preference over the subsequent years of the vehicle’s operational life. Balancing the pace of electric tire development investment against the financial constraints of managing existing conventional product lines and the uncertainty of electric two-wheeler platform adoption trajectories across diverse markets presents a strategic resource allocation challenge for the industry.

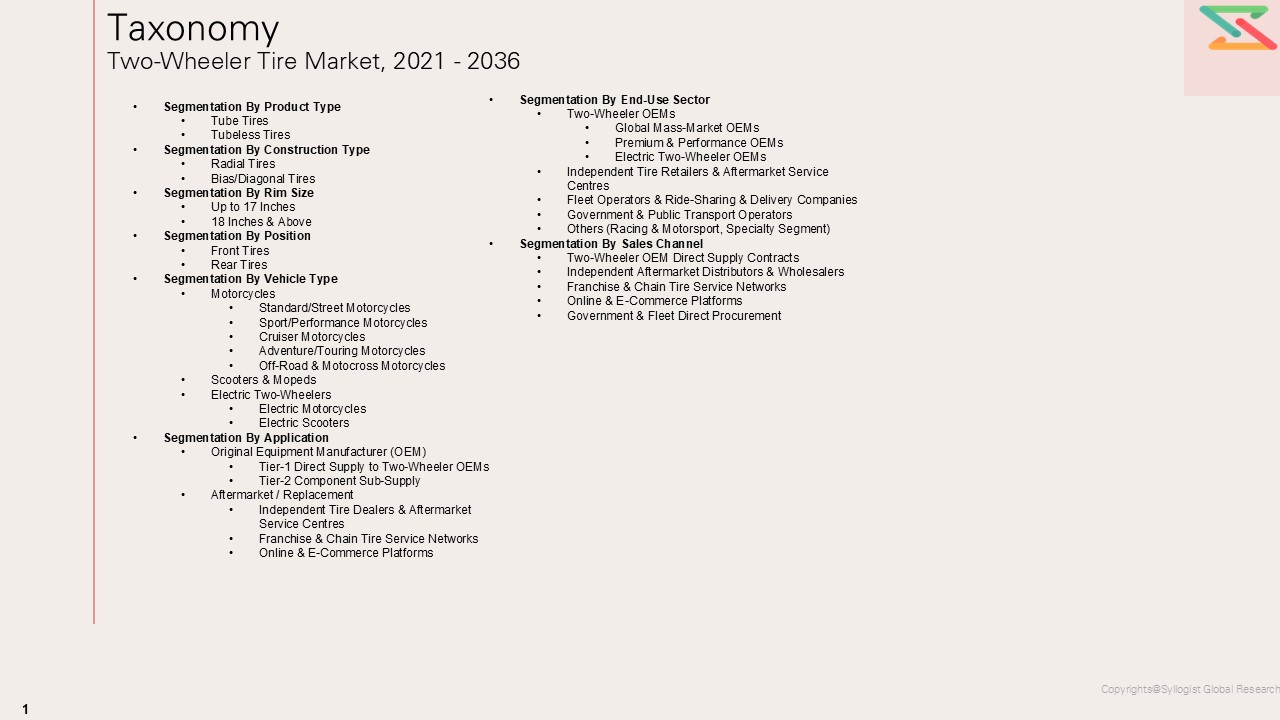

Market Segmentation

- Segmentation By Vehicle Type

- Motorcycles

- Scooters and Maxi-Scooters

- Mopeds

- Electric Two-Wheelers

- Sport and Supersport Motorcycles

- Adventure and Dual-Sport Motorcycles

- Touring and Cruiser Motorcycles

- Off-Road and Motocross Motorcycles

- Others

- Segmentation By Tire Construction Type

- Radial Tires

- Bias-Ply Tires

- Belted Bias Tires

- Others

- Segmentation By Tire Design

- Tubeless Tires

- Tube-Type Tires

- Run-Flat Tires

- Others

- Segmentation By Rim Size

- Below 14 Inches

- 14 to 17 Inches

- 18 Inches and Above

- Segmentation By Application and Terrain

- On-Road Tires

- Off-Road and Knobby Tires

- Dual-Sport and All-Terrain Tires

- Track and Racing Slick Tires

- All-Season Tires

- Winter and Snow Tires

- Others

- Segmentation By Tread Pattern

- Symmetrical Tread

- Asymmetrical Tread

- Directional Tread

- Block Tread

- Slick and Semi-Slick Tread

- Others

- Segmentation By Rubber Compound Technology

- Natural Rubber Compound

- Synthetic Rubber Compound

- Silica-Based Compound

- Carbon Black Compound

- Multi-Compound and Dual-Compound

- Bio-Based and Sustainable Compound

- Others

- Segmentation By Sales Channel

- Original Equipment Manufacturer (OEM) Channel

- Independent Aftermarket

- Authorized Dealer and Service Network

- Roadside and Local Fitment Centers

- Online and E-Commerce Channel

- Fleet and Commercial Operator Direct Supply

- Others

- Segmentation By End User

- Individual Consumers and Private Riders

- Delivery and Logistics Fleet Operators

- Ride-Hailing and Motorcycle Taxi Platforms

- Racing Teams and Motorsport Organizations

- Government and Para-Military Fleet Operators

- Agricultural and Rural Utility Users

- Others

- Segmentation By Price Tier

- Premium Tier

- Mid-Range Tier

- Economy Tier

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021–2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027–2036

Key Questions this Study Will Answer

- What is the projected global market valuation and volume for two-wheeler tires through 2036, segmented by vehicle type, tire construction, sales channel, and region, and which product categories and geographies are expected to generate the highest incremental revenue and volume growth across the forecast period?

- How is the accelerating adoption of electric two-wheelers reshaping product development priorities, OEM fitment strategies, and replacement market dynamics within the two-wheeler tire industry, and which tire construction, compound, and performance specification requirements specific to electric platforms are expected to establish the most durable technology differentiation opportunities for leading manufacturers?

- What are the projected relative growth trajectories of the original equipment and replacement market segments across major geographies, and how are evolving consumer preferences for tubeless construction, radial technology, and premium compound performance influencing product mix dynamics and average selling price trends in both channels?

- How are raw material cost volatility, the proliferation of low-cost and counterfeit products in price-sensitive emerging markets, and the competitive pricing dynamics of the economy and mid-range segments expected to influence the revenue and profitability profiles of tire manufacturers across different market tiers and geographic operating environments?

- Who are the leading tire manufacturers, compound technology developers, distribution network operators, and electric two-wheeler OEM fitment partners currently defining the competitive landscape of the global two-wheeler tire market, and what are their respective technology investment priorities, geographic expansion strategies, and product portfolio development trajectories through the forecast horizon?

- Product Definition

- Scope of the Study

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Industry Publications, Two-Wheeler OEM Reports & Press Releases

- Government Transport & Road Safety Authority Data (MoRTH, NHTSA, BIS, etc.)

- Two-Wheeler Tire Production, Trade & Replacement Market Statistics

- OEM Procurement & Two-Wheeler Supply Chain Databases

- Primary Research Design & Execution

- In-depth Interviews with Two-Wheeler Tire Manufacturers, OEM Procurement Heads & Aftermarket Distributors

- Surveys with Two-Wheeler OEMs, Independent Tire Dealers & Fleet Operators

- Expert Panel Validation

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Bottom-Up & Top-Down Reconciliation

- Two-Wheeler Production & Parc Model for OEM & Replacement Demand

- Replacement Rate & Mileage-Driven Aftermarket Tire Market Sizing Model

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Technology & Innovation Highlights

- Manufacturing Economics & Unit Economics Summary

- Average Plant CAPEX & OPEX Benchmarks

- OEM vs Aftermarket Margin & Profitability Analysis

- Performance & Premium Tire Revenue Model Summary

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Geographic & Regional Trends

- Risk Assessment Framework

- Geopolitical & Trade Policy Risk

- Raw Material Price Volatility (Natural Rubber, Synthetic Rubber, Carbon Black) Risk

- Environmental & Regulatory Risk

- Financial / Market Risk

- Technology Substitution & Electric Two-Wheeler Transition Risk

- Regulatory Framework & Policy Standards

- Global Two-Wheeler Tire Market Economics

- Manufacturing Economics & Unit Economics Framework

- Capital Expenditure (CAPEX) Structure

- Operating Expenditure (OPEX) Structure

- Revenue Model & Monetisation Levers

- Capacity Utilisation & Throughput Economics

- Payback Period & Return on Investment (ROI) Analysis

- Total Cost of Production vs Alternative Tire Technologies

- Raw Material & Input Cost Analysis

- Natural Rubber & Synthetic Rubber Price Trends (USD/tonne, 2021–2035)

- Carbon Black & Silica Reinforcement Cost Dynamics

- Steel Cord, Nylon & Textile Reinforcement Cost Analysis

- Chemical Additives & Compounding Cost Structure

- Energy Cost Structure in Tire Manufacturing

- Scrap Tire Recycling & Circular Economy Value Chain Economics

- Aftermarket & Replacement Tire Economics

- Replacement Cost Structure by Geography & Service Channel

- Mileage-Driven Replacement Rate & Demand Dynamics

- Roadside Assistance & Mobile Tire Fitment Service Delivery Cost Comparison

- Warranty & Guarantee Economics in OEM vs Aftermarket Tires

- Global Two-Wheeler Tire Market Outlook

- Market Size & Forecast by Value (USD Billion, 2021–2036)

- Market Size & Forecast by Product Type

- Tube Tires

- Tubeless Tires

- Market Size & Forecast by Construction Type

- Radial Tires

- Bias/Diagonal Tires

- Market Size & Forecast by Rim Size

- Up to 17 Inches

- 18 Inches & Above

- Market Size & Forecast by Position

- Front Tires

- Rear Tires

- Market Size & Forecast by Vehicle Type

- Motorcycles

- Standard/Street Motorcycles

- Sport/Performance Motorcycles

- Cruiser Motorcycles

- Adventure/Touring Motorcycles

- Off-Road & Motocross Motorcycles

- Scooters & Mopeds

- Electric Two-Wheelers

- Electric Motorcycles

- Electric Scooters

- Market Size & Forecast by Application

- Original Equipment Manufacturer (OEM)

- Tier-1 Direct Supply to Two-Wheeler OEMs

- Tier-2 Component Sub-Supply

- Aftermarket / Replacement

- Independent Tire Dealers & Aftermarket Service Centres

- Franchise & Chain Tire Service Networks

- Online & E-Commerce Platforms

- Market Size & Forecast by End-Use Sector

- Two-Wheeler OEMs

- Global Mass-Market OEMs

- Premium & Performance OEMs

- Electric Two-Wheeler OEMs

- Independent Tire Retailers & Aftermarket Service Centres

- Fleet Operators & Ride-Sharing & Delivery Companies

- Government & Public Transport Operators

- Others (Racing & Motorsport, Specialty Segment)

- Two-Wheeler OEMs

- Market Size & Forecast by Sales Channel

- Two-Wheeler OEM Direct Supply Contracts

- Independent Aftermarket Distributors & Wholesalers

- Franchise & Chain Tire Service Networks

- Online & E-Commerce Platforms

- Government & Fleet Direct Procurement

- Asia-Pacific Two-Wheeler Tire Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Product Type

- By Construction Type

- By Vehicle Type

- By Application

- By End-Use Sector

- By Sales Channel

- Key Demand Drivers (APAC-Specific)

- Competitive Landscape (APAC)

- Europe Two-Wheeler Tire Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Product Type

- By Construction Type

- By Vehicle Type

- By Application

- By End-Use Sector

- By Sales Channel

- Key Demand Drivers (Europe-Specific)

- Competitive Landscape (Europe)

- North America Two-Wheeler Tire Market Outlook

- Market Overview & Strategic Importance

- Market Size & Forecast

- By Value (2020–2035)

- By Product Type

- By Construction Type

- By Vehicle Type

- By Application

- By End-Use Sector

- By Sales Channel

- Key Demand Drivers (North America-Specific)

- Competitive Landscape (North America)

- Latin America Two-Wheeler Tire Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Product Type

- By Construction Type

- By Vehicle Type

- By Application

- By End-Use Sector

- By Sales Channel

- Key Demand Drivers (LATAM-Specific)

- Competitive Landscape (Latin America)

- Middle East & Africa Two-Wheeler Tire Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Product Type

- By Construction Type

- By Vehicle Type

- By Application

- By End-Use Sector

- By Sales Channel

- Key Demand Drivers (MEA-Specific)

- Competitive Landscape (MEA)

- Country-Wise Two-Wheeler Tire Market Outlook

- Market Size & Forecast by Country

- By Value

- By Product Type

- By Construction Type

- By Vehicle Type

- By Application

- By End-Use Sector

- By Sales Channel

- Market Size & Forecast by Country

- Market Size & Forecast

- Market Size & Forecast

- Market Size & Forecast

- Market Size & Forecast

- Original Equipment Manufacturer (OEM)

- Motorcycles

- Manufacturing Economics & Unit Economics Framework

Countries Covered: India, China, Indonesia, Thailand, Vietnam, Japan, South Korea, Australia, Germany, United Kingdom, France, Italy, Spain, United States, Canada, Brazil, Mexico, Saudi Arabia, United Arab Emirates, South Africa

- Technology Landscape & Innovation Analysis

- Two-Wheeler Tire Technology Maturity Assessment

- Emerging & Disruptive Technologies in Two-Wheeler Tires

- Digital Technologies in Manufacturing Operations & Quality Control

- Technology Readiness & Commercialisation Matrix – Key Two-Wheeler Tire Technologies

- Patent Landscape Analysis

- R&D Investment Benchmarking

- Value Chain & Supply Chain Analysis

- Two-Wheeler Tire Value Chain Mapping

- Supply Chain Concentration & Dependency Analysis

- Key Supplier Mapping by Product & Technology Programme

- Supplier Risk Heat Map

- Make vs Buy Strategy Trends Among Two-Wheeler Tire Manufacturers

- Pricing Analysis

- Two-Wheeler Tire Pricing Dynamics & Mechanisms

- Pricing by Construction Type & Vehicle Segment

- Total Cost of Ownership (TCO) Analysis

- OEM vs Aftermarket Pricing Trends & Benchmarks

- Sustainability & Environmental Stewardship

- Environmental & Sustainability Landscape in Two-Wheeler Tire Manufacturing

- Carbon Footprint Benchmarking Across Tire Production Technologies

- Recycled & Bio-Based Material Integration Roadmap for Tire Manufacturers

- Tire Recyclability & End-of-Life Tire (ELT) Circular Economy Assessment

- Lightweighting & Rolling Resistance Reduction Pathway for Two-Wheeler OEMs

- ESG Reporting & Lifecycle Assessment (LCA) in Two-Wheeler Tire Operations

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level: Global Leaders vs Regional Players

- Top 5 Two-Wheeler Tire Manufacturers Market Revenue Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis by Product & Application Segment

- Competitive Intensity Map by Segment & Region

- Player Classification

- Tier-1 Global Integrated Two-Wheeler Tire Manufacturers

- Tier-2 Regional & Specialist Tire Manufacturers

- Aftermarket & Replacement Tire Service Network Players

- Emerging & Disruptive Players

- Competitive Analysis Frameworks

- Market Share Analysis by Product Type & Geography

- R&D Intensity Benchmarking

- OEM Customer Revenue & Long-Term Supply Contract Portfolio Comparison

- Geographic Revenue Exposure Comparison

- Company Profiles

- Company Overview, HQ & Organisational Structure

- Two-Wheeler Tire Products & Services Portfolio

- Revenue Breakdown

- Key OEM Supply Programmes & Platform Deployments

- Manufacturing Footprint & Key Facilities

- Recent Developments (M&A, Partnerships, New Products, Financial Results)

- SWOT Analysis

- Strategic Focus: Performance Tire Innovation, OEM Platform Wins, Aftermarket Expansion

- Strategic Output

- Market Opportunity Matrix

- High-Value Opportunity Quadrant Analysis

- Addressable Market by Segment & Region

- Time-to-Revenue Assessment by Opportunity

- White Space Opportunity Analysis

- Underserved Vehicle Segment & Product Type Gaps

- Geographic Markets with Low Penetration

- Technology Gaps with High Commercialisation Potential

- Customer Segment Unmet Needs

- Strategic Recommendations

- Product Portfolio & Innovation Strategy

- Technology & Digitalization Strategy

- Manufacturing Footprint & Capacity Expansion Strategy

- Aftermarket & Replacement Channel Growth Strategy

- Pricing & Commercial Strategy

- Sustainability & Regulatory Compliance Strategy

- Supply Chain & Raw Material Sourcing Strategy

- Partnership, M&A & Expansion Strategy

- Regional Growth Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-Term (2025–2028)

- Mid-Term (2029–2032)

- Long-Term (2033–2036)

- Market Opportunity Matrix

- Market Structure & Concentration