Market Definition

The Global Mining Tire Market encompasses the development, manufacturing, supply, and servicing of large and ultra-large off-the-road tires specifically engineered for the demanding operational requirements of surface mining, underground mining, quarrying, and bulk material handling applications across the global extractive industries sector. Mining tires are purpose-built components that must simultaneously deliver extraordinary load-carrying capacity, resistance to cut, chip, and tear damage from sharp rock and ore surfaces, heat dissipation performance under sustained high-speed and high-load operating cycles, and structural integrity under the severe impact and dynamic loading conditions characteristic of haul roads, ramps, loading zones, and crushing circuits. The product scope of this market includes tires fitted to ultra-class and large rigid dump trucks, articulated dump trucks, wheel loaders, mining shovels and excavators, graders and dozers, scrapers, underground load-haul-dump vehicles, drill rigs, and ancillary support equipment deployed across open-pit and underground mining operations for coal, iron ore, copper, gold, bauxite, potash, and other metallic and non-metallic mineral extraction activities. The market value chain encompasses natural rubber and synthetic compound suppliers, steel cord and fabric producers, specialized tire manufacturing facilities, authorized dealerships and distribution networks, mine-site tire management service providers, and retreading operations that extend the serviceable life of high-value mining tire casings. The economics of this market are characterized by the exceptional unit values of large and ultra-large mining tires, the critical influence of tire performance on mine site productivity and total cost of extraction, and the strategic importance that mining operators assign to tire supply continuity, service support quality, and total cost of ownership optimization across their heavy equipment fleets.

Market Insights

The global mining tire market is operating within a complex but fundamentally constructive demand environment in 2026, shaped by the sustained operational requirements of the global mining industry, the structural demand growth for critical minerals essential to energy transition technologies, and the progressive modernization of heavy mining equipment fleets across major producing regions. Global mining activity across the copper, lithium, cobalt, nickel, iron ore, and coal segments is generating consistent and volume-intensive demand for replacement mining tires, as operational haul roads, loading zones, and ramp grades subject large tires to wear and damage cycles that necessitate regular replacement to maintain equipment availability and operational safety standards. The original equipment segment is simultaneously receiving support from sustained capital expenditure commitments by major mining operators expanding production capacity at existing operations and developing new mine projects in response to the strong structural demand outlook for energy transition metals. The market is additionally benefiting from the ongoing trend toward larger and higher-capacity mobile mining equipment, as mining operators seek to improve payload efficiency and reduce operating cost per tonne, driving incremental demand for ultra-large tire sizes in the largest diameter categories that command the highest unit values and most specialized manufacturing capabilities.

A defining characteristic of the current mining tire market landscape is the intensifying focus of both tire manufacturers and mining operators on total cost of ownership optimization frameworks that evaluate tire performance not merely on the basis of purchase price per unit but on the comprehensive economic metrics of cost per tonne hauled, tyre hours achieved relative to benchmark life targets, unplanned downtime attributable to tire failures, and the residual casing value available for retreading at end of first service life. This total cost of ownership orientation is driving demand for premium tire products manufactured to the highest compound durability and structural integrity specifications, as the productivity and availability costs of a premature tire failure on a haul truck carrying hundreds of tonnes of ore per cycle substantially outweigh the incremental purchase cost of a superior tire product. Mine site tire management programs, encompassing inflation pressure monitoring, rotation scheduling, load and speed compliance management, and damage cause analysis, are becoming increasingly formalized and data-driven as mining operators leverage telematics and sensor technology to maximize the performance of their tire asset base. These programs are generating commercially valuable operational data that is enabling more precise tire product specification and failure root cause analysis, creating closer technical collaboration relationships between tire manufacturers and their largest mine site customers.

The retreading and remanufacturing segment represents an economically and strategically important component of the global mining tire market, particularly for large and ultra-large tire sizes where the initial casing investment is substantial and the recovery of value through one or more retreading cycles can materially reduce the effective cost per tyre hour across the asset lifecycle. The viability of retreading as a cost management strategy is contingent on the structural integrity of the original tire casing at end of first service life, which in turn depends on the quality of the original tire construction, the adherence of the operating mine to load, speed, and inflation management protocols, and the discipline of the mine site tire inspection program in identifying and retiring damaged casings before structural integrity is compromised. Leading tire manufacturers are investing in casing durability as a distinct engineering objective alongside tread compound performance and structural load capacity, recognizing that the retreadability of their tires constitutes a commercially significant customer value proposition in cost-sensitive mining market conditions. The availability of certified retreading services by authorized retreaders using original equipment manufacturer-approved tread compounds and construction processes is an important factor in mine operator tire sourcing decisions for large fleets where the economics of retreading can generate substantial aggregate cost savings.

From a regional perspective, the Asia-Pacific region dominates global mining tire demand by volume, underpinned by the scale of mining activity in Australia, China, India, and Indonesia across iron ore, coal, copper, bauxite, and nickel commodity categories that collectively represent the largest installed bases of heavy mining equipment globally. Australia is a particularly critical market owing to the combination of large-scale iron ore and coal operations utilizing ultra-class haul fleets, high operational intensity, and a well-developed tire management and retreading service infrastructure. Latin America, led by Chile and Peru as the world’s dominant copper producing nations, and Brazil with its extensive iron ore and bauxite mining operations, represents the second most significant regional demand base and one of the highest-value markets owing to the prevalence of large and ultra-large equipment fleets at major porphyry copper mines operating at significant altitudes and in challenging haul road conditions. North America and Africa represent structurally important markets with distinct commodity profiles, with North American demand supported by coal, copper, gold, and oil sands operations and African demand growing in line with expanding copper, cobalt, and gold production particularly across the Central African Copperbelt and West African gold producing regions.

Key Drivers

Structural Demand Growth for Critical and Energy Transition Minerals Driving Sustained Mining Investment and Equipment Utilization

The most consequential long-term demand driver for the global mining tire market is the structural and policy-reinforced expansion of mining activity directed at critical minerals whose extraction and processing are fundamental to the global energy transition, including copper for electrical wiring and charging infrastructure, lithium for battery cell manufacturing, nickel and cobalt for battery cathode chemistry, and rare earth elements for permanent magnet applications in electric motors and wind turbines. The scale of mineral supply expansion required to support ambitious global electrification and decarbonization trajectories across the power generation, automotive, and industrial sectors is compelling mining operators and project developers to accelerate capital expenditure on new mine development and existing operation expansion programs, driving growth in the installed base of heavy mining equipment and consequently in the demand for original equipment and replacement tires. The sustained high price environments for several critical minerals are supporting the economic viability of capital-intensive mine developments in geologically complex and geographically remote locations that require larger equipment fleets and generate more demanding haul road conditions, both of which are favorable factors for mining tire demand volume and average product specification. This structural demand driver is expected to maintain an elevated trajectory of mining investment and equipment utilization across the forecast period, providing durable and volume-intensive market support for the global mining tire industry.

Progressive Fleet Modernization and the Transition Toward Ultra-Class Equipment to Improve Mining Productivity Economics

A powerful and commercially significant driver reshaping the product mix and average unit value dynamics of the global mining tire market is the ongoing transition by major open-pit mining operators toward larger and higher-payload equipment configurations as a primary lever for reducing operating cost per tonne of material moved and improving the economic competitiveness of their operations in an environment of progressively deeper open pits, longer haul distances, and intensifying productivity optimization pressures. The migration from standard large rigid dump trucks to ultra-class payload configurations is driving demand for the largest diameter tires in the market, which are manufactured by a limited number of qualified facilities globally, command the highest unit values, and generate the most technically demanding performance requirements in terms of heat dissipation, load endurance, and structural fatigue resistance. Concurrently, mining operators are investing in the expansion of their wheel loader, motor grader, and ancillary support equipment fleets to sustain the material movement capacity required to service larger primary haulage equipment, generating parallel demand growth across the broader range of off-the-road tire size categories. The equipment fleet modernization trend is additionally being reinforced by the progressive introduction of autonomous haulage systems at major open-pit operations, which impose distinct tire performance and uniformity requirements owing to the precision of load, speed, and routing management algorithms that govern autonomous vehicle operation and the implications of tire-related deviations for system-level operational efficiency.

Rising Operational Cost Consciousness and the Adoption of Advanced Tire Management Programs to Maximize Asset Productivity

The intensifying focus of mining operators on operational cost efficiency and equipment availability optimization is constituting a market driver that is simultaneously elevating the average specification and unit value of mining tires purchased and deepening the commercial engagement between tire suppliers and mine site customers through value-added service relationships. As tire costs represent a significant line item within the total operating cost structure of large open-pit mining operations, procurement and operational teams are applying increasingly rigorous analytical frameworks to tire purchasing decisions, service contract structures, and operational management practices, creating demand for premium tire products that can demonstrably deliver superior tyre hours, lower failure rates, and higher retreadable casing recovery rates relative to lower-cost alternatives. The adoption of real-time tire pressure and temperature monitoring systems, predictive tire failure analytics platforms, and integrated tire management software solutions is enabling mine site operators to extract a higher proportion of the design service life from their tire assets while simultaneously improving safety through early detection of pressure loss and structural anomalies. These technology investments are creating new commercial opportunities for tire manufacturers and service providers to develop bundled product and service offerings that align tire supplier revenue with mine site productivity outcomes, strengthening customer retention and supporting premium pricing by demonstrating quantified total cost of ownership advantages over the full tire asset lifecycle.

Key Challenges

Supply Concentration Risk and the Structural Constraints of Ultra-Large Mining Tire Manufacturing Capacity

A structurally distinctive challenge within the global mining tire market is the high degree of manufacturing capacity concentration for large and ultra-large mining tires among a small number of globally qualified producers, which creates periodic supply tightness conditions that can restrict mine operators from sourcing adequate tire volumes to maintain planned equipment availability targets during periods of elevated mining industry capital expenditure and equipment procurement. The manufacturing of ultra-large mining tires for the highest-payload haul truck platforms requires specialized and capital-intensive production facilities, precision vulcanization equipment, and highly skilled technical workforces that represent significant barriers to capacity expansion and limit the universe of qualified suppliers. Lead times for large mining tires from major manufacturers can extend to many months in high-demand periods, compelling mine operators to maintain substantial buffer inventory holdings and enter into long-term supply agreements with preferred suppliers to secure allocation certainty, effectively shifting procurement risk management from a transactional to a strategic relationship orientation. This supply concentration dynamic also limits the negotiating leverage of individual mine operators in pricing discussions with major tire suppliers during periods of market tightness, and the capital requirements and extended gestation period for new large tire manufacturing capacity mean that supply responses to demand upswings are inherently slow, perpetuating cyclical imbalances between supply availability and operational requirements across the mining investment cycle.

Haul Road Quality, Operational Discipline, and the Challenge of Managing Tire Performance in Adverse Mine Site Conditions

A persistent operational and commercial challenge in the mining tire market is the wide variability in haul road design standards, maintenance discipline, and operational compliance with load, speed, and inflation management protocols across different mining operations, which creates substantial dispersion in the tire service life and failure rates achieved by nominally identical tire products deployed in different mine site environments. Poorly designed or maintained haul roads characterized by sharp rock fall, inadequate drainage, excessive gradient, or insufficient turning radius impose disproportionate stress on tire sidewalls, tread compounds, and carcass structures that accelerates wear and increases the incidence of cut, impact, and heat-related failures, reducing achieved tyre hours to levels substantially below design targets and increasing the effective cost per tonne of tire-related expenditure for the affected operation. The relationship between haul road quality and tire performance is well established technically, but the capital and operational discipline required to maintain haul road standards to the specifications that maximize tire life is not uniformly applied across the global mining industry, particularly at smaller operations, in remote locations with constrained maintenance resources, or during periods of production pressure that prioritize throughput over infrastructure maintenance. Tire manufacturers invest significant technical support resources in haul road assessment and remediation advisory services as part of their mine site customer relationships, but the translation of recommendations into sustained operational improvements remains dependent on the management commitment and operational capacity of individual mine site teams, limiting the ability of tire suppliers to guarantee performance outcomes independently of customer behavior.

Volatility in Natural Rubber Prices and the Management of Raw Material Cost Exposure in a Cyclically Sensitive End Market

The global mining tire industry faces a compounding cost management challenge arising from the exposure of its primary raw material inputs, most notably natural rubber, synthetic elastomers, and specialty carbon black compounds, to price volatility driven by supply-side agricultural dynamics, global energy market cycles, and speculative financial market activity, combined with the cyclical purchasing behavior of mining industry customers who intensify cost reduction pressure on tire suppliers during commodity price downturns that reduce mining operator revenue and compress operating margins. Natural rubber represents a significant input cost for large mining tire production, and price movements in global natural rubber markets, driven by weather events in key producing regions, replanting cycle dynamics, and demand signals from the automotive and industrial tire industries, can meaningfully affect mining tire production economics across relatively short time horizons. Synthetic rubber and specialty compound costs are correlated with crude oil price cycles, adding a second layer of input cost volatility that tends to coincide with broader industrial commodity market conditions that also influence mining operator capital expenditure decisions. The combination of input cost volatility and the cyclically sensitive negotiating environment with major mining customers creates a challenging margin management dynamic for tire manufacturers, who must balance the need to maintain investment in product development and manufacturing capacity against the financial constraints imposed by periods of simultaneous raw material cost elevation and customer price resistance.

Market Segmentation

- Segmentation By Equipment Type

- Rigid Dump Trucks (Large and Ultra-Class)

- Articulated Dump Trucks

- Wheel Loaders

- Motor Graders

- Bulldozers and Dozers

- Scrapers

- Underground Load-Haul-Dump (LHD) Vehicles

- Underground Dump Trucks

- Drill Rigs and Rock Drills

- Mining Shovels and Excavators

- Ancillary and Support Equipment

- Others

- Segmentation By Tire Size

- Below 49 Inches

- 49 to 57 Inches

- 58 to 63 Inches

- Above 63 Inches (Ultra-Large)

- Segmentation By Tire Construction

- Radial Tires

- Bias-Ply Tires

- Others

- Segmentation By Mining Type

- Surface and Open-Pit Mining

- Underground Mining

- Quarrying and Aggregates

- Oil Sands and Mineral Sands Operations

- Others

- Segmentation By Commodity Mined

- Coal

- Iron Ore

- Copper

- Gold

- Bauxite and Aluminum

- Lithium

- Nickel and Cobalt

- Potash and Phosphate

- Rare Earth Elements

- Construction Aggregates and Limestone

- Others

- Segmentation By Tread Compound Technology

- Standard Cut and Chip Resistant Compound

- Heat-Resistant Compound

- Enhanced Traction Compound

- Low Rolling Resistance Compound

- Multi-Compound and Hybrid Formulation

- Others

- Segmentation By Sales Channel

- Original Equipment Manufacturer (OEM) Channel

- Replacement and Aftermarket Channel

- Authorized Dealer and Distributor Network

- Direct Mine Site Supply Agreement

- Others

- Segmentation By Service and Lifecycle Management

- New Tire Supply

- Retreading and Remanufacturing Services

- Tire Repair and Maintenance Services

- Tire Management and Fleet Monitoring Programs

- Tire Pressure and Temperature Monitoring Systems

- Others

- Segmentation By Autonomous and Digitally Managed Fleet Application

- Conventionally Operated Fleet Tires

- Autonomous Haulage System (AHS) Optimized Tires

- Others

- Segmentation By End User

- Large-Scale Integrated Mining Corporations

- Mid-Tier and Independent Mining Operators

- Contract Mining and Mining Services Companies

- Quarrying and Aggregates Producers

- State-Owned Mining Enterprises

- Others

- Segmentation By Region

- North America

- Latin America

- Europe

- Asia-Pacific

- Middle East and Africa

All market revenues are presented in USD

Historical Year: 2021–2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027–2036

Key Questions this Study Will Answer

- What is the projected global market valuation and volume for mining tires through 2036, segmented by equipment type, tire size, mining type, commodity mined, and region, and which product size categories and end-use mining segments are expected to generate the highest incremental revenue contribution across the forecast period?

- How is the structural expansion of critical and energy transition mineral mining activity, encompassing copper, lithium, nickel, cobalt, and rare earth element operations, expected to reshape regional demand distribution, average tire size mix, and original equipment versus replacement channel dynamics within the global mining tire market over the forecast horizon?

- To what extent is the ongoing migration toward ultra-class haul truck payloads and the introduction of autonomous haulage systems at major open-pit operations expected to alter the performance specification requirements, supply chain qualification standards, and service relationship frameworks demanded by leading mining operators from their tire suppliers?

- How are the total cost of ownership economics of retreading and tire lifecycle management programs expected to evolve across the forecast period, and what is the projected revenue contribution and growth trajectory of the retreading, casing management, and tire monitoring service segments relative to new tire supply revenues?

- Who are the leading mining tire manufacturers, specialty compound technology developers, retreading service providers, and mine site tire management solution operators currently defining the competitive landscape of the global mining tire market, and what are their respective technology investment priorities, geographic capacity expansion plans, and strategic partnership and direct supply agreement approaches through the forecast horizon?

- Product Definition

- Scope of the Study

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Industry Publications, Mining OEM Reports & Press Releases

- Government Mining & Safety Authority Data (MSHA, DGMS, ILO, etc.)

- Mining Tire Production, Trade & Replacement Market Statistics

- OEM Procurement & Mining Equipment Supply Chain Databases

- Primary Research Design & Execution

- In-depth Interviews with Mining Tire Manufacturers, Mining OEM Procurement Heads & Fleet Managers

- Surveys with Mining OEMs, Independent Tire Dealers & Mine Site Operators

- Expert Panel Validation

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Bottom-Up & Top-Down Reconciliation

- Mining Equipment Fleet & Haul Cycle Model for OEM & Replacement Demand

- Replacement Rate & Operating Hours-Driven Aftermarket Tire Market Sizing Model

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Technology & Innovation Highlights

- Manufacturing Economics & Unit Economics Summary

- Average Plant CAPEX & OPEX Benchmarks

- OEM vs Aftermarket Margin & Profitability Analysis

- Ultra-Large & Giant OTR Tire Revenue Model Summary

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Geographic & Regional Trends

- Risk Assessment Framework

- Geopolitical & Trade Policy Risk

- Raw Material Price Volatility (Natural Rubber, Synthetic Rubber, Carbon Black, Steel) Risk

- Environmental & Regulatory Risk

- Financial / Market Risk

- Commodity Price Cyclicality & Mining Investment Risk

- Autonomous & Electric Mining Vehicle Transition Risk

- Regulatory Framework & Policy Standards

- Global Mining Tire Market Economics

- Manufacturing Economics & Unit Economics Framework

- Capital Expenditure (CAPEX) Structure

- Operating Expenditure (OPEX) Structure

- Revenue Model & Monetisation Levers

- Capacity Utilisation & Throughput Economics

- Payback Period & Return on Investment (ROI) Analysis

- Total Cost of Production vs Alternative Tire & Non-Pneumatic Technologies

- Raw Material & Input Cost Analysis

- Natural Rubber & Synthetic Rubber Price Trends (USD/tonne, 2021–2035)

- Carbon Black & Silica Reinforcement Cost Dynamics

- Steel Cord & Bead Wire Cost Analysis

- Chemical Additives & Compounding Cost Structure

- Energy Cost Structure in Mining Tire Manufacturing

- Scrap Tire & Retread Material Recycling Value Chain Economics

- Impact of Ultra-Large & Giant OTR Tire Specifications on Product Economics

- Aftermarket & Replacement Tire Economics

- Replacement Cost Structure by Mine Type & Geography

- Operating Hours-Driven Replacement Rate & Demand Dynamics

- On-Site Tire Management Service & Tire Management Agreement (TMA) Economics

- Retread & Repair Economics for Mining Tires

- Warranty & Guarantee Economics in OEM vs Aftermarket Mining Tires

- Global Mining Tire Market Outlook

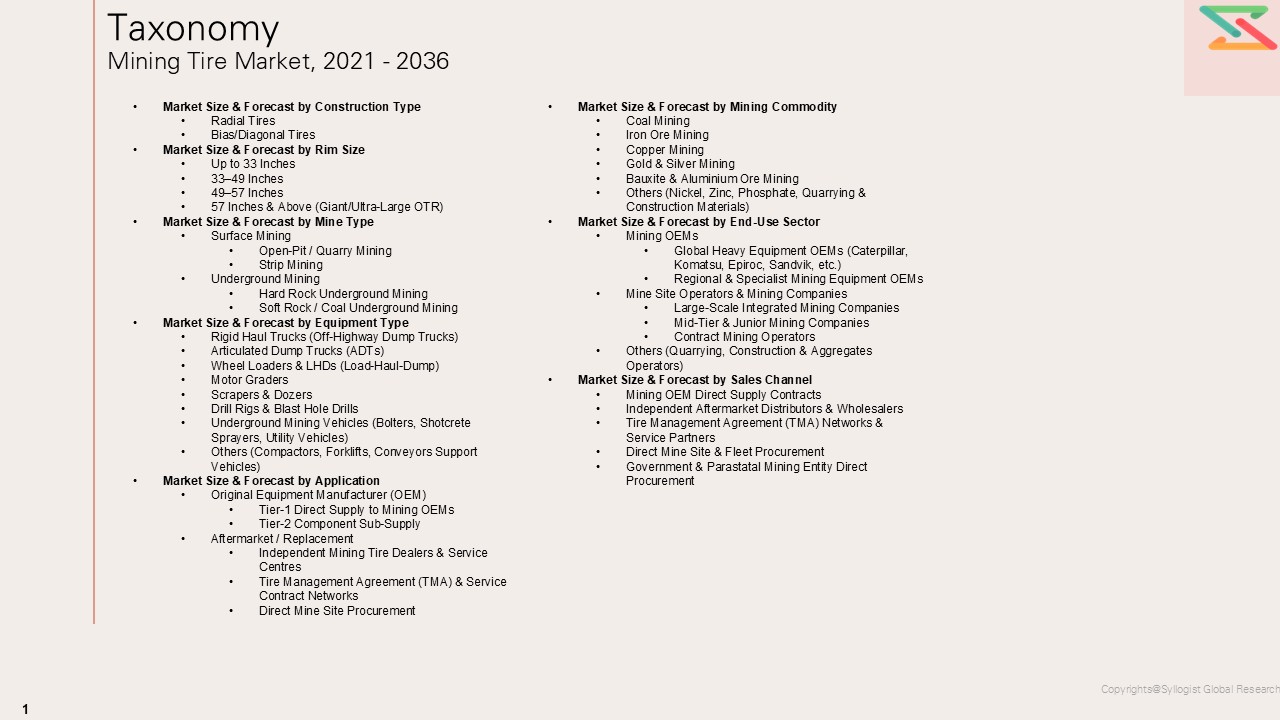

- Market Size & Forecast by Value (USD Billion, 2021–2036)

- Market Size & Forecast by Construction Type

- Radial Tires

- Bias/Diagonal Tires

- Market Size & Forecast by Rim Size

- Up to 33 Inches

- 33–49 Inches

- 49–57 Inches

- 57 Inches & Above (Giant/Ultra-Large OTR)

- Market Size & Forecast by Mine Type

- Surface Mining

- Open-Pit / Quarry Mining

- Strip Mining

- Underground Mining

- Hard Rock Underground Mining

- Soft Rock / Coal Underground Mining

- Market Size & Forecast by Equipment Type

- Rigid Haul Trucks (Off-Highway Dump Trucks)

- Articulated Dump Trucks (ADTs)

- Wheel Loaders & LHDs (Load-Haul-Dump)

- Motor Graders

- Scrapers & Dozers

- Drill Rigs & Blast Hole Drills

- Underground Mining Vehicles (Bolters, Shotcrete Sprayers, Utility Vehicles)

- Others (Compactors, Forklifts, Conveyors Support Vehicles)

- Market Size & Forecast by Application

- Original Equipment Manufacturer (OEM)

- Tier-1 Direct Supply to Mining OEMs

- Tier-2 Component Sub-Supply

- Aftermarket / Replacement

- Independent Mining Tire Dealers & Service Centres

- Tire Management Agreement (TMA) & Service Contract Networks

- Direct Mine Site Procurement

- Market Size & Forecast by Mining Commodity

- Coal Mining

- Iron Ore Mining

- Copper Mining

- Gold & Silver Mining

- Bauxite & Aluminium Ore Mining

- Others (Nickel, Zinc, Phosphate, Quarrying & Construction Materials)

- Market Size & Forecast by End-Use Sector

- Mining OEMs

- Global Heavy Equipment OEMs (Caterpillar, Komatsu, Epiroc, Sandvik, etc.)

- Regional & Specialist Mining Equipment OEMs

- Mine Site Operators & Mining Companies

- Large-Scale Integrated Mining Companies

- Mid-Tier & Junior Mining Companies

- Contract Mining Operators

- Others (Quarrying, Construction & Aggregates Operators)

- Mining OEMs

- Market Size & Forecast by Sales Channel

- Mining OEM Direct Supply Contracts

- Independent Aftermarket Distributors & Wholesalers

- Tire Management Agreement (TMA) Networks & Service Partners

- Direct Mine Site & Fleet Procurement

- Government & Parastatal Mining Entity Direct Procurement

- Asia-Pacific Mining Tire Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Construction Type

- By Rim Size

- By Mine Type

- By Equipment Type

- By Application

- By Mining Commodity

- By End-Use Sector

- By Sales Channel

- Key Demand Drivers (APAC-Specific)

- Competitive Landscape (APAC)

- Europe Mining Tire Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Construction Type

- By Rim Size

- By Mine Type

- By Equipment Type

- By Application

- By Mining Commodity

- By End-Use Sector

- By Sales Channel

- Key Demand Drivers (Europe-Specific)

- Competitive Landscape (Europe)

- North America Mining Tire Market Outlook

- Market Overview & Strategic Importance

- Market Size & Forecast

- By Value (2020–2035)

- By Construction Type

- By Rim Size

- By Mine Type

- By Equipment Type

- By Application

- By Mining Commodity

- By End-Use Sector

- By Sales Channel

- Key Demand Drivers (North America-Specific)

- Competitive Landscape (North America)

- Latin America Mining Tire Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Construction Type

- By Rim Size

- By Mine Type

- By Equipment Type

- By Application

- By Mining Commodity

- By End-Use Sector

- By Sales Channel

- Key Demand Drivers (LATAM-Specific)

- Competitive Landscape (Latin America)

- Middle East & Africa Mining Tire Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Construction Type

- By Rim Size

- By Mine Type

- By Equipment Type

- By Application

- By Mining Commodity

- By End-Use Sector

- By Sales Channel

- Key Demand Drivers (MEA-Specific)

- Competitive Landscape (MEA)

- Country-Wise Mining Tire Market Outlook

- Market Size & Forecast by Country

- By Value

- By Construction Type

- By Rim Size

- By Mine Type

- By Equipment Type

- By Application

- By Mining Commodity

- By End-Use Sector

- By Sales Channel

- Market Size & Forecast by Country

- Market Size & Forecast

- Market Size & Forecast

- Market Size & Forecast

- Market Size & Forecast

- Original Equipment Manufacturer (OEM)

- Surface Mining

- Manufacturing Economics & Unit Economics Framework

Countries Covered: Australia, China, India, Indonesia, South Africa, Russia, United States, Canada, Chile, Brazil, Peru, Mexico, Kazakhstan, Mongolia, Democratic Republic of Congo, Zambia, Ghana, Germany, United Kingdom, Saudi Arabia

- Technology Landscape & Innovation Analysis

- Mining Tire Technology Maturity Assessment

- Emerging & Disruptive Technologies in Mining Tires

- Digital Technologies in Manufacturing Operations & Quality Control

- Tire Pressure Monitoring Systems (TPMS) & Real-Time Fleet Monitoring Technologies

- Technology Readiness & Commercialisation Matrix – Key Mining Tire Technologies

- Patent Landscape Analysis

- R&D Investment Benchmarking

- Value Chain & Supply Chain Analysis

- Mining Tire Value Chain Mapping

- Supply Chain Concentration & Dependency Analysis

- Key Supplier Mapping by Product & Technology Programme

- Supplier Risk Heat Map

- Make vs Buy Strategy Trends Among Mining Tire Manufacturers

- Pricing Analysis

- Mining Tire Pricing Dynamics & Mechanisms

- Pricing by Construction Type, Rim Size & Equipment Type

- Total Cost of Ownership (TCO) Analysis – Including Tire Life, TKPH & Productivity Impact

- OEM vs Aftermarket Pricing Trends & Benchmarks

- Tire Management Agreement (TMA) vs. Outright Purchase Pricing Models

- Sustainability & Environmental Stewardship

- Environmental & Sustainability Landscape in Mining Tire Manufacturing

- Carbon Footprint Benchmarking Across Tire Production Technologies

- Recycled & Bio-Based Material Integration Roadmap for Mining Tire Manufacturers

- Mining Tire Recyclability & End-of-Life Tire (ELT) Circular Economy Assessment

- Retread & Retreading Technology as a Sustainability Pathway

- ESG Reporting & Lifecycle Assessment (LCA) in Mining Tire Operations

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level: Global Leaders vs Regional Players

- Top 5 Mining Tire Manufacturers Market Revenue Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis by Product & Application Segment

- Competitive Intensity Map by Segment & Region

- Player Classification

- Tier-1 Global Integrated Mining Tire Manufacturers

- Tier-2 Regional & Specialist Mining Tire Manufacturers

- Retread, Repair & Tire Management Service Network Players

- Emerging & Disruptive Players

- Competitive Analysis Frameworks

- Market Share Analysis by Product Type & Geography

- R&D Intensity Benchmarking

- OEM Customer Revenue & Long-Term Supply Contract Portfolio Comparison

- Geographic Revenue Exposure Comparison

- Company Profiles

- Company Overview, HQ & Organisational Structure

- Mining Tire Products & Services Portfolio

- Revenue Breakdown

- Key OEM Supply Programmes & Mine Site Fleet Deployments

- Manufacturing Footprint & Key Facilities

- Recent Developments (M&A, Partnerships, New Products, Financial Results)

- SWOT Analysis

- Strategic Focus: Giant OTR Innovation, Mine Site Fleet Wins, TMA Expansion

- Strategic Output

- Market Opportunity Matrix

- High-Value Opportunity Quadrant Analysis

- Addressable Market by Segment & Region

- Time-to-Revenue Assessment by Opportunity

- White Space Opportunity Analysis

- Underserved Equipment Type & Mine Type Gaps

- Geographic Markets with Low Penetration

- Technology Gaps with High Commercialisation Potential

- Customer Segment Unmet Needs

- Strategic Recommendations

- Product Portfolio & Innovation Strategy

- Technology & Digitalization Strategy

- Manufacturing Footprint & Capacity Expansion Strategy

- Aftermarket, Retread & TMA Channel Growth Strategy

- Pricing & Commercial Strategy

- Sustainability & Regulatory Compliance Strategy

- Supply Chain & Raw Material Sourcing Strategy

- Partnership, M&A & Expansion Strategy

- Regional Growth Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-Term (2025–2028)

- Mid-Term (2029–2032)

- Long-Term (2033–2036)

- Market Opportunity Matrix

- Market Structure & Concentration