Market Definition

The Global Construction Tire Market encompasses the design, manufacturing, distribution, and servicing of off-the-road tires specifically engineered for the diverse range of heavy equipment and vehicles deployed across building construction, civil engineering, road building, earthmoving, demolition, port handling, and industrial material movement applications worldwide. Construction tires are purpose-designed components that must deliver simultaneous performance across multiple demanding and often conflicting operational requirements, including resistance to puncture and sidewall damage from sharp construction debris such as rebar, broken concrete, and compacted aggregate, load-carrying capacity sufficient for the heaviest earthmoving and material handling equipment configurations, traction performance on loose, wet, and unstable ground surfaces, heat dissipation capability under sustained high-torque low-speed working cycles, and durability in abrasive environments that accelerate tread compound wear. The product scope of this market encompasses tires fitted to wheeled excavators, backhoe loaders, skid-steer loaders, compact track loaders, telehandlers and telescopic handlers, rough terrain and all-terrain forklifts, rigid and articulated site dumpers, motor graders, compactors and rollers, concrete mixer trucks, crane carriers, and the broad range of specialized construction support vehicles operating within active construction sites and civil infrastructure projects. The market further includes tires deployed on port and intermodal terminal handling equipment including reach stackers, empty container handlers, and rubber-tyred gantry cranes, which share construction tire performance characteristics and supply chain structures. The value chain of this market spans natural and synthetic rubber compound producers, fabric and steel reinforcement material suppliers, specialized tire manufacturing operations, authorized dealer and distribution networks, construction equipment rental companies, and tire repair and retreading service operations that support the lifecycle management requirements of high-value construction tire casings across the full spectrum of project types and operating environments.

Market Insights

The global construction tire market is experiencing a period of sustained and broadly based demand growth as of 2026, underpinned by the continued acceleration of infrastructure investment programs across both developed and emerging economies, the recovery and expansion of residential and commercial construction activity in key regional markets, and the progressive modernization of construction equipment fleets toward larger, more productive, and more technologically sophisticated platforms that generate elevated per-unit tire specification and value requirements. Infrastructure investment is functioning as the most durable demand anchor for construction tires globally, with government-led programs in road network expansion, rail and transit infrastructure, port development, energy infrastructure including wind farm foundations and solar park civil works, and water and sanitation systems collectively maintaining high levels of earthmoving, compaction, and material handling equipment utilization across multiple geographies simultaneously. The combination of strong original equipment demand from construction equipment manufacturers operating near-peak production rates and robust replacement tire demand from the large and continuously expanding global parc of in-service construction equipment is providing the market with a balanced and resilient revenue base that is less susceptible to single-source demand disruption than equipment categories with more concentrated end-use profiles.

A strategically significant trend reshaping product development priorities and commercial positioning within the construction tire market is the growing adoption of solid and foam-filled tire solutions as alternatives to pneumatic tires in specific construction applications characterized by particularly high puncture risk environments, including demolition sites, recycling facilities, waste handling operations, and construction zones with dense concentrations of sharp metallic or concrete debris. Solid and foam-filled tires eliminate the risk of sudden deflation events that compromise equipment stability, operator safety, and project schedule continuity, and while they involve higher initial acquisition costs relative to equivalent pneumatic products, the total cost of ownership economics in high-risk environments are often favorable owing to the elimination of puncture repair costs, unplanned downtime incidents, and the operational disruption associated with on-site tire changes. Leading tire manufacturers are responding to this demand trend by expanding their solid and foam-fill product ranges across a broader range of rim sizes and equipment categories, while simultaneously developing advanced pneumatic constructions with reinforced puncture protection features that offer improved resistance for applications where the ride quality and traction advantages of pneumatic tires remain operationally important.

The construction equipment rental sector constitutes a structurally important and commercially distinct customer segment within the construction tire market, with implications for product specification preferences, replacement cycle frequency, distribution channel requirements, and service relationship structures that differ meaningfully from those of equipment owner-operators and construction contractors maintaining their own fleet assets. Rental fleet operators managing large and geographically dispersed equipment inventories across multiple simultaneous project deployments apply rigorous total cost of ownership criteria to tire procurement decisions, prioritizing products that deliver consistent and predictable service life across diverse site conditions, low maintenance intervention requirements, and high casing integrity for retreading at end of first service life. The expansion of the construction equipment rental market globally, driven by the capital efficiency benefits of rental for project-based construction operations and the increasing adoption of rental as a fleet strategy by contractors seeking to reduce balance sheet exposure to equipment ownership costs, is progressively increasing the share of total construction tire procurement flowing through rental channel relationships and aligning purchasing decision-making with professional fleet economics rather than individual site operator preferences.

From a regional standpoint, Asia-Pacific constitutes the largest and most volume-intensive market for construction tires globally, with China, India, Southeast Asia, and Australia collectively representing the dominant share of equipment fleet size, new equipment deployment activity, and replacement tire demand. China remains central to global construction tire market dynamics both as the world’s largest construction equipment production and deployment market and as the home base of a rapidly expanding domestic tire manufacturing industry that is exerting increasing competitive influence on product pricing and distribution channel structures across regional and global markets. India is emerging as one of the most consequential growth markets for construction tires over the forecast period, driven by the government’s sustained commitment to national highway expansion, urban infrastructure development, affordable housing programs, and port and logistics infrastructure investment that are collectively maintaining elevated construction equipment utilization rates. Europe and North America represent mature but high-value markets characterized by premium product specifications, established service channel infrastructure, strong demand for technologically advanced tire products, and well-developed retreading ecosystems that reflect the cost management discipline of professional construction fleet operators in these geographies. The Middle East is sustaining strong construction tire demand through ongoing large-scale civil and real estate development programs, while Sub-Saharan Africa and Latin America represent developing but structurally growing markets driven by infrastructure investment programs and expanding construction activity tied to urbanization and commodity sector development.

Key Drivers

Sustained Global Infrastructure Investment and the Accelerating Execution of Civil Engineering Programs Across Major Economies

The most powerful and enduring demand driver for the global construction tire market is the sustained and, in many jurisdictions, accelerating commitment of governments and multilateral development institutions to infrastructure investment programs that are generating continuous demand for earthmoving, compaction, lifting, and material handling equipment across road construction, bridge and tunnel projects, urban transit systems, port expansion, renewable energy infrastructure, and industrial facility development. The global infrastructure investment cycle entered a new phase of intensity in the post-2020 period as governments across North America, Europe, and Asia deployed fiscal stimulus programs with strong infrastructure components, and the execution of these committed programs is translating into multi-year equipment deployment visibility that underpins durable replacement tire demand across the construction sector. The energy transition is independently contributing a new and growing category of infrastructure investment, including wind farm civil works requiring substantial earthmoving equipment hours, solar park ground preparation and cable laying operations, electric vehicle charging infrastructure installation, and grid expansion projects, all of which generate construction equipment utilization and consequent tire wear that adds incremental demand to the established infrastructure construction base. Emerging market urbanization dynamics are additionally sustaining high construction activity levels in the world’s most populous developing economies, where urban population growth is driving continuous demand for residential construction, urban road networks, water and sanitation infrastructure, and commercial and industrial facilities that collectively represent a large and growing source of construction equipment deployment and tire replacement demand.

Construction Equipment Fleet Modernization and the Adoption of Higher-Productivity Machine Configurations

A commercially significant driver reshaping the product mix and average unit value trajectory of the construction tire market is the progressive modernization of construction equipment fleets by contractors, rental companies, and public works operators toward larger payload capacities, higher productivity configurations, and more technologically advanced machine specifications that generate corresponding increases in tire size, load rating requirements, and average selling price per unit. The economic imperative to maximize output per machine hour and reduce operating cost per cubic metre of material moved is driving construction fleet operators to specify larger wheel loaders, higher-capacity articulated dumpers, and more powerful backhoe and wheeled excavator configurations that require tires at the upper end of the construction tire size range and command premium pricing reflective of their engineering complexity and performance requirements. The growing penetration of telematics and machine productivity monitoring systems on modern construction equipment is providing fleet managers with granular data on equipment utilization, idle time, fuel consumption, and component wear patterns that is being applied to tire management decision-making, driving demand for premium tire products whose performance credentials can be validated against measured productivity outcomes. This fleet modernization trend is expected to sustain an upward trajectory in average construction tire revenue per unit that amplifies the commercial impact of volume growth and provides tire manufacturers with a favorable product mix dynamic over the forecast period.

Growth of Emerging Market Construction Activity and the Expansion of Organized Equipment and Tire Distribution Infrastructure

The accelerating pace of construction activity across emerging economies in South and Southeast Asia, Sub-Saharan Africa, the Middle East, and Latin America is constituting a growth driver of increasing structural importance for the global construction tire market, as the combination of expanding equipment fleet sizes and the progressive formalization of tire distribution and service channel infrastructure in these geographies creates a growing and increasingly commercially accessible replacement market alongside the original equipment demand generated by new machine deployments. In markets where construction activity has historically been served by informal and fragmented tire supply chains, the entry of organized dealer networks, rental company procurement programs, and construction equipment manufacturer authorized service channels is improving product availability, elevating average product specification toward performance-differentiated offerings, and reducing the market share of substandard or counterfeit products that had previously captured disproportionate volume in price-sensitive segments. The expansion of construction activity in these markets is additionally generating demand for tire products engineered for specific regional operating conditions, including tropical climate heat resistance, performance on laterite and clay soil surfaces, and durability under the maintenance and inflation management standards achievable in field conditions with limited technical support infrastructure, creating product development and localization opportunities for manufacturers with the engineering resources and regional market commitment to address these requirements.

Key Challenges

Intense Price Competition and the Persistent Presence of Low-Cost Products in Emerging and Price-Sensitive Market Segments

A structural competitive challenge confronting established tire manufacturers in the global construction tire market is the sustained and intensifying price competition from low-cost manufacturers, particularly those operating from Asia-Pacific production bases with lower labor and overhead cost structures, whose products have achieved significant market penetration across the emerging market replacement segment and are increasingly present in the tender processes of cost-sensitive public infrastructure procurement programs in both developing and developed markets. The price differential between premium branded construction tires and lower-cost alternatives can be substantial in certain size categories, creating a purchase decision environment in which procurement managers and site operators under budget pressure may prioritize initial acquisition cost over total cost of ownership considerations, particularly on projects with short durations where the full lifecycle performance advantage of premium products is not fully realized within the contract period. The proliferation of trading platforms and digital procurement channels has further increased price transparency and competitive pressure in the replacement market, enabling buyers to access the broadest range of tire options at market-clearing prices and reducing the ability of established manufacturers to sustain price premiums without clear and quantified performance differentiation. Addressing this challenge requires sustained investment in product performance documentation, total cost of ownership demonstration programs, and distribution channel relationships that reinforce the value proposition of premium construction tires across the diverse purchasing environments that characterize the global market.

Raw Material Cost Volatility and the Complexity of Managing Input Cost Exposure Across the Construction Tire Manufacturing Value Chain

The global construction tire manufacturing industry is structurally exposed to significant volatility in the prices of its principal input materials, including natural rubber, synthetic rubber compounds, carbon black, steel cord, and specialized fabric reinforcements, each of which is subject to distinct supply and demand dynamics that can produce material cost movements across time horizons that are difficult to manage within the pricing structures and contract frameworks that govern commercial relationships with construction equipment manufacturers and large fleet customers. Natural rubber supply is concentrated in a limited number of Southeast Asian and West African producing regions and is susceptible to disruption from weather events, disease pressures, and labor market dynamics in ways that can generate sudden and sustained price increases that compress manufacturer margins when pass-through to customers is constrained by competitive conditions or contractual price adjustment mechanisms. Synthetic rubber and carbon black costs are correlated with petrochemical feedstock markets and move with crude oil and natural gas price cycles, adding a second dimension of input cost volatility that can reinforce or counteract natural rubber price movements. The management of aggregate raw material cost exposure through procurement hedging strategies, compound formulation flexibility programs, and supply chain diversification initiatives represents a significant and ongoing operational complexity for tire manufacturers, and the ability to respond to sustained input cost increases with product pricing adjustments without losing competitive position in price-sensitive market segments remains one of the most challenging aspects of financial management within the construction tire industry.

Operational Demands of Construction Site Conditions and the Challenge of Delivering Consistent Tire Performance Across Diverse Applications

A distinctive technical and commercial challenge in the construction tire market is the exceptional diversity of operating conditions, equipment configurations, and site-specific hazard profiles across which construction tires are required to deliver reliable and consistent performance, creating product development complexity that makes it difficult to engineer a single tire solution that performs optimally across the full spectrum of construction applications without requiring a broad and operationally complex product portfolio. Construction site conditions range from soft and waterlogged ground at foundation excavation stages to hardened compacted surfaces at later project phases, from mild temperatures in temperate climate markets to extreme heat in Middle Eastern and tropical construction environments, and from relatively clean earthmoving operations to heavily contaminated demolition and recycling sites where tire damage risk is at its highest. Each distinct operating environment imposes different performance priorities in terms of traction, flotation, cut resistance, heat dissipation, and sidewall protection, requiring tire manufacturers to develop and maintain differentiated product lines across multiple tread pattern designs, compound formulations, and construction architectures to serve the full range of customer requirements. Communicating the performance differentiation between these products and guiding procurement managers and equipment operators toward the correct tire specification for their specific application and site conditions demands significant investment in technical sales capability, application engineering support, and dealer training programs, representing an ongoing operational cost and capability investment requirement that constrains the efficiency of the go-to-market model relative to less technically complex tire market segments.

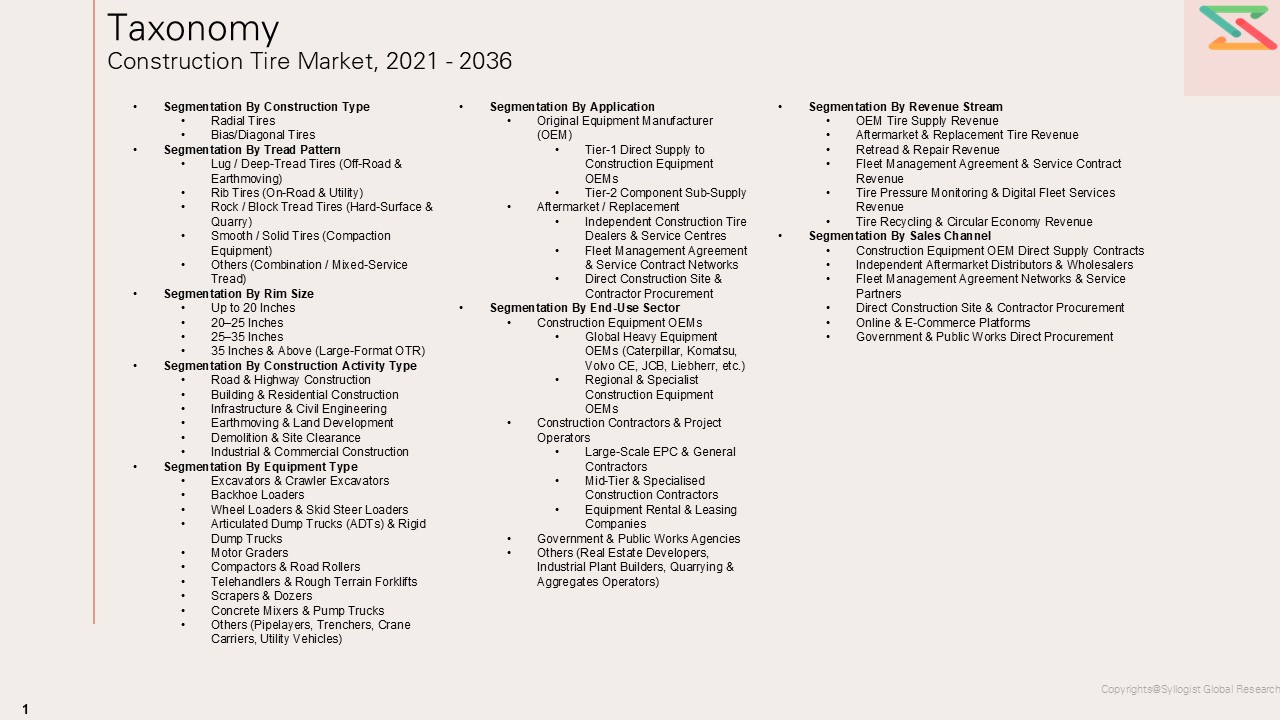

Market Segmentation

- Segmentation By Equipment Type

- Wheeled Excavators

- Backhoe Loaders

- Skid-Steer Loaders

- Compact Track Loaders

- Wheel Loaders

- Telehandlers and Telescopic Handlers

- Articulated and Rigid Site Dumpers

- Motor Graders

- Compactors and Rollers

- Rough Terrain and All-Terrain Forklifts

- Crane Carriers

- Concrete Mixer Trucks

- Port and Terminal Handling Equipment

- Others

- Segmentation By Tire Type

- Pneumatic Tires

- Solid Tires

- Foam-Filled Tires

- Cushion Tires

- Others

- Segmentation By Tire Construction

- Radial Tires

- Bias-Ply Tires

- Others

- Segmentation By Rim Size

- Below 20 Inches

- 20 to 25 Inches

- 25 to 35 Inches

- Above 35 Inches

- Segmentation By Tread Pattern

- Block Tread

- Lug Tread

- Rib Tread

- Rock Tread

- Combination and Multi-Purpose Tread

- Smooth and Semi-Smooth Tread

- Others

- Segmentation By Compound Technology

- Cut and Puncture Resistant Compound

- Abrasion Resistant Compound

- Heat Resistant Compound

- Low Rolling Resistance Compound

- Multi-Compound and Dual-Compound Formulation

- Others

- Segmentation By Application and Construction Activity Type

- General Building Construction

- Road and Highway Construction

- Civil and Infrastructure Engineering

- Demolition and Site Clearance

- Quarrying and Aggregates Handling

- Port and Intermodal Terminal Operations

- Industrial and Warehouse Facility Construction

- Renewable Energy Infrastructure Construction

- Others

- Segmentation By Sales Channel

- Original Equipment Manufacturer (OEM) Channel

- Replacement and Aftermarket Channel

- Authorized Dealer and Distributor Network

- Construction Equipment Rental Company Direct Supply

- Online and Digital Procurement Channel

- Others

- Segmentation By Service and Lifecycle Management

- New Tire Supply

- Retreading and Casing Remanufacturing

- On-Site Repair and Maintenance Services

- Foam-Filling and Solid Conversion Services

- Tire Pressure Monitoring and Fleet Management Programs

- Others

- Segmentation By End User

- General Contractors and Civil Engineering Companies

- Construction Equipment Rental Operators

- Public Works and Government Infrastructure Agencies

- Specialty Contractors and Demolition Companies

- Port and Terminal Operators

- Industrial and Logistics Park Developers

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021–2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027–2036

Key Questions this Study Will Answer

- What is the projected global market valuation and volume for construction tires through 2036, segmented by equipment type, tire type, rim size, application, and region, and which product categories and end-use construction segments are expected to generate the highest incremental revenue growth across the forecast period?

- How are the evolving dynamics of global infrastructure investment, including the renewable energy construction wave, urban transit and road network expansion programs, and port and logistics infrastructure development, expected to influence regional demand distribution, equipment fleet composition, and average tire specification requirements within the construction tire market over the forecast horizon?

- What are the projected growth trajectories and total cost of ownership economics of solid and foam-filled tire segments relative to pneumatic construction tires, and which equipment categories and application environments are expected to exhibit the most significant shift toward non-pneumatic tire solutions as operators seek to eliminate puncture-related downtime and maintenance costs on high-risk construction sites?

- How is the growing market share of construction equipment rental operators as a tire procurement channel expected to reshape product specification priorities, distribution channel structures, and service relationship frameworks within the construction tire industry, and what are the implications for tire manufacturers seeking to establish and sustain preferred supplier relationships with leading rental fleet operators?

- Who are the leading construction tire manufacturers, compound technology developers, retreading service providers, and fleet management solution operators currently defining the competitive landscape of the global construction tire market, and what are their respective technology investment priorities, regional distribution expansion strategies, and product portfolio development trajectories through the forecast horizon?

- Product Definition

- Scope of the Study

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Industry Publications, Construction Equipment OEM Reports & Press Releases

- Government Construction & Safety Authority Data (OSHA, BIS, ISO, Regional Infrastructure Authorities, etc.)

- Construction Tire Production, Trade & Replacement Market Statistics

- OEM Procurement & Construction Equipment Supply Chain Databases

- Primary Research Design & Execution

- In-depth Interviews with Construction Tire Manufacturers, OEM Procurement Heads & Fleet Managers

- Surveys with Construction Equipment OEMs, Independent Tire Dealers & Construction Site Operators

- Expert Panel Validation

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Bottom-Up & Top-Down Reconciliation

- Construction Equipment Fleet & Project Activity Model for OEM & Replacement Demand

- Replacement Rate & Operating Hours-Driven Aftermarket Tire Market Sizing Model

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Technology & Innovation Highlights

- Manufacturing Economics & Unit Economics Summary

- Average Plant CAPEX & OPEX Benchmarks

- OEM vs Aftermarket Margin & Profitability Analysis

- Performance OTR & Specialty Construction Tire Revenue Model Summary

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Geographic & Regional Trends

- Risk Assessment Framework

- Geopolitical & Trade Policy Risk

- Raw Material Price Volatility (Natural Rubber, Synthetic Rubber, Carbon Black, Steel) Risk

- Environmental & Regulatory Risk

- Financial / Market Risk

- Construction Spending Cyclicality & Infrastructure Project Pipeline Risk

- Electric & Autonomous Construction Equipment Transition Risk

- Regulatory Framework & Policy Standards

- Global Construction Tire Market Economics

- Manufacturing Economics & Unit Economics Framework

- Capital Expenditure (CAPEX) Structure

- Operating Expenditure (OPEX) Structure

- Revenue Model & Monetisation Levers

- Capacity Utilisation & Throughput Economics

- Payback Period & Return on Investment (ROI) Analysis

- Total Cost of Production vs Alternative Tire & Non-Pneumatic Technologies

- Raw Material & Input Cost Analysis

- Natural Rubber & Synthetic Rubber Price Trends (USD/tonne, 2021–2035)

- Carbon Black & Silica Reinforcement Cost Dynamics

- Steel Cord & Bead Wire Cost Analysis

- Chemical Additives & Compounding Cost Structure

- Energy Cost Structure in Construction Tire Manufacturing

- Scrap Tire & Retread Material Recycling Value Chain Economics

- Impact of Large-Format & Specialty Construction Tire Specifications on Product Economics

- Aftermarket & Replacement Tire Economics

- Replacement Cost Structure by Construction Activity Type & Geography

- Operating Hours-Driven Replacement Rate & Demand Dynamics

- On-Site Tire Management Service & Fleet Management Agreement Economics

- Retread & Repair Economics for Construction Tires

- Warranty & Guarantee Economics in OEM vs Aftermarket Construction Tires

- Global Construction Tire Market Outlook

- Market Size & Forecast by Value (USD Billion, 2021–2036)

- Market Size & Forecast by Construction Type

- Radial Tires

- Bias/Diagonal Tires

- Market Size & Forecast by Tread Pattern

- Lug / Deep-Tread Tires (Off-Road & Earthmoving)

- Rib Tires (On-Road & Utility)

- Rock / Block Tread Tires (Hard-Surface & Quarry)

- Smooth / Solid Tires (Compaction Equipment)

- Others (Combination / Mixed-Service Tread)

- Market Size & Forecast by Rim Size

- Up to 20 Inches

- 20–25 Inches

- 25–35 Inches

- 35 Inches & Above (Large-Format OTR)

- Market Size & Forecast by Construction Activity Type

- Road & Highway Construction

- Building & Residential Construction

- Infrastructure & Civil Engineering

- Earthmoving & Land Development

- Demolition & Site Clearance

- Industrial & Commercial Construction

- Market Size & Forecast by Equipment Type

- Excavators & Crawler Excavators

- Backhoe Loaders

- Wheel Loaders & Skid Steer Loaders

- Articulated Dump Trucks (ADTs) & Rigid Dump Trucks

- Motor Graders

- Compactors & Road Rollers

- Telehandlers & Rough Terrain Forklifts

- Scrapers & Dozers

- Concrete Mixers & Pump Trucks

- Others (Pipelayers, Trenchers, Crane Carriers, Utility Vehicles)

- Market Size & Forecast by Application

- Original Equipment Manufacturer (OEM)

- Tier-1 Direct Supply to Construction Equipment OEMs

- Tier-2 Component Sub-Supply

- Aftermarket / Replacement

- Independent Construction Tire Dealers & Service Centres

- Fleet Management Agreement & Service Contract Networks

- Direct Construction Site & Contractor Procurement

- Market Size & Forecast by End-Use Sector

- Construction Equipment OEMs

- Global Heavy Equipment OEMs (Caterpillar, Komatsu, Volvo CE, JCB, Liebherr, etc.)

- Regional & Specialist Construction Equipment OEMs

- Construction Contractors & Project Operators

- Large-Scale EPC & General Contractors

- Mid-Tier & Specialised Construction Contractors

- Equipment Rental & Leasing Companies

- Government & Public Works Agencies

- Others (Real Estate Developers, Industrial Plant Builders, Quarrying & Aggregates Operators)

- Construction Equipment OEMs

- Market Size & Forecast by Revenue Stream

- OEM Tire Supply Revenue

- Aftermarket & Replacement Tire Revenue

- Retread & Repair Revenue

- Fleet Management Agreement & Service Contract Revenue

- Tire Pressure Monitoring & Digital Fleet Services Revenue

- Tire Recycling & Circular Economy Revenue

- Market Size & Forecast by Sales Channel

- Construction Equipment OEM Direct Supply Contracts

- Independent Aftermarket Distributors & Wholesalers

- Fleet Management Agreement Networks & Service Partners

- Direct Construction Site & Contractor Procurement

- Online & E-Commerce Platforms

- Government & Public Works Direct Procurement

- Asia-Pacific Construction Tire Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Construction Type

- By Tread Pattern

- By Rim Size

- By Construction Activity Type

- By Equipment Type

- By Application

- By End-Use Sector

- By Revenue Stream

- By Sales Channel

- Key Demand Drivers (APAC-Specific)

- Competitive Landscape (APAC)

- Europe Construction Tire Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Construction Type

- By Tread Pattern

- By Rim Size

- By Construction Activity Type

- By Equipment Type

- By Application

- By End-Use Sector

- By Revenue Stream

- By Sales Channel

- Key Demand Drivers (Europe-Specific)

- Competitive Landscape (Europe)

- North America Construction Tire Market Outlook

- Market Overview & Strategic Importance

- Market Size & Forecast

- By Value (2020–2035)

- By Construction Type

- By Tread Pattern

- By Rim Size

- By Construction Activity Type

- By Equipment Type

- By Application

- By End-Use Sector

- By Revenue Stream

- By Sales Channel

- Key Demand Drivers (North America-Specific)

- Competitive Landscape (North America)

- Latin America Construction Tire Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Construction Type

- By Tread Pattern

- By Rim Size

- By Construction Activity Type

- By Equipment Type

- By Application

- By End-Use Sector

- By Revenue Stream

- By Sales Channel

- Key Demand Drivers (LATAM-Specific)

- Competitive Landscape (Latin America)

- Middle East & Africa Construction Tire Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Construction Type

- By Tread Pattern

- By Rim Size

- By Construction Activity Type

- By Equipment Type

- By Application

- By End-Use Sector

- By Revenue Stream

- By Sales Channel

- Key Demand Drivers (MEA-Specific)

- Competitive Landscape (MEA)

- Country-Wise Construction Tire Market Outlook

- Market Size & Forecast by Country

- By Value

- By Construction Type

- By Tread Pattern

- By Rim Size

- By Construction Activity Type

- By Equipment Type

- By Application

- By End-Use Sector

- By Revenue Stream

- By Sales Channel

- Market Size & Forecast by Country

- Market Size & Forecast

- Market Size & Forecast

- Market Size & Forecast

- Market Size & Forecast

- Original Equipment Manufacturer (OEM)

- Manufacturing Economics & Unit Economics Framework

Countries Covered: United States, Canada, Germany, United Kingdom, France, Italy, Spain, China, India, Japan, South Korea, Australia, Indonesia, Brazil, Mexico, Saudi Arabia, United Arab Emirates, Turkey, Russia, South Africa

- Technology Landscape & Innovation Analysis

- Construction Tire Technology Maturity Assessment

- Emerging & Disruptive Technologies in Construction Tires

- Digital Technologies in Manufacturing Operations & Quality Control

- Tire Pressure Monitoring Systems (TPMS) & Real-Time Fleet Monitoring Technologies

- Technology Readiness & Commercialisation Matrix – Key Construction Tire Technologies

- Patent Landscape Analysis

- R&D Investment Benchmarking

- Value Chain & Supply Chain Analysis

- Construction Tire Value Chain Mapping

- Supply Chain Concentration & Dependency Analysis

- Key Supplier Mapping by Product & Technology Programme

- Supplier Risk Heat Map

- Make vs Buy Strategy Trends Among Construction Tire Manufacturers

- Pricing Analysis

- Construction Tire Pricing Dynamics & Mechanisms

- Pricing by Construction Type, Tread Pattern, Rim Size & Equipment Type

- Total Cost of Ownership (TCO) Analysis – Including Tire Life, Traction Performance & Productivity Impact

- OEM vs Aftermarket Pricing Trends & Benchmarks

- Fleet Management Agreement vs. Outright Purchase Pricing Models

- Sustainability & Environmental Stewardship

- Environmental & Sustainability Landscape in Construction Tire Manufacturing

- Carbon Footprint Benchmarking Across Tire Production Technologies

- Recycled & Bio-Based Material Integration Roadmap for Construction Tire Manufacturers

- Construction Tire Recyclability & End-of-Life Tire (ELT) Circular Economy Assessment

- Retread & Retreading Technology as a Sustainability Pathway

- ESG Reporting & Lifecycle Assessment (LCA) in Construction Tire Operations

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level: Global Leaders vs Regional Players

- Top 5 Construction Tire Manufacturers Market Revenue Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis by Product & Application Segment

- Competitive Intensity Map by Segment & Region

- Player Classification

- Tier-1 Global Integrated Construction Tire Manufacturers

- Tier-2 Regional & Specialist Construction Tire Manufacturers

- Retread, Repair & Fleet Management Service Network Players

- Emerging & Disruptive Players

- Competitive Analysis Frameworks

- Market Share Analysis by Product Type & Geography

- R&D Intensity Benchmarking

- OEM Customer Revenue & Long-Term Supply Contract Portfolio Comparison

- Geographic Revenue Exposure Comparison

- Company Profiles

- Company Overview, HQ & Organisational Structure

- Construction Tire Products & Services Portfolio

- Revenue Breakdown

- Key OEM Supply Programmes & Construction Fleet Deployments

- Manufacturing Footprint & Key Facilities

- Recent Developments (M&A, Partnerships, New Products, Financial Results)

- SWOT Analysis

- Strategic Focus: OTR & Specialty Tire Innovation, OEM Platform Wins, Aftermarket Expansion

- Strategic Output

- Market Opportunity Matrix

- High-Value Opportunity Quadrant Analysis

- Addressable Market by Segment & Region

- Time-to-Revenue Assessment by Opportunity

- White Space Opportunity Analysis

- Underserved Equipment Type & Construction Activity Type Gaps

- Geographic Markets with Low Penetration

- Technology Gaps with High Commercialisation Potential

- Customer Segment Unmet Needs

- Strategic Recommendations

- Product Portfolio & Innovation Strategy

- Technology & Digitalization Strategy

- Manufacturing Footprint & Capacity Expansion Strategy

- Aftermarket, Retread & Fleet Management Channel Growth Strategy

- Pricing & Commercial Strategy

- Sustainability & Regulatory Compliance Strategy

- Supply Chain & Raw Material Sourcing Strategy

- Partnership, M&A & Expansion Strategy

- Regional Growth Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-Term (2025–2028)

- Mid-Term (2029–2032)

- Long-Term (2033–2036)

- Market Opportunity Matrix

- Market Structure & Concentration