Market Definition

The Global Scrap Metal Recycling Market encompasses the integrated industrial and commercial ecosystem responsible for the collection, sorting, processing, trading, and remelting of ferrous and non-ferrous metallic waste materials generated across post-consumer, post-industrial, and end-of-life product streams, and the conversion of these materials into secondary metal feedstocks that substitute for virgin primary metal inputs across the full range of metal-consuming manufacturing and construction industries worldwide. Scrap metal recycling constitutes a foundational pillar of the global circular economy, enabling the recovery of finite and energy-intensive metallic resources at a fraction of the energy cost required for primary metal production from ore, and delivering measurable reductions in greenhouse gas emissions, water consumption, mining waste generation, and landfill burden relative to linear production systems reliant on continuous primary ore extraction. The ferrous scrap segment encompasses iron and steel scrap derived from end-of-life vehicles, demolition steel, obsolete industrial machinery, discarded consumer appliances, manufacturing offcuts, and prompt industrial scrap generated in steel fabrication and forming operations, all of which serve as essential raw material inputs for electric arc furnace steelmaking and basic oxygen furnace charge blending at integrated steel mills globally. The non-ferrous scrap segment encompasses the recovery and reprocessing of aluminum, copper, stainless steel, lead, zinc, nickel, titanium, and a broad range of specialty and precious metals sourced from post-consumer electronics, automotive components, electrical wiring and cable, plumbing and HVAC systems, aerospace structures, and industrial process equipment. The value chain of this market extends from informal and organized scrap collection networks, municipal recycling programs, and industrial scrap generation points through scrap dealers, brokers, and aggregators; shredding, shearing, baling, and separation processing facilities; metal refining and upgrading operations; commodity trading platforms and exchange mechanisms; and the steel mills, secondary smelters, foundries, and specialty metal producers that constitute the ultimate consumers of processed scrap metal inputs. The market is defined by the interaction of commodity metal price cycles, industrial production activity levels, end-of-life product generation rates, trade policy and scrap export regulations, energy cost dynamics, and the expanding influence of decarbonization imperatives that are progressively elevating the strategic and commercial value assigned to recycled secondary metal feedstocks across the global metals industry.

Market Insights

The global scrap metal recycling market is navigating a period of structural evolution in 2026, shaped by the convergence of industrial decarbonization imperatives, the progressive modernization of scrap processing technology, the realignment of global scrap trade flows following successive rounds of import policy revisions in major consuming economies, and the strengthening commercial recognition of recycled metal feedstocks as a strategically valuable and low-carbon alternative to primary metal production inputs. The market is operating with strong underlying demand fundamentals anchored in the accelerating adoption of electric arc furnace steelmaking technology by steel producers seeking to reduce carbon intensity, lower energy costs relative to integrated blast furnace routes, and increase operational flexibility in response to volatile iron ore and coking coal price environments. Electric arc furnace steelmaking is inherently dependent on high-quality scrap metal as its primary input, and the sustained global investment in new electric arc furnace capacity across North America, Europe, and emerging steel markets in Asia and the Middle East is generating structural and growing demand for ferrous scrap that is creating a favorable commercial environment for the organized collection, processing, and trading segments of the recycling value chain.

A defining structural trend reshaping the operational and commercial landscape of the scrap metal recycling industry is the accelerating deployment of advanced shredding, sensor-based sorting, and automated material separation technologies that are fundamentally improving the purity, consistency, and alloy specificity of processed scrap outputs, enabling recycling operators to supply metal consumers with materials that meet increasingly exacting feedstock specifications and to extract value from complex and contaminated waste streams that were previously processed at lower grades or directed to landfill. The deployment of eddy current separators, optical and X-ray fluorescence sorting systems, dense media separation, and artificial intelligence-assisted material classification platforms is enabling the differentiation of mixed scrap streams into alloy-specific and grade-separated fractions whose market value substantially exceeds that of undifferentiated mixed scrap, creating strong economic incentives for investment in technology-upgraded processing capacity. This technological modernization of the scrap processing sector is additionally enabling the recovery of valuable non-ferrous metals from shredder residue and composite material streams that contain significant metallic content, improving the overall resource recovery efficiency of the recycling system and generating incremental revenue from material fractions that were historically treated as residual waste. Processing operators investing in advanced sorting capabilities are establishing durable competitive advantages in their ability to serve the most quality-sensitive and highest-value metal consumer segments, including specialty steel producers, automotive aluminum recyclers, and copper wire rod manufacturers, whose feedstock specifications are too demanding for conventionally processed scrap.

The intersection of the global energy transition and the scrap metal recycling market is creating a set of demand dynamics that are simultaneously generating new scrap supply streams from the decommissioning of fossil fuel infrastructure and creating incremental demand for recycled metal inputs in the manufacturing of clean energy equipment and electric vehicle platforms. The decommissioning of aging coal-fired power generation assets, oil and gas infrastructure, and industrial heating systems is releasing large tonnages of ferrous and non-ferrous metal scrap with known composition and in many cases high intrinsic metal value, representing a structurally growing supply category for scrap processors with the logistics and processing capabilities to access these decommissioning flows. Simultaneously, the manufacturing of wind turbines, solar panels, battery storage systems, electric vehicle drivetrains, and grid transmission infrastructure is consuming large and growing volumes of steel, aluminum, copper, and specialty metals, driving incremental demand for recycled feedstocks as clean energy manufacturers seek to reduce the embodied carbon of their products and satisfy supply chain sustainability requirements imposed by green procurement standards and project financing conditions. The alignment between the energy transition-driven generation of end-of-life metal scrap and the energy transition-driven demand for low-carbon recycled metal inputs is creating a circular material flow dynamic that is expected to strengthen over the forecast period as both decommissioning activity and clean energy manufacturing scale accelerate.

From a regional perspective, Asia-Pacific dominates global scrap metal consumption by volume, with China, Japan, South Korea, and India collectively representing the largest markets for ferrous and non-ferrous scrap processing and utilization, driven by the concentration of global steel and non-ferrous metal production capacity in the region and the scale of manufacturing industrial activity that generates both post-industrial scrap supply and metal product demand. China’s domestic scrap collection and recycling infrastructure has expanded significantly following the restriction of imported scrap, creating a growing internal recycling sector that is progressively reducing the economy’s reliance on primary ore-based metal production and reshaping global scrap trade flows as Chinese volumes that were previously exported are absorbed domestically. Europe represents the most advanced market in terms of recycling regulatory frameworks, collection infrastructure maturity, and the integration of recycled metal supply chains with corporate decarbonization commitments across the automotive, construction, and packaging sectors, and is the primary reference jurisdiction for the policy and commercial standards that are progressively influencing circular metal economy development in other regions. North America maintains a structurally important position as both one of the world’s largest scrap generating economies and a major exporter of ferrous and non-ferrous scrap to markets in Asia, Latin America, and the Middle East, with the domestic electric arc furnace steel sector providing a large and growing captive demand base for domestic ferrous scrap. Emerging markets across Southeast Asia, the Middle East, and Sub-Saharan Africa are developing their scrap processing and utilization capabilities in line with expanding industrial production and growing awareness of the economic and environmental value of domestic scrap recovery.

Key Drivers

Accelerating Transition to Electric Arc Furnace Steelmaking and the Structural Growth in Ferrous Scrap Demand from Decarbonizing Steel Producers

The most consequential structural demand driver for the global scrap metal recycling market is the accelerating transition of the global steel industry away from integrated blast furnace and basic oxygen furnace production routes and toward electric arc furnace technology, motivated by the compelling carbon intensity, energy cost, and operational flexibility advantages that electric arc furnace steelmaking offers relative to coal-dependent primary steel production in an environment of rising carbon prices, tightening emissions regulations, and growing customer and investor scrutiny of steel sector decarbonization commitments. Electric arc furnace steelmaking consumes scrap metal as its primary or sole metallic charge, making the availability of adequate volumes of high-quality processed ferrous scrap a direct operational requirement for the expanding global electric arc furnace fleet. The substantial pipeline of new electric arc furnace capacity under construction and in advanced planning stages across North America, Europe, and emerging steel markets in India, Southeast Asia, and the Middle East is translating this structural demand growth into contracted scrap procurement requirements that are providing processing operators and scrap traders with multi-year demand visibility and commercial incentives to invest in collection network expansion, processing capacity, and quality upgrading capabilities. Steel producers committed to science-based emissions reduction targets and green steel product programs for automotive and construction customers are additionally seeking scrap suppliers capable of providing certified low-carbon feedstocks with verifiable chain of custody documentation, creating a quality and certification premium layer within the ferrous scrap market that rewards operators investing in traceable and sustainably sourced scrap supply chains.

Industrial Decarbonization Mandates and the Growing Premium for Low-Embodied-Carbon Recycled Metal Feedstocks Across Key End-Use Industries

A powerful and progressively intensifying demand driver for recycled secondary metal across both ferrous and non-ferrous categories is the systematic integration of embodied carbon reduction requirements into the procurement standards, product carbon footprint disclosure frameworks, and supply chain sustainability commitments of major metal-consuming industries including automotive manufacturing, aerospace and defense, building and construction, consumer electronics, and energy infrastructure. Carbon border adjustment mechanisms, extended producer responsibility regulations, and mandatory environmental product declaration requirements are collectively making the embodied carbon content of metal inputs a commercially consequential characteristic in procurement decisions across these industries, driving a structural shift in buying criteria from unit price-based evaluation toward total carbon cost and sustainability compliance assessment that systematically favors recycled secondary metal over primary ore-derived alternatives. Automotive manufacturers operating under fleet average emission regulations and supply chain scope three reduction targets are specifying recycled metal content thresholds for steel, aluminum, and copper inputs across body, chassis, and powertrain component categories, generating structured demand for certified recycled metal feedstocks with verifiable composition and carbon intensity documentation. Construction sector green building certification programs including LEED, BREEAM, and national equivalents are awarding credits for recycled steel and aluminum content in structural and cladding materials, creating procurement preferences at project level that translate into sustained demand for high recycled content certified metal products. These regulatory and voluntary sustainability frameworks are operating in a mutually reinforcing manner that is progressively expanding the commercial premium attached to recycled secondary metal and providing durable economic justification for investment in scrap collection infrastructure, processing technology, and certification systems.

Rising Primary Metal Production Costs, Resource Scarcity Concerns, and the Compelling Economics of Secondary Metal Recovery

A fundamental and long-duration economic driver supporting the commercial viability and investment attractiveness of scrap metal recycling is the structural advantage in production economics that secondary metal recovery from scrap offers relative to primary metal production from ore across the full range of ferrous and non-ferrous metals, an advantage that is being amplified by the rising cost trajectory of primary production inputs including energy, water, mining royalties, and environmental compliance obligations in an operating environment of progressively tightening resource extraction regulation. The energy required to produce steel from scrap in an electric arc furnace is a fraction of that required for integrated blast furnace production from iron ore, and the energy intensity advantage of secondary aluminum production from recycled scrap relative to primary smelting from bauxite ore is among the largest in the metals industry, providing secondary producers with a structural cost competitiveness that strengthens as energy prices rise and carbon costs increase. Growing geopolitical attention to critical mineral supply security and the concentration of primary metal ore reserves and processing capacity in a limited number of geographies is elevating the strategic importance of domestic scrap metal recycling as a supply security lever for metal-importing economies, motivating government investment in domestic scrap collection infrastructure, preferential treatment of secondary metal producers in industrial policy frameworks, and restrictions on the export of scrap metals that are classified as strategically important industrial inputs. The combination of cost economics, energy security, and carbon intensity advantages is creating a compelling and multi-dimensional investment case for scrap metal recycling capacity expansion that extends beyond commodity cycle considerations and is increasingly attracting long-term infrastructure capital alongside the traditional trading and processing operators that have historically dominated the sector.

Key Challenges

Commodity Price Volatility and the Structural Sensitivity of Scrap Metal Economics to Steel and Non-Ferrous Metal Market Cycles

The global scrap metal recycling industry is fundamentally exposed to the commodity price cycles of the steel and non-ferrous metal markets whose derived demand determines scrap metal pricing, creating a structural financial volatility characteristic that affects the investment planning, operating margin management, and capital allocation decisions of participants across the collection, processing, and trading segments of the value chain. Scrap metal prices are derived from and move closely with primary metal benchmark prices, but with additional volatility introduced by the responsiveness of scrap generation rates to economic activity levels, the sensitivity of scrap collection economics to energy, labor, and logistics cost movements, and the amplifying effect of speculative inventory management practices by traders seeking to optimize buying and selling timing in volatile market conditions. Periods of sharp primary metal price decline, such as those associated with global economic slowdowns or oversupply conditions in specific metal markets, can rapidly compress scrap metal margins to levels that make collection and processing operations uneconomic, leading to temporary contraction in scrap supply that subsequently contributes to price spikes when industrial activity recovers. The capital-intensive nature of modern scrap processing infrastructure, particularly large shredding facilities, advanced sorting systems, and non-ferrous metal recovery plants, requires operators to commit to long-duration investments whose financial returns are highly sensitive to the price environment prevailing over multi-year operating horizons, creating significant financial risk that can deter investment in processing capacity modernization and expansion during periods of market uncertainty. Managing this commodity price exposure through trading hedging strategies, long-term supply and offtake agreements with steel mills and metal consumers, and operational flexibility in material flow management between market segments is a central and ongoing financial management challenge for the industry.

Scrap Contamination, Quality Inconsistency, and the Technical Challenges of Meeting Increasingly Stringent Metal Consumer Feedstock Specifications

A persistent technical and commercial challenge confronting the scrap metal recycling industry is the difficulty of consistently delivering processed scrap materials that meet the increasingly precise chemical composition, tramp element, and physical preparation specifications required by modern steel producers operating electric arc furnaces with tight product quality requirements, non-ferrous metal producers manufacturing high-specification alloys, and specialty metal processors requiring certified compositional purity. Post-consumer scrap streams are inherently heterogeneous in composition, contaminated with non-metallic materials including plastics, rubber, coatings, and fluids, and contain tramp elements introduced through coating systems, alloying additions, and composite material construction that cannot be economically removed through conventional mechanical processing, requiring either sophisticated sorting and separation technology or blending management to maintain outbound scrap quality within acceptable tolerance ranges. The growing complexity of end-of-life products, particularly vehicles, consumer electronics, and construction systems that incorporate an increasing variety of material combinations and joining technologies, is progressively increasing the processing intensity required to separate and upgrade scrap streams to commercial quality specifications. The introduction of high-strength steel grades, advanced aluminum alloys, and multi-material lightweight constructions in automotive and aerospace applications is creating new scrap quality management challenges as the metallurgical characteristics of these newer material categories differ from the conventional scrap streams for which processing operations and quality standards were originally developed, requiring ongoing investment in processing technology adaptation and quality monitoring capability to maintain feedstock acceptability for the most demanding metal consumer segments.

Regulatory Fragmentation, Scrap Export Restrictions, and the Complexity of Managing Compliance Across Evolving International Trade Frameworks

A significant operational and commercial challenge for participants in the global scrap metal recycling market is the progressive proliferation of national regulatory frameworks governing scrap metal classification, export permitting, hazardous waste designation, and trade restriction that are reshaping global material flows, creating compliance burdens for internationally operating scrap traders and processors, and generating market access uncertainty that complicates the long-term commercial planning required to justify investment in scrap collection and processing infrastructure. A growing number of economies have implemented or are actively considering restrictions on the export of domestically generated scrap metal, driven by industrial policy objectives of securing preferential access to secondary metal feedstocks for domestic steel and non-ferrous industries, and these restrictions are fragmenting previously integrated global scrap trade flows and creating regional market imbalances between scrap generating and consuming geographies. The application of hazardous waste classification frameworks to certain categories of scrap metal under international trade conventions, including the Basel Convention’s restrictions on transboundary movements of waste materials, creates compliance complexity and additional documentation requirements for scrap exporters and importers that increase transaction costs and can effectively serve as non-tariff barriers to otherwise commercially viable cross-border scrap trade. The absence of internationally harmonized standards for scrap metal quality grading, compositional specification, and environmental compliance verification increases the due diligence requirements and risk management costs associated with cross-border scrap transactions, limiting the efficiency of global scrap market integration and reducing the ability of recycling operators to optimize material flows between regions with complementary scrap generation and consumption profiles.

Market Segmentation

- Segmentation By Metal Type

- Ferrous Scrap

- Aluminum Scrap

- Copper Scrap

- Stainless Steel and Nickel Alloy Scrap

- Lead Scrap

- Zinc Scrap

- Titanium Scrap

- Precious Metal Scrap (Gold, Silver, Platinum Group)

- Rare Earth and Critical Mineral Scrap

- Others

- Segmentation By Scrap Category

- Post-Consumer Scrap (Old Scrap)

- Post-Industrial and Prompt Industrial Scrap (New Scrap)

- End-of-Life Vehicle Scrap

- Demolition and Construction Scrap

- Electrical and Electronic Equipment Scrap (E-Scrap)

- Packaging and Consumer Product Scrap

- Industrial Machinery and Equipment Scrap

- Aerospace and Defense Component Scrap

- Energy Infrastructure Decommissioning Scrap

- Others

- Segmentation By Processing Technology

- Shredding and Size Reduction

- Shearing and Baling

- Magnetic Separation

- Eddy Current Separation

- Sensor-Based Sorting (XRF, LIBS, Optical)

- Dense Media Separation

- Thermal and Chemical Processing

- Hydrometallurgical Recovery

- Pyrometallurgical Remelting and Refining

- Robotic Disassembly and Selective Dismantling

- Others

- Segmentation By End-Use Industry

- Steel and Iron Foundries

- Aluminum Smelters and Secondary Producers

- Copper and Brass Mills

- Stainless Steel and Specialty Alloy Producers

- Automotive Manufacturing

- Building and Construction

- Electrical and Electronics Manufacturing

- Aerospace and Defense

- Energy and Power Generation

- Packaging and Consumer Goods

- Others

- Segmentation By Source Sector

- Automotive and Transportation

- Building Demolition and Construction

- Manufacturing and Industrial

- Electrical and Electronic Equipment

- Municipal Solid Waste and Household Collection

- Shipbreaking and Marine

- Aerospace and Defense

- Energy Infrastructure and Utilities

- Others

- Segmentation By Business Model

- Integrated Collection and Processing Operators

- Scrap Dealer and Broker Networks

- Captive Recycling Operations of Steel and Metal Producers

- Municipal and Government-Run Collection Programs

- Informal Sector Collection and Aggregation

- Industrial Scrap Management Outsourcing

- Digital Scrap Trading and Exchange Platforms

- Others

- Segmentation By Certification and Traceability

- Certified Low-Carbon Secondary Metal

- Chain-of-Custody Certified Scrap

- Responsible Sourcing and Conflict-Free Certified

- Environmental Product Declaration Compliant

- ISO 14001 and Environmental Management Certified Operations

- Science-Based Targets Aligned Supply Chain

- Others

- Segmentation By Sales Channel

- Direct Long-Term Supply Agreements with Steel Mills and Smelters

- Spot Market and Commodity Exchange Trading

- Scrap Export and International Trade

- Industrial Scrap Management Contracts

- Online and Digital Trading Platforms

- Auction and Tender-Based Procurement

- Others

- Segmentation By End User

- Integrated Steel Producers

- Electric Arc Furnace Mini-Mill Operators

- Secondary Aluminum Smelters

- Copper and Non-Ferrous Metal Refiners

- Specialty Alloy and Superalloy Producers

- Foundries and Die Casters

- Battery and Energy Storage Manufacturers

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

All market revenues are presented in USD

Historical Year: 2021–2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027–2036

Key Questions this Study Will Answer

- What is the projected global market valuation and volume for scrap metal recycling through 2036, segmented by metal type, scrap category, end-use industry, and region, and which metal categories and source sectors are expected to generate the highest incremental revenue and volume contribution as industrial decarbonization mandates and electric arc furnace capacity expansion accelerate across the forecast period?

- How will the accelerating global transition to electric arc furnace steelmaking, driven by carbon pricing mechanisms, green steel product demand, and the operational economics of scrap-based production, reshape the regional distribution of ferrous scrap demand, the quality and specification requirements applied to scrap feedstocks, and the competitive dynamics between integrated processors and independent scrap trading operators over the forecast horizon?

- To what extent are advanced scrap sorting technologies including sensor-based alloy identification, artificial intelligence-assisted material classification, and robotic disassembly systems expected to improve the purity, grade specificity, and commercial value of processed scrap outputs, and what are the investment economics, adoption timeline projections, and competitive differentiation implications for processing operators that deploy these technologies relative to those relying on conventional mechanical separation methods?

- How are national scrap export restrictions, evolving hazardous waste classification frameworks under international trade conventions, and carbon border adjustment mechanisms expected to reshape global scrap trade flows, regional market price dynamics, and the investment economics of domestic scrap processing capacity in both established recycling markets and emerging industrial economies across the forecast period?

- Who are the leading scrap collection and processing operators, advanced sorting technology providers, digital trading platform developers, and secondary metal producers currently defining the competitive landscape of the global scrap metal recycling market, and what are their respective technology investment priorities, geographic expansion strategies, certification and traceability program commitments, and strategic partnership and vertical integration approaches through the forecast horizon?

- Product Definition

- Scope of the Study

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Industry Publications, Metal Recycling Association Reports & Trade Press Releases

- Government & Regulatory Authority Data (US EPA, EU Commission, UNEP, BIS, Basel Convention Secretariat, etc.)

- Scrap Metal Generation, Collection, Trade Flow & Recycling Rate Statistics

- Scrap Processor, Steelmaker, Smelter & Metal Exchange Supply Chain Databases

- Primary Research Design & Execution

- In-depth Interviews with Scrap Processors, Secondary Metal Producers, OEM Procurement Heads & Sustainability Directors

- Surveys with Scrap Dealers, Metal Traders, End-Use Manufacturers & Waste Management Operators

- Expert Panel Validation

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Bottom-Up & Top-Down Reconciliation

- Scrap Generation, Collection Rate & Secondary Metal Output Model

- End-Use Consumption, Recycled Content & Closed-Loop Rate Forecasting Model

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Technology & Innovation Highlights

- Processing Economics & Unit Economics Summary

- Average Facility CAPEX & OPEX Benchmarks

- Primary vs Secondary Metal Cost & Margin Comparison

- Green & Low-Carbon Metal Premium & Revenue Model Summary

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Geographic & Regional Trends

- Risk Assessment Framework

- Geopolitical & Trade Policy Risk (Scrap Export Bans, Tariffs & Trade Restrictions)

- Scrap Metal & Commodity Price Volatility (LME Steel, Aluminum, Copper, Stainless) Risk

- Environmental & Regulatory Risk

- Financial / Market Risk

- Primary Metal Price Competition & Energy Cost Risk

- Scrap Quality, Contamination & Sorting Complexity Risk

- Carbon Border Adjustment Mechanism (CBAM), Extended Producer Responsibility (EPR) & Decarbonisation Transition Risk

- Regulatory Framework & Policy Standards

- Global Scrap Metal Recycling Market Economics

- Processing Economics & Unit Economics Framework

- Capital Expenditure (CAPEX) Structure

- Operating Expenditure (OPEX) Structure

- Revenue Model & Monetisation Levers

- Capacity Utilisation & Throughput Economics

- Payback Period & Return on Investment (ROI) Analysis

- Total Cost of Secondary Metal Production vs Primary Metal Production

- Scrap Input & Raw Material Cost Analysis

- Ferrous Scrap Price Benchmarks & Price Trends (USD/tonne, 2021–2035)

- Non-Ferrous Scrap Price Benchmarks by Metal (Aluminum, Copper, Stainless, Nickel, Zinc, Lead, Brass)

- Pre-Consumer (Prompt/New) Scrap vs Post-Consumer (Old/Obsolete) Scrap Cost Differentials

- End-of-Life Vehicle (ELV) & WEEE Scrap Procurement Cost Dynamics

- Energy Cost Structure in Scrap Processing & Secondary Smelting Operations

- Flux, Slag Treatment & Alloying Element Input Cost Analysis

- Impact of Scrap Quality, Grade Segregation & Contamination on Processing Economics

- Scrap Collection, Sorting & Pre-Processing Economics

- Collection Infrastructure & Logistics Cost Structure by Geography

- Sorting Technology (Manual, Magnetic, Eddy Current, XRF, AI-Vision, Sensor-Based) Cost Comparison

- Shredding, Shearing, Baling & Pre-Treatment Cost Economics

- Scrap Yield, Metal Recovery Rate & Residue Management Economics

- Secondary Melting & Refining Economics

- Electric Arc Furnace (EAF), Induction Furnace & Cupola Furnace Cost Benchmarks

- Basic Oxygen Furnace (BOF) with Scrap Charge Economics

- Slag, Dross & By-Product Recovery Economics

- Alloying, Casting & Quality Assurance Economics

- Carbon Cost & Emissions Trading (ETS) Economics in Scrap Metal Recycling

- Regulatory & Standards Compliance Economics

- Scrap Metal Quality & Grading Standards Compliance Cost Benchmarks (ISRI, BIR, EN, ISO, etc.)

- Extended Producer Responsibility (EPR), Take-Back Scheme & Basel Convention Compliance Costs

- CBAM, Environmental Permit & Hazardous Waste Regulation Compliance Costs

- Global Scrap Metal Recycling Market Outlook

- Market Size & Forecast by Value (USD Billion, 2021–2036)

- Market Size & Forecast by Volume (Million Tonnes, 2021–2036)

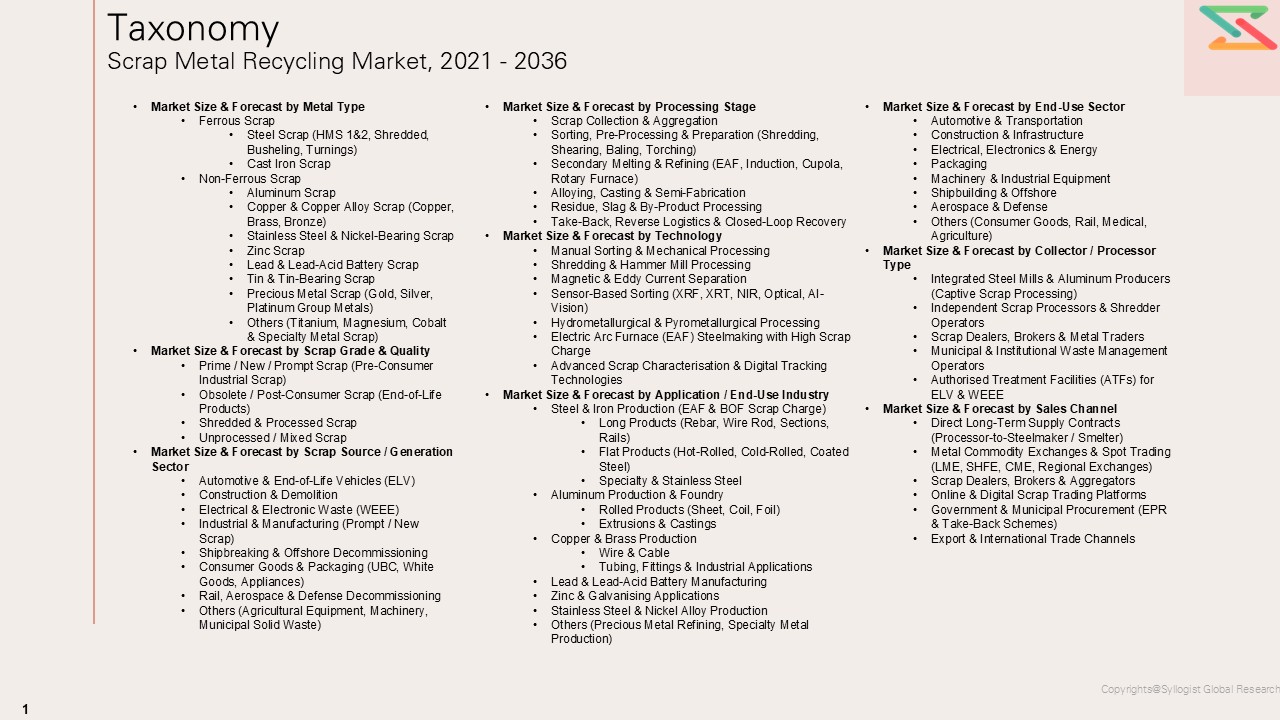

- Market Size & Forecast by Metal Type

- Ferrous Scrap

- Steel Scrap (HMS 1&2, Shredded, Busheling, Turnings)

- Cast Iron Scrap

- Non-Ferrous Scrap

- Aluminum Scrap

- Copper & Copper Alloy Scrap (Copper, Brass, Bronze)

- Stainless Steel & Nickel-Bearing Scrap

- Zinc Scrap

- Lead & Lead-Acid Battery Scrap

- Tin & Tin-Bearing Scrap

- Precious Metal Scrap (Gold, Silver, Platinum Group Metals)

- Others (Titanium, Magnesium, Cobalt & Specialty Metal Scrap)

- Market Size & Forecast by Scrap Grade & Quality

- Prime / New / Prompt Scrap (Pre-Consumer Industrial Scrap)

- Obsolete / Post-Consumer Scrap (End-of-Life Products)

- Shredded & Processed Scrap

- Unprocessed / Mixed Scrap

- Market Size & Forecast by Scrap Source / Generation Sector

- Automotive & End-of-Life Vehicles (ELV)

- Construction & Demolition

- Electrical & Electronic Waste (WEEE)

- Industrial & Manufacturing (Prompt / New Scrap)

- Shipbreaking & Offshore Decommissioning

- Consumer Goods & Packaging (UBC, White Goods, Appliances)

- Rail, Aerospace & Defense Decommissioning

- Others (Agricultural Equipment, Machinery, Municipal Solid Waste)

- Market Size & Forecast by Processing Stage

- Scrap Collection & Aggregation

- Sorting, Pre-Processing & Preparation (Shredding, Shearing, Baling, Torching)

- Secondary Melting & Refining (EAF, Induction, Cupola, Rotary Furnace)

- Alloying, Casting & Semi-Fabrication

- Residue, Slag & By-Product Processing

- Take-Back, Reverse Logistics & Closed-Loop Recovery

- Market Size & Forecast by Technology

- Manual Sorting & Mechanical Processing

- Shredding & Hammer Mill Processing

- Magnetic & Eddy Current Separation

- Sensor-Based Sorting (XRF, XRT, NIR, Optical, AI-Vision)

- Hydrometallurgical & Pyrometallurgical Processing

- Electric Arc Furnace (EAF) Steelmaking with High Scrap Charge

- Advanced Scrap Characterisation & Digital Tracking Technologies

- Market Size & Forecast by Application / End-Use Industry

- Steel & Iron Production (EAF & BOF Scrap Charge)

- Long Products (Rebar, Wire Rod, Sections, Rails)

- Flat Products (Hot-Rolled, Cold-Rolled, Coated Steel)

- Specialty & Stainless Steel

- Aluminum Production & Foundry

- Rolled Products (Sheet, Coil, Foil)

- Extrusions & Castings

- Copper & Brass Production

- Wire & Cable

- Tubing, Fittings & Industrial Applications

- Lead & Lead-Acid Battery Manufacturing

- Zinc & Galvanising Applications

- Stainless Steel & Nickel Alloy Production

- Others (Precious Metal Refining, Specialty Metal Production)

- Steel & Iron Production (EAF & BOF Scrap Charge)

- Market Size & Forecast by End-Use Sector

- Automotive & Transportation

- Construction & Infrastructure

- Electrical, Electronics & Energy

- Packaging

- Machinery & Industrial Equipment

- Shipbuilding & Offshore

- Aerospace & Defense

- Others (Consumer Goods, Rail, Medical, Agriculture)

- Market Size & Forecast by Collector / Processor Type

- Integrated Steel Mills & Aluminum Producers (Captive Scrap Processing)

- Independent Scrap Processors & Shredder Operators

- Scrap Dealers, Brokers & Metal Traders

- Municipal & Institutional Waste Management Operators

- Authorised Treatment Facilities (ATFs) for ELV & WEEE

- Market Size & Forecast by Revenue Stream

- Scrap Metal Sales Revenue (Ferrous & Non-Ferrous)

- Scrap Collection, Aggregation & Logistics Services Revenue

- Toll-Processing, Sorting & Pre-Treatment Services Revenue

- Secondary Metal & Alloy Production Revenue

- By-Product, Slag & Residue Recovery Revenue

- Carbon Credit, ETS & Sustainability Services Revenue

- Recycling Technology Licensing & Equipment Supply Revenue

- Market Size & Forecast by Sales Channel

- Direct Long-Term Supply Contracts (Processor-to-Steelmaker / Smelter)

- Metal Commodity Exchanges & Spot Trading (LME, SHFE, CME, Regional Exchanges)

- Scrap Dealers, Brokers & Aggregators

- Online & Digital Scrap Trading Platforms

- Government & Municipal Procurement (EPR & Take-Back Schemes)

- Export & International Trade Channels

- Asia-Pacific Scrap Metal Recycling Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Volume (Million Tonnes)

- By Metal Type

- By Scrap Grade & Quality

- By Scrap Source / Generation Sector

- By Processing Stage

- By Technology

- By Application / End-Use Industry

- By End-Use Sector

- By Collector / Processor Type

- By Revenue Stream

- By Sales Channel

- Key Demand Drivers (APAC-Specific)

- Competitive Landscape (APAC)

- Europe Scrap Metal Recycling Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Volume (Million Tonnes)

- By Metal Type

- By Scrap Grade & Quality

- By Scrap Source / Generation Sector

- By Processing Stage

- By Technology

- By Application / End-Use Industry

- By End-Use Sector

- By Collector / Processor Type

- By Revenue Stream

- By Sales Channel

- Key Demand Drivers (Europe-Specific)

- Competitive Landscape (Europe)

- North America Scrap Metal Recycling Market Outlook

- Market Overview & Strategic Importance

- Market Size & Forecast

- By Value (2020–2035)

- By Volume (Million Tonnes)

- By Metal Type

- By Scrap Grade & Quality

- By Scrap Source / Generation Sector

- By Processing Stage

- By Technology

- By Application / End-Use Industry

- By End-Use Sector

- By Collector / Processor Type

- By Revenue Stream

- By Sales Channel

- Key Demand Drivers (North America-Specific)

- Competitive Landscape (North America)

- Latin America Scrap Metal Recycling Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Volume (Million Tonnes)

- By Metal Type

- By Scrap Grade & Quality

- By Scrap Source / Generation Sector

- By Processing Stage

- By Technology

- By Application / End-Use Industry

- By End-Use Sector

- By Collector / Processor Type

- By Revenue Stream

- By Sales Channel

- Key Demand Drivers (LATAM-Specific)

- Competitive Landscape (Latin America)

- Middle East & Africa Scrap Metal Recycling Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Volume (Million Tonnes)

- By Metal Type

- By Scrap Grade & Quality

- By Scrap Source / Generation Sector

- By Processing Stage

- By Technology

- By Application / End-Use Industry

- By End-Use Sector

- By Collector / Processor Type

- By Revenue Stream

- By Sales Channel

- Key Demand Drivers (MEA-Specific)

- Competitive Landscape (MEA)

- Country-Wise Scrap Metal Recycling Market Outlook

- Market Size & Forecast by Country

- By Value

- By Volume (Million Tonnes)

- By Metal Type

- By Scrap Grade & Quality

- By Scrap Source / Generation Sector

- By Processing Stage

- By Technology

- By Application / End-Use Industry

- By End-Use Sector

- By Collector / Processor Type

- By Revenue Stream

- By Sales Channel

- Countries Covered: United States, Canada, Germany, United Kingdom, France, Italy, Netherlands, Belgium, Turkey, Russia, China, Japan, South Korea, India, Australia, Brazil, Mexico, South Africa, UAE, Saudi Arabia

- Market Size & Forecast by Country

- Global Scrap Metal Trade Flow Analysis

- Global Scrap Metal Export & Import Volume & Value by Metal Type (2021–2036)

- Key Scrap Exporting Nations & Export Dependency Analysis

- Key Scrap Importing Nations & Import Reliance Assessment

- Impact of Scrap Export Bans, Tariffs & Trade Policy Shifts on Global Flows

- Intra-Regional vs Inter-Regional Trade Flow Dynamics

- Scrap Metal Shipping Routes, Port Infrastructure & Logistics Cost Analysis

- Technology Landscape & Innovation Analysis

- Scrap Metal Recycling Technology Maturity Assessment

- Emerging & Disruptive Technologies in Scrap Metal Processing & Recycling

- Advanced Sorting Technologies (AI-Vision, Hyperspectral, XRF, XRT, Sensor-Based)

- Electric Arc Furnace (EAF) Innovation & High Scrap-Charge Steelmaking

- Hydrometallurgical & Pyrometallurgical Advances for Complex Scrap Streams

- Digital Material Passports, Blockchain Traceability & Scrap Certification Platforms

- Robotics & Automation in Scrap Processing Yards

- Technology Readiness & Commercialisation Matrix – Key Scrap Metal Recycling Technologies

- Patent Landscape Analysis

- R&D Investment Benchmarking

- Value Chain & Supply Chain Analysis

- Scrap Metal Recycling Value Chain Mapping

- Scrap Generation, Collection & Reverse Logistics Network Analysis

- Supply Chain Concentration & Dependency Analysis

- Key Supplier Mapping by Metal Type, Scrap Source & Processing Stage

- Supplier Risk Heat Map

- Make vs Buy Strategy Trends Among Scrap Processors & Secondary Metal Producers

- Pricing Analysis

- Scrap Metal Pricing Dynamics & Mechanisms

- Ferrous Scrap Price Trends (HMS 1&2, Shredded, Busheling – USD/tonne, 2021–2035)

- Non-Ferrous Scrap Price Trends by Metal (Aluminum, Copper, Stainless, Zinc, Lead, Nickel)

- LME Benchmark Pricing, Regional Premiums & Scrap Spreads Analysis

- Total Cost of Ownership (TCO) – Secondary vs Primary Metal Lifecycle Cost & Carbon Cost

- Direct Contract vs Spot Market Pricing Trends & Benchmarks

- Green Metal & Certified Recycled Content Price Premium Analysis

- Sustainability & Circular Economy Performance

- Carbon Footprint Benchmarking: Secondary vs Primary Metal Production (Scope 1, 2 & 3 Emissions)

- Scrap Metal Recycling Rate Analysis by Metal Type, Region & Generation Sector

- Extended Producer Responsibility (EPR), Take-Back Schemes & Deposit Return Systems

- Closed-Loop Recycling Programmes & Industry Commitments (Automotive, Packaging, Construction)

- EU Green Deal, Critical Raw Materials Act, Basel Convention & Global Circular Economy Policy Impact Assessment

- Green Steel, Green Aluminum & Certified Recycled Content Frameworks (ResponsibleSteel, ASI, LME Green)

- ESG Reporting, Lifecycle Assessment (LCA) & Science-Based Targets in Scrap Metal Recycling Operations

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level: Global Integrated Players vs Regional Scrap Processors

- Top 5 Scrap Metal Recycling Companies Market Revenue Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis by Metal Type & Geography

- Competitive Intensity Map by Segment & Region

- Player Classification

- Tier-1 Global Integrated Scrap Metal Processors & Secondary Metal Producers

- Tier-2 Regional & Specialist Scrap Processors

- Scrap Dealers, Brokers & Metal Trading Companies

- Recycling Technology & Equipment Providers

- Emerging & Disruptive Players

- Competitive Analysis Frameworks

- Market Share Analysis by Metal Type, Processing Stage & Geography

- R&D Intensity & Green Metal Innovation Benchmarking

- Long-Term Supply Contract & Closed-Loop Partnership Portfolio Comparison

- Geographic Revenue Exposure & Scrap Sourcing Footprint Comparison

- Company Profiles

- Company Overview, HQ & Organisational Structure

- Scrap Metal Products, Services & Processing Portfolio

- Revenue Breakdown (By Metal Type, By Segment, By Geography)

- Key Customer Supply Programmes & Closed-Loop Recycling Partnerships

- Processing Facility & Yard Footprint

- Recent Developments (M&A, Capacity Expansion, New Partnerships, Financial Results)

- SWOT Analysis

- Strategic Focus: Processing Capacity Expansion, Technology Upgrade, Green Metal Certification

- Strategic Output

- Market Opportunity Matrix

- High-Value Opportunity Quadrant Analysis

- Addressable Market by Segment & Region

- Time-to-Revenue Assessment by Opportunity

- White Space Opportunity Analysis

- Underserved Metal Type, Scrap Source & Processing Stage Gaps

- Geographic Markets with Low Recycling Penetration & High Scrap Generation Potential

- Technology Gaps with High Commercialisation Potential

- Customer Segment Unmet Needs

- Strategic Recommendations

- Product Portfolio & Processing Capability Strategy

- Technology & Digitalization Strategy

- Processing Capacity Expansion & Facility Investment Strategy

- Scrap Sourcing, Collection Network & Reverse Logistics Strategy

- Pricing & Commercial Strategy

- Sustainability, Decarbonisation & Regulatory Compliance Strategy

- Supply Chain & Raw Material Sourcing Strategy

- Partnership, M&A & Expansion Strategy

- Regional Growth Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-Term (2025–2028)

- Mid-Term (2029–2032)

- Long-Term (2033–2036)

- Market Opportunity Matrix

- Market Structure & Concentration

- Market Size & Forecast

- Market Size & Forecast

- Market Size & Forecast

- Market Size & Forecast

- Ferrous Scrap

- Processing Economics & Unit Economics Framework