Market Definition

The Global Floating Offshore Wind Market encompasses the engineering, procurement, construction, installation, operation, and decommissioning of wind energy generation systems in which wind turbines and their supporting structures are mounted on buoyant substructures that are moored to the seabed through dynamic mooring line and anchor systems rather than fixed to the seabed through monopile, jacket, or gravity-based foundation structures, enabling the deployment of large-scale wind energy capacity in water depths typically exceeding 60 meters where the resource quality is superior to nearshore zones but where conventional fixed-bottom offshore wind technology is technically and economically impractical. The product and infrastructure scope of this market includes semi-submersible floating platform structures fabricated from steel or concrete with multiple columns and pontoons configured to provide the hydrostatic stability required to support multi-megawatt wind turbines in open ocean wave and current environments, spar-buoy floating foundations utilizing deep-draft cylindrical ballast structures to achieve stability through low center of gravity positioning, tension leg platform substructures employing vertical taut mooring tendons to provide high-stiffness heave restraint in moderate water depths, barge-type and multi-unit shared mooring platform concepts targeting cost reduction through standardization and series fabrication, dynamic array cable systems engineered to accommodate floating platform motions while transmitting generated power to seabed-mounted inter-array cable networks, dynamic inter-array and export cable configurations incorporating bend stiffeners, buoyancy modules, and cable management systems that protect against fatigue damage accumulation over operational lifespans exceeding 25 years, mooring systems comprising synthetic fiber ropes, studless chain, wire rope, and drag embedment or suction pile anchors engineered to maintain platform position within defined watch circles under extreme sea state and storm loading conditions, and the specialized marine installation vessels, offshore construction equipment, and operations and maintenance infrastructure required to install and service floating wind assets in deep water locations that are frequently beyond the operational range of conventional jackup installation vessels. The technology landscape within this market spans the adaptation of commercial turbine platforms from the 8 megawatt to 15 megawatt and beyond class for floating installation, including the engineering modifications to tower base interface design, drivetrain dynamics, blade load management, and control system architecture required to accommodate the additional motion degrees of freedom that floating foundations introduce relative to fixed-bottom installations, as well as the emerging category of purpose-designed floating wind turbines whose structural and aerodynamic designs are optimized from conception for floating platform integration rather than adapted from land or fixed-bottom offshore designs. The value chain of this market extends from steel and concrete material producers, synthetic fiber rope and anchor chain manufacturers, dynamic cable and umbilical specialists, and wind turbine original equipment manufacturers through floating platform fabricators, mooring system suppliers, marine installation and heavy lift contractors, offshore electrical infrastructure developers, project development and financing entities, independent power producers, utility offtake counterparties, and the operations and maintenance service organizations that sustain floating wind asset performance across multi-decade operational periods in remote deep water locations.

Market Insights

The global floating offshore wind market is at a pivotal juncture in its commercial development in 2026, transitioning from a pre-commercial demonstration phase characterized by pilot projects of one to three turbines to an early commercial scale phase defined by the development and financing of utility-scale projects in the 200 megawatt to 1,000 megawatt capacity range, the concurrent advancement of multiple competing floating substructure technology platforms toward the cost reduction trajectories required for grid-competitive power generation economics, and the progressive mobilization of sovereign policy support mechanisms, port infrastructure investment, and supply chain development programs in leading markets including the United Kingdom, Norway, France, South Korea, Japan, and the United States. The global floating offshore wind market was valued at approximately USD 1.8 billion in 2025 and is projected to expand at a compound annual growth rate of 38 percent through 2036, reaching approximately USD 51 billion by the end of the forecast period, a trajectory driven by the structural demand for deep water offshore wind capacity in markets where the fixed-bottom offshore wind resource is constrained by seabed bathymetry and where national renewable energy targets require the exploitation of superior wind resources at water depths accessible only through floating technology. The competitive landscape of the market is structured around a small number of established offshore wind developers with the balance sheet strength and project development expertise to advance first commercial-scale floating projects through multi-year permitting, engineering, and financing processes, a cohort of technology developers and industrial conglomerates promoting proprietary floating platform concepts and seeking strategic partnerships with utilities and energy majors to accelerate their technology commercialization pathways, an emerging specialized offshore supply chain oriented toward the unique fabrication, installation, and service requirements of floating wind assets, and national and regional policy frameworks whose design and implementation consistency will be the primary determinant of the pace and geographic distribution of commercial project development activity over the forecast period.

A defining technological and commercial trend reshaping the competitive structure and cost reduction trajectory of the floating offshore wind market is the accelerating scale-up of turbine ratings deployed on floating platforms, with the industry advancing rapidly from the 6 megawatt to 8 megawatt turbine class that characterized early demonstration projects toward the deployment of 12 megawatt to 15 megawatt turbines on semi-submersible and spar platforms in projects currently in advanced development, and with turbine original equipment manufacturers actively developing platform-compatible variants of their 15 megawatt to 18 megawatt next-generation turbine families for floating wind application. The economic significance of turbine rating scale-up in floating wind is amplified relative to fixed-bottom offshore wind because the high unit cost of floating substructure fabrication, mooring system installation, and dynamic cable infrastructure creates a strong economic incentive to maximize energy capture per installed unit, as the proportion of total project cost attributable to balance-of-plant and infrastructure components that do not scale proportionally with turbine rating is higher in floating projects than in conventional offshore developments. The engineering challenges associated with deploying very large turbines on floating platforms, including the management of higher aerodynamic and gyroscopic loading on platform stability, the design of tower and turbine control systems capable of mitigating platform motion-induced fatigue loading on drivetrain and blade components, and the development of floating-specific turbine certification standards that regulatory bodies and project lenders can rely upon for technical due diligence, are being addressed through collaborative programs between turbine manufacturers, floating platform developers, classification societies, and research institutions, with certification frameworks for floating-specific turbine configurations advancing toward the completeness required to support project financing in the near-term commercial development pipeline.

The supply chain development and port infrastructure investment requirements of the floating offshore wind market represent both a critical enabler and a near-term constraint on commercial project deployment, as the fabrication, assembly, and installation of floating wind platforms demands manufacturing capabilities, heavy lift port facilities, and specialized marine vessel assets that are substantially different from those deployed in fixed-bottom offshore wind and that require large-scale capital investment in advance of confirmed project pipelines to achieve the cost reduction through series production and learned fabrication efficiency that commercial project economics require. Floating platform fabrication requires large sheltered port areas with heavy load-bearing quaysides, deep-water access for platform wet-tow or semi-submersible heavy lift vessel installation, and proximity to steel, concrete, or advanced composite material supply chains, specifications that exclude the majority of existing fixed-bottom offshore wind port facilities and that are driving targeted port infrastructure development investment programs in Scotland, Norway, France, Spain, South Korea, and Japan specifically oriented toward floating wind platform fabrication and turbine assembly. The dynamic cable and mooring system supply chain represents a particularly acute bottleneck given the specialized manufacturing processes required for dynamic power cable production, the limited number of globally operating facilities currently capable of producing floating-wind-grade dynamic array cables to the fatigue resistance and bending stiffness specifications required, and the long manufacturing lead times that constrain the pace at which supply chain capacity can be expanded to match accelerating project development activity. Industry and government stakeholders in leading floating wind markets are responding to these supply chain constraints through a combination of targeted port infrastructure grant programs, contracts for difference auction design adjustments that provide supply chain investment confidence, and joint industry programs coordinating supply chain development investment across multiple project developers to achieve the volume commitments required to justify fabrication facility capital expenditure.

From a regional perspective, Europe leads the global floating offshore wind market in installed capacity, project development pipeline maturity, policy framework development, and technology intellectual property concentration, with the United Kingdom, Norway, and France collectively hosting the largest number of demonstration projects, the most advanced commercial-scale project development pipelines, and the most developed policy support mechanisms including contracts for difference specifically configured for floating wind, seabed leasing programs allocating deep water zones for commercial floating wind development, and port infrastructure investment programs targeting floating-specific fabrication and assembly capabilities. The United Kingdom is the most significant single national market for near-term floating wind commercial deployment, with seabed leasing rounds allocating substantial deep water capacity in Scottish and Irish Sea zones suited to floating development and with a government commitment to floating wind capacity targets that is providing the policy confidence required for supply chain investment mobilization. The Asia-Pacific region, led by South Korea and Japan, represents the most significant medium-term growth market for floating offshore wind capacity, driven by the deep water bathymetric profile of Pacific coastal zones that limits the developable fixed-bottom offshore wind resource in both countries while simultaneously providing access to high-quality offshore wind resources at floating-accessible depths, and by national energy security imperatives that are elevating floating wind from a long-term research interest to an active near-term industrial policy priority. The United States Atlantic and Pacific coasts, together with the Gulf of Mexico deepwater zone, represent a large-scale long-term floating wind opportunity whose commercial development timeline is influenced by the federal leasing and permitting framework for offshore wind and by state-level renewable energy procurement programs whose configuration and volume commitment will determine the pace at which floating wind projects can advance to financial close in the United States market.

Key Drivers

Structural Limitations of Fixed-Bottom Offshore Wind Resource Availability and the Necessity of Floating Technology to Access Superior Deep Water Wind Resources in Key Markets

The most fundamental and geographically universal demand driver for floating offshore wind technology is the physical constraint imposed by seabed bathymetry on the developable fixed-bottom offshore wind resource in the majority of global coastal markets with significant offshore wind potential, a constraint that makes floating wind not merely a complementary technology extension but the only technically and economically viable pathway to exploiting the offshore wind resource in countries including Japan, South Korea, Norway, the United States Pacific Coast, and significant portions of Southern European and Mediterranean coastlines where the seabed depth exceeds 60 meters within the economic transmission distance from shore. In Japan, where the national energy transition strategy requires substantial offshore wind capacity deployment to meet carbon neutrality commitments and reduce fossil fuel import dependency, the bathymetric profile of the Japanese coastline means that fixed-bottom offshore wind development is technically viable only in a limited number of relatively shallow coastal zones, and that the scale of offshore wind capacity required by national energy policy objectives necessitates the commercial deployment of floating wind technology in the deep water zones that constitute the majority of Japan’s accessible offshore wind resource. The energy quality argument for floating wind investment is reinforced by the consistent finding across multiple national resource assessments that deep water wind resources accessible only through floating technology exhibit higher average wind speeds, higher capacity factors, reduced wake interaction losses within large arrays, and lower atmospheric turbulence intensities than nearshore shallow water zones where fixed-bottom development is concentrated, translating into higher annual energy production per megawatt of installed capacity that directly improves the economics of floating wind projects relative to fixed-bottom alternatives in markets where both technology options are in principle available. The combination of bathymetric resource exclusivity in the most commercially important near-term floating wind markets and the energy quality premium of deep water wind resources in markets where both technologies are deployable creates a structural demand for floating wind development that is independent of relative cost competitiveness with fixed-bottom alternatives and that will sustain investment and policy support for floating wind commercialization across the forecast period regardless of the pace at which floating wind capital costs converge toward fixed-bottom levels.

National Renewable Energy and Energy Security Policy Commitments Driving Sovereign Support for Floating Wind Commercial Deployment as a Strategic Industrial and Energy Transition Priority

The accelerating policy commitment of governments in leading floating offshore wind markets to deploying commercial-scale floating wind capacity as a component of national renewable energy transition strategies is providing the most direct and immediate commercial demand driver for floating wind project development, supply chain investment, and technology commercialization activity, operating through a combination of capacity target announcements, seabed leasing programs, revenue support mechanism design, port infrastructure grant funding, and research and development investment that collectively create the investment confidence framework required to mobilize the multi-billion USD project development and supply chain capital commitments necessary for commercial-scale floating wind deployment. The United Kingdom government’s commitment to 5 gigawatts of floating offshore wind capacity by 2030, supported by contracts for difference auction rounds specifically configured for floating wind with strike prices reflecting the current cost of early commercial-scale floating projects, represents the most advanced example of sovereign policy support providing direct commercial project development stimulus and has catalyzed a large pipeline of project development activity in Scottish and Irish Sea deep water zones by both incumbent fixed-bottom offshore wind developers and emerging floating wind specialist developers. South Korea’s designation of floating offshore wind as a national strategic industry, supported by dedicated research and development investment programs, port infrastructure development planning for floating platform fabrication, and offshore wind capacity procurement targets that incorporate floating wind deployment objectives, reflects the pattern of sovereign industrial policy support that is replicated with varying degrees of specificity and commitment across the leading floating wind markets and that collectively constitutes the primary demand creation mechanism for an industry whose project economics have not yet reached the point of self-sustaining commercial development independent of policy support. The energy security dimension of floating wind policy support, which has intensified following the disruptions to European and Asian energy markets created by geopolitical events affecting natural gas supply security, is elevating the political priority accorded to domestic offshore wind development including floating wind in a manner that is broadening the policy support base beyond environment-focused renewable energy constituencies to include energy security, industrial policy, and trade balance arguments that reinforce the durability of government commitment to floating wind commercialization investment across the forecast horizon.

Key Challenges

High Levelized Cost of Energy and the Substantial Gap Between Current Floating Wind Project Economics and the Cost Benchmarks Required for Grid-Competitive Power Generation Without Sustained Policy Support

The most consequential near-term commercial challenge confronting the global floating offshore wind industry is the substantial gap between the current levelized cost of energy of floating wind projects and the cost benchmarks at which floating wind power generation becomes competitive with fixed-bottom offshore wind, onshore wind, and utility-scale solar photovoltaic on a grid parity basis without material revenue support mechanisms, a gap that constrains the commercial development pace to the rate at which sovereign policy support programs are designed, funded, and executed rather than the rate at which the underlying market demand for clean energy capacity would naturally support. Current levelized cost of energy estimates for first commercial-scale floating wind projects reflect the combined effect of high floating substructure fabrication costs driven by limited series production volumes and the absence of learned efficiency improvements, elevated dynamic cable and mooring system costs reflecting supply chain immaturity and limited supplier competition, high marine installation costs driven by the limited availability of suitable installation vessels and the complex multi-stage tow-out and hook-up operations required for floating platform deployment, and project development cost burdens associated with the engineering complexity and regulatory novelty of floating wind assets in jurisdictions where consenting frameworks for this technology category are still being developed and tested. The cost reduction pathway for floating wind to the levelized cost of energy benchmarks required for subsidy-independent commercial viability requires the simultaneous achievement of multiple scale-dependent improvements including the transition from one-off bespoke platform fabrication to series production of standardized platform designs, the development of a mature and competitive supply chain for dynamic cables, mooring systems, and specialized installation vessels, the scale-up of project sizes from early commercial developments to multi-gigawatt clusters that amortize shared infrastructure costs across larger energy volumes, and the accumulation of operational performance data that enables financing institutions to reduce the risk premiums embedded in floating wind project cost of capital to levels comparable with those applied to the well-characterized fixed-bottom offshore wind asset class. The timeline for achieving these cost reductions is sensitive to the volume and pacing of near-term commercial project deployment, creating a policy dependency in the cost reduction trajectory where inadequate near-term policy support reduces deployment volumes, slows the accumulation of supply chain learning, and delays the achievement of the cost benchmarks that would eventually enable market-driven deployment without policy subsidy.

Consenting, Environmental Permitting, and Grid Connection Complexity Creating Extended Development Timelines That Elevate Project Development Risk and Capital Cost

A structurally significant commercial challenge constraining the pace of floating offshore wind project progression from development concept to construction commencement is the complexity, duration, and outcome uncertainty of the consenting, environmental permitting, and grid connection approval processes that floating wind projects must navigate in all major markets, processes that are in most jurisdictions based on regulatory frameworks originally designed for fixed-bottom offshore wind or oil and gas platforms and that require substantial adaptation to address the specific physical characteristics, environmental interaction profiles, and marine spatial planning implications of floating wind arrays deployed in deep water zones that frequently overlap with commercial fishing grounds, shipping lanes, military exercise areas, and ecologically sensitive seabed habitats. The consenting timeline for floating offshore wind projects in European markets is currently measured in years from initial project notification to final permit issuance, reflecting the combination of extensive environmental impact assessment requirements covering potential interactions with seabed ecology, migratory fish species, marine mammal populations, seabird colonies, and commercial fisheries, the coordination burden of multi-agency permit processes involving maritime authorities, fisheries regulators, aviation and radar authorities, defense departments, and environmental agencies each applying separate statutory consultation timelines, and the legal vulnerability of consenting decisions to judicial review challenges from objecting stakeholder groups whose procedural rights in offshore consenting processes are in many jurisdictions broadly defined and whose intervention can extend overall project timelines by multiple years beyond the originally planned consent issuance date. The grid connection challenge for floating offshore wind projects is further compounded by the deep water deployment locations typical of floating wind sites, which require longer submarine export cable routes to reach onshore grid connection points, greater uncertainty in the environmental impact assessment of cable landfall routes through intertidal and nearshore habitats, and in many markets the absence of transmission infrastructure of sufficient capacity in the coastal grid regions nearest to floating wind development zones, necessitating either substantial grid reinforcement investment or the development of offshore grid hub and meshed offshore network concepts whose regulatory and commercial frameworks are still being developed in most jurisdictions. Governments in leading floating wind markets are responding to these consenting and grid connection challenges through targeted regulatory reform programs, the designation of floating wind development zones with pre-qualified environmental baselines that reduce site-specific assessment burden, and coordinated offshore transmission planning processes that align grid infrastructure investment with floating wind development pipelines to reduce connection delay risk.

Market Segmentation

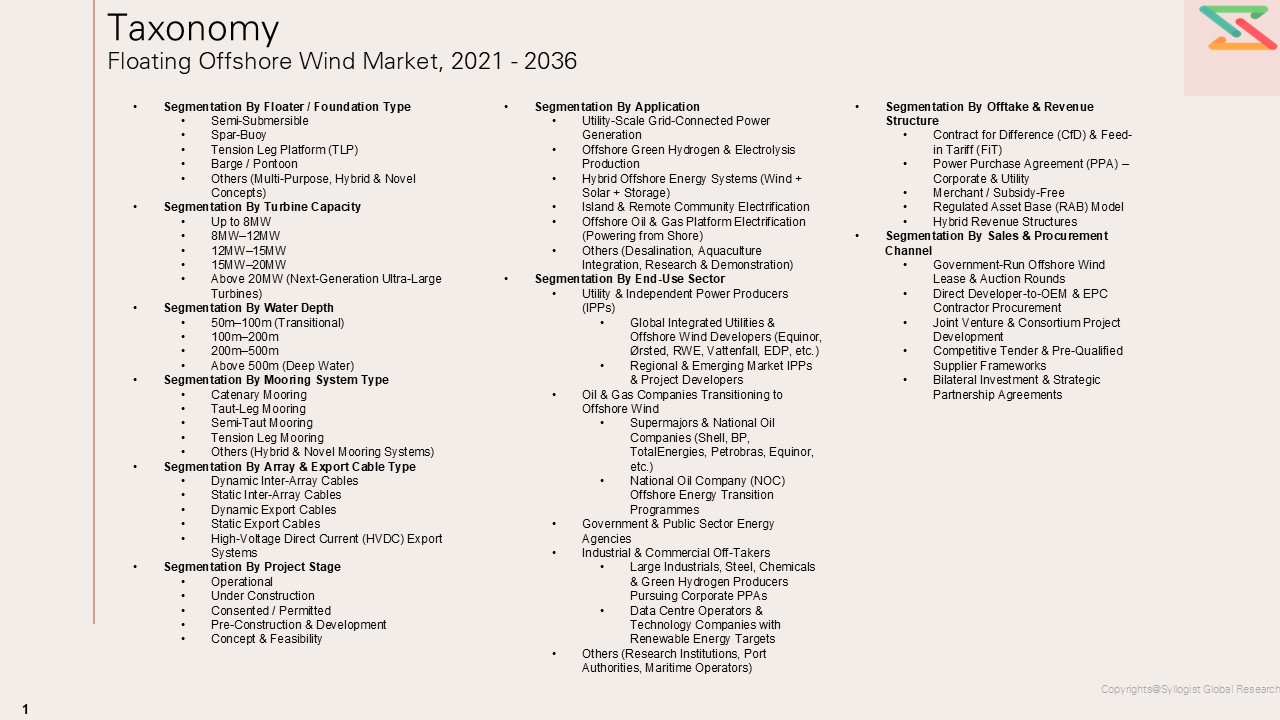

- Segmentation By Floating Substructure Type

- Semi-Submersible Floating Platforms

- Spar-Buoy Floating Foundations

- Tension Leg Platforms (TLP)

- Barge-Type Floating Platforms

- Multi-Unit Shared Mooring Platforms

- Hybrid and Novel Concept Platforms

- Others

- Segmentation By Turbine Rating

- Below 6 Megawatts

- 6 to 9 Megawatts

- 10 to 12 Megawatts

- 13 to 15 Megawatts

- Above 15 Megawatts

- Segmentation By Water Depth

- 60 to 100 Meters

- 101 to 200 Meters

- 201 to 500 Meters

- Above 500 Meters

- Segmentation By Mooring System Type

- Catenary Mooring with Drag Embedment Anchors

- Taut Leg Mooring with Suction Pile Anchors

- Semi-Taut Mooring Systems

- Tension Leg Mooring with Driven Pile Anchors

- Synthetic Fiber Rope Mooring Systems

- Others

- Segmentation By Platform Material

- Steel Fabricated Platforms

- Concrete Fabricated Platforms

- Hybrid Steel and Concrete Platforms

- Advanced Composite Material Platforms

- Others

- Segmentation By Project Scale

- Pilot and Demonstration Projects (Below 30 MW)

- Pre-Commercial Projects (30 to 100 MW)

- Early Commercial Projects (101 to 500 MW)

- Utility-Scale Commercial Projects (501 MW to 1 GW)

- Large-Scale Commercial Clusters (Above 1 GW)

- Segmentation By Component

- Floating Substructure and Hull

- Mooring Lines and Anchor Systems

- Dynamic Array Cables

- Submarine Export Cables

- Wind Turbine and Tower

- Offshore Substation and Converter Platform

- Marine Installation and Commissioning Services

- Operations and Maintenance Services

- Others

- Segmentation By End Use

- Utility-Scale Grid-Connected Power Generation

- Offshore Green Hydrogen Production

- Isolated Island and Remote Community Power Supply

- Hybrid Floating Wind and Wave Energy Systems

- Offshore Aquaculture and Multi-Use Platforms

- Others

- Segmentation By Offtake Mechanism

- Government Contracts for Difference and Feed-in Tariffs

- Corporate Power Purchase Agreements

- Merchant Wholesale Electricity Market Sales

- Regulated Utility Rate-Base Procurement

- Others

- Segmentation By Region

- Europe

- Asia-Pacific

- North America

- Latin America

- Middle East and Africa

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2036

Key Questions this Study Will Answer

- What is the projected global market valuation and installed capacity for floating offshore wind through 2036, segmented by floating substructure type, turbine rating, water depth class, component category, and region, and which technology platforms and geographic markets are expected to generate the highest incremental revenue and capacity addition across the forecast period?

- What is the levelized cost of energy trajectory for commercial-scale floating offshore wind projects across leading markets through 2036, and at what installed capacity milestones and supply chain development thresholds is floating wind projected to achieve cost parity with fixed-bottom offshore wind, enabling subsidy-independent commercial project deployment in the United Kingdom, Norway, South Korea, Japan, and the United States?

- How are the competing semi-submersible, spar-buoy, tension leg platform, and barge-type floating substructure concepts differentiating their technical and commercial propositions across water depth classes, turbine rating scales, and fabrication location constraints, and which platform configurations are projected to capture the largest share of commercial project deployments across the first and second waves of utility-scale floating wind development over the forecast period?

- What are the critical supply chain investment requirements, port infrastructure development gaps, and dynamic cable and mooring system manufacturing capacity constraints that are limiting the pace of commercial floating wind project deployment in leading markets, and what combinations of government infrastructure support, developer volume commitment frameworks, and supply chain consolidation strategies are most effective in resolving these constraints within the near-term project development pipeline?

- How are the consenting, environmental permitting, marine spatial planning, and offshore grid connection frameworks in the United Kingdom, Norway, France, South Korea, Japan, and the United States evolving to reduce development timeline uncertainty and enable the acceleration of floating wind project progression from site selection to financial close, and what regulatory reform priorities are most consequential for the pace of commercial project delivery across the forecast period?

- Who are the leading floating platform technology developers, offshore wind project developers, turbine original equipment manufacturers, dynamic cable suppliers, marine installation contractors, and operations and maintenance service providers currently defining the competitive landscape of the global floating offshore wind market, and what are their respective technology platform strategies, project development pipelines, geographic expansion priorities, and partnership structures for advancing floating wind from early commercial deployment toward utility-scale industrial activity through the forecast horizon?

- Product Definition

- Scope of the Study

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Industry Publications, Offshore Wind Developer & OEM Reports & Press Releases

- Government Energy, Maritime & Offshore Regulatory Authority Data (IEA, IRENA, GWEC, BOEM, Crown Estate, BEIS, etc.)

- Floating Offshore Wind Installed Capacity, Pipeline & LCOE Statistics

- Project Developer, EPC Contractor & Supply Chain Databases

- Primary Research Design & Execution

- In-depth Interviews with Floating Wind Developers, Turbine OEM Executives, Mooring & Subsea Specialists & Offshore EPC Contractors

- Surveys with Utility-Scale Investors, Grid Operators, Port Authorities & Offshore Service Vessel (OSV) Operators

- Expert Panel Validation

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Bottom-Up & Top-Down Reconciliation

- Project Pipeline Advancement, Award & Financial Close-Driven Market Sizing Model

- LCOE Reduction Trajectory & Technology Learning Rate Adjustment Framework

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Technology & Innovation Highlights

- Project Economics & Unit Economics Summary

- Average Project CAPEX & OPEX Benchmarks

- LCOE by Floater Type & Water Depth Comparison

- Spar-Buoy, Semi-Submersible & TLP Revenue & Capacity Model Summary

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Geographic & Regional Trends

- Risk Assessment Framework

- Geopolitical & Offshore Lease Licensing Policy Risk

- Supply Chain Bottleneck Risk (Steel, Mooring Chain, Dynamic Export Cable, Specialised Installation Vessels)

- Environmental, Seabed & Marine Ecology Regulatory Risk

- Financial / Project Financing & Merchant Price Risk

- Metocean Severity, Extreme Weather & Asset Integrity Risk

- Grid Connection, Curtailment & Offshore Transmission Infrastructure Risk

- Technology Readiness & First-of-a-Kind (FOAK) Project Execution Risk

- Regulatory Framework & Policy Standards

- Global Floating Offshore Wind Market Economics

- Project Development & Construction Economics Framework

- Capital Expenditure (CAPEX) Structure

- Operating Expenditure (OPEX) Structure

- Revenue Model & Monetisation Levers (CfD, PPA, Merchant, Hybrid)

- Capacity Factor, Availability & Annual Energy Production (AEP) Economics

- Payback Period & Return on Investment (ROI) Analysis

- Levelised Cost of Energy (LCOE) vs Fixed-Bottom Offshore Wind & Alternative Low-Carbon Generation

- Equipment & Component Cost Analysis

- Floating Foundation (Spar-Buoy, Semi-Submersible, TLP, Barge) Cost Trends (USD/MW, 2021–2035)

- Offshore Wind Turbine (Nacelle, Rotor, Tower) Cost Dynamics

- Mooring System (Catenary, Taut-Leg, Semi-Taut) & Anchor Cost Structure

- Dynamic Array & Export Cable Cost Analysis

- Offshore Substation & Floating Electrical Infrastructure Cost Structure

- Marine Spread, Heavy-Lift & Installation Vessel Day-Rate Economics

- Impact of Turbine Upscaling (15MW+) & Series Manufacturing on Project Economics

- Operations, Maintenance & Decommissioning Economics

- Offshore Access Strategy & Crew Transfer Vessel (CTV) / Service Operation Vessel (SOV) Cost Structure

- Condition Monitoring, Digital Twin & Predictive Maintenance Platform Economics

- Major Component Replacement (MCR) & Lifetime Extension Economics

- Floating Wind Farm Decommissioning Cost Estimation Framework

- Regulatory & Standards Compliance Economics

- Offshore Wind Design & Certification Standards Compliance Cost Benchmarks (DNV, GL, IEC, DNVGL-ST-0119, etc.)

- Environmental Impact Assessment (EIA), Marine Spatial Planning & Permitting Cost Structure

- Decommissioning Bond, Financial Assurance & End-of-Life Obligation Compliance Costs

- Global Floating Offshore Wind Market Outlook

- Market Size & Forecast by Value (USD Billion, 2021–2036)

- Market Size & Forecast by Installed Capacity (GW, 2021–2036)

- Market Size & Forecast by Floater / Foundation Type

- Semi-Submersible

- Spar-Buoy

- Tension Leg Platform (TLP)

- Barge / Pontoon

- Others (Multi-Purpose, Hybrid & Novel Concepts)

- Market Size & Forecast by Turbine Capacity

- Up to 8MW

- 8MW–12MW

- 12MW–15MW

- 15MW–20MW

- Above 20MW (Next-Generation Ultra-Large Turbines)

- Market Size & Forecast by Water Depth

- 50m–100m (Transitional)

- 100m–200m

- 200m–500m

- Above 500m (Deep Water)

- Market Size & Forecast by Mooring System Type

- Catenary Mooring

- Taut-Leg Mooring

- Semi-Taut Mooring

- Tension Leg Mooring

- Others (Hybrid & Novel Mooring Systems)

- Market Size & Forecast by Array & Export Cable Type

- Dynamic Inter-Array Cables

- Static Inter-Array Cables

- Dynamic Export Cables

- Static Export Cables

- High-Voltage Direct Current (HVDC) Export Systems

- Market Size & Forecast by Project Stage

- Operational

- Under Construction

- Consented / Permitted

- Pre-Construction & Development

- Concept & Feasibility

- Market Size & Forecast by Application

- Utility-Scale Grid-Connected Power Generation

- Offshore Green Hydrogen & Electrolysis Production

- Hybrid Offshore Energy Systems (Wind + Solar + Storage)

- Island & Remote Community Electrification

- Offshore Oil & Gas Platform Electrification (Powering from Shore)

- Others (Desalination, Aquaculture Integration, Research & Demonstration)

- Market Size & Forecast by End-Use Sector

- Utility & Independent Power Producers (IPPs)

- Global Integrated Utilities & Offshore Wind Developers (Equinor, Ørsted, RWE, Vattenfall, EDP, etc.)

- Regional & Emerging Market IPPs & Project Developers

- Oil & Gas Companies Transitioning to Offshore Wind

- Supermajors & National Oil Companies (Shell, BP, TotalEnergies, Petrobras, Equinor, etc.)

- National Oil Company (NOC) Offshore Energy Transition Programmes

- Government & Public Sector Energy Agencies

- Industrial & Commercial Off-Takers

- Large Industrials, Steel, Chemicals & Green Hydrogen Producers Pursuing Corporate PPAs

- Data Centre Operators & Technology Companies with Renewable Energy Targets

- Others (Research Institutions, Port Authorities, Maritime Operators)

- Utility & Independent Power Producers (IPPs)

- Market Size & Forecast by Offtake & Revenue Structure

- Contract for Difference (CfD) & Feed-in Tariff (FiT)

- Power Purchase Agreement (PPA) – Corporate & Utility

- Merchant / Subsidy-Free

- Regulated Asset Base (RAB) Model

- Hybrid Revenue Structures

- Market Size & Forecast by Sales & Procurement Channel

- Government-Run Offshore Wind Lease & Auction Rounds

- Direct Developer-to-OEM & EPC Contractor Procurement

- Joint Venture & Consortium Project Development

- Competitive Tender & Pre-Qualified Supplier Frameworks

- Bilateral Investment & Strategic Partnership Agreements

- Asia-Pacific Floating Offshore Wind Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Installed Capacity (GW)

- By Floater / Foundation Type

- By Turbine Capacity

- By Water Depth

- By Mooring System Type

- By Array & Export Cable Type

- By Project Stage

- By Application

- By End-Use Sector

- By Offtake & Revenue Structure

- By Sales & Procurement Channel

- Key Demand Drivers (APAC-Specific)

- Competitive Landscape (APAC)

- Europe Floating Offshore Wind Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Installed Capacity (GW)

- By Floater / Foundation Type

- By Turbine Capacity

- By Water Depth

- By Mooring System Type

- By Array & Export Cable Type

- By Project Stage

- By Application

- By End-Use Sector

- By Offtake & Revenue Structure

- By Sales & Procurement Channel

- Key Demand Drivers (Europe-Specific)

- Competitive Landscape (Europe)

- North America Floating Offshore Wind Market Outlook

- Market Overview & Strategic Importance

- Market Size & Forecast

- By Value (2020–2035)

- By Installed Capacity (GW)

- By Floater / Foundation Type

- By Turbine Capacity

- By Water Depth

- By Mooring System Type

- By Array & Export Cable Type

- By Project Stage

- By Application

- By End-Use Sector

- By Offtake & Revenue Structure

- By Sales & Procurement Channel

- Key Demand Drivers (North America-Specific)

- Competitive Landscape (North America)

- Latin America Floating Offshore Wind Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Installed Capacity (GW)

- By Floater / Foundation Type

- By Turbine Capacity

- By Water Depth

- By Mooring System Type

- By Array & Export Cable Type

- By Project Stage

- By Application

- By End-Use Sector

- By Offtake & Revenue Structure

- By Sales & Procurement Channel

- Key Demand Drivers (LATAM-Specific)

- Competitive Landscape (LATAM)

- Middle East & Africa Floating Offshore Wind Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Installed Capacity (GW)

- By Floater / Foundation Type

- By Turbine Capacity

- By Water Depth

- By Mooring System Type

- By Array & Export Cable Type

- By Project Stage

- By Application

- By End-Use Sector

- By Offtake & Revenue Structure

- By Sales & Procurement Channel

- Key Demand Drivers (MEA-Specific)

- Competitive Landscape (MEA)

- Country-Wise Floating Offshore Wind Market Outlook

- Market Size & Forecast by Country

- By Value

- By Installed Capacity (GW)

- By Floater / Foundation Type

- By Turbine Capacity

- By Water Depth

- By Mooring System Type

- By Array & Export Cable Type

- By Project Stage

- By Application

- By End-Use Sector

- By Offtake & Revenue Structure

- By Sales & Procurement Channel

- Market Size & Forecast by Country

- Market Size & Forecast

- Market Size & Forecast

- Market Size & Forecast

- Market Size & Forecast

- Project Development & Construction Economics Framework

Countries Covered: United Kingdom, Norway, France, Portugal, Spain, Italy, Germany, Denmark, Netherlands, Japan, South Korea, China, United States, Canada, Brazil, Australia, India, Taiwan, Ireland, Greece

- Technology Landscape & Innovation Analysis

- Floating Offshore Wind Technology Maturity Assessment

- Emerging & Disruptive Technologies in Floating Wind

- Next-Generation Floating Foundation Concepts: Steel vs Concrete vs Hybrid Structures

- Offshore Wind Turbine Upscaling: 15MW to 20MW+ Rotor, Drivetrain & Generator Technology Roadmap

- Dynamic Export Cable & Wet-Mate Connector Technology Innovations

- Floating Offshore Substation & HVDC Converter Platform Technology Developments

- Offshore Green Hydrogen Integration: Electrolyser Co-location, Offshore Pipeline & Ammonia Carrier Systems

- Digital Twin, Remote Inspection, Autonomous Underwater Vehicle (AUV) & AI-Driven O&M Technology

- Technology Readiness & Commercialisation Matrix – Key Floating Offshore Wind Technologies

- Patent Landscape Analysis

- R&D Investment Benchmarking

- Value Chain & Supply Chain Analysis

- Floating Offshore Wind Value Chain Mapping

- Supply Chain Concentration & Dependency Analysis

- Key Supplier Mapping by Component & Technology Programme

- Floating Foundation Fabricator & Steel / Concrete Supplier Mapping

- Offshore Wind Turbine OEM & Drivetrain Component Supplier Mapping

- Mooring Chain, Fibre Rope & Anchor Manufacturer Mapping

- Dynamic Cable, Umbilical & Subsea Connector Supplier Mapping

- Marine Spread, Heavy-Lift Vessel & Installation Contractor Mapping

- Supplier Risk Heat Map

- Make vs Buy Strategy Trends Among Floating Wind Developers & EPC Contractors

- Pricing Analysis

- Floating Offshore Wind Project Pricing Dynamics & Mechanisms

- LCOE & CAPEX Benchmarking by Floater Type, Turbine Capacity & Water Depth

- Total Cost of Ownership (TCO) Analysis – Including Construction, O&M, Grid Connection & Decommissioning

- CfD Strike Price vs Merchant PPA Price Trends & Benchmarks by Market

- Floating Wind vs Fixed-Bottom Offshore Wind vs Onshore Wind vs Solar PV LCOE Comparison

- Sustainability & Environmental Stewardship

- Environmental & Sustainability Landscape in Floating Offshore Wind Development

- Carbon Footprint & Life-Cycle GHG Emissions Benchmarking Across Floater Types & Project Configurations

- Marine Ecosystem, Seabed Habitat & Biodiversity Impact Assessment

- Floating Wind’s Contribution to Net-Zero Targets, Energy Security & Green Hydrogen Economy

- Recyclability of Floating Foundations, Turbine Blades & Mooring Materials: Circular Economy Pathway

- ESG Reporting & Lifecycle Assessment (LCA) in Floating Offshore Wind Project Development

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level: Global Integrated Utilities & Oil Majors vs Pure-Play Offshore Wind Developers & Startups

- Top 5 Floating Offshore Wind Developers & Technology Providers Market Capacity Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis by Floater Type, Application & Region

- Competitive Intensity Map by Segment & Region

- Player Classification

- Tier-1 Global Integrated Offshore Wind Developers & Utilities with Floating Wind Portfolios

- Tier-2 Specialist Floating Foundation Technology Providers, Turbine OEMs & EPC Contractors

- Emerging Floating Wind Startups, University Spin-offs & Technology Demonstrator Operators

- Emerging & Disruptive Players

- Competitive Analysis Frameworks

- Market Share Analysis by Installed & Pipeline Capacity, Technology Type & Geography

- R&D Intensity & Technology Platform Breadth Benchmarking

- Project Pipeline Size, CfD/Auction Win Portfolio & Offtake Agreement Comparison

- Geographic Revenue Exposure & Lease Portfolio Comparison

- Company Profiles

- Company Overview, HQ & Organisational Structure

- Floating Offshore Wind Technology Platform, Foundation Type & Project Portfolio

- Revenue Breakdown

- Key Projects, CfD Wins, Joint Ventures & Offtake Agreements

- Manufacturing Footprint, Port Infrastructure & Key Facilities

- Recent Developments (M&A, Partnerships, New Projects, Financial Results)

- SWOT Analysis

- Strategic Focus: Floater Commercialisation, Turbine Upscaling, Green Hydrogen Integration & Lease Round Expansion

- Strategic Output

- Market Opportunity Matrix

- High-Value Opportunity Quadrant Analysis

- Addressable Market by Floater Type, Application & Region

- Time-to-Revenue Assessment by Opportunity

- White Space Opportunity Analysis

- Underserved Water Depth, Application & Geographic Market Gaps

- Geographic Markets with Low Floating Wind Penetration & High Resource Potential

- Technology & Supply Chain Gaps with High Commercialisation Potential

- Customer Segment & Offtake Unmet Needs

- Strategic Recommendations

- Project Portfolio & Technology Platform Strategy

- Technology Innovation & Turbine Upscaling Strategy

- Manufacturing, Port Infrastructure & Fabrication Yard Capacity Expansion Strategy

- Offtake, Revenue Certainty & Grid Integration Strategy

- Pricing, LCOE Reduction & Commercial Strategy

- Sustainability, Environmental Compliance & Marine Stewardship Strategy

- Supply Chain Localisation, Resilience & Sourcing Strategy

- Partnership, M&A & Consortium Development Strategy

- Regional Growth & Lease Round Participation Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-Term (2025–2028)

- Mid-Term (2029–2032)

- Long-Term (2033–2036)

- Market Opportunity Matrix

- Market Structure & Concentration