Market Definition

The Global Methane Monitoring and Emissions Technologies Market encompasses the development, manufacturing, deployment, calibration, and lifecycle management of sensor systems, atmospheric measurement instruments, airborne and satellite-based remote sensing platforms, software analytics engines, and emissions quantification services specifically designed to detect, locate, measure, attribute, and report methane emissions from anthropogenic and natural sources across the oil and gas value chain, coal mining operations, agricultural systems, municipal solid waste landfills, wastewater treatment infrastructure, and natural wetland and permafrost environments whose methane flux contributes to global greenhouse gas inventories. The product and service scope of this market includes point-source continuous emissions monitoring systems incorporating electrochemical, optical absorption, cavity ring-down spectroscopy, and tunable diode laser absorption spectroscopy sensor technologies for facility-level methane concentration and flux measurement at compressor stations, processing plants, wellheads, and pipeline metering stations, mobile survey platforms integrating high-sensitivity methane analyzers with global positioning systems and meteorological sensors aboard ground vehicles, marine vessels, and manned aircraft for emission source identification and quantification across distributed asset networks, uncrewed aerial vehicle-mounted methane detection systems enabling targeted survey of individual equipment components and facility perimeters at spatial resolutions inaccessible to ground or fixed-wing platforms, fixed-wing and helicopter airborne measurement systems carrying open-path Fourier transform infrared spectrometers, laser dispersion spectrometers, and imaging spectrometers capable of detecting and mapping methane plumes across large industrial areas and agricultural landscapes in a single survey pass, satellite-based methane monitoring systems spanning low-earth orbit hyperspectral imaging sensors, shortwave infrared spectrometers, and thermal infrared instruments aboard dedicated commercial methane monitoring satellites, multi-mission government science satellites, and cubesat constellations providing near-daily global revisit capability for persistent methane plume detection and super-emitter attribution, atmospheric inversion modeling systems that assimilate surface monitoring network data, airborne measurement profiles, and satellite column retrievals within chemical transport models to produce spatially resolved methane emission flux estimates at regional and national scales for greenhouse gas inventory verification and emissions trend attribution, leak detection and repair program management software platforms that integrate multi-source measurement data streams, equipment inspection records, emissions factor libraries, and regulatory reporting requirements to support continuous improvement of methane abatement programs at operating companies, and the methane emissions quantification, third-party verification, and emissions intensity certification services that oil and gas producers, agricultural commodity buyers, and emissions trading scheme administrators require to support commercially credible methane performance reporting and the monetization of methane emission reductions through carbon credit and low-carbon commodity premium markets. The technology landscape spans in-situ contact sensor technologies operating at the component and facility level, active and passive optical remote sensing systems operating from ground, airborne, and spaceborne vantage points, and the data integration, artificial intelligence-assisted plume detection, and atmospheric dispersion modeling software that converts raw measurement signals into actionable emissions quantification and attribution intelligence across spatial scales from individual equipment valves to national greenhouse gas inventory domains. The value chain of this market extends from optical component, photodetector, laser source, and semiconductor gas sensor element manufacturers through methane detection instrument and sensor system developers, satellite platform operators and data downlink infrastructure providers, software analytics and artificial intelligence platform developers, emissions measurement and verification service providers, regulatory consultancy organizations, and the oil and gas operators, agricultural producers, utilities, waste management companies, national environmental agencies, and voluntary carbon market administrators whose measurement, reporting, and verification obligations and commercial incentives define the demand structure and investment pace of this rapidly expanding technology market globally.

Market Insights

The global methane monitoring and emissions technologies market is experiencing a period of exceptional commercial momentum in 2026, characterized by the simultaneous maturation of multiple complementary measurement technology platforms, the progressive implementation of mandatory methane measurement and reporting regulations in the United States, European Union, and a growing number of major hydrocarbon-producing nations, and the rapidly expanding commercial market for methane emissions intensity certification that is enabling oil and gas producers and agricultural commodity suppliers to capture price premiums for demonstrably low-methane products in buyer markets that are progressively incorporating emissions performance criteria into procurement and investment decisions. The global methane monitoring and emissions technologies market was valued at approximately USD 5.2 billion in 2025 and is projected to expand at a compound annual growth rate of 19 percent through 2036, reaching approximately USD 32 billion by the end of the forecast period, a trajectory driven by the structural expansion of regulatory measurement and reporting obligations across the oil and gas, agriculture, coal mining, and waste sectors in major economies, the declining unit cost and improving sensitivity of satellite-based methane detection capability that is creating a persistent global monitoring infrastructure accessible to regulators, investors, and non-governmental organizations independently of operator-reported emissions data, and the growing commercial value of methane emission reductions monetized through carbon credit markets and differentiated commodity pricing mechanisms that are incentivizing voluntary investment in methane monitoring and abatement technology beyond mandatory compliance requirements. The competitive landscape of the market encompasses specialist methane detection instrument manufacturers, diversified environmental monitoring equipment companies, satellite data analytics companies operating commercial methane monitoring satellite constellations, major technology corporations deploying artificial intelligence platforms for methane plume detection and attribution in satellite and airborne imagery, engineering service companies providing integrated methane measurement and verification services, and national metrology institutes and accreditation bodies whose reference measurement standards and calibration infrastructure underpin the technical credibility of the entire measurement ecosystem.

A defining technological development reshaping the commercial structure and competitive dynamics of the methane monitoring market is the rapid maturation and commercial deployment of dedicated methane monitoring satellite constellations by multiple commercial operators, which are collectively creating a persistent, globally comprehensive, and independently verifiable methane emissions observation infrastructure that is fundamentally transforming the information environment within which regulators, investors, commodity buyers, and the general public evaluate the credibility of operator-reported methane emissions performance. The first generation of commercial methane monitoring satellites, equipped with shortwave infrared spectrometers capable of detecting methane plume column enhancements above large point sources at horizontal resolutions of tens of meters, demonstrated the ability to identify and attribute major methane super-emitters at oil and gas facilities, coal mines, and landfills across every major hydrocarbon-producing region globally, including facilities in countries and jurisdictions where ground-level regulatory oversight and emissions reporting obligations were limited or entirely absent. The second generation of commercial methane monitoring satellites advancing toward and entering deployment in the 2024 to 2026 period is delivering substantial improvements in spatial resolution, sensitivity threshold, and daily revisit frequency that are extending the detection capability from the largest point-source super-emitters to a substantially wider population of smaller emission sources across distributed oil and gas gathering and transmission infrastructure, enabling persistent monitoring of emission trends at individual facility level and providing the measurement data density required to support scientifically defensible regional methane flux estimates that can be compared against national inventory submissions to greenhouse gas reporting frameworks. The proliferation of satellite methane monitoring capability is simultaneously creating commercial opportunities for data analytics platform companies that transform raw satellite measurement data into actionable emissions intelligence products for oil and gas company asset management teams, environmental compliance departments, and investor relations organizations, and creating competitive pressure on operating companies to invest in ground-level continuous monitoring infrastructure that can detect and remediate emission events before they are identified and publicly reported through satellite observation channels.

The regulatory landscape governing methane emissions measurement, reporting, and abatement has undergone transformative change across major emitting sectors and jurisdictions over the preceding three years, creating the most significant expansion in mandatory methane monitoring obligations since the establishment of the first greenhouse gas reporting programs, and generating a large and structurally durable demand stream for methane measurement technology and verification services that is providing the investment confidence required to sustain the commercial development and manufacturing scale-up of the full range of methane monitoring technology platforms. The United States Environmental Protection Agency Methane Emissions Reduction Program, which applies waste emissions charges to oil and gas facilities exceeding defined methane emissions intensity thresholds and requires the deployment of advanced monitoring technologies for leak detection and repair across the upstream, midstream, and downstream oil and gas sectors, represents the most financially consequential regulatory driver of methane monitoring technology investment in the North American market, with the waste emissions charge creating a direct financial incentive for facility operators to invest in continuous monitoring systems capable of detecting and quantifying emission events at detection limits below the charge threshold and enabling rapid remediation before cumulative emissions accumulate to charge-triggering levels. The European Union Methane Regulation, which entered into force in 2024 and applies progressive measurement, reporting, and verification requirements to European oil, gas, and coal imports as well as domestic production, is creating a compliance-driven demand for third-party measurement and verification services, emissions quantification methodology development, and supply chain methane monitoring capabilities that extends the European regulatory reach to hydrocarbon-producing nations in North Africa, Central Asia, the Middle East, and Sub-Saharan Africa whose production feeds European energy markets. The alignment of national methane pledges made under the Global Methane Pledge with the technical measurement and verification infrastructure required to demonstrate pledge compliance is creating sustained government procurement of atmospheric monitoring network infrastructure, mobile measurement capability, and methane inventory verification modeling services across the more than 150 signatory countries whose emissions reduction commitments require credible measurement systems to track and verify.

From a regional perspective, North America, and specifically the United States and Canada, represents the largest and most commercially mature national market for methane monitoring and emissions technologies, driven by the combination of the largest oil and gas producing infrastructure base of any single country, the most developed regulatory framework for methane emissions measurement and reporting, a large and technically sophisticated community of commercial methane measurement service providers and technology developers, and the active participation of major oil and gas operating companies in voluntary industry initiatives such as the Oil and Gas Methane Partnership 2.0 and the Methane Guiding Principles whose performance commitments are driving investment in advanced continuous monitoring infrastructure across upstream and midstream asset portfolios. Europe represents the most significant near-term growth market for methane monitoring technology investment attributable to new regulatory requirements, with the European Union Methane Regulation creating mandatory measurement and reporting obligations for the European energy sector and creating substantial near-term demand for third-party measurement service providers, monitoring instrument suppliers, and software platforms capable of supporting the multi-source data integration and transparent reporting workflows required for regulatory compliance across complex multi-jurisdiction supply chains. Asia-Pacific, led by Australia, China, and the major Southeast Asian hydrocarbon-producing nations, represents a large and growing market for methane monitoring technology where the expansion of liquefied natural gas production and export infrastructure, the progressive adoption of domestic greenhouse gas reporting frameworks, and the incorporation of methane performance criteria into liquefied natural gas supply agreements by Asian utility buyers are creating commercial demand for facility-level continuous emissions monitoring, airborne survey services, and satellite data products that provide the emissions measurement evidence base required to support commercially credible low-methane liquefied natural gas marketing. The agricultural sector, representing the largest single source of anthropogenic methane emissions from enteric fermentation in livestock and flooded rice cultivation, is emerging as an important and structurally growing application segment for methane monitoring technology as agricultural supply chain decarbonization commitments from major food and beverage companies drive investment in farm-level methane measurement programs for cattle, dairy, and rice production systems across North America, Europe, Australia, and Latin America.

Key Drivers

Escalating Mandatory Methane Measurement and Reporting Regulations Across the Oil and Gas and Agricultural Sectors Creating Structural Compliance-Driven Demand for Monitoring Technologies

The most structurally consequential and commercially durable demand driver for methane monitoring and emissions technologies is the accelerating implementation of mandatory methane measurement, reporting, and verification regulations across the largest emitting sectors in major hydrocarbon-producing and consuming economies, regulations that are converting the previously discretionary investment in methane monitoring infrastructure into a non-negotiable compliance expenditure category for oil and gas operators, coal mining companies, landfill operators, and agricultural producers subject to the new legal requirements and their associated financial penalty frameworks. The United States Environmental Protection Agency Methane Emissions Reduction Program’s waste emissions charge mechanism, which imposes progressive financial charges on methane emissions from covered oil and gas facilities based on the volume of methane emitted above defined intensity thresholds measured through approved quantification methodologies, represents a regulatory design that directly monetizes the commercial value of methane monitoring investment by enabling operators to reduce their waste emissions charge liability through the deployment of monitoring systems capable of detecting and quantifying emission events at detection limits sufficient to identify and remediate sub-threshold emission sources before they accumulate to charge-triggering emission levels. The regulatory requirement for continuous emissions monitoring at covered facilities as an alternative to periodic equipment survey under traditional leak detection and repair programs is driving demand for facility-level continuous monitoring system installations across tens of thousands of compressor stations, processing plants, gathering system facilities, and storage terminals that are subject to the advanced monitoring technology requirements of the updated new source performance standards and their equivalent state-level implementation regulations. The European Union Methane Regulation’s requirements for measurement, reporting, and verification of methane emissions from oil, gas, and coal imported into the European Union, which entered into force in a phased implementation timeline through 2025 and 2026, are creating mandatory compliance obligations for hydrocarbon-exporting nations and their producing companies that extend the European regulatory framework’s practical reach to the upstream production assets of North African, Middle Eastern, Central Asian, and West African suppliers whose export contracts with European buyers are now conditioned on the demonstration of measurement-verified methane performance credentials that meet the technical specifications of the European regulatory measurement and reporting framework.

Growing Commercial Value of Methane Emission Reductions Monetized Through Carbon Markets and Low-Methane Commodity Premiums Driving Voluntary Investment Beyond Mandatory Compliance

The expanding commercial ecosystem for the monetization of methane emission reductions through voluntary carbon credit markets, compliance carbon trading schemes, and differentiated commodity pricing premiums is creating a powerful demand driver for methane monitoring and emissions verification technologies that operates in parallel with and additive to the mandatory compliance driver, incentivizing investment in monitoring infrastructure by operators who perceive the commercial value of credibly quantified methane reduction credits and low-methane commodity certifications as sufficient to justify monitoring technology expenditures that generate positive financial returns beyond mere regulatory penalty avoidance. The voluntary carbon market for methane emission reduction credits, which prices the global warming potential equivalence of methane relative to carbon dioxide at a substantial premium reflecting the higher near-term climate forcing of methane, is creating financially significant credit generation opportunities for oil and gas operators, agricultural producers, and landfill operators who can demonstrate credible, measurement-verified methane emission reductions against appropriate baselines using monitoring methodologies that satisfy the additionality, permanence, and measurement uncertainty requirements of carbon credit certification standards recognized by voluntary carbon market buyers. The differentiated natural gas market for low-methane-intensity certified gas, in which producers supplying pipeline natural gas or liquefied natural gas with independently verified methane emissions intensity credentials below defined threshold values can command price premiums from utility buyers, industrial consumers, and liquefied natural gas importers who incorporate natural gas supply chain methane performance into their own scope three emissions reporting and net-zero commitment strategies, is creating a recurring commercial incentive for continuous methane monitoring investment at upstream and midstream natural gas infrastructure that enables the maintenance of the measurement-verified low-methane credentials required for premium pricing qualification across the production and transportation chain from wellhead to delivery point. The emerging agricultural methane credit market, in which livestock producers, rice farmers, and manure management facility operators can generate carbon credits for verified methane emission reductions achieved through feed additives, water management practices, and manure processing technology adoption, is creating farm-level demand for methane flux measurement systems and remote sensing tools capable of providing the measurement data required to support carbon credit issuance under approved agricultural methane quantification methodologies.

Key Challenges

Measurement Uncertainty and Intercomparability Limitations Constraining the Scientific and Regulatory Credibility of Methane Quantification Across Technology Platforms and Spatial Scales

The most fundamental technical and commercial challenge limiting the full realization of the methane monitoring market’s potential for enabling credible, actionable, and legally defensible emissions quantification is the significant and incompletely characterized measurement uncertainty that affects all operational methane monitoring technology platforms across the range of atmospheric conditions, source geometries, emission rates, and co-pollutant backgrounds encountered in real-world deployment environments, uncertainties that constrain the comparability of results between different measurement approaches and limit the regulatory and commercial confidence with which methane quantification data generated by novel monitoring technologies can be used as the primary basis for compliance determination, financial penalty assessment, and carbon credit issuance at individual facility and regional scales. The measurement uncertainty challenge is multidimensional in character, arising from fundamental limitations in sensor calibration traceability to national measurement standards for atmospheric methane concentration in complex multi-component gas matrices, from the challenge of accurately reconstructing spatially integrated emission fluxes from point concentration measurements using atmospheric dispersion models whose accuracy is sensitive to wind field characterization at spatial and temporal resolutions that are practically difficult to achieve in remote and complex terrain environments, from the variable detection and quantification performance of airborne and satellite remote sensing systems under differing atmospheric water vapor loading, aerosol optical depth, surface albedo, and solar zenith angle conditions that affect instrument sensitivity and retrieval algorithm accuracy in ways that are partially correctable through retrieval scheme refinement but remain a source of systematic uncertainty in cross-site and cross-season emission comparisons. The intercomparability challenge between different measurement technology platforms, which has been documented through multiple controlled release experiments and blind intercomparison studies in which different instrument systems deployed simultaneously at the same facility have returned emission rate estimates spanning an order of magnitude for the same source, creates fundamental difficulties for regulatory frameworks seeking to use any single approved technology as the authoritative measurement basis for compliance determination without independent verification through complementary measurement approaches. National metrology institutes, international standards organizations, and joint government and industry measurement programs are investing in the development of primary calibration standards, certified reference materials, and standardized intercomparison protocols for methane monitoring systems, but the translation of improved measurement standards into regulatory-grade uncertainty specifications for the full diversity of deployed monitoring technologies will require sustained investment across a multi-year development and validation timeline that represents a persistent near-term limitation on the regulatory application of advanced monitoring technology outputs.

Highly Fragmented and Technically Complex Methane Source Landscape Creating Deployment Cost and Operational Scalability Barriers for Comprehensive Emissions Monitoring Programs

A structurally significant commercial challenge limiting the pace of comprehensive methane monitoring program deployment across the oil and gas, agriculture, coal, and waste sectors is the extraordinary spatial fragmentation and technical heterogeneity of the anthropogenic methane source landscape, which encompasses millions of geographically dispersed emission points spanning individual wellheads, pipeline valves, and compressor seals in oil and gas systems, billions of individual livestock animals across continental-scale agricultural production systems, thousands of abandoned and active coal mine ventilation shafts and coal seam outgassing points, and tens of thousands of municipal solid waste landfill cells whose surface methane flux varies at meter-scale spatial resolution in response to waste composition, moisture content, compaction history, and cover material integrity in ways that make spatially representative monitoring technically demanding and operationally expensive to achieve at the national inventory scale required for credible greenhouse gas reporting. The cost of deploying and maintaining continuous monitoring infrastructure at the density required to achieve statistically representative facility-level methane emission quantification at the millions of individual oil and gas facilities across the United States, Canada, the Middle East, Russia, and Central Asia whose aggregate emissions constitute the majority of the global oil and gas methane budget is substantially beyond the operational monitoring expenditure budgets of the majority of producing companies, particularly smaller independent operators and national oil companies in developing economies with limited environmental management resources and competing capital allocation priorities. The operational scalability challenge for facility-level continuous monitoring is compounded by the maintenance and calibration burden associated with sensor drift, contamination, and physical damage in remote and harsh environment installations where the combination of temperature extremes, humidity cycles, particulate contamination from dust and production aerosols, and physical interference from wildlife and equipment operation requires systematic sensor maintenance programs that add operational cost and logistical complexity to monitoring programs covering large numbers of geographically dispersed installations. The integration of data streams from heterogeneous monitoring technology platforms, including point sensors, mobile survey results, airborne measurement campaign data, and satellite observations, each with different spatial resolutions, temporal sampling frequencies, measurement uncertainties, and data format conventions, into coherent facility-level and regional emission inventories that support regulatory reporting and carbon accounting creates a data management and quality assurance challenge that requires substantial investment in software platform development, data engineering infrastructure, and technical workforce capability that represents a meaningful operational cost barrier for smaller operators and public sector monitoring agencies with limited technology investment budgets.

Market Segmentation

- Segmentation By Technology Platform

- Continuous Emissions Monitoring Systems (CEMS)

- Optical Gas Imaging Cameras

- Cavity Ring-Down Spectroscopy (CRDS) Analyzers

- Tunable Diode Laser Absorption Spectroscopy (TDLAS) Systems

- Open-Path Fourier Transform Infrared (OP-FTIR) Spectrometers

- Laser Dispersion Spectroscopy Systems

- Metal Oxide Semiconductor (MOS) Sensor Arrays

- Electrochemical Methane Sensors

- Photoacoustic Spectroscopy Sensors

- Satellite-Based Hyperspectral and SWIR Methane Instruments

- Uncrewed Aerial Vehicle (UAV) Methane Detection Systems

- Airborne Measurement and Flux Quantification Systems

- Atmospheric Inversion Modeling and Data Assimilation Systems

- Others

- Segmentation By Monitoring Approach

- Fixed-Point Continuous Facility-Level Monitoring

- Periodic Mobile Ground Survey

- Airborne Survey Campaigns

- Satellite Persistent Observation

- Fence-Line Perimeter Monitoring

- Flux Chamber and Eddy Covariance Measurement

- Atmospheric Inversion and Top-Down Quantification

- Others

- Segmentation By Application

- Leak Detection and Repair (LDAR) Programs

- Regulatory Compliance Monitoring and Reporting

- Carbon Credit Quantification and Verification

- Methane Emissions Intensity Certification

- Super-Emitter Detection and Attribution

- National Greenhouse Gas Inventory Verification

- Voluntary Emissions Disclosure and ESG Reporting

- Methane Abatement Program Performance Tracking

- Supply Chain Emissions Transparency and Due Diligence

- Others

- Segmentation By Emitting Sector

- Upstream Oil and Gas (Exploration and Production)

- Midstream Oil and Gas (Gathering, Processing, and Transmission)

- Downstream Oil and Gas (Refining and Distribution)

- Liquefied Natural Gas (LNG) Production and Export Terminals

- Coal Mining (Active and Abandoned Mines)

- Livestock and Enteric Fermentation (Agriculture)

- Manure Management and Agricultural Waste Systems

- Flooded Rice Cultivation

- Municipal Solid Waste Landfills

- Wastewater Treatment Infrastructure

- Natural Wetlands and Permafrost Systems

- Others

- Segmentation By Spatial Coverage Scale

- Component and Equipment Level

- Facility and Site Level

- Asset Portfolio and Basin Level

- Regional and National Level

- Global and Satellite Observation Level

- Segmentation By End User

- Oil and Gas Exploration and Production Companies

- Midstream Pipeline and Processing Operators

- LNG Producers and Exporters

- Coal Mining Companies

- Agricultural Producers and Agribusiness Companies

- Waste Management and Landfill Operators

- National Environmental Regulatory Agencies

- Carbon Market Administrators and Verification Bodies

- Energy and Commodity Investors

- Non-Governmental Organizations and Research Institutions

- Others

- Segmentation By Component

- Methane Detection Hardware and Sensor Systems

- Data Acquisition and Telemetry Infrastructure

- Emissions Quantification and Analytics Software

- Satellite Data and Imagery Products

- Measurement and Verification Services

- Regulatory Reporting and Compliance Management Platforms

- Calibration, Maintenance, and Field Services

- Others

- Segmentation By Deployment Mode

- On-Premises Hardware Installation

- Cloud-Based Data and Analytics Platform

- Monitoring-as-a-Service (MaaS)

- Satellite Data Subscription Services

- Hybrid On-Premises and Cloud Integrated Systems

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2036

Key Questions this Study Will Answer

- What is the projected global market valuation for methane monitoring and emissions technologies through 2036, segmented by technology platform, monitoring approach, application, emitting sector, spatial coverage scale, and region, and which technology categories and geographic markets are expected to generate the highest incremental revenue and adoption growth across the forecast period?

- How are the mandatory methane measurement and reporting requirements of the United States Environmental Protection Agency Methane Emissions Reduction Program, the European Union Methane Regulation, and equivalent national regulatory frameworks being implemented across the oil and gas, coal, agriculture, and waste sectors, and what are the projected compliance technology investment volumes and monitoring system deployment timelines that these regulatory obligations are creating across major hydrocarbon-producing and consuming regions?

- What is the commercial development trajectory of dedicated commercial methane monitoring satellite constellations, how are competing satellite operators differentiating their spatial resolution, revisit frequency, detection sensitivity, and data analytics service offerings, and how is the proliferation of independent satellite methane observation capability reshaping the information environment and competitive dynamics between operators, regulators, investors, and non-governmental organizations in the global methane accountability ecosystem?

- How are measurement uncertainty characterization, cross-platform intercomparability validation, and regulatory-grade calibration standard development programs advancing across national metrology institutes, international standards bodies, and joint industry measurement programs, and what are the projected timelines for the establishment of harmonized measurement uncertainty specifications and approved quantification methodologies that would enable advanced monitoring technologies to serve as the primary regulatory compliance determination basis across major emissions reporting jurisdictions?

- What is the projected scale and geographic distribution of voluntary methane monitoring investment driven by carbon credit market monetization, low-methane commodity premium certification, Oil and Gas Methane Partnership 2.0 performance commitments, and scope three supply chain emissions due diligence requirements, and how are the financial returns from methane credit issuance and certified gas premiums comparing with the capital and operational costs of the continuous monitoring infrastructure required to generate and sustain commercially credible measurement-verified emissions performance credentials?

- Who are the leading methane detection instrument manufacturers, satellite methane monitoring operators, airborne and drone survey service providers, emissions analytics software platform developers, and third-party measurement and verification service organizations currently defining the competitive landscape of the global methane monitoring and emissions technologies market, and what are their respective technology differentiation strategies, regulatory approval roadmaps, sector vertical focus areas, and partnership structures with oil and gas operators, agricultural commodity companies, and carbon market administrators for advancing methane monitoring from a compliance-driven cost center toward a commercially productive emissions intelligence and carbon value generation capability across the forecast horizon?

- Product Definition

- Scope of the Study

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Industry Publications, Environmental Monitoring OEM Reports, Scientific Journals & Press Releases

- Government Environmental, Climate & Energy Regulatory Authority Data (EPA, IEA, UNFCCC, UNEP, EC DG CLIMA, CCAC, etc.)

- Methane Emissions Inventory, Detection Technology Deployment & Regulatory Compliance Statistics

- Oil & Gas Operator, Agricultural Sector & Waste Management Procurement & Emissions Reporting Databases

- Primary Research Design & Execution

- In-depth Interviews with Methane Monitoring Technology Developers, Environmental Compliance Officers, Regulatory Affairs Specialists & Remote Sensing Experts

- Surveys with Oil & Gas Operators, Agricultural Producers, Waste Management Companies, Utilities & Government Environmental Agencies

- Expert Panel Validation

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Bottom-Up & Top-Down Reconciliation

- Regulatory Mandate Rollout, Emissions Reporting Obligation & Technology Adoption Rate-Driven Market Sizing Model

- Methane Emission Source Inventory, Detection Gap Analysis & Compliance Spend Projection Framework

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Technology & Innovation Highlights

- Manufacturing Economics & Unit Economics Summary

- Average System CAPEX & OPEX Benchmarks

- Hardware vs Software vs Monitoring-as-a-Service (MaaS) Margin & Profitability Analysis

- Point Sensor, OGI Camera, Drone-Based, Satellite & Aircraft Remote Sensing Revenue Model Summary

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Geographic & Regional Trends

- Risk Assessment Framework

- Geopolitical & International Climate Policy Fragmentation Risk (Paris Agreement, Global Methane Pledge, OGMP 2.0)

- Regulatory Uncertainty & Compliance Timeline Variability Risk Across Jurisdictions

- Technology Accuracy, False Positive / False Negative Rate & Measurement Uncertainty Risk

- Data Sovereignty, Satellite Imagery Access & Remote Sensing IP Risk

- Industry Resistance, Voluntary vs Mandatory Reporting Adoption Risk

- Financial / Market Risk: Carbon Price Volatility & Methane Credit Value Uncertainty

- Competing Emissions Monitoring Technologies & Integrated ESG Platform Substitution Risk

- Regulatory Framework & Policy Standards

- Global Methane Monitoring & Emissions Technologies Market Economics

- Manufacturing & Platform Development Economics Framework

- Capital Expenditure (CAPEX) Structure

- Operating Expenditure (OPEX) Structure

- Revenue Model & Monetisation Levers (Hardware Sales, Software Subscriptions, Data Analytics Platforms, Monitoring-as-a-Service, Carbon Credit Verification)

- Capacity Utilisation & Throughput Economics

- Payback Period & Return on Investment (ROI) Analysis

- Total Cost of Compliance: Methane Monitoring vs Regulatory Fine Avoidance & Carbon Credit Generation Economics

- Sensor, Instrument & Platform Input Cost Analysis

- Laser-Based Gas Sensor (TDLAS, CRDS, DIAL) & Photodetector Cost Trends (USD/unit, 2021–2035)

- Optical Gas Imaging (OGI) Camera & Infrared Detector Array Cost Dynamics

- Metal Oxide Semiconductor (MOS), Electrochemical & Catalytic Bead Sensor Cost Structure

- Drone (UAV) Airframe, Navigation System & Gas Sensor Payload Integration Cost Analysis

- Satellite Methane Detection Payload, Launch & Ground Station Infrastructure Cost Structure

- Connectivity Module (IoT, LoRaWAN, Cellular, Satellite IoT) & Edge Computing Cost Economics

- Impact of Miniaturisation, MEMS-Based Sensing & High-Volume Manufacturing on System Economics

- Data Analytics, Reporting & Verification Platform Economics

- Cloud Data Processing, AI/ML Model Training & Emissions Quantification Platform Cost Structure

- Emissions Reporting, Regulatory Submission & Third-Party Verification Service Economics

- Continuous Emissions Monitoring System (CEMS) vs Periodic Measurement Campaign Cost Comparison

- Carbon Credit Generation, Methane Credit Registry & MRV (Measurement, Reporting & Verification) Platform Economics

- Regulatory & Standards Compliance Economics

- Methane Detection Equipment Certification & Calibration Standards Compliance Cost Benchmarks (EPA Method 21, ISO 13686, OGP, OGMP 2.0, EU Methane Regulation, etc.)

- Continuous Emissions Monitoring System (CEMS) Type Approval & QA/QC Programme Costs

- Third-Party Audit, Measurement Uncertainty Assessment & Independent Verification Cost Structure

- Global Methane Monitoring & Emissions Technologies Market Outlook

- Market Size & Forecast by Value (USD Billion, 2021–2036)

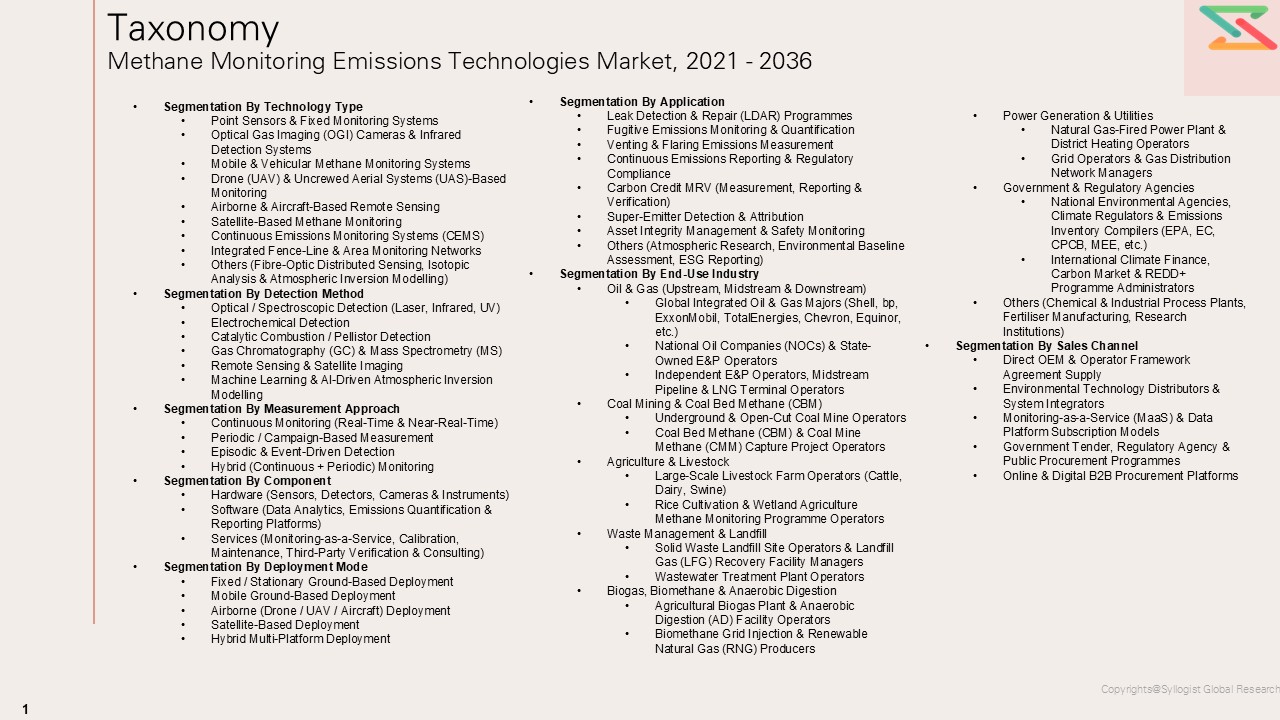

- Market Size & Forecast by Technology Type

- Point Sensors & Fixed Monitoring Systems

- Laser-Based Sensors (TDLAS, CRDS, DIAL, LIDAR)

- Metal Oxide Semiconductor (MOS) & Catalytic Bead Sensors

- Electrochemical & Photoionisation Detection (PID) Sensors

- Optical Gas Imaging (OGI) Cameras & Infrared Detection Systems

- Cooled & Uncooled Infrared (IR) OGI Camera Systems

- Hyperspectral & Multispectral Gas Imaging Systems

- Mobile & Vehicular Methane Monitoring Systems

- Vehicle-Mounted Gas Chromatograph & Cavity Ring-Down Spectroscopy (CRDS) Systems

- Mobile Laser Dispersion Spectroscopy (LDS) & Sniffing Systems

- Drone (UAV) & Uncrewed Aerial Systems (UAS)-Based Monitoring

- Fixed-Wing UAV Methane Monitoring Platforms

- Multi-Rotor UAV & VTOL Gas Sensor Payload Systems

- Airborne & Aircraft-Based Remote Sensing

- Crewed Aircraft Methane Flux Measurement & Aerial Surveying Systems

- Hyperspectral Airborne Imaging Spectrometer (AVIRIS, GHGSat-A) Systems

- Satellite-Based Methane Monitoring

- Low-Earth Orbit (LEO) Commercial Methane Detection Satellites (GHGSat, MethaneSAT, Carbon Mapper, etc.)

- Government & Public Agency Satellite Systems (Sentinel-5P TROPOMI, GOSAT, EMIT, etc.)

- Continuous Emissions Monitoring Systems (CEMS)

- Integrated Fence-Line & Area Monitoring Networks

- Others (Fibre-Optic Distributed Sensing, Isotopic Analysis & Atmospheric Inversion Modelling)

- Point Sensors & Fixed Monitoring Systems

- Market Size & Forecast by Detection Method

- Optical / Spectroscopic Detection (Laser, Infrared, UV)

- Electrochemical Detection

- Catalytic Combustion / Pellistor Detection

- Gas Chromatography (GC) & Mass Spectrometry (MS)

- Remote Sensing & Satellite Imaging

- Machine Learning & AI-Driven Atmospheric Inversion Modelling

- Market Size & Forecast by Measurement Approach

- Continuous Monitoring (Real-Time & Near-Real-Time)

- Periodic / Campaign-Based Measurement

- Episodic & Event-Driven Detection

- Hybrid (Continuous + Periodic) Monitoring

- Market Size & Forecast by Component

- Hardware (Sensors, Detectors, Cameras & Instruments)

- Software (Data Analytics, Emissions Quantification & Reporting Platforms)

- Services (Monitoring-as-a-Service, Calibration, Maintenance, Third-Party Verification & Consulting)

- Market Size & Forecast by Deployment Mode

- Fixed / Stationary Ground-Based Deployment

- Mobile Ground-Based Deployment

- Airborne (Drone / UAV / Aircraft) Deployment

- Satellite-Based Deployment

- Hybrid Multi-Platform Deployment

- Market Size & Forecast by Application

- Leak Detection & Repair (LDAR) Programmes

- Fugitive Emissions Monitoring & Quantification

- Venting & Flaring Emissions Measurement

- Continuous Emissions Reporting & Regulatory Compliance

- Carbon Credit MRV (Measurement, Reporting & Verification)

- Super-Emitter Detection & Attribution

- Asset Integrity Management & Safety Monitoring

- Others (Atmospheric Research, Environmental Baseline Assessment, ESG Reporting)

- Market Size & Forecast by End-Use Industry

- Oil & Gas (Upstream, Midstream & Downstream)

- Global Integrated Oil & Gas Majors (Shell, bp, ExxonMobil, TotalEnergies, Chevron, Equinor, etc.)

- National Oil Companies (NOCs) & State-Owned E&P Operators

- Independent E&P Operators, Midstream Pipeline & LNG Terminal Operators

- Coal Mining & Coal Bed Methane (CBM)

- Underground & Open-Cut Coal Mine Operators

- Coal Bed Methane (CBM) & Coal Mine Methane (CMM) Capture Project Operators

- Agriculture & Livestock

- Large-Scale Livestock Farm Operators (Cattle, Dairy, Swine)

- Rice Cultivation & Wetland Agriculture Methane Monitoring Programme Operators

- Waste Management & Landfill

- Solid Waste Landfill Site Operators & Landfill Gas (LFG) Recovery Facility Managers

- Wastewater Treatment Plant Operators

- Biogas, Biomethane & Anaerobic Digestion

- Agricultural Biogas Plant & Anaerobic Digestion (AD) Facility Operators

- Biomethane Grid Injection & Renewable Natural Gas (RNG) Producers

- Power Generation & Utilities

- Natural Gas-Fired Power Plant & District Heating Operators

- Grid Operators & Gas Distribution Network Managers

- Government & Regulatory Agencies

- National Environmental Agencies, Climate Regulators & Emissions Inventory Compilers (EPA, EC, CPCB, MEE, etc.)

- International Climate Finance, Carbon Market & REDD+ Programme Administrators

- Others (Chemical & Industrial Process Plants, Fertiliser Manufacturing, Research Institutions)

- Oil & Gas (Upstream, Midstream & Downstream)

- Market Size & Forecast by Sales Channel

- Direct OEM & Operator Framework Agreement Supply

- Environmental Technology Distributors & System Integrators

- Monitoring-as-a-Service (MaaS) & Data Platform Subscription Models

- Government Tender, Regulatory Agency & Public Procurement Programmes

- Online & Digital B2B Procurement Platforms

- Asia-Pacific Methane Monitoring & Emissions Technologies Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Technology Type

- By Detection Method

- By Measurement Approach

- By Component

- By Deployment Mode

- By Application

- By End-Use Industry

- By Sales Channel

- Key Demand Drivers (APAC-Specific)

- Competitive Landscape (APAC)

- Europe Methane Monitoring & Emissions Technologies Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Technology Type

- By Detection Method

- By Measurement Approach

- By Component

- By Deployment Mode

- By Application

- By End-Use Industry

- By Sales Channel

- Key Demand Drivers (Europe-Specific)

- Competitive Landscape (Europe)

- North America Methane Monitoring & Emissions Technologies Market Outlook

- Market Overview & Strategic Importance

- Market Size & Forecast

- By Value (2020–2035)

- By Technology Type

- By Detection Method

- By Measurement Approach

- By Component

- By Deployment Mode

- By Application

- By End-Use Industry

- By Sales Channel

- Key Demand Drivers (North America-Specific)

- Competitive Landscape (North America)

- Latin America Methane Monitoring & Emissions Technologies Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Technology Type

- By Detection Method

- By Measurement Approach

- By Component

- By Deployment Mode

- By Application

- By End-Use Industry

- By Sales Channel

- Key Demand Drivers (LATAM-Specific)

- Competitive Landscape (LATAM)

- Middle East & Africa Methane Monitoring & Emissions Technologies Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Technology Type

- By Detection Method

- By Measurement Approach

- By Component

- By Deployment Mode

- By Application

- By End-Use Industry

- By Sales Channel

- Key Demand Drivers (MEA-Specific)

- Competitive Landscape (MEA)

- Country-Wise Methane Monitoring & Emissions Technologies Market Outlook

- Market Size & Forecast by Country

- By Value

- By Technology Type

- By Detection Method

- By Measurement Approach

- By Component

- By Deployment Mode

- By Application

- By End-Use Industry

- By Sales Channel

- Market Size & Forecast by Country

- Market Size & Forecast

- Market Size & Forecast

- Market Size & Forecast

- Market Size & Forecast

- Manufacturing & Platform Development Economics Framework

Countries Covered: United States, Canada, Mexico, Brazil, Argentina, United Kingdom, Germany, France, Netherlands, Norway, Russia, China, India, Australia, Indonesia, Saudi Arabia, UAE, Nigeria, South Africa, Kazakhstan

- Technology Landscape & Innovation Analysis

- Methane Monitoring Technology Maturity Assessment

- Emerging & Disruptive Technologies in Methane Detection & Quantification

- Next-Generation Miniaturised Laser Spectroscopy: TDLAS, CRDS & OA-ICOS on-a-Chip for Low-Cost Continuous Monitoring

- AI/ML-Driven Atmospheric Inversion Modelling & Super-Emitter Source Attribution Advances

- High-Resolution Commercial Satellite Constellation Expansion: Methane Detection Frequency, Coverage & Latency Improvements

- Autonomous Drone Swarm & Persistent UAV Monitoring Networks for Large-Area Fugitive Emission Surveying

- Integrated Fence-Line & Distributed Sensor Network Architectures with IoT, LoRaWAN & Satellite IoT Backhaul

- Digital Twin & Emissions Modelling Platform Integration with SCADA, ERP & ESG Reporting Systems

- Technology Readiness & Commercialisation Matrix – Key Methane Monitoring & Emissions Technologies

- Patent Landscape Analysis

- R&D Investment Benchmarking

- Value Chain & Supply Chain Analysis

- Methane Monitoring & Emissions Technologies Value Chain Mapping

- Supply Chain Concentration & Dependency Analysis

- Key Supplier Mapping by Technology Platform & Component

- Laser Source, Photodetector & Optical Component Supplier Mapping

- Gas Sensor Module, MEMS Sensing Element & Detector Array Supplier Mapping

- Satellite Payload, Launch Vehicle & Ground Station Infrastructure Supplier Mapping

- UAV Airframe, Navigation System & Gas Sensor Payload Supplier Mapping

- IoT Connectivity Module, Edge Computing & Cloud Analytics Platform Supplier Mapping

- Supplier Risk Heat Map

- Make vs Buy Strategy Trends Among Methane Monitoring Technology Developers & Environmental Service Providers

- Pricing Analysis

- Methane Monitoring & Emissions Technology Pricing Dynamics & Mechanisms

- Pricing by Technology Type, Detection Method, Deployment Mode & Application

- Total Cost of Compliance (TCC) Analysis – Including Hardware, Software, Calibration, Data Management, Verification & Regulatory Submission Costs

- Point Sensor vs OGI Camera vs Drone vs Satellite Monitoring Pricing Trends & Benchmarks

- Hardware Sale vs Monitoring-as-a-Service (MaaS) vs Data-as-a-Service (DaaS) Pricing & Value Proposition

- Sustainability & Environmental Stewardship

- Environmental & Sustainability Landscape in Methane Monitoring Technology Manufacturing & Deployment

- Carbon Footprint & Lifecycle GHG Emissions Benchmarking of Methane Monitoring System Manufacture vs Avoided Methane Emission Value

- Contribution of Methane Monitoring Technologies to Global Methane Pledge, Paris Agreement & Net-Zero Targets

- Role of Accurate Methane MRV in Enabling High-Integrity Carbon Markets & Methane Credit Mechanisms

- Recyclability of Sensor Hardware, Electronic Components & Satellite Infrastructure: Circular Economy Assessment

- ESG Reporting & Lifecycle Assessment (LCA) in Methane Monitoring System Operations

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level: Global Environmental Monitoring Majors vs Climate-Tech Startups & Satellite Data Pure-Plays

- Top 5 Methane Monitoring & Emissions Technology Companies Market Revenue Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis by Technology Type, Application & Region

- Competitive Intensity Map by Segment & Region

- Player Classification

- Tier-1 Global Integrated Environmental Monitoring & Gas Detection OEMs with Methane Technology Portfolios (Honeywell, Emerson, ABB, Teledyne Technologies, MSA Safety, etc.)

- Tier-2 Specialist Methane Detection Instrument, OGI Camera & Laser Spectroscopy Manufacturers (FLIR / Teledyne FLIR, LI-COR Biosciences, Aeroqual, Pergam, etc.)

- Emerging Methane Satellite Data, Drone Monitoring & AI-Driven Emissions Analytics Startups (GHGSat, Kayrros, Satellogic, Arcadia, SeekOps, etc.)

- Emerging & Disruptive Players

- Competitive Analysis Frameworks

- Market Share Analysis by Technology Type, Application & Geography

- R&D Intensity & Emissions Detection Technology Platform Breadth Benchmarking

- Operator Framework Agreement, Regulatory Approval Portfolio & Long-Term Monitoring Contract Comparison

- Geographic Revenue Exposure & Regulatory Compliance Footprint Comparison

- Company Profiles

- Company Overview, HQ & Organisational Structure

- Methane Monitoring Products, Detection Technology Platform & Data Analytics Portfolio

- Revenue Breakdown

- Key Operator Supply Programmes, Regulatory Compliance Contracts & Monitoring Network Deployments

- Manufacturing Footprint, Satellite Operations & Key Facilities

- Recent Developments (M&A, Partnerships, New Products, Regulatory Approvals, Financial Results)

- SWOT Analysis

- Strategic Focus: Detection Sensitivity & Accuracy Leadership, Regulatory Approval Expansion, Satellite Constellation Growth & MaaS Platform Strategy

- Strategic Output

- Market Opportunity Matrix

- High-Value Opportunity Quadrant Analysis

- Addressable Market by Technology Type, Application & Region

- Time-to-Revenue Assessment by Opportunity

- White Space Opportunity Analysis

- Underserved Emission Source Category, End-Use Industry & Detection Method Gaps

- Geographic Markets with Low Methane Monitoring Penetration & High Regulatory Mandate Growth

- Technology, Deployment Mode & Data Integration Gaps with High Commercialisation Potential

- Customer Segment Unmet Needs

- Strategic Recommendations

- Product Portfolio & Detection Technology Innovation Strategy

- Technology Platform, AI Analytics & Digital Integration Strategy

- Manufacturing Footprint, Satellite Constellation & Capacity Expansion Strategy

- Regulatory Approval, Operator Framework Agreement & Channel Growth Strategy

- Pricing, Monitoring-as-a-Service & Carbon Market Monetisation Strategy

- Sustainability, Regulatory Compliance & Climate Policy Engagement Strategy

- Supply Chain, Optical Component & Sensor Module Sourcing Strategy

- Partnership, M&A & Expansion Strategy

- Regional Growth Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-Term (2025–2028)

- Mid-Term (2029–2032)

- Long-Term (2033–2036)

- Market Opportunity Matrix

- Market Structure & Concentration