Market Definition

The Global Advanced Aerospace Materials Market encompasses the full commercial ecosystem involved in the research, development, production, processing, and supply of high-performance materials specifically engineered to meet the extreme mechanical, thermal, chemical, and electromagnetic demands of commercial aviation, military aviation, rotorcraft, unmanned aerial vehicles (UAVs), spacecraft, missiles, and next-generation propulsion systems. These materials are distinguished from commodity-grade industrial materials by their exceptional combinations of properties, including high strength-to-weight ratio, fatigue and fracture resistance, elevated-temperature performance, corrosion resistance, damage tolerance, and, increasingly, multifunctional capabilities such as radar signal absorption, electromagnetic shielding, and self-sensing, that enable aerospace OEMs and their supply chains to achieve performance, efficiency, safety, and sustainability standards unattainable through conventional metallurgy or polymer science.

The market encompasses five principal material categories: advanced metallic alloys (including aluminium-lithium alloys, titanium alloys, high-strength steel alloys, and nickel-based superalloys); advanced composite materials (carbon fibre-reinforced polymers, CFRP, glass fibre-reinforced polymers, GFRP, aramid fibre composites, and ceramic matrix composites, CMC); advanced polymers and thermoplastics (including polyetheretherketone, PEEK, polyetherimide, PEI, and high-performance epoxy and bismaleimide resin systems); advanced ceramics and ultra-high-temperature materials (including silicon carbide, zirconia-based thermal barrier coatings, and UHTC compounds for hypersonic applications); and emerging material platforms (including metal matrix composites, MMC, additive-manufactured metallic and composite parts, nano-reinforced materials, bio-inspired structural materials, thermoplastic composites for high-rate manufacturing, and self-healing material systems). The market scope further includes the associated manufacturing process technologies, prepreg production, automated fibre placement (AFP), automated tape laying (ATL), resin transfer moulding (RTM), out-of-autoclave (OOA) curing, and additive manufacturing, that determine the cost, rate, and quality at which advanced materials are converted into structural and functional aerospace components.

From an application standpoint, the market spans aerostructures (fuselage skins and frames, wings, empennages, nacelles, and pylons), engine and propulsion systems (fan blades, combustor liners, turbine blades, exhaust nozzles, and thermal protection components), interior systems (cabin panels, overhead bins, galley structures, and seat frames), landing gear and actuation systems, avionics housings and radomes, and space structures (satellite buses, launch vehicle fairings, rocket nozzles, and re-entry heat shields). End-users include commercial aircraft OEMs (Airbus, Boeing, Embraer, COMAC), military prime contractors (Lockheed Martin, RTX, Northrop Grumman, BAE Systems, Dassault Aviation), aero-engine manufacturers (GE Aerospace, Rolls-Royce, Pratt & Whitney, Safran), spacecraft and launch vehicle manufacturers (SpaceX, NASA, ESA, Arianespace, ISRO), and the broad global tier-1 and tier-2 aerostructure supply chain.

Market Insights

As of early 2026, the global advanced aerospace materials market is experiencing robust structural growth underpinned by a convergence of rising commercial air travel demand, record global defence budgets, intensifying sustainability mandates, and accelerating next-generation aircraft programmes. Valuations across leading research providers range from USD 29.2 billion, reflecting differences in whether conventional aluminium alloys and bulk steels are included alongside higher-performance material systems. Consensus projections across principal analyst sources point to a market CAGR of 8% through 2030, with the broader aerospace materials market forecast to reach USD 62.3 billion by 2030. Looking further ahead to 2036, the market is positioned to exceed USD 120 billion as next-generation single-aisle and wide-body aircraft programmes, hypersonic vehicle development, commercial space expansion, and the UAM/eVTOL aircraft industry collectively amplify material demand across every principal segment.

The composites segment, led by carbon fibre-reinforced polymers (CFRP), is the market’s dominant and fastest-growing material class, accounting for 40.4% of the aerospace and defence materials revenue share in 2024. The Airbus A350 XWB incorporates approximately 53% composites by weight, while the Boeing 787 Dreamliner uses approximately 50%, and both programmes have validated the transformative impact of CFRP on commercial aviation fuel efficiency, corrosion resistance, and passenger cabin pressurisation potential. The global aerospace CFRP composites market reached USD 2.91 billion in 2025 and is forecast to reach USD 4.37 billion by 2030 at a CAGR of 8.4%. At the October 2024 Carbon Fiber conference, Counterpoint Market Intelligence forecast aerospace CFRP composites would surpass USD 1.93 billion in sub-segment revenue by 2026, advancing at a 10.5% CAGR to USD 2.23 billion by 2028, as production rates of composites-intensive aircraft continue to increase. Hexcel’s launch of HexTow IM9 24K carbon fibre at Aero India 2025 and its OOA prepreg systems including HexPly M51, delivering full cure in 40 minutes, are emblematic of the material innovation pipeline feeding OEM production ramp-up ambitions.

Advanced aluminium and aluminium-lithium alloys remain the largest segment by volume, accounting for the dominant share of commercial narrowbody aircraft aerostructure content, with 446.5 kilotons consumed in 2024 in the aerospace and defence materials context. The Airbus A320neo family and Boeing 737 MAX continue to represent the single largest volume driver for aerospace-grade aluminium, and both OEMs are targeting production rates approaching 100 aircraft per month in aggregate to address order backlogs that, at current rates, would take more than 13 years to clear. Titanium alloys represent the fastest-growing metallic segment, advancing at a CAGR of 6.2% through 2030, driven by their unique combination of high strength, low density, biocompatibility at elevated temperatures, and corrosion resistance, properties that make titanium irreplaceable in engine pylons, landing gear structures, wing attachments, and aeroengine rotating components. Nickel-based superalloys and ceramic matrix composites (CMCs) are the critical enablers of next-generation turbine engine efficiency, with CMC hot-section components in GE Aerospace’s LEAP and GE9X engines enabling operating temperatures 500–700°F above the capability of metallic alloys, directly translating into fuel burn improvements of 10–15%.

The defence materials segment is experiencing a pronounced step-change in demand driven by record global defence spending following geopolitical disruptions in Europe and the Indo-Pacific. The US Department of Defense raised its missiles and munitions procurement R&D budget from USD 9 billion in 2015 to USD 30.6 billion in fiscal year 2024. Germany pledged €130 billion through 2030 for defence equipment as part of its historic Zeitenwende rearmament commitment, while Belgium, Romania, and multiple NATO allies have committed to raising defence spending above 2% of GDP. The US Air Force’s Next Generation Air Dominance (NGAD) F-47 fighter jet contract, awarded to Boeing by the Trump administration, targeting production before 2029 at an estimated USD 20 billion programme cost, represents a landmark advanced materials demand signal, as fifth- and sixth-generation combat aircraft require the highest-performance stealth composites, titanium structures, and thermal management materials available. GE Aerospace’s USD 650 million 2024 investment in its additive manufacturing facilities in Alabama and Ohio further signals the sector’s commitment to next-generation production technologies.

Geographically, North America commands the largest revenue share at 42–55% across scope definitions in 2024, anchored by the US aerospace and defence ecosystem encompassing Boeing, Lockheed Martin, Northrop Grumman, RTX, GE Aerospace, and a deep-tier supply chain for advanced composites, titanium, and superalloys. Europe holds the second position, led by Airbus’s adoption of composites across the A220, A350, and next-generation single-aisle platforms, and by the UK’s ASCEND programme, led by GKN Aerospace, which achieved TRL 6 readiness across 42 composites manufacturing projects in 2025. Asia-Pacific is the fastest-growing region, at a CAGR of 8%+, driven by COMAC’s C919 programme integrating CFRP fuselage and wing structures, Japan’s established carbon fibre production leadership through Toray Industries and Mitsubishi Chemical, and India’s expanding aerospace and defence composites sector. The UAE’s Strata Manufacturing has established itself as a Tier-1 CFRP component supplier to both Airbus and Boeing, embedding the Middle East into global aerospace materials supply chains.

Key Drivers

Relentless Lightweighting Imperative and Commercial Aviation Fleet Expansion

The most fundamental and durable structural driver of the advanced aerospace materials market is the aviation industry’s unrelenting imperative to reduce aircraft structural weight as the primary lever for improving fuel efficiency, reducing CO2 emissions, and lowering airline operating costs. Every kilogram of structural weight reduction in a commercial aircraft generates measurable fuel savings over a multi-decade service life, and at the production rates targeting 100 aircraft per month by Airbus and Boeing combined, the cumulative value of weight-optimised advanced materials across a generation of narrow-body and wide-body platforms is enormous. Modern commercial aircraft now incorporate 50–70% composites by structural weight in their primary airframes, and next-generation aircraft designs, including the Airbus next-generation single-aisle announced at the Airbus Summit in March 2025 featuring advanced biomass and thermoplastic composites, folding composite wingtips, and open-fan CFRP fan blades targeting an additional 20% fuel burn reduction, will push composites content even higher. Boeing’s and Airbus’s combined backlog of 42,000–44,000 aircraft required by 2043, of which approximately 33,000 are narrowbodies, underpins a decade-long sustained demand signal for advanced aluminium-lithium alloys, CFRP aerostructures, titanium structural components, and nickel superalloy engine parts across the global aerospace materials supply chain.

Surging Global Defence Budgets and Next-Generation Military Platform Procurement

Geopolitical instability across Eastern Europe, the South China Sea, and the Middle East has catalysed a multi-year, multi-jurisdictional defence spending supercycle that is generating unprecedented demand for the most performance-demanding advanced aerospace materials. Record defence procurement budgets, US DoD at USD 30.6 billion in FY2024 for missiles and munitions R&D alone, Germany’s €130 billion commitment through 2030, and NATO’s collective push toward 2%+ GDP defence spending, are translating directly into procurement of sixth-generation fighter programmes, stealth UAV fleets, hypersonic glide vehicles, advanced cruise missile airframes, and military helicopter modernisation. Each of these platform classes requires advanced materials at the frontier of current capability: radar-absorbing polymer matrix composites and structural coatings for stealth aircraft, titanium alloy structural members and carbon fibre fuselages for manoeuvrable combat aircraft, ultra-high-temperature ceramic composites (UHTCs) for hypersonic leading edges and nose cones, and refractory metal alloys for advanced propulsion nozzle systems. The US F-47 NGAD programme, SpaceX’s Starship fleet expansion, and Northrop Grumman’s B-21 Raider programme each represent multi-billion-dollar demand centres for the highest-specification aerospace materials over the forecast period.

Aviation Sustainability Mandates and SAF Integration Driving Materials Innovation

The global aviation industry’s commitment to achieving net-zero carbon by 2050, as formally endorsed by IATA and supported by the International Civil Aviation Organization’s (ICAO) Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA), is fundamentally reshaping the material technology priorities of aircraft OEMs and their supply chains. Structural weight reduction through advanced composites remains the primary in-service lever for reducing fuel burn and emissions per seat-kilometre, and is being complemented by the development of materials compatible with 100% sustainable aviation fuel (SAF) operation, hydrogen propulsion system structural demands (including high-pressure composite storage vessels and cryogenic-compatible alloys), and hybrid-electric propulsion architectures. The PLEIADES project, launched in 2025, advances composite aerostructures through new materials, induction welding automation, and integrated structural health monitoring. Hexcel and Arkema’s 2024 joint venture to develop recyclable thermoplastic composites for aerospace reflects the growing emphasis on end-of-life material circularity, addressing the sustainability challenge of non-recyclable thermoset CFRP that currently dominates primary aircraft structures. Bio-based resin systems and recycled-fibre composites are progressing through technology readiness levels, positioning sustainable materials as a commercially significant sub-segment before 2036.

Advanced Manufacturing Technology Adoption Accelerating Materials Utilisation

The commercialisation of advanced manufacturing process technologies, particularly automated fibre placement (AFP), automated tape laying (ATL), resin transfer moulding (RTM), out-of-autoclave (OOA) curing, and industrial-scale additive manufacturing of metallic and composite aerospace components, is fundamentally expanding the economic viability of advanced material application across a wider range of aerospace structures and production volumes. These process innovations directly address the historically high fabrication cost and slow production rate that have constrained the adoption of advanced composites to high-value structural applications in premium aircraft programmes. The ASCEND programme led by GKN Aerospace achieved TRL 6 readiness across 42 composites manufacturing projects, including fast-cure prepreg systems validated in complex parts with AFP and ATL processes. Rocket Lab commissioned a 12-metre, 99-tonne AFP machine from Electroimpact in August 2024 for manufacturing Neutron rocket components, achieving approximately 150,000 labour-hour savings per vehicle. GE Aerospace USD 650 million investment in additive manufacturing facilities targets both commercial and defence production efficiency. As these advanced process technologies mature and achieve production certification, the total addressable market for advanced aerospace materials expands materially, as cost barriers that previously restricted adoption to narrowbody and widebody flagships are progressively dismantled.

Commercial Space Expansion, Hypersonics, and eVTOL Creating New Material Demand Frontiers

Beyond the established commercial aviation and military aircraft markets, three emerging demand vectors, commercial space, hypersonic vehicles, and electric vertical take-off and landing (eVTOL) aircraft, are creating structurally new addressable markets for advanced aerospace materials that will make a growing contribution to market revenue through the forecast horizon. The commercial space launch industry, led by SpaceX Starship, Rocket Lab Neutron, and a wide field of new entrant launch vehicle developers, demands high-performance composites, ablative thermal protection materials, and refractory alloys at increasing volumes as launch cadences accelerate. NASA Artemis and international lunar and Mars exploration missions create demand for the most extreme-environment materials ever developed, including UHTC composites for re-entry vehicles and advanced insulation systems. The hypersonic vehicle segment, encompassing both military glide vehicles and nascent commercial point-to-point hypersonic transport concepts, is driving intensive R&D into UHTC, CMC, and carbon-carbon composite systems capable of sustained operation at temperatures exceeding 2000 degrees Celsius. The eVTOL industry, with over 800 programme concepts having been evaluated and a dozen credible commercial-scale programmes in certification, requires lightweight CFRP airframes, composite rotor blades, and structural polymer components that meet aviation certification standards while achieving the weight targets necessary for battery-powered flight economics.

Key Challenges

High Production and Raw Material Costs Constraining Broader Adoption

Advanced aerospace-grade materials, particularly CFRP, titanium alloys, and nickel-based superalloys, carry materially higher raw material, processing, and qualification costs than the conventional aluminium alloys and steels they displace, creating persistent economic barriers to adoption across lower-margin aircraft programmes and cost-sensitive aerostructure applications. Aerospace-grade carbon fibre prices remain substantially above industrial-grade equivalents due to the stringent polyacrylonitrile (PAN) precursor quality requirements, energy-intensive carbonisation and surface treatment processes, and limited global supply concentrated among a small number of Japanese (Toray, Teijin, Mitsubishi Chemical) and US producers (Hexcel, Solvay). Titanium alloys require extensive vacuum arc remelting and carefully controlled thermomechanical processing to meet aerospace certification standards, maintaining cost premiums of 10–20 times over equivalent aluminium billets for comparable structural forms. Nickel superalloy investment castings and directionally solidified turbine blades involve extreme precision processing that limits economies of scale even at full production volumes. These cost structures mean that advanced material adoption decisions involve complex life-cycle cost modelling, and in price-sensitive narrowbody and regional aircraft programmes, the performance premium of the most advanced material options must be carefully weighed against airframe and operating economics.

Supply Chain Concentration, Geopolitical Risk, and Raw Material Volatility

The global advanced aerospace materials supply chain exhibits significant geographic and corporate concentration across several critical raw material and intermediate product categories, creating systemic exposure to supply disruption, geopolitical access risk, and pricing volatility. Carbon fibre supply is dominated by Japanese manufacturers, Toray Industries alone supplies approximately 34% of global aerospace-grade carbon fibre, creating dependencies that are difficult to rapidly diversify given the decade-long investment and qualification timelines associated with new carbon fibre production capacity. Titanium supply was historically concentrated in Russia through VSMPO-AVISMA, which supplied approximately 30–35% of Boeing’s titanium requirements prior to 2022; the geopolitical rupture following Russia’s invasion of Ukraine has compelled major OEMs and material suppliers to undertake urgent supply chain re-routing toward North American, European, and Asia-Pacific titanium sources, at significant cost and lead-time impact. Rare earth elements essential for advanced aluminium alloys, high-temperature coatings, and certain electronic materials used in aerospace systems are heavily concentrated in China, creating strategic vulnerability for Western defence programmes. The US DoD and NATO have both formally identified critical materials supply chain resilience as a national security priority, with active re-shoring and allied-nation diversification programmes underway, but structural change is measured in decades rather than years.

Certification Complexity and Extended Qualification Timelines for New Materials

The introduction of new materials into certified aerospace structures involves one of the most rigorous, time-consuming, and cost-intensive qualification processes in any industry, reflecting the safety-critical nature of primary aircraft structures and the conservative, evidence-based culture of aviation regulators including the FAA, EASA, and CAAC. A comprehensive building-block qualification programme for a new aerospace material system, from coupon-level mechanical property characterisation through sub-component and full-scale structural testing, environmental durability assessment, and repair methodology development, typically requires five to ten years and investments of tens to hundreds of millions of dollars before a new material can be incorporated into a certified primary structure. This qualification overhead creates strong path-dependency around established material systems, particularly for incumbent CFRP prepreg, aluminium alloy, and titanium specifications that carry FAA-approved design allowables databases accumulated over decades of service experience. Novel material systems, including next-generation thermoplastic composites, bio-based resins, nano-reinforced materials, and self-healing polymers, face the full qualification burden without the accumulated data advantage, creating a structural innovation lag between material science advancement and commercial aerospace deployment.

Recyclability Deficits, End-of-Life Sustainability Challenges, and Circular Economy Pressure

The aerospace industry’s growing adoption of thermoset CFRP as the primary structural material in next-generation aircraft creates a compounding end-of-life recyclability challenge that is receiving increasing regulatory, investor, and public scrutiny. Conventional thermoset epoxy-matrix CFRP cannot be remoulded or resharpened after curing, and current commercial recycling processes, primarily pyrolysis and solvolysis, recover carbon fibre at degraded length and properties relative to virgin fibre, limiting the structural recyclate to secondary applications such as non-aerospace short-fibre reinforced moulding compounds. The global aviation fleet will retire tens of thousands of composite-rich aircraft between 2025 and 2050, creating a potentially massive waste stream of non-recyclable structural composites. European circular economy legislation, the EU Green Deal, and increasingly stringent Extended Producer Responsibility frameworks are beginning to impose material circularity obligations on industrial sectors including aerospace, creating medium-term compliance risk for OEMs and material suppliers whose product portfolios remain dominated by non-recyclable thermosets. Thermoplastic composites offer an inherently recyclable alternative, and the Hexcel-Arkema JV and Airbus’s thermoplastic fuselage demonstrator programmes are advancing this transition, but thermoplastic aerospace composites remain at TRL 5–6 for primary structures, with full commercial deployment on a new aircraft programme unlikely before the mid-2030s.

Market Segmentation

- Segmentation By Material Type

- Advanced Aluminium Alloys

- Conventional High-Strength Aluminium Alloys (2xxx, 7xxx series)

- Aluminium-Lithium (Al-Li) Alloys

- Aluminium Metal Matrix Composites (Al-MMC)

- Titanium Alloys

- Alpha & Near-Alpha Titanium Alloys

- Alpha-Beta Titanium Alloys (Ti-6Al-4V and derivatives)

- Beta Titanium Alloys

- Advanced Steel Alloys

- Ultra-High-Strength Steel (UHSS)

- Maraging Steel

- Corrosion-Resistant Steel Alloys

- Nickel-Based Superalloys

- Wrought Superalloys

- Cast Superalloys (Equiaxed, Directionally Solidified, Single Crystal)

- Powder Metallurgy Superalloys

- Advanced Composite Materials

- Carbon Fibre-Reinforced Polymers (CFRP)

- Glass Fibre-Reinforced Polymers (GFRP)

- Aramid / Kevlar Fibre Composites

- Ceramic Matrix Composites (CMC, SiC/SiC, Oxide/Oxide)

- Metal Matrix Composites (MMC)

- Thermoplastic Composites (PEEK, PEI, PEKK matrix systems)

- Hybrid Fibre Composites

- Advanced Polymers & Resins

- Epoxy Resin Systems (Thermoset)

- Bismaleimide (BMI) Resins

- Polyimide Resins

- High-Performance Thermoplastics (PEEK, PEI, PEKK)

- Bio-Based / Sustainable Resin Systems

- Advanced Ceramics & Ultra-High-Temperature Materials (UHTCs)

- Silicon Carbide (SiC) Ceramics

- Zirconia-Based Thermal Barrier Coatings (TBCs)

- Hafnium & Zirconium Diboride UHTCs

- Carbon / Carbon (C/C) Composites

- Emerging & Nano-Enhanced Materials

- Carbon Nanotube (CNT) and Graphene-Reinforced Composites

- Self-Healing Material Systems

- Bio-Inspired and Biomimetic Structural Materials

- Additive-Manufactured Metallic Structures (Ti, Al, Ni alloy AM parts)

- Multifunctional / Smart Materials (Structural Health Monitoring Integrated)

- Segmentation By Manufacturing Process

- Autoclave-Cured Prepreg Processing

- Out-of-Autoclave (OOA) Curing (VARTM, VBRTM)

- Automated Fibre Placement (AFP)

- Automated Tape Laying (ATL)

- Resin Transfer Moulding (RTM) & Compression RTM (C-RTM)

- Filament Winding

- Pultrusion

- Investment Casting & Die Casting (Metallic Alloys)

- Additive Manufacturing (Laser Powder Bed Fusion, DED, Binder Jetting)

- Superplastic Forming / Diffusion Bonding (SPF/DB) for Titanium

- Electroforming & Advanced Machining (EDM, Laser Cutting)

- Segmentation By Application / Structural Zone

- Aerostructures

- Fuselage Skins, Frames & Stringers

- Wing Skins, Spars & Ribs

- Empennage (Horizontal & Vertical Stabilisers)

- Nacelles, Thrust Reversers & Pylons

- Floor Beams & Cabin Structural Panels

- Engine & Propulsion Systems

- Fan Blades & Cases (CFRP, Titanium)

- Combustor Liners (CMC, Superalloy)

- High-Pressure Turbine Blades & Vanes (Single Crystal Superalloy, CMC)

- Low-Pressure Turbine Components

- Exhaust Nozzles & Afterburner Components

- Thermal Barrier Coatings (TBC)

- Landing Gear & Actuation Systems

- Avionics Housings, Radomes & Electromagnetic Structures

- Interior Cabin Components (Panels, Bins, Seats, Galleys)

- Space Structures (Satellite Buses, Launch Vehicle Fairings, Re-entry Heat Shields)

- Missiles, Munitions & Hypersonic Vehicle Structures

- Rotor Blades (Helicopter & eVTOL)

- Segmentation By Aircraft / Platform Type

- Narrowbody Commercial Aircraft (A320 family, Boeing 737 MAX)

- Widebody Commercial Aircraft (A350, Boeing 787, 777X)

- Regional Jets & Turboprops

- Business & General Aviation Aircraft

- Military Fighter & Multi-Role Combat Aircraft

- Military Transport & Tanker Aircraft

- Military Helicopters

- Civil Helicopters & Rotorcraft

- Unmanned Aerial Vehicles (UAVs / UCAVs / MALE / HALE Drones)

- eVTOL Aircraft (Urban Air Mobility)

- Launch Vehicles (Expendable & Reusable)

- Satellites & Spacecraft

- Hypersonic Vehicles (Glide Vehicles & Experimental Aircraft)

- Segmentation By End-Use Industry

- Commercial Aviation

- Military & Defence Aviation

- General Aviation

- Space & Launch Vehicles

- Unmanned Systems (Civil & Military UAV)

- Urban Air Mobility (eVTOL)

- MRO (Maintenance, Repair & Overhaul)

- Segmentation By Ownership / Procurement Type

- Private Sector (Commercial OEM, Airline, Business Jet Operators)

- Public Sector / Government (Military, Space Agency, Defence Prime)

- Segmentation By Tier / Value Chain Position

- Tier 0: Raw Material Producers (Carbon Fibre, PAN Precursor, Titanium Sponge, Aluminium)

- Tier 1: Material Intermediaries (Prepreg, Woven Fabric, Alloy Mill Products)

- Tier 2: Component & Sub-Assembly Manufacturers

- Tier 3: Aerostructure & Engine Integrators

- Tier 4: Aircraft OEM Final Assembly

- Aftermarket & MRO Materials Supply

- Segmentation By Region

- North America (United States, Canada, Mexico)

- Europe (France, Germany, United Kingdom, Italy, Spain, Rest of Europe)

- Asia-Pacific (Japan, China, South Korea, India, Australia, Rest of APAC)

- Middle East & Africa (UAE, Saudi Arabia, Rest of MEA)

- Latin America (Brazil, Rest of Latin America)

All market revenues are presented in USD

Historical Year: 2021–2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027–2036

Key Questions this Study Will Answer

What is the projected global market valuation (USD billion) and volume (metric tonnes) for advanced aerospace materials across all material categories, application zones, aircraft types, and regions through 2036? This quantitative baseline provides the essential foundation for material supplier strategy, OEM procurement planning, investment allocation, and competitive benchmarking across the global aerospace materials value chain.

- How will the composites segment, particularly CFRP, CMC, and emerging thermoplastic composite systems, evolve in terms of market share, production technology maturity, cost trajectory, and adoption rate across commercial and military aircraft programmes through 2036, and what does the Airbus next-generation single-aisle, Boeing F-47 NGAD, and eVTOL aircraft pipeline mean for aggregate CFRP volume demand?

- What are the titanium supply chain re-configuration implications following the exclusion of VSMPO-AVISMA from Western aerospace supply chains, and how are North American, European, and Asia-Pacific titanium sponge, mill product, and fastener suppliers positioned to absorb redirected demand volume, and at what cost and lead-time premium, through the forecast horizon?

- How will advanced manufacturing process technologies, including AFP, ATL, OOA curing, RTM, thermoplastic welding, and additive manufacturing of metallic and composite aerospace parts, reduce the per-kilogram cost of advanced composite and metallic components over the 2027–2036 period, and at what cost thresholds does broader adoption of CFRP into narrowbody primary structures become economically compelling relative to advanced aluminium alternatives?

- What are the competitive dynamics among the leading advanced aerospace materials producers, including Toray Industries, Hexcel, Solvay, Teijin, Mitsubishi Chemical (composites), VSMPO-AVISMA replacements, Arconic, Constellium (aluminium), ATI, PCC (titanium & superalloys), and SGL Carbon, across R&D investment intensity, OEM long-term agreement coverage, geographic manufacturing footprint, and material innovation pipeline depth?

- How are the aviation industry’s net-zero by 2050 commitment and European circular economy regulations reshaping the R&D investment priorities of advanced materials producers toward recyclable thermoplastic composites, bio-based resin systems, and sustainable fibre manufacturing processes, and what commercial readiness timelines are realistic for these sustainable material platforms to enter primary aircraft structure certification programmes?

- What is the advanced aerospace materials demand profile for the emerging commercial space, hypersonic vehicle, and eVTOL aircraft segments through 2036, including the required material performance parameters for sustained hypersonic flight at Mach 5+, the structural and thermal demands of reusable launch vehicle hot structures, and the specific lightweight CFRP and composite requirements of battery-mass-constrained eVTOL airframes?

- How are critical material supply chain resilience risks, encompassing carbon fibre PAN precursor supply concentration, rare earth elements dependencies, titanium source diversification requirements, and geopolitical export control exposure, being assessed and mitigated by leading aerospace OEMs, defence primes, and government procurement agencies, and which material categories carry the highest strategic supply chain vulnerability through 2036?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Processing Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Geographic & Regional Trends

- Risk Assessment Framework

- Geopolitical & Political Risk

- Raw Material Supply Chain Risk

- Environmental & Regulatory Compliance Risk

- Financial / Market Risk

- Technology Maturity & Adoption Risk

- Defense Budget & Procurement Risk

- Regulatory Framework & Standards

- Global Advanced Aerospace Materials Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume

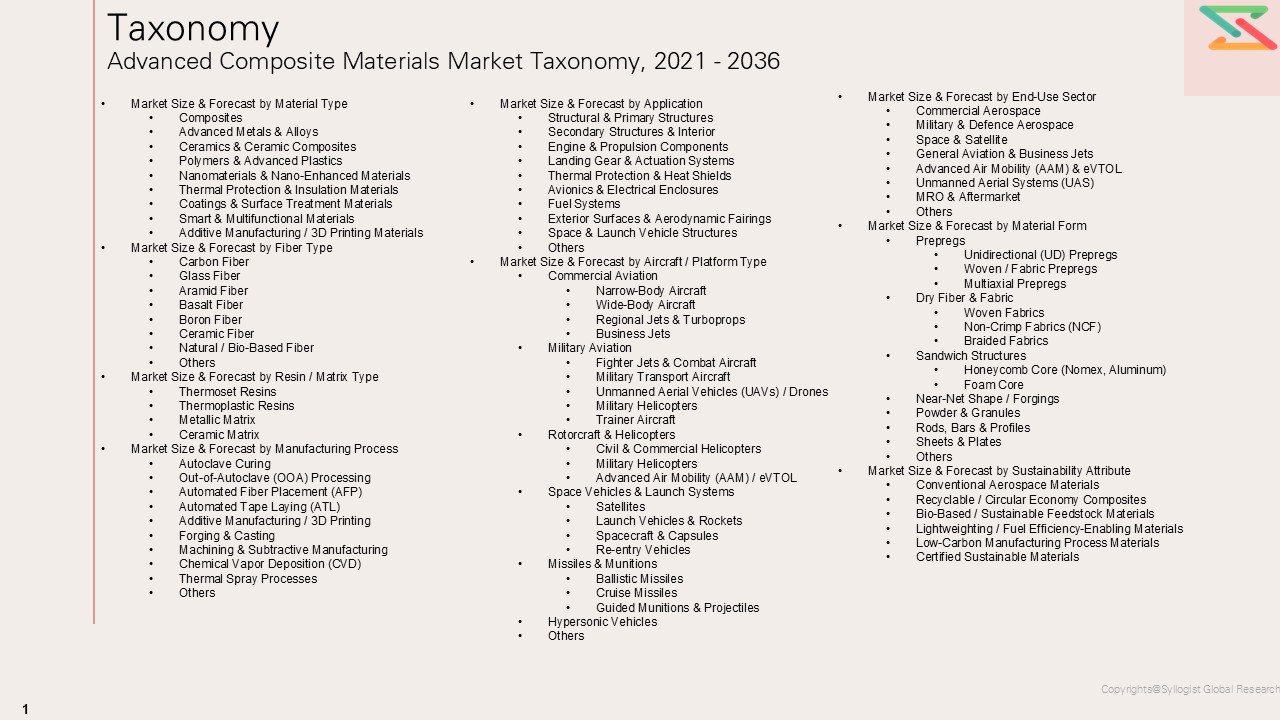

- Market Size & Forecast by Material Type

- Composites

- Carbon Fiber Reinforced Polymer (CFRP)

- Glass Fiber Reinforced Polymer (GFRP)

- Aramid Fiber Reinforced Polymer (AFRP)

- Ceramic Matrix Composites (CMC)

- Metal Matrix Composites (MMC)

- Thermoplastic Composites

- Thermoset Composites

- Hybrid Composites

- Others

- Advanced Metals & Alloys

- Titanium & Titanium Alloys

- Aluminum & Aluminum Alloys

- Nickel-Based Superalloys

- Cobalt-Based Superalloys

- Steel & High-Strength Steel Alloys

- Magnesium Alloys

- Refractory Metals (Tungsten, Molybdenum, Niobium)

- Beryllium & Beryllium Alloys

- Others

- Ceramics & Ceramic Composites

- Alumina (Al₂O₃) Ceramics

- Silicon Carbide (SiC) Ceramics

- Silicon Nitride (Si₃N₄) Ceramics

- Zirconia (ZrO₂) Ceramics

- Ultra-High Temperature Ceramics (UHTC)

- Boron Nitride Ceramics

- Others

- Polymers & Advanced Plastics

- Polyether Ether Ketone (PEEK)

- Polyimide (PI)

- Polyphenylene Sulfide (PPS)

- Polyetherimide (PEI)

- Fluoropolymers (PTFE, PVDF)

- Liquid Crystal Polymers (LCP)

- High-Performance Epoxy Resins

- Others

- Nanomaterials & Nano-Enhanced Materials

- Carbon Nanotubes (CNT)

- Graphene & Graphene Oxide

- Nano-Silica Reinforced Materials

- Nano-Alumina Reinforced Materials

- Nano-Clay Composites

- Others

- Thermal Protection & Insulation Materials

- Ablative Materials

- Aerogel Insulation

- Thermal Barrier Coatings (TBC)

- Reusable Surface Insulation (RSI) Tiles

- High-Temperature Blanket Insulation

- Others

- Coatings & Surface Treatment Materials

- Anti-Corrosion Coatings

- Thermal Spray Coatings

- Environmental Barrier Coatings (EBC)

- Stealth / Radar-Absorbing Materials (RAM)

- Self-Healing Coatings

- Anti-Icing & De-Icing Coatings

- Others

- Smart & Multifunctional Materials

- Shape Memory Alloys (SMA)

- Piezoelectric Materials

- Magnetostrictive Materials

- Electrostrictive Materials

- Self-Healing Polymers & Composites

- Structural Health Monitoring (SHM) Materials

- Others

- Additive Manufacturing / 3D Printing Materials

- Metal Powders for AM (Ti, Al, Ni Alloys)

- Polymer Filaments & Resins for AM

- Ceramic Powders for AM

- Composite Feedstocks for AM

- Others

- Composites

- Market Size & Forecast by Fiber Type

- Carbon Fiber

- Standard Modulus (SM) Carbon Fiber

- Intermediate Modulus (IM) Carbon Fiber

- High Modulus (HM) Carbon Fiber

- Ultra-High Modulus (UHM) Carbon Fiber

- Glass Fiber

- E-Glass Fiber

- S-Glass Fiber

- R-Glass Fiber

- Aramid Fiber

- Kevlar Fiber

- Twaron Fiber

- Technora Fiber

- Basalt Fiber

- Boron Fiber

- Ceramic Fiber

- Natural / Bio-Based Fiber

- Others

- Carbon Fiber

- Market Size & Forecast by Resin / Matrix Type

- Thermoset Resins

- Epoxy Resin

- Bismaleimide (BMI) Resin

- Polyimide Resin

- Cyanate Ester Resin

- Phenolic Resin

- Others

- Thermoplastic Resins

- PEEK

- PPS (Polyphenylene Sulfide)

- PEKK (Polyetherketoneketone)

- PEI (Polyetherimide)

- Others

- Metallic Matrix

- Aluminum Matrix

- Titanium Matrix

- Copper Matrix

- Others

- Ceramic Matrix

- Silicon Carbide (SiC) Matrix

- Carbon-Carbon (C-C) Matrix

- Oxide-Oxide Matrix

- Others

- Thermoset Resins

- Market Size & Forecast by Manufacturing Process

- Autoclave Curing

- Out-of-Autoclave (OOA) Processing

- Resin Transfer Moulding (RTM)

- Vacuum Infusion / VARTM

- Compression Moulding

- Filament Winding

- Pultrusion

- Automated Fiber Placement (AFP)

- Automated Tape Laying (ATL)

- Additive Manufacturing / 3D Printing

- Selective Laser Sintering (SLS)

- Direct Metal Laser Sintering (DMLS)

- Electron Beam Melting (EBM)

- Fused Deposition Modelling (FDM)

- Stereolithography (SLA)

- Forging & Casting

- Investment Casting

- Die Casting

- Isothermal Forging

- Hot Isostatic Pressing (HIP)

- Machining & Subtractive Manufacturing

- Chemical Vapor Deposition (CVD)

- Thermal Spray Processes

- Others

- Market Size & Forecast by Application

- Structural & Primary Structures

- Fuselage Structures

- Wing Structures & Skins

- Empennage (Tail Structures)

- Pressure Bulkheads

- Floor Beams & Frames

- Secondary Structures & Interior

- Cabin Panels & Fairings

- Overhead Bins & Liners

- Flooring

- Galleys & Lavatories

- Engine & Propulsion Components

- Fan Blades & Cases

- Compressor Components

- Combustion Chamber Liners

- Turbine Blades & Vanes

- Exhaust Nozzles & Components

- Nacelles & Thrust Reversers

- Landing Gear & Actuation Systems

- Landing Gear Structures

- Hydraulic System Components

- Actuator & Control Components

- Thermal Protection & Heat Shields

- Re-entry Vehicle Heat Shields

- Engine Thermal Barriers

- Hypersonic Vehicle Structures

- Avionics & Electrical Enclosures

- Radomes

- Antenna Housings

- Electronic Enclosures & Housings

- Fuel Systems

- Fuel Tanks

- Fuel Lines & Fittings

- Exterior Surfaces & Aerodynamic Fairings

- Nose Cones & Radomes

- Wing Tips & Winglets

- Pylons & Struts

- Space & Launch Vehicle Structures

- Satellite Structures & Bus Panels

- Launch Vehicle Fairing & Payload Adapters

- Propellant Tanks

- Solar Panel Substrates

- Others

- Structural & Primary Structures

- Market Size & Forecast by Aircraft / Platform Type

- Commercial Aviation

- Narrow-Body Aircraft

- Wide-Body Aircraft

- Regional Jets & Turboprops

- Business Jets

- Military Aviation

- Fighter Jets & Combat Aircraft

- Military Transport Aircraft

- Unmanned Aerial Vehicles (UAVs) / Drones

- Military Helicopters

- Trainer Aircraft

- Rotorcraft & Helicopters

- Civil & Commercial Helicopters

- Military Helicopters

- Advanced Air Mobility (AAM) / eVTOL

- Space Vehicles & Launch Systems

- Satellites

- Launch Vehicles & Rockets

- Spacecraft & Capsules

- Re-entry Vehicles

- Missiles & Munitions

- Ballistic Missiles

- Cruise Missiles

- Guided Munitions & Projectiles

- Hypersonic Vehicles

- Others

- Commercial Aviation

- Market Size & Forecast by End-Use Sector

- Commercial Aerospace

- Military & Defence Aerospace

- Space & Satellite

- General Aviation & Business Jets

- Advanced Air Mobility (AAM) & eVTOL

- Unmanned Aerial Systems (UAS)

- MRO & Aftermarket

- Others

- Market Size & Forecast by Material Form

- Prepregs

- Unidirectional (UD) Prepregs

- Woven / Fabric Prepregs

- Multiaxial Prepregs

- Dry Fiber & Fabric

- Woven Fabrics

- Non-Crimp Fabrics (NCF)

- Braided Fabrics

- Sandwich Structures

- Honeycomb Core (Nomex, Aluminum)

- Foam Core

- Near-Net Shape / Forgings

- Powder & Granules

- Rods, Bars & Profiles

- Sheets & Plates

- Others

- Prepregs

- Market Size & Forecast by Sustainability Attribute

- Conventional Aerospace Materials

- Recyclable / Circular Economy Composites

- Bio-Based / Sustainable Feedstock Materials

- Lightweighting / Fuel Efficiency-Enabling Materials

- Low-Carbon Manufacturing Process Materials

- Certified Sustainable Materials

- Asia-Pacific Advanced Aerospace Materials Market Outlook

- Market Size & Forecast

- By Value

- By Volume

- By Material Type

- By Fiber Type

- By Resin / Matrix Type

- By Manufacturing Process

- By Application

- By Aircraft / Platform Type

- By End-Use Sector

- By Material Form

- By Sustainability Attribute

- Market Size & Forecast

- Europe Advanced Aerospace Materials Market Outlook

- Market Size & Forecast

- By Value

- By Volume

- By Material Type

- By Fiber Type

- By Resin / Matrix Type

- By Manufacturing Process

- By Application

- By Aircraft / Platform Type

- By End-Use Sector

- By Material Form

- By Sustainability Attribute

- Market Size & Forecast

- North America Advanced Aerospace Materials Market Outlook

- Market Size & Forecast

- By Value

- By Volume

- By Material Type

- By Fiber Type

- By Resin / Matrix Type

- By Manufacturing Process

- By Application

- By Aircraft / Platform Type

- By End-Use Sector

- By Material Form

- By Sustainability Attribute

- Market Size & Forecast

- Latin America Advanced Aerospace Materials Market Outlook

- Market Size & Forecast

- By Value

- By Volume

- By Material Type

- By Fiber Type

- By Resin / Matrix Type

- By Manufacturing Process

- By Application

- By Aircraft / Platform Type

- By End-Use Sector

- By Material Form

- By Sustainability Attribute

- Market Size & Forecast

- Middle East & Africa Advanced Aerospace Materials Market Outlook

- Market Size & Forecast

- By Value

- By Volume

- By Material Type

- By Fiber Type

- By Resin / Matrix Type

- By Manufacturing Process

- By Application

- By Aircraft / Platform Type

- By End-Use Sector

- By Material Form

- By Sustainability Attribute

- Market Size & Forecast

- Country Wise* Advanced Aerospace Materials Market Outlook

- Market Size & Forecast

- By Value

- By Volume

- By Material Type

- By Fiber Type

- By Resin / Matrix Type

- By Manufacturing Process

- By Application

- By Aircraft / Platform Type

- By End-Use Sector

- By Material Form

- By Sustainability Attribute

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Germany, United Kingdom, France, Italy, Spain, Netherlands, Switzerland, Russia, China, Japan, India, South Korea, Australia, Singapore, Brazil, Mexico, Saudi Arabia, UAE, South Africa

- Technology Landscape & Innovation Analysis

- Value Chain & Supply Chain Analysis

- Pricing Analysis

- Sustainability & Energy Efficiency

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented Vs Consolidated)

- Top 5 Players Market Share

- HHI (Herfindahl–Hirschman Index) Concentration Analysis

- Competitive Intensity Map

- Player Classification

- Market Leaders

- Strong Challengers

- Specialist / Niche Players

- Emerging Players

- Regional Players

- Competitive Analysis Frameworks

- Market Share Analysis

- Company Profile

- Company Overview & HQ

- Products & Solutions Portfolio

- Overall Revenue & Segmental Revenue

- Geographic Presence

- Recent Developments (M&A, Launches, Partnerships)

- SWOT Analysis

- Strategic Focus Areas

- Competitive Positioning Map

- Market Structure & Concentration

- Strategic Output

- Market Opportunity Matrix

- White Space Opportunity Analysis

- Strategic Recommendations

- Material Portfolio & Product Innovation Strategy

- Advanced Manufacturing & Process Optimization Strategy

- Lightweighting & Fuel Efficiency Strategy

- Composites & Next-Generation Material Development Strategy

- Pricing & Commercial Strategy

- Regulatory Compliance & Certification Strategy

- Sustainability & Circular Economy Strategy

- Supply Chain Resilience & Raw Material Sourcing Strategy

- Partnership, M&A & Global Expansion Strategy

- Regional & Country-Level Market Entry Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025–2028)

- Mid-term (2029–2032)

- Long-term (2033–2036)