Market Definition

The Global Agriculture Tire Market encompasses the design, manufacturing, distribution, and servicing of tires and related wheel assemblies specifically engineered for the full range of agricultural machinery and farm equipment deployed across crop cultivation, soil preparation, harvesting, material handling, and ancillary farm operations worldwide. Agriculture tires are highly specialized components that must perform reliably across an exceptionally demanding and variable set of operating conditions, including soft and waterlogged field soils where flotation and minimal soil compaction are critical to preserving soil structure and agronomic productivity, hard and abrasive surfaces on farm roads and concrete yards, steep gradients and undulating terrain on hillside farming operations, and the high-speed road transport requirements of modern farm equipment between field locations and grain storage facilities. The product scope of this market encompasses tires for tractors across all power categories from compact utility tractors to high-horsepower articulated four-wheel-drive platforms, combine harvesters and grain headers, self-propelled forage harvesters, sprayers and application equipment, telehandlers and agricultural loading equipment, trailers and grain carts, seeding and tillage equipment, and the growing range of specialty and horticultural equipment operating in orchards, vineyards, and protected cultivation environments. The technology spectrum within this market includes conventional bias-ply tires, radial tires, very high flexion and intermediate flexion tires, low sidewall radial tires, foam-filled and solid tires for specific applications, central tire inflation system compatible constructions, and the emerging category of tires engineered for electric and hybrid-electric agricultural machinery platforms. The value chain of this market extends from natural rubber, synthetic elastomer, steel cord, and specialty compound material producers through to tire manufacturers, authorized dealer and fitment networks, agricultural machinery dealers and their parts operations, farm cooperative procurement organizations, and tire management service providers supporting professional farming operations across all scales of commercial agriculture globally.

Market Insights

The global agriculture tire market is exhibiting a robust and structurally grounded demand trajectory in 2026, supported by the sustained investment of the global agricultural sector in machinery modernization, precision farming technology adoption, and the progressive mechanization of agricultural production in emerging farming economies across Asia, Africa, and Latin America. The fundamental economic driver underlying this demand trajectory is the intensifying pressure on agricultural producers to maximize yield per hectare, reduce input costs per unit of production, and manage the escalating operational costs of farm labor through increased mechanization and productivity-enhancing technology, all of which translate directly into sustained demand for modern high-specification farm equipment and the advanced tire products that enable these machines to perform at their engineered productivity potential. The market is operating with a favorable demand balance between its two primary revenue channels, with the original equipment segment benefiting from sustained new tractor and combine harvester production activity at leading agricultural machinery manufacturers, and the replacement segment drawing structural support from the large and expanding global parc of in-service agricultural equipment whose tire replacement cycles generate a recurring and geographically diversified demand stream that is substantially insulated from short-term agricultural commodity price fluctuations.

A defining technological and commercial trend reshaping the agriculture tire market is the accelerating adoption of very high flexion and intermediate flexion tire technologies by professional farming operations seeking to address the agronomic and operational challenges associated with soil compaction, which represents one of the most economically significant sources of yield loss and long-term soil health degradation in mechanized agriculture globally. Very high flexion tires are engineered to operate at significantly lower inflation pressures than conventional radial tires of equivalent load capacity, enabling a substantially larger and more evenly distributed tire footprint that reduces the peak ground contact pressure transmitted to the soil by heavy agricultural machinery. The agronomic benefits of reduced soil compaction, including improved root penetration depth, enhanced soil water infiltration, better aeration, and the preservation of earthworm populations and soil biological activity, are increasingly recognized and quantified by agronomy research institutions, and the resulting farmer awareness is translating into growing demand for very high flexion tire products across the tractor, sprayer, and trailer segments where soil contact pressure management is most consequential. Tire manufacturers are responding with expanding very high flexion product portfolios that cover a broader range of equipment categories and rim sizes, and with agronomic support programs that provide farming customers with pressure setting recommendations and compaction reduction guidance that reinforces the technical value proposition of their premium tire products.

The precision farming and agricultural technology revolution is creating a new and commercially significant interface between agriculture tire performance characteristics and the operational effectiveness of precision guidance, variable rate application, and yield monitoring systems that are becoming standard equipment on modern high-specification farm machinery. The accuracy of GPS-guided auto-steer and precision application systems is sensitive to tire dimensions, inflation pressure consistency, and rolling radius uniformity, as variations in these parameters can introduce positional errors that compromise the agronomic precision of seeding, fertilizer application, and crop protection operations whose economic value depends directly on the accuracy of placement relative to field prescription maps. This requirement for dimensional and performance consistency across the operational life of a tire set is elevating the technical standards applied to agriculture tire manufacturing quality and is driving demand for premium products whose dimensional tolerances, compound consistency, and structural uniformity can be certified to the specifications required by precision farming system integrators. Central tire inflation systems, which enable on-the-go adjustment of tire inflation pressure between field and road operating conditions, are gaining traction as a technology that optimizes both soil compaction management and road transport efficiency, and the growing adoption of these systems is creating demand for tires specifically engineered to perform reliably across the wide pressure range that central tire inflation system operation requires.

From a regional perspective, Europe represents the most technologically advanced and commercially sophisticated market for agriculture tires globally, characterized by the highest penetration rates of very high flexion and intermediate flexion technology, a well-established premium brand culture driven by the stringent agronomic and environmental standards applied by professional farm operators, and a mature dealer and service channel infrastructure that supports technically demanding tire management practices. North America constitutes the largest market by revenue value, underpinned by the concentration of the world’s highest-horsepower tractor and combine harvester fleets in the grain belt states and prairie provinces of the United States and Canada where large-scale row crop production operations drive significant demand for the largest and highest-specification agriculture tire products. Asia-Pacific, and India in particular, is the most important market by volume and the fastest-growing market by investment in mechanization and tire product specification upgrading, with India’s large tractor production base, expanding farm mechanization coverage, and government support for agricultural productivity enhancement collectively creating the world’s largest single-country tractor tire demand pool. Latin America, led by Brazil and Argentina as major commercial agriculture economies with large and growing mechanized crop production bases, represents a high-value and expanding market with strong demand for large radial tires serving the extensive soybean, corn, and sugarcane farming operations that dominate agricultural activity in the region.

Key Drivers

Global Agricultural Mechanization Expansion and the Sustained Modernization of Farm Equipment Fleets Across Emerging Economies

The most structurally significant and long-duration demand driver for the global agriculture tire market is the progressive expansion of agricultural mechanization coverage across the large and densely populated farming economies of Asia, Africa, and Latin America, where the economic and demographic imperatives of improving agricultural labor productivity, reducing post-harvest losses, and enhancing food security are driving sustained investment in tractor ownership, power-driven tillage equipment, and mechanized harvesting solutions at both household and commercial farm scales. In India, Southeast Asia, and Sub-Saharan Africa, the combination of government subsidy programs for tractor acquisition, rural credit expansion, agricultural input subsidization, and farmer income support schemes is actively accelerating the rate of mechanization adoption, translating directly into growth in new tractor registrations and in the installed base of agricultural equipment requiring original equipment and replacement tires. The modernization of existing farm equipment fleets in more mature agricultural markets, driven by the productivity advantages and precision farming integration capabilities of newer machinery generations, is simultaneously sustaining original equipment demand and shortening effective equipment replacement cycles in ways that generate incremental tire procurement activity. This dual dynamic of mechanization expansion in developing markets and fleet modernization in mature markets is providing the agriculture tire industry with a geographically diversified and mutually reinforcing demand base that spans the full spectrum of tire size categories, technology levels, and price positioning from economy bias-ply products to premium very high flexion radial tires.

Precision Agriculture Adoption and the Growing Agronomic Recognition of Advanced Tire Technology as a Productivity Enabler

The rapid and broadening adoption of precision farming technologies, encompassing GPS-guided auto-steer systems, variable rate seeding and fertilizer application, satellite and drone-based crop monitoring, and yield mapping, is creating a commercially important demand driver for technically advanced agriculture tire products by establishing a direct and quantifiable link between tire performance characteristics and the agronomic and economic outcomes of precision farming operations. As farming operations invest in the digital and sensor infrastructure required for precision agriculture, the sensitivity of these systems to tire-related variables including inflation pressure consistency, dimensional uniformity, and rolling radius stability is creating a technology pull for premium tire products that can be certified to the performance standards required for optimal precision system operation. The parallel and reinforcing trend of growing farmer awareness of soil compaction as a primary constraint on yield potential and long-term soil health is creating a strong demand pull for very high flexion and intermediate flexion tires whose agronomically demonstrated benefits in compaction reduction, yield preservation, and soil structure maintenance are increasingly supported by peer-reviewed field trial data and promoted through manufacturer agronomic support programs. The convergence of precision agriculture technology investment and agronomic awareness of tire performance consequences is progressively elevating the purchasing criteria applied to agriculture tire selection by professional farming operations from a predominantly price-based evaluation toward a performance and total agronomic value framework that favors premium and technically differentiated products and supports the favorable average selling price dynamics that are contributing to above-volume revenue growth across the market.

Expanding Global Food Demand and the Intensification of Commercial Agricultural Production to Improve Yield and Input Efficiency

The fundamental and long-term demand driver underpinning sustained investment in agricultural mechanization, precision farming technology, and high-specification farm equipment is the structural growth in global food, feed, and fiber demand driven by population expansion, rising per-capita protein consumption in developing economies, and the growing demand for agricultural feedstocks in bioenergy and industrial applications. Meeting this demand trajectory within the constraints of finite arable land availability, water resource limitations, and environmental sustainability requirements demands a continuous improvement in crop yields per hectare and input use efficiency that is practically achievable only through the adoption of more advanced farming equipment, more precise application technologies, and more sophisticated soil and crop management practices. The imperative to maximize yield on every cultivated hectare reinforces the agronomic case for soil compaction management through advanced tire technology, as the yield losses attributable to compaction-related root restriction and soil structural degradation represent a direct and measurable cost against the profitability of intensive cropping systems. Government agricultural policy frameworks across major food-producing nations are increasingly incorporating soil health preservation and input use efficiency objectives into farm subsidy and support structures, creating policy incentives that align with the adoption of very high flexion tire technology and other soil-protective practices, and providing an institutional demand driver for premium agriculture tires that supplements the commercially-driven mechanization and precision farming demand dynamics described above.

Key Challenges

Price Sensitivity in Smallholder and Subsistence Farming Segments and the Challenge of Delivering Value Across Diverse Customer Economics

A persistent structural challenge facing the global agriculture tire industry is the fundamental heterogeneity of the farming customer base, which spans from large-scale professional commercial farming operations in developed economies with the agronomic sophistication and financial resources to invest in premium very high flexion tire technology, to smallholder farmers in developing economies for whom tire acquisition cost is the primary purchasing criterion and the economic case for premium tire products cannot be made on agronomic performance grounds alone. This customer heterogeneity creates a market segmentation challenge for tire manufacturers who must simultaneously develop and position premium technically advanced products for the professional farming segment while maintaining competitive and accessible entry-tier product lines for the large volume economy segment without undermining the brand equity and price positioning of their premium offerings. In price-sensitive emerging markets, the prevalence of low-cost domestic and imported tire products at price points substantially below those of established international brands creates significant market share pressure in the economy segment, while the agronomic awareness and technical buying criteria that support premium product adoption in mature markets are less developed, limiting the effectiveness of performance-based value proposition communication in markets where price remains the dominant purchasing driver. Developing distribution channel strategies, product portfolio structures, and customer education approaches that address the full spectrum of the global farmer customer base without sacrificing premium segment profitability or ceding volume in economy segments to unbranded competitors represents an ongoing strategic challenge for leading agriculture tire manufacturers.

Seasonal Demand Concentration and the Operational Complexity of Managing Supply Chain and Inventory Economics Across Agricultural Cycles

A structurally distinctive operational challenge in the agriculture tire market is the high seasonal concentration of replacement tire demand, driven by the characteristic pattern of pre-season equipment preparation and in-season tire failure replacement that creates pronounced demand peaks ahead of and during the primary tillage, planting, and harvesting seasons in each regional market, and corresponding demand troughs in the inter-season periods when equipment is largely idle and farmers defer discretionary equipment expenditure. This seasonal demand pattern creates significant inventory management, logistics planning, and working capital challenges for tire manufacturers, distributors, and dealers who must build and position inventory in anticipation of seasonal peaks without creating excessive stockholding costs in the trough periods, and who must manage the geographic dispersion of demand across multiple regional agricultural seasons that are offset in timing between the northern and southern hemispheres and across different latitudinal climate zones. The consequence of inventory miscalculation in either direction is commercially damaging, as stockouts during peak demand periods result in lost sales to competitors and damage customer relationships, while excess inventory at the end of peak periods generates carrying costs, potential product degradation risk, and capital inefficiency. The challenge is further compounded by the difficulty of accurately forecasting seasonal demand in markets where agricultural equipment utilization and tire wear rates are influenced by weather conditions, commodity price signals affecting planting area decisions, and government policy changes affecting mechanization incentive programs, all of which introduce forecast uncertainty that is difficult to manage within the lead time constraints of tire manufacturing and supply chain operations.

Raw Material Cost Volatility and the Increasing Input Cost Complexity Associated with Advanced Tire Compound Development

The global agriculture tire manufacturing industry faces sustained and structurally complex exposure to raw material cost volatility that is intensifying as the product mix shifts toward technically advanced very high flexion and radial constructions whose performance requirements demand increasingly specialized and often higher-cost compound formulations, reinforcement materials, and processing technologies relative to conventional bias-ply tire production. Natural rubber price volatility, driven by supply concentration in Southeast Asian producing regions and susceptibility to weather, disease, and regulatory disruption, represents the primary raw material cost risk for agriculture tire manufacturers, and the exposure is amplified in the premium agriculture tire segment where natural rubber content is typically higher relative to equivalent synthetic rubber blends owing to the dynamic flexion and heat dissipation performance requirements of very high flexion constructions. The increasing incorporation of specialty silica compounds, advanced processing oils, and high-strength steel cord materials in premium agriculture tire formulations is adding further dimensions of input cost complexity that are partially decorrelated from the natural rubber price cycle and require separate supply chain management disciplines. Translating these input cost movements into product pricing adjustments without disrupting the dealer channel pricing structures, long-term supply agreements with agricultural machinery manufacturers, and farm customer price expectations that govern commercial relationships across the agriculture tire market is a demanding financial management challenge, particularly in market environments where farm income is simultaneously under pressure from commodity price cycles that reduce farmer willingness to absorb price increases on agricultural inputs including tires.

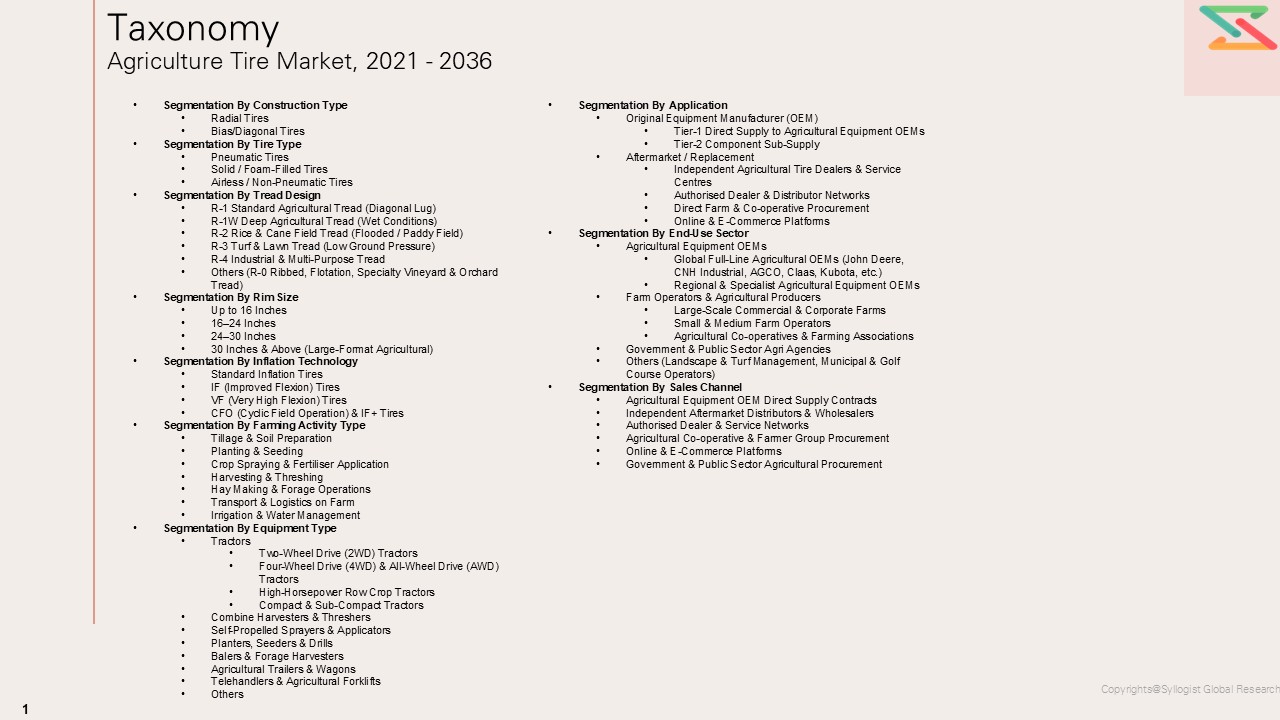

Market Segmentation

- Segmentation By Equipment Type

- Tractors (Compact, Utility, and High-Horsepower)

- Articulated Four-Wheel-Drive Tractors

- Combine Harvesters

- Self-Propelled Forage Harvesters

- Self-Propelled Sprayers and Application Equipment

- Telehandlers and Agricultural Loaders

- Agricultural Trailers and Grain Carts

- Seeding and Tillage Equipment

- Specialty and Horticultural Equipment

- Compact Utility and Vineyard Tractors

- Others

- Segmentation By Tire Technology

- Very High Flexion (VF) Tires

- Intermediate Flexion (IF) Tires

- Standard Radial Tires

- Bias-Ply Tires

- Low Sidewall Radial Tires

- Central Tire Inflation System (CTIS) Compatible Tires

- Solid and Foam-Filled Tires

- Electric and Hybrid-Electric Machine Optimized Tires

- Others

- Segmentation By Application

- Field and Crop Cultivation

- Soil Preparation and Tillage

- Planting and Seeding Operations

- Crop Protection and Spraying

- Harvesting Operations

- Baling and Forage Operations

- Material Handling and Loading

- Road Transport and Farm Logistics

- Orchard, Vineyard, and Protected Cultivation

- Others

- Segmentation By Crop Type

- Grain and Cereal Crops

- Row Crops and Oilseeds

- Sugarcane

- Cotton

- Fruits and Vegetables

- Viticulture and Orchards

- Fodder and Forage Crops

- Others

- Segmentation By Drive Axle Position

- Front Axle Tires

- Rear Drive Axle Tires

- Implement and Trailer Tires

- Others

- Segmentation By Rim Size

- Below 24 Inches

- 24 to 34 Inches

- 35 to 46 Inches

- Above 46 Inches

- Segmentation By Tread Design

- R-1 Field and Agricultural Lug Tread

- R-1W Deep Lug Tread for Wet Conditions

- R-2 Cane and Rice Tread

- R-3 Turf and Minimal Disturbance Tread

- R-4 Industrial and All-Purpose Tread

- Flotation and Wide Tread

- Others

- Segmentation By Rubber Compound Technology

- Natural Rubber-Dominant Compound

- Synthetic Rubber and Silica Compound

- Multi-Compound and Dual-Compound Formulation

- Bio-Based and Sustainable Compound

- Others

- Segmentation By Sales Channel

- Original Equipment Manufacturer (OEM) Channel

- Independent Aftermarket and Replacement Channel

- Agricultural Machinery Dealer Parts Network

- Farm Cooperative and Group Procurement

- Online and Digital Procurement Channel

- Others

- Segmentation By Farm Scale and Operator Type

- Large-Scale Commercial Farming Operations

- Mid-Scale Professional Farming Operations

- Smallholder and Family Farms

- Agricultural Contractor and Custom Operator

- Government and Institutional Farm Operations

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

All market revenues are presented in USD

Historical Year: 2021–2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027–2036

Key Questions this Study Will Answer

- What is the projected global market valuation and volume for agriculture tires through 2036, segmented by equipment type, tire technology, crop application, and region, and which product technology categories and geographic markets are expected to generate the highest incremental revenue and volume growth across the forecast period?

- How is the accelerating adoption of very high flexion and intermediate flexion tire technology reshaping the product mix, average selling price dynamics, and competitive positioning of leading agriculture tire manufacturers, and what are the agronomic, operational, and economic factors that are expected to drive or constrain the rate of very high flexion penetration across different equipment categories, farm scales, and regional markets over the forecast horizon?

- What is the projected growth trajectory and competitive landscape of the agriculture tire market in India, Brazil, and the major Southeast Asian farming economies, and how are government mechanization incentive programs, farm credit expansion, and rural infrastructure investment expected to influence tractor production volumes, farm equipment fleet composition, and replacement tire demand in these markets across the forecast period?

- How is the convergence of precision agriculture technology adoption, central tire inflation system deployment, and digital farm management platforms expected to elevate the technical performance standards and dimensional consistency requirements applied to agriculture tire procurement by professional farming operations, and what are the implications for product development investment priorities and quality certification requirements among leading tire manufacturers?

- Who are the leading agriculture tire manufacturers, specialty compound technology developers, and authorized distribution and service network operators currently defining the competitive landscape of the global agriculture tire market, and what are their respective product portfolio strategies, geographic expansion priorities, agronomic support program investments, and technology development roadmaps for very high flexion, electric machinery, and precision farming-compatible tire products through the forecast horizon?

- Product Definition

- Scope of the Study

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Industry Publications, Agricultural Equipment OEM Reports & Press Releases

- Government Agriculture & Rural Development Authority Data (USDA, FAO, ICAR, EU DG AGRI, etc.)

- Agriculture Tire Production, Trade & Replacement Market Statistics

- OEM Procurement & Agricultural Equipment Supply Chain Databases

- Primary Research Design & Execution

- In-depth Interviews with Agriculture Tire Manufacturers, OEM Procurement Heads & Dealer Networks

- Surveys with Agricultural Equipment OEMs, Independent Tire Dealers & Farm Operators

- Expert Panel Validation

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Bottom-Up & Top-Down Reconciliation

- Agricultural Equipment Fleet & Cultivated Area Model for OEM & Replacement Demand

- Replacement Rate & Seasonal Operating Hours-Driven Aftermarket Tire Market Sizing Model

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Technology & Innovation Highlights

- Manufacturing Economics & Unit Economics Summary

- Average Plant CAPEX & OPEX Benchmarks

- OEM vs Aftermarket Margin & Profitability Analysis

- Radial & Specialty Agriculture Tire Revenue Model Summary

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Geographic & Regional Trends

- Risk Assessment Framework

- Geopolitical & Trade Policy Risk

- Raw Material Price Volatility (Natural Rubber, Synthetic Rubber, Carbon Black, Steel) Risk

- Environmental & Regulatory Risk

- Financial / Market Risk

- Agricultural Commodity Price Cyclicality & Farm Income Risk

- Climate Change, Soil Compaction Regulation & Seasonal Demand Variability Risk

- Precision Farming & Autonomous Agricultural Equipment Transition Risk

- Regulatory Framework & Policy Standards

- Global Agriculture Tire Market Economics

- Manufacturing Economics & Unit Economics Framework

- Capital Expenditure (CAPEX) Structure

- Operating Expenditure (OPEX) Structure

- Revenue Model & Monetisation Levers

- Capacity Utilisation & Throughput Economics

- Payback Period & Return on Investment (ROI) Analysis

- Total Cost of Production vs Alternative Tire & Non-Pneumatic / Foam-Fill Technologies

- Raw Material & Input Cost Analysis

- Natural Rubber & Synthetic Rubber Price Trends (USD/tonne, 2021–2035)

- Carbon Black & Silica Reinforcement Cost Dynamics

- Steel Cord & Bead Wire Cost Analysis

- Chemical Additives & Compounding Cost Structure

- Energy Cost Structure in Agriculture Tire Manufacturing

- Scrap Tire & Retread Material Recycling Value Chain Economics

- Impact of Large-Format, VF (Very High Flexion) & IF (Improved Flexion) Tire Specifications on Product Economics

- Aftermarket & Replacement Tire Economics

- Replacement Cost Structure by Farming Activity Type & Geography

- Seasonal Operating Hours-Driven Replacement Rate & Demand Dynamics

- On-Farm Tire Management Service & Dealer Service Network Economics

- Retread & Repair Economics for Agriculture Tires

- Warranty & Guarantee Economics in OEM vs Aftermarket Agriculture Tires

- Regulatory & Standards Compliance Economics

- Agriculture Tire Safety Standards Compliance Cost Benchmarks (ISO, ETRTO, TRA, BIS, etc.)

- Load Index, Speed Rating & Inflation Pressure Regulation Compliance Costs

- End-of-Life Tire (ELT) & Environmental Regulation Compliance Costs

- Global Agriculture Tire Market Outlook

- Market Size & Forecast by Value (USD Billion, 2021–2036)

- Market Size & Forecast by Construction Type

- Radial Tires

- Bias/Diagonal Tires

- Market Size & Forecast by Tire Type

- Pneumatic Tires

- Solid / Foam-Filled Tires

- Airless / Non-Pneumatic Tires

- Market Size & Forecast by Tread Design

- R-1 Standard Agricultural Tread (Diagonal Lug)

- R-1W Deep Agricultural Tread (Wet Conditions)

- R-2 Rice & Cane Field Tread (Flooded / Paddy Field)

- R-3 Turf & Lawn Tread (Low Ground Pressure)

- R-4 Industrial & Multi-Purpose Tread

- Others (R-0 Ribbed, Flotation, Specialty Vineyard & Orchard Tread)

- Market Size & Forecast by Rim Size

- Up to 16 Inches

- 16–24 Inches

- 24–30 Inches

- 30 Inches & Above (Large-Format Agricultural)

- Market Size & Forecast by Inflation Technology

- Standard Inflation Tires

- IF (Improved Flexion) Tires

- VF (Very High Flexion) Tires

- CFO (Cyclic Field Operation) & IF+ Tires

- Market Size & Forecast by Farming Activity Type

- Tillage & Soil Preparation

- Planting & Seeding

- Crop Spraying & Fertiliser Application

- Harvesting & Threshing

- Hay Making & Forage Operations

- Transport & Logistics on Farm

- Irrigation & Water Management

- Market Size & Forecast by Equipment Type

- Tractors

- Two-Wheel Drive (2WD) Tractors

- Four-Wheel Drive (4WD) & All-Wheel Drive (AWD) Tractors

- High-Horsepower Row Crop Tractors

- Compact & Sub-Compact Tractors

- Combine Harvesters & Threshers

- Self-Propelled Sprayers & Applicators

- Planters, Seeders & Drills

- Balers & Forage Harvesters

- Agricultural Trailers & Wagons

- Telehandlers & Agricultural Forklifts

- Others (Specialty Vineyard & Orchard Tractors, ATVs, Utility Vehicles)

- Tractors

- Market Size & Forecast by Application

- Original Equipment Manufacturer (OEM)

- Tier-1 Direct Supply to Agricultural Equipment OEMs

- Tier-2 Component Sub-Supply

- Aftermarket / Replacement

- Independent Agricultural Tire Dealers & Service Centres

- Authorised Dealer & Distributor Networks

- Direct Farm & Co-operative Procurement

- Online & E-Commerce Platforms

- Market Size & Forecast by End-Use Sector

- Agricultural Equipment OEMs

- Global Full-Line Agricultural OEMs (John Deere, CNH Industrial, AGCO, Claas, Kubota, etc.)

- Regional & Specialist Agricultural Equipment OEMs

- Farm Operators & Agricultural Producers

- Large-Scale Commercial & Corporate Farms

- Small & Medium Farm Operators

- Agricultural Co-operatives & Farming Associations

- Government & Public Sector Agri Agencies

- Others (Landscape & Turf Management, Municipal & Golf Course Operators)

- Agricultural Equipment OEMs

- Market Size & Forecast by Sales Channel

- Agricultural Equipment OEM Direct Supply Contracts

- Independent Aftermarket Distributors & Wholesalers

- Authorised Dealer & Service Networks

- Agricultural Co-operative & Farmer Group Procurement

- Online & E-Commerce Platforms

- Government & Public Sector Agricultural Procurement

- Asia-Pacific Agriculture Tire Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Construction Type

- By Tire Type

- By Tread Design

- By Rim Size

- By Inflation Technology

- By Farming Activity Type

- By Equipment Type

- By Application

- By Farm Size

- By End-Use Sector

- By Sales Channel

- Key Demand Drivers (APAC-Specific)

- Competitive Landscape (APAC)

- Europe Agriculture Tire Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Construction Type

- By Tire Type

- By Tread Design

- By Rim Size

- By Inflation Technology

- By Farming Activity Type

- By Equipment Type

- By Application

- By Farm Size

- By End-Use Sector

- By Sales Channel

- Key Demand Drivers (Europe-Specific)

- Competitive Landscape (Europe)

- North America Agriculture Tire Market Outlook

- Market Overview & Strategic Importance

- Market Size & Forecast

- By Value (2020–2035)

- By Construction Type

- By Tire Type

- By Tread Design

- By Rim Size

- By Inflation Technology

- By Farming Activity Type

- By Equipment Type

- By Application

- By Farm Size

- By End-Use Sector

- By Sales Channel

- Key Demand Drivers (North America-Specific)

- Competitive Landscape (North America)

- Latin America Agriculture Tire Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Construction Type

- By Tire Type

- By Tread Design

- By Rim Size

- By Inflation Technology

- By Farming Activity Type

- By Equipment Type

- By Application

- By Farm Size

- By End-Use Sector

- By Sales Channel

- Key Demand Drivers (LATAM-Specific)

- Competitive Landscape (Latin America)

- Middle East & Africa Agriculture Tire Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Construction Type

- By Tire Type

- By Tread Design

- By Rim Size

- By Inflation Technology

- By Farming Activity Type

- By Equipment Type

- By Application

- By Farm Size

- By End-Use Sector

- By Sales Channel

- Key Demand Drivers (MEA-Specific)

- Competitive Landscape (MEA)

- Country-Wise Agriculture Tire Market Outlook

- Market Size & Forecast by Country

- By Value

- By Construction Type

- By Tire Type

- By Tread Design

- By Rim Size

- By Inflation Technology

- By Farming Activity Type

- By Equipment Type

- By Application

- By Farm Size

- By End-Use Sector

- By Sales Channel

- Market Size & Forecast by Country

- Market Size & Forecast

- Market Size & Forecast

- Market Size & Forecast

- Market Size & Forecast

- Original Equipment Manufacturer (OEM)

- Manufacturing Economics & Unit Economics Framework

Countries Covered: United States, Canada, Brazil, Argentina, France, Germany, United Kingdom, Italy, Spain, Poland, Russia, Ukraine, China, India, Japan, Australia, Indonesia, Turkey, South Africa, Nigeria

- Technology Landscape & Innovation Analysis

- Agriculture Tire Technology Maturity Assessment

- Emerging & Disruptive Technologies in Agriculture Tires

- Digital Technologies in Manufacturing Operations & Quality Control

- Tire Pressure Monitoring Systems (TPMS), Central Tire Inflation Systems (CTIS) & Precision Farming Integration

- VF & IF Tire Technology: Low Ground Pressure & Soil Compaction Mitigation

- Technology Readiness & Commercialisation Matrix – Key Agriculture Tire Technologies

- Patent Landscape Analysis

- R&D Investment Benchmarking

- Value Chain & Supply Chain Analysis

- Agriculture Tire Value Chain Mapping

- Supply Chain Concentration & Dependency Analysis

- Key Supplier Mapping by Product & Technology Programme

- Supplier Risk Heat Map

- Make vs Buy Strategy Trends Among Agriculture Tire Manufacturers

- Pricing Analysis

- Agriculture Tire Pricing Dynamics & Mechanisms

- Pricing by Construction Type, Tread Design, Rim Size & Equipment Type

- Total Cost of Ownership (TCO) Analysis – Including Tire Life, Soil Compaction Impact & Fuel Efficiency

- OEM vs Aftermarket Pricing Trends & Benchmarks

- Premium VF/IF Tire vs Standard Bias Tire Pricing & Value Proposition

- Sustainability & Environmental Stewardship

- Environmental & Sustainability Landscape in Agriculture Tire Manufacturing

- Carbon Footprint Benchmarking Across Tire Production Technologies

- Recycled & Bio-Based Material Integration Roadmap for Agriculture Tire Manufacturers

- Agriculture Tire Recyclability & End-of-Life Tire (ELT) Circular Economy Assessment

- Soil Compaction Reduction & Sustainable Farming Pathway Through VF/IF Tire Adoption

- ESG Reporting & Lifecycle Assessment (LCA) in Agriculture Tire Operations

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level: Global Leaders vs Regional Players

- Top 5 Agriculture Tire Manufacturers Market Revenue Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis by Product & Application Segment

- Competitive Intensity Map by Segment & Region

- Player Classification

- Tier-1 Global Integrated Agriculture Tire Manufacturers

- Tier-2 Regional & Specialist Agriculture Tire Manufacturers

- Retread, Repair & Dealer Service Network Players

- Emerging & Disruptive Players

- Competitive Analysis Frameworks

- Market Share Analysis by Product Type & Geography

- R&D Intensity Benchmarking

- OEM Customer Revenue & Long-Term Supply Contract Portfolio Comparison

- Geographic Revenue Exposure Comparison

- Company Profiles

- Company Overview, HQ & Organisational Structure

- Agriculture Tire Products & Services Portfolio

- Revenue Breakdown

- Key OEM Supply Programmes & Agricultural Fleet Deployments

- Manufacturing Footprint & Key Facilities

- Recent Developments (M&A, Partnerships, New Products, Financial Results)

- SWOT Analysis

- Strategic Focus: VF/IF & Radial Tire Innovation, OEM Platform Wins, Dealer Network Expansion

- Strategic Output

- Market Opportunity Matrix

- High-Value Opportunity Quadrant Analysis

- Addressable Market by Segment & Region

- Time-to-Revenue Assessment by Opportunity

- White Space Opportunity Analysis

- Underserved Equipment Type & Farming Activity Type Gaps

- Geographic Markets with Low Penetration

- Technology Gaps with High Commercialisation Potential

- Customer Segment Unmet Needs

- Strategic Recommendations

- Product Portfolio & Innovation Strategy

- Technology & Digitalization Strategy

- Manufacturing Footprint & Capacity Expansion Strategy

- Aftermarket, Retread & Dealer Network Channel Growth Strategy

- Pricing & Commercial Strategy

- Sustainability & Regulatory Compliance Strategy

- Supply Chain & Raw Material Sourcing Strategy

- Partnership, M&A & Expansion Strategy

- Regional Growth Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-Term (2025–2028)

- Mid-Term (2029–2032)

- Long-Term (2033–2036)

- Market Opportunity Matrix

- Market Structure & Concentration