Market Definition

The Agrochemicals market comprises a wide range of crop nutrition and crop protection products, including fertilizers (NPK, micronutrients), biofertilizers, chemical pesticides (herbicides, insecticides, fungicides), and biopesticides, used across diverse agricultural systems to enhance crop yield, soil health, and pest resistance. Agrochemicals form the backbone of global food production systems by improving nutrient availability, managing pest pressures, and enabling farmers to maintain stable productivity despite climatic, biological, and resource constraints. Over the past two years, the global agrochemicals industry has been influenced significantly by geopolitical disruptions, fertilizer price volatility, shifting regulatory frameworks, and rising adoption of sustainable and biological alternatives.

Market Insights

Global agrochemical demand has been strongly shaped by disruptions in fertilizer supply chains triggered by the Russo–Ukrainian conflict, export restrictions by key fertilizer-producing nations, and dramatic fluctuations in raw material prices such as urea, potash, phosphates, and ammonia. The years 2021 and 2022 witnessed elevated fertilizer and pesticide demand due to concerns over food security, volatile commodity markets, and rising pest outbreaks driven by climate variability. Biofertilizers and biopesticides also gained momentum during this period, supported by government incentives, stringent residue regulations, and the growing shift toward regenerative agriculture.

Demand stabilized in 2023 as fertilizer prices corrected and supply chains improved; however, global consumption of agrochemicals remains strong due to continued food demand growth, acreage expansion in emerging markets, and the rising need for high-efficiency inputs. The sector is increasingly shaped by sustainability priorities, such as the transition from synthetic inputs to integrated nutrient management (INM), precision farming, and microbial-based crop protection. Digital farming tools, real-time soil diagnostics, and optimized application technologies are further elevating product efficiency and reducing wastage.

Industry projections indicate that the global agrochemicals market will grow at a moderate CAGR of about 5.45% between 2023 and 2029, supported primarily by Asia-Pacific, Latin America, and Africa, regions that continue to experience strong population growth, lower mechanization levels, and higher fertilizer–crop yield gaps. Meanwhile, Europe and North America are witnessing a structural transition toward low-residue pesticides, biological formulations, micronutrient blends, and fertilizer use-efficiency enhancers as part of broader environmental and carbon reduction policies.

Increasing regulatory scrutiny, especially around chemical pesticide residues, groundwater contamination, and greenhouse gas emissions from nitrogen fertilizers, continues to reshape product portfolios. Countries such as India, China, and Brazil are accelerating domestic manufacturing under localization policies while simultaneously expanding bio-based input production. However, the market remains vulnerable to global feedstock price swings, stringent compliance costs, and evolving sustainability standards that require farmers and manufacturers to rapidly modernize their practices.

Market Dynamics: Drivers

Rising global food demand, expansion of high-value crops, declining soil fertility, and increasing pest and disease pressures continue to drive consistent demand for agrochemical products. Fertilizers remain essential for bridging nutrient gaps in intensive agriculture regions, while pesticide use is supported by rising pest infestations linked to climate change. Government interventions through subsidies, crop support programs, and sustainable farming missions, such as organic transition schemes and biofertilizer adoption incentives, further support market growth. In emerging economies, rapid mechanization, improved farm credit access, and farmer awareness programs accelerate adoption of both chemical and biological inputs.

Market Dynamics: Challenges

The agrochemicals industry faces major challenges, including extreme price volatility of raw materials, supply dependence on select producing nations, and increasingly stringent environmental norms related to runoff, residue levels, and soil degradation. Regulatory bans on select pesticide molecules, high R&D costs, long registration timelines, and data requirements significantly constrain innovation cycles. Environmental pressures and consumer awareness are pushing industry participants toward low-toxicity and residue-free solutions, requiring companies to diversify portfolios and invest in biologicals, nanotechnology, and precision farming tools. Furthermore, counterfeit agrochemicals, fragmented distribution networks, and farmer affordability issues continue to impact product penetration and quality assurance.

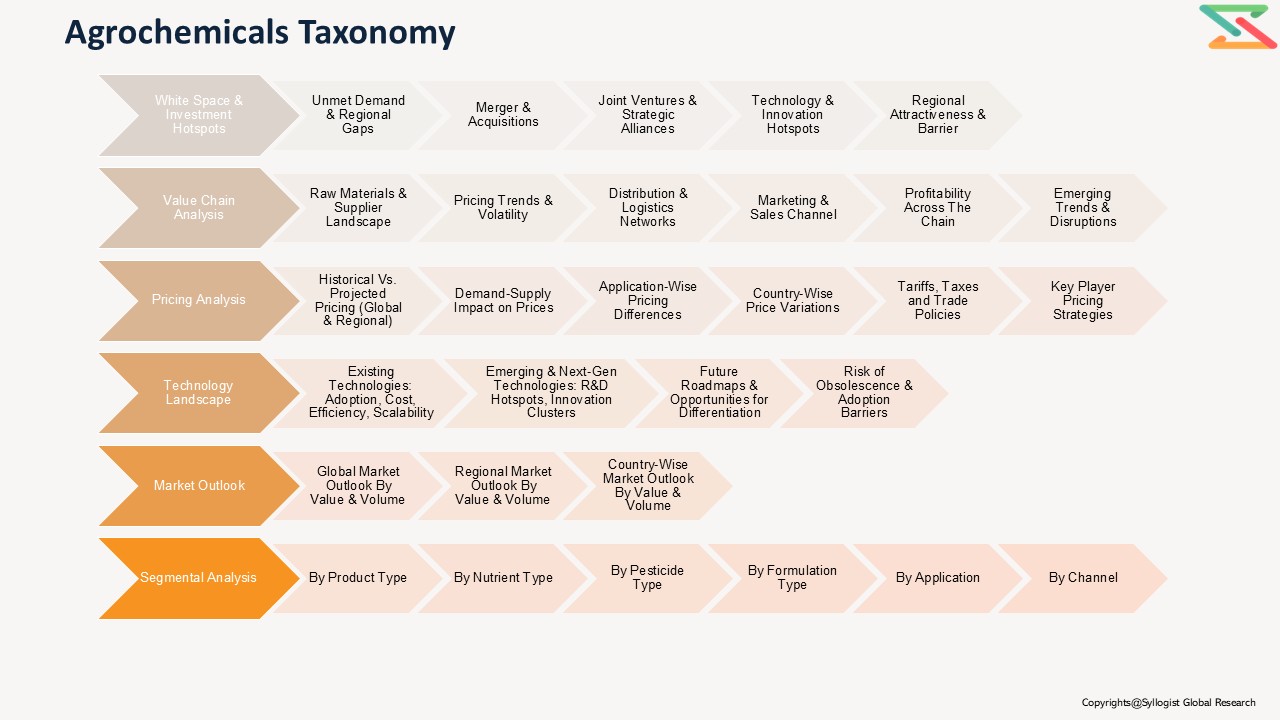

Market Segmentation

Based on Product Type, the Global Agrochemicals Market is segmented into:

- Fertilizers (Nitrogen, Phosphate, Potash, Micronutrients)

- Biofertilizers (Rhizobium, Azotobacter, Mycorrhiza, Others)

- Pesticides (Herbicides, Insecticides, Fungicides)

- Biopesticides (Microbial, Botanical, Biochemical)

- Soil Conditioners & Specialty Nutrients

- Others

Based on Formulation Type:

- Liquid Formulations

- Granules

- Powder/WP

- Emulsifiable Concentrates (EC)

- Suspension Concentrates (SC)

- Water-Dispersible Granules (WDG)

Based on Application:

- Cereals & Grains

- Fruits & Vegetables

- Oilseeds & Pulses

- Plantation Crops

- Commercial/Industrial Crops

- Organic Farming & Regenerative Agriculture

Based on Distribution Channel:

- Retail Dealers

- Cooperatives

- FPOs

- Direct-to-Farmer Digital Platforms

- Government Procurement

All market revenues are presented in USD, with volumes expressed in metric tons (fertilizers/pesticides) or million liters (liquid formulations).

Historical Year: 2020–2025 | Base Year: 2026 | Estimated Year: 2027 | Forecast Period: 2028–2035

Key Questions this Study Will Answer

- What are the key market statistics and forecasts (market size by value and volume, segment shares, growth trends) for the Global Agrochemicals Market?

- What are the region-wise market dynamics, growth drivers, challenges, consumption patterns, and emerging trends?

- What are the key innovations, regulatory shifts, sustainability trends, and opportunities shaping the agrochemicals landscape?

- Who are the major competitors, and how do they perform based on product portfolio strength, pricing, distribution reach, and innovation benchmarks?

- What insights have been derived from farmer surveys, agronomist interviews, and stakeholder consultations conducted during the market assessment?

- Market Foundations & Dynamics

- Introduction

- Product Overview (Definition & Scope of Agrochemicals: Fertilizers, Biofertilizers, Pesticides, Biopesticides)

- Agrochemical Value Chain Overview (Raw Materials → Formulation → Distribution → Farm Application → Crop Output)

- Research Methodology

- Executive Summary

- Major Trends Shaping the Market (Sustainable Farming, Biologicals Adoption, Precision Agriculture, Regulatory Tightening)

- Short-Term vs. Long-Term Opportunities

- Comparison of Key Agrochemical Categories (Synthetic Fertilizers, Biofertilizers, Chemical Pesticides, Biopesticides)

- Scenario Planning (Base, Optimistic, Conservative Adoption of Biological Inputs)

- Sensitivity Analysis (Crop Prices, Monsoon Variability, Input Cost Inflation, Regulatory Changes)

- Identification of Regional Growth Hotspots

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Ecosystem & Value Chain

- Overview of Value Chain Participants

- Basic Chemical Producers (Ammonia, Phosphates, Potash, Technicals for pesticides)

- Bio-Input Developers (Microbial strains, fermentation-based producers)

- Formulation Companies (Wettable powder, EC, SC, granules, liquid bio-inputs)

- Packaging & Application Technology Providers

- Distribution Networks (Dealers, Cooperatives, Retail Chains)

- Farmer Producer Organizations (FPOs) & Agronomy Service Providers

- Raw Material & Equipment Suppliers

- Flow of Value & Material Through the Chain

- Value Addition & Margins at Each Stage

- Manufacturing

- Formulation & Blending

- Branding & Distribution

- On-ground Agronomy Advisory

- Integration Trends (Backward integration into raw materials; forward integration into farmer advisory)

- Impact of Vertical Integration

- Mapping of Roles & Interdependencies

- Market Trends & Developments

- White Space Analysis

- Demand Supply Analysis

- Demand–Supply Gaps (Fertilizer nutrient imbalance, local biofertilizer capacity constraints)

- Unmet Needs (Low-residue solutions, resistance management, microbial stability technologies)

- Risk Assessment Framework

- Political / Geopolitical Risk (Trade restrictions on fertilizers, raw material dependency on Russia/China)

- Operational Risk (Batch failure in fermentation, supply chain delays, climatic impact on demand)

- Environmental Risk (Soil degradation, eutrophication, chemical run-off)

- Financial Risk (Currency volatility in fertilizer imports, subsidy delays)

- Regulatory Framework & Standards

- Global Regulatory Overview

- Fertilizer Standards (ISO, regional nutrient labeling norms)

- Pesticide Registration Regulations (EPA, EU EFSA, OECD guidelines)

- Biologicals Compliance & Registration (FAO/WHO, EU Biological Framework, India FCO amendments)

- Local Country Regulations (EPA, REACH, BIS, FCO, MAPA Brazil)

- Production, Storage & Application Regulations

- Safety & Quality Standards (Nutrient quality, microbial count, pesticide toxicity classes)

- Environmental Compliance (Residue limits, safe disposal, leaching & run-off norms)

- Liability & Insurance Requirements

- Digital Traceability (Blockchain for fertilizers, QR-coded pesticide tracking)

- Technology Landscape

- Fertilizer Technologies (Urea coatings, nano-fertilizers, controlled-release formulations)

- Biological Innovations (Microbial consortia, next-gen biopesticides, fermentation improvements)

- Formulation Technologies (SC/EC/OD/GR, carrier technology, encapsulation, stabilization)

- Monitoring & Precision Application Tools (IoT soil sensors, drones, variable-rate spraying)

- Digital Agronomy Platforms

- Future Outlook (Microbiome engineering, AI-based nutrient modeling, carbon farming inputs)

- Global, Regional & Country Forecasts (2019–2029)

- Global Agrochemicals Market Outlook (Value & Volume)

- Market Share by:

- Product Type: Fertilizer, Biofertilizer, Pesticide, Biopesticide

- Nutrient Type (N, P, K, Secondary, Micronutrients)

- Pesticide Type (Herbicide, Insecticide, Fungicide)

- Formulation Type

- Application (Cereals, Fruits & Vegetables, Plantation Crops, Commercial Crops)

- Channel (Retail, FPOs, Digital Platforms)

- Company

- Regional Outlook (North America, Europe, Asia-Pacific, Latin America, Middle East & Africa)

- Pricing Analysis

- Overview of Pricing Structures (Per kg, per nutrient unit, per acre application)

- Price Trends by Product Type (Urea, DAP, NPK, glyphosate, biologicals)

- Cost Benchmark

- Synthetic vs Biological Inputs

- Imported vs Domestic Production

- Price Sensitivity (Input costs like ammonia, phosphates, solvents, fermentation media)

- Historical Pricing (2019–2023)

- Forecast Pricing (2024–2029)

- Factors Influencing Price

- Raw Material Availability

- Energy Costs

- Logistics

- Regulatory Burden

- R&D & Registration Costs

- Regional Pricing Differentiation

- Impact of Sustainability Transition

- Competition Outlook

- Market Concentration vs Fragmentation

- Company Market Shares

- Competitive Strategies

- Capacity Expansion

- Biological Portfolio Diversification

- Distribution Strengthening

- R&D Alliances

- Benchmarking Matrix (Portfolio Mix vs Scale vs Innovation)

- Recent Developments (M&A, Biological Acquisitions, New Registrations)

- Cost Structure & Margin Analysis

- Detailed Cost Breakdown

- Average Cost per Stage

- Profitability & Margin Distribution

- Sensitivity Analysis (Input costs, crop prices, regulatory delays)

- Cost Reduction Opportunities (Localization, automation, process optimization)

- Business Models & Strategic Insights

- Integrated Agrochemical Producers

- Bio-Input Specialists

- Distribution-Driven Models

- Subscription-Based Agronomy / Output-Based Pricing

- PPP Models in Soil Health & Biological Adoption

- SWOT of Leading Business Models

- Investment & Financial Analysis

- CAPEX & OPEX Benchmarks for Fertilizer Plants, Formulation Units, Fermentation Plants

- Payback & IRR Sensitivity

- Financial Modeling Assumptions

- Revenue Streams: Input Sales, Advisory Services, Bundled Solutions

- Investment Case Studies

- Funding Landscape (Institutional, Agri-Funds, Development Banks)

- Sales & Distribution Channel Analysis

- GTM Channels (Dealers, Retailers, FPOs, Digital Platforms)

- Channel Share by Region

- Typical Channel Flow Diagram (Producer → Distributor → Retailer → Farmer)

- Sales Process & Farmer Engagement

- Distribution Strategy of Leading Players

- Emerging Trends (Embedded Finance, Digital advisory platforms, performance-based models)

- Strategic Recommendations & Roadmap

- Competitor Strategic Initiatives

- Future Outlook (2024–2029: biologicals growth, precision inputs)

- Strategic Recommendations for Stakeholders

- Adoption Roadmap for Biologicals & Sustainable Inputs

- Tailored Recommendations (Producers, Formulators, Investors, Policymakers)

- Key Success Factors (Agronomy advisory, manufacturing localization, digital engagement, compliance)

- Introduction