Market Definition

The Bio-Petrochemical Hybrid Feedstocks Market refers to the industrial convergence of renewable biological inputs and traditional fossil-based hydrocarbons within the chemical manufacturing value chain. This market encompasses the co-processing, co-cracking, and blending of bio-based intermediates, such as vegetable oils, lignin derivatives, or pyrolysis oils, with conventional petrochemical streams like naphtha and natural gas liquids. By integrating these diverse sources into a single production infrastructure, manufacturers can produce drop-in chemicals and performance polymers that maintain identical molecular structures to their fossil counterparts while significantly reducing the overall lifecycle carbon intensity and embedded carbon of the final products.

Market Insights

As of early 2026, the global bio-based chemicals sector is experiencing a period of rapid structural alignment, with the hybrid segment emerging as the preferred pathway for immediate industrial decarbonization. Rather than constructing standalone, high-CapEx biorefineries, integrated chemical majors are increasingly utilizing their existing world-scale steam crackers and refineries to co-process bio-feedstocks. This co-processing strategy allows for a pragmatic transition toward net-zero targets by leveraging billions of dollars in existing infrastructure, effectively lowering the financial barrier for large-scale renewable chemical production.

A major trend in the 2026 landscape is the repurposing of legacy petrochemical sites into hybrid refineries. To accommodate this, companies are installing advanced pre-treatment modules designed to deoxygenate and stabilize bio-oils before they are injected into traditional fluid catalytic cracking (FCC) units or steam crackers. This integration supports the mass balance accounting method, where a percentage of the final output, such as bio-ethylene, bio-propylene, and bio-aromatics, is attributed to the renewable input. This certification allows downstream brands to claim significant carbon reductions without requiring a total disruption of their established global supply chains.

The focus of the hybrid market has moved beyond basic biofuels toward high-value chemical intermediates and specialty monomers. Significant research and development investments are flowing into the production of bio-cumene and bio-benzene pathways, which serve as the precursors for essential building blocks like phenol and acetone. These intermediates are critical for the manufacturing of high-performance polycarbonates, epoxy resins, and engineering plastics used in the automotive and electronics sectors. By utilizing hybrid feedstocks, manufacturers can provide green variants of these essential chemical families that meet the same rigorous purity and performance specifications as their fossil-derived equivalents.

From a regional perspective, the market is defined by a shift in production capacity toward the Asia-Pacific region, despite Europe and North America leading in regulatory frameworks. Southeast Asia, in particular, is emerging as a critical hub for the hybrid market due to its abundant supply of agricultural residues and waste-based oils. By 2026, regional hubs are increasingly focusing on localized hybrid ecosystems that link domestic biomass availability with established petrochemical complexes. This proximity effectively lowers logistics costs and enhances supply chain resilience against the volatility of global crude oil and natural gas prices.

Key Drivers

Aggressive Regulatory Mandates and Carbon Pricing

The primary driver of the market is the global implementation of rigorous decarbonization mandates and the expansion of carbon pricing mechanisms. Regulators in major economies are hard-coding lifecycle carbon intensity reductions into industrial and fuel policies, such as the EU’s RED III and the U.S. Renewable Fuel Standard. In 2026, the implementation of mechanisms like the Carbon Border Adjustment Mechanism (CBAM) is compelling global chemical producers to integrate lower-carbon bio-feedstocks to maintain their competitiveness in high-value export markets and avoid carbon-related penalties.

Surge in Corporate ESG Commitments and Downstream Demand

A secondary driver is the escalating demand for sustainable materials from consumer-facing brands in the packaging, apparel, and automotive sectors. These organizations are actively seeking to reduce their Scope 3 emissions and are increasingly willing to pay a green premium for bio-attributed chemicals and polymers to meet their 2030 net-zero targets. This market pull provides the long-term offtake certainty required for chemical majors to commit to the multi-million dollar investments needed for process optimization and hybrid feedstock integration.

Key Challenges

Technical Complexity and Feedstock Pre-treatment Costs

A significant challenge lies in the logistical and technical difficulty of handling heterogeneous biomass-derived feedstocks. Unlike consistent petrochemical streams, bio-feedstocks often contain high levels of oxygen, moisture, and inorganic impurities that can cause catalyst poisoning and foul refinery equipment. In 2026, the industry continues to struggle with the high operational costs associated with the advanced pre-treatment and upgrading processes required to make renewable inputs fully compatible with high-precision petrochemical infrastructure.

Economic Viability and Feedstock Price Volatility

Despite technological advancements, the cost of bio-based chemical production remains significantly higher than traditional fossil-only routes, with premiums often ranging from 20% to over 100%. This economic gap is exacerbated by the inherent volatility of both agricultural commodity prices and global energy markets. Without a stable and significant green premium or robust carbon taxes across all regions, many hybrid feedstock projects face difficulty in achieving a competitive internal rate of return (IRR), particularly in commoditized segments of the high-volume chemical market.

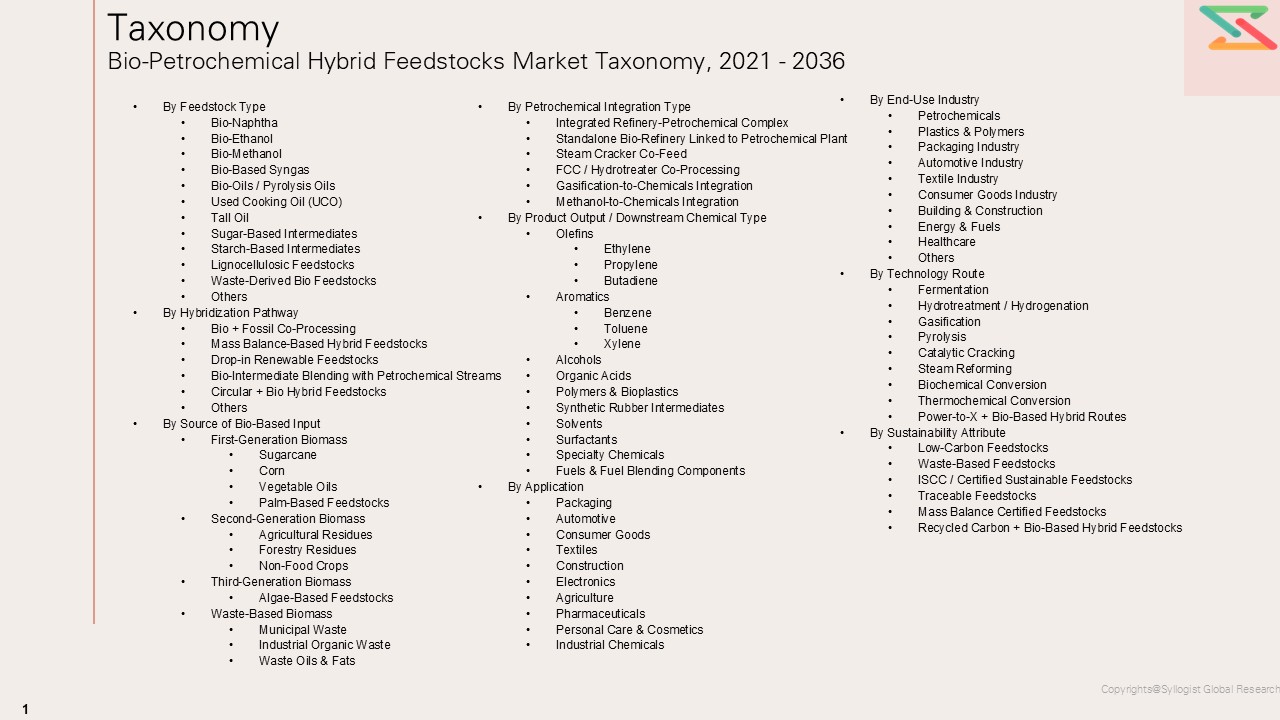

Market Segmentation

- Segmentation By Feedstock Type

- Bio-Naphtha

- Bio-Ethanol

- Bio-Methanol

- Bio-Based Syngas

- Bio-Oils / Pyrolysis Oils

- Used Cooking Oil (UCO)

- Tall Oil

- Sugar-Based Intermediates

- Starch-Based Intermediates

- Lignocellulosic Feedstocks

- Waste-Derived Bio Feedstocks

- Others

- Segmentation By Hybridization Pathway

- Bio + Fossil Co-Processing

- Mass Balance-Based Hybrid Feedstocks

- Drop-in Renewable Feedstocks

- Bio-Intermediate Blending with Petrochemical Streams

- Circular + Bio Hybrid Feedstocks

- Others

- Segmentation By Source of Bio-Based Input

- First-Generation Biomass

- Sugarcane

- Corn

- Vegetable Oils

- Palm-Based Feedstocks

- Second-Generation Biomass

- Agricultural Residues

- Forestry Residues

- Non-Food Crops

- Third-Generation Biomass

- Algae-Based Feedstocks

- Waste-Based Biomass

- Municipal Waste

- Industrial Organic Waste

- Waste Oils & Fats

- Segmentation By Petrochemical Integration Type

- Integrated Refinery-Petrochemical Complex

- Standalone Bio-Refinery Linked to Petrochemical Plant

- Steam Cracker Co-Feed

- FCC / Hydrotreater Co-Processing

- Gasification-to-Chemicals Integration

- Methanol-to-Chemicals Integration

- Segmentation By Product Output / Downstream Chemical Type

- Olefins

- Ethylene

- Propylene

- Butadiene

- Aromatics

- Benzene

- Toluene

- Xylene

- Alcohols

- Organic Acids

- Polymers & Bioplastics

- Synthetic Rubber Intermediates

- Solvents

- Surfactants

- Specialty Chemicals

- Fuels & Fuel Blending Components

- Segmentation By Application

- Packaging

- Automotive

- Consumer Goods

- Textiles

- Construction

- Electronics

- Agriculture

- Pharmaceuticals

- Personal Care & Cosmetics

- Industrial Chemicals

- Segmentation By End-Use Industry

- Petrochemicals

- Plastics & Polymers

- Packaging Industry

- Automotive Industry

- Textile Industry

- Consumer Goods Industry

- Building & Construction

- Energy & Fuels

- Healthcare

- Others

- By Technology Route

- Fermentation

- Hydrotreatment / Hydrogenation

- Gasification

- Pyrolysis

- Catalytic Cracking

- Steam Reforming

- Biochemical Conversion

- Thermochemical Conversion

- Power-to-X + Bio-Based Hybrid Routes

- By Sustainability Attribute

- Low-Carbon Feedstocks

- Waste-Based Feedstocks

- ISCC / Certified Sustainable Feedstocks

- Traceable Feedstocks

- Mass Balance Certified Feedstocks

- Recycled Carbon + Bio-Based Hybrid Feedstocks

All market revenues are presented in USD

Historical Year: 2021–2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027–2036

Key Questions this Study Will Answer

- What is the projected global market valuation and volume (MT) for bio-petrochemical hybrid feedstocks through 2031? This provides the quantitative baseline required for long-term strategic planning and capital allocation across the chemical value chain.

- How will the implementation of global carbon pricing and mechanisms like the EU’s Carbon Border Adjustment Mechanism (CBAM) accelerate the adoption of hybrid co-processing? The study will analyze how regulatory costs are narrowing the price gap between traditional fossil feedstocks and their lower-carbon renewable counterparts.

- Which specific bio-based inputs (e.g., lignin, pyrolysis oils, or waste-derived lipids) offer the highest compatibility and yield when integrated into existing steam crackers? This question focuses on the technical drop-in potential and the pre-treatment requirements needed to maintain infrastructure integrity.

- What is the expected evolution of green premiums, and to what extent will downstream consumer brands commit to long-term offtake agreements for bio-attributed materials? This analysis evaluates the willingness of sectors like packaging and automotive to fund the transition through certified mass-balance products.

- Who are the leading petrochemical incumbents and technology providers currently dominating the hybrid refinery space, and what are their strategic moats regarding catalyst IP and feedstock procurement? A detailed competitive landscape will reveal which players have successfully integrated renewable streams into world-scale operations.

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Consumer & Demand Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Geographic & Regional Trends

- Risk Assessment Framework

- Political / Geopolitical Risk

- Fuel & Component Supply Risk

- Environmental and Regulatory Risk

- Financial / Market Risk

- Regulatory Framework & Standards

- Global Bio-Petrochemical Hybrid Feedstocks Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Feedstock Type

- Bio-Naphtha

- Bio-Ethanol

- Bio-Methanol

- Bio-Based Syngas

- Bio-Oils / Pyrolysis Oils

- Used Cooking Oil (UCO)

- Tall Oil

- Sugar-Based Intermediates

- Starch-Based Intermediates

- Lignocellulosic Feedstocks

- Waste-Derived Bio Feedstocks

- Others

- Market Size & Forecast by Hybridization Pathway

- Bio + Fossil Co-Processing

- Mass Balance-Based Hybrid Feedstocks

- Drop-in Renewable Feedstocks

- Bio-Intermediate Blending with Petrochemical Streams

- Circular + Bio Hybrid Feedstocks

- Others

- Market Size & Forecast by Source of Bio-Based Input

- First-Generation Biomass

- Sugarcane

- Corn

- Vegetable Oils

- Palm-Based Feedstocks

- Second-Generation Biomass

- Agricultural Residues

- Forestry Residues

- Non-Food Crops

- Third-Generation Biomass

- Algae-Based Feedstocks

- Waste-Based Biomass

- Municipal Waste

- Industrial Organic Waste

- Waste Oils & Fats

- First-Generation Biomass

- Market Size & Forecast by Petrochemical Integration Type

- Integrated Refinery-Petrochemical Complex

- Standalone Bio-Refinery Linked to Petrochemical Plant

- Steam Cracker Co-Feed

- FCC / Hydrotreater Co-Processing

- Gasification-to-Chemicals Integration

- Methanol-to-Chemicals Integration

- Market Size & Forecast by Product Output / Downstream Chemical Type

- Olefins

- Ethylene

- Propylene

- Butadiene

- Aromatics

- Benzene

- Toluene

- Xylene

- Alcohols

- Organic Acids

- Polymers & Bioplastics

- Synthetic Rubber Intermediates

- Solvents

- Surfactants

- Specialty Chemicals

- Fuels & Fuel Blending Components

- Olefins

- Market Size & Forecast by Application

- Packaging

- Automotive

- Consumer Goods

- Textiles

- Construction

- Electronics

- Agriculture

- Pharmaceuticals

- Personal Care & Cosmetics

- Industrial Chemicals

- Market Size & Forecast by End-Use Industry

- Petrochemicals

- Plastics & Polymers

- Packaging Industry

- Automotive Industry

- Textile Industry

- Consumer Goods Industry

- Building & Construction

- Energy & Fuels

- Healthcare

- Others

- Market Size & Forecast by Technology Route

- Fermentation

- Hydrotreatment / Hydrogenation

- Gasification

- Pyrolysis

- Catalytic Cracking

- Steam Reforming

- Biochemical Conversion

- Thermochemical Conversion

- Power-to-X + Bio-Based Hybrid Routes

- Market Size & Forecast by Sustainability Attribute

- Low-Carbon Feedstocks

- Waste-Based Feedstocks

- ISCC / Certified Sustainable Feedstocks

- Traceable Feedstocks

- Mass Balance Certified Feedstocks

- Recycled Carbon + Bio-Based Hybrid Feedstocks

- Asia-Pacific Bio-Petrochemical Hybrid Feedstocks Market Outlook

- Market Size & Forecast

- By Value

- By Feedstock Type

- By Hybridization Pathway

- By Source of Bio-Based Input

- By Petrochemical Integration Type

- By Product Output / Downstream Chemical Type

- By Application

- By End-Use Industry

- By Technology Route

- By Sustainability Attribute

- Market Size & Forecast

- Europe Bio-Petrochemical Hybrid Feedstocks Market Outlook

- Market Size & Forecast

- By Value

- By Feedstock Type

- By Hybridization Pathway

- By Source of Bio-Based Input

- By Petrochemical Integration Type

- By Product Output / Downstream Chemical Type

- By Application

- By End-Use Industry

- By Technology Route

- By Sustainability Attribute

- Market Size & Forecast

- North America Bio-Petrochemical Hybrid Feedstocks Market Outlook

- Market Size & Forecast

- By Value

- By Feedstock Type

- By Hybridization Pathway

- By Source of Bio-Based Input

- By Petrochemical Integration Type

- By Product Output / Downstream Chemical Type

- By Application

- By End-Use Industry

- By Technology Route

- By Sustainability Attribute

- Market Size & Forecast

- Latin America Bio-Petrochemical Hybrid Feedstocks Market Outlook

- Market Size & Forecast

- By Value

- By Feedstock Type

- By Hybridization Pathway

- By Source of Bio-Based Input

- By Petrochemical Integration Type

- By Product Output / Downstream Chemical Type

- By Application

- By End-Use Industry

- By Technology Route

- By Sustainability Attribute

- Market Size & Forecast

- Middle East & Africa Bio-Petrochemical Hybrid Feedstocks Market Outlook

- Market Size & Forecast

- By Value

- By Feedstock Type

- By Hybridization Pathway

- By Source of Bio-Based Input

- By Petrochemical Integration Type

- By Product Output / Downstream Chemical Type

- By Application

- By End-Use Industry

- By Technology Route

- By Sustainability Attribute

- Market Size & Forecast

- Country Wise* Bio-Petrochemical Hybrid Feedstocks Market Outlook

- Market Size & Forecast

- By Value

- By Feedstock Type

- By Hybridization Pathway

- By Source of Bio-Based Input

- By Petrochemical Integration Type

- By Product Output / Downstream Chemical Type

- By Application

- By End-Use Industry

- By Technology Route

- By Sustainability Attribute

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Germany, United Kingdom, France, Italy, Spain, Netherlands, Switzerland, China, Japan, India, South Korea, Australia, Brazil, Mexico, Saudi Arabia, South Africa, UAE

- Technology Landscape & Innovation Analysis

- Value Chain & Supply Chain Analysis

- Pricing Analysis

- Sustainability & Energy Efficiency

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented Vs Consolidated)

- Top 5 Players Market Share

- HHI (Herfindahl–Hirschman Index) Concentration Analysis

- Competitive Intensity Map

- Player Classification

- Market Leaders

- Strong Challengers

- Specialist / Niche Players

- Emerging Players

- Regional Players

- Competitive Analysis Frameworks

- Market Share Analysis

- Company Profile

- Company Overview & HQ

- Products & Solutions Portfolio

- Overall Revenue & Segmental Revenue

- Geographic Presence

- Recent Developments (M&A, Launches, Partnerships)

- SWOT Analysis

- Strategic Focus Areas

- Competitive Positioning Map

- Market Structure & Concentration

- Strategic Output

- Market Opportunity Matrix

- White Space Opportunity Analysis

- Strategic Recommendations

- Feedstock Sourcing Strategy

- Technology & Process Optimization Strategy

- Refinery–Petrochemical Integration Strategy

- Product Portfolio Strategy

- Pricing & Commercial Strategy

- Sustainability & Certification Strategy

- Supply Chain & Logistics Strategy

- Partnership & Expansion Strategy

- Regional Growth Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025–2028)

- Mid-term (2029–2032)

- Long-term (2033–2036)