Market Definition

Biodiesel is a renewable, biodegradable fuel manufactured through transesterification of vegetable oils, animal fats, or waste cooking oils with alcohols (typically methanol). It serves as a substitute or blend component for petroleum diesel, offering reduced greenhouse gas emissions and improved lubricity. Biodiesel is commonly categorized by blend levels:

- B5 (up to 5% biodiesel, 95% petroleum diesel)

- B6–B20 (moderate blends, widely used in fleets)

- B100 (pure biodiesel, niche applications)

Market Insights

In 2023, the market value stood at USD 43,095 million, rising modestly to USD 44,603 million in 2024. This incremental growth reflects stable demand supported by regulatory mandates and ongoing adoption in transportation and industrial sectors. By 2030, the market is projected to reach USD 55,324 million, representing a significant expansion of about 24% compared to 2024. The long-term outlook is even stronger, with the market expected to climb to USD 65,707 million by 2035, marking nearly 47% growth from 2024 levels. This consistent upward trend underscores the resilience of biodiesel despite challenges such as feedstock price volatility and competition from renewable diesel. The forecast suggests that policy support, sustainability initiatives, and feedstock diversification will remain central to driving growth, positioning biodiesel as a reliable contributor to global energy transition strategies.

The biodiesel market in 2026 is still fundamentally policy-led, but the most important structural change is that biodiesel is no longer competing only with petroleum diesel, it is increasingly competing within the broader pool of “low-carbon diesel substitutes,” especially renewable diesel (HVO) in markets where refinery integration and drop-in performance matter. Blending mandates, carbon-intensity programs, and tax/credit mechanisms continue to create “must-blend” demand, so consumption often rises or falls less with pure fuel demand and more with regulatory volumes, credit prices, and eligibility rules. As governments tighten transport decarbonization targets, demand is also spreading beyond conventional road blends into adjacent sectors (and compliance regimes), which increases competition for the same limited set of sustainable feedstocks.

Biodiesel economics are dominated by feedstock, and that is where most margin volatility comes from. In most plants, oils and fats account for the large majority of variable cost, so profitability swings more with soy/rapeseed/palm oil cycles, used cooking oil (UCO) and tallow availability, and sustainability certification outcomes than with refinery “crack spreads” alone. When vegetable oil prices rise (weather shocks, crush constraints, food demand), producers face margin compression unless policy credits and blend economics expand in tandem. Conversely, when waste and residue feedstocks become scarce or expensive, often due to traceability tightening, fraud concerns, and cross-sector demand, premiums widen and disadvantage smaller producers without strong procurement networks. The result is a market where secure feedstock access and optionality (ability to switch among multiple oils/fats) is often more valuable than nameplate capacity.

Market Dynamics: Drivers

Regionally, the biodiesel market’s direction is increasingly being set by mandate decisions and credit-market design, not just by underlying diesel demand. In the United States, the Renewable Fuel Standard, and especially how biomass-based diesel volumes are set, can quickly swing expectations for soybean oil demand and for biodiesel/renewable diesel credit values, which then ripple through producer margins, run rates, and import/export economics. In Europe, the push for higher renewable content and greenhouse-gas intensity reduction, paired with tighter sustainability requirements, tends to favor pathways and feedstocks that can demonstrate strong compliance and lower indirect land-use change (ILUC) risk, reinforcing the premium for waste/residue lipids such as used cooking oil (UCO) and tallow. In Indonesia, higher blends (such as B40 and ambitions toward B50) can pull significant palm-derived supply into domestic fuel use, tightening export availability and influencing global pricing. In South America, higher blending mandates, particularly where they absorb more soybean oil domestically, can redraw trade flows, reducing exportable surplus and shifting import dependencies elsewhere.

Market Dynamics: Challenges

Operationally, an underestimated constraint is infrastructure and fuel quality management. Even where production is available, real bottlenecks show up in blending terminals, storage segregation, cold-flow compliance in winter markets, and OEM/fleet acceptance, especially at higher blends. This is why integrated players that can manage logistics, guarantee spec compliance, and support customers with blending guidance tend to win offtake contracts. Alongside this, sustainability proof is becoming a “license to operate”: buyers and regulators increasingly demand auditable chain-of-custody for UCO and residues, robust certification, and defensible lifecycle carbon accounting, which raises compliance costs but also creates a moat for producers with strong governance and traceability systems.

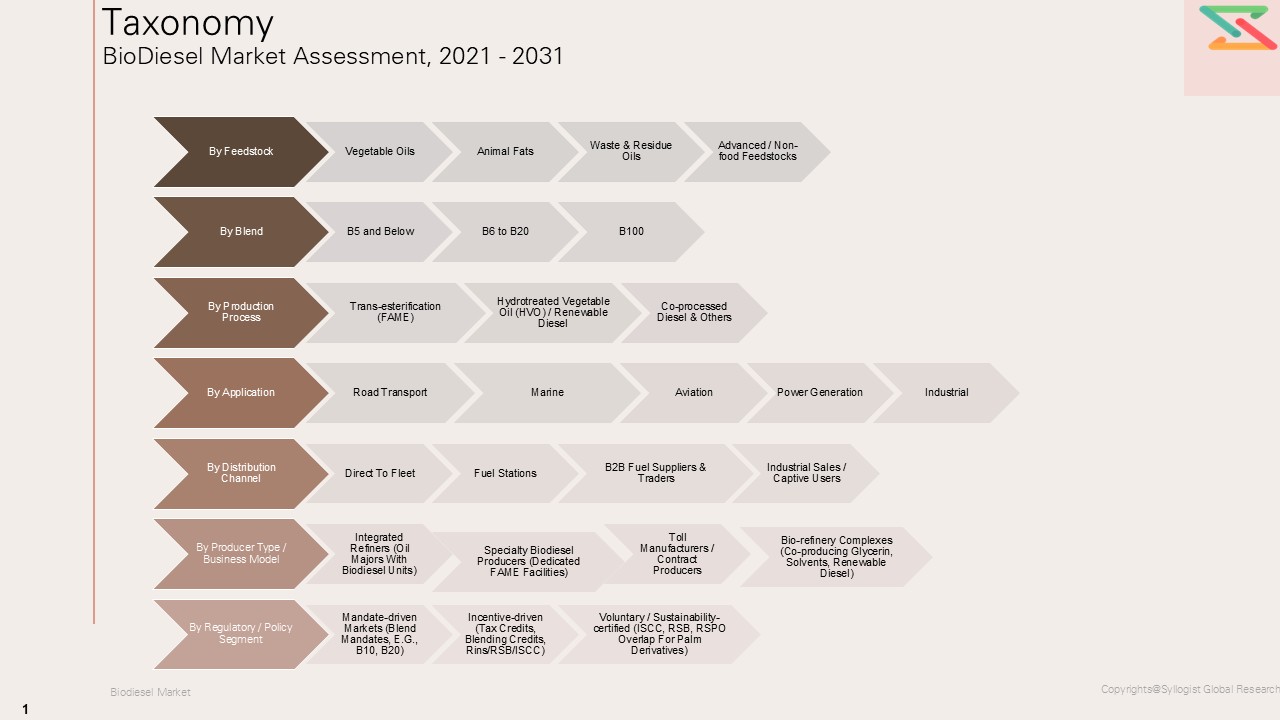

Market Segmentation

- By Feedstock

- Soybean Oil

- Palm Oil

- Rapeseed Oil

- Animal Fats

- UCO

- Algae

- Others

- By Production Process

- Transesterification

- Enzymatic

- Hydro-Processing

- By Application / End-Use

- Transportation

- Power Generation

- Marine

- Industrial

- By Blend

- B5

- B10

- B20

- B50

- B100

- By Distribution Channel

- Direct Sales

- Distributors

- Blending Terminals

- By Region

All market revenues are presented in USD, with production volumes expressed in metric tons and operating rates expressed as percentage capacity utilization.

Historical Year: 2021–2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027–2031

Key Questions this Study Will Answer

- What are the key market statistics and forecasts (market size by value and volume, derivative split, regional growth trends) for the Global biodiesel Market?

- What are the region-wise supply-demand balances, trade flows, and feedstock linkages?

- How are feedstock volatility, energy pricing, and regulatory mandates shaping profitability?

- Who are the leading producers, and how do they benchmark across integration depth, cost position, derivative portfolio, and regional footprint?

- What insights emerge from interviews with producers, derivative manufacturers, traders, and downstream end-users conducted during the market assessment?

- Market Foundations & Dynamics

- Introduction

- Product Overview (Definition & Scope of Biodiesel)

- Biodiesel Production Process Overview (Feedstock → Transesterification → Biodiesel & Glycerin)

- Research Methodology

- Executive Summary

- Major Trends Shaping the Biodiesel Market

- Short-Term vs. Long-Term Opportunitie

- Comparison of Biodiesel vs. Renewable Diesel vs. Bioethanol

- Scenario Planning (Base, Optimistic, Conservative)

- Sensitivity Analysis

- Identification of Regional Investment Hotspots

- Market Dynamics (Drivers, Restraints, Opportunities, Challenges, Porter’s Five Forces Analysis, PESTLE Analysis)

- Market Ecosystem & Value Chain

- Overview of Value Chain Participants

- Feedstock Producers (Soybean, Palm, Rapeseed, Used Cooking Oil, Animal Fat Suppliers)

- Biodiesel Producers / Refiners

- Technology Providers (Transesterification, Catalysts, Process Equipment)

- Distributors / Blenders / Oil Marketing Companies

- End-Use Sectors (Transportation, Power Generation, Marine, Agriculture, Aviation – SAF blending)

- Regulatory Bodies & Certification Agencies

- Flow of Value and Material Through the Chain

- Value Addition and Margins at Each Stage

- Feedstock Procurement

- Feedstock Procurement

- Processing & Refining

- Distribution / Blending

- Retail / End-Use

- Value Addition and Margins at Each Stage

- Integration Trends (Vertically Integrated Biofuel Companies vs. Independent Blenders)

- Impact of Vertical Integration

- Mapping of Roles and Interdependencies

- Market Trends & Developments

- Emerging Feedstock Trends (Waste Oils, Algae, Advanced Feedstocks)

- Feedstock Availability and Competition with Food Crops

- Blending Mandates and Renewable Energy Targets

- Technological Advancements (Continuous Transesterification, Enzymatic Catalysis, Process Efficiency)

- Demand–Supply Gaps

- Investment Hotspots

- Unmet Needs and White Market Spaces

- Risk Assessment Framework

- Political / Geopolitical Risk

- Feedstock Supply Risk

- Environmental and Regulatory Risk

- Financial / Market Risk

- Regulatory Framework & Standards

- Global Policy and Mandate Overview

- EU Renewable Energy Directive (RED II / RED III)

- S. EPA Renewable Fuel Standard (RFS) & California LCFS

- Brazil’s National Biodiesel Program (PNPB)

- Indonesia’s B30–B50 Mandates

- India’s National Biofuel Policy (E20, B20 Targets)

- China and ASEAN Biodiesel Policies

- Compliance & Certification Requirements (ISCC, RSPO, ASTM D6751, EN 14214)

- Transportation and Storage Regulations

- Sustainability and GHG Reduction Standards

- Environmental & Liability Considerations

- Global Policy and Mandate Overview

- Technology Landscape

- Overview of Biodiesel Production Technologies

- Transesterification (Base / Acid / Enzymatic Catalysis)

- Feedstock Pretreatment and Refining Technologies

- Process Intensification and Continuous Flow Systems

- Glycerin Utilization Technologies

- Cost Optimization Technologies (Automation, Energy Recovery, Catalyst Efficiency)

- Future Outlook: Next-Gen Biofuels (Algae, Fischer–Tropsch Biodiesel, Hydrotreated Vegetable Oil)

- Overview of Biodiesel Production Technologies

- Global, Regional & Country Forecasts (2021–2031)

- Global Biodiesel Market Outlook (Value & Volume)

- Market Share by:

- Feedstock (Soybean Oil, Palm Oil, Rapeseed Oil, Animal Fats, UCO, Algae, Others)

- Production Process (Transesterification, Enzymatic, Hydro-Processing)

- Application / End-Use (Transportation, Power Generation, Marine, Industrial)

- Blend (B5, B10, B20, B50, B100)

- Distribution Channel (Direct Sales, Distributors, Blending Terminals)

- Region

- Regional & Country Outlook (2021–2031)

- Asia-Pacific: Indonesia, Malaysia, Thailand, China, India, Australia

- Europe: Germany, France, Spain, Italy, Netherlands, UK

- North America: United States, Canada, Mexico

- Latin America: Brazil, Argentina, Colombia, Chile

- Middle East & Africa: South Africa, Nigeria, Egypt, UAE, Saudi Arabia

- Pricing Analysis

- Overview of Pricing Structures (per Liter / per Gallon Basis)

- Average Selling Price Trends by Feedstock and Region

- Cost Benchmark: Biodiesel vs. Fossil Diesel vs. Renewable Diesel

- Historical Price Evolution

- Forecast Pricing Curve

- Factors Influencing Price:

- Feedstock Cost Volatility

- Production Efficiency

- Policy Incentives / Carbon Credit Value

- Logistics & Blending Costs

- Regional Pricing Differentiation (EU vs. U.S. vs. Asia-Pacific)

- Competition Outlook

- Market Concentration and Fragmentation Level

- Company Market Shares (Top 10 Producers)

- Competitive Strategies

- Feedstock Integration

- Technology Partnerships

- Capacity Expansions and Joint Ventures

- Benchmarking Matrix (Feedstock Diversity vs. Scale vs. Regional Reach)

- Recent Developments: Partnerships, M&A, and Policy-Driven Expansions

- Cost Structure & Margin Analysis

- Detailed Cost Breakdown

- Feedstock Procurement

- Catalyst / Processing Cost

- Energy and Utilities

- Transportation / Blending / Storage

- Labor and Certification

- Average Cost per Liter

- Profitability and Margin Distribution Along the Value Chain

- Sensitivity Analysis: How Feedstock Price and Policy Incentives Impact Margin

- Cost Reduction Opportunities through Process Optimization

- Detailed Cost Breakdown

- Business Models & Strategic Insights

- Vertically Integrated Biofuel Companies

- Independent Biodiesel Producers

- Public–Private Partnership (PPP) Models

- Joint Ventures with Oil & Gas Firms

- Circular Economy and Waste-Based Feedstock Models

- SWOT Analysis of Leading Business Models

- Investment & Financial Analysis

- CAPEX and OPEX Benchmarks for Biodiesel Plants

- Payback Period and IRR Sensitivity (by Feedstock and Region)

- Financial Modeling Assumptions (Yield, Feedstock Mix, Carbon Credit Value)

- Revenue Streams:

- Biodiesel Sales

- Glycerin Sales

- Carbon Credits / Renewable Fuel Certificates

- Blending Incentives and Subsidies

- Investment Case Studies

- Funding Landscape: Government Grants, Green Bonds, Venture & Private Investments

- Sales & Distribution Channel Analysis

- Overview of Go-to-Market Channels

- Direct Sales to Oil Marketing Companies

- Distributors / Blenders / Traders

- Partnerships with Fuel Retailers

- Online B2B Platforms for Biofuels

- Channel Share by Region

- Distribution Strategies by Leading Players

- Emerging Trends: Blending Infrastructure, Decentralized Production Units

- Overview of Go-to-Market Channels

- Strategic Recommendations & Roadmap

- Competitors’ Strategic Initiatives

- Future Outlook (Next 5–10 Years, Emerging Players, Success Factors)

- Strategic Recommendations

- Technology Advancements to Watch

- Circular Biofuel Integration Roadmap (2021–2031)

- Biodiesel Market Acceleration Roadmap

- Short-Term

- Mid-Term

- Long-Term

- Tailored Recommendations for:

- Biodiesel Producers

- Feedstock Suppliers

- Policymakers / Regulators

- Investors

- Recommendations on Key Success Factors

- Feedstock Security

- Technology Partnerships

- Policy Alignment

- Supply Chain Integration

- Investor Confidence

- Market Share by:

- Global Biodiesel Market Outlook (Value & Volume)

- Overview of Value Chain Participants

- Introduction