Market Definition

The Global Circular Aluminum Economy Market encompasses the integrated system of activities, technologies, policies, business models, and commercial relationships that collectively enable aluminum and aluminum alloy materials to be recovered, reprocessed, and reintroduced into productive use at the highest possible value and with the lowest feasible energy and environmental cost throughout their end-of-life and post-industrial lifecycle. The circular aluminum economy represents a fundamental reorientation of the conventional linear aluminum value chain, in which primary aluminum is smelted from bauxite ore through an energy-intensive electrolytic reduction process and ultimately discarded at end of product life, toward a regenerative model in which aluminum scrap and waste streams are systematically captured, sorted, refined, remelted, and recycled into secondary aluminum products that substitute for primary aluminum across a broad range of industrial and commercial applications. This market encompasses the full spectrum of aluminum circularity activities, including post-consumer scrap collection and aggregation from end-of-life vehicles, construction demolition materials, packaging waste, consumer electronics, and industrial equipment; post-industrial and manufacturing process scrap recovery and direct remelting; aluminum scrap sorting, shredding, decoating, and upgrading technologies; secondary smelting and refining operations; closed-loop alloy recovery and wrought alloy remelting processes; aluminum dross and salt cake reprocessing; and the commercial trading, logistics, and certification infrastructure that connects material flows across the secondary aluminum value chain. The market is further defined by the enabling policy and regulatory landscape that governs extended producer responsibility frameworks, recycled content mandates, carbon border adjustment mechanisms, and green procurement standards across major aluminum-consuming industries and jurisdictions. Stakeholders operating within this ecosystem include primary and secondary aluminum producers, scrap dealers and aggregators, sorting and processing technology providers, automotive and aerospace recyclers, packaging material recovery organizations, industrial waste management companies, secondary alloy foundries, specialty metals refiners, financial institutions providing green finance for circular infrastructure investment, and regulatory bodies whose mandates shape the economic incentives and obligations that determine the commercial viability of circular aluminum business models globally.

Market Insights

The global circular aluminum economy market is operating in a period of accelerating structural transformation as of 2026, driven by the convergence of intensifying corporate decarbonization commitments, tightening regulatory frameworks for industrial carbon accountability, and the growing recognition across aluminum-consuming industries that the energy intensity differential between primary and secondary aluminum production represents one of the most commercially accessible and cost-effective levers available for reducing the embodied carbon of manufactured products. Secondary aluminum production requires a fraction of the energy consumed in primary smelting from bauxite ore, and this fundamental thermodynamic advantage is being translated into a powerful competitive and regulatory differentiator as carbon pricing mechanisms, product carbon footprint disclosure requirements, and supply chain sustainability standards progressively assign a financial and reputational value to low-carbon material sourcing decisions. The market is consequently experiencing a structural shift in the premium assigned to certified low-carbon secondary aluminum, with buyers across the automotive, packaging, aerospace, and construction sectors increasingly willing to pay a measurable price premium for products manufactured with high recycled content and verifiable green credentials, creating commercial incentives for investment in circular aluminum infrastructure that did not exist in equivalent form in earlier market cycles.

A defining structural development reshaping the commercial landscape of the circular aluminum economy is the progressive tightening of the quality gap between secondary aluminum alloys produced from recycled scrap and the performance specifications of primary aluminum products in the most demanding end-use applications, driven by advances in scrap sorting technology, alloy-specific recovery processes, and secondary refining capabilities that are enabling producers of recycled aluminum to meet specifications previously accessible only through primary production routes. The deployment of sensor-based scrap sorting systems incorporating X-ray fluorescence, laser-induced breakdown spectroscopy, and advanced optical recognition technologies is enabling the separation of post-consumer aluminum scrap streams by alloy family and even individual alloy grade with an accuracy and throughput that is commercially transforming the economics of high-purity recycled aluminum production. This improvement in sorted scrap quality is enabling secondary producers to manufacture closed-loop recycled wrought aluminum products for applications in automotive body panels, aerospace structural components, and high-specification packaging alloys where alloy composition tolerances are narrow and contamination thresholds are strictly controlled, broadening the addressable market for secondary aluminum beyond the traditional cast alloy and foundry applications that have historically dominated the recycled material output mix.

The automotive sector is functioning as the most commercially consequential arena for circular aluminum economy development across the forecast period, with the intersection of lightweighting-driven aluminum content growth per vehicle, the accelerating adoption of battery electric vehicle platforms with elevated aluminum structural requirements, and the strengthening of automotive extended producer responsibility and recycled content regulations collectively creating both a large and growing scrap return flow and a powerful demand pull for secondary aluminum alloys in automotive manufacturing. The shift toward battery electric vehicle architectures is significantly increasing the aluminum content per vehicle through the adoption of large battery enclosures, structural castings, and heat management components that require high-specification aluminum alloys, and the simultaneous deployment of end-of-life vehicle recycling legislation in major automotive markets is ensuring that this elevated aluminum content is systematically recovered at end of vehicle life rather than directed to lower-value shredder residue fractions. Automotive manufacturers are entering into direct material partnerships with secondary aluminum producers and scrap aggregators to establish closed-loop recycling circuits for specific alloy grades, creating a new category of vertically integrated circular material supply chains that offer producers long-term demand visibility and manufacturers verifiable recycled content credentials for product carbon footprint reporting and regulatory compliance purposes.

From a regional perspective, Europe represents the most advanced and policy-driven market for circular aluminum economy development globally, characterized by the most comprehensive extended producer responsibility frameworks, the most stringent carbon pricing environment under the European Union Emissions Trading System and the Carbon Border Adjustment Mechanism, and the highest recycling rates for aluminum packaging and automotive scrap among major economic regions. The European market is setting the regulatory and commercial standards that are progressively being adopted or adapted in other jurisdictions, making it the primary reference point for circular aluminum business model design and investment criteria globally. North America constitutes the largest market by secondary aluminum production volume, supported by well-developed scrap collection infrastructure, a large automotive recycling sector, and growing corporate sustainability commitments from major aluminum consumers in the beverage packaging, automotive, and aerospace sectors. Asia-Pacific, and China in particular, dominates global aluminum scrap trade flows and secondary production capacity by volume, and the progressive tightening of China’s domestic scrap import policies and the expansion of its internal recycling infrastructure are reshaping regional and global scrap material flows in ways that are creating new commercial opportunities for circular economy investment across the Asia-Pacific region. India is emerging as a significant growth market for secondary aluminum production capacity investment, driven by rapidly expanding domestic aluminum demand, supportive government policy for secondary industry development, and a growing scrap generation base from expanding automotive and packaging industries.

Key Drivers

Intensifying Carbon Pricing, Embodied Carbon Disclosure Mandates, and the Regulatory Imperative for Low-Carbon Material Sourcing

The most structurally transformative driver of the global circular aluminum economy market is the progressive implementation of carbon pricing mechanisms, embodied carbon reporting requirements, and supply chain decarbonization regulations across major industrial economies that are systematically assigning a financial cost to the carbon intensity of aluminum production and translating the fundamental energy efficiency advantage of secondary production over primary smelting into a quantified and commercially actionable economic premium for recycled aluminum products. The European Union’s Carbon Border Adjustment Mechanism is imposing carbon costs on imported aluminum products proportional to their production carbon intensity, creating an immediate financial incentive for international aluminum suppliers to the European market to shift toward secondary production or renewable energy-powered primary smelting to maintain cost competitiveness. Product-level environmental product declaration requirements in the construction sector and supply chain carbon disclosure frameworks in the automotive industry are making the embodied carbon content of aluminum inputs a visible and commercially differentiated characteristic in procurement decisions, shifting buyer evaluation criteria from unit price alone toward a total value assessment that incorporates carbon cost, regulatory compliance, and sustainability reporting benefits. These regulatory and disclosure frameworks are expected to progressively tighten across major jurisdictions over the forecast period, providing an escalating and durable policy tailwind for investment in circular aluminum infrastructure, closed-loop recycling technology, and secondary alloy production capacity that directly reduces the embodied carbon of aluminum delivered to end-use markets.

Growing Corporate Sustainability Commitments and the Expansion of Recycled Content Requirements Across Key End-Use Industries

A powerful commercial driver complementing the regulatory framework is the expanding adoption of voluntary and increasingly mandatory recycled content commitments by major corporations across the beverage and food packaging, automotive, consumer electronics, and building and construction sectors, whose procurement decisions collectively represent the dominant share of global aluminum demand and whose sustainability targets are creating direct and structured demand signals for high-recycled-content secondary aluminum products. Global beverage companies, packaging manufacturers, and consumer goods corporations have made public commitments to achieving minimum recycled aluminum content thresholds in their packaging and product materials, and the credibility of these commitments in the context of stakeholder scrutiny, investor ESG evaluation, and consumer sustainability expectations is creating durable procurement preferences that favor secondary aluminum suppliers over primary producers irrespective of short-term price relationships. Automotive manufacturers operating under fleet average carbon intensity regulations and supply chain scope three emission reduction commitments are specifying minimum secondary aluminum content targets in material procurement standards for vehicle body, structural, and powertrain components, generating long-term offtake demand for closed-loop and certified recycled alloys that provide the supply chain traceability and composition verification required for corporate carbon accounting purposes. These corporate demand commitments are functioning as investment anchors for circular aluminum infrastructure development, enabling secondary producers and recycling technology providers to secure offtake agreements with creditworthy counterparties that support the project finance structures required for capital-intensive circular economy investments.

Advances in Scrap Sorting, Alloy Recovery, and Decoating Technologies Enabling High-Purity Secondary Aluminum Production at Commercial Scale

A critical enabling driver that is directly expanding the technical and commercial boundaries of the circular aluminum economy is the rapid advancement and commercial deployment of sorting, processing, and refining technologies that are progressively overcoming the alloy contamination, tramp element accumulation, and coating residue challenges that have historically constrained the quality and application range of secondary aluminum produced from post-consumer scrap streams. Next-generation sensor-based sorting systems combining X-ray fluorescence spectrometry, laser-induced breakdown spectroscopy, and machine learning-assisted spectral classification are enabling the identification and separation of aluminum scrap at the alloy family and grade level with speed and accuracy that support commercially viable throughput at industrial processing scale, unlocking the ability to produce high-purity alloy-specific recycled streams from previously undifferentiated mixed scrap inputs. Advanced thermal decoating technologies are enabling the efficient removal of organic coatings, lacquers, and paint layers from aluminum packaging, automotive components, and construction profiles prior to remelting, reducing the carbon and energy cost of secondary production while improving the purity of recovered metal and reducing the formation of aluminum dross. The convergence of these technological advances with improvements in secondary refining and alloying control capabilities is enabling secondary aluminum producers to manufacture products meeting the composition and property specifications of the most demanding wrought alloy applications, substantially expanding the addressable market for recycled aluminum beyond the foundry and casting alloy segments toward higher-value flat-rolled, extrusion, and forging products where secondary material has historically been at a quality disadvantage relative to primary aluminum.

Key Challenges

Scrap Quality Degradation, Alloy Dilution, and the Technical Challenge of Maintaining Secondary Aluminum Purity Across Complex Scrap Streams

The most significant technical challenge confronting the global circular aluminum economy is the progressive complexity and contamination of post-consumer aluminum scrap streams arising from the increasing prevalence of multi-material assemblies, multi-alloy products, and surface treatment systems in modern aluminum applications, which collectively make the recovery of high-purity alloy-specific scrap fractions increasingly difficult and costly within the constraints of commercially viable processing economics. Modern automotive aluminum components are engineered from a variety of alloy grades with distinct compositions optimized for specific structural, thermal, or surface quality requirements, and the commingling of these alloys in end-of-life vehicle shredding operations generates mixed scrap streams whose tramp element content, particularly of copper, zinc, and magnesium, can exceed the composition tolerances of high-specification wrought alloy production. The accumulation of iron, silicon, and other impurities through successive recycling cycles creates a phenomenon of alloy dilution over time that progressively degrades the mechanical properties and application range of recycled aluminum unless dilution is managed through careful scrap blending, primary aluminum addition, or advanced refining operations that add cost and complexity to the secondary production process. Addressing the alloy quality challenge requires both upstream improvements in scrap collection and sorting infrastructure to capture alloy-specific fractions before they are commingled in general scrap flows, and downstream investment in refining and alloying adjustment capabilities that can produce high-specification products from inherently variable secondary inputs, both of which require sustained capital investment and technical capability development that may not be economically justified in all market contexts.

Scrap Supply Volatility, Collection Infrastructure Gaps, and the Challenge of Securing Adequate Secondary Raw Material Volumes for Growing Circular Capacity

A structural supply-side challenge facing the circular aluminum economy is the mismatch between the growing demand for secondary aluminum from end-use industries committed to increasing recycled content and the constrained and geographically uneven availability of high-quality aluminum scrap from post-consumer collection systems, particularly in developing and emerging markets where scrap collection infrastructure is fragmented, informal sector participation is dominant, and the institutional frameworks for organized material recovery and certification are at early stages of development. The temporal lag between the deployment of aluminum in long-lived products including vehicles, buildings, and industrial equipment and the generation of the scrap from these products at end of life creates an inherent supply constraint for post-consumer scrap that limits the pace at which secondary production capacity can expand without drawing on post-industrial and manufacturing process scrap, which is already highly recovered in mature industrial economies and offers limited additional supply growth potential. Scrap price volatility, driven by the interplay of commodity aluminum price cycles, export trade flows, and regional collection economics, creates uncertainty in the raw material cost structures of secondary producers that complicates long-term investment planning and pricing agreements with downstream customers who require supply continuity and cost predictability. Developing the collection, aggregation, sorting, and certification infrastructure required to significantly increase post-consumer scrap recovery rates in growing aluminum markets in Asia, the Middle East, and Africa requires coordinated investment by governments, producers, and brand owners whose individual commercial incentives may not fully capture the systemic economic value of improved scrap recovery at the market level.

Regulatory Fragmentation Across Jurisdictions and the Complexity of Managing Circular Aluminum Compliance Across Global Supply Chains

A significant operational and commercial challenge for participants in the global circular aluminum economy is the lack of harmonized regulatory frameworks governing recycled content certification, scrap trade, secondary production standards, and extended producer responsibility obligations across major aluminum-consuming and producing jurisdictions, which creates compliance complexity, market access uncertainty, and competitive asymmetries that constrain the development of the globally integrated circular material flows necessary for an efficient circular aluminum economy. Extended producer responsibility regulations for aluminum-containing products including vehicles, packaging, and electronic equipment differ substantially in scope, recovery rate targets, financing mechanisms, and compliance verification standards across the European Union, North America, Japan, China, and emerging market jurisdictions, making it difficult for multinational producers and brand owners to develop coherent global circular material strategies that satisfy all applicable regulatory requirements simultaneously. The absence of internationally recognized standards for recycled aluminum content measurement, chain of custody verification, and alloy composition certification creates barriers to cross-border trade in secondary aluminum products and increases the transaction costs associated with establishing verifiable recycled content claims for global supply chains. The evolving and jurisdiction-specific nature of carbon border adjustment mechanisms, green taxonomy definitions, and sustainable finance disclosure requirements is adding a further layer of regulatory complexity for circular aluminum economy participants seeking to access green financing, qualify for sustainability-linked trade instruments, and satisfy the due diligence requirements of institutional investors evaluating circular economy investment opportunities across multiple market environments.

Market Segmentation

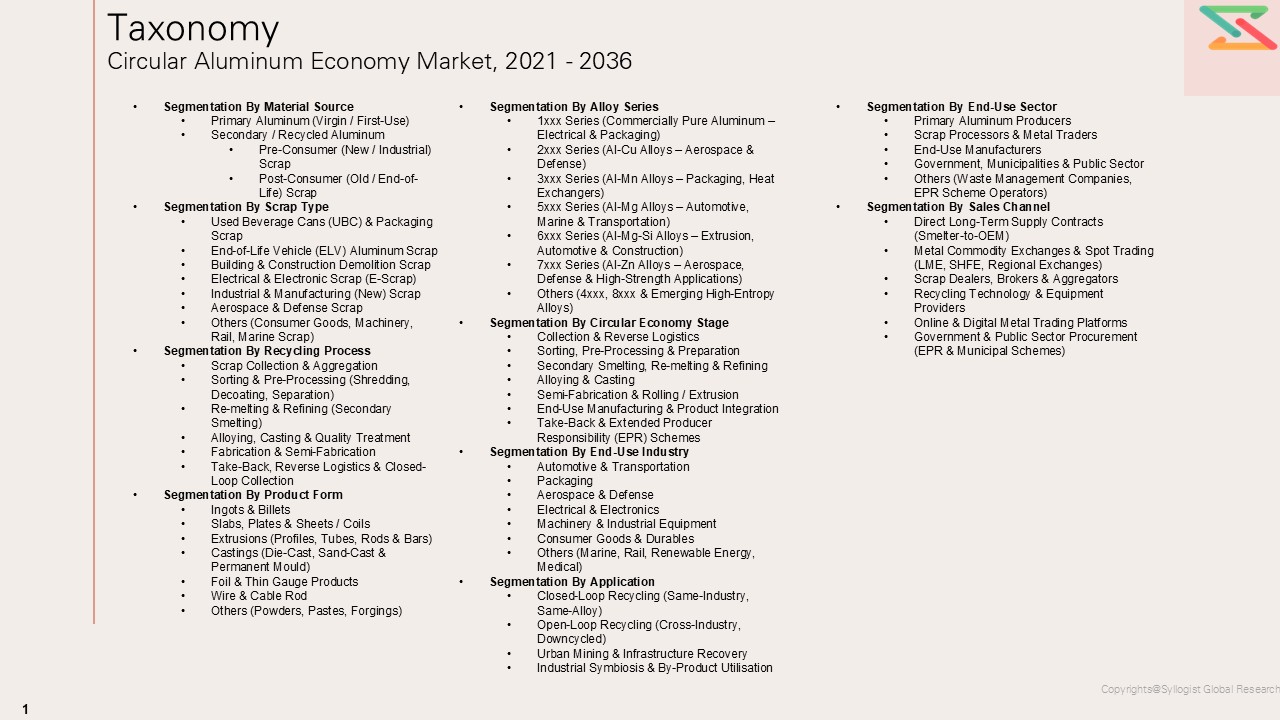

- Segmentation By Scrap Type

- Post-Consumer Scrap

- Post-Industrial and Manufacturing Process Scrap

- Old Scrap from End-of-Life Vehicles

- Building and Construction Demolition Scrap

- Packaging and Beverage Can Scrap

- Consumer Electronics and Electrical Equipment Scrap

- Industrial Machinery and Equipment Scrap

- Aerospace and Defense Component Scrap

- Dross and Salt Cake Secondary Materials

- Others

- Segmentation By Process Technology

- Scrap Collection and Aggregation

- Mechanical Shredding and Separation

- Sensor-Based Scrap Sorting (XRF, LIBS, Optical)

- Thermal Decoating and Organic Removal

- Secondary Smelting and Remelting

- Refining and Alloying Adjustment

- Dross and Salt Cake Reprocessing

- Closed-Loop Alloy-Specific Recovery

- Aluminum Powder and Flake Recovery

- Others

- Segmentation By Alloy Type

- Wrought Aluminum Alloys (1xxx to 7xxx Series)

- Cast and Foundry Aluminum Alloys

- High-Purity Secondary Aluminum

- Aluminum Alloying Additions and Master Alloys

- Others

- Segmentation By Product Form

- Secondary Aluminum Ingot

- Aluminum Billet and Slab

- Aluminum Sheet and Coil

- Aluminum Extrusion Billet

- Aluminum Casting Alloy

- Aluminum Powder and Granules

- Others

- Segmentation By End-Use Industry

- Automotive and Transportation

- Building and Construction

- Packaging and Beverage Can Manufacturing

- Aerospace and Defense

- Consumer Electronics and Electrical Equipment

- Industrial Machinery and Equipment

- Marine and Shipbuilding

- Energy and Power Generation

- Others

- Segmentation By Circular Business Model

- Closed-Loop Recycling and Direct-Return Programs

- Extended Producer Responsibility (EPR) Schemes

- Deposit-Return Systems for Aluminum Packaging

- Take-Back and End-of-Life Vehicle Recycling Programs

- Industrial Symbiosis and By-Product Exchange

- Product-as-a-Service and Aluminum Leasing Models

- Material Certification and Chain-of-Custody Programs

- Others

- Segmentation By Certification and Sustainability Standard

- Recycled Content Certified Aluminum

- Aluminium Stewardship Initiative (ASI) Certified

- Low-Carbon and Green Aluminum Certified

- Environmental Product Declaration (EPD) Compliant

- Carbon Border Adjustment Mechanism (CBAM) Compliant

- Science-Based Targets (SBTi) Aligned Supply Chain

- Others

- Segmentation By Application Technology in Circular Processing

- Artificial Intelligence and Machine Learning in Scrap Sorting

- Digital Twin and Process Simulation for Secondary Smelting

- Blockchain and Distributed Ledger for Scrap Traceability

- Advanced Spectrometry and Inline Composition Analysis

- Robotic Disassembly and Component Recovery

- IoT-Enabled Collection and Logistics Optimization

- Others

- Segmentation By Sales Channel

- Scrap Dealer and Broker Network

- Direct Scrap Purchase from Industrial Generators

- Municipal and Organized Collection Programs

- Online Scrap Trading Platforms

- Long-Term Offtake and Supply Agreements

- Commodity Exchange and Spot Market

- Others

- Segmentation By End User

- Primary Aluminum Producers with Secondary Operations

- Independent Secondary Aluminum Smelters

- Automotive Parts Foundries and Die Casters

- Flat-Rolled Aluminum Producers

- Extrusion and Forging Manufacturers

- Packaging and Can Sheet Manufacturers

- Specialty Alloy Producers

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

All market revenues are presented in USD

Historical Year: 2021–2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027–2036

Key Questions this Study Will Answer

- What is the projected global market valuation and volume for the circular aluminum economy through 2036, segmented by scrap type, process technology, end-use industry, and region, and which material recovery categories, processing technologies, and geographic markets are expected to generate the highest incremental revenue and volume contribution across the forecast period?

- How are carbon pricing mechanisms including the European Union Carbon Border Adjustment Mechanism, national emissions trading systems, and corporate scope three emission reduction commitments expected to reshape the price premium for low-carbon certified secondary aluminum relative to primary aluminum across key end-use sectors, and what thresholds of carbon cost will be required to fully close the production cost gap between secondary and primary routes in the most energy-intensive aluminum applications?

- What are the projected commercial adoption trajectories of advanced scrap sorting technologies including sensor-based alloy identification and robotic disassembly systems, and to what extent will these technologies enable secondary aluminum producers to qualify for wrought alloy flat-rolled and extrusion product markets that have historically been supplied exclusively by primary aluminum, effectively expanding the total addressable market for high-purity secondary material?

- How are closed-loop recycling programs, extended producer responsibility frameworks, and deposit-return systems in major aluminum-consuming industries including automotive, beverage packaging, and construction expected to influence post-consumer scrap collection rates, material quality, and the commercial structure of scrap supply relationships between brand owners, producers, and secondary processors over the forecast horizon?

- Who are the leading secondary aluminum producers, scrap processing technology developers, circular business model innovators, and sustainability certification and traceability platform operators currently defining the competitive landscape of the global circular aluminum economy market, and what are their respective technology investment priorities, strategic partnership structures, geographic expansion plans, and product portfolio positioning strategies through the forecast horizon?

- Product Definition

- Scope of the Study

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Industry Publications, Aluminum Producer Reports, Recycling Industry Association Reports & Press Releases

- Government & Regulatory Authority Data (European Commission, US EPA, IEA, World Bank, UNEP, etc.)

- Aluminum Scrap Production, Trade, Recycling Rate & Secondary Metal Market Statistics

- Aluminum Producer, Scrap Trader & Recycler Supply Chain Databases

- Primary Research Design & Execution

- In-depth Interviews with Secondary Aluminum Smelters, Scrap Processors, OEM Procurement Heads & Sustainability Directors

- Surveys with End-Use Industry Players, Scrap Collectors & Recycling Technology Providers

- Expert Panel Validation

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Bottom-Up & Top-Down Reconciliation

- Scrap Generation, Collection Rate & Secondary Metal Output Model

- End-Use Consumption & Closed-Loop Recycling Rate Forecasting Model

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Technology & Innovation Highlights

- Circular Economy Economics & Unit Economics Summary

- Average Facility CAPEX & OPEX Benchmarks

- Primary vs Secondary Aluminum Cost & Margin Comparison

- Green & Low-Carbon Aluminum Premium & Revenue Model Summary

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Geographic & Regional Trends

- Risk Assessment Framework

- Geopolitical & Trade Policy Risk (Aluminum Tariffs, Export Restrictions, Scrap Trade Policies)

- Aluminum & Scrap Price Volatility (LME Aluminum, Regional Scrap Premiums) Risk

- Environmental & Regulatory Risk

- Financial / Market Risk

- Primary Aluminum Price Competition & Energy Cost Risk

- Scrap Quality Variability, Contamination & Alloy Sorting Risk

- Carbon Border Adjustment Mechanism (CBAM) & Decarbonisation Transition Risk

- Regulatory Framework & Policy Standards

- Global Circular Aluminum Economy Market Economics

- Circular Economy Value Chain Economics Framework

- Capital Expenditure (CAPEX) Structure

- Operating Expenditure (OPEX) Structure

- Revenue Model & Monetisation Levers

- Capacity Utilisation & Throughput Economics

- Payback Period & Return on Investment (ROI) Analysis

- Total Cost of Secondary Aluminum Production vs Primary Aluminum Production

- Raw Material & Scrap Input Cost Analysis

- Aluminum Scrap Price Benchmarks & LME Price Trends (USD/tonne, 2021–2035)

- Pre-Consumer (New) Scrap vs Post-Consumer (Old) Scrap Cost Differentials

- Used Beverage Can (UBC) Scrap Procurement & Premium Analysis

- End-of-Life Vehicle (ELV) Aluminum Scrap Cost Dynamics

- Energy Cost Structure in Secondary Smelting & Re-melting Operations

- Fluxes, Dross Treatment & Alloying Element Input Cost Analysis

- Impact of Scrap Quality, Alloy Sorting & Contamination on Processing Economics

- Scrap Collection, Sorting & Pre-Processing Economics

- Collection Infrastructure & Logistics Cost Structure by Geography

- Sorting Technology (Manual, Eddy Current, XRF, AI-Vision) Cost Comparison

- Decoating & Pre-Treatment Cost Economics

- Scrap Yield & Metal Recovery Rate Economics

- Secondary Smelting & Refining Economics

- Re-melting Furnace Types (Reverberatory, Rotary, Induction) Cost Benchmarks

- Dross Recovery & Salt Slag Processing Economics

- Alloying, Casting & Quality Assurance Economics

- Carbon Cost & Emissions Trading (ETS) Economics in Aluminum Recycling

- Global Circular Aluminum Economy Market Outlook

- Market Size & Forecast by Value (USD Billion, 2021–2036)

- Market Size & Forecast by Volume (Million Tonnes, 2021–2036)

- Market Size & Forecast by Material Source

- Primary Aluminum (Virgin / First-Use)

- Secondary / Recycled Aluminum

- Pre-Consumer (New / Industrial) Scrap

- Post-Consumer (Old / End-of-Life) Scrap

- Market Size & Forecast by Scrap Type

- Used Beverage Cans (UBC) & Packaging Scrap

- End-of-Life Vehicle (ELV) Aluminum Scrap

- Building & Construction Demolition Scrap

- Electrical & Electronic Scrap (E-Scrap)

- Industrial & Manufacturing (New) Scrap

- Aerospace & Defense Scrap

- Others (Consumer Goods, Machinery, Rail, Marine Scrap)

- Market Size & Forecast by Recycling Process

- Scrap Collection & Aggregation

- Sorting & Pre-Processing (Shredding, Decoating, Separation)

- Re-melting & Refining (Secondary Smelting)

- Alloying, Casting & Quality Treatment

- Fabrication & Semi-Fabrication

- Take-Back, Reverse Logistics & Closed-Loop Collection

- Market Size & Forecast by Product Form

- Ingots & Billets

- Slabs, Plates & Sheets / Coils

- Extrusions (Profiles, Tubes, Rods & Bars)

- Castings (Die-Cast, Sand-Cast & Permanent Mould)

- Foil & Thin Gauge Products

- Wire & Cable Rod

- Others (Powders, Pastes, Forgings)

- Market Size & Forecast by Alloy Series

- 1xxx Series (Commercially Pure Aluminum – Electrical & Packaging)

- 2xxx Series (Al-Cu Alloys – Aerospace & Defense)

- 3xxx Series (Al-Mn Alloys – Packaging, Heat Exchangers)

- 5xxx Series (Al-Mg Alloys – Automotive, Marine & Transportation)

- 6xxx Series (Al-Mg-Si Alloys – Extrusion, Automotive & Construction)

- 7xxx Series (Al-Zn Alloys – Aerospace, Defense & High-Strength Applications)

- Others (4xxx, 8xxx & Emerging High-Entropy Alloys)

- Market Size & Forecast by Circular Economy Stage

- Collection & Reverse Logistics

- Sorting, Pre-Processing & Preparation

- Secondary Smelting, Re-melting & Refining

- Alloying & Casting

- Semi-Fabrication & Rolling / Extrusion

- End-Use Manufacturing & Product Integration

- Take-Back & Extended Producer Responsibility (EPR) Schemes

- Market Size & Forecast by End-Use Industry

- Automotive & Transportation

- Body Panels, Chassis & Structural Components

- Powertrain, Engine & Transmission Components

- EV Battery Housings, Enclosures & Thermal Management

- Wheels, Suspension & Braking Systems

- Building & Construction

- Facades, Cladding & Curtain Walls

- Windows, Doors & Architectural Profiles

- Roofing, Structural Framing & Civil Applications

- Packaging

- Beverage Cans & Food Cans

- Flexible Packaging, Foil & Laminates

- Aerosol Cans, Closures & Caps

- Aerospace & Defense

- Electrical & Electronics

- Power Transmission, Grid Infrastructure & Cables

- Consumer Electronics, IT Hardware & Data Centres

- EV Charging Infrastructure & Energy Storage Systems

- Machinery & Industrial Equipment

- Consumer Goods & Durables

- Others (Marine, Rail, Renewable Energy, Medical)

- Automotive & Transportation

- Market Size & Forecast by Application

- Closed-Loop Recycling (Same-Industry, Same-Alloy)

- Open-Loop Recycling (Cross-Industry, Downcycled)

- Urban Mining & Infrastructure Recovery

- Industrial Symbiosis & By-Product Utilisation

- Market Size & Forecast by End-Use Sector

- Primary Aluminum Producers (Integrated Circular Operations)

- Global Integrated Producers (Novelis, Hydro, Norsk Hydro, Hindalco, Constellium, etc.)

- Regional Secondary Smelters & Recyclers

- Scrap Processors & Metal Traders

- Large-Scale Industrial Scrap Processors

- Scrap Brokers, Traders & Commodity Exchanges

- End-Use Manufacturers (OEMs & Fabricators)

- Automotive OEMs & Tier-1 Suppliers

- Packaging Manufacturers & Can Makers

- Construction & Building Products Manufacturers

- Government, Municipalities & Public Sector

- Others (Waste Management Companies, EPR Scheme Operators)

- Primary Aluminum Producers (Integrated Circular Operations)

- Market Size & Forecast by Sales Channel

- Direct Long-Term Supply Contracts (Smelter-to-OEM)

- Metal Commodity Exchanges & Spot Trading (LME, SHFE, Regional Exchanges)

- Scrap Dealers, Brokers & Aggregators

- Recycling Technology & Equipment Providers

- Online & Digital Metal Trading Platforms

- Government & Public Sector Procurement (EPR & Municipal Schemes)

- Asia-Pacific Circular Aluminum Economy Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Volume (Million Tonnes)

- By Material Source

- By Scrap Type

- By Recycling Process

- By Product Form

- By Alloy Series

- By Circular Economy Stage

- By End-Use Industry

- By End-Use Sector

- By Sales Channel

- Key Demand Drivers (APAC-Specific)

- Competitive Landscape (APAC)

- Europe Circular Aluminum Economy Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Volume (Million Tonnes)

- By Material Source

- By Scrap Type

- By Recycling Process

- By Product Form

- By Alloy Series

- By Circular Economy Stage

- By End-Use Industry

- By End-Use Sector

- By Sales Channel

- Key Demand Drivers (Europe-Specific)

- Competitive Landscape (Europe)

- North America Circular Aluminum Economy Market Outlook

- Market Overview & Strategic Importance

- Market Size & Forecast

- By Value (2020–2035)

- By Volume (Million Tonnes)

- By Material Source

- By Scrap Type

- By Recycling Process

- By Product Form

- By Alloy Series

- By Circular Economy Stage

- By End-Use Industry

- By End-Use Sector

- By Sales Channel

- Key Demand Drivers (North America-Specific)

- Competitive Landscape (North America)

- Latin America Circular Aluminum Economy Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Volume (Million Tonnes)

- By Material Source

- By Scrap Type

- By Recycling Process

- By Product Form

- By Alloy Series

- By Circular Economy Stage

- By End-Use Industry

- By End-Use Sector

- By Sales Channel

- Key Demand Drivers (LATAM-Specific)

- Competitive Landscape (Latin America)

- Middle East & Africa Circular Aluminum Economy Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Volume (Million Tonnes)

- By Material Source

- By Scrap Type

- By Recycling Process

- By Product Form

- By Alloy Series

- By Circular Economy Stage

- By End-Use Industry

- By End-Use Sector

- By Sales Channel

- Key Demand Drivers (MEA-Specific)

- Competitive Landscape (MEA)

- Country-Wise Circular Aluminum Economy Market Outlook

- Market Size & Forecast by Country

- By Value

- By Volume (Million Tonnes)

- By Material Source

- By Scrap Type

- By Recycling Process

- By Product Form

- By Alloy Series

- By Circular Economy Stage

- By End-Use Industry

- By End-Use Sector

- By Sales Channel

- Market Size & Forecast by Country

- Market Size & Forecast

- Market Size & Forecast

- Market Size & Forecast

- Market Size & Forecast

- Circular Economy Value Chain Economics Framework

Countries Covered: United States, Canada, Germany, France, United Kingdom, Italy, Spain, Netherlands, Norway, China, Japan, South Korea, India, Australia, Brazil, Mexico, Russia, Turkey, United Arab Emirates, South Africa

- Technology Landscape & Innovation Analysis

- Circular Aluminum Technology Maturity Assessment

- Emerging & Disruptive Technologies in Aluminum Recycling & Circular Economy

- Advanced Sorting Technologies

- Low-Carbon & Green Smelting Technologies

- Closed-Loop Alloy-to-Alloy Recycling & Alloy Segregation Technologies

- Digital Material Passports, Blockchain Traceability & Scrap Certification Platforms

- Solid-State Recycling & Novel Processing Technologies

- Technology Readiness & Commercialisation Matrix – Key Circular Aluminum Technologies

- Patent Landscape Analysis

- R&D Investment Benchmarking

- Value Chain & Supply Chain Analysis

- Circular Aluminum Economy Value Chain Mapping

- Scrap Generation, Collection & Reverse Logistics Network Analysis

- Supply Chain Concentration & Dependency Analysis

- Key Supplier Mapping by Scrap Type, Process & End-Use Industry

- Supplier Risk Heat Map

- Make vs Buy Strategy Trends Among Secondary Smelters & Fabricators

- Pricing Analysis

- Circular Aluminum Pricing Dynamics & Mechanisms

- LME Aluminum Price Trends, Regional Premiums & Scrap Spreads (2021–2035)

- Pricing by Scrap Type, Alloy Series & Product Form

- Total Cost of Ownership (TCO) Analysis – Secondary vs Primary Aluminum Lifecycle Cost & Carbon Cost

- OEM Contract vs Spot Market Pricing Trends & Benchmarks

- Green Aluminum & Certified Recycled Content Price Premium Analysis

- Sustainability & Circular Economy Performance

- Carbon Footprint Benchmarking: Secondary vs Primary Aluminum (Scope 1, 2 & 3 Emissions)

- Aluminum Recycling Rate Analysis by Region, Scrap Type & End-Use Industry

- Green & Low-Carbon Aluminum Certification Frameworks (ASI, LME Green, ResponsibleSteel)

- Extended Producer Responsibility (EPR), Take-Back Schemes & Deposit Return Systems

- Closed-Loop Recycling Programmes & Industry Commitments (Automotive, Packaging, Construction)

- EU Green Deal, Critical Raw Materials Act & Global Circular Economy Policy Impact Assessment

- ESG Reporting, Lifecycle Assessment (LCA) & Science-Based Targets in Aluminum Recycling Operations

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level: Global Integrated Leaders vs Regional Secondary Smelters

- Top 5 Circular Aluminum Economy Players Market Revenue Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis by Product Form & End-Use Industry

- Competitive Intensity Map by Segment & Region

- Player Classification

- Tier-1 Global Integrated Aluminum Producers with Circular Economy Operations

- Tier-2 Regional Secondary Smelters & Specialist Recyclers

- Scrap Processors, Collectors & Metal Trading Companies

- Recycling Technology & Equipment Providers

- Emerging & Disruptive Players

- Competitive Analysis Frameworks

- Market Share Analysis by Product Form, Alloy Series & Geography

- R&D Intensity & Green Aluminum Innovation Benchmarking

- Long-Term Supply Contract & Closed-Loop Partnership Portfolio Comparison

- Geographic Revenue Exposure & Scrap Sourcing Footprint Comparison

- Company Profiles

- Company Overview, HQ & Organisational Structure

- Circular Aluminum Products, Services & Portfolio

- Revenue Breakdown (Primary vs Secondary, By Segment)

- Key OEM Supply Programmes & Closed-Loop Recycling Partnerships

- Manufacturing & Recycling Facility Footprint

- Recent Developments (M&A, Partnerships, New Capacity, Financial Results)

- SWOT Analysis

- Strategic Focus: Closed-Loop Recycling Capacity, Green Aluminum Certification, Downstream Integration

- Strategic Output

- Market Opportunity Matrix

- High-Value Opportunity Quadrant Analysis

- Addressable Market by Segment & Region

- Time-to-Revenue Assessment by Opportunity

- White Space Opportunity Analysis

- Underserved Scrap Type, Alloy Series & End-Use Industry Gaps

- Geographic Markets with Low Recycling Penetration

- Technology Gaps with High Commercialisation Potential

- Customer Segment Unmet Needs

- Strategic Recommendations

- Product Portfolio & Circular Economy Programme Strategy

- Technology & Digitalization Strategy

- Recycling Capacity Expansion & Facility Investment Strategy

- Scrap Sourcing, Collection Network & Reverse Logistics Strategy

- Pricing & Commercial Strategy

- Sustainability, Decarbonisation & Regulatory Compliance Strategy

- Supply Chain & Raw Material Sourcing Strategy

- Partnership, M&A & Expansion Strategy

- Regional Growth Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-Term (2025–2028)

- Mid-Term (2029–2032)

- Long-Term (2033–2036)

- Market Opportunity Matrix

- Market Structure & Concentration