Market Definition

Electrochemical chemical manufacturing encompasses industrial processes that use controlled electrochemical reactions, the directed movement of electrons at electrode-electrolyte interfaces under applied or generated electrical potential, to synthesise, transform, separate, or purify chemical compounds that would otherwise require thermal, catalytic, or biological routes characterised by higher energy consumption, lower selectivity, or greater reliance on hazardous reagents. The market is defined across four principal process categories that together span the majority of global electrochemical production volume: chlor-alkali electrolysis, which is the largest single electrochemical manufacturing process by installed capacity and energy consumption, producing chlorine (Cl₂), caustic soda (NaOH), and hydrogen (H₂) simultaneously from the electrolysis of brine using membrane cell, mercury cell (being phased out globally), or diaphragm cell technology, with global production exceeding 90 million tonnes per year of chlorine and caustic soda combined; electroplating, electrorefining, and electrodeposition processes that deposit metal layers of controlled thickness, grain structure, and purity on substrate surfaces for functional (corrosion protection, electrical conductivity, hardness) or decorative purposes, encompassing copper electrorefining and electrodeposition for semiconductor interconnects and EV busbars, nickel and chromium plating for automotive and aerospace, and precious metal plating for electronics and medical devices; electrochemical synthesis of specialty and fine chemicals, including the electrochemical production of hydrogen peroxide (H₂O₂) via anthraquinone oxidation and direct electrochemical routes, adiponitrile (ADN) via electrochemical hydrodimerisation of acrylonitrile for nylon-66 precursor, sodium chlorate and sodium hypochlorite for pulp bleaching and water treatment, and fluorine and fluorine-based intermediates for specialty materials; and water electrolysis for green hydrogen production, encompassing proton exchange membrane (PEM), alkaline, and solid oxide electrolysis cell (SOEC) technologies. The market also includes electrochemical machining, electrodialysis for water desalination and pharmaceutical separation, electro-oxidation and electro-reduction in pharmaceutical synthesis, and the emerging fields of electrochemical CO₂ reduction (e-CO₂R) for chemical feedstock production and electrochemical nitrogen fixation for green ammonia synthesis. Critical enabling components span the electrolyser stack architecture, electrodes (dimensionally stable anodes, cathodes, gas diffusion layers), membranes and diaphragms (Nafion®, Flemion®, Zirfon®), electrolytes, bipolar plates, and rectifier power supply systems, as well as the process engineering, plant design, and operational optimisation infrastructure required to achieve industrially competitive energy efficiency (expressed as kilowatt-hours per tonne of product) and Faradaic efficiency (the fraction of electrical charge converted to desired product versus side reactions) across large-scale continuous manufacturing operations.

Market Insights

The most consequential structural transformation reshaping the global electrochemical chemical manufacturing market in 2026 is the convergence of three historically separate technology trajectories, industrial chlor-alkali electrolysis, green hydrogen water electrolysis, and electrochemical synthesis of decarbonised chemical feedstocks, into a unified electrochemical manufacturing paradigm driven by the availability of increasingly affordable renewable electricity, the commercial maturation of advanced ion exchange membrane and electrode technologies, and the chemical industry’s obligation under carbon pricing regimes and corporate net-zero commitments to eliminate Scope 1 emissions from thermally intensive chemical production routes. The transformation is most consequential in the chlor-alkali sector, which accounts for approximately 40 TWh of electricity consumption per year globally and which is simultaneously facing two restructuring forces: the transition from mercury-cell and diaphragm-cell technology to membrane-cell electrolysis, which reduces specific energy consumption from 3,200–3,500 kWh per tonne of chlorine to 2,400–2,600 kWh per tonne and eliminates mercury contamination from products; and the emergence of oxygen-depolarised cathode (ODC) technology, which by eliminating hydrogen evolution at the cathode and replacing it with oxygen reduction achieves specific energy consumption of 1,600–1,800 kWh per tonne of chlorine, a 30–40% further reduction that translates directly to USD 50–90 per tonne operating cost advantage and a proportional reduction in carbon footprint when powered by grid or renewable electricity. Thyssen’s ODC demonstration at the Bayer MaterialScience (now Covestro) Uerdingen plant, Evonik’s commercial deployment at Antwerp, and INEOS’s ODC integration programme represent the leading industrial implementations of a technology that has the potential to displace the majority of conventional membrane cell installed base over a 15–20 year replacement cycle, fundamentally reshaping the competitive economics of global chlorine and caustic soda production.

The green hydrogen electrolysis market, which was valued at approximately USD 1.2 billion in 2024 and is projected by multiple scenario analyses including the IEA, BloombergNEF, and Wood Mackenzie to reach USD 65–140 billion by 2035 under accelerated deployment scenarios, represents by far the most rapidly expanding segment of the global electrochemical manufacturing market and the segment attracting the greatest share of venture capital, private equity, and government grant investment. The technology bifurcation between PEM electrolysis, favoured for its high power density, rapid dynamic response to variable renewable electricity input, and ability to produce high-pressure hydrogen directly at the electrolyser outlet, and alkaline electrolysis, favoured for its lower capital cost per MW, longer stack lifetime, tolerance of impure water inputs, and absence of precious metal catalysts, is being supplemented by the accelerating development of anion exchange membrane (AEM) electrolysis, which aims to combine the performance characteristics of PEM with the non-precious-metal catalyst economics of alkaline, and high-temperature solid oxide electrolysis (SOEC), which achieves theoretically superior efficiency by operating at 700–900°C where the thermodynamic demand for electrical energy is partially offset by available heat. The electrolyser capacity manufacturing race has produced announced gigafactory projects from Nel Hydrogen, ITM Power, Cummins, Plug Power, Sunfire, ThyssenKrupp Nucera, and Chinese manufacturers including PERIC and Longi that collectively represent planned annual manufacturing capacity of 35–45 GW by 2027–2028, substantially exceeding any plausible near-term demand scenario and creating the preconditions for the same structural overcapacity, margin compression, and manufacturing consolidation that characterised the solar PV module market between 2010 and 2018.

The primary structural growth driver of the electrochemical chemical manufacturing market is the progressive decarbonisation of the chemical industry value chain, which is the third-largest industrial source of greenhouse gas emissions globally behind steel and cement and which faces a fundamentally different decarbonisation challenge from those sectors: chemical manufacturing emissions are predominantly Scope 1 process emissions from thermally intensive synthesis routes, not fuel combustion emissions, and they can only be addressed by replacing thermal chemistry with electro-chemistry rather than by fuel switching or carbon capture alone. The IEA’s Net Zero by 2050 scenario requires a 90% reduction in chemical sector emissions by 2050, which the IEA itself characterises as achievable only through a combination of electrification of chemical processes (electrochemical synthesis routes replacing Haber-Bosch ammonia, steam cracking, and steam reforming), green hydrogen as a feedstock for ammonia and methanol production, and electro-CO₂R for producing chemical building blocks from captured carbon dioxide. The commercial opportunity this creates across the full electrochemical manufacturing value chain, from electrode and membrane materials suppliers through electrolyser OEMs and system integrators to chemical plant operators and specialty chemical producers adopting electrochemical routes, is being progressively validated by demonstration projects that are crossing the TRL 7–8 threshold at a pace that suggests initial commercial-scale deployments in green ammonia electrosynthesis, electrochemical hydrogen peroxide production, and electrochemical adiponitrile will occur within the 2027–2032 window. The market is further energised by the structural cost advantage that electrochemical routes offer in a world of falling renewable electricity costs: unlike thermal chemical processes whose operating costs are dominated by fossil fuel feedstock prices that are volatile, geopolitically dependent, and subject to carbon pricing, electrochemical processes have operating costs predominantly determined by electricity price, which in regions with abundant solar and wind resources is converging toward USD 15–25 per MWh, creating a fundamentally different and potentially transformative cost structure for electrochemically-produced chemicals versus their thermal equivalents.

Key Drivers

- The foundational and structurally irreversible driver of the electrochemical chemical manufacturing market is the rapid and continuing decline in renewable electricity costs that is making electrochemical synthesis routes, which consume electricity as their primary input rather than fossil fuel feedstocks, increasingly cost-competitive with thermal chemical manufacturing routes that have dominated industrial chemistry for 150 years. Solar photovoltaic levelised cost of electricity (LCOE) has declined from approximately USD 350 per MWh in 2010 to USD 25–40 per MWh in established solar markets by 2025, with power purchase agreement (PPA) prices for large-scale solar projects in Chile, Saudi Arabia, India, and Australia falling below USD 15 per MWh, prices at which green hydrogen electrolysis achieves production costs of USD 1.80–2.80 per kg, within the range at which it begins to be cost-competitive with steam methane reforming (grey hydrogen) at European natural gas prices post-2022. The direct implication for the broader electrochemical manufacturing sector is transformative: every electrochemical synthesis process whose product competitiveness has historically been constrained by electricity cost, including electrolytic hydrogen peroxide, electrochemical adiponitrile, electrochemical fluorine production, electrosynthesis of pharmaceutical intermediates, and electrochemical reduction of CO₂ to formic acid, ethylene, or methanol, becomes progressively more economically viable as electricity costs fall toward USD 15–25 per MWh at the plant gate. The compounding effect is that falling renewable electricity costs simultaneously improve the economics of green hydrogen production (which is the feedstock for green ammonia, green methanol, and direct reduced iron), electrochemical chlorine production (reducing the dominant operating cost of chlor-alkali plants), and electrochemical specialty chemical synthesis (where electricity represents 30–60% of cash operating cost), creating a broad-based cost deflation across the entire electrochemical manufacturing universe that is structurally analogous to, and likely to be at least as commercially disruptive as, the cost deflation of battery cells that transformed the electric vehicle industry between 2015 and 2025.

- The second transformative driver is the convergence of escalating carbon pricing, chemical industry net-zero commitments, and the downstream customer pull from decarbonisation-motivated procurement decisions that is creating non-discretionary demand for electrochemically manufactured chemicals even at current prices that remain above thermal route equivalents. The EU Emissions Trading System (ETS) carbon price, which has traded in the EUR 60–90 per tonne CO₂ range since 2022 and which the EU Commission’s stated trajectory projects reaching EUR 150+ per tonne by 2030 under the Fit for 55 framework, directly increases the cash operating cost of thermally intensive chemical processes by EUR 15–30 per tonne of chemical produced in carbon-intensive routes while simultaneously incentivising capital investment in low-carbon electrochemical alternatives through the Innovation Fund, Hydrogen Bank, and Important Projects of Common European Interest (IPCEI) mechanisms. The EU Carbon Border Adjustment Mechanism (CBAM), which from 2026 applies a carbon price to imports of ammonia, fertilisers, iron, steel, aluminium, and electricity that do not carry a carbon price in their country of production, creates a structural cost advantage for electrochemically manufactured chemicals produced in high-carbon-price jurisdictions versus conventional imports, and will progressively expand its product scope to include other carbon-intensive chemicals. At the corporate level, more than 200 major chemical companies including BASF, Dow, Covestro, Solvay, Bayer, Mitsubishi Chemical, Sumitomo Chemical, and LyondellBasell have published Science Based Targets (SBTi) net-zero commitments that require Scope 1 emission reductions only achievable through electrochemical process substitution, creating a binding demand signal for electrochemical manufacturing investment that is independent of near-term carbon price levels.

- The third critical driver is the direct and rapidly expanding demand for electrochemical manufacturing capacity created by the global energy transition and clean technology deployment programmes that are generating demand for electrochemically produced chemicals, metals, and materials that cannot be met through conventional chemical synthesis routes. Green hydrogen, which can only be produced at scale through water electrolysis, is required as a feedstock for green ammonia synthesis (the Haber-Bosch process requires pure hydrogen as a reactant), green methanol production (the dominant low-carbon maritime fuel candidate and a potential chemical feedstock), and direct use in hydrogen fuel cell vehicles and industrial heating applications, creating an electrolyser market that Wood Mackenzie projects to reach USD 100–150 billion in annual revenue by 2035 under base case deployment scenarios. Battery-grade copper for EV busbars, power electronics, and charging infrastructure requires electrochemical refining and electrodeposition to achieve the 99.99%+ purity and controlled microstructure specifications demanded by semiconductor-grade applications. Semiconductor manufacturing, which underpins the entire digital and clean energy infrastructure of the transition, depends critically on electrochemical copper deposition (damascene copper electroplating for chip interconnects), electrochemical polishing (for wafer planarisation), and ultrapure chemical supply (including electrochemically produced ultrapure hydrogen peroxide and hydrofluoric acid). The expansion of lithium-ion battery gigafactories globally, with announced capacity of 6,000+ GWh by 2030, creates demand for electrochemically deposited lithium metal for battery anodes, electrochemical formation processes for cell activation, and specialty electrolyte additives produced by electrochemical synthesis. Collectively, these clean technology demand vectors create a forward order book for electrochemical manufacturing capacity that has no precedent in the sector’s post-war history and that is driving the largest single cycle of electrolyser manufacturing investment, electrode material development, and membrane technology commercialisation since the chlor-alkali industry’s post-war buildout.

Key Challenges

- The most structurally significant technical and economic challenge confronting the global electrochemical chemical manufacturing market is the persistent gap between laboratory-scale Faradaic efficiency, current density, and lifetime performance metrics for advanced electrochemical synthesis processes and the energy efficiency, selectivity, and electrode durability that must be demonstrated at commercially relevant current densities and operating hours to justify the capital investment required for industrial-scale deployment. This performance gap is most acute in the commercially most strategically valuable emerging electrochemical processes: electrochemical CO₂ reduction (e-CO₂R) to ethylene, formic acid, or methanol operates at Faradaic efficiencies of 60–80% for ethylene and 85–90% for formate at laboratory scale, but at the current densities of 200–500 mA/cm² required for commercial energy efficiency, catalyst degradation through active site poisoning, electrolyte flooding of gas diffusion layers, and carbonate formation in alkaline environments reduces sustained Faradaic efficiency to 40–60% and electrode lifetime to hundreds of hours rather than the thousands of hours required for economically viable operation. Electrochemical nitrogen reduction for ammonia synthesis faces even more fundamental kinetic barriers: the N≡N triple bond dissociation energy of 945 kJ/mol makes selective electrocatalytic cleavage at ambient temperature and pressure, without the competing hydrogen evolution reaction (HER) dominating the electrode current, an unsolved fundamental catalysis challenge that has produced laboratory demonstrations of ammonia Faradaic efficiency above 90% but exclusively at current densities below 1 mA/cm², seven orders of magnitude below commercial viability. Even in the more mature PEM water electrolysis market, the iridium catalyst loading required for anode stability under the acidic, oxidising conditions of oxygen evolution at high current density represents a fundamental materials constraint: current best-in-class PEM electrolysers use 0.3–0.8 mg/cm² of iridium at the anode, and at the GW-scale electrolyser deployment required to meet IEA net-zero hydrogen targets, cumulative iridium demand would exceed 200–400% of current annual global iridium production, creating an existential supply constraint that makes iridium loading reduction to below 0.05 mg/cm² or viable iridium-free catalyst alternatives a prerequisite for the technology’s long-term commercial scalability.

- A compounding structural challenge is the capital intensity, long project development timelines, and complex process integration requirements that characterise industrial-scale electrochemical plant construction, creating financing barriers that are slowing the pace of commercial deployment for new electrochemical manufacturing routes even when the underlying chemistry is sufficiently mature. A world-scale chlor-alkali plant with an annual capacity of 500,000 tonnes of chlorine equivalent requires a capital investment of USD 800 million–1.2 billion; a 100 MW PEM electrolyser facility producing approximately 1,600 tonnes per year of green hydrogen requires USD 120–200 million at current equipment costs; and an industrial-scale electrochemical adiponitrile plant producing 50,000 tonnes per year requires USD 300–500 million in electrolyser, power supply, and downstream purification infrastructure. At these investment scales, the financing of electrochemical plants requires the same project finance, revenue certainty, and risk allocation frameworks that characterise large infrastructure investments, long-term offtake agreements that provide revenue visibility over the 15–25 year project life, government grant or loan guarantee backstops to de-risk first-of-a-kind commercial deployments, and technology risk insurance or performance guarantees from electrolyser OEMs that have historically not been available for novel electrochemical processes. The combination of these financing requirements with the empirical observation that first-of-a-kind electrochemical plants almost universally underperform their design performance and cost projections during the 12–24 month ramp-up period creates a risk perception among industrial project finance banks that is systematically more conservative than the technology’s commercial potential warrants, and that can only be progressively resolved through the accumulation of a track record of commercial-scale operating performance from the pioneering projects that are currently under construction or in early operation across the US, EU, and Asia Pacific.

Market Segmentation

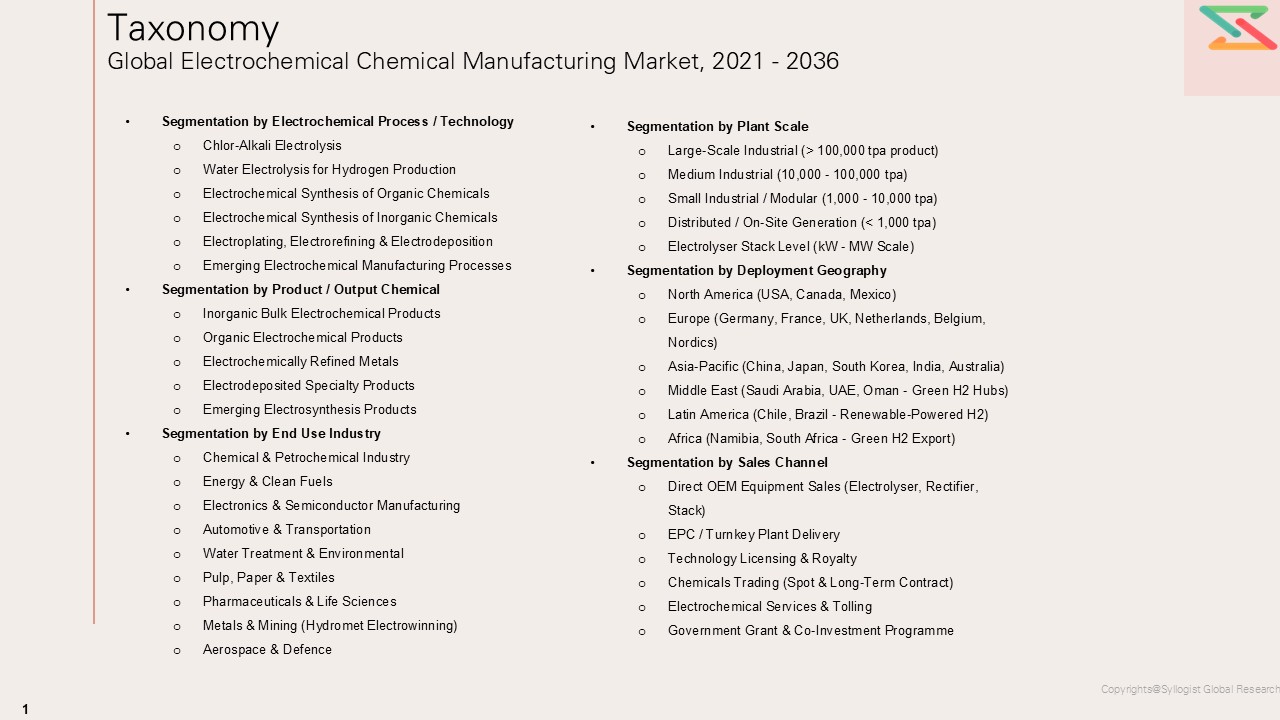

- Segmentation by Electrochemical Process / Technology

- Chlor-Alkali Electrolysis

- Membrane Cell Technology

- Diaphragm Cell Technology (Legacy)

- Mercury Cell Technology (Phase-Out)

- Oxygen-Depolarised Cathode (ODC) Technology

- Water Electrolysis for Hydrogen Production

- Proton Exchange Membrane (PEM) Electrolysis

- Alkaline Electrolysis (AWE)

- Anion Exchange Membrane (AEM) Electrolysis

- Solid Oxide Electrolysis Cell (SOEC)

- High-Pressure Electrolysis (> 30 bar)

- Electrochemical Synthesis of Organic Chemicals

- Electrochemical Adiponitrile (ADN) Synthesis

- Electrochemical Hydrogen Peroxide Production

- Electrochemical Fluorination

- Paired Electrosynthesis Processes

- Pharmaceutical Electrochemical Synthesis

- Electrochemical Synthesis of Inorganic Chemicals

- Sodium Chlorate & Sodium Hypochlorite

- Potassium Hydroxide & Potassium Permanganate

- Sodium Persulfate & Ammonium Persulfate

- Electrochemical Fluorine Production

- Electroplating, Electrorefining & Electrodeposition

- Copper Electrorefining & Electrodeposition

- Nickel Electroplating & Electroforming

- Chromium & Trivalent Chrome Plating

- Precious Metal Plating (Au, Ag, Pt, Pd, Rh)

- Tin & Tin Alloy Electroplating

- Zinc & Zinc Alloy Electroplating

- Semiconductor Copper Damascene (IC Manufacturing)

- Emerging Electrochemical Manufacturing Processes

- Electrochemical CO2 Reduction (e-CO2R)

- Electrochemical Nitrogen Fixation (Green Ammonia)

- Electrochemical Biomass Conversion

- Electrodialysis & Electromembrane Separation

- Electrochemical Machining & Polishing

- Segmentation by Product / Output Chemical

- Inorganic Bulk Electrochemical Products

- Chlorine (Cl2)

- Caustic Soda (NaOH)

- Green Hydrogen (H2 via Electrolysis)

- Hydrogen Peroxide (H2O2)

- Sodium Chlorate (NaClO3)

- Sodium Hypochlorite (NaOCl)

- Fluorine (F2) & HF Derivatives

- Organic Electrochemical Products

- Adiponitrile (ADN)

- Succinic Acid (Electrochemical Route)

- Glyoxylic Acid

- Gluconolactone & Gluconic Acid

- 4-Methoxybenzyl Alcohol

- Pharmaceutical Intermediates (Electrochemical)

- Electrochemically Refined Metals

- Electrolytic Copper Cathode (99.99% Cu)

- Electrolytic Nickel

- Electrolytic Cobalt

- Electrolytic Manganese

- Electrolytic Zinc

- Electrolytic Aluminium (Hall-Heroult)

- Electrodeposited Specialty Products

- Electrodeposited Copper Foil (EV & PCB)

- Electroformed Components (Aerospace, Medical)

- Electrolytic MnO2 (Battery Cathode Material)

- Electrolytic Manganese Sulphate (Battery Grade)

- Emerging Electrosynthesis Products

- Formic Acid (from e-CO2R)

- Ethylene (from e-CO2R)

- Green Methanol (via e-H2 + CO2)

- Green Ammonia (via e-N2 Fixation or e-H2)

- Segmentation by End Use Industry

- Chemical & Petrochemical Industry

- Chlorine Derivatives (PVC, MDI, TDI, Epichlorohydrin)

- Caustic Soda Derivatives (Alumina, Pulp & Paper, Textiles)

- Hydrogen as Chemical Feedstock (Ammonia, Methanol, HCl)

- Specialty Chemical Synthesis (ADN, H2O2, Fluorochemicals)

- Energy & Clean Fuels

- Green Hydrogen for Fuel Cell Vehicles (FCEV)

- Green Ammonia as Marine Fuel & Power Generation

- Green Methanol as Maritime Fuel

- Grid Energy Storage (via Electrochemical Flow Batteries)

- Electronics & Semiconductor Manufacturing

- Copper Damascene Electroplating for IC Interconnects

- PCB Copper Electroplating

- Ultrapure H2O2 for Semiconductor Cleaning

- Electrochemical Polishing & Etching

- Automotive & Transportation

- EV Battery Copper Foil & Busbars

- Zinc, Nickel & Chrome Plating for Automotive Components

- Fuel Cell Stack Platinum Group Metal Catalysts

- Water Treatment & Environmental

- Sodium Hypochlorite for Disinfection

- Electrochlorination for Municipal Water Treatment

- Electro-Oxidation for Industrial Wastewater

- PFAS Destruction via Electrochemical Oxidation

- Pulp, Paper & Textiles

- Pharmaceuticals & Life Sciences

- Metals & Mining (Hydromet Electrowinning)

- Aerospace & Defence

- Chemical & Petrochemical Industry

- Segmentation by Plant Scale

- Large-Scale Industrial (> 100,000 tpa product)

- Medium Industrial (10,000 – 100,000 tpa)

- Small Industrial / Modular (1,000 – 10,000 tpa)

- Distributed / On-Site Generation (< 1,000 tpa)

- Electrolyser Stack Level (kW – MW Scale)

- Segmentation by Deployment Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, France, UK, Netherlands, Belgium, Nordics)

- Asia-Pacific (China, Japan, South Korea, India, Australia)

- Middle East (Saudi Arabia, UAE, Oman – Green H2 Hubs)

- Latin America (Chile, Brazil – Renewable-Powered H2)

- Africa (Namibia, South Africa – Green H2 Export)

- Segmentation by Sales Channel

- Direct OEM Equipment Sales (Electrolyser, Rectifier, Stack)

- EPC / Turnkey Plant Delivery

- Technology Licensing & Royalty

- Chemicals Trading (Spot & Long-Term Contract)

- Electrochemical Services & Tolling

- Government Grant & Co-Investment Programme

- Inorganic Bulk Electrochemical Products

- Chlor-Alkali Electrolysis

All market revenues are presented in USD; volumes in metric tonnes per year of product output or GW of installed electrolyser capacity as applicable

Historical Year: 2021–2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027–2036

Key Questions this Study Will Answer

- What are the critical market metrics and forward-looking projections for the Global Electrochemical Chemical Manufacturing Market, including total market revenue (USD), installed electrolyser capacity (GW), product volume by chemical category (metric tonnes per year), and energy consumption benchmarking (kWh per tonne of product), segmented across Electrochemical Process / Technology (Chlor-Alkali with sub-technologies, Water Electrolysis with PEM/AWE/AEM/SOEC, Organic Electrochemical Synthesis, Inorganic Electrochemical Synthesis, Electroplating/Electrorefining, Electrodeposition, Emerging e-CO₂R/e-N₂), Product / Output Chemical (Cl₂, NaOH, Green H₂, H₂O₂, ADN, sodium chlorate, fluorochemicals, electrolytic metals, electrodeposited copper foil, formic acid, green methanol, green ammonia), End Use Industry, Plant Scale, Deployment Geography, and Sales Channel?

- How are the EU ETS carbon price trajectory, EU Carbon Border Adjustment Mechanism (CBAM) product scope expansion, IRA clean hydrogen production tax credit (Section 45V providing up to USD 3/kg), IRA advanced manufacturing credits (Section 45X for electrolyser components), EU Hydrogen Bank auction results and electrolyser subsidy design, Japan Green Innovation Fund, and national industrial decarbonisation grant programmes collectively restructuring the cost competitiveness, investment geography, and technology selection dynamics across PEM versus alkaline versus AEM versus SOEC electrolysis, oxygen-depolarised cathode chlor-alkali, electrochemical organic synthesis, and e-CO₂R, and what is the breakeven renewable electricity price threshold at which each electrochemical manufacturing route achieves cost parity with its incumbent thermal chemical equivalent at current capital costs and at projected 2030 learning-curve capital costs?

- In what ways are electrode and membrane performance constraints, specifically iridium catalyst loading requirements and degradation mechanisms in PEM electrolysis, oxygen-depolarised cathode lifetime and selectivity in chlor-alkali, Nafion® membrane durability and cost in PEM systems, Faradaic efficiency decay at commercially relevant current densities in e-CO₂R and electrochemical nitrogen reduction, and gas diffusion layer flooding and carbonate precipitation in alkaline e-CO₂R, determining the commercial deployment timeline, achievable plant economics, competitive positioning of PEM versus alkaline versus AEM technologies, and the R&D investment priorities that would most effectively compress the gap between current laboratory performance and the energy efficiency, current density, and electrode lifetime benchmarks required for competitive industrial-scale electrochemical manufacturing?

- Who are the leading global electrolyser OEMs, chlor-alkali plant technology licensors, electrode and membrane materials suppliers, electrochemical synthesis technology developers, electroplating equipment manufacturers, and specialty electrochemical chemical producers, and how do they benchmark across key competitive dimensions including installed electrolyser capacity (GW shipped and operational), specific energy consumption (kWh/kg H₂ or kWh/tonne Cl₂), stack lifetime at rated current density (hours to end of life), catalyst loading (mg/cm² iridium and platinum), Faradaic efficiency at target current density, capital cost per MW or per tonne of annual capacity (USD/kW or USD/tonne/year), technology licensing revenue and installed plant base, government grant and co-investment portfolio, and pipeline of contracted versus announced projects across PEM, alkaline, chlor-alkali, and electrochemical synthesis categories?

- What strategic insights emerge from primary discussions with electrolyser OEM engineering and commercial leadership, chlor-alkali plant operators and technology licensors, industrial gas company hydrogen infrastructure developers, chemical company CDOs and process technology heads responsible for electrification roadmaps, specialty electrochemical chemical producers adopting emerging synthesis routes, semiconductor and PCB electroplating facility managers, investment banks and infrastructure funds evaluating electrochemical project finance, and government programme directors for electrolyser manufacturing grants and green hydrogen hub development, regarding the actual versus projected levelised cost of green hydrogen from PEM and alkaline systems at operating plants versus design specification, the credible commercial deployment timeline for AEM electrolysis and SOEC, the competitive threat from Chinese alkaline electrolyser manufacturers (PERIC, NEL Hyderogen China, REDT) to Western PEM manufacturers in price-sensitive markets, the readiness of electrochemical CO₂ reduction for industrial pilot-scale deployment, the gap between carbon credit economics and actual plant investment decisions, and the critical technology, workforce, and infrastructure investment priorities that would most accelerate the displacement of thermal chemical manufacturing by electrochemical routes across the chlorine, ammonia, hydrogen peroxide, and specialty chemical sectors?

- Market Overview

- Product Overview

- Research Methodology

- Executive Summary

- Market Dynamics

- Market Dynamics (Drivers, Restraints, Opportunities, Challenges, Porter’s Five Forces Analysis, PESTLE Analysis)

- Market Trends & Developments

- Risk Assessment Framework

- Electricity Price & Renewable Energy Supply Risk

- Technology Performance & Scale-Up Risk

- Regulatory, Carbon Pricing & Policy Risk

- Capital Intensity, Financing & Project Execution Risk

- Regulatory Framework & Standards

- Global Regulatory Overview

- Key Regulations, Industrial Policy & Carbon Pricing Frameworks

- Chemical Industry Regulatory Standards

- Mercury Phase-Out & Chlor-Alkali Standards

- Electroplating & Surface Treatment Standards

- Sustainability & ESG Standards

- Regulatory Impact on Market

- Global Electrochemical Chemical Manufacturing Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Installed Electrolyser Capacity (GW)

- Market Size & Forecast by Energy Consumption (TWh/year)

- Market Size & Forecast by Electrochemical Process / Technology

- Chlor-Alkali Electrolysis

- Membrane Cell Technology

- Diaphragm Cell Technology (Legacy Asset Base)

- Mercury Cell Technology (Phase-Out)

- Oxygen-Depolarised Cathode (ODC) Technology

- Chlor-Alkali with Renewable Power Integration

- Water Electrolysis for Hydrogen Production

- Proton Exchange Membrane (PEM) Electrolysis

- Alkaline Water Electrolysis (AWE)

- Anion Exchange Membrane (AEM) Electrolysis

- Solid Oxide Electrolysis Cell (SOEC)

- High-Pressure Electrolysis (> 30 bar)

- Offshore & Marine Electrolysis Systems

- Electrochemical Synthesis of Organic Chemicals

- Electrochemical Adiponitrile (ADN) Synthesis

- Electrochemical Hydrogen Peroxide (H2O2) Production

- Electrochemical Fluorination (ECF)

- Paired Electrosynthesis Processes

- Electrochemical Pharmaceutical Synthesis

- Electrochemical Biomass Valorisation

- Electrochemical Synthesis of Inorganic Chemicals

- Sodium Chlorate (NaClO3) Electrolysis

- Sodium Hypochlorite (NaOCl) Generation

- Potassium Hydroxide (KOH) Production

- Sodium Persulfate & Ammonium Persulfate

- Electrochemical Fluorine (F2) Production

- Potassium Permanganate (KMnO4) Synthesis

- Electroplating, Electrorefining & Electrodeposition

- Copper Electrorefining

- Copper Electrodeposition

- Copper Electrodeposition

- Nickel Electroplating & Electroforming

- Hexavalent & Trivalent Chromium Electroplating

- Precious Metal Electroplating (Au, Ag, Pt, Pd, Rh)

- Tin & Tin Alloy Electroplating

- Zinc & Zinc Alloy Electroplating

- Electrodeposited Copper Foil for EV Batteries & PCBs

- Electrolytic MnO2 (EMD) for Battery Cathodes

- Emerging & Advanced Electrochemical Processes

- Electrochemical CO2 Reduction (e-CO2R)

- Electrochemical Nitrogen Fixation (Green Ammonia via e-N2)

- Electrodialysis for Desalination & Chemical Separation

- Electrochemical Machining (ECM) & Electrochemical Polishing (ECP)

- Electrochemical Wastewater Treatment & PFAS Destruction

- Bioelectrochemical Systems (Microbial Electrosynthesis)

- Chlor-Alkali Electrolysis

- Market Size & Forecast by Product / Output Chemical

- Inorganic Bulk Electrochemical Products

- Chlorine (Cl2)

- Caustic Soda (NaOH)

- Green Hydrogen (H2 via Electrolysis)

- Hydrogen Peroxide (H2O2)

- Sodium Chlorate (NaClO3)

- Sodium Hypochlorite (NaOCl)

- Fluorine (F2) & Fluorinated Intermediates

- Sodium Persulfate & Ammonium Persulfate

- Organic Electrochemical Products

- Adiponitrile (ADN)

- Succinic Acid (Electrochemical Route)

- Glyoxylic Acid

- Gluconolactone & Gluconic Acid

- Pharmaceutical API Intermediates (Electrochemical)

- Electrochemically Refined Metals

- Electrolytic Copper Cathode (99.99% Cu, LME Grade A)

- Electrolytic Nickel (Class I, 99.8%+)

- Electrolytic Cobalt

- Electrolytic Manganese Metal (EMM)

- Electrolytic Zinc (SHG Grade)

- Electrolytic Aluminium (Hall-Héroult Process)

- Electrodeposited Specialty Products

- Electrodeposited Copper Foil (6–18 μm)

- Electroformed Precision Components (Aerospace, Medical)

- Electrolytic MnO2 (EMD)

- Electrolytic Manganese Sulphate (EMS)

- Emerging Electrosynthesis Products

- Formic Acid (from e-CO2R)

- Ethylene

- Carbon Monoxide (from e-CO2R for Syngas)

- Green Methanol (via e-H2 + CO2)

- Green Ammonia (via e-H2 or Direct e-N2 Fixation)

- Inorganic Bulk Electrochemical Products

- Market Size & Forecast by End Use Industry

- Chemical & Petrochemical Industry

- PVC Production (Chlorine Value Chain)

- MDI & TDI for Polyurethane (Chlorine Value Chain)

- Epichlorohydrin & Epoxy Resins

- Caustic Soda for Alumina Refining

- H2 Feedstock for Ammonia & Methanol

- H2O2 for Chemical Synthesis & Bleaching

- Specialty Chemicals (ADN, Fluorochemicals, Persulfates)

- Energy & Clean Fuels

- Green Hydrogen for FCEV & Industrial Heat

- Green Ammonia as Maritime Fuel & Power Generation

- Green Methanol as Maritime Fuel (IMO 2050)

- Grid Energy Storage — Flow Batteries

- Power-to-X — Electrochemical Syngas & Fischer-Tropsch

- Electronics & Semiconductor Manufacturing

- Copper Damascene Electroplating for Advanced IC Nodes

- PCB Copper Electroplating

- Ultrapure H2O2 for Semiconductor Wafer Cleaning

- Electrochemical CMP & Polishing

- Precious Metal Plating for IC Bonding Pads

- Electric Vehicle & Battery Manufacturing

- Electrodeposited Copper Foil for Li-Ion Battery Anodes

- Electrolytic Manganese Sulphate for LMFP Cathode

- Electrochemical Formation Cycling for Cell Activation

- EV Busbar & Component Surface Treatment

- Water Treatment & Environmental Remediation

- Sodium Hypochlorite for Municipal & Industrial Disinfection

- Electro-Oxidation for Industrial Wastewater COD Removal

- Electrochemical PFAS Destruction

- Electrodialysis for Brackish Water Desalination

- Electrolytic Heavy Metal Removal from Effluent

- Pulp, Paper & Textiles

- Sodium Chlorate for Chlorine Dioxide Bleaching

- Caustic Soda for Kraft Pulping & Textile Processing

- H2O2 for Totally Chlorine-Free (TCF) Bleaching

- Pharmaceuticals & Life Sciences

- Metals & Mining

- Aerospace, Defence & Precision Engineering

- Food & Beverage

- Chemical & Petrochemical Industry

- Market Size & Forecast by Plant Scale

- Large-Scale Industrial (> 100,000 tpa product)

- Medium Industrial (10,000–100,000 tpa)

- Small Industrial / Modular (1,000–10,000 tpa)

- Distributed / On-Site Generation (< 1,000 tpa)

- Electrolyser Stack Level (kW–MW Scale)

- Market Size & Forecast by Sales Channel

- Direct OEM Equipment Sales (Electrolyser, Stack, Rectifier)

- EPC / Turnkey Plant Delivery

- Technology Licensing & Royalty (Membrane, Process IP)

- Chemicals Trading (Spot & Long-Term Contract)

- Electrochemical Tolling & Contract Manufacturing

- Government Grant & Co-Investment Programme

- Market Size & Forecast by Region

- North America

- Europe

- Asia-Pacific

- Middle East & Africa

- Latin America

- Asia-Pacific Electrochemical Chemical Manufacturing Market Outlook

- Market Size & Forecast

- By Value

- By Electrochemical Process / Technology

- By Product / Output Chemical

- By End Use Industry

- By Plant Scale

- By Sales Channel

- Market Size & Forecast

- Europe Electrochemical Chemical Manufacturing Market Outlook

- Market Size & Forecast

- By Value

- By Electrochemical Process / Technology

- By Product / Output Chemical

- By End Use Industry

- By Plant Scale

- By Sales Channel

- Market Size & Forecast

- North America Electrochemical Chemical Manufacturing Market Outlook

- Market Size & Forecast

- By Value

- By Electrochemical Process / Technology

- By Product / Output Chemical

- By End Use Industry

- By Plant Scale

- By Sales Channel

- Market Size & Forecast

- Latin America Electrochemical Chemical Manufacturing Market Outlook

- Market Size & Forecast

- By Value

- By Electrochemical Process / Technology

- By Product / Output Chemical

- By End Use Industry

- By Plant Scale

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Electrochemical Chemical Manufacturing Market Outlook

- Market Size & Forecast

- By Value

- By Electrochemical Process / Technology

- By Product / Output Chemical

- By End Use Industry

- By Plant Scale

- By Sales Channel

- Market Size & Forecast

- Country Wise* Electrochemical Chemical Manufacturing Market Outlook

- Market Size & Forecast

- By Value

- By Electrochemical Process / Technology

- By Product / Output Chemical

- By End Use Industry

- By Plant Scale

- By Sales Channel

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: Germany, United States, China, Japan, France, Belgium, Netherlands, South Korea, United Kingdom, Saudi Arabia, UAE, India, Australia, Brazil, Canada, Norway, Sweden, Denmark, Spain, Italy, Russia, Indonesia, Chile, South Africa, Oman, Namibia, Austria, Switzerland, Finland, Poland

- Technology Analysis

- Electrochemical Technology Readiness Level (TRL) Assessment

- Chlor-Alkali Technology Deep-Dive

- Water Electrolysis Technology Deep-Dives

- Electrochemical Organic Synthesis Technology

- Electrochemical CO2 Reduction (e-CO2R) Technology

- Electroplating & Surface Treatment Technology

- Electrode & Membrane Materials Technology

- Advanced Manufacturing & Scale-Up Technology

- Emerging Technologies & Innovation Pipeline

- Value Chain & Supply Chain Analysis

- Electrode & Catalyst Materials

- Membrane & Diaphragm Materials

- Bipolar Plates & Stack Hardware (Ti, Stainless Steel, Graphite)

- Gas Diffusion Layers & Porous Transport Layers

- Power Electronics

- Electrolyser / Electrochemical Reactor OEMs & Stack Assembly

- Balance of Plant (BOP)

- System Integration & EPC Contractors

- Chemical Plant Operations

- Downstream Chemical Processors & End-Use Customers

- Ecosystem Map

- Supply Chain Analysis

- Iridium & Platinum Supply Concentration

- Nafion Membrane

- Titanium for Bipolar Plates

- Electricity Grid Connection

- Skilled Workforce

- Renewable Electricity Availability

- Trade Flow Analysis

- Chlorine & Caustic Soda Regional Production vs Demand Imbalances

- Green Hydrogen Export Trade Flows

- Electrolyser Equipment Export

- Membrane & Electrode Material Trade Flows

- Pricing Analysis

- Electricity Price Sensitivity: Operating Cost Modelling by Process

- Capital Cost Benchmarking by Technology & Scale

- Operating Cost Benchmarking by Process

- Specific Energy Consumption (kWh/tonne or kWh/kg) by Technology

- Electrode & Membrane Replacement Cycle Cost Contribution

- Levelised Cost of Chemical Production

- Levelised Cost of Green Hydrogen (LCOH): USD/kg by Region & Technology

- Levelised Cost of Electrochemical Chlorine vs Thermal Chlorine

- Levelised Cost of Green Ammonia: Electrolyser + Haber-Bosch Route

- Levelised Cost of Electrochemical Formic Acid vs Conventional

- Pricing Tier Analysis

- Commodity Electrochemical Products (Cl2, NaOH, H2)

- Intermediate Electrochemical Products (H2O2, NaClO3, ADN)

- Specialty & High-Purity Electrochemical Products

- Electrodeposited Precision Products & Semiconductor Chemicals

- Carbon Price & Policy Incentive Impact on Effective Cost

- IRA 45V Credit Impact on Green Hydrogen Effective Cost (USD/kg)

- EU ETS Carbon Cost Impact on Thermal vs Electrochemical Route

- EU Hydrogen Bank Subsidy Impact on PEM Project IRR

- Sustainability, Green Chemistry & ESG Analysis

- Carbon Footprint by Process Route: Scope 1, 2 & 3 (tCO2e/tonne Product)

- Green Hydrogen Lifecycle Emissions: Well-to-Gate by Electricity Source

- Chlor-Alkali Decarbonisation Pathway: ODC + Renewable Power

- Electrochemical vs Thermal Chemical Route LCA Comparison

- Green H2 vs Grey H2 vs Blue H2 Well-to-Gate Emissions

- Electrochemical ADN vs Thermal ADN (Sohio Acrylonitrile Process)

- Electrochemical H2O2 vs Anthraquinone Process Emissions

- Water Consumption & Effluent Management

- Demineralised Water Consumption per kg H2 Produced

- Brine Effluent Management in Chlor-Alkali

- Electroplating Rinsewater Treatment & Metal Recovery

- Hazardous Chemical Substitution: Green Chemistry Advantage

- Trivalent Chrome vs Hexavalent Chrome (REACH SVHC Elimination)

- In-Situ H2O2 Generation vs Concentrated H2O2 Transport & Storage

- On-Site Sodium Hypochlorite Generation vs Chlorine Gas Cylinders

- ESG & Sustainability Reporting for Electrochemical Manufacturers

- EU Taxonomy Alignment: Electrolysis as Climate-Enabling Activity

- GRI 305: Emissions Disclosure for Electrochemical Plants

- SBTi Net-Zero for Chemical Company Value Chains

- TCFD Physical & Transition Risk for Electricity-Intensive Assets

- Circular Economy: Electrode & Membrane End-of-Life

- Iridium & Platinum Recycling from Spent PEM Electrolyser MEAs

- DSA Coating Reactivation & Substrate Reuse in Chlor-Alkali

- Nafion Membrane Recycling: PFAS Handling & Disposal

- Go-to-Market & Distribution

- Sales Channel Overview

- Direct OEM Equipment Sales to Industrial Customers

- EPC & Turnkey Plant Delivery (Electrolyser + BOP + Civil)

- Technology Licensing: Membrane, Process IP & Know-How

- Chemicals Product Trading: Spot, Contract & Exchange

- Electrochemical Tolling & Contract Manufacturing Services

- Government Grant, Loan & Co-Investment Frameworks

- Customer Acquisition Strategies by Segment

- Green Hydrogen: Offtake Agreement Structures & Pricing Mechanisms

- Chlor-Alkali: Long-Term Chlorine & Caustic Supply Contracts

- Electroplating: OEM Automotive, Electronics & Aerospace Qualification

- Specialty Chemicals: Pharma & Fine Chemical B2B Sales

- Partnership & Ecosystem Strategies

- Electrolyser OEM: Renewable Energy Developer JVs

- Chemical Company: Electrolyser Manufacturer Co-Development

- EPC Contractor: Technology Licensor Integration Partnerships

- Project Development & Financing Cycle

- Feasibility Study: Technology Selection, Site & Offtake

- Front-End Engineering Design (FEED): Cost & Schedule Basis

- Project Finance: Debt, Equity & Government Grant Structure

- EPC Contract: Lump-Sum vs Cost-Reimbursable

- Commissioning, Ramp-Up & Performance Testing

- Sales Channel Overview

- Competitive Landscape

- Market Structure & Concentration

- Chlor-Alkali Market Concentration

- Water Electrolysis

- Electroplating Equipment Market Fragmentation

- Competitive Intensity Map: Process Technology vs Geography

- Player Classification

- Chlor-Alkali Technology Licensors & Equipment Suppliers

- Water Electrolysis OEMs: PEM Leaders

- Water Electrolysis OEMs: Alkaline & SOEC

- Chinese Electrolyser Manufacturers

- Membrane & Electrode Materials Suppliers

- Electrochemical Synthesis & Specialty Chemical Producers

- Electroplating Equipment & Process Chemical Suppliers

- Emerging & New Entrant Players

- Competitive Analysis Frameworks

- Market Share Analysis by Process Technology & Revenue

- Company Profile (Top 20 Compaies)

- Company Overview & Headquarters

- Electrochemical Technology Portfolio: Process & Product Focus

- Installed Capacity (GW Electrolyser or Tonne/Year Chemical)

- Specific Energy Consumption (kWh/kg or kWh/tonne) vs Benchmark

- Electrode & Membrane Technology IP

- Revenue & Electrochemical Manufacturing Segment Revenue

- Geographic Manufacturing & Customer Presence

- Government Contract, Grant & Co-Investment Portfolio

- Key Customer & Offtake Agreement Portfolio

- Recent Developments (Gigafactory, Investment, Partnership, Test Results)

- SWOT Analysis

- Technology Roadmap

- Competitive Positioning Map (Energy Efficiency vs Scale vs Capital Cost)

- Patent Landscape

- Market Structure & Concentration

- Investment & Project Finance Landscape

- Project Pipeline: Announced, FID, Under Construction (2025–2030)

- Strategic Recommendations

- For Electrolyser OEMs & Stack Manufacturers

- For Electrode & Membrane Materials Suppliers

- For Chlor-Alkali Producers & Chemical Manufacturers

- For Green Hydrogen & Power-to-X Project Developers

- For Chemical & Industrial Companies Adopting Electrochemical Routes

- For Investors & Private Equity

- For Governments & Regulators

- White Space & Opportunity Analysis

- Strategic Priority Matrix & Roadmap

- Near-term (2025–2028)

- Mid-term (2029–2032)

- Long-term (2033–2036)