Market Definition

The Global Floating Carbon Capture Systems Market encompasses the engineering, design, fabrication, deployment, operation, and lifecycle management of marine-based platforms and integrated process systems specifically configured to capture carbon dioxide from point-source industrial emitters located on or adjacent to water bodies, from the open atmosphere through direct air capture processes adapted for offshore or marine deployment, and from dissolved and biogenic carbon stocks in the ocean itself, utilizing buoyant hull structures, ship-hulls, semi-submersible platforms, barge-mounted systems, or purpose-engineered floating process vessels as the physical installation substrate for carbon capture process equipment that would conventionally be installed on fixed onshore or fixed offshore foundations. The product and system scope of this market includes ship-mounted post-combustion carbon capture systems integrated into the exhaust treatment trains of large ocean-going vessels including bulk carriers, container ships, crude oil tankers, and liquefied natural gas carriers, capturing carbon dioxide from engine and boiler flue gases and either storing the compressed liquefied carbon dioxide in onboard tanks for periodic offloading to shore-based sequestration or utilization infrastructure or transferring it to dedicated carbon dioxide transport vessels through ship-to-ship transfer operations at sea, floating direct air capture platforms deploying solid sorbent or liquid solvent contactor arrays on marine structures moored in coastal or open ocean locations where prevailing wind conditions and access to low-carbon energy sources support cost-effective atmospheric carbon dioxide extraction, ocean-based enhanced alkalinity and electrochemical ocean capture systems mounted on floating platforms that modify local seawater chemistry to increase oceanic carbon dioxide uptake and facilitate the storage of additional carbon dioxide as bicarbonate ions within the ocean’s dissolved inorganic carbon pool, floating biomass carbon capture and storage platforms that pyrolyze or hydrothermally liquify marine or terrestrially sourced biomass at sea and sink the resulting carbon-rich biochar or bio-oil into deep ocean sediments or inject captured carbon dioxide into sub-seabed geological formations accessed through subsea wellheads connected to floating injection platforms, floating carbon capture systems integrated into offshore oil and gas production facilities on floating production storage and offloading vessels, tension leg platforms, and semi-submersibles to capture carbon dioxide from combustion turbine exhaust gases and reinject the captured carbon dioxide into producing or depleted offshore reservoirs for enhanced oil recovery or permanent geological storage, and the carbon dioxide compression, dehydration, conditioning, temporary storage, liquefaction, and offloading system modules that constitute the downstream carbon handling infrastructure within floating carbon capture process trains. The technology landscape within this market spans amine-based chemical absorption processes utilizing monoethanolamine, piperazine, and proprietary advanced solvent formulations as the primary post-combustion capture chemistry for ship and offshore platform applications, temperature and pressure swing adsorption processes using structured solid sorbent contactors for direct air capture and flue gas treatment in compact modular configurations suited to space-constrained floating platform installations, membrane separation systems employing polymeric and inorganic composite membranes for carbon dioxide selective permeation from mixed gas streams in configurations compatible with marine motion environments, calcium and magnesium carbonate looping and enhanced weathering processes adapted for ocean alkalinity enhancement on floating platforms, electrochemical carbon dioxide capture and release cells enabling electrically driven capture cycles without thermal regeneration energy requirements, and the process intensification engineering innovations including rotating packed bed contactors, printed circuit heat exchangers, and modular skid-mounted process equipment packages that reduce the weight, footprint, and motion sensitivity of carbon capture process systems to levels compatible with marine floating platform operation. The value chain of this market extends from specialty amine solvent and solid sorbent material producers, membrane fabricators, heat exchanger and rotating equipment manufacturers, and marine-grade structural steel and composite material suppliers through floating platform designers and naval architects, carbon capture process equipment original equipment manufacturers, offshore and marine engineering procurement and construction contractors, vessel conversion and retrofitting shipyards, carbon dioxide transport and logistics operators, offshore geological storage assessment and well engineering service providers, and the shipping companies, offshore energy operators, independent carbon removal project developers, voluntary carbon market buyers, and regulatory compliance-driven industrial emitters whose capital investment decisions and carbon credit procurement commitments define the commercial demand structure and growth pace of this nascent but strategically important market globally.

Market Insights

The global floating carbon capture systems market is at an early but rapidly accelerating stage of commercial development in 2026, characterized by the transition of multiple distinct technology application categories from pilot demonstration and front-end engineering study activity toward the first commercial-scale project commitments, driven by the convergence of strengthening maritime decarbonization regulations creating compliance demand for shipboard carbon capture, the maturation of offshore carbon dioxide storage project pipelines that are creating the geological sequestration infrastructure prerequisite for large-scale floating capture deployment, the progressive inclusion of ocean-based carbon dioxide removal methodologies within voluntary carbon market crediting frameworks, and the growing appetite of major industrial emitters, sovereign wealth funds, and climate-focused investment vehicles for verified, large-scale, and permanent carbon removal solutions that only geological and deep ocean storage pathways can credibly provide at the scale required by net-zero transition commitments. The global floating carbon capture systems market was valued at approximately USD 1.3 billion in 2025 and is projected to expand at a compound annual growth rate of 43 percent through 2036, reaching approximately USD 46 billion by the end of the forecast period, a trajectory reflecting the intersection of mandatory compliance-driven shipboard adoption across the global commercial shipping fleet, the commercial scaling of offshore geological carbon dioxide storage infrastructure that expands the accessible sequestration capacity available to floating capture systems, and the progressive cost reduction of direct air capture and ocean carbon dioxide removal process technologies through manufacturing scale-up, material science improvements, and process intensification that are making the economics of floating carbon removal increasingly competitive with alternative carbon dioxide removal pathways. The competitive landscape encompasses dedicated maritime carbon capture technology developers offering proprietary shipboard capture system packages to shipping companies, offshore engineering and construction contractors with the project execution capability to deliver floating direct air capture and offshore capture and storage projects at commercial scale, major industrial gases companies whose carbon dioxide liquefaction, handling, and logistics competencies position them as essential supply chain participants in floating capture project value chains, emerging ocean carbon dioxide removal startups developing electrochemical and enhanced alkalinity capture technologies for marine platform deployment, and the integrated energy majors whose offshore engineering capability, balance sheet strength, and access to offshore geological storage assets position them as anchor investors and project developers in the largest floating capture and storage project concepts currently advancing through feasibility and front-end engineering study phases.

A defining technology and commercial development reshaping the trajectory of the floating carbon capture market is the accelerating regulatory and commercial pressure on the global shipping industry to reduce its greenhouse gas emissions intensity, with the International Maritime Organization’s 2023 revised greenhouse gas strategy setting binding carbon intensity reduction trajectories for the international shipping fleet that are progressively tightening through 2030 and 2040 toward net-zero shipping emissions by or around 2050, creating a structural compliance demand for carbon abatement technologies including onboard carbon capture systems that complement but cannot be fully replaced by alternative fuel switching strategies given the fleet composition, operational profile, and fuel availability constraints of the existing and near-term newbuild commercial shipping fleet. The shipboard carbon capture market segment is advancing rapidly along its technology development and commercial qualification pathway, with multiple pilot installations on operating commercial vessels having accumulated sufficient operational hours of flue gas treatment, carbon dioxide absorption, and compressed liquid carbon dioxide storage performance data to support the engineering basis for commercial system design at the scale required for bulk carriers, container ships, and crude oil tankers operating on long-distance international trade routes. The primary technical and operational challenges of shipboard carbon capture, including the management of high-sulfur and particulate-contaminated flue gas streams that require upstream pretreatment before contact with amine solvent capture media, the onboard storage volume and weight constraints that limit liquid carbon dioxide storage capacity relative to the full capture potential of large marine engine exhaust streams, the logistics of periodic liquid carbon dioxide offloading at port facilities equipped for receiving and further processing captured carbon dioxide, and the energy penalty of thermal solvent regeneration that reduces fuel efficiency and partially offsets the greenhouse gas benefit of captured carbon dioxide, are being addressed through systematic engineering development programs that are producing increasingly compact, energy-efficient, and operationally robust capture system designs whose performance on the commercial operational pilots is providing the technical evidence base for fleet-wide deployment commitments by major shipping operators.

The floating direct air capture and ocean carbon dioxide removal segment of the market, while at an earlier stage of commercial development than shipboard carbon capture, is attracting substantial and growing investment from technology developers, climate-focused private equity funds, voluntary carbon market buyers, and government research programs motivated by the unique combination of location flexibility, access to low-cost marine renewable energy sources, and potential for very large-scale deployment in open ocean environments unencumbered by the land use competition and visual amenity conflicts that constrain onshore direct air capture facility siting. Floating direct air capture platforms, which deploy solid sorbent or liquid solvent contactor arrays on moored or dynamically positioned marine structures powered by co-located offshore wind, wave, or tidal energy generation or by submarine power cable connections to onshore renewable electricity grids, are being developed in multiple geographic contexts including the North Sea, the North Atlantic, coastal California, and the Western Pacific, where combinations of high atmospheric carbon dioxide mixing ratios, accessible offshore renewable energy resources, and proximity to sub-seabed geological storage formations or deep ocean basins suitable for biochar and alkalinity-enhanced seawater storage are creating favorable site conditions for early commercial demonstration. Ocean alkalinity enhancement platforms, which deploy electrochemical or mineral dissolution systems to increase the buffering capacity of surface seawater and accelerate its natural carbon dioxide uptake from the atmosphere, represent a technically distinct but commercially complementary floating carbon dioxide removal approach whose measurement, reporting, and verification methodology development is advancing through large-scale ocean trials and atmospheric-ocean carbon exchange modeling programs that are establishing the scientific foundation for carbon credit issuance under emerging ocean carbon dioxide removal crediting standards. The integration of floating carbon capture and storage systems into offshore oil and gas production facilities on existing floating production infrastructure represents an additional commercially significant application pathway where the co-location of capture equipment with both a concentrated carbon dioxide emission source and access to offshore geological storage through existing subsea injection well infrastructure is creating a potentially favorable project economics structure relative to greenfield floating capture deployments.

From a regional perspective, Europe represents the most commercially advanced market for floating carbon capture system development and deployment, combining the world’s most developed offshore carbon dioxide transport and storage infrastructure pipeline concentrated in the North Sea basin, including the Northern Lights project providing the first commercial offshore carbon dioxide storage service accessible to third-party emitters, with the most ambitious maritime decarbonization regulatory framework in the European Union Emissions Trading System’s progressive inclusion of shipping sector emissions and the FuelEU Maritime regulation, and with the deepest concentration of offshore engineering competency, project development expertise, and specialized marine installation capability required to execute complex floating capture and storage projects at commercial scale. Norway and the United Kingdom are the most active national markets for offshore carbon dioxide storage development that underpins the sequestration infrastructure required for large-scale floating capture system commercial viability, with multiple licensed offshore storage sites advancing through characterization and permitting processes in both the Norwegian Continental Shelf and the United Kingdom Continental Shelf that will collectively provide the geological storage capacity foundation for a substantial floating capture industry in the North Sea region over the forecast period. Asia-Pacific, led by Japan, South Korea, Singapore, and Australia, represents a large and rapidly developing market for floating carbon capture technology driven by the significant maritime industry concentration in these economies, the active government investment programs in carbon capture, utilization, and storage infrastructure in Japan and Australia, the leading role of Japanese and South Korean shipbuilders and shipping companies in shipboard carbon capture technology development and pilot deployment programs, and the advanced offshore carbon dioxide storage licensing and development activity in Australian continental shelf basins. North America, and specifically the Gulf of Mexico and the Pacific Coast, represents a growing market for floating carbon capture investment driven by the Inflation Reduction Act’s enhanced 45Q tax credit for carbon capture and geological storage that is improving the economics of offshore capture and injection projects, the large pipeline of offshore carbon dioxide storage permitting activity in Gulf of Mexico deepwater and shelf zones, and the active shipboard carbon capture pilot programs being advanced by major bulk commodity shipping operators serving North American export trade routes.

Key Drivers

Binding International Maritime Organization Greenhouse Gas Regulations and Shipping Sector Emissions Trading Obligations Creating Mandatory Compliance Demand for Onboard Carbon Capture Technology

The most immediate and commercially consequential demand driver for floating carbon capture systems in the shipboard application segment is the implementation of binding international and regional regulatory frameworks governing the greenhouse gas emissions of the global commercial shipping fleet, which together are creating a mandatory compliance market for carbon abatement technologies including onboard carbon capture systems whose adoption pace will be determined by the stringency and enforcement credibility of the applicable regulations and the relative cost competitiveness of shipboard capture against alternative compliance pathways including alternative fuel adoption, operational efficiency improvement, and carbon credit procurement. The International Maritime Organization’s Carbon Intensity Indicator framework, which assigns ratings to individual ships based on their annual carbon intensity calculated from fuel consumption and transport work data and restricts the operational flexibility of ships rated below defined threshold levels, is creating an immediate and graduated financial incentive for shipping operators to invest in carbon intensity reduction technologies including onboard carbon capture systems whose capture efficiency improvements can directly improve Carbon Intensity Indicator ratings and restore the operational flexibility of affected vessels. The European Union’s inclusion of international shipping within the European Emissions Trading System from 2024, which requires shipping companies to surrender emissions allowances for carbon dioxide emitted from voyages within, entering, and departing from European ports, is creating a direct carbon price exposure for major shipping operators on European trade routes that is substantially improving the financial case for onboard carbon capture system investment relative to the uncapped allowance purchase cost of continuing to emit without abatement. The progressive tightening of the International Maritime Organization’s carbon intensity trajectory requirements through 2030 and the anticipated adoption of a global maritime carbon levy mechanism under the International Maritime Organization’s revised greenhouse gas strategy are providing the long-term regulatory signal that shipping companies and their financial backers require to justify the capital commitment for fleet-wide onboard carbon capture system installation programs, with the regulatory stringency trajectory ensuring that the financial case for shipboard capture investment strengthens progressively over the forecast period rather than being subject to regulatory reversal risk. The combination of regional emissions trading scheme exposure and global carbon intensity regulation is creating a dual compliance pressure on major shipping operators that is generating active procurement evaluation programs for shipboard carbon capture systems across the bulk carrier, container ship, and tanker segments of the global fleet, with the first commercial purchase orders for fleet-scale onboard carbon capture installations expected to materialize in the near-term forecast period as pilot system operational performance data provides the engineering confidence basis for fleet deployment commitments.

Expanding Offshore Carbon Dioxide Geological Storage Infrastructure and the Commercial Maturation of Carbon Dioxide Transport Logistics Networks Enabling Floating Capture at Scale

The development of commercially accessible offshore geological carbon dioxide storage infrastructure and the parallel maturation of carbon dioxide marine transport logistics networks represent the essential enabling conditions for floating carbon capture systems to scale beyond standalone pilot demonstrations toward the integrated capture, transport, and permanent storage value chain architecture required for commercially credible and climate-relevant deployment at the tens of millions of tonnes of carbon dioxide per year scale that both the shipping decarbonization compliance market and the voluntary carbon removal market are progressively requiring. The Northern Lights carbon dioxide storage project on the Norwegian Continental Shelf, which achieved first commercial carbon dioxide injection in 2024 and is advancing toward its full commercial storage capacity, represents the first operational proof of concept for the third-party accessible offshore geological storage service model that underpins the business case for distributed floating capture systems lacking individual access to dedicated geological storage assets, demonstrating that the regulatory, technical, commercial, and liability frameworks for open-access offshore carbon dioxide storage are practically implementable and investable by carbon dioxide storage project developers and their financing institutions. The large pipeline of offshore carbon dioxide storage projects advancing through geological characterization, regulatory permitting, and front-end engineering study phases across the Norwegian Continental Shelf, the United Kingdom Continental Shelf, the Australian continental shelf, the Gulf of Mexico, and the Sarawak Basin in Southeast Asia is collectively creating the geological storage capacity foundation that will enable a substantially larger fleet of floating carbon capture systems to reach final investment decision within the forecast period, as the availability of credible and commercially accessible storage capacity is a necessary condition for floating capture project financing and customer offtake agreement execution. The development of carbon dioxide marine transport infrastructure, including purpose-built carbon dioxide carrier vessels of progressively larger capacity as ship design experience accumulates, dedicated carbon dioxide loading terminals at major port facilities serving as liquefied carbon dioxide collection hubs for periodic offload from onboard capture system storage tanks, and the regulatory and commercial standardization of carbon dioxide cargo transport contracts and transfer liability frameworks under international maritime conventions, is creating the logistical backbone that enables the decoupling of shipboard carbon capture from ship-specific geological storage access and allows captured carbon dioxide from vessel onboard systems to be aggregated and transported to shared offshore storage infrastructure in a commercially and operationally practical manner. The investable certainty provided by long-term carbon dioxide storage service agreements between floating capture project developers and geological storage operators, backed by the creditworthiness of large energy company storage project sponsors and supported by government co-investment and liability frameworks in Norway, the United Kingdom, and Australia, is providing the revenue visibility that floating capture project developers and their financing institutions require to advance projects from engineering study to construction commitment.

Key Challenges

High Capital and Operating Cost of Floating Carbon Capture Systems and the Substantial Gap Between Current Project Economics and Commercially Self-Sustaining Cost Levels

The most consequential near-term commercial challenge limiting the pace of floating carbon capture system deployment across all application segments is the high capital expenditure intensity and operating cost structure of current floating carbon capture technology configurations, which result in carbon dioxide capture costs that substantially exceed the revenue available from current carbon credit prices, shipping sector carbon allowance prices, and government capture incentive mechanisms in most project contexts, requiring persistent and substantial policy support or voluntary carbon market premium pricing to bridge the economic gap between project costs and commercial revenues across the investment lifecycle of floating capture assets. Shipboard carbon capture system capital costs, including the capture absorber and regenerator columns, solvent circulation and heat exchange systems, carbon dioxide compression and liquefaction modules, onboard liquid carbon dioxide storage tanks, and the associated structural reinforcement and stability modification required for marine installation, currently represent a significant addition to vessel acquisition cost for new build installations and a larger proportional cost for retrofit installations on existing vessels that require more extensive structural modification and space reconfiguration to accommodate capture system modules within existing hull envelopes. The operating cost structure of shipboard carbon capture is further burdened by the energy penalty of thermal amine solvent regeneration, which consumes a fraction of main engine or auxiliary boiler thermal output and reduces the effective fuel efficiency of the vessel, partially offsetting the greenhouse gas benefit of the captured carbon dioxide and adding to the fuel cost per unit of transport work that must be recovered through freight rate adjustments or carbon compliance cost avoidance. Floating direct air capture platform economics face an even more challenging cost structure than shipboard capture, as the very low atmospheric concentration of carbon dioxide relative to industrial flue gas streams requires processing vastly larger volumes of air per tonne of captured carbon dioxide, demanding larger contactor systems, higher sorbent or solvent material inventories, greater energy consumption per tonne of capture, and more complex marine platform structures capable of supporting the large contactor array areas required for commercially meaningful capture rates, all of which combine to produce current capital and operating costs per tonne of carbon dioxide removed that are substantially above the carbon credit prices prevailing in both compliance and voluntary markets. The cost reduction pathway for floating carbon capture requires progress on multiple simultaneous fronts including process intensification through rotating contactor and printed circuit heat exchanger adoption, sorbent and solvent material cost reduction through manufacturing scale-up and material science improvement, offshore engineering cost reduction through standardized modular platform designs enabling series fabrication learning curve benefits, and renewable energy cost reduction for the large power demands of direct air capture thermal and electrochemical regeneration cycles, a multidimensional cost reduction challenge whose achievement requires sustained technology development investment and commercial deployment volume over a multi-year timeline.

Regulatory and Liability Framework Uncertainty for Offshore Carbon Dioxide Storage and Ocean-Based Carbon Dioxide Removal Creating Project Development and Financing Risk

A structurally significant commercial challenge constraining the pace of floating carbon capture project development and final investment decision commitment is the incompleteness and jurisdictional fragmentation of the regulatory and legal liability frameworks governing the offshore geological storage of carbon dioxide captured by floating systems and the ocean-based carbon dioxide removal activities conducted by floating enhanced alkalinity and direct ocean capture platforms, creating legal uncertainty for project developers and their financing institutions regarding the long-term liability for stored carbon dioxide permanence, the regulatory approval pathway and timeline for offshore storage permits, and the legal status of ocean modification activities under international maritime and environmental law. The London Protocol amendments permitting the offshore geological storage of carbon dioxide and the export of carbon dioxide for the purpose of offshore storage, while adopted by the contracting parties, had not been ratified and given force of law by a sufficient number of jurisdictions to provide unambiguous legal certainty for cross-border carbon dioxide transport and injection projects in several commercially important regional contexts as of the study reference period, creating a legal risk that affects the ability of floating capture project developers to structure bankable carbon dioxide supply and disposal agreements across international maritime boundaries with confidence in the enforceability of contractual rights and obligations over the multi-decade project life of offshore storage assets. The regulatory approval framework for offshore carbon dioxide storage permits, which in most jurisdictions requires extensive geological characterization of the proposed storage formation, modeling of carbon dioxide plume migration and containment integrity over century timescales, environmental impact assessment of storage site disturbance and potential leakage pathways, and monitoring plan development for post-injection storage performance verification, involves multi-year permitting timelines and regulatory agency capacity constraints that create a bottleneck between floating capture project development timelines and the availability of approved storage permits necessary to anchor the capture project business case and support financing. Ocean-based carbon dioxide removal activities conducted by floating platforms face additional regulatory uncertainty arising from the incomplete development of permitting frameworks for deliberate ocean modification at commercial scale under the London Protocol and the Convention on Biological Diversity, with the potential for both domestic regulatory requirements and international convention constraints to impose activity restrictions, monitoring obligations, and liability regimes on floating ocean carbon dioxide removal projects that are currently undefined and that represent a material regulatory risk factor for investors evaluating ocean carbon dioxide removal platform investments in advance of regulatory framework clarity.

Market Segmentation

- Segmentation By System Type

- Ship-Mounted Onboard Carbon Capture Systems (OCCS)

- Floating Direct Air Capture (DAC) Platforms

- Floating Offshore Capture and Geological Storage Systems

- Ocean Alkalinity Enhancement Platforms

- Electrochemical Ocean Carbon Dioxide Removal Platforms

- Floating Biomass Carbon Capture and Storage (BiCCS) Systems

- Floating Production Facility-Integrated Carbon Capture Systems

- Others

- Segmentation By Capture Technology

- Amine-Based Chemical Absorption (Post-Combustion)

- Advanced Solvent and Proprietary Blend Absorption

- Solid Sorbent Temperature Swing Adsorption

- Pressure Swing Adsorption

- Membrane Separation Systems

- Calcium and Magnesium Carbonate Looping

- Electrochemical Carbon Dioxide Capture and Release

- Enhanced Ocean Alkalinity and Mineral Dissolution

- Cryogenic Carbon Dioxide Separation

- Others

- Segmentation By Carbon Dioxide Disposition Pathway

- Offshore Geological Storage and Sequestration

- Onboard Liquid Carbon Dioxide Storage and Port Offloading

- Ship-to-Ship Carbon Dioxide Transfer at Sea

- Sub-Seabed Injection via Floating Injection Platform

- Deep Ocean Dissolved Inorganic Carbon Storage

- Carbon Dioxide Utilization (Enhanced Oil Recovery, Mineralization)

- Others

- Segmentation By Vessel and Platform Type

- Bulk Carriers and Dry Cargo Vessels

- Container Ships

- Crude Oil and Product Tankers

- Liquefied Natural Gas (LNG) Carriers

- Floating Production Storage and Offloading (FPSO) Vessels

- Semi-Submersible Offshore Platforms

- Barge-Mounted Floating Process Platforms

- Purpose-Built Floating Direct Air Capture Vessels

- Moored Ocean Carbon Dioxide Removal Arrays

- Others

- Segmentation By Carbon Dioxide Source Type

- Marine Diesel Engine and Boiler Flue Gas

- Offshore Gas Turbine Exhaust

- Atmospheric Carbon Dioxide (Direct Air Capture)

- Dissolved Ocean Carbon Dioxide

- Offshore Associated Gas Combustion Flue Gas

- Others

- Segmentation By Energy Source

- Main Engine Waste Heat Recovery

- Auxiliary Boiler Steam Integration

- Co-Located Offshore Wind Power

- Wave and Tidal Energy Integration

- Submarine Grid-Connected Renewable Electricity

- Onboard Generator Power

- Hybrid Multi-Source Energy Systems

- Others

- Segmentation By Revenue Mechanism

- Voluntary Carbon Market Credit Sales

- Compliance Emissions Trading Scheme Allowance Avoidance

- Carbon Capture Government Incentive (45Q and Equivalent)

- Carbon Intensity Indicator Compliance Premium

- Low-Carbon Commodity Shipping Freight Premium

- Carbon Dioxide Utilization Revenue

- Others

- Segmentation By End User

- International Shipping Companies and Fleet Operators

- Offshore Oil and Gas Exploration and Production Companies

- Independent Carbon Removal Project Developers

- National Energy and Climate Agencies

- Port Authorities and Coastal Industrial Zone Operators

- Voluntary Carbon Market Buyers and Corporates

- Climate-Focused Investment Funds

- Others

- Segmentation By Region

- Europe (North Sea and Norwegian Continental Shelf)

- Asia-Pacific (Japan, South Korea, Singapore, Australia)

- North America (Gulf of Mexico and Pacific Coast)

- Latin America (Brazil Pre-Salt and Offshore)

- Middle East and Africa

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2036

Key Questions this Study Will Answer

- What is the projected global market valuation for floating carbon capture systems through 2036, segmented by system type, capture technology, carbon dioxide disposition pathway, vessel and platform type, revenue mechanism, and region, and which application categories and geographic markets are expected to generate the highest incremental revenue and installed capture capacity growth across the forecast period?

- What is the current technical readiness and commercial deployment pace of shipboard onboard carbon capture systems across the bulk carrier, container ship, crude oil tanker, and liquefied natural gas carrier fleet segments, and how are the operational performance data emerging from commercial pilot installations influencing the engineering specifications, procurement timelines, and fleet-scale deployment commitment decisions of major international shipping operators subject to tightening Carbon Intensity Indicator and European Emissions Trading System compliance obligations?

- How is the expansion of commercially accessible offshore geological carbon dioxide storage infrastructure across the North Sea, Australian Continental Shelf, Gulf of Mexico, and Southeast Asian basins expected to evolve through 2036, and at what storage capacity availability thresholds and carbon dioxide transport logistics maturity levels are floating capture project developers projected to achieve the sequestration access conditions necessary to support bankable final investment decisions for large-scale floating capture and storage projects in each major regional market?

- What are the projected cost reduction trajectories for shipboard carbon capture, floating direct air capture, and ocean-based carbon dioxide removal system configurations through 2036, driven by process intensification, sorbent and solvent material manufacturing scale, marine platform standardization, and offshore renewable energy cost reduction, and at what levelized carbon dioxide capture cost milestones are different floating capture technology categories expected to achieve competitiveness with current voluntary carbon market credit prices and compliance carbon allowance price trajectories in major emissions trading scheme jurisdictions?

- How are the regulatory frameworks governing offshore carbon dioxide geological storage permits under national continental shelf legislation, cross-border carbon dioxide transport authorizations under London Protocol amendments, and ocean modification activity permitting for floating enhanced alkalinity and electrochemical ocean capture platforms expected to develop across European, Asia-Pacific, and North American jurisdictions over the forecast period, and what are the residual regulatory and legal liability uncertainties that are creating the most material financing and project development risk for floating carbon capture investors and project developers in each regional market?

- Who are the leading shipboard carbon capture technology developers, floating direct air capture platform companies, ocean carbon dioxide removal technology innovators, offshore engineering and construction contractors, carbon dioxide marine transport operators, and offshore geological storage project developers currently defining the competitive landscape of the global floating carbon capture systems market, and what are their respective technology platform strategies, pilot project reference portfolios, regulatory approval roadmaps, carbon credit market partnership structures, and capital raising activities for advancing floating carbon capture from early commercial demonstration toward the multi-million tonne annual capture scale required for climate-relevant contribution to global carbon dioxide removal targets through the forecast horizon?

- Product Definition

- Scope of the Study

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Industry Publications, Offshore Technology OEM Reports, Carbon Capture Project Developer Filings & Press Releases

- Government Energy, Climate & Maritime Regulatory Authority Data (IEA, IMO, UNFCCC, EC DG CLIMA, DOE, BEIS, IRENA, etc.)

- Floating Carbon Capture System Project Pipeline, CAPEX Investment & CO₂ Removal Capacity Statistics

- Shipping Operator, Offshore Platform Owner & Carbon Credit Registry Procurement & MRV Databases

- Primary Research Design & Execution

- In-depth Interviews with Floating CCS Technology Developers, Offshore EPC Contractors, Shipping Company Technical Directors & Carbon Market Specialists

- Surveys with Offshore Oil & Gas Operators, Shipping Lines, Port Authorities, Carbon Finance Investors & Government Climate Agencies

- Expert Panel Validation

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Bottom-Up & Top-Down Reconciliation

- Carbon Capture Project Pipeline Advancement, Regulatory Incentive Rollout & Technology Cost Reduction-Driven Market Sizing Model

- CO₂ Removal Capacity Deployment Rate, Carbon Credit Revenue & Technology Learning Curve Adjustment Framework

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Technology & Innovation Highlights

- Project Economics & Unit Economics Summary

- Average System CAPEX & OPEX Benchmarks

- Post-Combustion vs Oxyfuel vs Direct Air Capture (DAC) vs Ocean-Based Removal System Economics Comparison

- Vessel-Mounted, FPSO-Based, Dedicated Floating Platform & Offshore Hub Revenue Model Summary

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Geographic & Regional Trends

- Risk Assessment Framework

- Geopolitical & International Carbon Policy Fragmentation Risk (Paris Agreement, IMO GHG Strategy, EU ETS, Carbon Border Adjustment Mechanism)

- Technology Readiness & First-of-a-Kind (FOAK) Floating CCS System Deployment Risk

- CO₂ Geological Storage Site Availability, Subsea Reservoir Integrity & Long-Term Permanence Risk

- Supply Chain Bottleneck Risk (Offshore-Grade Amine Solvents, Cryogenic CO₂ Equipment, Floating Hull Fabrication)

- Carbon Credit Price Volatility, MRV Integrity & Market Confidence Risk

- Regulatory Permitting, Environmental Impact & Seabed / Marine Area Licensing Risk

- Financial / Project Financing & Long-Term Carbon Offtake Contract Risk

- Regulatory Framework & Policy Standards

- Global Floating Carbon Capture Systems Market Economics

- System Development & Construction Economics Framework

- Capital Expenditure (CAPEX) Structure

- Operating Expenditure (OPEX) Structure

- Revenue Model & Monetisation Levers (Carbon Credit Sales, Carbon Offtake Agreements, CO₂ EOR Revenue, Regulatory Compliance Fee Avoidance, Government Grant & Subsidy Income)

- Capacity Utilisation, CO₂ Capture Rate & Availability Economics

- Payback Period & Return on Investment (ROI) Analysis

- Cost per Tonne of CO₂ Captured vs Land-Based CCS, Direct Air Capture (DAC) & Nature-Based Solutions

- Equipment & Component Input Cost Analysis

- Amine Solvent, Liquid Sorbent & Solid Sorbent Material Cost Trends (USD/tonne, 2021–2035)

- CO₂ Absorber Column, Stripper & Heat Exchanger Fabrication Cost Dynamics

- Cryogenic CO₂ Liquefaction, Compression & Storage Tank Cost Structure

- Floating Hull, Mooring System & Marine Structural Steel Cost Analysis

- Subsea CO₂ Injection Well, Pipeline & Wellhead Equipment Cost Structure

- Power Generation (Offshore Wind, Gas Turbine, Waste Heat Recovery) & Utility System Integration Cost Economics

- Impact of Solvent Regeneration Energy Penalty Reduction & Process Intensification on System Economics

- CO₂ Transport, Injection & Storage Economics

- Offshore CO₂ Pipeline, Flexible Riser & Subsea Injection System Cost Structure

- Ship-Based CO₂ Transport: Liquefied CO₂ Carrier Vessel Economics & Logistics

- Subsea CO₂ Geological Storage Reservoir Assessment, Appraisal Well & Monitoring Cost Economics

- CO₂ Enhanced Oil Recovery (EOR) Revenue Offset & Storage Credit Economics

- Regulatory & Standards Compliance Economics

- Floating CCS System Design, Certification & Offshore Safety Standards Compliance Cost Benchmarks (DNV, Lloyd’s Register, IEC, ISO 27914, OSPAR, London Protocol, etc.)

- CO₂ MRV (Measurement, Reporting & Verification) Framework Compliance & Third-Party Audit Cost Structure

- Marine Environmental Impact Assessment (EIA), Subsea Storage Permitting & Seabed Licence Compliance Costs

- Global Floating Carbon Capture Systems Market Outlook

- Market Size & Forecast by Value (USD Billion, 2021–2036)

- Market Size & Forecast by CO₂ Capture Capacity (Mtpa, 2021–2036)

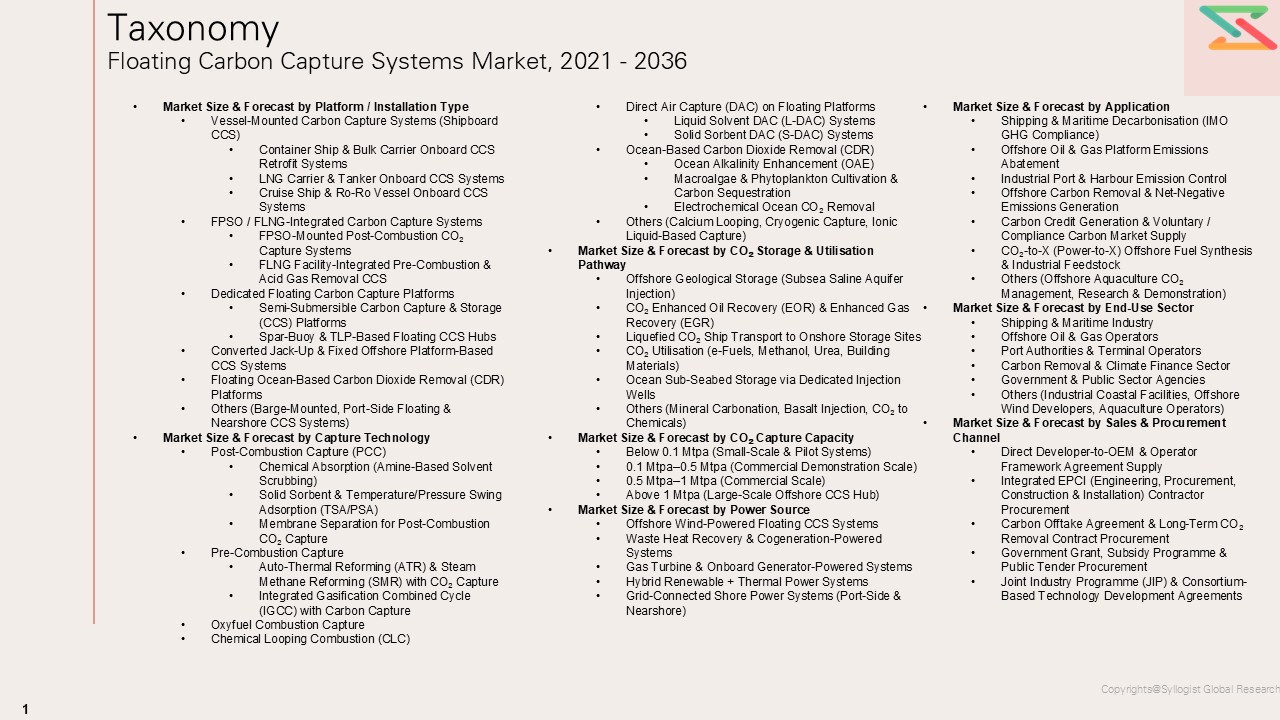

- Market Size & Forecast by Platform / Installation Type

- Vessel-Mounted Carbon Capture Systems (Shipboard CCS)

- Container Ship & Bulk Carrier Onboard CCS Retrofit Systems

- LNG Carrier & Tanker Onboard CCS Systems

- Cruise Ship & Ro-Ro Vessel Onboard CCS Systems

- FPSO / FLNG-Integrated Carbon Capture Systems

- FPSO-Mounted Post-Combustion CO₂ Capture Systems

- FLNG Facility-Integrated Pre-Combustion & Acid Gas Removal CCS

- Dedicated Floating Carbon Capture Platforms

- Semi-Submersible Carbon Capture & Storage (CCS) Platforms

- Spar-Buoy & TLP-Based Floating CCS Hubs

- Converted Jack-Up & Fixed Offshore Platform-Based CCS Systems

- Floating Ocean-Based Carbon Dioxide Removal (CDR) Platforms

- Others (Barge-Mounted, Port-Side Floating & Nearshore CCS Systems)

- Vessel-Mounted Carbon Capture Systems (Shipboard CCS)

- Market Size & Forecast by Capture Technology

- Post-Combustion Capture (PCC)

- Chemical Absorption (Amine-Based Solvent Scrubbing)

- Solid Sorbent & Temperature/Pressure Swing Adsorption (TSA/PSA)

- Membrane Separation for Post-Combustion CO₂ Capture

- Pre-Combustion Capture

- Auto-Thermal Reforming (ATR) & Steam Methane Reforming (SMR) with CO₂ Capture

- Integrated Gasification Combined Cycle (IGCC) with Carbon Capture

- Oxyfuel Combustion Capture

- Chemical Looping Combustion (CLC)

- Direct Air Capture (DAC) on Floating Platforms

- Liquid Solvent DAC (L-DAC) Systems

- Solid Sorbent DAC (S-DAC) Systems

- Ocean-Based Carbon Dioxide Removal (CDR)

- Ocean Alkalinity Enhancement (OAE)

- Macroalgae & Phytoplankton Cultivation & Carbon Sequestration

- Electrochemical Ocean CO₂ Removal

- Others (Calcium Looping, Cryogenic Capture, Ionic Liquid-Based Capture)

- Post-Combustion Capture (PCC)

- Market Size & Forecast by CO₂ Storage & Utilisation Pathway

- Offshore Geological Storage (Subsea Saline Aquifer Injection)

- CO₂ Enhanced Oil Recovery (EOR) & Enhanced Gas Recovery (EGR)

- Liquefied CO₂ Ship Transport to Onshore Storage Sites

- CO₂ Utilisation (e-Fuels, Methanol, Urea, Building Materials)

- Ocean Sub-Seabed Storage via Dedicated Injection Wells

- Others (Mineral Carbonation, Basalt Injection, CO₂ to Chemicals)

- Market Size & Forecast by CO₂ Capture Capacity

- Below 0.1 Mtpa (Small-Scale & Pilot Systems)

- 1 Mtpa–0.5 Mtpa (Commercial Demonstration Scale)

- 5 Mtpa–1 Mtpa (Commercial Scale)

- Above 1 Mtpa (Large-Scale Offshore CCS Hub)

- Market Size & Forecast by Power Source

- Offshore Wind-Powered Floating CCS Systems

- Waste Heat Recovery & Cogeneration-Powered Systems

- Gas Turbine & Onboard Generator-Powered Systems

- Hybrid Renewable + Thermal Power Systems

- Grid-Connected Shore Power Systems (Port-Side & Nearshore)

- Market Size & Forecast by Application

- Shipping & Maritime Decarbonisation (IMO GHG Compliance)

- Offshore Oil & Gas Platform Emissions Abatement

- Industrial Port & Harbour Emission Control

- Offshore Carbon Removal & Net-Negative Emissions Generation

- Carbon Credit Generation & Voluntary / Compliance Carbon Market Supply

- CO₂-to-X (Power-to-X) Offshore Fuel Synthesis & Industrial Feedstock

- Others (Offshore Aquaculture CO₂ Management, Research & Demonstration)

- Market Size & Forecast by End-Use Sector

- Shipping & Maritime Industry

- Global Container Shipping Lines (Maersk, MSC, CMA CGM, Evergreen, Hapag-Lloyd, etc.)

- Bulk Carrier, Tanker & LNG Carrier Operators

- Cruise Lines & Ro-Ro Vessel Operators

- Offshore Oil & Gas Operators

- Global Integrated Oil & Gas Majors (Equinor, Shell, bp, TotalEnergies, ExxonMobil, Chevron, etc.)

- National Oil Companies (NOCs) & State-Owned Offshore E&P Operators

- Independent Offshore E&P & Midstream Operators

- Port Authorities & Terminal Operators

- Major Global Container & Bulk Terminal Operators & Port Authorities

- LNG Bunkering & Marine Fuel Terminal Operators

- Carbon Removal & Climate Finance Sector

- Voluntary Carbon Market Buyers, Carbon Removal Offtake Investors & CDR Platforms

- Compliance Carbon Market Participants & ETS Obligated Entities

- Government & Public Sector Agencies

- National Energy Transition Authorities, Climate Finance Bodies & CCS Infrastructure Programme Administrators

- Defence & Naval Authorities with Maritime Emissions Obligations

- Others (Industrial Coastal Facilities, Offshore Wind Developers, Aquaculture Operators)

- Shipping & Maritime Industry

- Market Size & Forecast by Sales & Procurement Channel

- Direct Developer-to-OEM & Operator Framework Agreement Supply

- Integrated EPCI (Engineering, Procurement, Construction & Installation) Contractor Procurement

- Carbon Offtake Agreement & Long-Term CO₂ Removal Contract Procurement

- Government Grant, Subsidy Programme & Public Tender Procurement

- Joint Industry Programme (JIP) & Consortium-Based Technology Development Agreements

- Asia-Pacific Floating Carbon Capture Systems Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By CO₂ Capture Capacity (Mtpa)

- By Platform / Installation Type

- By Capture Technology

- By CO₂ Storage & Utilisation Pathway

- By CO₂ Capture Capacity

- By Power Source

- By Application

- By End-Use Sector

- By Sales & Procurement Channel

- Key Demand Drivers (APAC-Specific)

- Competitive Landscape (APAC)

- Europe Floating Carbon Capture Systems Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By CO₂ Capture Capacity (Mtpa)

- By Platform / Installation Type

- By Capture Technology

- By CO₂ Storage & Utilisation Pathway

- By CO₂ Capture Capacity

- By Power Source

- By Application

- By End-Use Sector

- By Sales & Procurement Channel

- Key Demand Drivers (Europe-Specific)

- Competitive Landscape (Europe)

- North America Floating Carbon Capture Systems Market Outlook

- Market Overview & Strategic Importance

- Market Size & Forecast

- By Value (2020–2035)

- By CO₂ Capture Capacity (Mtpa)

- By Platform / Installation Type

- By Capture Technology

- By CO₂ Storage & Utilisation Pathway

- By CO₂ Capture Capacity

- By Power Source

- By Application

- By End-Use Sector

- By Sales & Procurement Channel

- Key Demand Drivers (North America-Specific)

- Competitive Landscape (North America)

- Latin America Floating Carbon Capture Systems Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By CO₂ Capture Capacity (Mtpa)

- By Platform / Installation Type

- By Capture Technology

- By CO₂ Storage & Utilisation Pathway

- By CO₂ Capture Capacity

- By Power Source

- By Application

- By End-Use Sector

- By Sales & Procurement Channel

- Key Demand Drivers (LATAM-Specific)

- Competitive Landscape (LATAM)

- Middle East & Africa Floating Carbon Capture Systems Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By CO₂ Capture Capacity (Mtpa)

- By Platform / Installation Type

- By Capture Technology

- By CO₂ Storage & Utilisation Pathway

- By CO₂ Capture Capacity

- By Power Source

- By Application

- By End-Use Sector

- By Sales & Procurement Channel

- Key Demand Drivers (MEA-Specific)

- Competitive Landscape (MEA)

- Country-Wise Floating Carbon Capture Systems Market Outlook

- Market Size & Forecast by Country

- By Value

- By CO₂ Capture Capacity (Mtpa)

- By Platform / Installation Type

- By Capture Technology

- By CO₂ Storage & Utilisation Pathway

- By CO₂ Capture Capacity

- By Power Source

- By Application

- By End-Use Sector

- By Sales & Procurement Channel

- Market Size & Forecast by Country

- Market Size & Forecast

- Market Size & Forecast

- Market Size & Forecast

- Market Size & Forecast

- System Development & Construction Economics Framework

Countries Covered: Norway, United Kingdom, Netherlands, Denmark, France, Germany, United States, Canada, Japan, South Korea, China, Australia, Brazil, Singapore, UAE, Saudi Arabia, Nigeria, India, Indonesia, Iceland

- Technology Landscape & Innovation Analysis

- Floating Carbon Capture System Technology Maturity Assessment

- Emerging & Disruptive Technologies in Floating CCS & Ocean-Based CDR

- Next-Generation Solvent & Sorbent Materials: Low-Regeneration-Energy Amines, Ionic Liquids & Metal-Organic Frameworks (MOFs)

- Modular & Compact Carbon Capture Process Intensification: Rotating Packed Beds, Microreactors & 3D-Printed Absorbers for Marine Applications

- Direct Air Capture (DAC) Integration on Floating Platforms: High-Seas CDR Scalability Roadmap

- Ocean Alkalinity Enhancement (OAE) & Electrochemical CO₂ Removal: Marine Chemistry & Permanence Verification Advances

- Offshore Wind-Powered Floating CCS: Grid-Independent, Renewable-Driven CO₂ Capture Architecture

- Digital Twin, AI-Driven Process Optimisation & Remote Monitoring Platforms for Floating CCS Operations

- Technology Readiness & Commercialisation Matrix – Key Floating Carbon Capture System Technologies

- Patent Landscape Analysis

- R&D Investment Benchmarking

- Value Chain & Supply Chain Analysis

- Floating Carbon Capture Systems Value Chain Mapping

- Supply Chain Concentration & Dependency Analysis

- Key Supplier Mapping by Component & Technology Programme

- Amine Solvent, Chemical Absorbent & Solid Sorbent Material Supplier Mapping

- CO₂ Absorber, Stripper, Heat Exchanger & Process Vessel Fabricator Mapping

- Cryogenic CO₂ Compressor, Liquefaction Unit & Storage Tank Manufacturer Mapping

- Floating Hull, Mooring System & Marine Structure Fabrication Yard Mapping

- Subsea CO₂ Injection Equipment, Pipeline & Wellhead Supplier Mapping

- Supplier Risk Heat Map

- Make vs Buy Strategy Trends Among Floating CCS Technology Developers & Offshore EPCI Contractors

- Pricing Analysis

- Floating Carbon Capture System Pricing Dynamics & Mechanisms

- Pricing by Platform Type, Capture Technology, CO₂ Capacity & Storage Pathway

- Total Cost of CO₂ Capture (TCOC) Analysis – Including System CAPEX, OPEX, Energy Penalty, Storage, Transport & MRV Costs (USD/tCO₂)

- Vessel-Mounted vs FPSO-Integrated vs Dedicated Floating Platform Pricing Trends & Benchmarks

- Hardware Sale vs Integrated EPCI Package vs Carbon Offtake-Backed Service Agreement Pricing & Value Proposition

- Sustainability & Environmental Stewardship

- Environmental & Sustainability Landscape in Floating Carbon Capture System Development & Deployment

- Lifecycle GHG Emissions & Net CO₂ Removal Efficiency Benchmarking Across Platform Types & Capture Technologies

- Marine Ecosystem, Ocean Chemistry & Biodiversity Risk Assessment for Ocean-Based CDR & CO₂ Storage Operations

- Floating CCS’s Contribution to IMO 2050 GHG Targets, Paris Agreement Temperature Goals & Net-Zero Shipping Pathways

- Recyclability of Floating Platform Materials, Solvent Waste Streams & Offshore Equipment: Circular Economy Assessment

- ESG Reporting & Lifecycle Assessment (LCA) in Floating Carbon Capture System Operations

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level: Global Energy Majors & Offshore Technology OEMs vs Climate-Tech Startups & Ocean CDR Specialists

- Top 5 Floating Carbon Capture System Companies Market Revenue & Capacity Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis by Platform Type, Capture Technology & Region

- Competitive Intensity Map by Segment & Region

- Player Classification

- Tier-1 Global Integrated Energy, Offshore Technology & Carbon Capture OEMs with Floating CCS Portfolios (Shell, Equinor, TotalEnergies, Mitsubishi Heavy Industries, Wartsila, Babcock & Wilcox, etc.)

- Tier-2 Specialist Floating CCS Technology Developers, Shipboard Capture System OEMs & Marine Process Engineering Firms

- Emerging Ocean CDR, Direct Air Capture & Carbon Removal Startups (Eidesvik, Carbon Clean, Seabound, Heimdal, Running Tide, Planetary Technologies, etc.)

- Emerging & Disruptive Players

- Competitive Analysis Frameworks

- Market Share Analysis by Platform Type, Capture Technology, Application & Geography

- R&D Intensity & Carbon Capture Technology Platform Breadth Benchmarking

- Carbon Offtake Contract Portfolio, JIP Participation & Long-Term CCS Project Pipeline Comparison

- Geographic Revenue Exposure & Offshore Basin / Maritime Route Deployment Footprint Comparison

- Company Profiles

- Company Overview, HQ & Organisational Structure

- Floating CCS Products, Capture Technology Platform & CO₂ Storage Pathway Portfolio

- Revenue Breakdown

- Key Project References, Carbon Offtake Agreements & Operator Deployment Programmes

- Manufacturing Footprint, Offshore Fabrication Yards & Key Facilities

- Recent Developments (M&A, Partnerships, New Projects, Technology Qualifications, Financial Results)

- SWOT Analysis

- Strategic Focus: Capture Cost Reduction, Technology Qualification Leadership, Carbon Offtake Contract Expansion & Ocean CDR Scale-Up Strategy

- Strategic Output

- Market Opportunity Matrix

- High-Value Opportunity Quadrant Analysis

- Addressable Market by Platform Type, Capture Technology & Region

- Time-to-Revenue Assessment by Opportunity

- White Space Opportunity Analysis

- Underserved Platform Type, Application Segment & End-Use Sector Gaps

- Geographic Maritime Routes & Offshore Basins with Low Floating CCS Penetration & High Regulatory Mandate Growth

- Technology, CO₂ Storage Pathway & Power Source Gaps with High Commercialisation Potential

- Customer Segment Unmet Needs

- Strategic Recommendations

- Product Portfolio & Capture Technology Innovation Strategy

- Technology Qualification, Offshore Certification & Scale-Up Strategy

- Manufacturing Footprint, Fabrication Yard & Capacity Expansion Strategy

- Carbon Offtake Agreement, Operator Partnership & Channel Growth Strategy

- Pricing, Carbon Revenue Optimisation & Commercial Strategy

- Sustainability, Environmental Compliance & Ocean Stewardship Strategy

- Supply Chain, Solvent & Offshore Equipment Sourcing Strategy

- Partnership, M&A & Joint Industry Programme (JIP) Participation Strategy

- Regional Growth & Maritime Route Expansion Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-Term (2025–2028)

- Mid-Term (2029–2032)

- Long-Term (2033–2036)

- Market Opportunity Matrix

- Market Structure & Concentration