Market Definition

A genset, or generator set, is a self-contained power generation system that combines a prime mover (engine) with an alternator (generator) mounted on a common frame, typically integrated with a fuel system, control panel, and automatic transfer switch (ATS). Gensets convert chemical energy from diesel, natural gas, petrol, LPG, or alternative fuels into usable electrical power, functioning as either the primary source of electricity or as a reliable standby system when grid supply fails. The market is broadly segmented by power rating (below 75 kVA to above 5,000 kVA), fuel type (diesel, gas, dual-fuel, hydrogen, and hybrid), engine technology (reciprocating, gas turbine, microturbine, and fuel cell), and end-use application (standby, prime, continuous, CHP, and peak shaving). Diesel reciprocating gensets currently dominate the global installed base due to their fuel availability, robust load-handling capability, and proven reliability across extreme environments; however, the market is undergoing a structural shift driven by decarbonisation mandates, grid instability concerns, and the growing integration of battery energy storage systems (BESS) into hybrid genset configurations.

Market Insights

One of the most consequential structural shifts reshaping the genset industry is the explosive growth in data centre and telecom infrastructure investment, which has elevated uninterruptible backup power from a compliance checkbox to a mission-critical strategic asset. As hyperscale cloud operators, Amazon Web Services, Microsoft Azure, Google Cloud, and Meta, accelerate their global infrastructure rollouts, the specification requirements for gensets have evolved dramatically. No longer simply a diesel engine in a weatherproof enclosure, modern data centre gensets are expected to provide tier-rated load acceptance, sub-10-second transfer capability, ultra-low total harmonic distortion (THD), remote telematics integration, and N+1 or 2N redundancy configurations. In markets where AI workloads are driving power density per rack from 10 kW to over 100 kW, the genset, not the UPS, is increasingly viewed as the ultimate power assurance mechanism. This dynamic is generating premium-priced, multi-unit orders that are structurally different from the high-volume, lower-margin standby market that defined the industry a decade ago.

Geographically, Sub-Saharan Africa, South and Southeast Asia, and parts of the Middle East represent the most volume-intensive genset markets globally, not because of industry sophistication, but because of acute grid unreliability. In Nigeria alone, the industrial and commercial genset fleet is estimated to exceed 60 GW of installed capacity, surpassing the entire national grid. In India, despite improving grid quality, captive power requirements for manufacturing clusters, cold chains, and telecom towers sustain a multi-billion-dollar annual replacement and new-installation market. Conversely, the North American and Western European markets are driven by a different logic: aging grid infrastructure, the increasing frequency of extreme weather events, and regulatory mandates for critical facility resilience are pushing hospitals, utilities, and government institutions toward increasingly sophisticated, fuel-flexible standby solutions. The strategic implication is a bifurcated market, volume growth in emerging economies and value growth in mature ones.

The primary structural growth engine for the global genset market is the widening gap between electricity demand growth and reliable grid infrastructure investment. Industrial electrification, 5G network densification, electric vehicle charging infrastructure, and the reshoring of semiconductor and pharmaceutical manufacturing are all placing simultaneous, unprecedented stress on power grids that were designed for a pre-digital economy. This demand-side pressure is compounded on the supply side by grid vulnerability, cyber threats, physical climate events, geopolitical disruptions, that is causing risk managers across every critical industry to revisit their power resilience strategies. Simultaneously, tightening emission standards, EPA Tier 4 Final in the United States, EU Stage V in Europe, and CPCB IV+ in India, are forcing OEMs into expensive engine re-engineering and aftertreatment integration, raising barriers to entry and consolidating market share among technically capable players. Fuel cost volatility and the accelerating decarbonisation agenda are further complicating the picture by driving demand for gas, dual-fuel, and ultimately hydrogen-capable genset platforms whose commercial viability is still being established.

Key Drivers

- The foundational growth driver in 2026 and beyond is the structural acceleration of mission-critical infrastructure investment, with data centres at its epicentre. Global data centre construction spending is projected to exceed USD 500 billion over the next five years, with AI-dedicated facilities consuming power at densities that make generator-backed resilience non-negotiable. Each hyperscale data centre facility typically requires between 10 MW and 100+ MW of backup genset capacity, with multiple redundant units, real-time synchronisation systems, and extended fuel storage for 72-hour or 96-hour runtime at full load. Beyond data centres, the global rollout of 5G networks is requiring the retrofitting or replacement of hundreds of thousands of telecom tower gensets with lower-emission, higher-efficiency units capable of handling variable renewable energy integration. Healthcare systems in North America, Europe, and the Middle East are simultaneously upgrading their critical power infrastructure in the aftermath of pandemic-era stress tests that exposed dangerous gaps in power resilience. This convergence of data, telecom, and healthcare infrastructure investment is creating a quality-over-quantity demand dynamic that is structurally shifting the product mix toward high-margin, technically sophisticated genset systems.

- A parallel and increasingly powerful growth vector is the energy transition itself, a phenomenon that is simultaneously the genset industry’s greatest medium-term challenge and its most compelling near-term opportunity. The intermittency of solar and wind power creates a reliability gap that, in the absence of cost-effective grid-scale storage, is currently being filled by gas and dual-fuel gensets operating in island-mode, microgrid, and grid-support configurations. In Sub-Saharan Africa and Southeast Asia, solar-diesel hybrid gensets are displacing pure-diesel systems at scale, reducing fuel consumption by 30–60% while maintaining the reliability that off-grid communities and industrial operations demand. In developed markets, gas-fuelled and biogas-compatible gensets are being integrated into distributed energy resource (DER) portfolios that allow commercial and industrial (C&I) customers to participate in demand response programs, earning revenue during peak grid stress periods. The emergence of Power-as-a-Service (PaaS) and rental fleet models, pioneered by companies such as Aggreko, Atlas Copco, and SDMO, is further expanding the addressable market by converting large capital expenditures into operating expenditure arrangements that are attractive to budget-constrained infrastructure operators across emerging markets.

- The third major driver is the accelerating electrification of industrial and commercial activity in regions with chronically unreliable grid infrastructure. In Nigeria, Pakistan, Bangladesh, Indonesia, and several West African and Central Asian markets, the cost of grid power unreliability, measured in lost production, spoiled inventory, and equipment damage, dwarfs the total cost of ownership of a genset. This economic reality makes genset procurement a non-discretionary capital expenditure rather than an optional resilience investment. Manufacturing plants, cold storage facilities, hospitals, and data centres in these markets operate gensets as primary or co-primary power sources rather than as backup systems. This creates structurally higher utilisation rates, shorter replacement cycles (typically 8–12 years versus 20+ years in standby applications), and sustained after-sales revenue from spare parts, maintenance contracts, and fuel management services. As formalisation of economic activity accelerates across these markets, driven by mobile payments, digital logistics, and industrial zone development, the installed genset base is expanding at double-digit annual rates in several countries, generating a compounding installed base that guarantees long-run services and replacement revenue for established OEMs and their dealer networks.

Key Challenges

- The most structurally significant headwind facing the global genset industry is the accelerating tightening of emission regulations across all major markets, which is compressing OEM product development timelines and fundamentally raising the cost of engine compliance. The transition from EPA Tier 3 to Tier 4 Final in North America, from EU Stage IIIB to Stage V in Europe, and the phased implementation of CPCB IV+ norms in India has required OEMs to integrate diesel particulate filters (DPF), selective catalytic reduction (SCR) systems, exhaust gas recirculation (EGR), and diesel exhaust fluid (DEF/AdBlue) systems into engine-alternator configurations that were previously defined by their mechanical simplicity. These aftertreatment systems add 15–25% to unit manufacturing costs, introduce new failure modes, require specialised maintenance technician training, and impose DEF fluid logistics requirements that are impractical in many off-grid deployment environments. For smaller regional assemblers and importers who lack the R&D capability to indigenously develop compliant engine platforms, relying instead on sourced engines from Tier 1 suppliers, the transition creates acute vulnerability to supply chain disruptions, component lead-time extensions, and pricing pressure from OEMs who leverage compliance superiority as a competitive moat.

- A compounding operational challenge is the volatility and strategic uncertainty surrounding diesel fuel, the lifeblood of the global genset installed base, at precisely the moment when the industry must begin transitioning toward alternative fuels. Diesel price volatility, driven by crude oil market dynamics, refining capacity constraints, and geopolitical supply disruptions, directly impacts the total cost of ownership calculations that drive genset procurement decisions, particularly in prime and continuous power applications where fuel represents 60–80% of lifetime operating costs. Simultaneously, ESG mandates from institutional investors, sustainability frameworks from global brands, and direct regulatory pressure in markets such as the UK, Germany, and California are creating reputational and compliance risk for operators of large diesel genset fleets. The transition pathway to gas, dual-fuel, and ultimately hydrogen-fuelled platforms is technically clear but commercially uncertain, gas infrastructure is absent across many high-growth markets, hydrogen genset technology is pre-commercial, and the cost premium of fuel cell gensets over diesel reciprocating units remains prohibitive for the vast majority of applications. This creates a structural tension between the decarbonisation imperative and the operational realities of the markets that need reliable power most urgently, placing OEMs in the difficult position of managing two concurrent product roadmaps with incompatible infrastructure requirements.

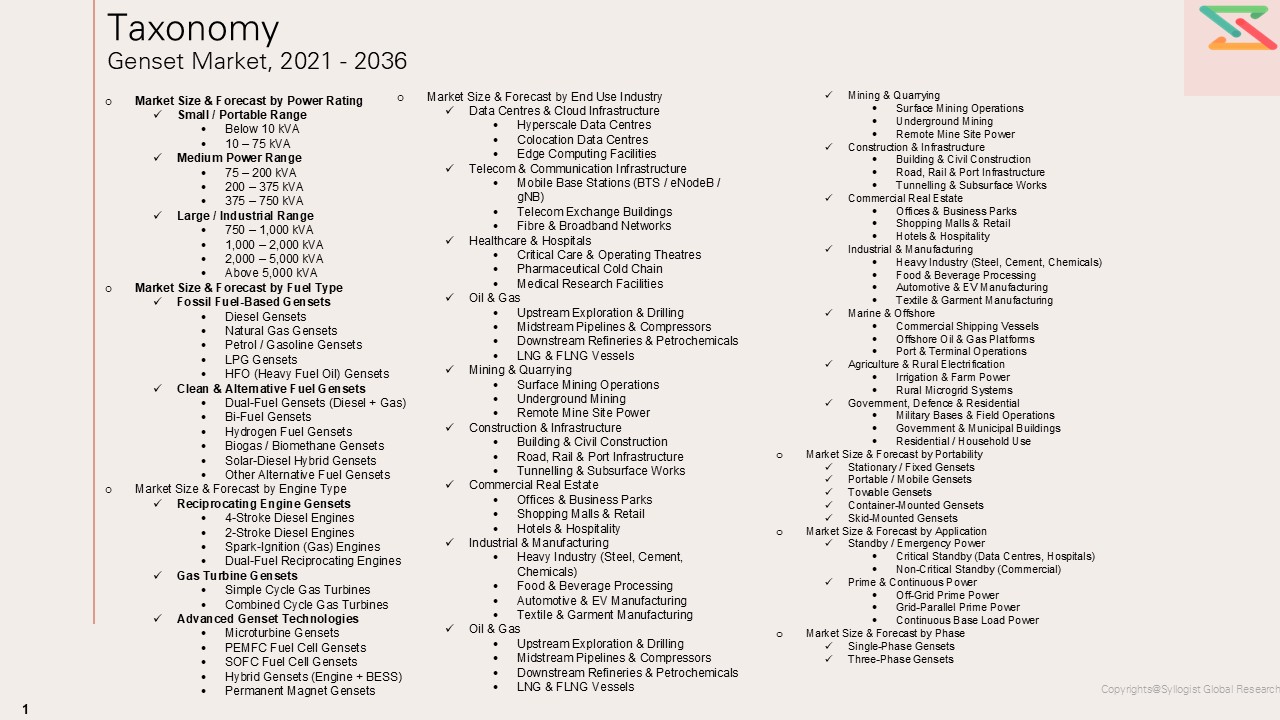

Market Segmentation

- Segmentation by Power Rating

- Below 75 kVA

- 75 – 375 kVA

- 375 – 1,000 kVA

- 1,000 – 2,000 kVA

- 2,000 – 5,000 kVA

- Above 5,000 kVA

- Segmentation by Fuel Type

- Diesel Gensets

- Natural Gas Gensets

- Petrol / Gasoline Gensets

- Dual-Fuel Gensets (Diesel + Gas)

- Bi-Fuel Gensets

- LPG Gensets

- HFO (Heavy Fuel Oil) Gensets

- Hydrogen Gensets

- Biogas / Biomethane Gensets

- Solar-Hybrid Gensets

- Other Alternative Fuel Gensets

- Segmentation by Engine Type

- Reciprocating Engine Gensets

- 4-Stroke Diesel Engines

- 2-Stroke Diesel Engines

- Spark-Ignition (Gaseous Fuel) Engines

- Dual-Fuel Reciprocating Engines

- Gas Turbine Gensets

- Simple Cycle Gas Turbines

- Combined Cycle Gas Turbines

- Microturbine Gensets

- Fuel Cell Gensets

- PEMFC (Proton Exchange Membrane)

- SOFC (Solid Oxide Fuel Cell)

- Hybrid Gensets (Engine + Battery Storage)

- Permanent Magnet Generator Gensets

- Reciprocating Engine Gensets

- Segmentation by Application

- Standby / Emergency Power

- Critical Standby (Data Centres, Hospitals, Telecoms)

- Non-Critical Standby (Commercial Buildings, Retail)

- Prime Power

- Off-Grid Prime Power

- Grid-Parallel Prime Power

- Continuous Power

- Peak Shaving & Load Management

- Combined Heat & Power (CHP / Cogeneration)

- Mobile / Rental Power

- Export / Distributed Grid Support

- Standby / Emergency Power

- Segmentation by End Use Industry

- Data Centres & Cloud Infrastructure

- Hyperscale Data Centres

- Colocation Data Centres

- Edge Computing Facilities

- Telecom & Communication Infrastructure

- Mobile Base Stations (BTS / eNodeB / gNB)

- Telecom Exchange Buildings

- Fibre & Broadband Networks

- Healthcare & Hospitals

- Critical Care & Operating Theatres

- Pharmaceutical Cold Chain

- Medical Research Facilities

- Oil & Gas

- Upstream Exploration & Drilling

- Midstream Pipelines & Compressor Stations

- Downstream Refineries & Petrochemicals

- LNG & FLNG Vessels

- Mining

- Surface Mining Operations

- Underground Mining

- Remote Mine Site Power

- Construction & Infrastructure

- Commercial Real Estate

- Offices & Business Parks

- Shopping Malls & Retail

- Hotels & Hospitality

- Industrial & Manufacturing

- Heavy Industry (Steel, Cement, Chemicals)

- Food & Beverage Processing

- Automotive Manufacturing

- Textile & Garment Manufacturing

- Marine & Offshore

- Commercial Shipping Vessels

- Offshore Oil & Gas Platforms

- Port & Terminal Operations

- Agriculture & Rural Electrification

- Government, Defence & Public Services

- Residential

- Data Centres & Cloud Infrastructure

- Segmentation by Portability

- Stationary / Fixed Gensets

- Portable / Mobile Gensets

- Towable Gensets

- Container-Mounted Gensets

- Skid-Mounted Gensets

- Segmentation by Phase

- Single-Phase Gensets

- Three-Phase Gensets

All market revenues are presented in USD and volume in units (number of gensets) and installed capacity (kVA / MW)

Historical Year: 2021–2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027–2036

Key Questions this Study Will Answer

- What are the critical market metrics and forward-looking projections for the Global Genset Market, including revenue size, unit volume, installed capacity (kVA/MW), and average selling prices by power rating (Below 75 kVA, 75–375 kVA, 375–1,000 kVA, 1,000–2,000 kVA, Above 2,000 kVA), fuel type (Diesel, Natural Gas, Dual-Fuel, LPG, Hydrogen, Biogas, Solar-Hybrid), engine type (Reciprocating, Gas Turbine, Microturbine, Fuel Cell, Hybrid), application (Standby, Prime, Continuous, CHP, Peak Shaving, Rental), end-use industry (Data Centres, Telecom, Healthcare, Oil & Gas, Mining, Construction, Marine, Industrial, Residential), portability (Stationary, Portable, Container-Mounted), and phase configuration (Single-Phase, Three-Phase)?

- How do supply–demand fundamentals vary across key regions and major consuming industries, and what role do grid reliability indices, industrial electrification rates, data centre construction pipelines, telecom tower densification, energy transition policies, emission compliance timelines, and infrastructure investment cycles play in shaping regional market competitiveness, alongside local manufacturing capability in engine assembly, alternator winding, control panel integration, canopy fabrication, and after-sales service network depth, as well as procurement structures across direct OEM sales, authorised dealer networks, EPC contractors, and rental fleet operators?

- In what ways are raw material and component price volatility and lead-time constraints, covering engine components (crankshafts, pistons, fuel injection systems, turbochargers, aftertreatment systems), alternator materials (copper windings, laminated steel cores, permanent magnets), electronic control modules, semiconductor chips, structural steel, and exhaust systems, influencing production costs, OEM pricing strategies, distributor margins, delivery lead times, and total cost of ownership calculations, especially for EPA Tier 4 Final and EU Stage V compliant units requiring diesel particulate filters, SCR systems, and EGR components?

- Who are the leading global and regional genset OEMs, engine manufacturers, alternator suppliers, and rental operators, and how do they benchmark across key performance dimensions including fuel efficiency (L/hr at rated load), load acceptance capability (motor starting kVA), transient response time, mean time between failures (MTBF), noise emission levels (dBA at 7m), emission compliance certification, remote monitoring and telematics capability, service network coverage, portfolio breadth across power ratings, fuel flexibility, and value-added solutions such as Power-as-a-Service, hybrid energy integration, and digital fleet management platforms?

- What strategic insights emerge from primary discussions with genset OEMs, engine and alternator manufacturers, EPC contractors, rental fleet operators, data centre developers, telecom infrastructure managers, and industrial facility managers regarding demand shifts toward fuel-flexible and lower-emission genset platforms, specification changes driven by EPA Tier 4 / EU Stage V and CPCB IV+ compliance requirements, substitution trends between diesel and gas-fuelled systems, regional sourcing strategies for compliant engines and aftertreatment components, rental versus ownership procurement preferences, and key purchase criteria such as fuel consumption efficiency, emission compliance, total cost of ownership, service network proximity, remote monitoring capability, load bank testing performance, and extended warranty coverage?

- Market Overview

- Product Overview

- Research Methodology

- Executive Summary

- Market Dynamics

- Market Dynamics (Drivers, Restraints, Opportunities, Challenges, Porter’s Five Forces Analysis, PESTLE Analysis)

- Market Trends & Developments

- Risk Assessment Framework

- Political / Geopolitical Risk

- Fuel & Component Supply Risk

- Environmental and Regulatory Risk

- Financial / Market Risk

- Regulatory Framework & Standards

- Global Regulatory Overview

- Key Regulations by Region

- EU: EU Machinery Directive, Emissions Stage V, CE Marking

- USA: EPA Tier 4 Final, CARB Regulations, NFPA 110

- China: GB Standards, MEE Emission Norms

- India: CPCB Norms (CPCB II / IV+), BIS Standards

- Emission Standards & Compliance

- Diesel Engine Emission Tiers (EPA Tier 1–Tier 4 Final)

- EU Stage I–Stage V Standards

- IMO Tier III for Marine Gensets

- Noise & Vibration Regulations

- Electrical Safety & Grid Connection Standards

- IEC 60034 (Rotating Electrical Machines)

- IEC 60947 (Low-voltage Switchgear)

- IEEE 1547 (Distributed Energy Resources)

- National Grid Codes & Synchronisation Standards

- Fuel Quality & Storage Regulations

- Diesel & HFO Sulphur Content Limits

- Natural Gas Purity Standards

- Hydrogen & Alternative Fuel Safety Codes

- Sustainability & ESG Compliance

- Carbon Footprint Reporting & Scope 1 Emissions Accounting

- Extended Producer Responsibility (EPR) for End-of-Life Equipment

- Green Building & Data Centre Sustainability Certifications

- Regulatory Impact on Market — Opportunities & Threats

- Global Genset Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume / Units

- Market Size & Forecast by Power Rating

- Below 75 kVA

- 75–375 kVA

- 375–1,000 kVA

- 1,000–2,000 kVA

- 2,000–5,000 kVA

- Above 5,000 kVA

- Market Size & Forecast by Fuel Type

- Diesel Gensets

- Natural Gas Gensets

- Petrol / Gasoline Gensets

- Dual-Fuel Gensets

- Bi-Fuel Gensets

- LPG Gensets

- HFO (Heavy Fuel Oil) Gensets

- Hydrogen Gensets

- Biogas / Biomethane Gensets

- Solar-Hybrid Gensets

- Other Alternative Fuel Gensets

- Market Size & Forecast by Engine Type

- Reciprocating Engine Gensets

- 4-Stroke Diesel Engines

- 2-Stroke Diesel Engines

- Spark-Ignition (Gaseous Fuel) Engines

- Dual-Fuel Reciprocating Engines

- Gas Turbine Gensets

- Simple Cycle Gas Turbines

- Combined Cycle Gas Turbines

- Microturbine Gensets

- Fuel Cell Gensets

- PEMFC (Proton Exchange Membrane Fuel Cell)

- SOFC (Solid Oxide Fuel Cell)

- Hybrid Gensets (Engine + Battery Storage)

- Permanent Magnet Generator Gensets

- Reciprocating Engine Gensets

- Market Size & Forecast by Application

- Standby / Emergency Power

- Critical Standby (Hospitals, Data Centres, Telecoms)

- Non-Critical Standby (Commercial Buildings)

- Prime Power

- Off-Grid Prime Power

- Grid-Parallel Prime Power

- Continuous Power

- Peak Shaving & Load Management

- Combined Heat & Power (CHP / Cogeneration)

- Mobile / Rental Power

- Export / Grid Support

- Standby / Emergency Power

- Market Size & Forecast by End Use Industry

- Data Centres & Cloud Infrastructure

- Hyperscale Data Centres

- Colocation Data Centres

- Edge Computing Facilities

- Telecom & Communication Infrastructure

- Mobile Base Stations (BTS / eNodeB / gNB)

- Telecom Exchange Buildings

- Fibre & Broadband Networks

- Healthcare & Hospitals

- Critical Care & Operating Theatres

- Pharmaceutical Cold Chain

- Medical Research Facilities

- Oil & Gas

- Upstream Exploration & Drilling

- Midstream Pipelines & Compressor Stations

- Downstream Refineries & Petrochemicals

- LNG & FLNG Vessels

- Mining

- Surface Mining Operations

- Underground Mining

- Remote Mine Site Power

- Construction & Infrastructure

- Building Construction

- Road & Rail Infrastructure

- Tunnelling & Underground Works

- Commercial Real Estate

- Offices & Business Parks

- Shopping Malls & Retail

- Hotels & Hospitality

- Industrial & Manufacturing

- Heavy Industry (Steel, Cement, Chemicals)

- Food & Beverage Processing

- Automotive Manufacturing

- Textile & Garment Manufacturing

- Utilities & Power Generation

- Distribution Grid Support

- Peaker Plants

- Island & Microgrid Systems

- Marine & Offshore

- Commercial Shipping Vessels

- Offshore Oil & Gas Platforms

- Yachts & Leisure Craft

- Port & Terminal Operations

- Agriculture & Rural Electrification

- Irrigation & Farm Power

- Cold Storage & Food Preservation

- Rural Microgrids

- Government, Defence & Public Services

- Military Bases & Field Operations

- Emergency Management & Disaster Relief

- Government Buildings & Municipalities

- Education & Research Institutions

- Residential

- Data Centres & Cloud Infrastructure

- Market Size & Forecast by Portability

- Stationary / Fixed Gensets

- Portable / Mobile Gensets

- Towable Gensets

- Container-Mounted Gensets

- Skid-Mounted Gensets

- Market Size & Forecast by Phase

- Single-Phase Gensets

- Three-Phase Gensets

- Market Size & Forecast by Region

- North America

- Europe

- Asia-Pacific

- Middle East & Africa

- Latin America

- Asia-Pacific Genset Market Outlook

- Market Size & Forecast

- By Value

- By Volume / Units

- By Power Rating

- By Fuel Type

- By Engine Type

- By Application

- By End Use Industry

- By Portability

- By Phase

- Market Size & Forecast

- Europe Genset Market Outlook

- Market Size & Forecast

- By Value

- By Volume / Units

- By Power Rating

- By Fuel Type

- By Engine Type

- By Application

- By End Use Industry

- By Portability

- By Phase

- Market Size & Forecast

- North America Genset Market Outlook

- Market Size & Forecast

- By Value

- By Volume / Units

- By Power Rating

- By Fuel Type

- By Engine Type

- By Application

- By End Use Industry

- By Portability

- By Phase

- Market Size & Forecast

- Latin America Genset Market Outlook

- Market Size & Forecast

- By Value

- By Volume / Units

- By Power Rating

- By Fuel Type

- By Engine Type

- By Application

- By End Use Industry

- By Portability

- By Phase

- Market Size & Forecast

- Middle East & Africa Genset Market Outlook

- Market Size & Forecast

- By Value

- By Volume / Units

- By Power Rating

- By Fuel Type

- By Engine Type

- By Application

- By End Use Industry

- By Portability

- By Phase

- Market Size & Forecast

- Country Wise* Genset Market Outlook

- Market Size & Forecast

- By Value

- By Volume / Units

- By Power Rating

- By Fuel Type

- By Engine Type

- By Application

- By End Use Industry

- By Portability

- By Phase

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, China, Germany, India, Japan, United Kingdom, Saudi Arabia, UAE, Australia, South Korea, Canada, Brazil, Nigeria, South Africa, Indonesia, Malaysia, Thailand, France, Italy, Mexico, Turkey, Egypt, Vietnam, Qatar, Kenya, Bangladesh, Philippines, Poland, Netherlands, Singapore

- Technology Analysis

- Conventional Vs Advanced Genset Technologies

- Diesel Reciprocating Engine Technology

- Gas Engine & Dual-Fuel Technology

- Gas Turbine Technology

- Hybrid Genset Technology (Engine + Battery)

- Fuel Cell Genset Technology

- Microturbine Technology

- Technology Readiness Levels (TRL) by Genset Type

- Emerging Technologies

- Hydrogen-Fuelled Gensets

- Ammonia-Fuelled Power Generation

- AI-Based Load Prediction & Adaptive Control

- Remote Monitoring, Telematics & IoT Integration

- Digital Twin for Predictive Maintenance

- Advanced Battery-Genset Hybrid Systems

- Green Hydrogen + Fuel Cell Gensets

- Conventional Vs Advanced Genset Technologies

- Value Chain & Supply Chain Analysis

- Raw Material & Component Suppliers

- Engine Manufacturers

- Alternator / Generator Manufacturers

- Control Panel & ATS Suppliers

- Genset OEM Assemblers

- Distributors, Dealers & Rental Companies

- End-Use Industries

- Ecosystem Map

- Supply Chain Analysis

- Key Components & Raw Materials (Engines, Alternators, Steel, Copper, Electronics)

- Supply Chain Risks & Disruptions

- China & Asia Dependency Analysis

- Semiconductor Shortage Impact on Genset Electronics

- Trade Flow Analysis

- Major Exporting Countries

- Major Importing Countries

- Import-Export Dynamics

- Pricing Analysis

- Global Average Selling Price by Power Rating

- Below 75 kVA Pricing ($/kVA)

- 75–375 kVA Pricing ($/kVA)

- 375–1,000 kVA Pricing ($/kVA)

- Above 1,000 kVA Pricing ($/kVA)

- Price Tier Analysis

- Economy / Entry-Level Gensets

- Mid-Range Gensets

- Premium & High-Performance Gensets

- Specialty / Rental-Grade Gensets

- Fuel Type Price Differential Analysis

- Diesel vs Natural Gas Total Cost of Ownership

- Hybrid Genset Premium Pricing

- Global Average Selling Price by Power Rating

- Sustainability & Energy Efficiency

- Emission Reduction Roadmap for Genset Industry

- Fuel Efficiency & Consumption Benchmarks

- Alternative Fuel Adoption & Green Genset Trends

- Carbon Footprint & Life Cycle Assessment (LCA)

- Circular Economy: Remanufacturing, Refurbishment & End-of-Life

- ESG Reporting by Major OEMs

- Go-to-Market & Distribution

- Sales Channel Overview

- Direct OEM Sales

- Authorised Dealer & Distributor Network

- Rental & Power-as-a-Service (PaaS) Models

- EPC & Project Contractor Channel

- Online & E-Commerce Channel

- After-Sales Service, AMC & Spare Parts Market

- Rental Market Analysis

- Short-Term vs Long-Term Rental Dynamics

- Key Rental Fleet Operators

- Distribution Strategies by Leading Players

- Sales Channel Overview

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented Vs Consolidated)

- Top 5 Players Market Share

- HHI (Herfindahl–Hirschman Index) Concentration Analysis

- Competitive Intensity Map

- Player Classification

- Market Leaders

- Strong Challengers

- Specialist / Niche Players

- Emerging Players

- Regional Players

- Competitive Analysis Frameworks

- Market Share Analysis

- Company Profile

- Company Overview & HQ

- Products & Solutions Portfolio

- Revenue & Genset Segment Revenue

- Geographic Presence

- Recent Developments (M&A, Launches, Partnerships)

- SWOT Analysis

- Strategic Focus Areas

- Competitive Positioning Map

- Market Structure & Concentration

- Strategic Recommendations

- For Genset Manufacturers (OEMs)

- Product & Technology Strategy

- Portfolio Strategy (Power Ratings, Fuel Types)

- Go-to-Market Strategy

- Sustainability & Emission Compliance Strategy

- M&A & Partnership Strategy

- For End-Use Industries

- Data Centre & Telecom Operators

- Oil & Gas Companies

- Healthcare Facility Managers

- Mining & Construction Contractors

- For Investors & Private Equity

- High-Priority Investment Themes

- M&A Opportunity Map

- Geographic Investment Priorities

- Risk Considerations

- For Governments & Regulators

- Policy Recommendations

- Rural Electrification & Energy Access Initiatives

- Supply Chain Resilience

- White Space & Opportunity Analysis

- Unmet Market Needs

- Emerging Business Models (PaaS, Hybrid Rental)

- Technology White Spaces (Hydrogen, Fuel Cell, AI Control)

- Strategic Priority Matrix & Roadmap

- Near-term (2025–2028)

- Mid-term (2029–2032)

- Long-term (2033–2036)

- For Genset Manufacturers (OEMs)