Market Definition

The Global Greenhouse Films Market encompasses the research, development, manufacturing, distribution, and end-of-life management of polymeric film materials engineered specifically for deployment as the primary cladding, covering, or enclosure material of protected cultivation structures including multi-span and single-span greenhouse tunnels, low tunnels, high tunnels, and walk-in production structures used in the commercial cultivation of vegetables, fruits, flowers, ornamental plants, and nursery stock across temperate, subtropical, and arid agricultural production environments worldwide. Greenhouse films are performance-engineered polymeric sheet materials produced primarily through blown film extrusion and cast film extrusion processes from polyethylene resin bases, including low-density polyethylene, linear low-density polyethylene, ethylene vinyl acetate copolymers, and thermoplastic polyolefin blends, incorporating multilayer coextrusion architectures that allow the simultaneous optimization of optical, mechanical, thermal, and functional properties within a single film structure tailored to the specific climatic, crop, and agronomic requirements of the end-use protected cultivation application. The product scope of this market encompasses standard polyethylene greenhouse films providing basic light transmission and weather protection for low-technology growing structures, multilayer diffuse light films incorporating light-scattering additives or microstructured surface layers that convert direct solar radiation into diffuse light distributed uniformly across the crop canopy to reduce photoinhibition, improve canopy light interception, and enhance yield and quality in high-value vegetable and floriculture applications, anti-drip and anti-fog functional films incorporating hydrophilic surface additives that prevent condensation droplet formation on the film interior surface and eliminate drip-induced disease infection and fruit quality damage, infrared blocking thermal films incorporating mineral or organic infrared-absorbing additives that selectively absorb and re-emit long-wave thermal radiation to reduce nighttime heat loss from protected structures and lower supplemental heating energy costs in cool and temperate climate growing regions, ultraviolet stabilized films formulated with hindered amine light stabilizer packages extending functional service life to multiple growing seasons, ultraviolet absorbing and ultraviolet blocking films incorporating benzophenone, benzotriazole, or triazine ultraviolet absorbers that selectively filter specific wavelengths of solar ultraviolet radiation to suppress insect navigation and reproduction within protected structures as an integrated pest management tool, anti-viral films formulated with copper-based or photocatalytic titanium dioxide antimicrobial additive systems providing surface-level pathogen suppression capability, thermochromic and photochromic functional films capable of dynamically modulating light transmission in response to temperature or solar intensity to manage crop heat stress during peak summer conditions, and the emerging category of bio-based and compostable greenhouse films formulated from polylactic acid, polyhydroxyalkanoate, or thermoplastic starch blends targeting circular economy and agricultural plastic waste reduction objectives in markets with stringent end-of-life plastic management regulations. The technology landscape within this market spans commodity single-layer polyethylene films at the entry-tier price and performance level, two-layer and three-layer coextruded films offering optimized mechanical and functional performance, and five-layer and seven-layer high-performance coextruded films incorporating specialized functional additive packages in discrete layers to achieve the demanding combinations of optical, thermal, mechanical, and durability properties required by high-technology commercial greenhouse operations in competitive horticultural production markets. The value chain of this market extends from ethylene monomer producers and polyethylene resin manufacturers through specialty chemical additive and masterbatch producers supplying ultraviolet stabilizers, infrared absorbers, anti-drip agents, and light diffusing additives, blown and cast film extrusion equipment manufacturers, greenhouse film converting and fabrication companies, agricultural distributor and dealer networks, and the commercial greenhouse operators, horticultural producers, contract growers, and smallholder farming households whose adoption decisions and replacement purchasing cycles define the volume and value structure of global greenhouse film demand across more than 90 countries with significant protected cultivation industries.

Market Insights

The global greenhouse films market is exhibiting a robust and structurally supported demand trajectory in 2026, underpinned by the sustained global expansion of protected cultivation area driven by rising consumer demand for year-round fresh produce supply, the intensification of commercial horticultural production in emerging economies pursuing food security and agricultural modernization objectives, and the growing recognition among farming communities worldwide that controlled environment agriculture enabled by greenhouse film covering represents the most accessible and capital-efficient pathway to productivity enhancement, water use efficiency improvement, and crop quality upgrading relative to open field production under unpredictable climate conditions. The global greenhouse films market was valued at approximately USD 3.1 billion in 2025 and is projected to expand at a compound annual growth rate of 6 percent through 2036, reaching approximately USD 5.9 billion by the end of the forecast period, a trajectory reflecting the structural expansion of protected cultivation area in Asia-Pacific, the Middle East, and Latin America, the progressive upgrading of film specifications from commodity single-layer polyethylene toward high-value multilayer functional films with enhanced service life and agronomic performance, and the growing regulatory and commercial pressure for the development and adoption of sustainable and recyclable greenhouse film formulations that address the significant agricultural plastic waste management challenges created by the annual replacement of large areas of end-of-life polyethylene greenhouse covering. The competitive landscape of the market encompasses global integrated petrochemical and specialty film producers who participate in the greenhouse film segment as one component of broader agricultural film and specialty packaging portfolios, dedicated agricultural film manufacturers whose technical expertise, product development investment, and agronomic application knowledge are focused exclusively on the protected cultivation film market, regional film extruders serving local greenhouse industries with standard commodity film products, and the specialty additive and masterbatch companies whose proprietary functional additive packages differentiate the technical performance of premium greenhouse film products and whose technology licensing relationships with film producers shape the innovation pipeline of the broader market.

A defining technological trend reshaping the competitive structure and value dynamics of the greenhouse films market is the accelerating adoption of multilayer diffuse light film technologies by commercial greenhouse operators in high-value vegetable and floriculture production segments, driven by the accumulating scientific and commercial evidence that controlled conversion of direct solar radiation into diffuse light through light-scattering film formulations delivers measurable and commercially significant improvements in crop yield, fruit quality uniformity, and growing season extension that justify the price premium of diffuse film products over commodity direct-light transmission alternatives in the economic calculus of professional greenhouse growers operating in competitive fresh produce and floriculture markets. Diffuse light greenhouse films, which incorporate barium sulfate, calcium carbonate, or engineered polymeric microsphere light-scattering additives at precisely controlled loading levels within one or more layers of a multilayer coextruded film structure, have demonstrated yield improvements across a range of high-value greenhouse crops including tomatoes, cucumbers, peppers, roses, and chrysanthemums that translate into return-on-investment calculations favoring the premium film specification over the commodity alternative across a broad range of greenhouse structure sizes and regional market conditions. The technology frontier within diffuse film development is advancing toward spectrally selective diffuse films that not only scatter incoming solar radiation but simultaneously shift the spectral distribution of transmitted light toward wavelengths most efficiently utilized by chlorophyll photosynthesis, combining the uniformity benefits of diffuse light distribution with the photosynthetic efficiency advantages of spectrum management in a single film product. Simultaneously, the integration of infrared blocking thermal functionality with diffuse light optical performance in high-specification three-layer and five-layer film architectures is enabling greenhouse operators in cool and temperate climate growing regions to simultaneously capture the yield benefits of diffuse light and the energy cost savings of improved nighttime thermal insulation within a single premium film product, significantly strengthening the total value proposition of advanced multilayer films relative to commodity alternatives and supporting the favorable average selling price dynamics that are contributing to above-volume revenue growth in the premium segment of the market.

The functional film segment of the greenhouse films market, encompassing ultraviolet blocking and ultraviolet absorbing films designed to suppress insect pest pressure within protected structures, is experiencing a period of intensified commercial development interest driven by the intersection of tightening regulatory restrictions on chemical insecticide use in food crop production in the European Union, Japan, and several advanced horticultural markets, the growing consumer and retail buyer demand for residue-free and organically certified fresh produce, and the demonstrated agronomic effectiveness of ultraviolet blocking film deployment as a physical barrier to the navigation and reproduction of key greenhouse pest species including whiteflies, thrips, and aphids that serve as primary vectors for economically destructive plant viruses in tomato, pepper, and cucumber production. Ultraviolet blocking films operate on the principle that key greenhouse insect pest species rely on ultraviolet wavelength light cues for navigation, host plant location, and reproductive behavior, and that removing or substantially attenuating the ultraviolet component of solar radiation entering the greenhouse structure through selective wavelength absorption by film additives disrupts these behavioral pathways sufficiently to significantly reduce pest population establishment rates and the associated virus transmission pressure within the protected structure. The commercial adoption of ultraviolet blocking film technology in Mediterranean, Middle Eastern, and East Asian greenhouse industries is translating into measurable reductions in insecticide application frequency and volume, reduced chemical residue levels in harvested produce, lower crop protection input costs per unit of production, and improved worker health outcomes in growing operations where chemical spray exposure had been a persistent occupational health concern, creating a multi-dimensional value proposition that is supporting the premium pricing of ultraviolet blocking film products and driving progressive market share expansion of this functional film category within the broader greenhouse films market.

From a regional perspective, Asia-Pacific represents the largest and fastest-growing regional market for greenhouse films by volume, driven by the world’s largest protected cultivation industries concentrated in China, Japan, South Korea, and the rapidly expanding greenhouse sectors of India, Vietnam, Indonesia, and Thailand, where the combination of government agricultural modernization programs, rural income enhancement initiatives, rising domestic demand for fresh vegetables and fruits, and the commercial development of export-oriented horticultural production systems is sustaining high rates of new greenhouse structure installation and film replacement demand across a highly fragmented and geographically extensive farming base. China alone accounts for the dominant share of global greenhouse film consumption by area, with its vast inventory of single-layer polyethylene-covered tunnel structures serving as the volume foundation of the market while the progressive upgrading of film specifications toward multilayer functional products in higher-value production systems is generating a quality mix improvement trend that is elevating average selling prices and revenue per unit area consumed across the Chinese market. Europe represents the most technically advanced regional market for greenhouse film innovation and premium product adoption, characterized by the highest penetration of long-life multilayer functional films, diffuse light technology, and bio-based film development activity, a well-organized greenhouse film collection and recycling infrastructure in several northern European countries, and stringent regulatory frameworks governing agricultural plastic management that are driving both film formulation innovation toward recyclable and bio-based alternatives and the development of industry-level extended producer responsibility programs for end-of-life film collection and material recovery. The Middle East and North Africa region, encompassing the large and expanding protected cultivation industries of Spain, Morocco, Turkey, Egypt, Israel, Saudi Arabia, and the United Arab Emirates, represents the most significant regional growth market for premium and functional greenhouse film products outside Asia-Pacific, where the combination of intense solar radiation requiring advanced film thermal management and ultraviolet control, water scarcity driving the adoption of covered cultivation to reduce evapotranspiration losses, and the commercial development of high-value export-oriented vegetable and fruit production for European markets is creating strong agronomic and economic pull for advanced multilayer film technologies.

Key Drivers

Global Expansion of Protected Cultivation Area and the Intensification of Commercial Horticultural Production Driven by Food Security, Water Efficiency, and Year-Round Fresh Produce Supply Imperatives

The most structurally significant and geographically universal demand driver for greenhouse films is the sustained global expansion of protected cultivation area as the primary agricultural technology response to the converging pressures of population growth, rising per-capita fresh produce consumption, agricultural water scarcity, climate variability increasing the frequency and severity of adverse growing conditions in open field production systems, and the commercial imperative of high-value horticultural producers to extend their productive growing seasons and supply fresh produce to retail and food service buyers who demand year-round supply consistency irrespective of regional growing season limitations. The adoption of greenhouse film-covered tunnel and multi-span structure cultivation is demonstrably the most capital-efficient and operationally accessible pathway to productivity and quality enhancement available to farmers across a wide range of economic and technological contexts, from the subsistence-oriented smallholder producing vegetables for local markets in South and Southeast Asia using low-cost single-layer polyethylene tunnel structures, to the large-scale commercial greenhouse enterprise in the Netherlands, Spain, or Mexico deploying advanced multi-span climate-controlled glass or film structures for export-grade tomato, pepper, and cucumber production. The yield advantage of protected cultivation relative to open field production for high-value vegetable and fruit crops is substantial and well-documented across growing regions and crop categories, with greenhouse-grown tomatoes, cucumbers, and strawberries typically yielding multiples of the open field production achievable per unit of land area, a productivity premium that provides the fundamental economic justification for greenhouse structure investment and the associated annual or biennial greenhouse film replacement cost that constitutes the primary recurring operating expense of the film-covered protected cultivation system. Government agricultural development programs in rapidly mechanizing and commercializing farming economies across Asia, the Middle East, Africa, and Latin America are actively promoting greenhouse cultivation adoption through subsidy programs for greenhouse structure construction, agricultural credit provision for film and equipment purchases, technical training initiatives demonstrating protected cultivation benefits to farming communities, and market infrastructure development supporting the commercial linkages between greenhouse producers and urban retail and food processing buyers, all of which are translating government agricultural modernization investment into direct and measurable greenhouse film demand growth that is structural and durable rather than cyclical in character.

Progressive Upgrading of Greenhouse Film Specifications Toward High-Performance Multilayer Functional Products Delivering Measurable Agronomic and Economic Value to Commercial Growers

The second major structural demand driver reshaping the revenue trajectory of the global greenhouse films market, operating alongside and in some markets more powerfully than the area expansion driver, is the ongoing and accelerating commercial upgrade of greenhouse film specifications from commodity single-layer and basic two-layer polyethylene products toward high-performance multilayer functional films incorporating diffuse light, infrared thermal blocking, extended ultraviolet stabilization, anti-drip, ultraviolet blocking, and combination multi-functional additive packages whose agronomic performance benefits deliver measurable and commercially quantifiable improvements in crop yield, quality, energy cost, pesticide use, and growing season extension that justify the premium price of advanced film products and generate favorable return-on-investment calculations even in price-sensitive production environments. The commercial mechanism driving the specification upgrade trend is the progressive demonstration and dissemination of agronomic performance data from commercial grower experience and controlled trial programs showing that the yield, quality, and cost savings benefits of premium multilayer film products consistently exceed the price premium charged relative to commodity alternatives, creating a growing body of evidence-based commercial justification for film specification upgrading that is being communicated to farming communities through agricultural extension programs, film manufacturer agronomic support services, greenhouse equipment supplier recommendations, and peer learning networks among commercially oriented greenhouse producers. The extended service life characteristic of ultraviolet-stabilized long-life film formulations provides an additional economic mechanism supporting the specification upgrade trend, as the ability of premium ultraviolet-stabilized film products to maintain mechanical integrity and optical performance across multiple growing seasons reduces the annualized film replacement cost per unit area of greenhouse coverage to a level that is competitive with or lower than the total cost of replacing shorter-life commodity films on more frequent replacement cycles, while simultaneously capturing the agronomic performance benefits of diffuse light, infrared blocking, and other functional additive packages in the premium multilayer film formulation. The specification upgrade trend is expected to be sustained across the forecast period by the continued commercial validation of next-generation film technologies including thermochromic films, spectrally selective photosynthetically optimized films, and bio-based long-life films, each of which adds new dimensions of agronomic value creation that will support the progressive elevation of average selling prices and revenue per unit area across the global greenhouse film market.

Key Challenges

Agricultural Plastic Waste Management and End-of-Life Greenhouse Film Collection, Recycling, and Regulatory Compliance Challenges Creating Cost and Operational Burden for Industry Stakeholders

The most consequential systemic challenge facing the global greenhouse films market is the growing scale and complexity of the agricultural plastic waste management problem created by the annual replacement of millions of tonnes of end-of-life polyethylene greenhouse film across global protected cultivation industries, whose end-of-life management through open field burning, landfill disposal, or uncontrolled abandonment generates significant environmental contamination, greenhouse gas emissions, and regulatory liability that are attracting increasing legislative attention and civil society pressure across major greenhouse film consuming regions and that are creating material compliance cost and operational complexity obligations for greenhouse film producers, distributors, and end users who must increasingly demonstrate responsibility for end-of-life film management as a condition of market access and commercial license. The collection and recycling of spent polyethylene greenhouse film presents substantial technical and logistical challenges that distinguish it from urban plastic waste streams more readily managed by conventional recycling infrastructure, as end-of-life greenhouse film is contaminated with soil, sand, crop residue, pesticide and fertilizer residues, and moisture that reduce its suitability for mechanical recycling into food-grade or packaging-grade secondary resin and that require specialized wash-line equipment and chemical pretreatment processes to clean the film to a quality level acceptable for extrusion into secondary polyethylene products including agricultural drainage pipe, refuse sacks, or construction film. The regulatory frameworks governing agricultural plastic waste management are tightening progressively across the European Union, several Latin American jurisdictions, and advanced Asian horticultural markets, with mandatory extended producer responsibility schemes requiring greenhouse film manufacturers to finance and administer take-back and recycling programs for the films they place on the market, plastic waste reduction targets setting declining thresholds for agricultural plastic disposed of through burning or landfill, and import and market access restrictions in some markets conditioning the commercial authorization of greenhouse film products on the demonstrable availability of end-of-life collection and recycling pathways accessible to the farming customers purchasing those products. The combination of regulatory compliance cost, extended producer responsibility program investment, and the capital expenditure required to develop dedicated agricultural plastic wash-line and recycling infrastructure is adding a significant cost burden to the greenhouse film industry’s operating structure that is particularly challenging for smaller regional film producers with limited financial resources and organizational capacity to establish compliant extended producer responsibility programs independently.

Volatility of Polyethylene Resin and Specialty Additive Raw Material Costs and the Margin Compression Challenge of Passing Through Input Cost Increases to Price-Sensitive Agricultural End Users

A persistent structural challenge confronting greenhouse film manufacturers is the exposure of their production economics to the significant and unpredictable price volatility of polyethylene resin and specialty functional additive raw materials, whose cost movements are driven by crude oil and natural gas feedstock price cycles, petrochemical capacity addition and turnaround schedules, geopolitical disruptions to ethylene and polyethylene trade flows, and the supply and demand dynamics of specialty chemical markets for ultraviolet stabilizers, infrared absorbers, anti-drip surfactants, and light-diffusing mineral additives, and whose transmission into greenhouse film production cost structures creates margin compression risk that is particularly acute in market environments where the agricultural character of the end customer base makes price increase acceptance difficult to achieve without volume loss to lower-priced competitors or alternative covering materials. The polyethylene resin cost, which typically represents the largest single component of greenhouse film manufacturing cost at more than half of total production cost for standard film formulations, exhibits cyclical volatility that has historically spanned a wide range from trough to peak within individual commodity price cycles, creating profit margin variability for film producers whose conversion cost structures are relatively fixed in the short term and who cannot rapidly adjust production volumes, product mix, or capacity utilization in response to resin price movements without incurring operational disruption and customer supply reliability risks. The specialty functional additive cost structure adds an additional and partially independent dimension of raw material cost variability, as the hindered amine light stabilizer, ultraviolet absorber, infrared blocking mineral, and anti-drip surfactant components of premium multilayer film formulations are produced by a limited number of specialty chemical manufacturers whose pricing reflects capacity constraints, raw material costs within their own supply chains, and the value-in-use pricing premium extractable from a differentiated specialty chemical customer base, creating supply concentration and price opacity challenges for film producers seeking to manage functional additive procurement costs within the context of competitive film pricing obligations to agricultural customers. The challenge of transmitting raw material cost increases through to greenhouse film selling prices is compounded by the seasonal and geographically dispersed character of greenhouse film demand, which creates procurement leverage for large distributor and cooperative buyer organizations that can aggregate demand across farming communities and negotiate price concessions from multiple competing film suppliers during the pre-season ordering window that determines the majority of film volume placement in most regional markets.

Market Segmentation

- Segmentation By Film Type

- Single-Layer Polyethylene Greenhouse Films

- Two-Layer Coextruded Greenhouse Films

- Three-Layer Coextruded Greenhouse Films

- Five-Layer Coextruded Greenhouse Films

- Seven-Layer Coextruded Greenhouse Films

- Bio-Based and Compostable Greenhouse Films

- Others

- Segmentation By Resin Base

- Low-Density Polyethylene (LDPE)

- Linear Low-Density Polyethylene (LLDPE)

- Ethylene Vinyl Acetate (EVA) Copolymer

- Thermoplastic Polyolefin (TPO) Blends

- Polylactic Acid (PLA) and Bio-Based Polymers

- Polyhydroxyalkanoate (PHA)-Based Films

- Hybrid and Multilayer Resin Blends

- Others

- Segmentation By Functional Additive Technology

- Diffuse Light and Light-Scattering Films

- Infrared Blocking and Thermal Retention Films

- Anti-Drip and Anti-Fog Functional Films

- Ultraviolet Stabilized Long-Life Films

- Ultraviolet Absorbing and Ultraviolet Blocking Pest Management Films

- Anti-Viral and Antimicrobial Functional Films

- Thermochromic and Photochromic Light-Modulating Films

- Spectrally Selective Photosynthetically Optimized Films

- Multi-Functional Combination Additive Films

- Others

- Segmentation By Service Life

- Single-Season Films (Below 12 Months)

- Standard Service Life Films (1 to 2 Years)

- Long-Life Films (3 to 4 Years)

- Extended Long-Life Films (5 Years and Above)

- Segmentation By Application Structure

- Multi-Span Commercial Greenhouse Structures

- Single-Span Tunnel Greenhouses

- High Tunnel and Walk-In Production Structures

- Low Tunnel and Row Cover Applications

- Shade Net and Net House Integration

- Nursery and Propagation Structures

- Others

- Segmentation By Crop Type

- Tomatoes

- Cucumbers and Gourds

- Peppers and Capsicum

- Strawberries and Soft Fruits

- Leafy Vegetables and Herbs

- Cut Flowers and Floriculture

- Ornamentals and Nursery Stock

- Melons and Watermelons

- Others

- Segmentation By End User

- Large-Scale Commercial Greenhouse Enterprises

- Mid-Scale Professional Horticultural Producers

- Smallholder and Family Farm Greenhouse Operators

- Agricultural Cooperative and Group Procurement Organizations

- Government and Institutional Agricultural Programs

- Others

- Segmentation By Sales Channel

- Agricultural Input Distributors and Dealers

- Greenhouse Equipment and Structure Suppliers

- Agricultural Cooperative Procurement Networks

- Direct Sales from Film Manufacturers

- Online and Digital Agricultural Procurement Platforms

- Government Agricultural Supply Programs

- Others

- Segmentation By Region

- Asia-Pacific

- Europe

- Middle East and Africa

- Latin America

- North America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2036

Key Questions this Study Will Answer

- What is the projected global market valuation and volume for greenhouse films through 2036, segmented by film type, resin base, functional additive technology, service life category, crop type, and region, and which product technology categories and geographic markets are expected to generate the highest incremental revenue and area coverage growth across the forecast period?

- How is the accelerating commercial adoption of multilayer diffuse light, infrared blocking thermal, and ultraviolet blocking pest management film technologies reshaping the product mix, average selling price dynamics, and profitability of greenhouse film manufacturers, and what agronomic performance evidence and return-on-investment metrics are most effectively driving the conversion of commodity film purchasers to premium functional film specifications across different regional markets and crop production systems?

- What is the trajectory of protected cultivation area expansion across Asia-Pacific, the Middle East and Africa, and Latin America through 2036, and how are government agricultural modernization programs, rural credit expansion, export-oriented horticultural development initiatives, and water scarcity adaptation strategies in these regions translating into greenhouse film volume demand growth that exceeds the replacement purchasing activity of mature established greenhouse industries in Europe and North America?

- How are the evolving extended producer responsibility regulatory frameworks for agricultural plastic waste management in the European Union, Latin America, and advanced Asian horticultural markets affecting the product development investment priorities, supply chain cost structures, and competitive positioning of greenhouse film manufacturers, and what bio-based, recyclable, and compostable film formulation technologies are advancing most rapidly toward the commercial readiness and cost-competitiveness required for adoption at commercial horticultural scale?

- What is the impact of polyethylene resin price volatility and specialty functional additive supply concentration on the gross margin profiles of greenhouse film manufacturers across different product mix and regional market positioning configurations, and what raw material procurement, hedging, vertical integration, and product pricing strategies are leading manufacturers deploying to manage input cost variability while sustaining the innovation investment required for competitive differentiation in premium functional film segments?

- Who are the leading greenhouse film manufacturers, specialty functional additive and masterbatch suppliers, agricultural plastic recycling infrastructure operators, and bio-based film technology developers currently defining the competitive landscape of the global greenhouse films market, and what are their respective product portfolio strategies, multilayer coextrusion technology investments, agronomic support program commitments, extended producer responsibility program designs, and regional expansion priorities for advancing greenhouse film performance and sustainability credentials through the forecast horizon?

- Product Definition

- Scope of the Study

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Industry Publications, Agriplastic & Greenhouse Film Manufacturer Reports & Press Releases

- Government Agriculture, Horticulture & Trade Authority Data (FAO, USDA, EU DG AGRI, MARD, ICAR, etc.)

- Greenhouse Film Production, Trade Volume & Covered Area Statistics

- Greenhouse Grower, Agrochemical Retailer & Plastics Distributor Procurement Databases

- Primary Research Design & Execution

- In-depth Interviews with Greenhouse Film Manufacturers, Resin Compounders, Greenhouse Constructors & Horticulture Input Distributors

- Surveys with Commercial Greenhouse Operators, Open-Field Fruit & Vegetable Growers, Flower Producers & Government Agricultural Development Agencies

- Expert Panel Validation

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Bottom-Up & Top-Down Reconciliation

- Covered Cultivation Area Expansion, Film Replacement Rate & Crop Intensity-Driven Market Sizing Model

- Resin Price Trajectory, Film Lifespan Improvement & Technology Substitution Adjustment Framework

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Technology & Innovation Highlights

- Manufacturing Economics & Unit Economics Summary

- Average Plant CAPEX & OPEX Benchmarks

- Mono-Layer vs Multi-Layer vs Anti-Drip vs UV-Stabilised Film Margin & Profitability Analysis

- PE, EVA, PVC & Bio-Based Greenhouse Film Revenue Model Summary

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Geographic & Regional Trends

- Risk Assessment Framework

- Geopolitical & Trade Policy Risk (Petrochemical Feedstock Export Restrictions, Anti-Dumping Measures)

- Raw Material Price Volatility (Polyethylene, EVA Resin, Plasticisers, UV Stabilisers, Antifog Additives) Risk

- Environmental & Plastic Waste Regulation Risk (EU Single-Use Plastics Directive, Extended Producer Responsibility)

- Climate Change & Extreme Weather Event Impact on Greenhouse Film Performance & Replacement Demand Risk

- Competing Covered Cultivation Technologies (Rigid Polycarbonate, Glass Panels, Shade Nets) Substitution Risk

- Financial / Market Risk: Agricultural Commodity Price Cyclicality & Grower Income Variability

- Bio-Based & Biodegradable Film Technology Adoption & Conventional Film Market Displacement Risk

- Regulatory Framework & Policy Standards

- Global Greenhouse Films Market Economics

- Manufacturing Economics & Unit Economics Framework

- Capital Expenditure (CAPEX) Structure

- Operating Expenditure (OPEX) Structure

- Revenue Model & Monetisation Levers (Film Sales, Custom Formulation Services, Technical Support & Agronomy Consulting)

- Capacity Utilisation & Throughput Economics

- Payback Period & Return on Investment (ROI) Analysis

- Total Cost of Production vs Competing Covering Materials (Rigid PC, Glass, Shade Net, Agrotextile)

- Raw Material & Input Cost Analysis

- Polyethylene (LDPE, LLDPE, HDPE, mLLDPE) Resin Price Trends (USD/tonne, 2021–2035)

- Ethylene Vinyl Acetate (EVA) & Polyvinyl Chloride (PVC) Resin Cost Dynamics

- UV Stabiliser (HALS, UV Absorber), Antioxidant & Thermal Stabiliser Additive Cost Structure

- Antifog, Anti-Drip, Diffusion & IR-Blocking Functional Additive Cost Analysis

- Pigment, Whitening Agent, Phosphorescent & Photoluminescent Additive Cost Structure

- Bio-Based Resin, Biodegradable Polymer (PLA, PBAT, PBS) & Compostable Film Feedstock Economics

- Energy Cost Structure in Greenhouse Film Extrusion & Blown Film Manufacturing

- Impact of Multi-Layer Co-Extrusion (3-Layer, 5-Layer, 7-Layer) on Film Product Economics

- Film Replacement, Disposal & End-of-Life Economics

- Film Replacement Rate by Crop Type, Climatic Zone & Film Lifespan Category

- Used Agricultural Film (UAF) Collection, Washing, Recycling & Regranulation Economics

- Extended Producer Responsibility (EPR) Scheme Compliance & Take-Back Programme Cost Economics

- Landfill Disposal vs Mechanical Recycling vs Energy Recovery Cost Comparison for End-of-Life Greenhouse Film

- Regulatory & Standards Compliance Economics

- Greenhouse Film Technical Performance & Durability Standards Compliance Cost Benchmarks (ISO, EN 13206, CEPLA, BPI, DIN, etc.)

- Food Contact, Pesticide Residue Migration & Crop Safety Certification Compliance Costs

- Plastic Packaging Recyclability, Recycled Content & EPR Levy Compliance Cost Structure

- Global Greenhouse Films Market Outlook

- Market Size & Forecast by Value (USD Billion, 2021–2036)

- Market Size & Forecast by Volume (Thousand Tonnes, 2021–2036)

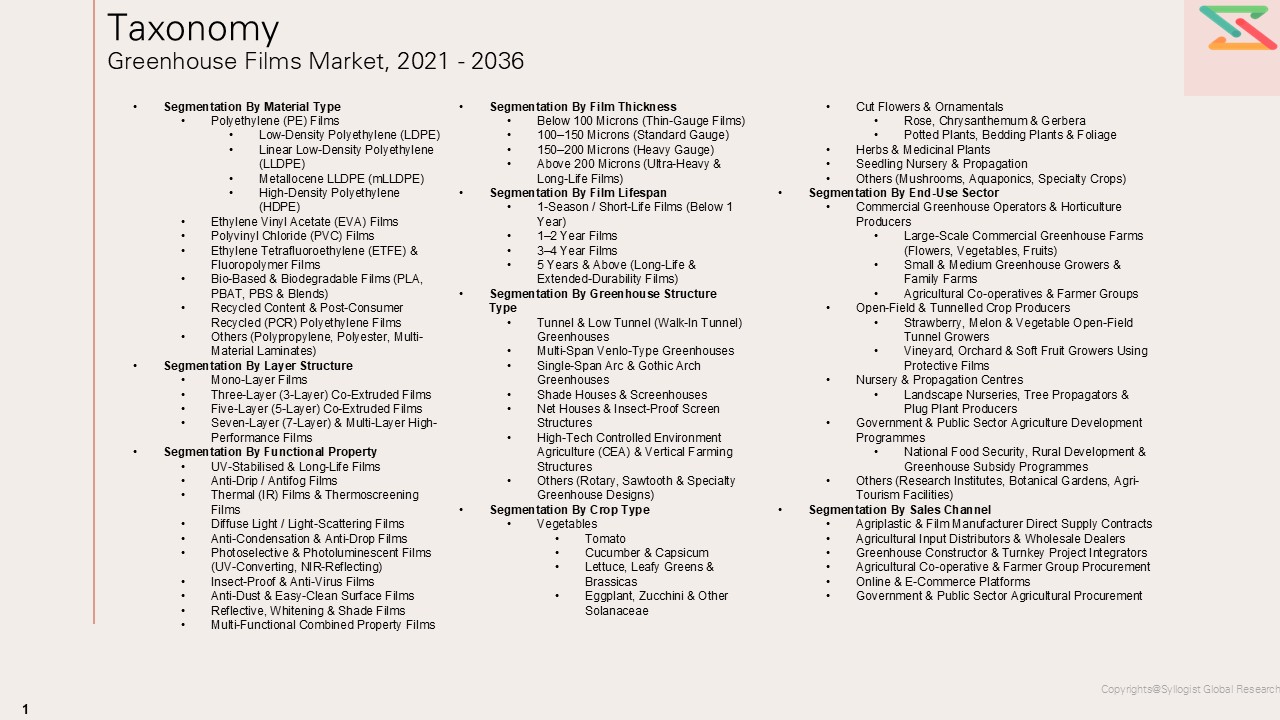

- Market Size & Forecast by Material Type

- Polyethylene (PE) Films

- Low-Density Polyethylene (LDPE)

- Linear Low-Density Polyethylene (LLDPE)

- Metallocene LLDPE (mLLDPE)

- High-Density Polyethylene (HDPE)

- Ethylene Vinyl Acetate (EVA) Films

- Polyvinyl Chloride (PVC) Films

- Ethylene Tetrafluoroethylene (ETFE) & Fluoropolymer Films

- Bio-Based & Biodegradable Films (PLA, PBAT, PBS & Blends)

- Recycled Content & Post-Consumer Recycled (PCR) Polyethylene Films

- Others (Polypropylene, Polyester, Multi-Material Laminates)

- Polyethylene (PE) Films

- Market Size & Forecast by Layer Structure

- Mono-Layer Films

- Three-Layer (3-Layer) Co-Extruded Films

- Five-Layer (5-Layer) Co-Extruded Films

- Seven-Layer (7-Layer) & Multi-Layer High-Performance Films

- Market Size & Forecast by Functional Property

- UV-Stabilised & Long-Life Films

- Anti-Drip / Antifog Films

- Thermal (IR) Films & Thermoscreening Films

- Diffuse Light / Light-Scattering Films

- Anti-Condensation & Anti-Drop Films

- Photoselective & Photoluminescent Films (UV-Converting, NIR-Reflecting)

- Insect-Proof & Anti-Virus Films

- Anti-Dust & Easy-Clean Surface Films

- Reflective, Whitening & Shade Films

- Multi-Functional Combined Property Films

- Market Size & Forecast by Film Thickness

- Below 100 Microns (Thin-Gauge Films)

- 100–150 Microns (Standard Gauge)

- 150–200 Microns (Heavy Gauge)

- Above 200 Microns (Ultra-Heavy & Long-Life Films)

- Market Size & Forecast by Film Lifespan

- 1-Season / Short-Life Films (Below 1 Year)

- 1–2 Year Films

- 3–4 Year Films

- 5 Years & Above (Long-Life & Extended-Durability Films)

- Market Size & Forecast by Greenhouse Structure Type

- Tunnel & Low Tunnel (Walk-In Tunnel) Greenhouses

- Multi-Span Venlo-Type Greenhouses

- Single-Span Arc & Gothic Arch Greenhouses

- Shade Houses & Screenhouses

- Net Houses & Insect-Proof Screen Structures

- High-Tech Controlled Environment Agriculture (CEA) & Vertical Farming Structures

- Others (Rotary, Sawtooth & Specialty Greenhouse Designs)

- Market Size & Forecast by Crop Type

- Vegetables

- Tomato

- Cucumber & Capsicum

- Lettuce, Leafy Greens & Brassicas

- Eggplant, Zucchini & Other Solanaceae

- Fruits

- Strawberry & Soft Fruits

- Melon, Watermelon & Citrus

- Grape & Table Grape

- Cut Flowers & Ornamentals

- Rose, Chrysanthemum & Gerbera

- Potted Plants, Bedding Plants & Foliage

- Herbs & Medicinal Plants

- Seedling Nursery & Propagation

- Others (Mushrooms, Aquaponics, Specialty Crops)

- Vegetables

- Market Size & Forecast by End-Use Sector

- Commercial Greenhouse Operators & Horticulture Producers

- Large-Scale Commercial Greenhouse Farms (Flowers, Vegetables, Fruits)

- Small & Medium Greenhouse Growers & Family Farms

- Agricultural Co-operatives & Farmer Groups

- Open-Field & Tunnelled Crop Producers

- Strawberry, Melon & Vegetable Open-Field Tunnel Growers

- Vineyard, Orchard & Soft Fruit Growers Using Protective Films

- Nursery & Propagation Centres

- Landscape Nurseries, Tree Propagators & Plug Plant Producers

- Government & Public Sector Agriculture Development Programmes

- National Food Security, Rural Development & Greenhouse Subsidy Programmes

- Others (Research Institutes, Botanical Gardens, Agri-Tourism Facilities)

- Commercial Greenhouse Operators & Horticulture Producers

- Market Size & Forecast by Sales Channel

- Agriplastic & Film Manufacturer Direct Supply Contracts

- Agricultural Input Distributors & Wholesale Dealers

- Greenhouse Constructor & Turnkey Project Integrators

- Agricultural Co-operative & Farmer Group Procurement

- Online & E-Commerce Platforms

- Government & Public Sector Agricultural Procurement

- Asia-Pacific Greenhouse Films Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Volume (Thousand Tonnes)

- By Material Type

- By Layer Structure

- By Functional Property

- By Film Thickness

- By Film Lifespan

- By Greenhouse Structure Type

- By Crop Type

- By End-Use Sector

- By Sales Channel

- Key Demand Drivers (APAC-Specific)

- Competitive Landscape (APAC)

- Europe Greenhouse Films Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Volume (Thousand Tonnes)

- By Material Type

- By Layer Structure

- By Functional Property

- By Film Thickness

- By Film Lifespan

- By Greenhouse Structure Type

- By Crop Type

- By End-Use Sector

- By Sales Channel

- Key Demand Drivers (Europe-Specific)

- Competitive Landscape (Europe)

- North America Greenhouse Films Market Outlook

- Market Overview & Strategic Importance

- Market Size & Forecast

- By Value (2020–2035)

- By Volume (Thousand Tonnes)

- By Material Type

- By Layer Structure

- By Functional Property

- By Film Thickness

- By Film Lifespan

- By Greenhouse Structure Type

- By Crop Type

- By End-Use Sector

- By Sales Channel

- Key Demand Drivers (North America-Specific)

- Competitive Landscape (North America)

- Latin America Greenhouse Films Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Volume (Thousand Tonnes)

- By Material Type

- By Layer Structure

- By Functional Property

- By Film Thickness

- By Film Lifespan

- By Greenhouse Structure Type

- By Crop Type

- By End-Use Sector

- By Sales Channel

- Key Demand Drivers (LATAM-Specific)

- Competitive Landscape (LATAM)

- Middle East & Africa Greenhouse Films Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Volume (Thousand Tonnes)

- By Material Type

- By Layer Structure

- By Functional Property

- By Film Thickness

- By Film Lifespan

- By Greenhouse Structure Type

- By Crop Type

- By End-Use Sector

- By Sales Channel

- Key Demand Drivers (MEA-Specific)

- Competitive Landscape (MEA)

- Country-Wise Greenhouse Films Market Outlook

- Market Size & Forecast by Country

- By Value

- By Volume (Thousand Tonnes)

- By Material Type

- By Layer Structure

- By Functional Property

- By Film Thickness

- By Film Lifespan

- By Greenhouse Structure Type

- By Crop Type

- By End-Use Sector

- By Sales Channel

- Market Size & Forecast by Country

- Market Size & Forecast

- Market Size & Forecast

- Market Size & Forecast

- Market Size & Forecast

- Manufacturing Economics & Unit Economics Framework

Countries Covered: China, Spain, Turkey, Italy, Netherlands, France, Morocco, Egypt, Iran, India, Mexico, South Korea, Japan, United States, Brazil, Israel, South Africa, Saudi Arabia, Argentina, Australia

- Technology Landscape & Innovation Analysis

- Greenhouse Film Technology Maturity Assessment

- Emerging & Disruptive Technologies in Greenhouse Film Materials & Manufacturing

- Next-Generation Metallocene & mLLDPE Resin Platforms: Enhanced Optical Clarity, Mechanical Strength & Long-Life Performance

- Photoselective & Spectral-Conversion Films: NIR-Reflecting, UV-Converting & Fluorescent Light Management for Crop Optimisation

- Smart Greenhouse Films: Thermochromic, Electrochromic & Phase-Change Material (PCM) Integration for Adaptive Climate Control

- Bio-Based & Fully Compostable Greenhouse Film Technology: PLA, PBAT, PBS & Starch-Blended Film Commercialisation Roadmap

- Nano-Additive & Surface Coating Technologies: Anti-Reflective, Self-Cleaning, Anti-Static & Enhanced UV-Stabilisation Coatings

- High-Speed Multi-Layer Co-Extrusion & Blown Film Line Advances for 5-Layer & 7-Layer Specialty Greenhouse Films

- Technology Readiness & Commercialisation Matrix – Key Greenhouse Film Technologies

- Patent Landscape Analysis

- R&D Investment Benchmarking

- Value Chain & Supply Chain Analysis

- Greenhouse Films Value Chain Mapping

- Supply Chain Concentration & Dependency Analysis

- Key Supplier Mapping by Material & Technology Programme

- Polyethylene & EVA Resin Producer & Petrochemical Feedstock Supplier Mapping

- UV Stabiliser (HALS), Antioxidant & Functional Additive Manufacturer Mapping

- Antifog, Anti-Drip, Diffusion & IR-Blocking Specialty Masterbatch Supplier Mapping

- Bio-Based Resin, Biodegradable Polymer & Compostable Film Feedstock Supplier Mapping

- Blown Film Extrusion & Co-Extrusion Line Equipment Manufacturer Mapping

- Supplier Risk Heat Map

- Make vs Buy Strategy Trends Among Greenhouse Film Manufacturers & Agriplastic Compounders

- Pricing Analysis

- Greenhouse Film Pricing Dynamics & Mechanisms

- Pricing by Material Type, Layer Structure, Functional Property, Film Thickness & Lifespan

- Total Cost of Ownership (TCO) Analysis – Including Film Purchase, Installation, Replacement Frequency, Disposal & Crop Yield Impact

- PE vs EVA vs PVC vs Bio-Based Film Pricing Trends & Benchmarks

- Standard Mono-Layer vs Premium Multi-Layer Specialty Film Pricing & Value Proposition

- Sustainability & Environmental Stewardship

- Environmental & Sustainability Landscape in Greenhouse Film Manufacturing & Agricultural Use

- Carbon Footprint & Energy Intensity Benchmarking Across Film Material Types & Production Technologies

- Used Agricultural Film (UAF) Collection, Recycling Infrastructure & Circular Economy Assessment

- Bio-Based & Biodegradable Greenhouse Film Adoption: Agronomic Performance, Soil Safety & End-of-Life Pathway Assessment

- Plastic Waste Reduction, Extended Producer Responsibility (EPR) & Microplastic Impact Mitigation in Horticulture

- ESG Reporting & Lifecycle Assessment (LCA) in Greenhouse Film Manufacturing & Agricultural Deployment

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level: Global Agriplastic Leaders vs Regional Manufacturers & Local Film Producers

- Top 5 Greenhouse Film Manufacturers Market Revenue Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis by Material Type, Functional Property & Region

- Competitive Intensity Map by Segment & Region

- Player Classification

- Tier-1 Global Integrated Agriplastic & Greenhouse Film Manufacturers (Politiv, Ginegar, Solarig, Armando Alvarez, Haygrove, Plastika Kritis, etc.)

- Tier-2 Regional & Specialist Greenhouse Film Manufacturers & Multi-Layer Film Producers

- Emerging Bio-Based, Biodegradable & Smart Film Technology Developers & Startups

- Emerging & Disruptive Players

- Competitive Analysis Frameworks

- Market Share Analysis by Material Type, Functional Property & Geography

- R&D Intensity & Film Technology Portfolio Benchmarking

- Grower Customer Revenue, Long-Term Supply Contract & Agronomic Trial Programme Comparison

- Geographic Revenue Exposure Comparison

- Company Profiles

- Company Overview, HQ & Organisational Structure

- Greenhouse Film Products, Material Platform & Functional Property Portfolio

- Revenue Breakdown

- Key Grower Supply Programmes & Crop Trial Deployments

- Manufacturing Footprint & Key Facilities

- Recent Developments (M&A, Partnerships, New Products, Financial Results)

- SWOT Analysis

- Strategic Focus: Multi-Layer Film Innovation, Functional Additive Leadership, Bio-Based Film Commercialisation & Distribution Network Expansion

- Strategic Output

- Market Opportunity Matrix

- High-Value Opportunity Quadrant Analysis

- Addressable Market by Material Type, Functional Property, Crop Type & Region

- Time-to-Revenue Assessment by Opportunity

- White Space Opportunity Analysis

- Underserved Crop Type, Greenhouse Structure & Functional Property Gaps

- Geographic Markets with Low Greenhouse Film Penetration & High Protected Cultivation Growth

- Technology & Material Gaps with High Commercialisation Potential

- Customer Segment Unmet Needs

- Strategic Recommendations

- Product Portfolio & Film Technology Innovation Strategy

- Technology Platform, Additive & Resin Development Strategy

- Manufacturing Footprint & Capacity Expansion Strategy

- Grower Customer Engagement, Distribution Network & Channel Growth Strategy

- Pricing & Commercial Strategy

- Sustainability, EPR Compliance & Circular Economy Strategy

- Supply Chain & Raw Material Sourcing Strategy

- Partnership, M&A & Expansion Strategy

- Regional Growth Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-Term (2025–2028)

- Mid-Term (2029–2032)

- Long-Term (2033–2036)

- Market Opportunity Matrix

- Market Structure & Concentration