Market Definition

The Global Grid-Forming Inverter Technologies Market encompasses the design, development, manufacturing, integration, and commercialization of power electronic inverter systems that autonomously establish and regulate voltage magnitude, frequency, and phase angle at their point of connection to an alternating current electrical network, providing the fundamental grid-forming services of voltage source behavior, synthetic inertia, frequency regulation, and black-start capability that were historically supplied exclusively by the rotating mass and electromagnetic characteristics of synchronous generators in conventional thermal, hydro, and nuclear power plants. Grid-forming inverters are distinguished from the dominant installed base of grid-following inverters by their fundamental control architecture, which operates the inverter as a controlled voltage source behind an output impedance rather than as a controlled current source synchronized to a pre-existing grid voltage signal through a phase-locked loop, enabling grid-forming units to function as autonomous voltage and frequency references capable of operating in islanded microgrids without any synchronous generation present, supporting grid recovery and black-start sequences following system collapse, stabilizing weak grid nodes where the short-circuit ratio is insufficient for reliable phase-locked loop synchronization of grid-following devices, and providing the virtual synchronous machine behavior and damping torque that modern power system stability analysis identifies as essential for maintaining transient and small-signal stability in power systems with high penetrations of inverter-based renewable energy resources. The product scope of this market includes utility-scale grid-forming inverters integrated into solar photovoltaic power plant balance-of-plant systems, grid-forming inverter systems embedded in battery energy storage systems from residential and commercial scale through grid-scale four-hour and longer duration storage assets, grid-forming capable wind turbine full power converter systems, grid-forming inverters for offshore wind collection network and HVDC converter station applications, modular multilevel converter systems with grid-forming control for high-voltage direct current transmission terminals, grid-forming inverter systems for diesel generator replacement and hybrid power systems in remote and island grids, microgrid master controllers incorporating grid-forming inverter functionality for seamless islanding and reconnection, and the advanced control software, firmware, real-time simulation validation platforms, grid code compliance testing services, and power system stability consultancy that constitute the enabling technical ecosystem for grid-forming inverter deployment in regulated electricity markets. The technology landscape spans virtual synchronous machine and virtual synchronous generator control architectures that emulate the swing equation dynamics of synchronous generators, droop-based grid-forming control implementing proportional frequency and voltage regulation without explicit machine emulation, matching control approaches that align inverter dynamics with the physical energy storage characteristics of the DC source, dispatchable virtual oscillator control implementing nonlinear oscillator dynamics that provide inherent synchronization and load-sharing properties, and hybrid control architectures combining elements of multiple grid-forming paradigms to optimize performance across a range of operating conditions from strong interconnected transmission networks to weak and islanded distribution system applications. The value chain of this market extends from power semiconductor device manufacturers supplying insulated-gate bipolar transistors and silicon carbide metal-oxide-semiconductor field-effect transistors as the switching elements of grid-forming converter power stages, through passive component suppliers providing the filter inductors, capacitors, and transformers that shape inverter output waveform quality, inverter power stage hardware manufacturers, control system and real-time controller hardware developers, grid-forming control algorithm developers and software vendors, system integrators assembling complete grid-forming inverter solutions for utility and microgrid applications, power system studies and compliance testing service providers, transmission and distribution network operators specifying grid-forming capability requirements in grid connection codes and procurement tenders, and the independent power producers, renewable energy developers, energy storage project developers, and remote power system operators who ultimately deploy grid-forming inverter assets in power system applications globally.

Market Insights

The global grid-forming inverter technologies market is experiencing a decisive acceleration in commercial adoption momentum in 2026, driven by the convergence of rapidly escalating renewable energy penetration levels that are exposing the frequency and voltage stability limitations of power systems dominated by grid-following inverter-based resources, the accumulation of operational evidence from pioneering grid-forming deployments in Australia, Great Britain, Ireland, Hawaii, and several European island systems demonstrating the practical stabilization benefits of grid-forming technology in real power systems, and the progressive incorporation of explicit grid-forming capability requirements into grid connection codes and system services procurement frameworks by transmission system operators who have determined that grid-following inverter control architectures cannot provide the system strength and inertia services necessary for secure power system operation at the renewable energy penetration levels mandated by national decarbonization targets. The global grid-forming inverter market was valued at approximately USD 2.4 billion in 2025 and is projected to expand at a compound annual growth rate of 29 percent through 2036, reaching approximately USD 30 billion by the end of the forecast period, a trajectory reflecting the structural necessity of grid-forming technology as the enabling power electronics infrastructure for power systems transitioning beyond 60 percent instantaneous inverter-based resource penetration toward the 100 percent renewable electricity systems that an increasing number of national and subnational jurisdictions have legislated as long-term targets. The competitive landscape of the market is structured around a small number of large power electronics and energy systems corporations that have invested in proprietary grid-forming control platforms and are embedding grid-forming capability into their utility-scale solar, battery storage, and wind converter product lines, a growing cohort of specialized grid-forming control software and algorithm developers whose proprietary virtual synchronous machine and matching control implementations are licensed to inverter hardware manufacturers and project developers, and the transmission system operator and national laboratory research community whose system strength and stability analysis work is defining the technical specifications that commercial grid-forming products must satisfy to qualify for regulated system services payments and grid connection approval in increasingly demanding power system environments.

A defining technical and commercial development reshaping the competitive and regulatory landscape of the grid-forming inverter market is the progressive transition of grid-forming capability from a specialist niche technology deployed in isolated island and microgrid applications toward a standard mandatory specification for utility-scale battery energy storage systems and renewable energy plants connecting to high-voltage transmission networks in markets where system strength and inertia adequacy have become binding power system security constraints. The Australian Energy Market Operator’s System Strength Remediation framework, which has driven the procurement of grid-forming battery energy storage systems at multiple locations across the South Australian and Victorian transmission networks to address system strength deficits created by the retirement of synchronous generation and the expansion of wind and solar capacity, represents the most advanced example of transmission system operator-led market creation for grid-forming inverter technology and has established a commercially significant precedent that is being studied and progressively replicated by system operators in Great Britain, Ireland, continental Europe, and North America as renewable energy penetration levels in their own systems approach the thresholds at which system strength inadequacy becomes a binding operational constraint. The Great Britain electricity system operator has incorporated grid-forming capability requirements into its stability pathfinder procurement programs, creating a commercially defined market for grid-forming battery storage and synchronous compensator assets at specific weak grid locations identified through power system stability analysis, and establishing the contractual and technical specification framework that grid-forming inverter suppliers must satisfy to compete for long-duration system stability service contracts whose revenue streams materially improve project economics relative to energy arbitrage and frequency response revenues alone. The accumulation of operational performance data from these pioneering transmission-connected grid-forming battery energy storage deployments is providing the empirical evidence base that regulatory bodies, transmission system operators, and project lenders require to advance grid-forming from a technically promising concept toward a bankable and standardly specified power system asset class.

The battery energy storage system segment has emerged as the primary commercial vehicle for grid-forming inverter technology deployment at utility scale, reflecting the unique suitability of battery storage as a grid-forming resource whose DC voltage source characteristic naturally supports the voltage-source inverter control architecture required for grid-forming operation, whose four-quadrant power flow capability enables simultaneous active and reactive power regulation essential for voltage and frequency support, and whose rapidly declining capital cost trajectory is enabling the deployment of grid-forming battery storage at system locations where the provision of system strength and inertia services justifies the incremental investment in grid-forming capable inverter hardware and control systems relative to equivalent grid-following battery storage installations. The integration of grid-forming control into battery energy storage system inverters is enabling a new generation of multi-service battery storage assets that simultaneously provide energy arbitrage revenue, frequency containment and restoration services, voltage regulation and reactive power support, system strength contribution quantified through short-circuit current injection capability, and black-start and islanding capability for critical load supply continuity, a multi-service revenue stacking model that materially improves project internal rates of return and is attracting increasing interest from energy storage project developers, independent power producers, and transmission network owners seeking cost-effective alternatives to synchronous compensator and gas peaker investments for system stability provision. Solar photovoltaic plant grid-forming inverters represent a growing secondary application segment, with several transmission system operators having issued grid connection requirements for new large-scale solar plants that include grid-forming capability specifications, and with solar inverter manufacturers progressively developing and certifying grid-forming control modes for their utility-scale central inverter and string inverter platforms to address this emerging specification requirement in competitive solar project procurement processes.

From a regional perspective, the Asia-Pacific region, led by Australia, represents the most commercially mature market for transmission-connected grid-forming inverter deployment, with Australia’s combination of high renewable energy penetration, geographically isolated synchronous power systems, a proactive transmission system operator with well-developed system strength assessment and remediation frameworks, and a large-scale battery energy storage procurement pipeline collectively creating the most commercially active environment for grid-forming inverter specification, procurement, and deployment at utility scale. Europe represents the most significant market for grid-forming technology development activity and regulatory framework evolution, with the United Kingdom, Ireland, and the Nordics at the forefront of grid code revision to incorporate grid-forming requirements, synchronous compensator and grid-forming battery storage procurement programs, and transmission system operator research investment in power system stability analysis methodologies for high inverter-based resource penetration systems. North America is the largest near-term growth opportunity for grid-forming inverter market expansion, with the accelerating retirement of thermal generation in the Electric Reliability Council of Texas, California Independent System Operator, and several Midcontinent Independent System Operator zones creating system strength and inertia adequacy challenges that are driving Federal Energy Regulatory Commission and independent system operator attention to grid-forming capability requirements, and with the large pipeline of battery energy storage projects seeking interconnection in these markets representing a substantial commercial opportunity for grid-forming inverter suppliers as interconnection studies begin to impose system strength contribution requirements on new storage and renewable energy projects as a condition of grid connection approval. Island power systems across the Caribbean, Pacific Islands, Mediterranean, and the Canary Islands represent a structurally important market segment for grid-forming inverter technology where the fundamental operating requirements of islanded systems with no synchronous generation create an absolute technical necessity for grid-forming capability that is independent of grid code evolution and system operator policy choices.

Key Drivers

Accelerating Renewable Energy Penetration Depleting Synchronous Inertia and System Strength Reserves, Creating Mandatory Demand for Grid-Forming Capability in Transmission-Connected Power Systems

The most structurally durable and commercially consequential demand driver for grid-forming inverter technologies is the fundamental and physically unavoidable depletion of the synchronous inertia and system strength resources that power systems require for frequency and voltage stability as the retirement of coal, gas, oil, and nuclear synchronous generation accelerates under national decarbonization policies and is replaced by grid-following inverter-based wind and solar resources that contribute no inherent inertia and actively reduce system short-circuit level through displacement of synchronous machines. The physics of power system stability are unambiguous on this point: a power system operating at high instantaneous penetrations of grid-following inverter-based resources without adequate synchronous inertia or synthetic inertia provision will exhibit rate-of-change-of-frequency responses to generation-load imbalance events that exceed the activation thresholds of under-frequency load shedding relays and potentially of under-frequency protection systems protecting synchronous generation, creating a cascade risk that conventional frequency response markets and grid-following inverter fast frequency response products cannot fully mitigate because grid-following inverters depend on the pre-existence of a stable grid voltage signal for their phase-locked loop synchronization and cannot maintain controlled operation during the transient voltage disturbances that accompany severe system contingency events. Transmission system operators in Australia, Great Britain, Ireland, and increasingly in continental European and North American markets have quantified these stability risks through detailed power system simulation studies and have determined that the maintenance of secure power system operation at renewable energy penetration levels consistent with national decarbonization targets requires either the retention of synchronous generation capacity beyond its economic operating life, the procurement of synchronous compensators to provide fault current and system strength contribution without energy conversion, or the deployment of grid-forming inverter-based resources capable of providing synthetic inertia and system strength contribution in a manner that is technically equivalent to synchronous machine provision for power system stability purposes. The economic comparison between these three system stability solution options is increasingly favoring grid-forming battery energy storage systems in markets where battery capital costs have declined sufficiently to make the grid-forming storage solution cost-competitive with synchronous compensator procurement on a per-unit-of-system-strength-contribution basis, creating the commercial demand environment in which grid-forming inverter technology is transitioning from research demonstration to mainstream procurement specification in transmission network investment programs.

Proliferation of Microgrids, Remote Power Systems, and Energy Resilience Infrastructure Creating Structural Demand for Grid-Forming Inverter Capability Across Distributed and Island Power Applications

The accelerating proliferation of microgrids, islanded power systems, and energy resilience infrastructure across a diverse range of application contexts spanning military base power security, critical facility backup power, remote community diesel replacement, island grid decarbonization, and industrial facility energy independence is creating a parallel and commercially significant demand stream for grid-forming inverter technology that is structurally distinct from the transmission system stability application and that is driven by the fundamental requirement of any autonomous alternating current power system for a voltage and frequency reference source that can establish and regulate the electrical conditions within which grid-following loads and generation assets can operate. The technical requirements of microgrid and island power system operation make grid-forming inverter capability not merely a desirable performance enhancement but an absolute functional prerequisite, as a microgrid operating in islanded mode without any synchronous generation asset present has no voltage source unless at least one grid-forming inverter or battery system with grid-forming control is present and active, a technical reality that has driven the near-universal adoption of grid-forming capable inverters in modern AC-coupled microgrid designs regardless of whether the specific application involves remote community power supply, military forward operating base energy security, or critical data center and hospital backup power infrastructure. The global military and defense sector represents a particularly significant and commercially distinctive demand segment for grid-forming inverter technology, with defense ministries in the United States, United Kingdom, European Union member states, and Australia actively investing in energy resilient microgrid infrastructure at military installations whose power supply security requirements cannot be satisfied by grid-following inverter systems dependent on utility grid connectivity for their operational reference, and with the procurement specifications for military microgrid energy storage and solar systems increasingly mandating grid-forming capability as a non-negotiable functional requirement. The global pipeline of remote community and island grid diesel replacement projects, driven by the combination of high diesel fuel costs, fuel logistics complexity in remote locations, and the availability of solar photovoltaic and battery storage at cost points that make diesel displacement economically attractive, represents a substantial volume market for grid-forming battery storage and solar inverter systems where the replacement of a diesel generator as the sole grid-forming source in a remote power system requires the battery inverter system to assume the voltage and frequency reference function previously provided by the rotating diesel generation asset.

Key Challenges

Absence of Standardized Grid-Forming Performance Specifications and Testing Protocols Creating Procurement Uncertainty and Slowing Large-Scale Commercial Deployment

The most consequential near-term commercial challenge limiting the pace of grid-forming inverter market expansion in transmission-connected utility applications is the absence of internationally harmonized and technically precise performance specifications defining what constitutes grid-forming capability for power system stability purposes, how grid-forming performance should be measured and verified through standardized laboratory and field testing protocols, and how the grid-forming contribution of inverter-based resources should be quantified and credited within power system stability assessment frameworks used by transmission system operators for grid connection approvals and system services procurement. The technical complexity of defining grid-forming performance specifications arises from the fundamental diversity of grid-forming control architectures currently in commercial development and deployment, encompassing virtual synchronous machine implementations, droop-based voltage source control, matching control, dispatchable virtual oscillator control, and proprietary hybrid approaches, each of which exhibits distinct dynamic response characteristics in terms of inertia constant equivalent, damping coefficient, fault current contribution magnitude and duration, voltage regulation bandwidth, and behavior during severe grid disturbances, making it technically challenging to define a single performance specification framework that is simultaneously technology-neutral, physically meaningful for power system stability analysis, and practically testable through standardized type-test procedures. Transmission system operators in different jurisdictions have responded to this specification gap by developing their own bespoke grid-forming performance requirements, with the Australian Energy Market Operator, Great Britain’s National Energy System Operator, Eirgrid and SONI in Ireland, and the Electricity Reliability Council of Texas all having developed distinct technical requirements for grid-forming capability that differ in their definition of minimum inertia constant equivalent, fault current contribution requirements, voltage regulation response time, and islanding and black-start capability specifications, creating a fragmented regulatory landscape in which grid-forming inverter products certified and deployed in one market may require substantial re-engineering or re-testing to satisfy the differing requirements of another market, increasing product development costs and reducing the economies of scale available to inverter manufacturers seeking to serve multiple national markets with standardized grid-forming product platforms. The Institute of Electrical and Electronics Engineers, CIGRE, and IEC technical committees are actively working on the development of international grid-forming performance specification and testing standards, but the timelines for standard development and national regulatory adoption mean that the commercial market will operate under fragmented jurisdiction-specific requirements throughout the near-term forecast period, sustaining the procurement complexity and compliance cost burden on both inverter suppliers and project developers.

Power System Operator Conservatism and the Extended Validation Requirements for New Grid-Forming Control Technologies Seeking Approval in Safety-Critical Electricity Transmission Infrastructure

A structurally significant commercial challenge constraining the pace of grid-forming inverter adoption in transmission-connected applications is the institutional conservatism of transmission system operators and electricity market regulators toward the deployment of novel power electronic control technologies in the safety-critical infrastructure of high-voltage transmission networks, where control system interactions, unforeseen instability modes, and protection system incompatibilities can have consequences extending from equipment damage at individual grid connection points to widespread system disturbances affecting large populations and critical national infrastructure. Transmission system operators responsible for maintaining power system security are institutionally incentivized toward caution in approving novel inverter control technologies for connection to transmission networks, given that the consequences of a control system failure or unexpected dynamic interaction between a new grid-forming inverter and the surrounding network can manifest as rapid voltage or frequency excursions affecting large areas of the interconnected transmission system, creating liability, regulatory, and reputational consequences for the system operator that are far more severe than those associated with the more gradual risks of delayed technology adoption. The validation requirements that transmission system operators impose on grid-forming inverter systems seeking approval for transmission-connected deployment reflect this institutional caution and typically encompass extensive power system model validation through electromagnetic transient simulation against detailed vendor-provided inverter models, hardware-in-the-loop testing using real-time digital simulators to verify control system behavior under a comprehensive set of system contingency and fault scenarios, factory acceptance testing with independent witnessing by transmission system operator technical staff, staged field commissioning tests verifying grid-forming performance against connection agreement specifications under live network conditions, and extended operational monitoring periods during which grid-forming performance is continuously assessed before full commercial service approval is granted. These validation requirements impose substantial time and cost burdens on grid-forming inverter projects, with the elapsed time from grid connection application submission to commercial service commencement for a transmission-connected grid-forming battery storage project frequently exceeding three years in markets with mature but conservative connection approval processes, creating project development timeline risks that affect project financing assumptions and that disadvantage grid-forming battery storage relative to synchronous compensator alternatives whose technology maturity and established connection approval processes provide greater development timeline certainty for transmission network owners and investors.

Market Segmentation

- Segmentation By Control Architecture

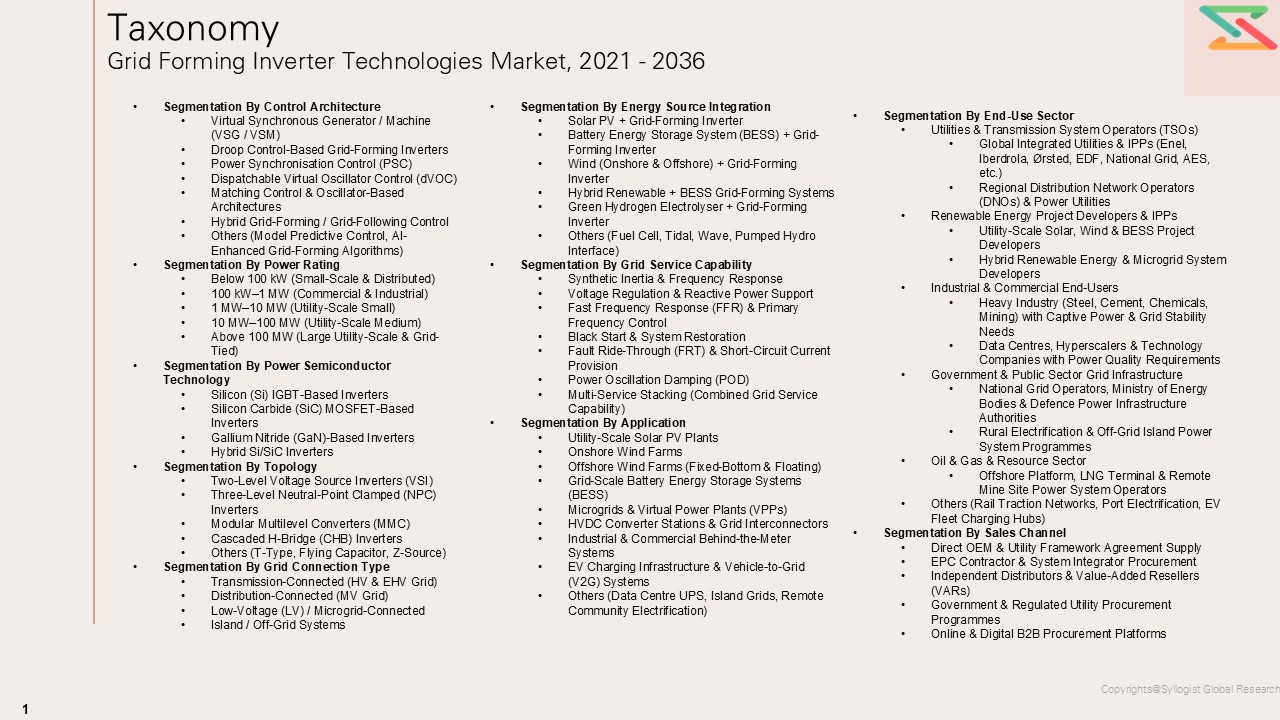

- Virtual Synchronous Machine (VSM) and Virtual Synchronous Generator (VSG)

- Droop-Based Voltage Source Grid-Forming Control

- Matching Control

- Dispatchable Virtual Oscillator Control (dVOC)

- Power Synchronization Control

- Hybrid Grid-Forming and Grid-Following Control

- Others

- Segmentation By Application

- Utility-Scale Battery Energy Storage Systems

- Utility-Scale Solar Photovoltaic Plants

- Onshore Wind Turbine Full Power Converters

- Offshore Wind Collection Network Converters

- HVDC Converter Station Controls

- Microgrid Master Controllers

- Remote and Island Grid Hybrid Power Systems

- Industrial and Commercial Microgrid Systems

- Military and Defense Energy Resilience Microgrids

- Others

- Segmentation By Inverter Topology

- Two-Level Voltage Source Inverters

- Three-Level Neutral Point Clamped Inverters

- Modular Multilevel Converters (MMC)

- Cascaded H-Bridge Inverters

- Impedance Source Inverters

- Others

- Segmentation By Power Rating

- Below 100 Kilowatts

- 100 Kilowatts to 1 Megawatt

- 1 Megawatt to 10 Megawatts

- 10 Megawatts to 100 Megawatts

- Above 100 Megawatts

- Segmentation By Switching Device Technology

- Silicon Insulated-Gate Bipolar Transistors (Si-IGBT)

- Silicon Carbide Metal-Oxide-Semiconductor FETs (SiC-MOSFET)

- Gallium Nitride Devices (GaN)

- Hybrid Silicon and Wide-Bandgap Device Modules

- Others

- Segmentation By Grid Connection Level

- Low Voltage Distribution (Below 1 kV)

- Medium Voltage Distribution (1 kV to 35 kV)

- High Voltage Sub-Transmission (35 kV to 150 kV)

- Extra High Voltage Transmission (Above 150 kV)

- Segmentation By System Service Capability

- Synthetic Inertia and Rate-of-Change-of-Frequency Support

- Frequency Containment and Restoration Reserve

- Voltage Regulation and Reactive Power Support

- System Strength and Short-Circuit Current Contribution

- Black-Start and System Restoration Capability

- Islanding and Seamless Reconnection

- Harmonic Mitigation and Power Quality Services

- Others

- Segmentation By End-Use Sector

- Utility and Transmission Network Operators

- Independent Power Producers and Energy Storage Developers

- Renewable Energy Plant Owners

- Industrial and Commercial Facility Operators

- Military and Defense

- Remote Communities and Island Grids

- Data Centers and Critical Infrastructure

- Others

- Segmentation By Component

- Grid-Forming Inverter Power Stage Hardware

- Grid-Forming Control Software and Firmware

- Real-Time Controller and DSP Hardware

- Output Filter and Transformer Systems

- Communication and SCADA Integration Systems

- Grid Code Compliance Testing and Validation Services

- Power System Stability Studies and Consultancy

- Others

- Segmentation By Region

- Asia-Pacific

- Europe

- North America

- Latin America

- Middle East and Africa

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2036

Key Questions this Study Will Answer

- What is the projected global market valuation for grid-forming inverter technologies through 2036, segmented by control architecture, application, power rating, inverter topology, system service capability, and region, and which product categories and geographic markets are expected to generate the highest incremental revenue growth across the forecast period?

- At what renewable energy penetration thresholds are transmission system operators in Australia, Great Britain, Ireland, continental Europe, and North America determining that system strength and inertia adequacy become binding power system security constraints, and how are these technical assessments translating into grid connection code revisions, system services procurement frameworks, and mandatory grid-forming capability specifications that are creating defined commercial markets for grid-forming inverter products and services?

- How are the competing virtual synchronous machine, droop-based voltage source, matching control, dispatchable virtual oscillator control, and hybrid grid-forming control architectures differentiating their technical and commercial propositions across transmission-connected utility scale battery storage, utility solar, wind converter, and microgrid application segments, and which control platform approaches are demonstrating the most favorable combination of power system stability contribution, interoperability with grid-following resources, and compliance testability against emerging grid code requirements?

- What is the projected commercial development trajectory of the microgrid, remote community power, island grid, and military energy resilience segments for grid-forming inverter technology, and how are the distinct technical requirements of islanded and weak grid applications, including black-start capability, seamless transition between grid-connected and islanded modes, and multi-source load sharing, shaping product development priorities and competitive positioning among grid-forming inverter suppliers targeting distributed and off-grid market segments?

- How are international standards development bodies including IEC, IEEE, and CIGRE progressing toward the establishment of harmonized grid-forming performance specifications and type-testing protocols, and what is the projected timeline for national regulatory adoption of international grid-forming standards that would reduce the current market fragmentation created by divergent jurisdiction-specific requirements and enable inverter manufacturers to achieve greater economies of scale through standardized multi-market product platforms?

- Who are the leading grid-forming inverter hardware manufacturers, grid-forming control software developers, power system stability consultancy firms, and real-time simulation platform providers currently defining the competitive landscape of the global grid-forming inverter technologies market, and what are their respective control architecture intellectual property strategies, utility-scale project reference portfolios, grid code compliance certification roadmaps, and product development investment plans for advancing grid-forming capability across solar, wind, battery storage, and HVDC converter applications through the forecast horizon?

- Product Definition

- Scope of the Study

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Industry Publications, Power Electronics OEM Reports, Grid Operator Technical Standards & Press Releases

- Government Energy, Grid Stability & Power System Authority Data (IEA, NERC, ENTSO-E, AEMO, CEA, FERC, etc.)

- Grid-Forming Inverter Shipment, Deployment & Grid Code Compliance Statistics

- Utility, IPP & Grid Operator Procurement & Power System Planning Databases

- Primary Research Design & Execution

- In-depth Interviews with Grid-Forming Inverter Manufacturers, Grid Operator Technical Heads, Utility Engineers & Power System Consultants

- Surveys with Renewable Energy Project Developers, BESS Integrators, EPC Contractors & Transmission System Operators (TSOs)

- Expert Panel Validation

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Bottom-Up & Top-Down Reconciliation

- Renewable Energy Capacity Expansion, Grid Code Mandate & Technology Substitution-Driven Market Sizing Model

- Grid Stability Service Requirement & Inertia-Constrained Power System Penetration Rate Adjustment Framework

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Technology & Innovation Highlights

- Manufacturing Economics & Unit Economics Summary

- Average Plant CAPEX & OPEX Benchmarks

- Grid-Following vs Grid-Forming Inverter Margin & Profitability Analysis

- Virtual Synchronous Generator (VSG), Droop Control & Dispatchable Inertia Revenue Model Summary

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Geographic & Regional Trends

- Risk Assessment Framework

- Geopolitical & Energy Policy Risk (Grid Code Mandate Fragmentation, Permitting & Interconnection Delays)

- Raw Material & Component Price Volatility (Power Semiconductors, Magnetic Cores, Capacitors, Rare Earth Magnets) Risk

- Interoperability, Certification & Grid Code Compliance Risk Across Jurisdictions

- Cybersecurity & Grid Control System Vulnerability Risk

- Technology Transition Risk: Grid-Following Installed Base Replacement & Retrofit Economics

- Financial / Project Financing & Merchant Power Price Risk

- Competing Inertia & Grid Stability Technologies (Synchronous Condensers, STATCOM, Flywheels) Substitution Risk

- Regulatory Framework & Policy Standards

- Global Grid-Forming Inverter Technologies Market Economics

- Manufacturing Economics & Unit Economics Framework

- Capital Expenditure (CAPEX) Structure

- Operating Expenditure (OPEX) Structure

- Revenue Model & Monetisation Levers (Hardware Sales, Firmware Licensing, Ancillary Services, Software-as-a-Service)

- Capacity Utilisation & Throughput Economics

- Payback Period & Return on Investment (ROI) Analysis

- Total Cost of Ownership vs Grid-Following Inverters, Synchronous Condensers & STATCOM Solutions

- Raw Material & Component Input Cost Analysis

- Power Semiconductor (IGBT, SiC MOSFET, GaN) Cost Trends (USD/unit, 2021–2035)

- Magnetic Core, Transformer & Reactor Material Cost Dynamics

- Film & Electrolytic Capacitor & DC-Link Component Cost Structure

- Gate Driver, DSP / FPGA Control Board & Embedded Computing Cost Analysis

- Enclosure, Cooling System (Air, Liquid, Forced Convection) & Thermal Management Cost Structure

- Energy Storage Interface (DC Coupling, Battery Management System) Component Cost Economics

- Impact of Power Semiconductor Technology Transition (Si IGBT to SiC/GaN) on Inverter Product Economics

- Grid Services & Ancillary Market Economics

- Frequency Response & Synthetic Inertia Ancillary Service Revenue Benchmarks by Market

- Voltage Support, Reactive Power & Fast Frequency Response (FFR) Service Revenue Dynamics

- Black Start Capability & System Restoration Service Monetisation Economics

- Grid Service Stacking & Revenue Optimisation Framework for Grid-Forming Inverter Asset Owners

- Regulatory & Standards Compliance Economics

- Grid Code & Technical Connection Requirements Compliance Cost Benchmarks (IEEE 1547, IEC 62116, VDE-AR-N 4110, AS/NZS 4777, etc.)

- Type Testing, Certification & Factory Acceptance Test (FAT) Cost Structure

- Cybersecurity, NERC CIP & IEC 62351 Compliance Cost Structure

- Global Grid-Forming Inverter Technologies Market Outlook

- Market Size & Forecast by Value (USD Billion, 2021–2036)

- Market Size & Forecast by Installed Capacity (GW, 2021–2036)

- Market Size & Forecast by Control Architecture

- Virtual Synchronous Generator / Machine (VSG / VSM)

- Droop Control-Based Grid-Forming Inverters

- Power Synchronisation Control (PSC)

- Dispatchable Virtual Oscillator Control (dVOC)

- Matching Control & Oscillator-Based Architectures

- Hybrid Grid-Forming / Grid-Following Control

- Others (Model Predictive Control, AI-Enhanced Grid-Forming Algorithms)

- Market Size & Forecast by Power Rating

- Below 100 kW (Small-Scale & Distributed)

- 100 kW–1 MW (Commercial & Industrial)

- 1 MW–10 MW (Utility-Scale Small)

- 10 MW–100 MW (Utility-Scale Medium)

- Above 100 MW (Large Utility-Scale & Grid-Tied)

- Market Size & Forecast by Power Semiconductor Technology

- Silicon (Si) IGBT-Based Inverters

- Silicon Carbide (SiC) MOSFET-Based Inverters

- Gallium Nitride (GaN)-Based Inverters

- Hybrid Si/SiC Inverters

- Market Size & Forecast by Topology

- Two-Level Voltage Source Inverters (VSI)

- Three-Level Neutral-Point Clamped (NPC) Inverters

- Modular Multilevel Converters (MMC)

- Cascaded H-Bridge (CHB) Inverters

- Others (T-Type, Flying Capacitor, Z-Source)

- Market Size & Forecast by Grid Connection Type

- Transmission-Connected (HV & EHV Grid)

- Distribution-Connected (MV Grid)

- Low-Voltage (LV) / Microgrid-Connected

- Island / Off-Grid Systems

- Market Size & Forecast by Energy Source Integration

- Solar PV + Grid-Forming Inverter

- Battery Energy Storage System (BESS) + Grid-Forming Inverter

- Wind (Onshore & Offshore) + Grid-Forming Inverter

- Hybrid Renewable + BESS Grid-Forming Systems

- Green Hydrogen Electrolyser + Grid-Forming Inverter

- Others (Fuel Cell, Tidal, Wave, Pumped Hydro Interface)

- Market Size & Forecast by Grid Service Capability

- Synthetic Inertia & Frequency Response

- Voltage Regulation & Reactive Power Support

- Fast Frequency Response (FFR) & Primary Frequency Control

- Black Start & System Restoration

- Fault Ride-Through (FRT) & Short-Circuit Current Provision

- Power Oscillation Damping (POD)

- Multi-Service Stacking (Combined Grid Service Capability)

- Market Size & Forecast by Application

- Utility-Scale Solar PV Plants

- Onshore Wind Farms

- Offshore Wind Farms (Fixed-Bottom & Floating)

- Grid-Scale Battery Energy Storage Systems (BESS)

- Microgrids & Virtual Power Plants (VPPs)

- HVDC Converter Stations & Grid Interconnectors

- Industrial & Commercial Behind-the-Meter Systems

- EV Charging Infrastructure & Vehicle-to-Grid (V2G) Systems

- Others (Data Centre UPS, Island Grids, Remote Community Electrification)

- Market Size & Forecast by End-Use Sector

- Utilities & Transmission System Operators (TSOs)

- Global Integrated Utilities & IPPs (Enel, Iberdrola, Ørsted, EDF, National Grid, AES, etc.)

- Regional Distribution Network Operators (DNOs) & Power Utilities

- Renewable Energy Project Developers & IPPs

- Utility-Scale Solar, Wind & BESS Project Developers

- Hybrid Renewable Energy & Microgrid System Developers

- Industrial & Commercial End-Users

- Heavy Industry (Steel, Cement, Chemicals, Mining) with Captive Power & Grid Stability Needs

- Data Centres, Hyperscalers & Technology Companies with Power Quality Requirements

- Government & Public Sector Grid Infrastructure

- National Grid Operators, Ministry of Energy Bodies & Defence Power Infrastructure Authorities

- Rural Electrification & Off-Grid Island Power System Programmes

- Oil & Gas & Resource Sector

- Offshore Platform, LNG Terminal & Remote Mine Site Power System Operators

- Others (Rail Traction Networks, Port Electrification, EV Fleet Charging Hubs)

- Utilities & Transmission System Operators (TSOs)

- Market Size & Forecast by Sales Channel

- Direct OEM & Utility Framework Agreement Supply

- EPC Contractor & System Integrator Procurement

- Independent Distributors & Value-Added Resellers (VARs)

- Government & Regulated Utility Procurement Programmes

- Online & Digital B2B Procurement Platforms

- Asia-Pacific Grid-Forming Inverter Technologies Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Installed Capacity (GW)

- By Control Architecture

- By Power Rating

- By Power Semiconductor Technology

- By Topology

- By Grid Connection Type

- By Energy Source Integration

- By Grid Service Capability

- By Application

- By End-Use Sector

- By Sales Channel

- Key Demand Drivers (APAC-Specific)

- Competitive Landscape (APAC)

- Europe Grid-Forming Inverter Technologies Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Installed Capacity (GW)

- By Control Architecture

- By Power Rating

- By Power Semiconductor Technology

- By Topology

- By Grid Connection Type

- By Energy Source Integration

- By Grid Service Capability

- By Application

- By End-Use Sector

- By Sales Channel

- Key Demand Drivers (Europe-Specific)

- Competitive Landscape (Europe)

- North America Grid-Forming Inverter Technologies Market Outlook

- Market Overview & Strategic Importance

- Market Size & Forecast

- By Value (2020–2035)

- By Installed Capacity (GW)

- By Control Architecture

- By Power Rating

- By Power Semiconductor Technology

- By Topology

- By Grid Connection Type

- By Energy Source Integration

- By Grid Service Capability

- By Application

- By End-Use Sector

- By Sales Channel

- Key Demand Drivers (North America-Specific)

- Competitive Landscape (North America)

- Latin America Grid-Forming Inverter Technologies Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Installed Capacity (GW)

- By Control Architecture

- By Power Rating

- By Power Semiconductor Technology

- By Topology

- By Grid Connection Type

- By Energy Source Integration

- By Grid Service Capability

- By Application

- By End-Use Sector

- By Sales Channel

- Key Demand Drivers (LATAM-Specific)

- Competitive Landscape (LATAM)

- Middle East & Africa Grid-Forming Inverter Technologies Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Installed Capacity (GW)

- By Control Architecture

- By Power Rating

- By Power Semiconductor Technology

- By Topology

- By Grid Connection Type

- By Energy Source Integration

- By Grid Service Capability

- By Application

- By End-Use Sector

- By Sales Channel

- Key Demand Drivers (MEA-Specific)

- Competitive Landscape (MEA)

- Country-Wise Grid-Forming Inverter Technologies Market Outlook

- Market Size & Forecast by Country

- By Value

- By Installed Capacity (GW)

- By Control Architecture

- By Power Rating

- By Power Semiconductor Technology

- By Topology

- By Grid Connection Type

- By Energy Source Integration

- By Grid Service Capability

- By Application

- By End-Use Sector

- By Sales Channel

- Market Size & Forecast by Country

- Market Size & Forecast

- Market Size & Forecast

- Market Size & Forecast

- Market Size & Forecast

- Manufacturing Economics & Unit Economics Framework

Countries Covered: United States, Canada, Germany, United Kingdom, France, Spain, Italy, Netherlands, Australia, China, Japan, South Korea, India, Brazil, Chile, South Africa, Saudi Arabia, UAE, Denmark, Sweden

- Technology Landscape & Innovation Analysis

- Grid-Forming Inverter Technology Maturity Assessment

- Emerging & Disruptive Technologies in Grid-Forming Power Electronics

- Next-Generation Control Algorithms: AI/ML-Enhanced Virtual Synchronous Generator & Adaptive Droop Control

- Wide-Bandgap (SiC & GaN) Power Semiconductor Integration for High-Frequency, High-Efficiency Grid-Forming Inverters

- Modular Multilevel Converter (MMC) & Cascaded Topology Advances for Transmission-Scale Grid-Forming Applications

- Grid-Forming Inverter Co-ordination in 100% Inverter-Based Resource (IBR) Grids & Multi-Infeed Stability

- Hardware-in-the-Loop (HIL), Real-Time Digital Simulation (RTDS) & Digital Twin Testing Platforms for Grid-Forming Validation

- Technology Readiness & Commercialisation Matrix – Key Grid-Forming Inverter Technologies & Control Architectures

- Patent Landscape Analysis

- R&D Investment Benchmarking

- Value Chain & Supply Chain Analysis

- Grid-Forming Inverter Technologies Value Chain Mapping

- Supply Chain Concentration & Dependency Analysis

- Key Supplier Mapping by Component & Technology Programme

- Power Semiconductor (IGBT, SiC MOSFET, GaN) Wafer & Module Supplier Mapping

- Magnetic Core, Transformer & Passive Component Supplier Mapping

- DSP, FPGA & Embedded Control Board Supplier Mapping

- Enclosure, Cooling System & Thermal Management Component Supplier Mapping

- Supplier Risk Heat Map

- Make vs Buy Strategy Trends Among Grid-Forming Inverter Manufacturers & System Integrators

- Pricing Analysis

- Grid-Forming Inverter Pricing Dynamics & Mechanisms

- Pricing by Control Architecture, Power Rating, Topology & Power Semiconductor Technology

- Total Cost of Ownership (TCO) Analysis – Including Hardware, Firmware, Grid Services Revenue, O&M & Replacement Costs

- Grid-Forming vs Grid-Following Inverter Pricing Trends & Benchmarks

- Hardware Sale vs Firmware Licensing vs Ancillary Service Revenue Pricing & Value Proposition

- Sustainability & Environmental Stewardship

- Environmental & Sustainability Landscape in Grid-Forming Inverter Manufacturing & Grid Deployment

- Carbon Footprint & Energy Efficiency Benchmarking Across Inverter Topologies & Power Semiconductor Technologies

- Recycled & Sustainable Material Integration Roadmap for Power Electronics Manufacturers

- End-of-Life, Circular Economy & E-Waste Management Assessment for Grid-Forming Inverter Hardware

- Grid-Forming Inverters’ Role in Enabling High Renewable Penetration & Grid Decarbonisation Targets

- ESG Reporting & Lifecycle Assessment (LCA) in Grid-Forming Inverter Operations

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level: Global Power Electronics OEM Giants vs Specialist Inverter Startups & Research Spin-offs

- Top 5 Grid-Forming Inverter Manufacturers Market Revenue Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis by Control Architecture, Application & Region

- Competitive Intensity Map by Segment & Region

- Player Classification

- Tier-1 Global Power Electronics & Energy Management OEMs with Grid-Forming Product Lines (ABB, Siemens Energy, GE Vernova, Hitachi Energy, Schneider Electric, SMA, etc.)

- Tier-2 Specialist Grid-Forming Inverter Manufacturers, BESS Integrators & Renewable Energy Converter OEMs

- Emerging Grid-Forming Technology Startups, University Spin-offs & National Laboratory Commercialisation Ventures

- Emerging & Disruptive Players

- Competitive Analysis Frameworks

- Market Share Analysis by Control Architecture, Power Rating, Application & Geography

- R&D Intensity & Grid-Forming Control Algorithm Portfolio Benchmarking

- Utility Framework Agreement, Grid Code Certification Portfolio & Long-Term Supply Contract Comparison

- Geographic Revenue Exposure & Grid Code Compliance Footprint Comparison

- Company Profiles

- Company Overview, HQ & Organisational Structure

- Grid-Forming Inverter Products, Control Architecture & Grid Service Capability Portfolio

- Revenue Breakdown

- Key Utility, IPP & Grid Operator Supply Programmes & Project Deployments

- Manufacturing Footprint & Key Facilities

- Recent Developments (M&A, Partnerships, New Products, Grid Code Certifications, Financial Results)

- SWOT Analysis

- Strategic Focus: Control Algorithm Innovation, Grid Code Certification Expansion, SiC/GaN Integration & Utility Partnership Strategy

- Strategic Output

- Market Opportunity Matrix

- High-Value Opportunity Quadrant Analysis

- Addressable Market by Control Architecture, Application & Region

- Time-to-Revenue Assessment by Opportunity

- White Space Opportunity Analysis

- Underserved Application Segment, Grid Connection Type & End-Use Sector Gaps

- Geographic Markets with Low Grid-Forming Inverter Penetration & High IBR Growth

- Technology, Grid Service & Control Architecture Gaps with High Commercialisation Potential

- Customer Segment Unmet Needs

- Strategic Recommendations

- Product Portfolio & Control Algorithm Innovation Strategy

- Technology Platform & Power Semiconductor Roadmap Strategy

- Manufacturing Footprint & Capacity Expansion Strategy

- Grid Code Certification, Utility Framework Agreement & Channel Growth Strategy

- Pricing, Grid Services Monetisation & Commercial Strategy

- Sustainability & Regulatory Compliance Strategy

- Supply Chain & Component Sourcing Strategy

- Partnership, M&A & Expansion Strategy

- Regional Growth Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-Term (2025–2028)

- Mid-Term (2029–2032)

- Long-Term (2033–2036)

- Market Opportunity Matrix

- Market Structure & Concentration