Market Definition

Hydrogen fuel cell trucks are heavy-duty commercial vehicles that use a proton exchange membrane fuel cell (PEMFC) system to convert compressed hydrogen gas into electrical energy through an electrochemical reaction, powering one or more electric drive motors with water vapour as the only tailpipe emission. Unlike battery-electric trucks, which store energy in large onboard battery packs and require multi-hour grid-connected recharging, hydrogen fuel cell trucks are refuelled in minutes at dedicated hydrogen refuelling stations and can achieve ranges of 500–1,000+ kilometres per fill, performance characteristics that make them directly competitive with diesel for long-haul, heavy payload, and time-sensitive freight applications. The market spans a broad vehicle weight and application spectrum: light commercial and distribution trucks (Class 4–6, GVW 7–12 tonnes), heavy-duty regional haul trucks (Class 7–8, GVW 26–44 tonnes), and long-haul articulated tractor-trailers (Class 8 semi-trucks, GVW above 44 tonnes / gross combination weight up to 80+ tonnes). Key system components include the fuel cell stack (typically Toyota, Ballard, Hyundai, Bosch, or proprietary OEM designs), hydrogen storage tanks (Type III aluminium-lined or Type IV carbon-fibre composite), high-voltage battery buffer pack, power control electronics, electric axle or central drive motor, and hydrogen safety systems. The ecosystem required to operationalise these vehicles encompasses hydrogen production (green, blue, and grey), compression, storage, and high-pressure dispensing infrastructure at strategic depot and public refuelling locations.

Market Insights

The most defining strategic shift reshaping the global hydrogen fuel cell truck market in 2026 is the decisive pivot from government-funded demonstration fleets to commercially contracted customer deployments, a transition that is simultaneously validating the technology’s operational performance and exposing the structural economics that will ultimately determine which OEM platforms and hydrogen supply models are viable at scale. Nikola, once the dominant public narrative around hydrogen trucking, has undergone fundamental restructuring following the collapse of its original business model, yet its operational Class 8 FCEV fleet continues to expand in North America under revised commercial terms. More strategically significant is the quiet but accelerating progress of incumbents: Daimler Truck’s HECTOR joint venture with Volvo (now branded cellcentric) has commenced customer trials of its GenH2 Truck in Europe, achieving verified ranges exceeding 1,000 km on a single fill; Hyundai’s XCIENT Fuel Cell has surpassed 10 million kilometres of cumulative commercial operation across Switzerland, Germany, South Korea, and the United States; and Toyota’s Class 8 FCEV semi-truck development programme, conducted in partnership with Kenworth, is generating fleet performance data from real-world port and logistics drayage operations in California. These concurrent programmes are generating a body of empirical evidence on fuel cell durability, hydrogen consumption rates, total cost of ownership, and driver acceptance that is materially shifting the risk perception of fleet operators who had previously adopted a wait-and-see posture toward the technology.

Geographically, the competitive landscape for hydrogen fuel cell trucks is developing on three distinct trajectories that reflect fundamentally different policy frameworks, hydrogen supply economics, and market structures. In Europe, the FuelCells2Drive programme, the Alternative Fuels Infrastructure Regulation (AFIR) mandating hydrogen refuelling at major TEN-T corridor nodes by 2030, and the European Hydrogen Bank’s first auction results, which delivered green hydrogen at €0.48–0.55/kg subsidised cost, are establishing the policy scaffolding for large-scale fleet deployment. However, the critical enabler remains not the trucks themselves but the 500+ bar high-capacity refuelling stations capable of serving Class 8 vehicles, of which fewer than 50 exist globally as of early 2026. In Asia, China and South Korea represent the two most advanced markets. China’s city-cluster subsidy model, under which hydrogen vehicle consortia in clusters such as Guangdong-Hong Kong-Macao, Wuhan, and Shanghai receive production and deployment subsidies calibrated to achieve 50,000 hydrogen commercial vehicles by 2025 and 500,000 by 2035, has created the world’s largest hydrogen truck installed base but also significant questions about long-term commercial sustainability beyond the subsidy window. South Korea, anchored by Hyundai’s vertically integrated strategy, is on a more commercially disciplined but slower trajectory, with hydrogen truck deployments in logistics, waste collection, and construction sectors supported by the government’s Hydrogen Economy Roadmap. In North America, California’s Advanced Clean Trucks rule and the Inflation Reduction Act’s USD 3/kg Clean Hydrogen Production Tax Credit (45V) are creating the strongest convergence of demand-side mandate and supply-side economics globally, positioning the US West Coast as the most likely location for the first commercially self-sustaining hydrogen truck ecosystem outside of subsidised city-cluster models.

The primary structural driver of long-run market growth is the inescapable physics and logistics of heavy freight decarbonisation. Battery-electric trucks, which have achieved significant traction in urban distribution and regional delivery applications up to approximately 300–400 km range with moderate payloads, face fundamental limitations in long-haul applications: a Class 8 battery-electric truck requires a battery pack of 600–800 kWh to achieve 500 km range at full payload, adding 5–7 tonnes to gross vehicle weight, reducing payload capacity by a corresponding amount, and requiring 1–2 hours of opportunity charging or a megawatt-scale charging infrastructure investment at every depot and terminal. For freight operators running multi-shift long-haul routes, particularly in temperature-controlled logistics, bulk construction materials, chemicals, and port-to-distribution-centre drayage, the total cost of ownership calculus firmly favours hydrogen when green hydrogen can be produced and dispensed at USD 6–8/kg delivered at the nozzle, a threshold that the IRA 45V credit and anticipated electrolyser cost reductions are projected to reach in mature markets by 2028–2030. This structural advantage is creating a bifurcated commercial vehicle decarbonisation roadmap in which battery-electric dominates urban and suburban routes while hydrogen fuel cells capture medium and long-haul operations, a segmentation that leading truck OEMs including Daimler, Volvo, Kenworth, IVECO, and Hyundai are now explicitly building their product strategies around.

Key Drivers

- The foundational demand accelerator for hydrogen fuel cell trucks in 2026 and beyond is the compounding pressure of fleet decarbonisation mandates, carbon pricing mechanisms, and corporate Scope 3 emissions commitments that are collectively transforming hydrogen trucks from an aspirational sustainability option into a procurement necessity for large freight operators. In the European Union, the CO₂ emission standards for heavy-duty vehicles regulation mandates a 45% reduction in new truck CO₂ emissions by 2030, 65% by 2035, and 90% by 2040 versus 2019 baseline levels, thresholds that effectively require large-scale zero-emission vehicle deployment and that hydrogen fuel cell trucks are uniquely positioned to satisfy in long-haul applications where battery-electric performance is insufficient. The EU Emissions Trading System (ETS) extension to road transport from 2027 will introduce a carbon price signal that directly penalises diesel truck operating costs, improving the total cost of ownership position of zero-emission alternatives by an estimated USD 0.05–0.12 per kilometre depending on carbon price trajectory. In North America, California’s Advanced Clean Trucks regulation mandates that truck manufacturers sell increasing percentages of zero-emission vehicles, with Class 7–8 trucks reaching 40% ZEV sales share by 2035 and 75% by 2040. Simultaneously, corporate sustainability commitments from shipper customers, Amazon, DHL, DB Schenker, Maersk, and Walmart having collectively announced hydrogen truck procurement programmes totalling over 30,000 units through 2030, are creating the contractual offtake visibility required for both OEM production investment and hydrogen infrastructure financing decisions. This demand-mandate convergence is the single most important structural change in the market’s commercial risk profile compared to the 2019–2021 period of demonstration-scale deployments.

- A transformative parallel driver is the rapid improvement in green hydrogen economics driven by electrolyser cost deflation, scaling manufacturing capacity, and the IRA 45V production tax credit in the United States, which together are compressing the gap between green hydrogen production costs and the USD 6–8/kg dispensed cost threshold required for commercial FCEV truck total cost of ownership parity with diesel. Electrolyser capital costs have fallen from approximately USD 1,200–1,500/kW in 2020 to USD 500–800/kW in 2025 for alkaline and PEM systems in volume configurations, with leading manufacturers including Nel Hydrogen, ITM Power, Cummins, and Plug Power projecting further reductions to USD 200–300/kW by 2030 as gigawatt-scale manufacturing facilities come online. The IRA 45V credit provides up to USD 3/kg for green hydrogen produced with lifecycle emissions below 0.45 kg CO₂e per kg H₂, a level achievable with electrolysers powered by additionality-compliant renewable electricity, effectively halving the production cost of qualifying green hydrogen projects in the United States. The combination of electrolyser deflation, low-cost solar and wind power purchase agreements in key production regions, and 45V credits positions US green hydrogen production at USD 1.50–2.50/kg by 2028–2030, and when combined with compression, storage, and dispensing costs of USD 3–4/kg, total delivered costs at the nozzle of USD 5–6/kg become achievable at scale. At this price level, hydrogen fuel cell trucks operating 150,000+ km annually achieve total cost of ownership parity with diesel, without factoring in escalating carbon price penalties on diesel operations, fundamentally shifting the technology from a premium sustainability purchase to an economically rational fleet investment decision for high-utilisation long-haul operators.

- The third critical driver is the accelerating maturation of the hydrogen fuel cell truck technology itself, measured not by press releases but by the hard operational data accumulating from commercial fleets in Switzerland, South Korea, California, and Germany that is demonstrating fuel cell stack durability, hydrogen consumption efficiency, and driver acceptance at levels that meet or exceed the performance requirements of commercial freight operations. Hyundai’s XCIENT Fuel Cell data from Swiss operations, the world’s largest commercial hydrogen truck fleet with over 1,000 units deployed, shows average fuel cell stack lifetimes exceeding 20,000 operating hours in commercial service, hydrogen consumption of approximately 8–9 kg per 100 km at full load on alpine routes, and roadside assistance rates comparable to equivalent diesel trucks after the first 18 months of operation, directly refuting the durability concerns that had historically been cited as the primary technical barrier to large-scale fleet adoption. Toyota’s FCEV Class 8 programme at the Port of Los Angeles has demonstrated over 1 million cumulative miles of operation with availability rates exceeding 95%, providing the OEM-agnostic performance validation that large freight customers require before committing to multi-year fleet procurement contracts. The rapid improvement in fuel cell stack power density, from approximately 80 kW/litre in 2020 to over 130 kW/litre in 2025 for heavy-duty automotive-grade stacks, is enabling more compact system packaging, higher continuous power output, and better cold-start performance in sub-zero conditions, expanding the operational geography and application range of hydrogen trucks into markets and seasons that were previously problematic.

Key Challenges

- The most acute structural challenge constraining the global hydrogen fuel cell truck market is the profound chicken-and-egg problem of hydrogen refuelling infrastructure: fleet operators will not commit to large hydrogen truck deployments without certainty of reliable, accessible, and cost-competitive refuelling coverage across their operating routes, while hydrogen infrastructure investors and developers will not finance the capital-intensive construction of high-capacity truck refuelling stations, each requiring USD 5–15 million in capital expenditure for a 1,000 kg/day heavy-duty dispensing facility, without binding offtake commitments from fleet operators. This coordination failure is the single most cited reason why commercially justified hydrogen truck projects fail to reach financial close. The infrastructure gap is particularly acute for long-haul freight applications, which require refuelling stations spaced at maximum 400–600 km intervals along major freight corridors, at strategic logistics hubs, and at depot locations capable of overnight high-capacity refuelling for returning fleets. As of early 2026, the global inventory of heavy-duty hydrogen refuelling stations capable of dispensing at 700 bar to Class 8 vehicles and servicing multiple trucks per day stands at fewer than 120 stations, a coverage network that is entirely inadequate for commercial long-haul operations outside of the California Bay Area-to-LA corridor, select Swiss motorway stations, and isolated depot-to-depot routes in South Korea and Japan. The capital required to build the refuelling network needed to support the EU’s 2030 ACT mandate targets alone is estimated at EUR 12–18 billion, requiring a combination of public grant funding, public-private partnership models, and energy company infrastructure investment at a pace and scale that has not yet been demonstrated by any existing programme.

- A compounding economic challenge is the current truck-level cost premium of hydrogen fuel cell powertrains relative to both diesel and battery-electric alternatives, which creates a financing gap that fleet operators, particularly small and medium-sized haulage companies operating on thin margins in competitive spot freight markets, are unable to bridge without substantial capital subsidy or favourable green financing terms. A hydrogen fuel cell Class 8 tractor currently commands a purchase price of approximately USD 350,000–500,000 depending on system configuration and volume, versus USD 150,000–200,000 for an equivalent diesel tractor and USD 300,000–400,000 for a battery-electric alternative with comparable range. The primary cost drivers of the FCEV premium are the fuel cell stack (approximately USD 80,000–120,000 at current production volumes, dominated by platinum group metal catalyst costs and the relatively small-scale manufacturing of automotive-grade stacks), the Type IV high-pressure hydrogen storage system (USD 40,000–8,0000 for multiple 700-bar tanks with sufficient capacity for long-haul operations), and the power control electronics. Fuel cell stack cost trajectories modelled by the US Department of Energy project costs falling to USD 80/kW by 2030 at volume production of 500,000 units per year, implying a 200 kW stack at approximately USD 16,000, but achieving these cost targets requires the simultaneous scaling of vehicle production and platinum reduction or replacement in catalyst design, both of which are dependent on market growth that has not yet materialised. Until truck acquisition costs are within approximately 20–30% of diesel equivalents, the premium threshold at which lower fuel costs over a 1–1.5 million km vehicle lifetime can offset the capital differential in operator business cases, the market will remain dependent on policy incentives including direct purchase subsidies, favourable tax treatment, green financing facilities, and carbon credit revenues to achieve the fleet deployment scale needed to bring costs down the experience curve.

Market Segmentation

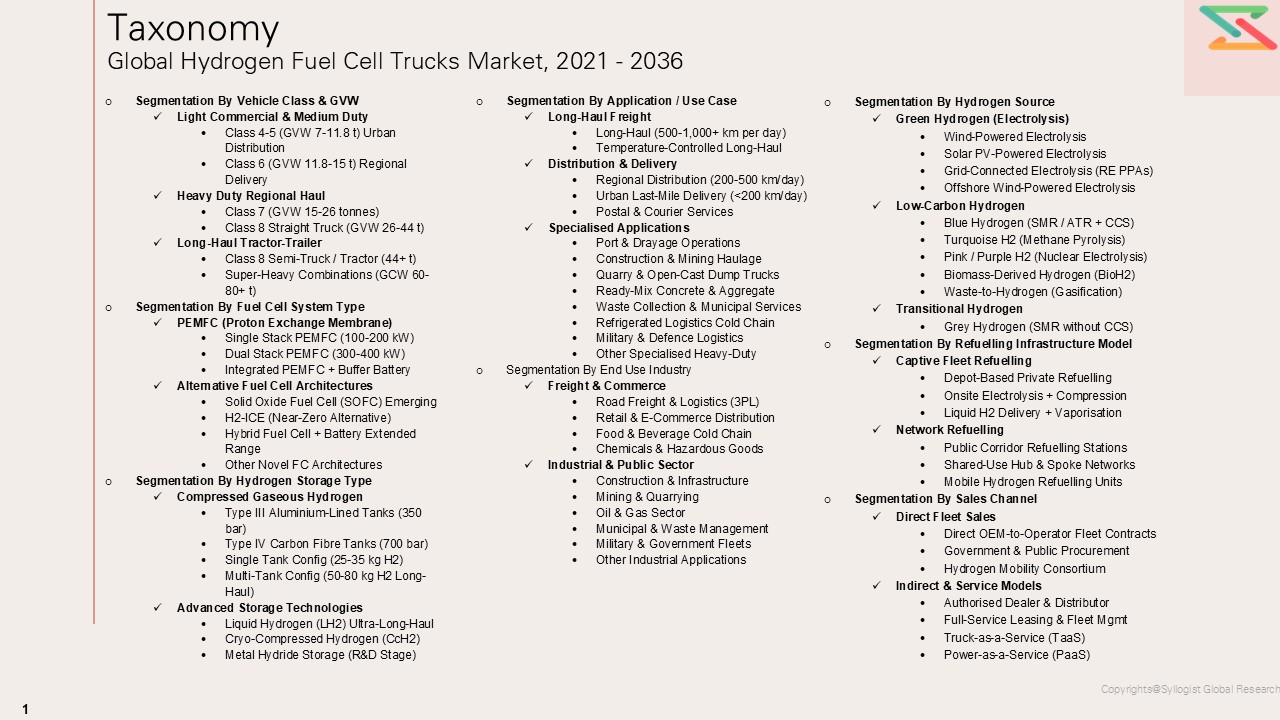

- Segmentation by Vehicle Class & GVW

- Light Commercial & Medium Duty

- Class 4–5 (GVW 7–11.8 tonnes)

- Class 6 (GVW 11.8–15 tonnes)

- Heavy Duty Regional Haul

- Class 7 (GVW 15–26 tonnes)

- Class 8 Straight Truck (GVW 26–44 tonnes)

- Long-Haul Tractor-Trailer

- Class 8 Semi-Truck / Tractor (GVW 44+ tonnes)

- Super-Heavy Combinations (GCW 60–80+ tonnes)

- Segmentation by Fuel Cell System Type

- Proton Exchange Membrane Fuel Cell (PEMFC)

- Single Stack PEMFC (150–200 kW)

- Dual Stack PEMFC (300–400 kW)

- Integrated PEMFC + Buffer Battery System

- Solid Oxide Fuel Cell (SOFC)

- Hydrogen Internal Combustion Engine (H2-ICE)

- Hybrid Fuel Cell + Battery (Extended Range)

- Proton Exchange Membrane Fuel Cell (PEMFC)

- Segmentation by Hydrogen Storage Type

- Type III Aluminium-Lined Composite Tanks (350 bar)

- Type IV Carbon Fibre Composite Tanks (700 bar)

- Single Tank Configuration (25–35 kg H₂)

- Multi-Tank Configuration (50–80 kg H₂ for Long-Haul)

- Liquid Hydrogen (LH₂) Storage

- Metal Hydride Storage

- Segmentation by Application / Use Case

- Long-Haul Freight (500–1,000+ km per day)

- Regional Distribution (200–500 km per day)

- Urban Last-Mile Delivery (< 200 km per day)

- Port & Drayage Operations

- Construction & Mining Haulage

- Quarry & Open-Cast Mining Dump Trucks

- Ready-Mix Concrete & Aggregate Delivery

- Temperature-Controlled / Refrigerated Logistics

- Waste Collection & Municipal Services

- Military & Defence Logistics

- Other Specialised Heavy-Duty Applications

- Segmentation by End Use Industry

- Road Freight & Logistics (3PL / Contract Logistics)

- Retail & E-Commerce Distribution

- Food & Beverage Cold Chain

- Chemicals & Hazardous Goods Transport

- Construction & Infrastructure

- Mining & Quarrying

- Oil & Gas Sector

- Municipal & Waste Management

- Postal & Courier Services

- Military & Government Fleets

- Segmentation by Hydrogen Source (Fuel Supply)

- Green Hydrogen (Electrolysis from Renewable Energy)

- Wind-Powered Electrolysis

- Solar PV-Powered Electrolysis

- Grid-Connected Electrolysis (Renewable PPAs)

- Blue Hydrogen (SMR / ATR + Carbon Capture & Storage)

- Turquoise Hydrogen (Methane Pyrolysis)

- Grey Hydrogen (SMR without CCS)

- Pink / Purple Hydrogen (Nuclear-Powered Electrolysis)

- Biomass-Derived Hydrogen

- Green Hydrogen (Electrolysis from Renewable Energy)

- Segmentation by Refuelling Infrastructure Model

- Depot-Based Private Refuelling (Fleet-Owned / Captive)

- Public Corridor Refuelling Stations

- Shared-Use Hub & Spoke Refuelling Networks

- Mobile Hydrogen Refuelling Units (Temporary / Remote)

- Liquid H₂ Delivery + On-Site Vaporisation

- Segmentation by Sales Channel

- Direct OEM Sales (Fleet Contracts)

- Authorised Dealer & Distributor Network

- Leasing & Full-Service Fleet Management

- Power-as-a-Service / Truck-as-a-Service (TaaS)

- Government & Public Procurement

- Hydrogen Mobility Consortium & Alliance Procurement

- Light Commercial & Medium Duty

All market revenues are presented in USD; volume in units (number of trucks) and installed fuel cell system capacity (MW)

Historical Year: 2021–2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027–2036

Key Questions this Study Will Answer

- What are the critical market metrics and forward-looking projections for the Global Hydrogen Fuel Cell Trucks Market, including total revenue, unit volume (number of trucks sold), installed fuel cell system capacity (MW), average selling price by vehicle class, and total cost of ownership benchmarking, segmented across Vehicle Class & GVW (Class 4–6 medium duty, Class 7–8 heavy duty, Class 8 long-haul tractor), Fuel Cell System Type (PEMFC single stack, dual stack, integrated PEMFC + buffer battery, H2-ICE), Hydrogen Storage Configuration (Type III 350 bar, Type IV 700 bar single and multi-tank, liquid H₂), Application / Use Case (long-haul freight, regional distribution, urban delivery, port drayage, construction, refrigerated logistics), End Use Industry, Hydrogen Source (green, blue, turquoise, grey), Refuelling Model, and Sales Channel?

- How do supply–demand fundamentals and total cost of ownership economics vary across key regions and major freight market segments, and what role do zero-emission vehicle mandates (EU CO₂ standards, California ACT rule, South Korea ZEV targets), carbon pricing mechanisms (EU ETS road transport extension, UK carbon tax, California LCFS credits), hydrogen production subsidies (IRA 45V, EU Hydrogen Bank, Korean H2 Economy Roadmap grants), refuelling infrastructure development programmes (EU AFIR mandates, US DOE H2@Scale hubs, Chinese city-cluster subsidies), and fleet operator procurement commitments from shippers (Amazon, DHL, DB Schenker, Walmart) play in shaping regional deployment velocity, technology adoption sequencing, and the competitive positions of domestic versus imported fuel cell truck platforms?

- In what ways are hydrogen supply cost and refuelling infrastructure constraints, covering green hydrogen production costs ($/kg at the electrolyser gate), compression, storage and dispensing costs ($/kg added), station capital expenditure (USD/station for 350 kg/day versus 1,000 kg/day Class 8-capable facilities), hydrogen delivery logistics (tube trailer versus liquid tanker versus pipeline), and the hydrogen price premium embedded in current commercial fleet contracts relative to long-run equilibrium costs, influencing fleet operator procurement decisions, OEM market entry timing, infrastructure developer investment commitments, and the pace at which hydrogen fuel cell trucks can achieve total cost of ownership parity with diesel and battery-electric alternatives in specific route and payload configurations?

- Who are the leading global hydrogen fuel cell truck OEMs, fuel cell system suppliers, hydrogen storage component manufacturers, refuelling infrastructure developers, and fleet operator early adopters, and how do they benchmark across key performance dimensions including fuel cell stack power output (kW), system gravimetric and volumetric power density, hydrogen consumption efficiency (kg H₂/100 km at rated GVW), demonstrated stack durability (operating hours to end of life), cold-start capability (minimum ambient temperature), vehicle range per fill (km at full payload), refuelling time (minutes to full tank), acquisition price premium versus diesel baseline (%), total cost of ownership at USD 6/kg and USD 8/kg dispensed hydrogen, warranty terms, service network coverage, and technology development roadmap toward next-generation stack platforms and solid-state hydrogen storage?

- What strategic insights emerge from primary discussions with fleet operators (long-haul carriers, logistics 3PLs, municipal fleet managers), truck OEMs (Daimler Truck, Volvo, Hyundai, Toyota, IVECO, Kenworth, Nikola), fuel cell system suppliers (Ballard, Bosch, cellcentric, Horizon, SinoHytec), hydrogen producers (Air Liquide, Linde, Shell Hydrogen, Plug Power, NEL), refuelling infrastructure developers (FirstElement Fuel, H2 Green Steel, TotalEnergies), and public procurement agencies regarding fleet operators’ actual willingness to pay for hydrogen trucks absent subsidy, the minimum refuelling network density required to trigger large-scale fleet commitment, the critical role of fuel supply price guarantees and long-term green hydrogen offtake contracts in de-risking fleet investment decisions, the competitive threat from battery-electric trucks in specific freight segments, the practical barriers to depot-based captive hydrogen refuelling for small and mid-sized fleets, and the key policy levers that would most accelerate commercial deployment at scale beyond current demonstration programmes?

- Market Overview

- Product Overview

- Research Methodology

- Executive Summary

- Market Dynamics

- Market Dynamics (Drivers, Restraints, Opportunities, Challenges, Porter’s Five Forces Analysis, PESTLE Analysis)

- Market Trends & Developments

- Risk Assessment Framework

- Political / Geopolitical Risk

- Hydrogen Supply Chain & Infrastructure Risk

- Technology Maturity & Scale-Up Risk

- Financial / Market & Total Cost of Ownership Risk

- Regulatory Framework & Standards

- Global Regulatory Overview

- Key Regulations by Region

- EU: CO₂ Emission Standards for Heavy-Duty Vehicles, AFIR Mandate, EU Hydrogen Strategy

- EU: Clean Vehicle Directive, TEN-T Corridor H2 Refuelling Requirements

- USA: California Advanced Clean Trucks (ACT) Rule, CARB ZEV Mandate, IRA 45V Tax Credit

- USA: US DOE H2@Scale Programme, Buy America Provisions

- South Korea: Hydrogen Economy Roadmap, FCEV Commercialisation Strategy

- China: National Hydrogen Energy Development Plan, City-Cluster Subsidy Model

- Japan: Green Growth Strategy, Hydrogen Society Promotion Act

- UK: Zero Emission HGV & Infrastructure Demonstrator Programme

- Vehicle Safety, Type-Approval & Homologation Standards

- UN GTR No. 13 (Hydrogen & Fuel Cell Vehicles)

- EU Regulation 2021/535 (FCEV Type Approval)

- SAE J2719 (Hydrogen Fuel Quality for FCEV)

- ISO 14687 (Hydrogen Fuel: Product Specification)

- ECE R134 (Hydrogen Fuel Cell Vehicles: UNECE)

- Hydrogen Infrastructure Standards & Codes

- SAE J2601 (Fuelling Protocols for Gaseous Hydrogen)

- ISO 19880 (Gaseous Hydrogen Fuelling Stations)

- NFPA 2 (Hydrogen Technologies Code)

- EU Pressure Equipment Directive (PED) for H2 Storage

- Emission & Environmental Standards

- Euro VII (Zero-Emission HDV Pathway)

- EPA Greenhouse Gas Phase 2 & Phase 3 Standards

- California LCFS (Low Carbon Fuel Standard) Credits

- Sustainability & ESG Compliance

- Scope 3 Well-to-Wheel Emissions Accounting for Hydrogen Trucks

- Green Hydrogen Certification (CertifHy, RFNBO under EU RED III)

- Science Based Targets Initiative (SBTi) — Transport Sector

- Corporate Sustainability Reporting Directive (CSRD) Fleet Disclosures

- Regulatory Impact on Market — Opportunities & Threats

- Global Hydrogen Fuel Cell Trucks Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Units)

- Market Size & Forecast by Vehicle Class & GVW

- Light Commercial & Medium Duty

- Class 4–5 (GVW 7–11.8 tonnes)

- Class 6 (GVW 11.8–15 tonnes)

- Heavy Duty Regional Haul

- Class 7 (GVW 15–26 tonnes)

- Class 8 Straight Truck (GVW 26–44 tonnes)

- Long-Haul Tractor-Trailer

- Class 8 Semi-Truck / Tractor (GVW 44+ tonnes)

- Super-Heavy Combinations (GCW 60–80+ tonnes)

- Light Commercial & Medium Duty

- Market Size & Forecast by Fuel Cell System Type

- Proton Exchange Membrane Fuel Cell (PEMFC)

- Single Stack PEMFC (100–200 kW)

- Dual Stack PEMFC (300–400 kW)

- Integrated PEMFC + Buffer Battery System

- Solid Oxide Fuel Cell (SOFC)

- Hydrogen Internal Combustion Engine (H2-ICE)

- Hybrid Fuel Cell + Battery

- Other / Novel Fuel Cell Architectures

- Proton Exchange Membrane Fuel Cell (PEMFC)

- Market Size & Forecast by Fuel Cell Stack Supplier

- Ballard Power Systems

- Bosch / Robert Bosch GmbH

- cellcentric (Daimler Truck + Volvo JV)

- Hyundai Motor Company (Proprietary Stack)

- Toyota Motor Corporation (Proprietary Stack)

- SinoHytec (Sinohytec)

- Horizon Fuel Cell Technologies

- Cummins Fuel Cell & Hydrogen Technologies

- Plug Power

- Other Fuel Cell Stack Suppliers

- Market Size & Forecast by Hydrogen Storage Type

- Type III Aluminium-Lined Composite Tanks (350 bar)

- Type IV Carbon Fibre Composite Tanks (700 bar)

- Single Tank Configuration (25–35 kg H₂)

- Multi-Tank Configuration (50–80 kg H₂ for Long-Haul)

- Liquid Hydrogen (LH₂) Storage

- Metal Hydride Storage

- Cryo-Compressed Hydrogen (CcH₂)

- Market Size & Forecast by Application / Use Case

- Long-Haul Freight (500–1,000+ km per day)

- Regional Distribution (200–500 km per day)

- Urban Last-Mile Delivery (< 200 km per day)

- Port & Drayage Operations

- Construction & Mining Haulage

- Quarry & Open-Cast Mining Dump Trucks

- Ready-Mix Concrete & Aggregate Delivery

- Heavy Equipment Haulage

- Temperature-Controlled / Refrigerated Logistics

- Waste Collection & Municipal Services

- Military & Defence Logistics

- Other Specialised Heavy-Duty Applications

- Market Size & Forecast by End Use Industry

- Road Freight & Logistics (3PL / Contract Logistics)

- Retail & E-Commerce Distribution

- Express Parcel & Last-Mile Delivery

- Ambient & Ambient-Temperature Freight

- Food & Beverage Cold Chain

- Chemicals & Hazardous Goods Transport

- Construction & Infrastructure

- Mining & Quarrying

- Oil & Gas Sector

- Municipal & Waste Management

- Postal & Courier Services

- Military & Government Fleets

- Other Industrial Applications

- Market Size & Forecast by Hydrogen Source

- Green Hydrogen (Electrolysis from Renewable Energy)

- Wind-Powered Electrolysis

- Solar PV-Powered Electrolysis

- Grid-Connected Electrolysis (Renewable PPAs)

- Offshore Wind-Powered Electrolysis

- Blue Hydrogen (SMR / ATR + Carbon Capture & Storage)

- Turquoise Hydrogen (Methane Pyrolysis)

- Grey Hydrogen (SMR without CCS)

- Pink / Purple Hydrogen (Nuclear-Powered Electrolysis)

- Biomass-Derived Hydrogen (BioH₂)

- Waste-to-Hydrogen (Gasification / Pyrolysis of Waste)

- Green Hydrogen (Electrolysis from Renewable Energy)

- Market Size & Forecast by Refuelling Infrastructure Model

- Depot-Based Private Refuelling (Fleet-Owned / Captive)

- Public Corridor Refuelling Stations

- Shared-Use Hub & Spoke Refuelling Networks

- Mobile Hydrogen Refuelling Units

- Liquid H₂ Delivery + On-Site Vaporisation

- Market Size & Forecast by Sales Channel

- Direct OEM Sales (Fleet Contracts)

- Authorised Dealer & Distributor Network

- Leasing & Full-Service Fleet Management

- Truck-as-a-Service (TaaS) / Power-as-a-Service

- Government & Public Procurement

- Hydrogen Mobility Consortium Procurement

- Market Size & Forecast by Region

- North America

- Europe

- Asia-Pacific

- Middle East & Africa

- Latin America

- Asia-Pacific Hydrogen Fuel Cell Trucks Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By Vehicle Class & GVW

- By Fuel Cell System Type

- By Hydrogen Storage Type

- By Application / Use Case

- By End Use Industry

- By Hydrogen Source

- By Refuelling Infrastructure Model

- By Sales Channel

- Market Size & Forecast

- Europe Hydrogen Fuel Cell Trucks Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By Vehicle Class & GVW

- By Fuel Cell System Type

- By Hydrogen Storage Type

- By Application / Use Case

- By End Use Industry

- By Hydrogen Source

- By Refuelling Infrastructure Model

- By Sales Channel

- Market Size & Forecast

- North America Hydrogen Fuel Cell Trucks Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By Vehicle Class & GVW

- By Fuel Cell System Type

- By Hydrogen Storage Type

- By Application / Use Case

- By End Use Industry

- By Hydrogen Source

- By Refuelling Infrastructure Model

- By Sales Channel

- Market Size & Forecast

- Latin America Hydrogen Fuel Cell Trucks Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By Vehicle Class & GVW

- By Fuel Cell System Type

- By Hydrogen Storage Type

- By Application / Use Case

- By End Use Industry

- By Hydrogen Source

- By Refuelling Infrastructure Model

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Hydrogen Fuel Cell Trucks Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By Vehicle Class & GVW

- By Fuel Cell System Type

- By Hydrogen Storage Type

- By Application / Use Case

- By End Use Industry

- By Hydrogen Source

- By Refuelling Infrastructure Model

- By Sales Channel

- Market Size & Forecast

- Country Wise* Hydrogen Fuel Cell Trucks Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By Vehicle Class & GVW

- By Fuel Cell System Type

- By Hydrogen Storage Type

- By Application / Use Case

- By End Use Industry

- By Hydrogen Source

- By Refuelling Infrastructure Model

- By Sales Channel

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, China, South Korea, Germany, Japan, France, United Kingdom, Netherlands, Norway, Switzerland, Canada, Australia, India, Brazil, Saudi Arabia, UAE, Sweden, Denmark, Belgium, Austria, Italy, Spain, Poland, Singapore, Malaysia, Thailand, South Africa, New Zealand, Portugal, Czech Republic

- Technology Analysis

- Conventional Diesel vs Battery-Electric vs Hydrogen Fuel Cell: TCO Comparison

- Total Cost of Ownership at USD 6/kg, USD 8/kg, and USD 10/kg Dispensed H₂

- Payback Period Analysis by Annual Mileage & Payload Profile

- Well-to-Wheel Carbon Intensity by Hydrogen Pathway & Energy Source

- Fuel Cell System Technology Deep-Dives

- PEMFC Stack Architecture

- Dual-Stack PEMFC Configurations for Class 8 Long-Haul

- Fuel Cell System Integration with High-Voltage Buffer Battery

- Air Management: Compressor Design, Humidification, Thermal Management

- Hydrogen Recirculation & Purge System Design

- Power Electronics: DC/DC Converters, Inverters, Power Control Units

- H2-ICE Technology: Port Injection vs Direct Injection, NOx Management

- SOFC for Heavy-Duty Trucks: Technology Readiness & Commercial Outlook

- Hydrogen Storage Technology

- Type IV Carbon Fibre Composite Tank Design & Manufacturing

- 700 Bar vs 350 Bar Storage Trade-Offs for Long-Haul

- Liquid Hydrogen (LH₂) Onboard Storage: Boil-Off Management, Refuelling

- Cryo-Compressed Hydrogen (CcH₂): Technical Status & Outlook

- Tank Cost Trajectory: Carbon Fibre & Manufacturing Learning Curves

- Electric Drivetrain & Vehicle Integration

- Central vs Distributed Electric Drive Architectures

- eAxle Integration for Fuel Cell Trucks

- Regenerative Braking & Energy Recovery

- Thermal Management System Design for Fuel Cell + Battery Systems

- Technology Readiness Levels (TRL) by System Component

- Emerging Technologies & Innovation Pipeline

- Platinum Group Metal (PGM) Reduction & Non-PGM Catalysts

- High-Temperature PEM Fuel Cells for Waste Heat Recovery

- Solid-State Hydrogen Storage (Metal Hydrides, Chemical Hydrides)

- AI-Based Fuel Cell Degradation Monitoring & Predictive Maintenance

- Digital Twin Applications for Fleet Fuel Consumption Optimisation

- Vehicle-to-Grid (V2G) Integration for Fuel Cell Trucks

- Autonomous Driving Integration with Fuel Cell Powertrain

- Conventional Diesel vs Battery-Electric vs Hydrogen Fuel Cell: TCO Comparison

- Hydrogen Supply Chain & Refuelling Infrastructure Analysis

- Hydrogen Production: Technology & Cost Benchmarking

- Alkaline Electrolysis: CAPEX, OPEX, Efficiency, Scale

- PEM Electrolysis: Cost per kW, Turndown Ratio, Stack Life

- SOEC (Solid Oxide) Electrolysis — Emerging High-Efficiency Option

- Steam Methane Reforming (SMR) + CCS: Blue H₂ Economics

- Methane Pyrolysis: Turquoise H₂, Carbon Black Co-Product

- Levelised Cost of Hydrogen (LCOH) by Technology & Region ($/kg)

- Hydrogen Compression, Storage & Distribution

- Pipeline vs Tube Trailer vs Liquid Tanker Delivery Logistics

- Compression Cost per kg at 200, 500, and 900 Bar

- Liquid Hydrogen Production, Liquefaction Cost & Boil-Off

- Onsite vs Offsite Hydrogen Production for Depot Refuelling

- Hydrogen Refuelling Station (HRS) Analysis

- Station CAPEX Benchmarking: 350 kg/day vs 1,000 kg/day HRS

- 700 Bar Class 8 Truck Dispensing Protocols & Equipment

- Station Utilisation Rate & Break-Even Economics

- Corridor HRS vs Depot HRS: Siting Strategy & Business Models

- Key HRS Developers: FirstElement, Air Liquide, Linde, Nel, H2 Energy

- Hydrogen Supply Cost Sensitivity Analysis

- LCOH Sensitivity to Renewable Electricity Price

- IRA 45V Credit Impact on US Green Hydrogen Economics

- EU Hydrogen Bank Auction Results & Green H₂ Premium Trajectory

- Delivered H₂ Cost at Nozzle: 2025, 2027, 2030, 2035 Scenarios

- Trade Flow Analysis

- Hydrogen Exporting Countries & Green Ammonia Reconversion

- Import-Export Dynamics: EU, Japan, South Korea H₂ Import Plans

- Impact of Geopolitical Events on Hydrogen Supply Security

- Hydrogen Production: Technology & Cost Benchmarking

- Total Cost of Ownership & Pricing Analysis

- Vehicle Acquisition Cost Benchmarking

- FCEV Truck Purchase Price vs Diesel vs Battery-Electric (Class 7–8)

- Fuel Cell System Cost Breakdown (Stack, Storage, Electronics, Integration)

- OEM Price Trajectory: 2025, 2028, 2030, 2035 Projections

- Residual Value & Depreciation Profiles for FCEV Trucks

- Operating Cost Analysis

- Hydrogen Fuel Cost per km at Various Dispensed H₂ Price Points

- Diesel vs H₂ Fuel Cost Break-Even Price ($/kg) by Mileage Profile

- Maintenance Cost Comparison: FCEV vs Diesel vs BEV

- Fuel Cell Stack Replacement Cost & Interval Planning

- Tyre, Brake & Component Wear Rates for FCEV Trucks

- Total Cost of Ownership Modelling

- 10-Year TCO at USD 6/kg, USD 8/kg, and USD 10/kg Dispensed H₂

- TCO Sensitivity to Annual Mileage (100k, 150k, 200k km)

- TCO Impact of Carbon Pricing (EU ETS, UK Carbon Tax, LCFS Credits)

- Government Incentive & Subsidy Impact on Effective Acquisition Cost

- Fleet Financing Models: Outright Purchase vs Leasing vs TaaS

- Price Tier Analysis by Segment

- Urban Distribution (Class 4–6): TCO vs Battery-Electric Benchmark

- Regional Haul (Class 7–8): Hydrogen vs Diesel Parity Timeline

- Long-Haul Class 8: Detailed Scenario Modelling

- Vehicle Acquisition Cost Benchmarking

- Sustainability, Well-to-Wheel Emissions & ESG Analysis

- Well-to-Wheel Lifecycle Emissions by Hydrogen Pathway (gCO₂e/km)

- Tank-to-Wheel Emissions Comparison: Diesel vs FCEV vs BEV

- Carbon Intensity of Hydrogen Supply by Country & Energy Mix

- EU Renewable Fuels of Non-Biological Origin (RFNBO) Compliance

- Green Hydrogen Certification Schemes: CertifHy, TUV, IRENA

- ESG Reporting Frameworks for Fleet Decarbonisation (TCFD, GRI, CDP)

- Science Based Targets (SBTi): Transport Sector Net-Zero Pathways

- Circular Economy Considerations: Fuel Cell Stack & Platinum Recycling

- Go-to-Market & Distribution

- Sales Channel Overview

- Direct Fleet Sales: OEM-to-Operator Contracts

- Dealer & Distributor Network Development for FCEV Trucks

- Full-Service Leasing & Fleet Management (Including H₂ Supply)

- Truck-as-a-Service (TaaS): Cost-per-km Commercial Models

- Government Tender & Public Procurement Channels

- Hydrogen Mobility Alliance & Consortium Procurement Models

- After-Sales Service, Maintenance & Spare Parts

- Fuel Cell Stack Maintenance Protocols & OEM Service Contracts

- Hydrogen System Safety Inspection & Certification Requirements

- Technician Training & Certification for H2 High-Voltage Systems

- Fleet Operator Onboarding: Pilot-to-Scale Pathway

- Distribution Strategies by Leading OEMs

- Sales Channel Overview

- Competitive Landscape

- Market Structure & Concentration

- Market Fragmentation Level: OEMs vs Startup Entrants vs Incumbents

- Top 10 Players by Units Deployed & Order Backlog

- HHI (Herfindahl–Hirschman Index) Concentration by Segment & Region

- Competitive Intensity Map: Vehicle Class vs Geography

- Player Classification

- Incumbent Heavy-Duty OEMs (Daimler Truck, Volvo, Hyundai, Toyota, IVECO)

- North American Class 8 Players (Kenworth, Nikola, Freightliner)

- Chinese OEMs (SAIC, FAW, Dongfeng, Foton, SINOTRUK, Yutong)

- Fuel Cell System Specialists (Ballard, Bosch, cellcentric, Cummins)

- Hydrogen Storage Specialists (Hexagon, Luxfer, Faber, NPROXX)

- Start-Up & Emerging Players (Quantron, Tevva, HVS, Gaussin)

- Regional & Niche Players

- Competitive Analysis Frameworks

- Market Share Analysis by Units & Revenue

- Company Profile

- Company Overview & HQ

- Fuel Cell Truck Product Portfolio (Models, GVW Classes, Range)

- Fuel Cell System Architecture & Stack Supplier

- Hydrogen Storage Configuration

- Revenue & Commercial Vehicle / FCEV Segment Revenue

- Geographic Presence & Target Markets

- Fleet Deployments & Customer Contracts (Units, Routes, Partners)

- Refuelling Infrastructure Partnerships

- Recent Developments (M&A, Orders, Partnerships, Plant Investments)

- SWOT Analysis

- Technology Roadmap & Next-Generation Platform Plans

- Competitive Positioning Map (Range vs Payload vs Cost)

- OEM Alliance & JV Landscape (cellcentric, Toyota-Kenworth, HECTOR)

- Market Structure & Concentration

- Investment & Ecosystem Financing Landscape

- Vehicle Production Investment: OEM CapEx & Manufacturing Scale-Up

- Fuel Cell Stack Manufacturing Investment by Major Suppliers

- Hydrogen Infrastructure Investment: Station Networks & Corridors

- Green Hydrogen Production Investment: Electrolyser Gigafactories

- Government Grant & Incentive Programmes by Region

- EU Innovation Fund, CEF Transport, Horizon Europe H2 Projects

- US DOE H2@Scale Hubs, FHWA Alternative Fuels Corridors

- South Korea FCEV Commercialisation Fund

- China City-Cluster Subsidy Programmes

- UK ZEHID (Zero Emission HGV & Infrastructure Demonstrator)

- Venture Capital & Private Equity Activity (2020–2026)

- Project Finance Structures for Hydrogen Refuelling Networks

- Fleet Financing: Green Bond, Sustainability-Linked Loan Markets

- Project Pipeline: Announced, Funded & Under Deployment (2025–2030)

- Strategic Recommendations

- For Hydrogen Fuel Cell Truck OEMs

- Product & Platform Strategy: Class Prioritisation & Modular Architecture

- Fuel Cell System Sourcing: In-House vs Tier-1 Supply Strategy

- Total Cost of Ownership Leadership Strategy

- Geographic Market Entry & Localisation Strategy

- Refuelling Infrastructure Partnership & Ecosystem Building Strategy

- Fleet-as-a-Service & TaaS Commercial Model Development

- M&A, JV & Technology Partnership Strategy

- For Fuel Cell System & Component Suppliers

- Stack Cost Reduction Roadmap: PGM Reduction, Volume Manufacturing

- Heavy-Duty Stack Durability & Warranty Extension Strategy

- OEM Co-Development & Long-Term Supply Agreement Strategy

- Hydrogen Storage System Cost & Weight Optimisation

- For Fleet Operators & Logistics Companies

- Hydrogen Truck Pilot-to-Scale Transition Framework

- Hydrogen Supply & Refuelling Security Strategy

- Optimal Route & Application Identification for FCEV Deployment

- Green Hydrogen Offtake Agreement & Price Hedging Strategy

- Financing & Incentive Optimisation for Fleet Transition

- For Hydrogen Producers, Distributors & Infrastructure Developers

- Green H₂ Cost Reduction Roadmap: Electrolyser & Renewable Energy

- Corridor HRS Network Development & Siting Strategy

- Fleet Anchor Tenant Strategy for Station Viability

- Liquid H₂ vs Gaseous Supply Model Selection by Use Case

- For Investors & Private Equity

- High-Priority Investment Themes by Technology & Geography

- M&A Opportunity Map: OEM vs Stack vs Infrastructure vs H₂ Supply

- Risk-Return Analysis by Technology Maturity Stage

- Geographic Investment Priorities

- Key Risk Considerations (H₂ Cost, Infrastructure, TCO, Policy)

- For Governments & Regulators

- Policy Recommendations to Accelerate FCEV Truck Deployment

- Infrastructure Mandate Design: AFIR-Style Corridor HRS Requirements

- Green Hydrogen Production Incentive Design (45V Model Adoption)

- Public Procurement Leadership: Government Fleet Mandates

- Interoperability & Standards Harmonisation Across Regions

- White Space & Opportunity Analysis

- Unmet Market Needs by Application & Route Profile

- Emerging Business Models: Hydrogen Mobility-as-a-Service

- Technology White Spaces: Liquid H₂, SOFC, Solid-State Storage

- Geographic White Spaces: Southeast Asia, Middle East, Latin America

- Strategic Priority Matrix & Roadmap

- Near-term (2025–2028)

- Mid-term (2029–2032)

- Long-term (2033–2036)

- For Hydrogen Fuel Cell Truck OEMs