Market Definition

The Global Industrial Water Circularity Platforms Market encompasses the integrated portfolio of technologies, software systems, digital solutions, infrastructure components, and service frameworks that collectively enable industrial enterprises to systematically minimize freshwater withdrawal, maximize the internal reuse and recycling of process water, recover valuable resources embedded in wastewater streams, and achieve verifiable progress toward closed-loop or near-zero liquid discharge water management objectives across their manufacturing and processing operations. Industrial water circularity platforms represent a structural departure from the conventional linear water management paradigm, in which freshwater is drawn from surface or groundwater sources, used once in industrial processes, treated to regulatory discharge standards, and released into receiving water bodies, toward a regenerative operational model in which water is continuously recaptured, treated, upgraded, and reintroduced into productive use within the industrial facility or shared across co-located industrial operations through water symbiosis arrangements. The technological and service scope of this market encompasses advanced wastewater treatment and reclamation systems including membrane bioreactors, ultrafiltration, nanofiltration, reverse osmosis, and electrodialysis; water reuse and recycling circuit design and engineering; industrial cooling water optimization and blowdown recovery systems; process water monitoring and quality management instrumentation; zero liquid discharge and minimum liquid discharge technology systems; resource recovery platforms extracting nutrients, minerals, energy, and specialty chemicals from industrial effluent streams; water accounting and digital twin platforms that model facility-level water flows and identify circularity optimization opportunities; IoT-enabled water quality and flow monitoring networks; artificial intelligence and machine learning platforms for predictive water treatment optimization; and the consultancy, managed service, and water-as-a-service commercial frameworks through which these technologies are deployed and operated at industrial scale. The market serves a broad and diverse industrial customer base spanning semiconductor and electronics manufacturing, food and beverage processing, pharmaceutical and biotechnology production, chemicals and petrochemicals, power generation, textiles and apparel, pulp and paper, mining and mineral processing, automotive manufacturing, and data center operations, each presenting distinct water quality requirements, contaminant profiles, reuse constraints, and regulatory compliance obligations that define the technical and commercial parameters of water circularity platform deployment across different industrial contexts.

Market Insights

The global industrial water circularity platforms market is entering a period of accelerated commercial and institutional maturation in 2026, driven by the simultaneous intensification of water scarcity conditions across major industrial geographies, the progressive tightening of industrial water discharge and abstraction regulations, the integration of water stewardship metrics into corporate sustainability reporting and investor ESG assessment frameworks, and the maturing of the enabling technology stack that makes industrial water circularity economically viable at progressively lower levels of water reuse intensity. The convergence of physical water stress, regulatory compliance pressure, and corporate accountability is creating a market environment in which water circularity investments are increasingly evaluated not merely as environmental expenditure but as strategic assets that protect operational continuity, reduce regulatory and reputational risk, and generate measurable financial returns through reduced freshwater procurement costs, lower wastewater treatment and discharge fee obligations, and the recovery of value from effluent streams that were previously managed as waste. The market is transitioning from a predominantly project-based engineering and construction model toward a more diversified commercial structure that includes recurring software subscription revenues, managed service and outsourced operations contracts, performance-based water service agreements, and digital platform licensing, creating a more stable and predictable revenue profile for solution providers and improving the financial accessibility of water circularity investments for industrial customers with constrained capital expenditure budgets.

A defining technological trend reshaping the industrial water circularity platform landscape is the rapid integration of digital intelligence, real-time sensing, and advanced analytics capabilities into water management systems that have historically been operated as standalone treatment infrastructure with limited connectivity to enterprise operational and sustainability reporting systems. The deployment of dense IoT sensor networks monitoring water quality parameters, flow rates, chemical dosing efficiency, and membrane performance in real time is enabling a shift from reactive to predictive water treatment management, reducing chemical consumption, energy use, and unplanned downtime while improving the consistency of treated water quality for reuse applications. Digital twin platforms that create high-fidelity virtual representations of facility water systems are enabling industrial operators and their technology partners to model the impact of process changes, demand fluctuations, and treatment system upgrades on overall water circularity performance before committing to physical investments, substantially reducing the cost and risk of circularity optimization programs. Artificial intelligence and machine learning algorithms trained on operational water system data are being applied to treatment process optimization, anomaly detection, predictive maintenance of water treatment assets, and dynamic water routing across complex multi-circuit industrial water networks, delivering efficiency improvements and operational cost reductions that strengthen the financial case for advanced circularity platform deployment and differentiate sophisticated integrated platform offerings from conventional equipment supply relationships.

The emergence of industrial water symbiosis as a commercially structured market segment within the broader water circularity platform landscape represents one of the most strategically significant developments of the current period, as co-located industrial enterprises within shared industrial parks, special economic zones, and integrated manufacturing campuses increasingly explore the potential for treating and exchanging water streams between facilities whose effluent quality from one process is compatible with the intake requirements of another, creating inter-company circular water flows that deliver system-level water efficiency improvements substantially beyond what any individual facility could achieve through internal recirculation alone. Water symbiosis arrangements require the development of shared water infrastructure including inter-facility transfer networks, shared treatment facilities, and centralized monitoring and quality assurance systems, as well as the commercial and legal frameworks governing water quality liability, pricing mechanisms, and service level obligations between participating enterprises. The growth of planned industrial cluster development, particularly across Asia-Pacific and the Middle East where large-scale industrial parks are being developed with integrated utility infrastructure from the outset, is creating enabling conditions for water symbiosis at a scale and with a planning horizon that makes shared water circularity infrastructure economically justified and operationally manageable. Technology platform providers are responding to this opportunity by developing multi-site water management software architectures that can model, optimize, and govern water flows across portfolios of connected industrial facilities, establishing a new and commercially significant platform category within the industrial water circularity market.

From a regional perspective, Asia-Pacific represents the largest and most urgently driven market for industrial water circularity platforms, with China, India, and the water-stressed industrial economies of Southeast Asia facing the most acute combination of severe groundwater depletion, river system degradation, tightening industrial discharge regulations, and expanding heavy water-consuming industrial base that collectively create the strongest imperative for systematic water circularity investment. China’s progressive strengthening of industrial water abstraction permitting, discharge standard enforcement, and the integration of water efficiency metrics into industrial enterprise environmental compliance assessments is compelling large-scale manufacturing and processing operations across energy, chemicals, textiles, and electronics sectors to invest in water recirculation and reuse infrastructure at an accelerating pace. Europe represents the most policy-sophisticated and technologically advanced market for water circularity, with the European Union’s Water Framework Directive, Industrial Emissions Directive, and emerging water stewardship legislation creating a comprehensive regulatory framework that is driving investment in advanced water reclamation, resource recovery, and digital water management across the full spectrum of water-intensive industries. North America is exhibiting growing market momentum, particularly in water-stressed Western states and provinces where industrial water use restrictions, groundwater depletion concerns, and the growing exposure of manufacturing operations to water availability risk are motivating capital investment in circularity infrastructure that reduces operational dependence on increasingly constrained freshwater resources. The Middle East, with its extreme water scarcity conditions and ambitious industrial diversification programs, represents a high-priority and high-investment growth market for water circularity platforms, with zero liquid discharge and advanced water reuse technologies receiving strong institutional support as components of national water security strategies.

Key Drivers

Intensifying Physical Water Scarcity, Industrial Water Use Restrictions, and the Operational Risk Imperative for Water Supply Resilience

The most fundamental and operationally urgent driver of the global industrial water circularity platforms market is the progressive deterioration of freshwater availability across major industrial geographies, driven by the compounding effects of climate change-altered precipitation patterns, accelerating groundwater depletion from over-extraction, increasing competition for surface water resources between industrial, agricultural, and municipal users, and the growing frequency and severity of drought events that disrupt the reliability of industrial water supply from conventional sources. Industrial enterprises operating in water-stressed regions are experiencing an escalating frequency of water use restrictions, abstraction permit curtailments, and supply interruptions that directly threaten production continuity and expose facilities to financially material operational risk if their water supply strategies remain dependent on unconstrained access to externally sourced freshwater. The business continuity and operational resilience imperative for securing industrial water supply through internal circularity, rather than relying solely on external water sources whose availability is increasingly uncertain, is translating water circularity investment from an environmental responsibility expenditure into a core operational risk management priority that commands board-level attention and capital allocation consideration independent of regulatory compliance requirements. Regulatory responses to water scarcity, including the tightening of industrial water abstraction licensing, the introduction of progressive water pricing mechanisms that increase the cost of high-volume freshwater use, and the mandating of water audits and efficiency improvement plans for major industrial water users, are reinforcing the operational risk driver with a financial cost signal that further strengthens the investment case for water circularity platforms across the full range of water-intensive industrial sectors.

Tightening Industrial Wastewater Discharge Regulations and the Growing Mandate for Zero Liquid Discharge Compliance Across Key Industrial Sectors

A powerful and jurisdictionally expanding regulatory driver for industrial water circularity platform investment is the progressive tightening of industrial wastewater discharge standards across major manufacturing economies, including the reduction of permissible contaminant concentration limits for a broadening range of emerging pollutants, the extension of discharge permitting requirements to industrial categories previously operating under less stringent compliance frameworks, and the active promotion or mandating of zero liquid discharge and minimum liquid discharge operational standards in the most environmentally sensitive and water-scarce contexts. Regulatory authorities in China, India, Europe, and several Latin American economies have implemented or are advancing regulations that specifically require textile, chemical, pharmaceutical, tannery, and other high-contaminant industrial sectors to achieve zero liquid discharge status, eliminating the option of external wastewater disposal and making internal water treatment and reuse infrastructure a regulatory compliance necessity rather than an operational choice. The financial penalties, production suspension powers, and reputational enforcement mechanisms associated with industrial discharge non-compliance are creating compelling risk-adjusted investment cases for water circularity platform deployment that extend beyond the direct economic benefits of reduced freshwater procurement and wastewater disposal costs to include the avoidance of regulatory penalty exposure, license-to-operate risk, and the brand and stakeholder relationship damage associated with visible environmental non-compliance incidents. The expansion of corporate environmental due diligence obligations, supply chain environmental audit requirements from major multinational customers, and investor ESG disclosure standards that include water-related metrics is further extending the effective regulatory perimeter for industrial water management compliance beyond direct regulatory requirements to encompass voluntary but commercially consequential supply chain and capital market accountability frameworks.

Corporate Water Stewardship Commitments, ESG Reporting Mandates, and the Integration of Water Metrics into Sustainability Accountability Frameworks

A commercially significant and structurally durable driver of industrial water circularity platform adoption is the progressive integration of water stewardship performance metrics into the corporate sustainability reporting frameworks, ESG investment evaluation criteria, and supply chain sustainability standards that govern the relationships between industrial enterprises, their investors, their major customers, and the communities in which they operate. Global corporations across consumer goods, food and beverage, apparel, electronics, and automotive sectors have made public water stewardship commitments aligned with science-based targets for water use reduction, watershed replenishment, and supply chain water risk disclosure, and the credibility of these commitments in the context of investor scrutiny and stakeholder accountability is creating structured procurement preferences and supplier qualification requirements that cascade water circularity investment obligations through industrial supply chains to raw material and component manufacturers. Institutional investors applying ESG screening criteria and climate and nature-related financial disclosure frameworks are assigning growing importance to corporate water risk exposure and water stewardship performance in investment analysis and portfolio management decisions, creating a capital market incentive for industrial enterprises to demonstrate measurable progress on water circularity metrics. International sustainability reporting standards including the Global Reporting Initiative, the Carbon Disclosure Project Water Security program, and the emerging Task Force on Nature-Related Financial Disclosures are establishing standardized water disclosure requirements that increase the visibility and comparability of industrial water performance data, creating accountability mechanisms that motivate investment in quantifiable water circularity improvements whose outcomes can be credibly reported against public commitments and investor expectations.

Key Challenges

High Capital Intensity of Advanced Water Circularity Infrastructure and the Challenge of Demonstrating Financial Returns on Complex Multi-Technology Deployments

A significant structural challenge confronting the industrial water circularity platforms market is the high upfront capital investment required for the deployment of advanced water reclamation, zero liquid discharge, and closed-loop water management systems, particularly at the levels of treatment sophistication and reuse intensity required for highly contaminated industrial effluent streams in sectors including semiconductors, pharmaceuticals, chemicals, and textiles where water quality requirements for reuse are stringent and treatment process complexity is consequently elevated. Zero liquid discharge systems incorporating multiple stages of evaporation, crystallization, advanced membrane separation, and brine concentration represent among the most capital-intensive water treatment investments in the industrial sector, and the financial return calculation for these systems requires sophisticated total cost of ownership modeling that incorporates avoided freshwater procurement costs, wastewater disposal fee reductions, regulatory penalty avoidance value, recovered resource revenue, and operational efficiency improvements that may be difficult to quantify with the precision required to satisfy corporate capital expenditure approval processes. The challenge of building financially compelling investment cases for water circularity is compounded in industrial contexts where water costs have historically been low, where water tariffs do not reflect the full economic scarcity value of freshwater, or where operational accounting systems do not capture the full cost of water across its lifecycle within the industrial facility, creating a perception that water circularity investments compete unfavorably with process efficiency or product quality investments for scarce capital budget. Platform providers and technology integrators are responding by developing water-as-a-service and outcome-based contract structures that transfer technology and performance risk to the service provider and convert capital expenditure to operational expenditure for industrial customers, but the commercial maturity and financial capacity of these alternative financing models varies significantly across geographies and customer segments.

Technical Complexity of Treating Highly Contaminated and Variable Industrial Effluent Streams for High-Quality Reuse Applications

A fundamental technical challenge in the industrial water circularity market is the difficulty of designing, operating, and maintaining treatment systems capable of consistently upgrading the diverse and often severely contaminated effluent streams generated by industrial processes to the quality standards required for reuse in sensitive applications including process water replenishment, cooling water make-up, boiler feed water, and product contact cleaning applications, where contaminant carryover can compromise product quality, damage equipment, or create safety and regulatory compliance risks. Industrial effluent streams are characterized by complex and variable mixtures of organic compounds, heavy metals, suspended solids, dissolved salts, surfactants, solvents, and biological contaminants whose composition fluctuates with production schedules, raw material changes, and operational conditions in ways that challenge the stable operation of treatment systems designed for specific inlet quality parameters. The presence of recalcitrant micropollutants, pharmaceutical active compounds, endocrine-disrupting substances, and per- and polyfluoroalkyl substances in industrial effluent streams from certain sectors is requiring the development and deployment of advanced treatment technologies including advanced oxidation processes, granular activated carbon adsorption, and specialized membrane configurations that add cost, operational complexity, and energy consumption to the treatment chain. Maintaining consistent treated water quality suitable for high-specification reuse applications as inlet water quality varies requires sophisticated monitoring, control, and treatment adjustment capabilities that demand a higher level of operational expertise and technology sophistication than conventional single-pass wastewater treatment, creating ongoing operational challenges for industrial facilities with limited in-house water treatment expertise and motivating the development of automated and remotely managed treatment systems that can maintain performance with reduced reliance on specialized on-site personnel.

Data Integration Complexity and the Challenge of Establishing Unified Digital Water Management Across Fragmented Industrial Operational Technology Environments

A structural challenge specifically confronting the digital and platform-oriented segment of the industrial water circularity market is the complexity of integrating water monitoring, treatment control, quality management, and sustainability reporting data across the heterogeneous and historically fragmented operational technology environments that characterize mature industrial facilities, where water management systems from multiple vendors, generations, and communication protocol standards must be connected into a coherent digital architecture that enables real-time visibility, analytical processing, and optimization across the full facility water cycle. Industrial facilities typically operate a combination of legacy supervisory control and data acquisition systems, proprietary sensor networks from individual equipment vendors, manually maintained laboratory quality records, and enterprise resource planning systems that hold production scheduling and utility consumption data, none of which were designed for interoperability with modern IoT platforms, digital twin systems, or cloud-based water analytics applications. Establishing the data infrastructure required for comprehensive real-time water circularity monitoring and optimization requires significant integration engineering investment, cybersecurity risk management across operational technology networks that must be protected from the vulnerabilities inherent in increased connectivity, and organizational change management to align the operational practices of plant engineers, environmental compliance teams, and sustainability reporting functions around shared data systems and performance metrics. The absence of universal data standards for industrial water system interoperability limits the scalability and cross-facility deployment efficiency of digital water circularity platforms, creating vendor lock-in risks for industrial customers and constraining the network effects and data aggregation advantages that would accelerate platform learning and optimization capability development across large portfolios of connected industrial water systems.

Market Segmentation

- Segmentation By Platform Type

- Water Reuse and Recirculation Systems

- Zero Liquid Discharge (ZLD) Platforms

- Minimum Liquid Discharge (MLD) Systems

- Industrial Wastewater Treatment and Reclamation Platforms

- Digital Water Management and Analytics Platforms

- Water Digital Twin and Simulation Platforms

- IoT-Enabled Water Monitoring and Control Systems

- Water Symbiosis and Inter-Facility Exchange Platforms

- Resource Recovery from Wastewater Platforms

- Water-as-a-Service Managed Platforms

- Others

- Segmentation By Treatment Technology

- Membrane Bioreactor (MBR)

- Ultrafiltration and Microfiltration

- Nanofiltration and Reverse Osmosis

- Electrodialysis and Ion Exchange

- Advanced Oxidation Processes

- Evaporation and Crystallization

- Electrocoagulation and Electrochemical Treatment

- Activated Carbon Adsorption

- Biological Treatment and Constructed Wetlands

- Brine Concentration and Solidification

- Others

- Segmentation By Digital and Software Component

- SCADA and Real-Time Control Systems

- IoT Sensor Networks and Edge Computing

- Artificial Intelligence and Machine Learning Optimization

- Digital Twin and Process Simulation

- Water Accounting and Material Flow Analysis Software

- Predictive Maintenance Platforms

- Regulatory Compliance and Reporting Software

- Water Risk and Scenario Modeling Tools

- Blockchain-Based Water Traceability Platforms

- Others

- Segmentation By Resource Recovery Output

- Recovered Water for Process Reuse

- Energy Recovery from Wastewater

- Nutrient Recovery (Nitrogen and Phosphorus)

- Mineral and Salt Recovery

- Specialty Chemical and Solvent Recovery

- Heavy Metal Recovery and Valorization

- Biogas and Biomass Production

- Others

- Segmentation By End-Use Industry

- Semiconductor and Electronics Manufacturing

- Food and Beverage Processing

- Pharmaceutical and Biotechnology

- Chemicals and Petrochemicals

- Textiles and Apparel

- Power Generation and Energy

- Automotive Manufacturing

- Pulp and Paper

- Mining and Mineral Processing

- Data Centers and Digital Infrastructure

- Oil and Gas

- Others

- Segmentation By Deployment Model

- On-Site Owned and Operated Systems

- Water-as-a-Service (WaaS) and Outsourced Operations

- Build-Own-Operate-Transfer (BOOT) Arrangements

- Performance-Based Water Service Contracts

- Industrial Park Shared Water Infrastructure

- Modular and Mobile Treatment Units

- Others

- Segmentation By Facility Scale

- Large-Scale Industrial Complexes

- Mid-Scale Manufacturing Facilities

- Small and Medium Industrial Operations

- Industrial Parks and Special Economic Zones

- Others

- Segmentation By Circularity Objective

- Zero Liquid Discharge Compliance

- Water Withdrawal Reduction and Conservation

- Closed-Loop Process Water Recycling

- Cooling Water Optimization and Recovery

- Wastewater-to-Resource Valorization

- Corporate Water Stewardship Target Achievement

- Regulatory Discharge Compliance

- Water Risk and Supply Resilience Management

- Others

- Segmentation By Service Type

- Engineering, Procurement, and Construction (EPC)

- Operations and Maintenance Services

- Water Audit and Circularity Assessment

- Technology Integration and System Commissioning

- Remote Monitoring and Managed Services

- Training and Capacity Building

- Water Stewardship Certification and Reporting

- Others

- Segmentation By End User

- Multinational Industrial Corporations

- Domestic Large-Scale Manufacturers

- Industrial Park and Free Zone Operators

- Government-Owned Industrial Enterprises

- Contract Manufacturers and Outsourced Production Operators

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021–2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027–2036

Key Questions this Study Will Answer

- What is the projected global market valuation for industrial water circularity platforms through 2036, segmented by platform type, treatment technology, end-use industry, deployment model, and region, and which technology categories and industrial sectors are expected to generate the highest incremental revenue contribution as water scarcity conditions intensify and zero liquid discharge mandates expand across major industrial geographies?

- How are digital intelligence capabilities including IoT-enabled monitoring networks, artificial intelligence-driven treatment optimization, and digital twin simulation platforms reshaping the competitive differentiation of industrial water circularity solution providers, and what is the projected revenue contribution of digital and software components relative to physical treatment infrastructure within the total platform market over the forecast horizon?

- To what extent are water-as-a-service, performance-based contract, and build-own-operate-transfer commercial structures expected to displace traditional capital equipment procurement as the dominant deployment model for advanced water circularity systems, and what are the financial structuring, risk allocation, and technology performance guarantee frameworks that are enabling these alternative models to gain traction across different industrial customer segments and geographies?

- How are industrial water symbiosis programs and shared water infrastructure models within industrial parks and special economic zones expected to create a new and commercially distinct platform market segment, and which regional development contexts, regulatory incentive structures, and technology platform architectures are most conducive to the commercial realization of inter-facility water circularity at scale?

- Who are the leading industrial water technology providers, digital water platform developers, engineering and managed service operators, and water-as-a-service commercial innovators currently defining the competitive landscape of the global industrial water circularity platforms market, and what are their respective technology investment priorities, geographic expansion strategies, end-use industry focus areas, and partnership and acquisition approaches through the forecast horizon?

- Product Definition

- Scope of the Study

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Industry Publications, Water Technology Provider Reports, Industry Association Reports & Press Releases

- Government & Regulatory Authority Data (US EPA, EU Commission, IEA, World Bank, UN-Water, FAO AQUASTAT, etc.)

- Industrial Water Withdrawal, Consumption, Reuse Rate & Discharge Market Statistics

- Platform Provider, Technology Vendor, Utility & Industrial End-User Supply Chain Databases

- Primary Research Design & Execution

- In-depth Interviews with Platform Providers, Water Technology Vendors, Industrial End-User Water Managers & Sustainability Directors

- Surveys with End-Use Industry Players, Engineering Procurement & Construction (EPC) Firms & Water Utilities

- Expert Panel Validation

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Bottom-Up & Top-Down Reconciliation

- Industrial Water Withdrawal, Reuse Potential & Platform Addressable Market Sizing Model

- Platform Adoption Rate, Digitisation Penetration & Revenue Forecasting Model

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Technology & Innovation Highlights

- Platform Economics & Unit Economics Summary

- Average Platform Deployment CAPEX & OPEX Benchmarks

- On-Premise vs Cloud-Based Platform Cost & Margin Comparison

- Water Savings, Recycling Rate Improvement & Revenue Model Summary

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Geographic & Regional Trends

- Risk Assessment Framework

- Geopolitical & Water Governance Risk (Transboundary Water Stress, National Water Restrictions)

- Cybersecurity & Data Privacy Risk in Connected Water Management Platforms

- Environmental & Regulatory Compliance Risk

- Financial / Market Risk

- Integration Complexity, Legacy Infrastructure & Interoperability Risk

- Water Quality Variability & Treatment Process Performance Risk

- Climate Change, Physical Water Scarcity & Extreme Weather Event Risk

- Regulatory Framework & Policy Standards

- Global Industrial Water Circularity Platforms Market Economics

- Platform Deployment Economics & Unit Economics Framework

- Capital Expenditure (CAPEX) Structure

- Operating Expenditure (OPEX) Structure

- Revenue Model & Monetisation Levers

- Platform Utilisation & Throughput Economics

- Payback Period & Return on Investment (ROI) Analysis

- Total Cost of Platform Ownership vs Conventional Water Management Approaches

- Water & Wastewater Input Cost Analysis

- Industrial Freshwater Procurement Cost Benchmarks & Price Trends (USD/m³, 2021–2035)

- Wastewater Treatment & Discharge Cost Dynamics

- Water Recycling & Reuse Cost Differentials vs Freshwater Intake

- Energy Cost Structure in Water Treatment, Recycling & Platform Operations

- Chemical Treatment, Membrane & Consumable Input Cost Analysis

- Water Loss, Leakage & Non-Revenue Water Cost Impact

- Impact of Water Quality, Contaminant Load & Zero Liquid Discharge (ZLD) Requirements on Platform Economics

- Platform Deployment & Integration Economics

- Software Licensing, SaaS Subscription & Platform-as-a-Service (PaaS) Cost Structure

- Sensor Network, IoT Hardware & Edge Computing Deployment Cost

- System Integration, API Connectivity & Legacy Infrastructure Retrofit Cost

- Data Management, Cloud Infrastructure & Cybersecurity Cost

- Operations, Maintenance & Customer Support Service Economics

- Water Savings, Recycling Rate & Productivity Benefit Quantification

- Water Savings Value (Volume Reduction & Cost Avoidance) per Platform Deployment

- Wastewater Recycling & Reuse Revenue & Cost Savings Economics

- Effluent Discharge Fee Avoidance & Regulatory Penalty Mitigation Economics

- Water-Related Carbon Emission Reduction & Carbon Credit Economics

- Regulatory & Standards Compliance Economics

- Industrial Effluent Discharge & Water Quality Standards Compliance Cost Benchmarks (ISO, EU WFD, US CWA, etc.)

- Zero Liquid Discharge (ZLD) & Near-ZLD Compliance Cost Analysis

- ESG Disclosure, Water Stewardship & Reporting Framework Compliance Costs (CDP Water, GRI, TCFD, etc.)

- Global Industrial Water Circularity Platforms Market Outlook

- Market Size & Forecast by Value (USD Billion, 2021–2036)

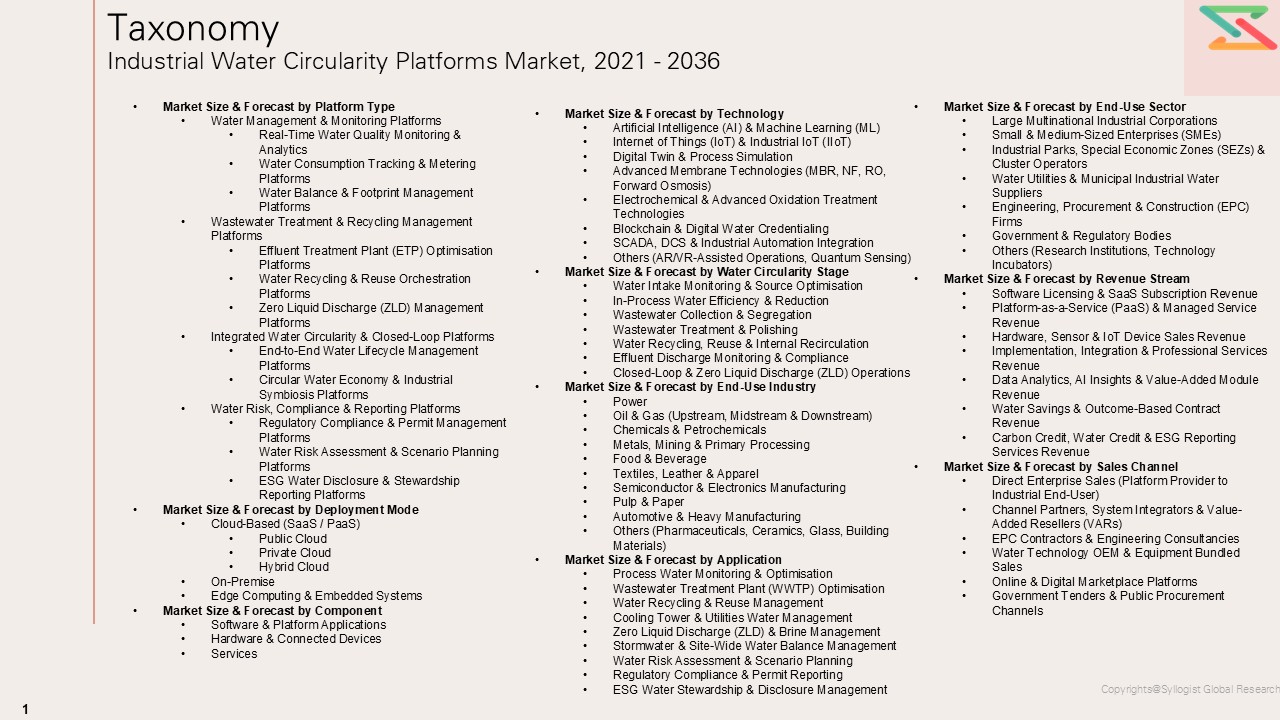

- Market Size & Forecast by Platform Type

- Water Management & Monitoring Platforms

- Real-Time Water Quality Monitoring & Analytics

- Water Consumption Tracking & Metering Platforms

- Water Balance & Footprint Management Platforms

- Wastewater Treatment & Recycling Management Platforms

- Effluent Treatment Plant (ETP) Optimisation Platforms

- Water Recycling & Reuse Orchestration Platforms

- Zero Liquid Discharge (ZLD) Management Platforms

- Integrated Water Circularity & Closed-Loop Platforms

- End-to-End Water Lifecycle Management Platforms

- Circular Water Economy & Industrial Symbiosis Platforms

- Water Risk, Compliance & Reporting Platforms

- Regulatory Compliance & Permit Management Platforms

- Water Risk Assessment & Scenario Planning Platforms

- ESG Water Disclosure & Stewardship Reporting Platforms

- Market Size & Forecast by Deployment Mode

- Cloud-Based (SaaS / PaaS)

- Public Cloud

- Private Cloud

- Hybrid Cloud

- On-Premise

- Edge Computing & Embedded Systems

- Cloud-Based (SaaS / PaaS)

- Market Size & Forecast by Component

- Software & Platform Applications

- Data Analytics, AI & Machine Learning Modules

- Digital Twin & Process Simulation Modules

- Dashboard, Reporting & Visualisation Tools

- Hardware & Connected Devices

- IoT Sensors, Flow Meters & Water Quality Analysers

- Edge Computing & Gateway Devices

- SCADA & PLC Integration Hardware

- Services

- Consulting, Design & Engineering Services

- Implementation, Integration & Commissioning Services

- Managed Services, Operations & Maintenance

- Training, Support & Platform Optimisation Services

- Market Size & Forecast by Technology

- Artificial Intelligence (AI) & Machine Learning (ML)

- Internet of Things (IoT) & Industrial IoT (IIoT)

- Digital Twin & Process Simulation

- Advanced Membrane Technologies (MBR, NF, RO, Forward Osmosis)

- Electrochemical & Advanced Oxidation Treatment Technologies

- Blockchain & Digital Water Credentialing

- SCADA, DCS & Industrial Automation Integration

- Others (AR/VR-Assisted Operations, Quantum Sensing)

- Market Size & Forecast by Water Circularity Stage

- Water Intake Monitoring & Source Optimisation

- In-Process Water Efficiency & Reduction

- Wastewater Collection & Segregation

- Wastewater Treatment & Polishing

- Water Recycling, Reuse & Internal Recirculation

- Effluent Discharge Monitoring & Compliance

- Closed-Loop & Zero Liquid Discharge (ZLD) Operations

- Market Size & Forecast by End-Use Industry

- Power Generation & Energy

- Thermal Power Plants (Coal, Gas, Nuclear)

- Renewable Energy (Concentrated Solar, Geothermal, Hydrogen)

- Oil & Gas (Upstream, Midstream & Downstream)

- Produced Water Management & Recycling

- Refinery Cooling Water & Process Water Recycling

- Chemicals & Petrochemicals

- Specialty Chemicals, Agrochemicals & Pharmaceuticals

- Basic Chemicals, Fertilisers & Polymers

- Metals, Mining & Primary Processing

- Mine Water Treatment & Acid Mine Drainage (AMD) Management

- Smelter & Refinery Process Water Recycling

- Food & Beverage

- Dairy, Brewery & Beverage Processing

- Meat Processing, Sugar & Starch Industries

- Textiles, Leather & Apparel

- Semiconductor & Electronics Manufacturing

- Ultra-Pure Water (UPW) Recycling & Reclaim

- Cooling Water & General Facility Water Management

- Pulp & Paper

- Automotive & Heavy Manufacturing

- Others (Pharmaceuticals, Ceramics, Glass, Building Materials)

- Power Generation & Energy

- Market Size & Forecast by Application

- Process Water Monitoring & Optimisation

- Wastewater Treatment Plant (WWTP) Optimisation

- Water Recycling & Reuse Management

- Cooling Tower & Utilities Water Management

- Zero Liquid Discharge (ZLD) & Brine Management

- Stormwater & Site-Wide Water Balance Management

- Water Risk Assessment & Scenario Planning

- Regulatory Compliance & Permit Reporting

- ESG Water Stewardship & Disclosure Management

- Market Size & Forecast by End-Use Sector

- Large Multinational Industrial Corporations

- Global Full-Line Industrial Conglomerates with In-House Water Management

- Multinational OEMs Procuring Water Circularity Platforms

- Small & Medium-Sized Enterprises (SMEs)

- Industrial Parks, Special Economic Zones (SEZs) & Cluster Operators

- Water Utilities & Municipal Industrial Water Suppliers

- Engineering, Procurement & Construction (EPC) Firms

- Government & Regulatory Bodies

- Others (Research Institutions, Technology Incubators)

- Large Multinational Industrial Corporations

- Market Size & Forecast by Revenue Stream

- Software Licensing & SaaS Subscription Revenue

- Platform-as-a-Service (PaaS) & Managed Service Revenue

- Hardware, Sensor & IoT Device Sales Revenue

- Implementation, Integration & Professional Services Revenue

- Data Analytics, AI Insights & Value-Added Module Revenue

- Water Savings & Outcome-Based Contract Revenue

- Carbon Credit, Water Credit & ESG Reporting Services Revenue

- Market Size & Forecast by Sales Channel

- Direct Enterprise Sales (Platform Provider to Industrial End-User)

- Channel Partners, System Integrators & Value-Added Resellers (VARs)

- EPC Contractors & Engineering Consultancies

- Water Technology OEM & Equipment Bundled Sales

- Online & Digital Marketplace Platforms

- Government Tenders & Public Procurement Channels

- Asia-Pacific Industrial Water Circularity Platforms Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Platform Type

- By Deployment Mode

- By Component

- By Technology

- By Water Circularity Stage

- By End-Use Industry

- By Application

- By End-Use Sector

- By Revenue Stream

- By Sales Channel

- Key Demand Drivers (APAC-Specific)

- Competitive Landscape (APAC)

- Europe Industrial Water Circularity Platforms Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Platform Type

- By Deployment Mode

- By Component

- By Technology

- By Water Circularity Stage

- By End-Use Industry

- By Application

- By End-Use Sector

- By Revenue Stream

- By Sales Channel

- Key Demand Drivers (Europe-Specific)

- Competitive Landscape (Europe)

- North America Industrial Water Circularity Platforms Market Outlook

- Market Overview & Strategic Importance

- Market Size & Forecast

- By Value (2020–2035)

- By Platform Type

- By Deployment Mode

- By Component

- By Technology

- By Water Circularity Stage

- By End-Use Industry

- By Application

- By End-Use Sector

- By Revenue Stream

- By Sales Channel

- Key Demand Drivers (North America-Specific)

- Competitive Landscape (North America)

- Latin America Industrial Water Circularity Platforms Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Platform Type

- By Deployment Mode

- By Component

- By Technology

- By Water Circularity Stage

- By End-Use Industry

- By Application

- By End-Use Sector

- By Revenue Stream

- By Sales Channel

- Key Demand Drivers (LATAM-Specific)

- Competitive Landscape (Latin America)

- Middle East & Africa Industrial Water Circularity Platforms Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Platform Type

- By Deployment Mode

- By Component

- By Technology

- By Water Circularity Stage

- By End-Use Industry

- By Application

- By End-Use Sector

- By Revenue Stream

- By Sales Channel

- Key Demand Drivers (MEA-Specific)

- Competitive Landscape (MEA)

- Country-Wise Industrial Water Circularity Platforms Market Outlook

- Market Size & Forecast by Country

- By Value

- By Platform Type

- By Deployment Mode

- By Component

- By Technology

- By Water Circularity Stage

- By End-Use Industry

- By Application

- By End-Use Sector

- By Revenue Stream

- By Sales Channel

- Countries Covered: United States, Canada, Germany, France, United Kingdom, Netherlands, Spain, Italy, China, India, Japan, South Korea, Australia, Singapore, Brazil, Mexico, Saudi Arabia, United Arab Emirates, South Africa, Israel

- Market Size & Forecast by Country

- Technology Landscape & Innovation Analysis

- Industrial Water Circularity Platform Technology Maturity Assessment

- Emerging & Disruptive Technologies in Industrial Water Circularity Platforms

- AI, ML & Predictive Analytics for Water Process Optimisation & Anomaly Detection

- Digital Twin Technology for Industrial Water System Simulation & Scenario Planning

- IoT Sensor Networks, Real-Time Monitoring & Edge Computing for Water Data Acquisition

- Advanced Membrane & Treatment Technologies (MBR, NF, RO, Forward Osmosis, Electrochemical)

- Blockchain & Digital Water Credentialing for Water Use Traceability & Trading

- Technology Readiness & Commercialisation Matrix – Key Industrial Water Circularity Platform Technologies

- Patent Landscape Analysis

- R&D Investment Benchmarking

- Value Chain & Ecosystem Analysis

- Industrial Water Circularity Platform Ecosystem Mapping

- Platform Provider, Technology Vendor & System Integrator Relationship Analysis

- Supply Chain Concentration & Dependency Analysis

- Key Partner Mapping by Platform Type, Technology & End-Use Industry

- Partner & Ecosystem Risk Heat Map

- Build vs Buy vs Partner Strategy Trends Among Industrial Platform Providers

- Pricing Analysis

- Industrial Water Circularity Platform Pricing Dynamics & Mechanisms

- Pricing by Platform Type, Deployment Mode & Component

- Total Cost of Ownership (TCO) Analysis – Including Water Savings, Regulatory Avoidance & Productivity Benefits

- SaaS Subscription vs Perpetual Licence vs Outcome-Based Contract Pricing Models

- Enterprise vs SME Pricing Tiers & Value Proposition

- Sustainability & Water Circularity Performance

- Industrial Water Withdrawal Intensity & Circularity Rate Benchmarking by Industry

- Platform-Enabled Water Savings, Reuse Rate Improvement & Wastewater Reduction Quantification

- Water-Related Carbon Footprint: Energy & Emission Reduction Through Circularity Platforms

- Water Stewardship Certification & Reporting Frameworks (CDP Water, AWS Standard, GRI 303, TCFD)

- Industrial Closed-Loop Water Programmes & Corporate Water Neutrality Commitments

- EU Water Framework Directive, US Clean Water Act & Global Industrial Water Policy Impact Assessment

- ESG Reporting, Lifecycle Assessment (LCA) & Science-Based Targets for Water in Industrial Operations

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level: Global Platform Leaders vs Niche & Regional Players

- Top 5 Industrial Water Circularity Platform Providers Market Revenue Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis by Platform Type & End-Use Industry

- Competitive Intensity Map by Segment & Region

- Player Classification

- Tier-1 Global Integrated Industrial Water Circularity Platform Providers

- Tier-2 Specialist & Niche Platform Providers

- Water Technology OEMs with Embedded Platform Capabilities

- System Integrators, EPC Firms & Digital Transformation Partners

- Emerging & Disruptive Players

- Competitive Analysis Frameworks

- Market Share Analysis by Platform Type, Deployment Mode & Geography

- R&D Intensity & Water AI / IoT Innovation Benchmarking

- Long-Term Enterprise Contract & Strategic Partnership Portfolio Comparison

- Geographic Revenue Exposure & Customer Industry Footprint Comparison

- Company Profiles

- Company Overview, HQ & Organisational Structure

- Industrial Water Circularity Platform Products & Services Portfolio

- Revenue Breakdown (By Platform Type, By Segment, By Geography)

- Key Customer Deployments & Closed-Loop Water Programme Partnerships

- Technology Infrastructure & Data Centre / Cloud Footprint

- Recent Developments (M&A, Product Launches, Partnerships, Financial Results)

- SWOT Analysis

- Strategic Focus: AI-Driven Water Optimisation, ZLD Platform Leadership, Industry Vertical Expansion

- Strategic Output

- Market Opportunity Matrix

- High-Value Opportunity Quadrant Analysis

- Addressable Market by Segment & Region

- Time-to-Revenue Assessment by Opportunity

- White Space Opportunity Analysis

- Underserved End-Use Industry, Platform Type & Geography Gaps

- Geographic Markets with Low Platform Penetration & High Water Stress

- Technology Gaps with High Commercialisation Potential

- Customer Segment Unmet Needs

- Strategic Recommendations

- Platform Portfolio & Product Innovation Strategy

- Technology & Digitalization Strategy

- Platform Deployment Capacity & Infrastructure Investment Strategy

- Customer Acquisition, Channel & Ecosystem Partnership Strategy

- Pricing & Commercial Strategy

- Sustainability, Water Stewardship & Regulatory Compliance Strategy

- Data Strategy, Cybersecurity & Platform Resilience Strategy

- Partnership, M&A & Expansion Strategy

- Regional Growth Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-Term (2025–2028)

- Mid-Term (2029–2032)

- Long-Term (2033–2036)

- Market Opportunity Matrix

- Market Structure & Concentration

- Market Size & Forecast

- Market Size & Forecast

- Market Size & Forecast

- Market Size & Forecast

- Software & Platform Applications

- Water Management & Monitoring Platforms

- Platform Deployment Economics & Unit Economics Framework