Market Definition

The last mile delivery market refers to the final and most critical segment of the logistics supply chain, encompassing the movement of goods from a localized distribution hub or fulfillment center to the end-user’s ultimate destination, typically a residential doorstep or a retail location. As the final touchpoint in the e-commerce journey, this market is defined by its focus on speed, precision, and cost-efficiency, serving as the bridge between large-scale regional logistics and individual consumer fulfillment. It involves a diverse ecosystem of transport modes, ranging from traditional delivery vans and two-wheelers to emerging autonomous solutions like drones and sidewalk robots, and is increasingly underpinned by sophisticated route-optimization software and real-time tracking technologies.

By 2026, the market has evolved beyond simple transportation into a high-tech service sector characterized by hyper-localization and a variety of delivery models, including same-day, on-demand, and click-and-collect options via automated lockers. The primary objective within this market is to solve the last mile problem, the inherent challenge of delivering small, frequent shipments to highly fragmented locations, which often accounts for up to 50% of total shipping costs. Driven by the global explosion of online retail and rising consumer expectations for nearly instantaneous fulfillment, the last mile delivery market is now a central battlefield for competitive differentiation, where operational excellence directly correlates with customer loyalty and brand reputation.

Market Insights

As of early 2026, the global last-mile delivery market has reached a critical valuation of approximately USD 195 billion, sustained by a robust annual growth rate of nearly 9%. This expansion is primarily propelled by the permanent shift in consumer behavior toward e-commerce, where platforms like Amazon and Alibaba have set a global standard for same-day and next-day fulfillment. Delivery is no longer viewed merely as a logistical necessity but as a primary competitive differentiator; studies indicate that over 80% of shoppers will abandon a purchase if their preferred delivery or return options are unavailable. This pressure to modernize has forced logistics providers to transition from legacy, manual processes to high-velocity, data-driven operations to maintain margins in an increasingly crowded field.

Technological transformation is the defining characteristic of the 2026 landscape, with agentic AI and autonomous systems moving from experimental pilots into core operational roles. Artificial intelligence is now the standard for dynamic route optimization, allowing fleets to adjust in real-time to traffic, weather, and shifting delivery windows. The deployment of micro-fulfillment centers (MFCs) and urban dark stores has effectively shrunk the last mile by positioning high-demand inventory closer to the end-user, often within a five-kilometer radius. Furthermore, autonomous delivery droids and drones are increasingly utilized for short-range, lightweight parcels, particularly in high-density urban zones and isolated rural areas where traditional van delivery is economically inefficient.

Sustainability has evolved from a corporate social responsibility initiative into a mandatory operational requirement due to tightening urban regulations and consumer demand. Across major metropolitan areas, the implementation of Zero-Emission Zones (ZEZs) and strict curb-space policies is accelerating the transition to electrified fleets and alternative micromobility modes, such as cargo bikes and electric two-wheelers. Leading carriers have committed significant capital to these transitions, with major players already operating thousands of electric heavy and light-duty vehicles. Beyond the environmental impact, these green logistics strategies are yielding measurable operational ROI through reduced fuel consumption and lower maintenance costs, though the high upfront investment for charging infrastructure remains a significant barrier for smaller operators.

From a regional perspective, North America continues to hold the largest market share, driven by a mature e-commerce ecosystem and advanced logistics infrastructure. However, the Asia-Pacific region is the fastest-growing hub, fueled by a surging middle class and high smartphone penetration in markets like India, Vietnam, and Indonesia. Despite this growth, the industry faces persistent structural challenges, most notably the last-mile problem, where the final leg of the journey can account for up to 50% of total shipping costs. Urban congestion, labor shortages in the driver pool, and the rising complexity of reverse logistics for product returns continue to strain profitability, prompting firms to explore collaborative elastic capacity models that utilize third-party couriers to manage seasonal peak volumes.

Market Drivers

Major Drivers of the Global Last-Mile Delivery Market

Proliferation of E-Commerce and Shifting Consumer Expectations The relentless expansion of the global e-commerce sector remains the primary engine of the last-mile delivery market. As digital marketplaces move from secondary to primary shopping channels, consumer expectations have fundamentally shifted toward instant gratification, making same-day and next-day delivery the new industry standard. This high-frequency demand is forcing retailers to move inventory closer to urban centers through micro-fulfillment hubs and dark stores, ensuring that the final leg of the journey is as rapid and seamless as the initial click-to-buy action.

Advancements in Autonomous Systems and AI Optimization

Rapid innovation in autonomous delivery technology is significantly reshaping the operational landscape of the last mile. From sidewalk robots and delivery drones to sophisticated AI-driven route optimization software, technology is being leveraged to decouple delivery volume from labor constraints. These systems allow carriers to dynamically adjust to real-time traffic patterns and weather disruptions, maximizing fleet utilization and ensuring that even the most complex urban routes are handled with a level of precision and speed that was previously unattainable through manual planning.

Market Challenges

High Operational Costs and the Last-Mile Problem

Despite its critical importance, the last mile remains the most expensive and inefficient segment of the entire supply chain, often accounting for up to 50% of total shipping costs. The inherent complexity of delivering small, individual parcels to fragmented residential locations, coupled with the rising costs of fuel and labor, creates a massive financial burden for logistics providers. This challenge is further exacerbated by the increasing volume of failed deliveries and the high cost of reverse logistics for product returns, which continue to strain the profitability of even the most established global carriers.

Increasing Urban Congestion and Regulatory Pressure

As metropolitan areas become more densely populated, the logistical burden of navigating high-traffic urban zones is becoming a major operational bottleneck. Many major global cities are now implementing strict Zero-Emission Zones (ZEZs) and curb-space regulations, forcing delivery firms to aggressively transition their fleets to electric vehicles and alternative micromobility solutions like cargo bikes. While these green mandates align with global sustainability goals, the massive capital expenditure required for electric fleet procurement and the lack of a robust charging infrastructure present a significant hurdle for many logistics players.

Market Segmentation

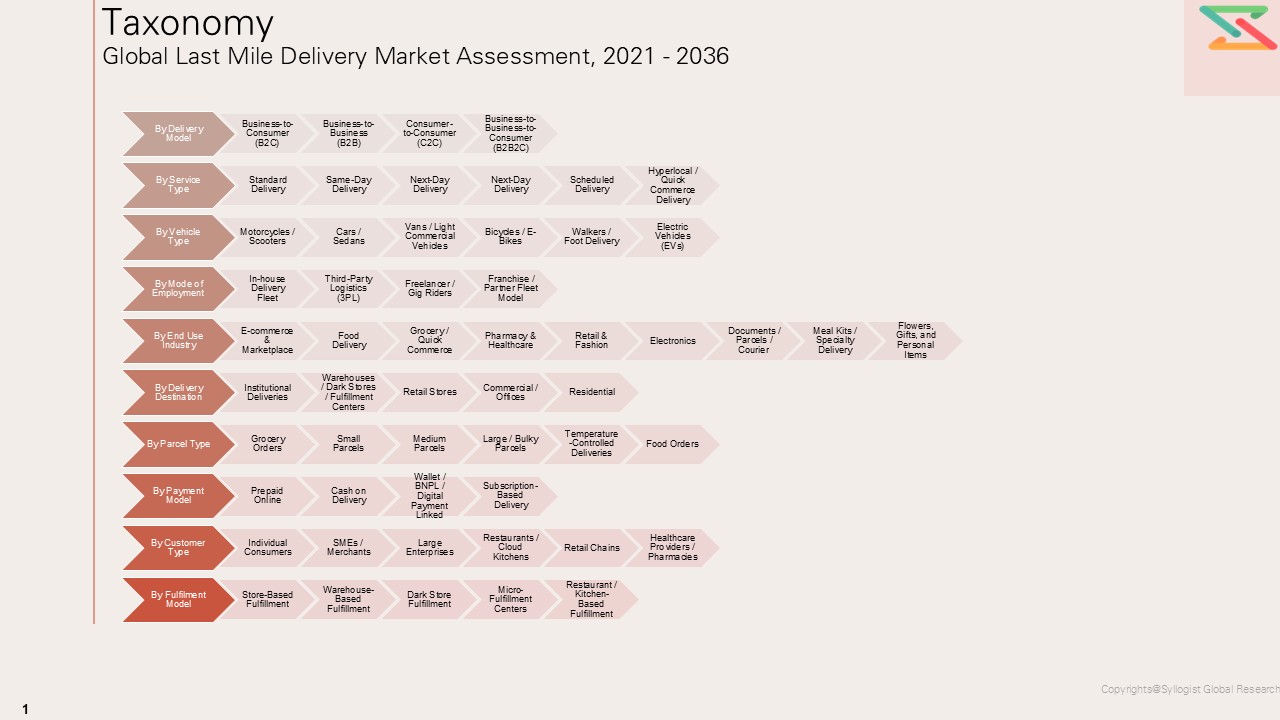

- Segmentation by Delivery Model

- Business-to-Consumer (B2C)

- Business-to-Business (B2B)

- Consumer-to-Consumer (C2C)

- Business-to-Business-to-Consumer (B2B2C)

- Segmentation by Service Type

- Standard Delivery

- Same-Day Delivery

- Next-Day Delivery

- Express / On-Demand Delivery

- Scheduled Delivery

- Hyperlocal / Quick Commerce Delivery

- Segmentation by Vehicle Type

- Motorcycles / Scooters

- Cars / Sedans

- Vans / Light Commercial Vehicles

- Bicycles / E-Bikes

- Walkers / Foot Delivery

- Electric Vehicles (EVs)

- Segmentation by Mode of Employment

- In-house Delivery Fleet

- Third-Party Logistics (3PL)

- Freelancer / Gig Riders

- Franchise / Partner Fleet Model

- Segmentation by End Use Industry

- E-commerce & Marketplace

- Food Delivery

- Grocery / Quick Commerce

- Pharmacy & Healthcare

- Retail & Fashion

- Electronics

- Documents / Parcels / Courier

- Meal Kits / Specialty Delivery

- Flowers, Gifts, and Personal Items

- Segmentation by Delivery Destination

- Residential

- Commercial / Offices

- Retail Stores

- Warehouses / Dark Stores / Fulfilment Centers

- Institutional Deliveries

- Segmentation by Parcel Type

- Food Orders

- Grocery Orders

- Small Parcels

- Medium Parcels

- Large / Bulky Parcels

- Temperature-Controlled Deliveries

- Segmentation by Payment Model

- Prepaid Online

- Cash on Delivery

- Wallet / BNPL / Digital Payment Linked

- Subscription-Based Delivery

- Segmentation by Customer Type

- Individual Consumers

- SMEs / Merchants

- Large Enterprises

- Restaurants / Cloud Kitchens

- Retail Chains

- Healthcare Providers / Pharmacies

- Segmentation by Fulfilment Model

- Store-Based fulfilment

- Warehouse-Based fulfilment

- Dark Store fulfilment

- Micro-fulfilment Centers

- Restaurant / Kitchen-Based fulfilment

Key Questions this Study Will Answer

- What is the current and projected market size (in both volume and value) through 2031? This provides the quantitative baseline for understanding the total opportunity and the expected compound annual growth rate (CAGR) over the next decade.

- Which specific segments and geographies are poised for the most rapid growth? By identifying bright spots (such as the shift to SUVs or the rise of Southeast Asian last-mile logistics), the study will pinpoint where capital should be allocated for maximum return.

- What are the primary macroeconomic and regulatory drivers shaping the industry’s future? This includes evaluating the impact of new trade tariffs, zero-emission zones, and government incentive programs like Brazil’s MOVER or the EAEU’s industrial policies.

- How will the transition to electrification and autonomous technology disrupt traditional supply chains? The study will analyze how the shift from ICE to EV platforms, and the introduction of AI-driven logistics, will alter manufacturing requirements and service delivery models.

- Who are the dominant market players, and what are their successful strategic playbooks? A competitive analysis will reveal the market share concentration and the specific maneuvers (such as localized production or asset-light delivery models) used by industry leaders.

- What are the most significant operational and financial risks facing new entrants and existing incumbents? By identifying challenges like high capital intensity, urban congestion, and technical complexity, the study provides a realistic framework for risk mitigation.

- What specific unmet needs or emerging niche opportunities exist for innovation? This question focuses on the next frontier, such as specialized EV tires for heavy fleets or the deployment of small-scale modular FLNG units for stranded gas monetization.

- Market Foundations & Dynamics

- Market Taxonomy

- Research Methodology

- Executive Summary

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Ecosystem & Value Chain

- Evolution of Last Mile Delivery

- Logistics Value Chain

- Role of E-commerce, Food Delivery, and Quick Commerce

- Market Structure

- Marketplace Platforms

- Logistics Operators

- Merchant Partners

- Dark Stores / Micro Fulfilment

- Payment Platforms

- Market Trends & Developments

- Investment Hotspots

- Unmet Needs and White Market Spaces

- Investment and Funding Trends

- Venture Capital Investments

- Startup Ecosystem

- Strategic Partnerships

- Market Consolidation

- Risk Assessment Framework

- Political / Geopolitical Risk

- Regulatory Risk

- Financial / Market Risk

- Regulatory Framework & Standards

- Labor Regulations for Gig Workers

- Delivery Licensing Requirements

- Traffic Regulations

- EV Adoption Policies

- Food Delivery Regulations

- Global Last Mile Delivery Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Number of Deliveries)

- Market Size & Forecast by Delivery Model

- Business-to-Consumer (B2C)

- Business-to-Business (B2B)

- Consumer-to-Consumer (C2C)

- Business-to-Business-to-Consumer (B2B2C)

- Market Size & Forecast by Service Type

- Standard Delivery

- Same-Day Delivery

- Next-Day Delivery

- Express / On-Demand Delivery

- Scheduled Delivery

- Hyperlocal / Quick Commerce Delivery

- Market Size & Forecast by Vehicle Type

- Motorcycles / Scooters

- Cars / Sedans

- Vans / Light Commercial Vehicles

- Bicycles / E-Bikes

- Walkers / Foot Delivery

- Electric Vehicles (EVs)

- Market Size & Forecast by Mode of Employment

- In-house Delivery Fleet

- Third-Party Logistics (3PL)

- Freelancer / Gig Riders

- Franchise / Partner Fleet Model

- Market Size & Forecast by End Use Industry

- E-commerce & Marketplace

- Food Delivery

- Grocery / Quick Commerce

- Pharmacy & Healthcare

- Retail & Fashion

- Electronics

- Documents / Parcels / Courier

- Meal Kits / Specialty Delivery

- Flowers, Gifts, and Personal Items

- Market Size & Forecast by Delivery Destination

- Residential

- Commercial / Offices

- Retail Stores

- Warehouses / Dark Stores / Fulfillment Centers

- Institutional Deliveries

- Market Size & Forecast by Parcel Type

- Food Orders

- Grocery Orders

- Small Parcels

- Medium Parcels

- Large / Bulky Parcels

- Temperature-Controlled Deliveries

- Market Size & Forecast by Payment Model

- Prepaid Online

- Cash on Delivery

- Wallet / BNPL / Digital Payment Linked

- Subscription-Based Delivery

- Market Size & Forecast by Customer Type

- Individual Consumers

- SMEs / Merchants

- Large Enterprises

- Restaurants / Cloud Kitchens

- Retail Chains

- Healthcare Providers / Pharmacies

- Market Size & Forecast by Fulfilment Model

- Store-Based fulfilment

- Warehouse-Based fulfilment

- Dark Store fulfilment

- Micro-fulfilment Centers

- Restaurant / Kitchen-Based fulfilment

- Asia-Pacific Last Mile Delivery Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Deliveries)

- By Delivery Model

- By Service Type

- By Vehicle Type

- By Mode of Employment

- By End Use Industry

- By Delivery Destination

- By Parcel Type

- By Payment Model

- By Customer Type

- By Fulfilment Model

- Europe Last Mile Delivery Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Deliveries)

- By Delivery Model

- By Service Type

- By Vehicle Type

- By Mode of Employment

- By End Use Industry

- By Delivery Destination

- By Parcel Type

- By Payment Model

- By Customer Type

- By Fulfilment Model

- North America Last Mile Delivery Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Deliveries)

- By Delivery Model

- By Service Type

- By Vehicle Type

- By Mode of Employment

- By End Use Industry

- By Delivery Destination

- By Parcel Type

- By Payment Model

- By Customer Type

- By Fulfilment Model

- South America Last Mile Delivery Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Deliveries)

- By Delivery Model

- By Service Type

- By Vehicle Type

- By Mode of Employment

- By End Use Industry

- By Delivery Destination

- By Parcel Type

- By Payment Model

- By Customer Type

- By Fulfilment Model

- Middle East & Africa Last Mile Delivery Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Deliveries)

- By Delivery Model

- By Service Type

- By Vehicle Type

- By Mode of Employment

- By End Use Industry

- By Delivery Destination

- By Parcel Type

- By Payment Model

- By Customer Type

- By Fulfilment Model

- Countrywise* Last Mile Delivery Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Deliveries)

- By Delivery Model

- By Service Type

- By Vehicle Type

- By Mode of Employment

- By End Use Industry

- By Delivery Destination

- By Parcel Type

- By Payment Model

- By Customer Type

- By Fulfilment Model

- Market Size & Forecast

- Market Size & Forecast

- Market Size & Forecast

- Market Size & Forecast

- Market Size & Forecast

- Market Size & Forecast

Countries: United States, China, India, United Kingdom, Germany, France, Japan, South Korea, Canada, Australia, Brazil, Mexico, Saudi Arabia, United Arab Emirates, Netherlands, Italy, Spain, Singapore, Indonesia, Thailand, Malaysia, Vietnam, Philippines, Turkey, South Africa, Egypt, Nigeria, Poland, Sweden, Belgium, Switzerland, Russia, Argentina, Chile, and Colombia

- Pricing and Cost Structure

- Delivery Fee Structure

- Cost per Delivery

- Rider Compensation

- Platform Commission

- Merchant Fees

- Operational Metrics Benchmarking

- Orders per Rider per Day

- Average Delivery Time

- Cost per Delivery

- Rider Productivity

- Fleet Utilization

- Technology Landscape

- Route Optimization

- AI Dispatching

- Delivery Tracking

- Dark Store Technology

- Autonomous Delivery

- Competitive Landscape

- Market Share Analysis

- Platform Strategies

- Pricing Strategies

- Partnerships and M&A

- Key Players:

- Talabat

- Deliveroo

- Careem

- Noon

- Amazon

- Aramex

- DHL

- Jeeny

- Jahez

- HungerStation

- Rider Economics

- Average Rider Income

- Incentive Models

- Cost Per Order

- Strategic Recommendations & Roadmap

- Competitors’ Strategic Initiatives

- Future Outlook (Next 5–10 Years, Emerging Players, Success Factors)

- Strategic Recommendations

- Market Acceleration Roadmap

- Short-Term

- Mid-Term

- Long-Term

- Tailored Recommendations for:

- Producers

- Raw Material Suppliers

- Policymakers / Regulators

- Recommendations on Key Success Factors

- Raw Material Security

- Policy Alignment

- Supply Chain Integration

- Market Acceleration Roadmap