Linoleic Acid: A Functional Omega-6 Ingredient Linking Nutrition, Skincare, and Specialty Formulation

Linoleic acid is an essential omega-6 polyunsaturated fatty acid (18:2) that the human body cannot synthesize and must obtain from diet or formulated products. In commercial terms, it is sold either as a purified fatty acid or as a functional component derived from vegetable oils such as soybean, sunflower, safflower, and corn oil. Its use pattern in India is split across nutraceuticals and functional foods, cosmetics and dermatology-oriented formulations, pharmaceuticals, and a smaller industrial tail in coatings, inks, and specialty chemicals. Its strongest value proposition is that it sits at the intersection of nutrition, skin-barrier support, and bio-based formulation chemistry rather than behaving like a bulk commodity acid.

India Linoleic Acid Market: Import-Linked Supply Structure with a Strong Oilseed Feedstock Base

India does not appear to have a large, transparent standalone merchant market for purified linoleic acid in public-domain data; instead, supply is best understood as a combination of indirect domestic availability from oilseed processing and imports of high-purity or specialty grades. On the domestic side, India’s total vegetable oil production is projected at 9.7 MMT in MY 2025/26, while sunflower oil imports alone were forecast at 1.9 MMT for MY 2024/25, showing that India has a large underlying fatty-acid feedstock base but still depends materially on imported oils and specialty derivatives. India is also a significant producer of safflower crude oil globally, which matters because safflower and sunflower oils are among the richest natural linoleic-acid sources. For purified linoleic acid imports, accessible shipment databases indicate India imports mainly from the United States, Germany, and China, with importer activity concentrated among specialty chemical and life-science distributors. Publicly accessible syndicated sources confirm that India is being tracked as a distinct linoleic-acid market through 2031, but they do not disclose an open India market value on the landing pages; because of that, any exact market-size or CAGR number in the public domain should be treated cautiously. As a working directional view, India’s specialty linoleic-acid market is likely growing faster than the mature global base market, while the broader global linoleic-acid market is variously estimated at roughly 2.9% to 8.5% CAGR depending on scope and methodology.

India Linoleic Acid Market Dynamics: Wellness-Led Demand Growth Tempered by Feedstock and Import Volatility

The India opportunity is being pulled by three linked forces: rising use of active ingredients in skincare and haircare, stronger consumer interest in nutrition and preventive wellness, and broader substitution toward plant-based, naturally derived inputs in food, personal care, and specialty formulation. In practical terms, this supports better demand visibility for cosmetic and nutraceutical grades than for industrial grades. The challenge side is equally important: India’s edible-oil and fatty-acid chain remains exposed to import-duty changes, international vegetable-oil volatility, and periodic supply dislocation from origin countries. That makes linoleic-acid pricing more sensitive to upstream oilseed and edible-oil economics than many buyers initially assume. The market therefore benefits from structural demand expansion, but margins can compress quickly when feedstock inflation or import disruptions hit.

Production Technologies and Innovation: From Conventional Oil Processing to High-Purity and Stabilized Linoleic Acid Solutions

Current linoleic-acid production is still anchored in conventional oil extraction, hydrolysis/splitting, fractionation, and purification from vegetable-oil streams, especially soybean, sunflower, safflower, and corn oil. For higher-purity grades and value-added forms, the technology roadmap is moving toward combinations of urea complexation, molecular distillation, chromatography, and enzymatic processing. The same direction of travel is visible in adjacent PUFA purification research, where hybrid routes are being used to improve purity and yield. Beyond purification, innovation is also happening in delivery format: microencapsulation and stabilization technologies are becoming more relevant for food, nutraceutical, and cosmetic systems because linoleic acid is oxidation-sensitive. For India, that means competitive advantage will increasingly shift from simply sourcing feedstock to controlling purity, stability, and application-specific formulation performance.

Growth Hotspots and High-Value Segments: Premium Purity Grades and Wellness-Led Applications Driving India’s Linoleic Acid Opportunity

In India, the clearest commercial hotspot is not geography alone but the cluster of end-use sectors concentrated around major formulation hubs such as western and southern India, where nutraceutical, pharma, personal-care, and specialty chemical manufacturing are strongest. By purity, the faster-growth pocket is likely high-purity cosmetic, pharma, and nutraceutical grades rather than lower-grade industrial material, because value creation is tied to efficacy, label claims, and formulation consistency. By application, cosmetics and skin-health products look especially strong, supported by linoleic acid’s documented relevance in skin-barrier function and inflammation-linked skin conditions; globally, cosmetics is also identified as the leading revenue application in one recent market source. By end use, food and beverages remain structurally important in the broader market, but in India the premium-growth opportunity looks sharper in cosmetics, dietary supplements, and pharma-adjacent wellness products than in commoditized food use.

Market Trends and Outlook: Transitioning from Commodity Fatty Acid to High-Value Functional Ingredient

Recent market direction points to a gradual repositioning of linoleic acid in India from a simple fatty-acid ingredient toward a more application-engineered input tied to clean-label nutrition, dermaceutical skincare, and higher-function specialty formulations. Two trends stand out: first, growing interest in plant-based and naturally derived active ingredients; second, greater emphasis on purity, traceability, and stabilized delivery systems. The bottom line is that India’s linoleic-acid opportunity is real, but it is not best viewed as a bulk standalone acid market. It is better understood as a specialty ingredients play sitting on top of India’s much larger edible-oil ecosystem. That means the winners are likely to be companies that can secure feedstock optionality, manage import exposure, and convert linoleic acid into differentiated grades for cosmetics, nutraceuticals, and pharma-led applications rather than compete only on basic supply.

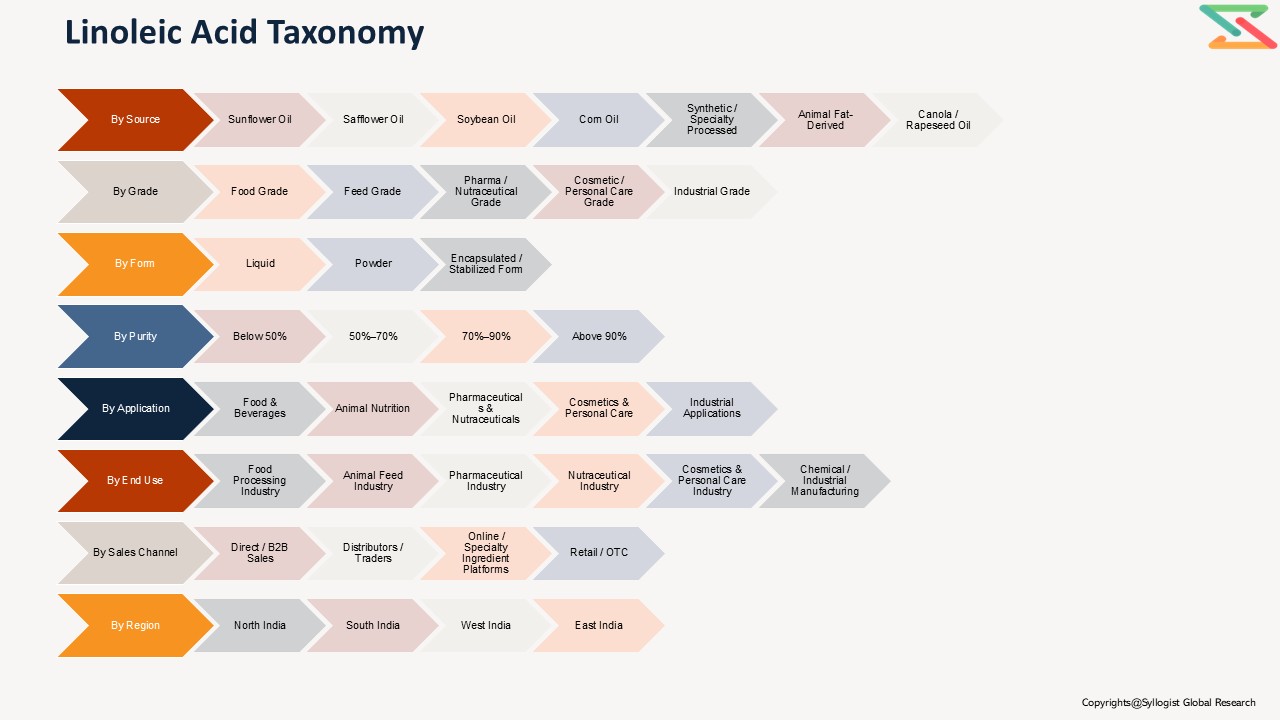

Market Segmentation:

- Segmentation by Source

- Vegetable Oil-Derived

- Sunflower Oil

- Safflower Oil

- Soybean Oil

- Corn Oil

- Canola / Rapeseed Oil

- Animal Fat-Derived

- Synthetic / Specialty Processed

- Vegetable Oil-Derived

- Segmentation by Grade

- Food Grade

- Feed Grade

- Pharma / Nutraceutical Grade

- Cosmetics / Personal Care Grade

- Industrial Grade

- Segmentation by Form

- Liquid

- Powder

- Encapsulated / Stabilized Form

- Segmentation by Purity

- Below 50%

- 50%–70%

- 70%–90%

- Above 90%

- Segmentation by Application

- Food & Beverages

- Edible Oils

- Functional Foods

- Fortified Food Products

- Dietary Supplements

- Animal Nutrition

- Poultry Feed

- Aquafeed

- Pet Food

- Livestock Feed

- Pharmaceuticals & Nutraceuticals

- Cosmetics & Personal Care

- Skin Care

- Hair Care

- Soap & Toiletries

- Industrial Applications

- Alkyd Resins

- Paints & Coatings

- Surfactants / Emulsifiers

- Lubricants

- Chemical Intermediates

- Segmentation by End Use Industry

- Food Processing Industry

- Animal Feed Industry

- Pharmaceutical Industry

- Nutraceutical Industry

- Cosmetics & Personal Care Industry

- Chemical / Industrial Manufacturing

- Segmentation by Sales Channel

- Direct / B2B Sales

- Distributors / Traders

- Online / Specialty Ingredient Platforms

- Retail / OTC

- Segmentation by Region

- East

- West

- North

- South

- Food & Beverages

- Introduction (Product Definition, Taxonomy and Research Methodology)

- Executive Summary

- Global Linoleic Acid Demand Supply Analysis

- Global Linoleic Acid Market Assessment, 2021-2036

- Global Market Outlook (Value, Volume and Segmental Analysis)

- India Linoleic Acid Market Assessment, 2021-2036

- Market Size & Forecast by Value

- Market Size & Forecast by Volume

- Market Size & Forecast by Source

- Vegetable Oil-Derived

- Sunflower Oil

- Safflower Oil

- Soybean Oil

- Corn Oil

- Canola / Rapeseed Oil

- Animal Fat-Derived

- Synthetic / Specialty Processed

- Vegetable Oil-Derived

- Market Size & Forecast by Grade

- Food Grade

- Feed Grade

- Pharma / Nutraceutical Grade

- Cosmetics / Personal Care Grade

- Industrial Grade

- Market Size & Forecast by Form

- Liquid

- Powder

- Encapsulated / Stabilized Form

- Market Size & Forecast by Purity

- Below 50%

- 50%–70%

- 70%–90%

- Above 90%

- Market Size & Forecast by Application

- Food & Beverages

- Edible Oils

- Functional Foods

- Fortified Food Products

- Dietary Supplements

- Animal Nutrition

- Poultry Feed

- Aquafeed

- Pet Food

- Livestock Feed

- Pharmaceuticals & Nutraceuticals

- Cosmetics & Personal Care

- Skin Care

- Hair Care

- Soap & Toiletries

- Industrial Applications

- Alkyd Resins

- Paints & Coatings

- Surfactants / Emulsifiers

- Lubricants

- Chemical Intermediates

- Market Size & Forecast by End Use Industry

- Food Processing Industry

- Animal Feed Industry

- Pharmaceutical Industry

- Nutraceutical Industry

- Cosmetics & Personal Care Industry

- Chemical / Industrial Manufacturing

- Market Size & Forecast by Sales Channel

- Direct / B2B Sales

- Distributors / Traders

- Online / Specialty Ingredient Platforms

- Retail / OTC

- Market Size & Forecast by Region

- East

- West

- North

- South

- White Space & Emerging Investment Hotspot

- Market White Space Opportunities

- Mergers & Acquisitions (M&A)

- Joint Ventures & Strategic Alliances

- Technology & Innovation Hotspots

- Regional Investment Attractiveness

- Barriers & Risks in Investment

- India Linoleic Acid Market Value Chain Analysis

- Raw Material Sourcing & Suppliers

- Key Raw Materials & Inputs

- Supplier Landscape & Concentration

- Pricing Trends & Volatility

- Dependence on Imports vs Domestic Availability

- Distribution & Logistics

- Marketing & Sales Channels

- Value Addition & Profitability across Chain

- Emerging Trends & Disruptions

- Raw Material Sourcing & Suppliers

- India Linoleic Acid Market Pricing Analysis

- Historical Vs Projected Pricing Analysis

- Demand-Supply Impact on Prices

- Application-wise Pricing Differences

- Impact of Tariffs, Taxes, and Trade Policies

- Key Player Pricing Strategies

- India Linoleic Acid Technology Landscape

- Key Existing Technologies

- Emerging & Next-gen Technologies

- Strategic Insights

- Future Technology Roadmap

- Opportunities for Differentiation via Technology

- Risks of Obsolescence & Barriers to Adoption

- Policy & Regulatory landscape

- Competition Outlook (Leading 10 Companies)

- Competition Benchmarking

- Market Leaders Vs New Entrants

- Strategic Recommendations

- Food & Beverages