Market Overview

The global lubricants market is increasingly shaped by structural drivers such as expanding automotive and industrial output, growing demand for high-performance and energy-efficient lubricants, rising adoption of synthetic and semi-synthetic formulations, and evolving regulatory standards focused on emissions reduction and environmental compliance. Lubricants are essential functional fluids designed to reduce friction, dissipate heat, prevent corrosion, and extend the operational life of machinery and mechanical components across a wide range of industrial and consumer applications.

These products are used across a diverse spectrum of applications including automotive engine and transmission systems, industrial machinery, power generation equipment, marine vessels, aviation systems, and food processing operations. The market encompasses both high-volume mineral oil-based lubricants and higher-value synthetic lubricants such as polyalphaolefins (PAO), polyalkylene glycols (PAG), and ester-based formulations used in demanding performance applications. Growing vehicle production volumes, expanding industrial manufacturing capacity, and increasing adoption of next-generation electric vehicle (EV) fluids are supporting sustained demand for lubricants globally. Simultaneously, tightening emissions standards and fuel economy regulations are accelerating the transition toward advanced low-viscosity and fully synthetic lubricant formulations.

Key Market Drivers

Growing Automotive Production and Vehicle Fleet Expansion

The global automotive industry remains the single largest end-use sector for lubricants, accounting for the majority of engine oil, transmission fluid, and gear oil consumption. Sustained growth in vehicle production across Asia Pacific, Latin America, and the Middle East is driving demand for both passenger car and commercial vehicle lubricants. Increasing vehicle ownership rates, expanding commercial logistics networks, and rising freight transport activity are generating continuous demand for automotive lubricant products.

The transition toward longer oil drain intervals and extended service life formulations is reshaping the automotive lubricant landscape. OEM specifications are increasingly mandating low-viscosity grades such as SAE 0W-20 and 0W-16 to improve fuel economy, while turbocharged direct-injection engines are demanding lubricants with enhanced thermal stability and oxidation resistance. As vehicle fleets continue to expand globally, particularly in emerging economies, automotive lubricant demand is expected to remain a primary volume growth engine for the market.

Industrial Manufacturing Growth and Machinery Lubrication Demand

The expansion of global manufacturing capacity, infrastructure development, and industrial automation is generating significant demand for industrial lubricants including hydraulic fluids, compressor oils, turbine oils, gear oils, and metalworking fluids. Industrial lubricants serve critical functions in manufacturing machinery, power generation turbines, mining equipment, construction machinery, and agricultural implements. Growth in capital-intensive industries such as steel, cement, mining, and energy is directly linked to rising industrial lubricant consumption.

In several regions, policies promoting industrial development, infrastructure investment, and manufacturing competitiveness are accelerating capital expenditure in machinery and equipment, which in turn increases lubricant consumption. The growing adoption of predictive maintenance programs and condition monitoring is also influencing lubricant selection, with increased preference for premium-grade products that offer extended service intervals, reduced maintenance downtime, and improved machinery reliability.

Shift Toward Synthetic and High-Performance Lubricants

The lubricants industry is undergoing a fundamental shift from conventional mineral oil-based products to advanced synthetic and semi-synthetic formulations. This transition is being driven by the need for improved thermal stability, wider operating temperature ranges, lower volatility, and enhanced oxidation resistance in modern high-performance applications. Synthetic lubricants, particularly PAO and ester-based products, offer significantly superior performance characteristics compared to mineral oils, making them increasingly preferred in automotive, aerospace, and critical industrial applications.

The shift toward synthetic lubricants is also supported by the growing adoption of energy efficiency standards and sustainability commitments by automotive OEMs and industrial equipment manufacturers. Synthetic lubricants enable reduced fuel consumption through lower internal friction, extended drain intervals that reduce waste lubricant generation, and improved machine protection that extends equipment life. As performance requirements continue to escalate across all major end-use sectors, the market share of synthetic lubricants is expected to grow consistently at the expense of conventional mineral oil-based products.

Growing Role of Electric Vehicle and Next-Generation Fluids

The rapid growth of electric vehicles and hybrid powertrains is creating a new and increasingly important segment within the lubricants market. While EVs eliminate the need for conventional engine oil, they introduce new fluid requirements including e-fluids for electric motors, transmission fluids for single-speed and multi-speed EV gearboxes, thermal management fluids for battery cooling systems, and dielectric fluids for high-voltage components. These next-generation fluids require highly specialized formulations that combine electrical insulating properties with excellent thermal conductivity, materials compatibility, and long service life.

Although commodity mineral oil lubricants account for a large share of current market volume, the value growth of the lubricants market is increasingly driven by specialty synthetic formulations and EV-specific fluid technologies. These products command premium pricing due to their technical complexity, application-specific performance requirements, and the growing importance of extended warranty protection in modern vehicles. As electric vehicle penetration accelerates globally, the role of specialty lubricant and fluid formulations is expected to expand significantly across the automotive value chain.

Technology Trends and Formulation Innovation

Continuous innovation in base oil refining, additive chemistry, and lubricant formulation science is reshaping the competitive landscape of the lubricants market. Advances in hydroprocessing technology have enabled the production of Group II and Group III base oils with significantly improved purity, viscosity index, and oxidation stability, narrowing the performance gap with fully synthetic Group IV and V base stocks. New additive packages incorporating advanced friction modifiers, antiwear agents, dispersants, and viscosity index improvers are enabling lubricant formulators to meet increasingly stringent OEM and regulatory specifications.

In addition, new lubricant formulations are being developed to address emerging application requirements including ultra-low viscosity engine oils for next-generation fuel-efficient engines, long-drain industrial lubricants for predictive maintenance programs, and food-grade lubricants for the expanding food and beverage processing industry. Emerging technologies such as nanoparticle-enhanced lubricant additives, ionic liquid-based lubricants, and bio-lubricants derived from vegetable oils and renewable feedstocks are also creating new product development opportunities. These innovations are enabling lubricant manufacturers to differentiate their product portfolios, command premium pricing, and address a broader range of application requirements.

Regional Market Insights

Market dynamics for lubricants vary considerably across regions reflecting differences in industrial development, vehicle fleet composition, regulatory environment, and climate conditions. Asia Pacific currently represents the largest and fastest-growing regional market, driven by strong automotive production in China, India, Japan, and South Korea, rapidly expanding industrial manufacturing capacity, and large commercial vehicle fleets. China alone accounts for the single largest national lubricant market globally, and India is emerging as one of the most attractive growth markets due to expanding vehicle ownership, infrastructure development, and industrial output growth.

North America and Europe represent mature but high-value markets characterized by strong demand for premium synthetic lubricants, stringent OEM specifications, and well-established re-refining and used oil collection infrastructure. The Middle East is a significant lubricant producer as well as a growing consumer market, with large base oil refining capacity supplying both domestic blending operations and global export markets. Latin America and Africa represent emerging growth opportunities driven by expanding vehicle fleets, infrastructure investment, and growing industrial activity, though market development is tempered by economic volatility and import dependency in several countries.

Market Outlook

The long-term outlook for the global lubricants market remains positive as automotive production, industrial manufacturing, and infrastructure development continue to expand across emerging economies. Increasing adoption of synthetic and semi-synthetic lubricants, growing demand for EV fluids and next-generation specialty formulations, and continuous innovation in base oil and additive technology will continue to support both volume growth and average selling price improvement. The market is expected to benefit from ongoing industrialization in Asia Pacific, the Middle East, Africa, and Latin America, which will sustain demand for both automotive and industrial lubricant products.

While commodity mineral oil lubricants will continue to account for the majority of market volume in the near term, synthetic lubricants and specialty fluid products are expected to capture an increasing share of market value, particularly as vehicle electrification advances, industrial automation deepens, and performance requirements continue to escalate. Companies that can combine formulation expertise, reliable base oil and additive supply chains, technical service capabilities, and cost-competitive blending operations are well positioned to strengthen their market share in the evolving global lubricants industry.

Market Segmentation

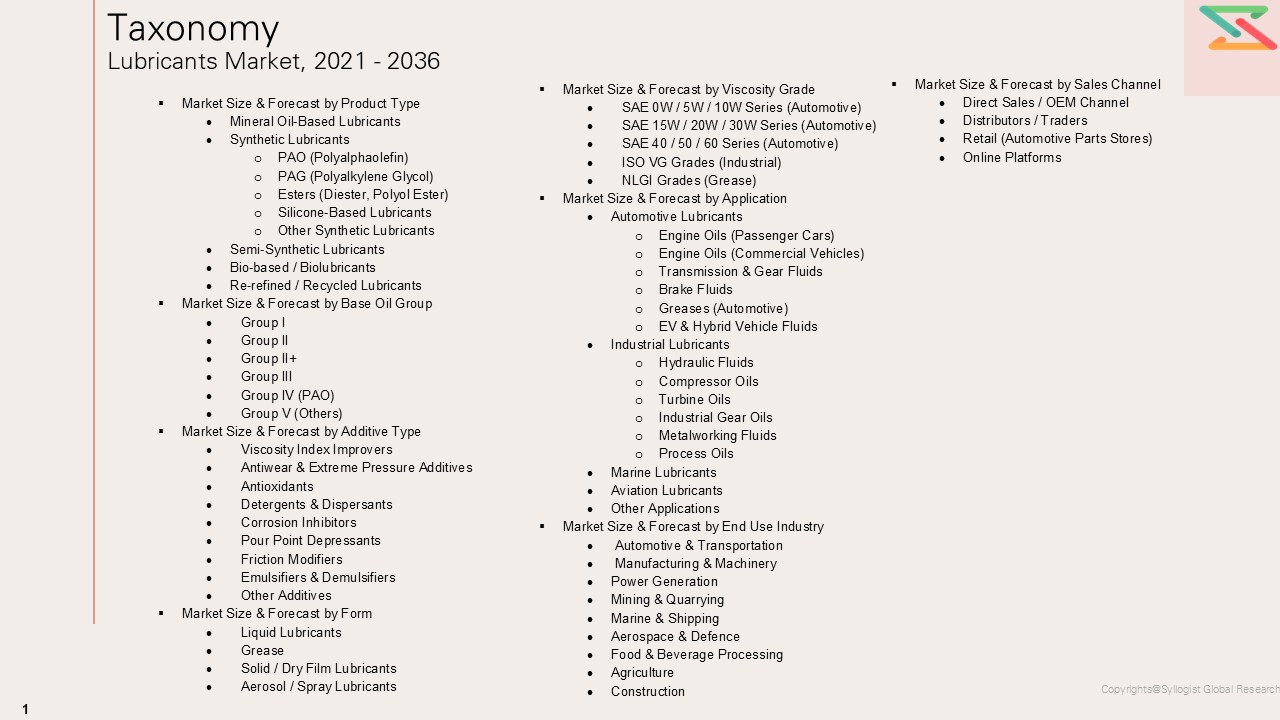

- Segmentation by Product Type

- Mineral Oil-Based Lubricants

- Synthetic Lubricants

- PAO (Polyalphaolefin)

- PAG (Polyalkylene Glycol)

- Esters (Diester, Polyol Ester)

- Silicone-Based Lubricants

- Other Synthetic Lubricants

- Semi-Synthetic Lubricants

- Bio-based / Biolubricants

- Re-refined / Recycled Lubricants

- Segmentation by Base Oil Group

- Group I

- Group II

- Group II+

- Group III

- Group IV (PAO)

- Group V (Others — Esters, PAG, Naphthenics)

- Segmentation by Additive Type

- Viscosity Index Improvers

- Antiwear & Extreme Pressure Additives

- Antioxidants

- Detergents & Dispersants

- Corrosion Inhibitors

- Pour Point Depressants

- Friction Modifiers

- Emulsifiers & Demulsifiers

- Other Additives

- Segmentation by Form

- Liquid Lubricants

- Grease

- Solid / Dry Film Lubricants

- Aerosol / Spray Lubricants

- Pastes & Compounds

- Segmentation by Viscosity Grade

- SAE 0W / 5W / 10W Series (Automotive)

- SAE 15W / 20W / 30W Series (Automotive)

- SAE 40 / 50 / 60 Series (Automotive)

- ISO VG Grades (Industrial Lubricants)

- NLGI Grades 000 to 6 (Grease)

- Segmentation by Application

- Automotive Lubricants

- Engine Oils (Passenger Cars)

- Engine Oils (Commercial Vehicles)

- Transmission & Gear Fluids

- Brake Fluids

- Greases (Automotive)

- EV & Hybrid Vehicle Fluids

- Industrial Lubricants

- Hydraulic Fluids

- Compressor Oils

- Turbine Oils

- Industrial Gear Oils

- Metalworking Fluids

- Process Oils

- Marine Lubricants

- Aviation Lubricants

- Other Applications

- Automotive Lubricants

- Segmentation by End Use Industry

- Automotive & Transportation

- Manufacturing & Machinery

- Power Generation

- Mining & Quarrying

- Marine & Shipping

- Aerospace & Defence

- Food & Beverage Processing

- Agriculture

- Construction

- Segmentation by Sales Channel

- Direct Sales / OEM Channel

- Distributors / Traders

- Retail (Automotive Parts Stores)

- Online Platforms

All market revenues are presented in USD and volume in tons

Historical Year: 2021–2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027–2036

Key Questions this Study Will Answer

- What are the critical market metrics and forward-looking projections for the Global Lubricants Market, including revenue size, volume consumption, and average selling prices, with performance segmentation across Product Type (Engine Oils, Transmission & Gear Oils, Hydraulic Fluids, Greases, Compressor Oils, Turbine Oils, Metalworking Fluids, Process Oils, Industrial Oils, Specialty Lubricants), Base Oil Type (Mineral Oil, Synthetic, Semi-Synthetic, Bio-based), Grade / Viscosity (Monograde, Multigrade, ISO VG categories, SAE grades), Application (Automotive, Industrial, Marine, Aviation, Construction, Mining, Agriculture, Power Generation), Functionality (Wear Protection, Thermal Stability, Oxidation Resistance, Fuel Economy, Extended Drain Intervals, Corrosion Protection, High-load Performance), Formulation Type (Conventional, High-Performance, Low-VOC, Environmentally Acceptable Lubricants), and End-Use Industry (Passenger Vehicles, Commercial Vehicles, Manufacturing, Metals & Mining, Oil & Gas, Power, Marine, Food Processing, Chemicals, Others)?

- How do supply–demand fundamentals vary across key regions and major lubricant-consuming industries, and what role do vehicle parc growth, industrial output, machinery utilization, freight movement, mining activity, marine trade, power generation demand, emission norms, fuel-efficiency standards, and sustainability regulations play in shaping regional competitiveness, alongside local manufacturing capability in base oil refining, additive blending, formulation development, packaging, and downstream distribution networks, as well as procurement structures across OEM approvals, industrial supply contracts, distributors, workshops, dealerships, fleet operators, and aftermarket retail channels?

- In what ways are raw material and energy price volatility and lead-time constraints for base oils, synthetic stocks, additive packages, viscosity modifiers, detergents, dispersants, anti-wear agents, antioxidants, corrosion inhibitors, packaging materials, and petrochemical feedstocks influencing production costs, pricing strategies, supplier margins, delivery schedules, and profitability, especially for full-synthetic lubricants, high-performance industrial oils, low-viscosity EV-compatible fluids, food-grade lubricants, and environmentally acceptable / bio-based lubricant formulations?

- Who are the leading global and regional lubricant manufacturers, base oil suppliers, additive companies, private-label producers, and distribution partners, and how do they benchmark across product performance, drain interval capability, thermal and oxidation stability, wear protection, fuel-economy benefits, OEM approvals, sustainability profile, regulatory compliance, price competitiveness, brand strength, and portfolio breadth, across standalone lubricant supply versus value-added offerings such as oil condition monitoring, fluid management, technical training, predictive maintenance support, used oil analysis, inventory management, and equipment reliability services?

- What strategic insights emerge from primary discussions with lubricant manufacturers, additive suppliers, base oil refiners, OEMs, industrial end users, fleet operators, distributors, workshops, and aftermarket participants regarding demand shifts toward synthetic lubricants, longer drain intervals, EV and hybrid-specific fluids, low-emission formulations, food-grade and biodegradable lubricants, and digitally enabled lubrication management, along with key purchase criteria such as price competitiveness, product performance, OEM approval status, supply reliability, energy-efficiency benefits, equipment protection, drain interval optimization, and technical service support?

- Market Foundations & Dynamics

- Product Overview

- Research Methodology

- Executive Summary

- Market Dynamics (Drivers, Restraints, Opportunities, Challenges, Porter’s Five Forces Analysis, PESTLE Analysis)

- Market Ecosystem & Value Chain

- Overview of Value Chain Participants

- Flow of Value and Material Through the Chain

- Value Addition and Margins at Each Stage

- Market Trends & Developments

- Emerging Base Oil & Additive Trends

- Raw Material Availability

- Technological Advancements

- Demand–Supply Gaps

- Investment Hotspots

- Unmet Needs and White Market Spaces

- Risk Assessment Framework

- Political / Geopolitical Risk

- Raw Material Supply Risk (Crude Oil, Base Oil, Additives)

- Environmental and Regulatory Risk

- Financial / Market Risk

- Regulatory Framework & Standards

- Global Policy and Mandate Overview

- Transportation, Storage and Handling Regulations

- Sustainability and GHG Reduction Standards

- Environmental & Liability Considerations

- Technology Landscape

- Overview of Lubricant Technologies

- Cost Optimization Technologies

- Future Outlook

- Global Lubricants Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume

- Market Size & Forecast by Product Type

- Mineral Oil-Based Lubricants

- Synthetic Lubricants

- PAO (Polyalphaolefin)

- PAG (Polyalkylene Glycol)

- Esters (Diester, Polyol Ester)

- Silicone-Based Lubricants

- Other Synthetic Lubricants

- Semi-Synthetic Lubricants

- Bio-based / Biolubricants

- Re-refined / Recycled Lubricants

- Market Size & Forecast by Base Oil Group

- Group I

- Group II

- Group II+

- Group III

- Group IV (PAO)

- Group V (Others)

- Market Size & Forecast by Additive Type

- Viscosity Index Improvers

- Antiwear & Extreme Pressure Additives

- Antioxidants

- Detergents & Dispersants

- Corrosion Inhibitors

- Pour Point Depressants

- Friction Modifiers

- Emulsifiers & Demulsifiers

- Other Additives

- Market Size & Forecast by Form

- Liquid Lubricants

- Grease

- Solid / Dry Film Lubricants

- Aerosol / Spray Lubricants

- Market Size & Forecast by Viscosity Grade

- SAE 0W / 5W / 10W Series (Automotive)

- SAE 15W / 20W / 30W Series (Automotive)

- SAE 40 / 50 / 60 Series (Automotive)

- ISO VG Grades (Industrial)

- NLGI Grades (Grease)

- Market Size & Forecast by Application

- Automotive Lubricants

- Engine Oils (Passenger Cars)

- Engine Oils (Commercial Vehicles)

- Transmission & Gear Fluids

- Brake Fluids

- Greases (Automotive)

- Industrial Lubricants

- Hydraulic Fluids

- Compressor Oils

- Turbine Oils

- Industrial Gear Oils

- Metalworking Fluids

- Process Oils

- Marine Lubricants

- Aviation Lubricants

- Other Applications

- Automotive Lubricants

- Market Size & Forecast by End Use Industry

- Automotive & Transportation

- Manufacturing & Machinery

- Power Generation

- Mining & Quarrying

- Marine & Shipping

- Aerospace & Defence

- Food & Beverage Processing

- Agriculture

- Construction

- Market Size & Forecast by Sales Channel

- Direct Sales / OEM Channel

- Distributors / Traders

- Retail (Automotive Parts Stores)

- Online Platforms

- Asia-Pacific Lubricants Market Outlook

- Market Size & Forecast

- By Value & Volume

- By Product Type

- By Base Oil Group

- By Additive Type

- By Form

- By Viscosity Grade

- By Application

- By End Use Industry

- By Sales Channel

- Market Size & Forecast

- Europe Lubricants Market Outlook

- Market Size & Forecast

- By Value & Volume

- By Product Type

- By Base Oil Group

- By Additive Type

- By Form

- By Viscosity Grade

- By Application

- By End Use Industry

- By Sales Channel

- Market Size & Forecast

- North America Lubricants Market Outlook

- Market Size & Forecast

- By Value & Volume

- By Product Type

- By Base Oil Group

- By Additive Type

- By Form

- By Viscosity Grade

- By Application

- By End Use Industry

- By Sales Channel

- Market Size & Forecast

- Latin America Lubricants Market Outlook

- Market Size & Forecast

- By Value & Volume

- By Product Type

- By Base Oil Group

- By Additive Type

- By Form

- By Viscosity Grade

- By Application

- By End Use Industry

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Lubricants Market Outlook

- Market Size & Forecast

- By Value & Volume

- By Product Type

- By Base Oil Group

- By Additive Type

- By Form

- By Viscosity Grade

- By Application

- By End Use Industry

- By Sales Channel

- Market Size & Forecast

- Country-wise Lubricants Market Outlook

- Market Size & Forecast

- By Value & Volume

- By Product Type

- By Base Oil Group

- By Additive Type

- By Form

- By Viscosity Grade

- By Application

- By End Use Industry

- By Sales Channel

- Market Size & Forecast

- Countries Analyzed in the Research Portfolio: China, United States, Germany, Saudi Arabia, Russia, India, Japan, South Korea, United Kingdom, France, Canada, Brazil, Australia, UAE, Indonesia, Malaysia, Thailand, Turkey, Italy, Spain, Mexico, Singapore, Netherlands, Poland, South Africa, Argentina, Nigeria, Egypt, Vietnam, Belgium

- Pricing Analysis

- Global Average Selling Price Trend

- Pricing Analysis by Product Type

- Pricing Analysis by Application

- Pricing Analysis by Region

- Pricing Strategies of Major Players

- Sustainability Premium and Green Lubricant Pricing

- Raw Material Price Impact on Lubricant Margins

- Raw Material Price Impact Analysis

- Overview of Raw Material Inputs

- Crude Oil and Base Oil Refining Feedstocks

- Base Oil Supply Chain and Group-wise Availability

- Additive Chemistry and Key Raw Material Inputs

- Supply Concentration Risk and Geopolitical Exposure

- Used Oil Re-refining as an Alternative Raw Material Source

- Raw Material Price Trend Analysis

- Strategic Raw Material Management

- Competition Outlook

- Market Concentration and Fragmentation Level

- Market Concentration and Fragmentation Level

- Global Market Concentration: HHI Index and Top-20 Producer Share

- Dual-Layer Structure: Integrated Majors vs. Regional Blenders and Independents

- Segment-Level Concentration: Automotive vs. Industrial vs. Marine vs. Aviation

- Geographic Concentration by Region: Market Share of Top Players per Country

- Private Label and Retailer-Own Brand Market Share in Consumer Automotive Segment

- Company Market Shares (Top 20 Producers)

- Business Overview, Revenue, Lubricant Revenue Share, and Blending Capacity

- Product Portfolio Breadth and OEM Approval Coverage

- Geographic Presence and Key Market Strongholds

- Base Oil Integration Level and Supply Chain Strategy

- R&D Investment, Patent Portfolio, and Innovation Pipeline

- Recent Strategic Initiatives, M&A Activity, and Capacity Expansions

- SWOT Analysis for Each Profiled Company

- Competitive Strategies

- OEM Approval Management as Primary Automotive Market Entry and Retention Strategy

- Total Cost of Ownership (TCO) Positioning in Industrial Lubricant Segments

- Brand Investment and Motorsport Association for Consumer Market Premium Positioning

- Geographic Expansion Through Acquisitions and Joint Ventures in Asia and Africa

- EV Fluid Co-Development Partnerships with Automotive OEMs and Battery Makers

- Digital Commerce and Direct-to-Consumer Channel Development

- Sustainability and Circular Economy Credentials as Competitive Differentiators

- Benchmarking Matrix

- Product Portfolio Breadth and Application Coverage Scoring

- OEM Approval Portfolio Depth: ACEA, API, OEM-Specific Specifications

- Base Oil Integration Level and Raw Material Cost Advantage

- Technical Service Organisation Depth: Field Engineers, Application Labs, Oil Analysis

- Geographic Distribution Network Reach: Blending Plants and Distributor Coverage

- Brand Strength and Consumer Recognition Index

- Innovation and R&D Investment Intensity (R&D as % of Revenue)

- Sustainability Credentials: Bio-Content, Re-refined Integration, Carbon Commitments

- Recent Developments: Partnerships, M&A, and Policy-Driven Expansions

- Major M&A Transactions in Lubricants (2020–2025): Acquirer, Target, Rationale, Value

- OEM Co-Development Partnerships for EV Fluids and Next-Generation Automotive Lubricants

- Capacity Expansion Announcements: New Blending Plants and Refinery Upgrades

- Chinese Producer International Expansion: Distribution Partnerships and Brand Development

- Indian Lubricant Industry Consolidation: Domestic M&A and Capacity Investment

- Re-refining and Used Oil Infrastructure Investment by Major Producers

- Bio-Lubricant and Sustainable Fluid Development Partnerships and Pilot Programs

- Sales & Distribution Channel Analysis

- Overview of Go-to-Market Channels

- Channel Share by Region

- Distribution Strategies by Leading Players

- Strategic Recommendations & Roadmap

- Competitors’ Strategic Initiatives

- Future Outlook (Next 5–10 Years, Emerging Players, Success Factors)

- Strategic Recommendations

- Market Acceleration Roadmap

- Short-Term

- Mid-Term

- Long-Term

- Tailored Recommendations for:

- Lubricant Producers

- Base Oil & Additive Suppliers

- Policymakers / Regulators

- Recommendations on Key Success Factors

- Base Oil & Additive Security

- Regulatory & Sustainability Alignment

- Supply Chain Integration

- Market Acceleration Roadmap