Market Definition

The Methylene Diphenyl Diisocyanate (MDI) market refers to the global industrial sector involved in the production, distribution, and application of a critical aromatic diisocyanate used primarily as a core building block in the manufacture of polyurethanes. The market is structurally divided into three primary chemical forms: Polymeric MDI (p-MDI), which is the dominant segment used for rigid thermal insulation foams; Monomeric MDI (m-MDI), utilized for high-performance elastomers, sealants, and coatings; and Modified MDI, tailored for specialized flexible foam and adhesive applications. As a fundamental component in the reactive chemistry of polyurethanes, MDI is indispensable across high-growth industries including construction, where it provides superior energy efficiency through insulation, automotive, refrigeration, and consumer goods. The market’s dynamics are heavily influenced by the global transition toward sustainable building standards, the increasing demand for lightweight materials in transportation, and the ongoing shift toward higher-purity grades required for advanced specialty applications.

Global MDI Market Insights

As of early 2026, the global Methylene Diphenyl Diisocyanate (MDI) market is valued at approximately USD 31.7 billion, moving through a period of steady stabilization with a projected compound annual growth rate (CAGR) of 5.8% to 6.2% through 2033. The market structure remains highly concentrated, dominated by a small group of super-majors, including Wanhua Chemical, BASF, Covestro, Huntsman, and Dow, who collectively control over 70% of global production capacity. Polymeric MDI continues to be the primary product segment, accounting for roughly 83% of consumption due to its critical role in rigid polyurethane foam production. While the industry faced a period of sluggish demand in mature markets throughout 2025, the underlying fundamentals remain robust, driven by the global transition toward net-zero construction standards and the rapid scaling of cold-chain logistics in emerging economies.

Current Producing Countries and Regional Concentration

China remains the undisputed epicenter of the MDI industry, serving as both the largest producer and consumer, supported by a vertically integrated polyurethane supply chain and massive domestic demand for construction insulation and appliance manufacturing. Behind China, the United States, Germany, and Japan maintain significant production hubs, characterized by advanced specialty MDI grades and high-purity monomeric MDI for technical elastomers. Asia-Pacific as a whole accounts for nearly 55% of global output, a share that is expected to expand as major players add capacity in India and Southeast Asia to capitalize on lower land and labor costs. Other notable contributors include South Korea, Mexico, and Brazil, which are increasingly positioned as regional assembly points for the automotive and furniture sectors.

Current and Emerging Production Technologies

The current industrial standard for MDI production is almost exclusively based on the phosgenation process, specifically the liquid-phase direct phosgenation method, which involves the reaction of methylene diphenyl diamine (MDA) with phosgene. While highly efficient, this method carries significant safety risks due to the toxicity of phosgene, prompting a shift toward Next-Gen manufacturing. Emerging technologies currently entering the pilot and early commercial stages focus on phosgene-free (non-phosgene) routes, such as the synthesis of carbamates using dimethyl carbonate (DMC). Additionally, 2026 has seen the rise of Digital Twin integration and AI-led reactor optimization, which have demonstrated the potential to increase yields by 30% while reducing energy consumption through more precise catalytic control and electrochemical synthesis.

Key Market Drivers and Challenges

The primary catalyst for the MDI market is the aggressive global push for energy efficiency; over 70 countries now have mandatory building codes that structurally favor MDI-based rigid foam insulation over traditional materials like fiberglass. Furthermore, the automotive industry’s pivot to electric vehicles is driving demand for lightweight, high-strength polyurethane components to offset battery mass. However, the industry faces formidable challenges, most notably extreme capital intensity, where a single world-scale plant can require investments exceeding USD 2 billion, and the persistent volatility of feedstock prices like benzene and aniline. Manufacturers must also navigate a tightening regulatory environment, with strict REACH and OSHA standards in Europe and North America requiring significant investments in low-VOC formulations and advanced emission-control systems.

Market Hotspots and Opportunity Analysis

The most significant hotspots for growth through 2031 are concentrated in the Asia-Pacific region and South America, where rapid urbanization and government-led infrastructure projects are creating massive demand for energy-efficient housing. A major emerging opportunity lies in the Bio-based MDI segment, which is currently witnessing a CAGR of 18% as consumer preferences and dual carbon mandates shift toward renewable biomass raw materials. Additionally, the rise of the circular economy is opening new niches for recycled polyurethane and chemical recycling technologies, allowing manufacturers to close the loop on waste. For strategic investors, the integration of MDI into advanced electronics and smart automotive interiors represents a high-margin frontier that balances the commoditized volume of the rigid foam construction market.

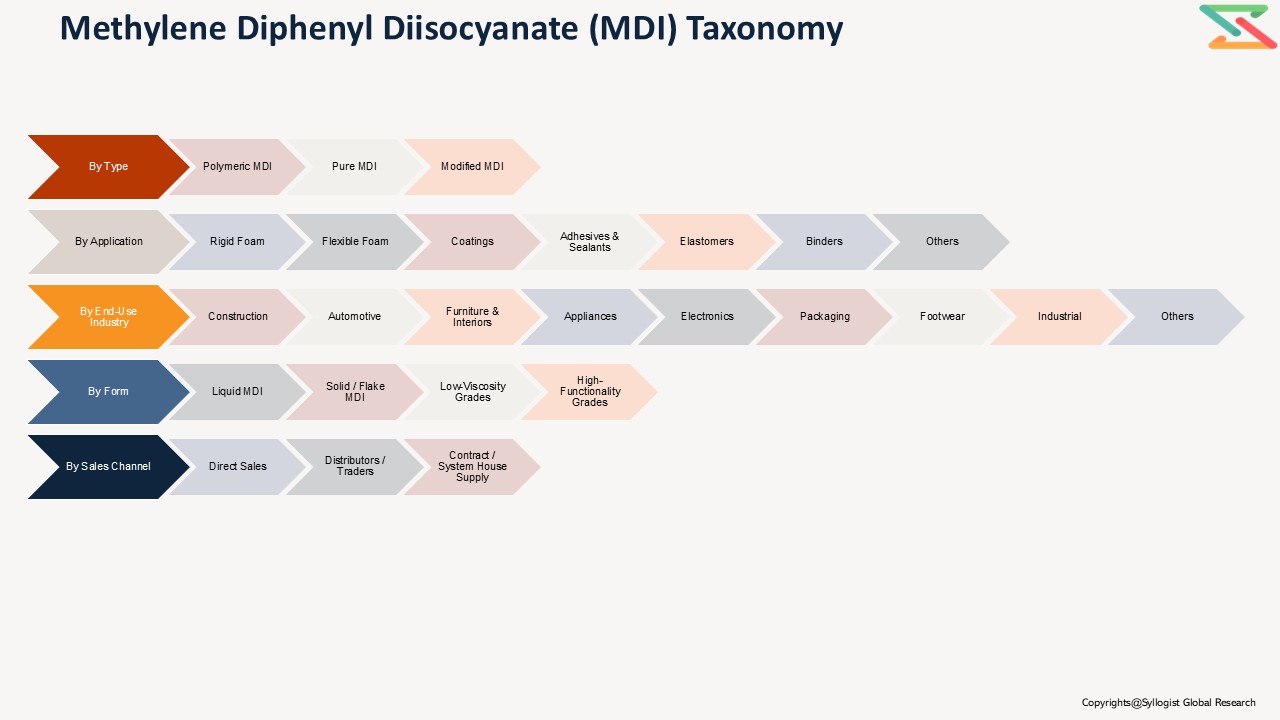

Market Segmentation

- Segmentation By Type

- Polymeric MDI

- Pure MDI

- Modified MDI

- Segmentation By Application

- Rigid Foam

- Flexible Foam

- Coatings

- Adhesives & Sealants

- Elastomers

- Binders

- Others

- Segmentation By End Use Industry

- Construction

- Automotive

- Furniture & Interiors

- Appliances

- Electronics

- Packaging

- Footwear

- Industrial

- Others

- Segmentation By Form

- Liquid MDI

- Solid / Flake MDI

- Low-Viscosity Grades

- High-Functionality Grades

- Segmentation By Sales Channel

- Direct Sales

- Distributors / Traders

- Contract / System House Supply

- Introduction (Product Definition, Taxonomy and Research Methodology)

- Executive Summary

- Global Methylene Diphenyl Diisocyanate (MDI) Demand Supply Analysis

- Global Methylene Diphenyl Diisocyanate (MDI) Market Assessment, 2021-2036

- Market Size & Forecast by Value

- Market Size & Forecast by Volume

- Market Size & Forecast by Type

- Polymeric MDI

- Pure MDI

- Modified MDI

- Market Size & Forecast by Application

- Rigid Foam

- Flexible Foam

- Coatings

- Adhesives & Sealants

- Elastomers

- Binders

- Others

- Market Size & Forecast by End Use Industry

- Construction

- Automotive

- Furniture & Interiors

- Appliances

- Electronics

- Packaging

- Footwear

- Industrial

- Others

- Market Size & Forecast by Form

- Liquid MDI

- Solid / Flake MDI

- Low-Viscosity Grades

- High-Functionality Grades

- Market Size & Forecast by Sales Channel

- Direct Sales

- Distributors / Traders

- Contract / System House Supply

- Asia-Pacific Methylene Diphenyl Diisocyanate (MDI) Market Assessment, 2021-2036

- Market Size & Forecast

- By Value

By Volume - By Type

- By Application

- By End Use Industry

- By Form

- By Sales Channel

- By Country (Market Share of Leading 5-6 Countries)

- By Value

- Market Size & Forecast

- North America Methylene Diphenyl Diisocyanate (MDI) Market Assessment, 2021-2036

- Market Size & Forecast

- By Value

By Volume - By Type

- By Application

- By End Use Industry

- By Form

- By Sales Channel

- By Country (Market Share of Leading 5-6 Countries)

- By Value

- Market Size & Forecast

- Europe Methylene Diphenyl Diisocyanate (MDI) Market Assessment, 2021-2036

- Market Size & Forecast

- By Value

By Volume - By Type

- By Application

- By End Use Industry

- By Form

- By Sales Channel

- By Country (Market Share of Leading 5-6 Countries)

- By Value

- Market Size & Forecast

- South America Methylene Diphenyl Diisocyanate (MDI) Market Assessment, 2021-2036

- Market Size & Forecast

- By Value

By Volume - By Type

- By Application

- By End Use Industry

- By Form

- By Sales Channel

- By Country (Market Share of Leading 5-6 Countries)

- By Value

- Market Size & Forecast

- Middle East & Africa Methylene Diphenyl Diisocyanate (MDI) Market Assessment, 2021-2036

- Market Size & Forecast

- By Value

By Volume - By Type

- By Application

- By End Use Industry

- By Form

- By Sales Channel

- By Country (Market Share of Leading 5-6 Countries)

- By Value

- Market Size & Forecast

- White Space & Emerging Investment Hotspot

- Market White Space Opportunities

- Mergers & Acquisitions (M&A)

- Joint Ventures & Strategic Alliances

- Technology & Innovation Hotspots

- Regional Investment Attractiveness

- Barriers & Risks in Investment

- Value Chain Analysis

- Raw Material Sourcing & Suppliers

- Key Raw Materials & Inputs

- Supplier Landscape & Concentration

- Pricing Trends & Volatility

- Dependence on Imports vs Domestic Availability

- Distribution & Logistics

- Marketing & Sales Channels

- Value Addition & Profitability across Chain

- Emerging Trends & Disruptions

- Raw Material Sourcing & Suppliers

- Pricing Analysis

- Historical Vs Projected Pricing Analysis

- Demand-Supply Impact on Prices

- Application-wise Pricing Differences

- Impact of Tariffs, Taxes, and Trade Policies

- Key Player Pricing Strategies

- Technology Landscape

- Key Existing Technologies

- Emerging & Next-gen Technologies

- Strategic Insights

- Future Technology Roadmap

- Opportunities for Differentiation via Technology

- Risks of Obsolescence & Barriers to Adoption

- Policy & Regulatory landscape

- Competition Outlook (Leading 10 Companies)

- Competition Benchmarking

- Market Leaders Vs New Entrants

- Strategic Recommendations