Market Definition

The Global Neuromorphic AI Chips Market encompasses the research, design, fabrication, and commercial deployment of integrated circuits and semiconductor architectures that replicate the structural and functional operating principles of biological neural systems, including the parallel event-driven processing of spiking neural networks, spike-timing-dependent plasticity-based on-chip learning, co-located memory and computation to eliminate the von Neumann bottleneck, and ultra-low-power asynchronous circuit operation, to deliver artificial intelligence inference and learning workloads at energy efficiencies and latency profiles that are fundamentally unachievable by conventional graphics processing unit and digital signal processor architectures operating on rate-coded neural network models. The product scope of this market includes dedicated neuromorphic processor integrated circuits implementing large-scale spiking neural network cores with configurable synaptic connectivity matrices, neuromorphic system-on-chip platforms integrating spiking neural network engines with conventional processor subsystems and sensor interface circuitry, mixed-signal neuromorphic devices incorporating analog subthreshold circuit elements that directly emulate membrane potential dynamics and synaptic weight modulation in biological neurons, in-memory computing architectures using resistive random-access memory, phase-change memory, or ferroelectric memory crossbar arrays as the physical substrate for synaptic weight storage and multiply-accumulate computation, neuromorphic development kits and evaluation platforms enabling algorithm and application development on neuromorphic hardware, neuromorphic co-processor modules designed for integration with edge computing and embedded system platforms, and the software development toolchains, spiking neural network compilers, neuromorphic simulation environments, and application programming interfaces that constitute the enabling software ecosystem without which neuromorphic hardware cannot be programmed, benchmarked, or deployed in end-user applications. The application landscape of this market spans always-on sensor processing and keyword spotting in consumer electronics, real-time gesture and facial expression recognition, robotic sensorimotor control and proprioception processing, autonomous vehicle perception pipeline acceleration at the sensor edge, industrial predictive maintenance through continuous vibration and acoustic signal pattern analysis, brain-machine interface signal decoding in medical neurotechnology devices, radar and lidar point cloud processing in defense surveillance systems, and scientific simulation of large-scale biological neural circuits in computational neuroscience research. The value chain extends from compound semiconductor material suppliers and specialized fabrication foundries through integrated device manufacturers with proprietary neuromorphic process nodes, fabless neuromorphic chip design companies, electronic design automation toolchain providers, neuromorphic algorithm and application software developers, system integration and module assembly specialists, and the original equipment manufacturer and government procurement channels that deliver neuromorphic computing capability into end-system deployments across commercial, defense, and research applications globally.

Market Insights

The global neuromorphic AI chips market is at an inflection point in its commercial development trajectory in 2026, transitioning from a primarily research-driven technology exploration phase toward an early commercial deployment phase characterized by the first production-volume design wins in edge AI inference applications, growing enterprise and government procurement of neuromorphic development systems for application pipeline construction, and the emergence of a nascent competitive ecosystem of dedicated neuromorphic chip companies offering commercially supported product families to system integrators and original equipment manufacturers. The market was valued at approximately USD 27 billion in 2025 and is projected to expand at a compound annual growth rate of 67 percent through 2036, reflecting the structural demand pressure created by the unsustainable energy consumption trajectory of conventional deep learning accelerator architectures and the demonstrated capability of neuromorphic spiking neural network processors to deliver equivalent or superior inference accuracy on sparse temporal data types at power consumption levels measured in milliwatts rather than the tens to hundreds of watts characteristic of graphics processing unit inference engines. The competitive structure of the market encompasses a small number of large semiconductor corporations that have sustained multi-year neuromorphic research programs and have transitioned initial architectures into commercially available products, a growing cohort of venture-backed neuromorphic chip startups delivering application-specific spiking neural network processors targeting defined vertical markets, national and international research institutions operating large-scale neuromorphic computing platforms as scientific infrastructure for the computational neuroscience and AI research communities, and defense research agencies whose investment programs in neuromorphic computing for autonomous systems and signal processing applications are providing a significant portion of the non-dilutive funding sustaining early-stage commercial development in the sector.

A defining architectural and commercial development reshaping the competitive positioning within the neuromorphic AI chips market is the progressive maturation and diversification of large-scale spiking neural network processor platforms from first-generation academic demonstrators into second and third-generation commercial architectures characterized by substantially increased neuron and synapse counts per chip, configurable inter-chip communication fabrics enabling scalable multi-chip neuromorphic computing systems, support for a broader repertoire of learning rules beyond spike-timing-dependent plasticity including reward-modulated plasticity and structural plasticity algorithms relevant to reinforcement learning applications, and the availability of application-level software abstractions that enable algorithm developers without deep neuromorphic hardware expertise to map trained spiking neural network models onto neuromorphic processor substrates. The progression to wafer-scale and chiplet-based neuromorphic architectures is enabling neuron counts per system that are approaching the scale of small mammalian brain regions, crossing a threshold of biological relevance that is attracting increasing interest from computational neuroscience institutions seeking hardware platforms capable of running mechanistic brain simulation models at timescales relevant to experimental neuroscience research. The parallel development of mixed-signal neuromorphic architectures, which implement neuron and synapse dynamics using analog subthreshold circuits that achieve the most energy-efficient per-synaptic-operation figures available in any semiconductor technology but at the cost of reduced programmability and greater sensitivity to process variation and temperature, is generating a technology differentiation axis within the market between maximum energy efficiency for fixed-application deployment and maximum programmability for research and application development contexts, with commercial product strategies increasingly converging on heterogeneous designs that combine analog neuromorphic cores for energy-critical inference workloads with digital spiking neural network engines for programmable learning and adaptation tasks.

The in-memory computing segment of the neuromorphic AI chips market, which encompasses crossbar array architectures using emerging non-volatile memory technologies as the physical implementation substrate for synaptic weight matrices, is attracting substantial research and early commercial investment as the most direct hardware analog of biological synaptic weight storage and as a compelling solution to the memory bandwidth bottleneck that limits the energy efficiency of conventional digital neural network accelerator architectures. Resistive random-access memory crossbar arrays enable multiply-accumulate operations, the dominant arithmetic primitive in neural network inference, to be executed in the analog domain at the physical location of weight storage, eliminating the repeated data movement between separate memory and compute units that accounts for the majority of energy consumption in conventional digital accelerator designs and enabling inference energy efficiencies that approach theoretical physical limits for the matrix-vector multiplication operations that constitute the core computational workload of deep neural networks. The commercial development of in-memory computing neuromorphic products is being pursued by both dedicated startups and the research divisions of major semiconductor corporations, with prototype demonstrations showing inference energy efficiencies several orders of magnitude superior to digital graphics processing unit implementations on benchmark neural network workloads, and with the primary technical challenges remaining in the areas of device-to-device variability compensation, write endurance for on-chip learning applications, and the development of training methodologies that account for the analog weight precision constraints and non-ideal device characteristics of physical crossbar array implementations. The convergence of in-memory computing with spiking neural network computational models in hybrid neuromorphic architectures is emerging as a particularly promising design direction that combines the temporal sparsity and event-driven processing advantages of spiking neural networks with the energy-efficient weight storage and matrix computation capabilities of resistive random-access memory crossbar arrays.

From a regional investment and commercialization perspective, North America leads the global neuromorphic AI chips market in terms of foundational intellectual property concentration, venture capital investment volume, and the depth of the research institution ecosystem sustaining neuromorphic computing science, with United States defense research agencies constituting the single largest source of sustained public funding for neuromorphic hardware development programs targeting autonomous systems, signals intelligence, and electronic warfare applications where the energy efficiency and real-time adaptive processing capabilities of neuromorphic architectures address specific operational requirements that conventional computing platforms cannot satisfy within acceptable size, weight, and power constraints. Europe represents the most significant geography for publicly coordinated neuromorphic computing research infrastructure investment, with large-scale neuromorphic computing platforms operated as open-access scientific infrastructure providing the computational neuroscience and AI research communities with the hardware resources needed to advance both the scientific understanding of neural computation and the practical development of neuromorphic algorithm methodologies that will underpin future commercial applications. Asia-Pacific, led by China, Japan, and South Korea, is the fastest-growing region for neuromorphic chip investment and commercialization activity, with Chinese national semiconductor policy frameworks identifying neuromorphic computing as a strategic technology priority and supporting both state-funded research programs at leading universities and commercial development initiatives at domestic semiconductor companies seeking to establish competitive positions in next-generation AI chip architectures before the technology reaches the mass commercialization phase where competitive differentiation becomes more difficult. The significant concentration of consumer electronics, robotics, industrial automation, and telecommunications original equipment manufacturers in Asia-Pacific is simultaneously generating a substantial near-term application pull for neuromorphic edge AI solutions in the region that is attracting commercial development focus from both domestic and international neuromorphic chip suppliers.

Key Drivers

Escalating Energy Consumption Crisis in Conventional AI Computing Infrastructure and the Structural Demand for Ultra-Low-Power Edge Inference Alternatives

The most powerful and structurally durable commercial demand driver for neuromorphic AI chip technology is the rapidly intensifying energy consumption crisis created by the exponential scaling of artificial intelligence model complexity and inference deployment volume on conventional graphics processing unit and tensor processing unit architectures, a crisis that is manifesting in the form of unsustainable data center power demand growth, the practical infeasibility of deploying large AI models on battery-powered edge devices within acceptable power envelopes, and the mounting environmental and economic pressure on hyperscale technology operators to identify fundamentally more energy-efficient computing paradigms for AI workload execution. The energy consumption of training and deploying large-scale transformer-based language models on conventional accelerator hardware has grown at a rate that substantially outpaces improvements in semiconductor process technology energy efficiency, creating a widening gap between the AI capabilities that enterprises and developers wish to deploy and the energy budgets within which those deployments must operate, particularly at the edge where battery capacity and thermal constraints impose absolute power ceilings that conventional AI accelerators exceed by orders of magnitude for non-trivial inference workloads. Neuromorphic spiking neural network processors address this energy gap through a combination of architectural principles that collectively reduce the energy cost of neural network inference by factors ranging from ten to several thousand times relative to equivalent graphics processing unit implementations on appropriate workload classes, including event-driven computation that consumes power only when and where neural activity occurs rather than clocking all processing elements continuously, sparse binary spike communication between neurons that eliminates the high-precision floating-point arithmetic and associated power consumption of rate-coded neural network models, and co-located memory and computation that eliminates the dominant energy cost in conventional accelerators associated with repeated weight matrix data movement between off-chip memory and compute units. The alignment between the neuromorphic architecture’s energy efficiency advantages and the specific characteristics of always-on sensor processing workloads at the edge, including the temporal sparsity, event-driven nature, and modest accuracy requirements of keyword spotting, gesture recognition, and anomaly detection applications, is creating an initial commercial beachhead for neuromorphic processors in edge AI applications that is expected to expand progressively as the software ecosystem matures and the range of application workloads demonstrably addressable by spiking neural network models broadens through continued research investment.

Growing Adoption of Event-Based Sensors and the Emergence of Neuromorphic Sensor-Processor Co-Design as a Disruptive Edge AI Architecture

The accelerating commercial adoption of event-based vision sensors, also known as dynamic vision sensors or silicon retinas, and the parallel development of event-based audio, tactile, and inertial sensors whose output data representations are natively compatible with spiking neural network processing, is creating a structurally important and self-reinforcing demand driver for neuromorphic AI chips by establishing a class of sensor-to-inference processing pipelines in which neuromorphic processors deliver qualitatively superior performance relative to conventional frame-based deep learning approaches and where the competitive case for neuromorphic computing rests on demonstrated application capability rather than energy efficiency arguments alone. Event-based vision sensors output asynchronous streams of pixel-level brightness change events with microsecond temporal resolution, producing a sparse and temporally precise data representation that captures high-speed motion and dynamic scene content with substantially lower data bandwidth and latency than conventional frame-based cameras operating at equivalent effective temporal resolution, and whose native data format is directly compatible with the spike-based input representation of spiking neural network neuromorphic processors without the frame reconstruction and preprocessing steps that are required to adapt event camera data for conventional convolutional neural network inference pipelines. The combination of event-based sensors and neuromorphic processors in co-designed perception systems is demonstrating compelling performance advantages in high-speed robotics applications where the microsecond-latency sensorimotor loop closure enabled by event-driven sensor-processor integration allows manipulation and locomotion control at speeds and precision levels inaccessible to frame-based camera and conventional processor combinations, in drone navigation under high-speed flight conditions where the motion blur immunity of event cameras and the low-latency obstacle avoidance inference capability of neuromorphic processors combine to enable flight envelope extensions beyond what conventional camera-processor perception systems can achieve, and in industrial inspection of high-speed production lines where the temporal resolution advantage of event cameras eliminates the motion blur artifacts that limit the defect detection sensitivity of frame-based machine vision systems. The growing commercial traction of event-based sensor products from multiple suppliers and the expanding research literature demonstrating the application performance advantages of neuromorphic sensor-processor co-design are establishing a technology pull for neuromorphic AI chips that is distinct from and additive to the energy efficiency-driven demand from conventional frame-based AI inference replacement applications.

Key Challenges

Immaturity of the Neuromorphic Software Ecosystem and the Absence of Standardized Programming Frameworks Accessible to Mainstream AI Application Developers

The most consequential near-term commercial challenge limiting the pace of neuromorphic AI chip adoption beyond specialized research and government-funded application domains is the profound immaturity and fragmentation of the software ecosystem supporting neuromorphic hardware programming, algorithm development, and application deployment, which creates a productivity barrier that prevents the large and growing community of mainstream AI application developers trained exclusively on conventional deep learning frameworks from accessing or evaluating neuromorphic hardware for their application development activities without investing prohibitive amounts of time in acquiring neuromorphic-specific algorithm expertise and hardware programming knowledge that has no direct transferable value to conventional computing platforms. The neuromorphic programming ecosystem currently comprises a collection of vendor-specific hardware description languages, spiking neural network simulation frameworks, spike-based learning algorithm libraries, and hardware abstraction interfaces that are architecturally incompatible across different neuromorphic processor platforms, require deep familiarity with spiking neural network dynamics and spike-timing-dependent plasticity learning rules to use effectively, and lack the high-level model definition abstractions, automatic differentiation tools, pre-trained model repositories, and deployment optimization pipelines that have made conventional deep learning frameworks accessible to millions of application developers without specialized hardware knowledge. The absence of a neuromorphic equivalent of the widely adopted deep learning framework ecosystem, which allows conventional AI developers to define, train, and deploy neural network models without understanding the underlying processor microarchitecture, means that neuromorphic hardware adoption currently requires either the rare combination of AI algorithm expertise and neuromorphic hardware knowledge within the same development team, or the engagement of specialized neuromorphic application development consultants whose scarcity and cost substantially elevate the effective barrier to neuromorphic technology evaluation and application prototyping. Addressing this challenge requires coordinated investment from neuromorphic hardware suppliers in software abstraction layer development, open-source spiking neural network framework ecosystems, model conversion tools that translate trained conventional artificial neural networks into spiking neural network equivalents with acceptable accuracy loss, and application-specific software development kits that provide domain-targeted algorithm templates and reference implementations reducing the application development effort required for neuromorphic adoption in defined vertical markets.

Benchmark Performance Comparability Deficit and the Challenge of Demonstrating Neuromorphic Advantage on Standardized AI Workloads Relevant to Commercial Procurement Decisions

A structurally significant commercial challenge constraining enterprise and original equipment manufacturer procurement interest in neuromorphic AI chips is the absence of widely accepted and commercially credible benchmark frameworks that allow neuromorphic processor performance, energy efficiency, and accuracy metrics to be compared against conventional graphics processing unit, neural processing unit, and digital signal processor alternatives on application workloads that are directly relevant to commercial deployment decisions, a gap that creates procurement uncertainty by making it difficult for engineering and procurement organizations to objectively assess the value proposition of neuromorphic hardware relative to incumbent computing platforms without undertaking expensive and time-consuming custom application benchmarking exercises. The fundamental challenge in neuromorphic benchmark development arises from the architectural incompatibility between spiking neural network computational models and the rate-coded deep neural network models that conventional AI benchmark suites such as MLPerf evaluate, making it impossible to directly compare neuromorphic and conventional accelerator performance on identical model implementations and requiring the development of spiking neural network equivalents of benchmark workloads whose accuracy on the target task must be demonstrated to be comparable before the energy and latency comparisons carry commercial credibility. The neuromorphic computing community has not yet converged on a standardized benchmark suite with the institutional endorsement and industry adoption breadth of the MLPerf benchmarks that govern conventional AI accelerator procurement evaluations, leaving individual neuromorphic chip vendors to conduct and publish proprietary benchmark comparisons whose methodology choices, workload selection, and accuracy reporting conventions are not standardized and whose results are consequently viewed with skepticism by procurement engineers accustomed to third-party verified benchmark standards. The commercial consequences of this benchmark comparability deficit are particularly acute in enterprise information technology and industrial automation procurement contexts where engineering investment decisions require objective multi-vendor performance comparison data and where the risk of adopting an insufficiently characterized technology platform carries operational and financial consequences that procurement organizations are institutionally risk-averse toward accepting without robust independent performance validation.

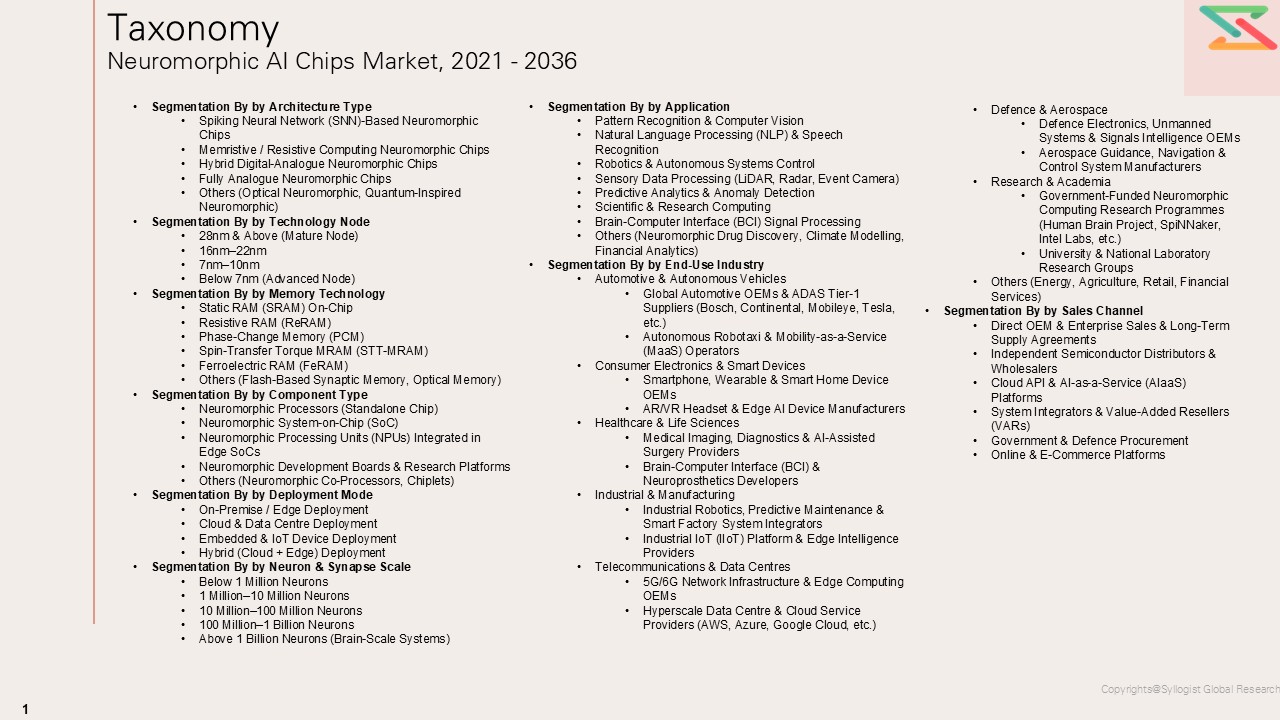

Market Segmentation

- Segmentation By Architecture Type

- Digital Spiking Neural Network Processors

- Analog and Mixed-Signal Neuromorphic Processors

- In-Memory Computing Crossbar Neuromorphic Architectures

- Hybrid Digital-Analog Neuromorphic Processors

- Wafer-Scale Neuromorphic Systems

- Neuromorphic System-on-Chip Platforms

- Others

- Segmentation By Memory Technology

- Static Random-Access Memory (SRAM)-Based Synaptic Arrays

- Resistive Random-Access Memory (ReRAM) Crossbar Arrays

- Phase-Change Memory (PCM) Synaptic Arrays

- Ferroelectric RAM (FeRAM) Synaptic Arrays

- Spin-Transfer Torque MRAM Synaptic Arrays

- Flash-Based Synaptic Storage

- Others

- Segmentation By Neuron Count Per Chip

- Below 1 Million Neurons

- 1 Million to 100 Million Neurons

- 100 Million to 1 Billion Neurons

- Above 1 Billion Neurons

- Segmentation By Application

- Always-On Keyword Spotting and Voice Activity Detection

- Real-Time Gesture and Facial Expression Recognition

- Robotic Sensorimotor Control and Proprioception

- Autonomous Vehicle Perception and Sensor Fusion

- Industrial Predictive Maintenance and Anomaly Detection

- Brain-Machine Interface Signal Decoding

- Radar and Lidar Point Cloud Processing

- Computational Neuroscience Research

- Natural Language and Audio Processing

- Others

- Segmentation By End-Use Industry

- Consumer Electronics

- Robotics and Industrial Automation

- Autonomous Vehicles and Advanced Driver Assistance Systems

- Healthcare and Medical Neurotechnology

- Aerospace and Defense

- Telecommunications and Edge Computing Infrastructure

- Energy Management and Smart Grid

- Scientific and Academic Research

- Others

- Segmentation By Deployment Mode

- Standalone Neuromorphic Processor Chip

- Neuromorphic Co-Processor Module

- Neuromorphic Development Kit and Evaluation Board

- Neuromorphic Computing System and Server

- Cloud-Accessible Neuromorphic Computing Platform

- Others

- Segmentation By Learning Paradigm

- Spike-Timing-Dependent Plasticity (STDP) On-Chip Learning

- Reward-Modulated Plasticity and Reinforcement Learning

- Offline-Trained Spiking Neural Network Inference

- Structural Plasticity and Network Architecture Adaptation

- Hybrid Backpropagation-STDP Training

- Others

- Segmentation By Fabrication Node

- 28 Nanometer and Above

- 14 to 22 Nanometer

- 7 to 12 Nanometer

- Below 7 Nanometer

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2036

Key Questions this Study Will Answer

- What is the projected global market valuation for neuromorphic AI chips through 2036, segmented by architecture type, memory technology, application, end-use industry, and region, and which product categories and geographic markets are expected to generate the highest incremental revenue and unit volume growth across the forecast period?

- How is the maturation of spiking neural network algorithm frameworks and the development of standardized neuromorphic programming interfaces expected to reduce the software ecosystem barrier to neuromorphic hardware adoption, and what milestones in open-source toolchain availability and pre-trained spiking neural network model library development are projected to trigger measurable acceleration in commercial design-in activity among mainstream AI application developers?

- What are the demonstrated energy efficiency and inference latency advantages of leading neuromorphic processor platforms relative to conventional neural processing unit and digital signal processor alternatives on commercially relevant edge AI workloads including keyword spotting, gesture recognition, and anomaly detection, and at what application performance thresholds are neuromorphic processors projected to achieve competitive parity with conventional accelerators on the accuracy metrics required for production deployment in defined vertical markets?

- How is the growing commercial adoption of event-based dynamic vision sensors and other neuromorphic-compatible sensor modalities reshaping the application development pipeline for neuromorphic AI chips in robotics, autonomous systems, and industrial inspection, and which sensor-processor co-design platform combinations are generating the most commercially advanced application demonstrations and design-win pipelines among tier-one system integrators and original equipment manufacturers?

- What is the strategic investment roadmap of leading defense research agencies in neuromorphic computing for autonomous systems, signals intelligence, and electronic warfare applications, and how are government-funded neuromorphic development programs influencing the technology roadmaps, wafer fabrication capacity investments, and commercial product strategies of neuromorphic chip suppliers receiving defense research contracts?

- Who are the leading neuromorphic chip developers, in-memory computing startups, event-based sensor suppliers, and neuromorphic software platform providers currently defining the competitive landscape of the global neuromorphic AI chips market, and what are their respective architecture differentiation strategies, fabrication node roadmaps, application vertical focus areas, and partnership structures for advancing neuromorphic computing from early commercial deployment toward mainstream AI inference adoption through the forecast horizon?

- Product Definition

- Scope of the Study

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Industry Publications, Semiconductor & AI Hardware Manufacturer Reports & Press Releases

- Government Technology, Innovation & Trade Authority Data (DARPA, NSF, EU Horizon, METI, DST, etc.)

- Neuromorphic Chip Shipment, Licensing & Deployment Market Statistics

- OEM Procurement, Data Centre & Edge AI System Supply Chain Databases

- Primary Research Design & Execution

- In-depth Interviews with Neuromorphic Chip Developers, AI Hardware OEM Procurement Heads & System Integrators

- Surveys with AI/ML Workload Operators, Cloud & Edge Computing OEMs, Research Institutions & End-Use Industry Buyers

- Expert Panel Validation

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Bottom-Up & Top-Down Reconciliation

- Wafer Shipment, Device Conversion & System Integration Model for OEM & End-User Demand

- Technology Adoption Curve & AI Hardware Substitution-Driven Market Sizing Model

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Technology & Innovation Highlights

- Manufacturing Economics & Unit Economics Summary

- Average Fab CAPEX & OPEX Benchmarks

- IDM vs Fabless vs Foundry Model Margin & Profitability Analysis

- Spiking Neural Network (SNN) vs Memristive vs Hybrid Architecture Revenue Model Summary

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Geographic & Regional Trends

- Risk Assessment Framework

- Geopolitical & Trade Policy Risk (Export Controls, Chip Supply Chain Restrictions)

- Raw Material & Advanced Node Fabrication Availability Risk (Advanced Logic Process, HBM, Packaging)

- Intellectual Property Litigation & Patent Concentration Risk

- Software Ecosystem Maturity & Developer Adoption Risk

- Competing AI Accelerator Architectures (GPU, TPU, FPGA, PIM) Substitution Risk

- Regulatory, Data Privacy & AI Governance Risk

- End-Market Demand Cyclicality & AI Investment Volatility Risk

- Regulatory Framework & Policy Standards

- Global Neuromorphic AI Chips Market Economics

- Manufacturing Economics & Unit Economics Framework

- Capital Expenditure (CAPEX) Structure

- Operating Expenditure (OPEX) Structure

- Revenue Model & Monetisation Levers (Chip Sales, IP Licensing, Cloud API, Software & Support)

- Capacity Utilisation & Throughput Economics

- Payback Period & Return on Investment (ROI) Analysis

- Total Cost of Ownership vs Competing AI Accelerator Architectures (GPU, TPU, FPGA, Custom ASIC)

- Raw Material & Process Input Cost Analysis

- Advanced Logic Node Process Cost Trends (USD/wafer, 2021–2035)

- Memristive Material (Phase-Change, ReRAM, PCM, STT-MRAM) & Novel Device Input Cost Dynamics

- Silicon Photonics & 3D-IC Integration Input Cost Analysis

- Advanced Packaging (Chiplet, Wafer-Level, CoWoS, SoIC) Cost Structure

- Energy & Cooling Cost Structure in Neuromorphic Chip Fabrication & System Deployment

- High-Bandwidth Memory (HBM) & On-Chip SRAM Integration Cost Economics

- Impact of 3D Stacking & In-Memory Computing Architectures on Product Economics

- System Integration & Deployment Economics

- Edge Device & Embedded System Integration Cost Structure by Application Segment & Geography

- Data Centre Rack-Level & Server Board Integration Economics

- Software Development Kit (SDK), Neuromorphic Framework & Developer Toolchain Economics

- Warranty, Lifecycle Management & Support Service Economics

- Regulatory & Standards Compliance Economics

- AI Safety, Functional Safety & Semiconductor Reliability Standards Compliance Cost Benchmarks (ISO 26262, IEC 61508, AEC-Q100, MIL-STD, etc.)

- Export Control, Data Localisation & AI Governance Compliance Cost Structure

- Environmental Compliance & RoHS / WEEE / REACH Regulation Costs

- Global Neuromorphic AI Chips Market Outlook

- Market Size & Forecast by Value (USD Billion, 2021–2036)

- Market Size & Forecast by Architecture Type

- Spiking Neural Network (SNN)-Based Neuromorphic Chips

- Memristive / Resistive Computing Neuromorphic Chips

- Hybrid Digital-Analogue Neuromorphic Chips

- Fully Analogue Neuromorphic Chips

- Others (Optical Neuromorphic, Quantum-Inspired Neuromorphic)

- Market Size & Forecast by Technology Node

- 28nm & Above (Mature Node)

- 16nm–22nm

- 7nm–10nm

- Below 7nm (Advanced Node)

- Market Size & Forecast by Memory Technology

- Static RAM (SRAM) On-Chip

- Resistive RAM (ReRAM)

- Phase-Change Memory (PCM)

- Spin-Transfer Torque MRAM (STT-MRAM)

- Ferroelectric RAM (FeRAM)

- Others (Flash-Based Synaptic Memory, Optical Memory)

- Market Size & Forecast by Component Type

- Neuromorphic Processors (Standalone Chip)

- Neuromorphic System-on-Chip (SoC)

- Neuromorphic Processing Units (NPUs) Integrated in Edge SoCs

- Neuromorphic Development Boards & Research Platforms

- Others (Neuromorphic Co-Processors, Chiplets)

- Market Size & Forecast by Deployment Mode

- On-Premise / Edge Deployment

- Cloud & Data Centre Deployment

- Embedded & IoT Device Deployment

- Hybrid (Cloud + Edge) Deployment

- Market Size & Forecast by Neuron & Synapse Scale

- Below 1 Million Neurons

- 1 Million–10 Million Neurons

- 10 Million–100 Million Neurons

- 100 Million–1 Billion Neurons

- Above 1 Billion Neurons (Brain-Scale Systems)

- Market Size & Forecast by Application

- Pattern Recognition & Computer Vision

- Natural Language Processing (NLP) & Speech Recognition

- Robotics & Autonomous Systems Control

- Sensory Data Processing (LiDAR, Radar, Event Camera)

- Predictive Analytics & Anomaly Detection

- Scientific & Research Computing

- Brain-Computer Interface (BCI) Signal Processing

- Others (Neuromorphic Drug Discovery, Climate Modelling, Financial Analytics)

- Market Size & Forecast by End-Use Industry

- Automotive & Autonomous Vehicles

- Global Automotive OEMs & ADAS Tier-1 Suppliers (Bosch, Continental, Mobileye, Tesla, etc.)

- Autonomous Robotaxi & Mobility-as-a-Service (MaaS) Operators

- Consumer Electronics & Smart Devices

- Smartphone, Wearable & Smart Home Device OEMs

- AR/VR Headset & Edge AI Device Manufacturers

- Healthcare & Life Sciences

- Medical Imaging, Diagnostics & AI-Assisted Surgery Providers

- Brain-Computer Interface (BCI) & Neuroprosthetics Developers

- Industrial & Manufacturing

- Industrial Robotics, Predictive Maintenance & Smart Factory System Integrators

- Industrial IoT (IIoT) Platform & Edge Intelligence Providers

- Telecommunications & Data Centres

- 5G/6G Network Infrastructure & Edge Computing OEMs

- Hyperscale Data Centre & Cloud Service Providers (AWS, Azure, Google Cloud, etc.)

- Defence & Aerospace

- Defence Electronics, Unmanned Systems & Signals Intelligence OEMs

- Aerospace Guidance, Navigation & Control System Manufacturers

- Research & Academia

- Government-Funded Neuromorphic Computing Research Programmes (Human Brain Project, SpiNNaker, Intel Labs, etc.)

- University & National Laboratory Research Groups

- Others (Energy, Agriculture, Retail, Financial Services)

- Automotive & Autonomous Vehicles

- Market Size & Forecast by Sales Channel

- Direct OEM & Enterprise Sales & Long-Term Supply Agreements

- Independent Semiconductor Distributors & Wholesalers

- Cloud API & AI-as-a-Service (AIaaS) Platforms

- System Integrators & Value-Added Resellers (VARs)

- Government & Defence Procurement

- Online & E-Commerce Platforms

- Asia-Pacific Neuromorphic AI Chips Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Architecture Type

- By Technology Node

- By Memory Technology

- By Component Type

- By Deployment Mode

- By Neuron & Synapse Scale

- By Application

- By End-Use Industry

- By Sales Channel

- Key Demand Drivers (APAC-Specific)

- Competitive Landscape (APAC)

- Europe Neuromorphic AI Chips Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Architecture Type

- By Technology Node

- By Memory Technology

- By Component Type

- By Deployment Mode

- By Neuron & Synapse Scale

- By Application

- By End-Use Industry

- By Sales Channel

- Key Demand Drivers (Europe-Specific)

- Competitive Landscape (Europe)

- North America Neuromorphic AI Chips Market Outlook

- Market Overview & Strategic Importance

- Market Size & Forecast

- By Value (2020–2035)

- By Architecture Type

- By Technology Node

- By Memory Technology

- By Component Type

- By Deployment Mode

- By Neuron & Synapse Scale

- By Application

- By End-Use Industry

- By Sales Channel

- Key Demand Drivers (North America-Specific)

- Competitive Landscape (North America)

- Latin America Neuromorphic AI Chips Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Architecture Type

- By Technology Node

- By Memory Technology

- By Component Type

- By Deployment Mode

- By Neuron & Synapse Scale

- By Application

- By End-Use Industry

- By Sales Channel

- Key Demand Drivers (LATAM-Specific)

- Competitive Landscape (LATAM)

- Middle East & Africa Neuromorphic AI Chips Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Architecture Type

- By Technology Node

- By Memory Technology

- By Component Type

- By Deployment Mode

- By Neuron & Synapse Scale

- By Application

- By End-Use Industry

- By Sales Channel

- Key Demand Drivers (MEA-Specific)

- Competitive Landscape (MEA)

- Country-Wise Neuromorphic AI Chips Market Outlook

- Market Size & Forecast by Country

- By Value

- By Architecture Type

- By Technology Node

- By Memory Technology

- By Component Type

- By Deployment Mode

- By Neuron & Synapse Scale

- By Application

- By End-Use Industry

- By Sales Channel

- Market Size & Forecast by Country

- Market Size & Forecast

- Market Size & Forecast

- Market Size & Forecast

- Market Size & Forecast

- Manufacturing Economics & Unit Economics Framework

Countries Covered: United States, Canada, Germany, France, United Kingdom, Netherlands, Sweden, China, Japan, South Korea, Taiwan, India, Australia, Israel, Singapore, Brazil, UAE, Saudi Arabia, South Africa, South Korea

- Technology Landscape & Innovation Analysis

- Neuromorphic AI Chip Technology Maturity Assessment

- Emerging & Disruptive Technologies in Neuromorphic Computing

- Next-Generation Spiking Neural Network (SNN) Algorithms & Training Methodologies

- In-Memory & Near-Memory Computing Architectures for Neuromorphic Workloads

- 3D-IC, Chiplet & Heterogeneous Integration Technologies for Scalable Neuromorphic Systems

- Neuromorphic Photonics: Optical Spiking Neural Networks & Photonic Synaptic Devices

- Artificial Intelligence (AI) Co-Design: Hardware-Software Co-optimisation for Brain-Inspired Computing

- Technology Readiness & Commercialisation Matrix – Key Neuromorphic AI Chip Technologies

- Patent Landscape Analysis

- R&D Investment Benchmarking

- Value Chain & Supply Chain Analysis

- Neuromorphic AI Chips Value Chain Mapping

- Supply Chain Concentration & Dependency Analysis

- Key Supplier Mapping by Component & Technology Programme

- Advanced Logic Foundry & Process Technology Suppliers (TSMC, Samsung, Intel Foundry, etc.)

- Novel Memory Device & Emerging Material Suppliers

- Advanced Packaging, Testing & Assembly Equipment & Service Providers

- EDA Tool, IP Core & Neuromorphic Framework Software Suppliers

- Supplier Risk Heat Map

- Make vs Buy Strategy Trends Among Neuromorphic Chip Developers & AI Hardware OEMs

- Pricing Analysis

- Neuromorphic AI Chip Pricing Dynamics & Mechanisms

- Pricing by Architecture Type, Technology Node & Neuron Scale

- Total Cost of Ownership (TCO) Analysis – Including Energy Efficiency, Latency, Accuracy & System-Level Savings vs GPU/TPU/FPGA

- IDM vs Fabless vs Foundry Model Pricing Trends & Benchmarks

- Chip Sale vs IP Licensing vs Cloud API Pricing & Value Proposition

- Sustainability & Environmental Stewardship

- Environmental & Sustainability Landscape in Neuromorphic Chip Manufacturing & AI Deployment

- Carbon Footprint & Energy Consumption Benchmarking Across Neuromorphic vs Conventional AI Accelerator Architectures

- Recycled & Sustainable Material Integration Roadmap for Neuromorphic Chip Manufacturers

- End-of-Life, Circular Economy & E-Waste Management Assessment for Neuromorphic AI Hardware

- Ultra-Low Power Neuromorphic Computing’s Contribution to Data Centre & Edge AI Energy Efficiency Goals

- ESG Reporting & Lifecycle Assessment (LCA) in Neuromorphic Chip Operations

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level: Global Semiconductor Leaders vs Deep-Tech Startups & Research Spin-offs

- Top 5 Neuromorphic AI Chip Companies Market Revenue Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis by Architecture & Application Segment

- Competitive Intensity Map by Segment & Region

- Player Classification

- Tier-1 Global Integrated Semiconductor Companies with Neuromorphic Divisions (Intel, IBM, Samsung, Qualcomm, etc.)

- Tier-2 Specialist Neuromorphic AI Chip Fabless Design Houses & Deep-Tech Startups

- Academic Spin-offs, National Research Programme Platforms & Open-Source Neuromorphic Initiatives

- Emerging & Disruptive Players

- Competitive Analysis Frameworks

- Market Share Analysis by Architecture Type, Application & Geography

- R&D Intensity & Chip Pipeline Breadth Benchmarking

- OEM Design-Win Programme, IP Licensing Portfolio & Long-Term Supply Contract Comparison

- Geographic Revenue Exposure & Government Research Programme Funding Comparison

- Company Profiles

- Company Overview, HQ & Organisational Structure

- Neuromorphic AI Chip Products, Architecture & Software Ecosystem Portfolio

- Revenue Breakdown

- Key OEM Design-Win Programmes, Customer Deployments & Research Collaborations

- Manufacturing Footprint & Key Facilities

- Recent Developments (M&A, Partnerships, New Products, Financial Results)

- SWOT Analysis

- Strategic Focus: Architecture Innovation, Software Ecosystem Development, OEM Platform Wins & Government Programme Participation

- Strategic Output

- Market Opportunity Matrix

- High-Value Opportunity Quadrant Analysis

- Addressable Market by Architecture, Application & Region

- Time-to-Revenue Assessment by Opportunity

- White Space Opportunity Analysis

- Underserved Application Segment & End-Use Industry Gaps

- Geographic Markets with Low Neuromorphic AI Chip Penetration

- Technology & Architecture Gaps with High Commercialisation Potential

- Customer Segment Unmet Needs

- Strategic Recommendations

- Product Portfolio & Architecture Innovation Strategy

- Technology Platform & Software Ecosystem Development Strategy

- Manufacturing Footprint & Advanced Node Capacity Strategy

- OEM Design-Win, System Integration & Channel Partner Growth Strategy

- Pricing & Commercial Strategy

- Sustainability & Regulatory Compliance Strategy

- Supply Chain & Advanced Materials Sourcing Strategy

- Partnership, M&A & Expansion Strategy

- Regional Growth Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-Term (2025–2028)

- Mid-Term (2029–2032)

- Long-Term (2033–2036)

- Market Opportunity Matrix

- Market Structure & Concentration