Market Definition

Paints and coatings are engineered surface treatment systems designed to provide protection, decoration, and functional enhancement to substrates including metals, concrete, wood, plastics, composites, glass, and packaging films. At their core, coatings consist of binders (resins), pigments, solvents or water, additives, and performance modifiers that collectively determine film formation, durability, chemical resistance, corrosion protection, and aesthetics.

Unlike commodity chemicals, coatings are performance-critical materials: they are often a small percentage of project cost but disproportionately influence lifecycle durability, corrosion resistance, energy efficiency, and regulatory compliance. The market broadly spans:

- Architectural / Decorative coatings

- Industrial & OEM coatings

- Protective & infrastructure coatings

- Specialty / high-performance functional coatings

The industry is not just about color or surface finish; it is about substrate longevity, compliance, and lifecycle economics.

Market Insights

The global paints and coatings market is increasingly defined by a structural shift from volume-driven growth toward value-driven innovation. Historically, growth was closely tied to construction cycles and automotive production. Today, while those remain core drivers, demand is being reshaped by:

- Sustainability mandates (low VOC, carbon footprint reduction)

- Durability economics (longer maintenance intervals)

- Energy efficiency requirements (cool roofs, reflective coatings)

- Electrification and advanced manufacturing (EV, semiconductors, renewables)

One of the most important structural trends is that coatings are moving from being a “protective layer” to becoming a performance-enabling material. In sectors like EV batteries, wind turbines, hydrogen infrastructure, and data centers, coatings are not optional — they are integral to corrosion resistance, thermal management, EMI shielding, and chemical compatibility.

At the same time, the market is consolidating in terms of technology sophistication but fragmenting in terms of application niches. Large global players dominate architectural and automotive coatings, while specialty high-performance segments are increasingly innovation-led and technical.

Market Dynamics: Structural Drivers

Infrastructure Durability & Asset Life Extension

Governments and asset owners are increasingly focused on extending the lifespan of bridges, ports, water treatment plants, and industrial assets. This is driving demand for:

- Zinc-rich primers

- Epoxy novolac linings

- Polysiloxane topcoats

- Chemical-resistant flooring systems

Maintenance cycles are being re-engineered around lifecycle cost, not just upfront price. As infrastructure ages globally, protective coatings are becoming a structural, recurring demand category.

Urbanization & Housing Upgradation

In emerging markets, decorative coatings remain volume-driven, but the mix is shifting toward:

- Premium emulsions

- Washable interior finishes

- Low-odor, low-VOC formulations

- Anti-microbial interior paints

Consumers are increasingly prioritizing air quality and durability over price alone, leading to premiumization even in traditionally cost-sensitive markets.

Automotive Transformation (EV Impact)

The transition to electric vehicles is changing coating demand structurally:

- Fewer engine components → lower demand for certain heat-resistant coatings

- Higher demand for battery pack coatings

- Thermal management coatings

- EMI shielding coatings

- Lightweight material-compatible coatings (aluminum, composites)

Additionally, automotive OEMs are accelerating adoption of:

- Waterborne basecoats

- Powder clearcoats

- Low-energy cure systems

The EV shift is altering not just volumes but the chemistry portfolio of coatings suppliers.

Sustainability & Regulatory Pressure

Environmental compliance is now a core competitive variable.

Major shifts include:

- Rapid conversion to waterborne and powder technologies

- Reduction in VOC and hazardous air pollutants

- Increased use of bio-based resins

- Formaldehyde-free and BPA-NI packaging coatings

Regulation is no longer regional; global supply chains require compliance with the most stringent standards (EU REACH, U.S. EPA, etc.). This is increasing R&D intensity and driving portfolio rationalization.

Market Dynamics: Challenges

Raw Material Volatility

The industry is heavily dependent on:

- Petrochemical-derived resins (epoxy, acrylic, PU)

- Titanium dioxide

- Solvents

- Additives

Feedstock volatility, especially during energy price shocks, directly impacts margins. Pricing power varies significantly by segment — architectural coatings have more pricing flexibility than contract OEM segments.

Technology Disruption & Capital Intensity

Shifts toward:

- Powder coating lines

- UV-curable systems

- High-solids equipment

- Digital color-matching systems

require capex both from manufacturers and applicators. Smaller players may struggle to adapt, accelerating consolidation.

Performance Liability

In protective and infrastructure coatings, performance failure can result in:

- Multi-million-dollar corrosion claims

- Structural damage

- Litigation

This increases the importance of:

- Specification control

- Application method integrity

- Certification & testing

Reputation and technical service capability are critical differentiators.

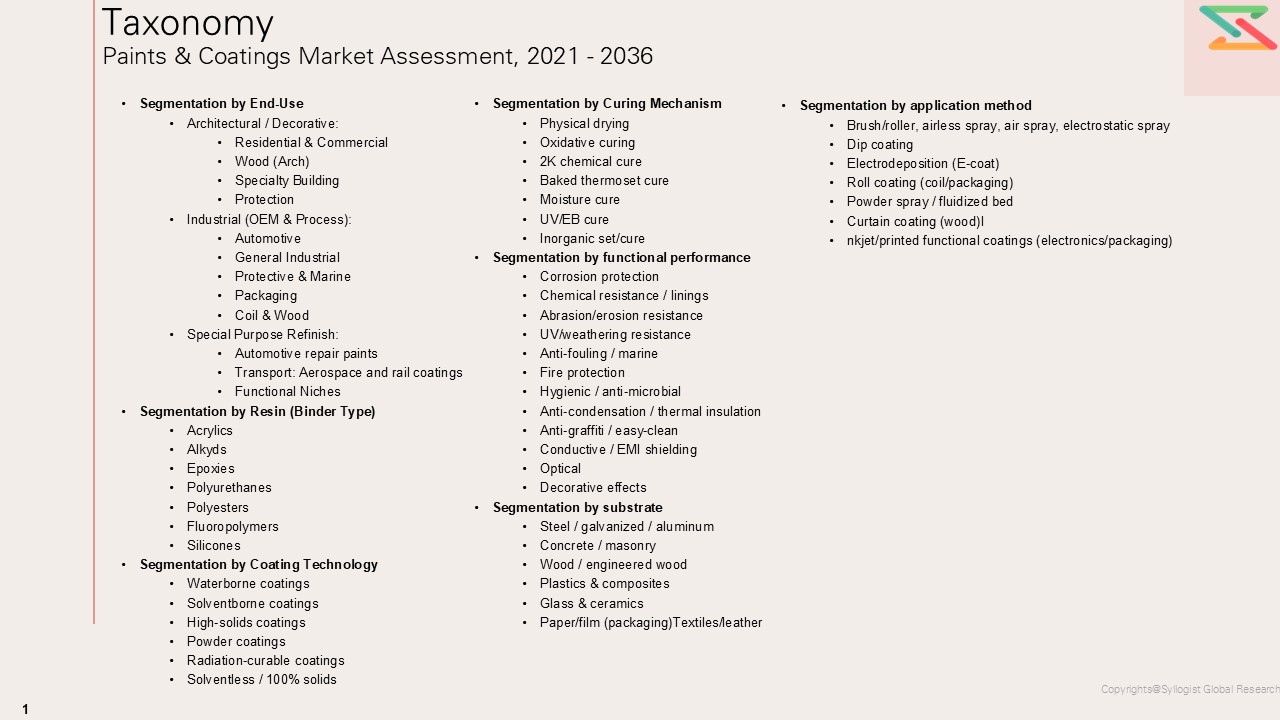

Market Segmentation

- By End Use

- Decorative Coatings

- Interior Wall Paints

- Exterior Wall Paints

- Primers & Sealers

- Wood Coatings (Architectural)

- Metal Paints for Buildings

- Roof Coatings

- Floor Coatings (Light Duty)

- Waterproofing Coatings

- Fire-Retardant Architectural

- Industrial Coatings

- OEM/Factory-Applied Coatings

- Automotive OEM

- Automotive Plastics Coatings

- Appliances (White Goods) Coatings

- General Metal OEM

- Protective / Industrial Maintenance

- Structural Steel & Bridges

- Oil & Gas

- Power & Utilities

- Marine Coatings

- Coil Coatings

- Packaging Coatings

- Wood Industrial (Furniture/Cabinets)

- Concrete Infrastructure

- OEM/Factory-Applied Coatings

- Special Purpose Coatings

- Automotive Refinish (Repair Paints, Clear Coats, Primers)

- Aerospace Coatings

- Rail Coatings

- High-Temperature Coatings

- Anti-Graffiti Coatings

- Anti-Microbial Coatings

- EMI/RFI Shielding Coatings

- Optical/Anti-Reflective Coatings

- Release / Non-Stick Coatings

- Conductive Coatings

- Thermal Barrier / Insulating Coatings

- Reflective Cool Roof Coatings

- Abrasion/Erosion Resistant Coatings

- Radiation/Chemical Resistant Linings

- Traffic/Road Marking Paints

- Textile/Leather Coatings

- By Resin

- Acrylics

- Alkyds

- Epoxies

- Polyurethanes (PU)

- Polyesters

- Vinyls

- Fluoropolymers

- Silicone / Polysiloxanes

- Chlorinated Rubber / Rubber Derivatives

- Phenolic / Amino Resins (Crosslinkers)

- Inorganic Binders

- By Coating Technology

- Waterborne Coatings

- Solvent borne Coatings

- High-Solids Coatings

- Powder Coatings

- Radiation-Curable Coatings

- Solventless / 100% Solids

- By Curing Mechanism

- Physical Drying

- Oxidative Curing

- 2K Chemical Cure

- Baked Thermoset Cure

- Moisture Cure (1K PU, Silane-Terminated Systems)

- UV/EB Cure (Radiation-Curable)

- Inorganic Set/Cure

- By Functional Performance

- Corrosion Protection

- Chemical Resistance / Linings

- Abrasion/Erosion Resistance

- UV/Weathering Resistance

- Anti-Fouling / Marine

- Fire Protection

- Hygienic / Anti-Microbial

- Anti-Condensation / Thermal Insulation Coatings

- Anti-Graffiti / Easy-Clean Coatings

- Conductive / EMI Shielding Coatings

- Optical

- Decorative Effects

- By Substrate

- Steel / Galvanized / Aluminum

- Concrete / Masonry

- Wood / Engineered Wood

- Plastics & Composites

- Glass Leather

- By Application Method

- Brush/Roller, Airless Spray, Air Spray, Electrostatic Spray

- Dip Coating

- Electrodeposition (E-Coat)

- Roll Coating (Coil/Packaging)

- Powder Spray / Fluidized Bed

- Curtain Coating (Wood)

- Inkjet/Printed Functional Coatings (Electronics/Packaging)

- & Ceramics

- Paper/Film (Packaging)

- Textiles/

- Decorative Coatings

All market revenues are presented in USD, with production volumes expressed in metric tons and operating rates expressed as percentage capacity utilization.

Historical Year: 2021–2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027–2036

Key Questions this Study Will Answer

- What are the critical market metrics and forward-looking projections for the Global Paints & Coatings Market, including revenue size, volume consumption, segment-wise performance, and regional growth dynamics?

- How do supply–demand fundamentals vary across key regions, and what role do trade flows, raw material sourcing patterns, and resin/pigment feedstock linkages play in shaping regional market structures?

- In what ways are raw material price volatility (resins, solvents, TiO₂, additives), energy costs, and evolving environmental regulations (VOC norms, REACH, sustainability mandates) influencing cost structures, pricing power, and overall profitability?

- Who are the leading global and regional manufacturers, and how do they compare in terms of backward integration, technology portfolio, innovation intensity, product mix (architectural vs industrial vs specialty), and geographic presence?

- What strategic insights emerge from primary interactions with coating producers, raw material suppliers, distributors, applicators, OEMs, and infrastructure end-users regarding demand outlook, specification shifts, and emerging performance requirements?

- Market Foundations & Dynamics

- Product Overview

- Research Methodology

- Executive Summary

- Market Dynamics (Drivers, Restraints, Opportunities, Challenges, Porter’s Five Forces Analysis, PESTLE Analysis)

- Market Ecosystem & Value Chain

- Overview of Value Chain Participants

- Flow of Value and Material Through the Chain

- Value Addition and Margins at Each Stage

- Market Trends & Developments

- Emerging Feedstock Trends

- Feedstock Availability

- Technological Advancements

- Demand–Supply Gaps

- Investment Hotspots

- Unmet Needs and White Market Spaces

- Risk Assessment Framework

- Political / Geopolitical Risk

- Feedstock Supply Risk

- Environmental and Regulatory Risk

- Financial / Market Risk

- Regulatory Framework & Standards

- Global Policy and Mandate Overview

- Transportation and Storage Regulations

- Sustainability and GHG Reduction Standards

- Environmental & Liability Considerations

- Technology Landscape

- Overview of Technologies

- Cost Optimization Technologies

- Future Outlook

- Global Paints & Coatings Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume

- Market Size & Forecast by End Use

- Decorative Coatings

- Interior Wall Paints

- Exterior Wall Paints

- Primers & Sealers

- Wood Coatings (Architectural)

- Metal Paints for Buildings

- Roof Coatings

- Floor Coatings (Light Duty)

- Waterproofing Coatings

- Fire-Retardant Architectural

- Industrial Coatings

- OEM/Factory-Applied Coatings

- Automotive OEM

- Automotive Plastics Coatings

- Appliances (White Goods) Coatings

- General Metal OEM

- Protective / Industrial Maintenance

- Structural Steel & Bridges

- Oil & Gas

- Power & Utilities

- Marine Coatings

- Coil Coatings

- Packaging Coatings

- Wood Industrial (Furniture/Cabinets)

- Concrete Infrastructure

- OEM/Factory-Applied Coatings

- Special Purpose Coatings

- Automotive Refinish (Repair Paints, Clear Coats, Primers)

- Aerospace Coatings

- Rail Coatings

- High-Temperature Coatings

- Anti-Graffiti Coatings

- Anti-Microbial Coatings

- EMI/RFI Shielding Coatings

- Optical/Anti-Reflective Coatings

- Release / Non-Stick Coatings

- Conductive Coatings

- Thermal Barrier / Insulating Coatings

- Reflective Cool Roof Coatings

- Abrasion/Erosion Resistant Coatings

- Radiation/Chemical Resistant Linings

- Traffic/Road Marking Paints

- Textile/Leather Coatings

- Market Size & Forecast by Resin

- Acrylics

- Alkyds

- Epoxies

- Polyurethanes (PU)

- Polyesters

- Vinyls

- Fluoropolymers

- Silicone / Polysiloxanes

- Chlorinated Rubber / Rubber Derivatives

- Phenolic / Amino Resins (Crosslinkers)

- Inorganic Binders

- Market Size & Forecast by Coating Technology

- Waterborne Coatings

- Solvent borne Coatings

- High-Solids Coatings

- Powder Coatings

- Radiation-Curable Coatings

- Solventless / 100% Solids

- Market Size & Forecast by Curing Mechanism

- Physical Drying

- Oxidative Curing

- 2K Chemical Cure

- Baked Thermoset Cure

- Moisture Cure (1K PU, Silane-Terminated Systems)

- UV/EB Cure (Radiation-Curable)

- Inorganic Set/Cure

- Market Size & Forecast by Functional Performance

- Corrosion Protection

- Chemical Resistance / Linings

- Abrasion/Erosion Resistance

- UV/Weathering Resistance

- Anti-Fouling / Marine

- Fire Protection

- Hygienic / Anti-Microbial

- Anti-Condensation / Thermal Insulation Coatings

- Anti-Graffiti / Easy-Clean Coatings

- Conductive / EMI Shielding Coatings

- Optical

- Decorative Effects

- Market Size & Forecast by Substrate

- Steel / Galvanized / Aluminum

- Concrete / Masonry

- Wood / Engineered Wood

- Plastics & Composites

- Glass Leather

- Market Size & Forecast by Application Method

- Brush/Roller, Airless Spray, Air Spray, Electrostatic Spray

- Dip Coating

- Electrodeposition (E-Coat)

- Roll Coating (Coil/Packaging)

- Powder Spray / Fluidized Bed

- Curtain Coating (Wood)

- Inkjet/Printed Functional Coatings (Electronics/Packaging)

- & Ceramics

- Paper/Film (Packaging)

- Textiles/

- Asia-Pacific Paints & Coatings Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume

- Market Size & Forecast by End Use

- Market Size & Forecast by Resin

- Market Size & Forecast by Coating Technology

- Market Size & Forecast by Curing Mechanism

- Market Size & Forecast by Functional Performance

- Market Size & Forecast by Substrate

- Market Size & Forecast by Application Method

- Europe Paints & Coatings Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume

- Market Size & Forecast by End Use

- Market Size & Forecast by Resin

- Market Size & Forecast by Coating Technology

- Market Size & Forecast by Curing Mechanism

- Market Size & Forecast by Functional Performance

- Market Size & Forecast by Substrate

- Market Size & Forecast by Application Method

- North America Paints & Coatings Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume

- Market Size & Forecast by End Use

- Market Size & Forecast by Resin

- Market Size & Forecast by Coating Technology

- Market Size & Forecast by Curing Mechanism

- Market Size & Forecast by Functional Performance

- Market Size & Forecast by Substrate

- Market Size & Forecast by Application Method

- Latin America Paints & Coatings Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume

- Market Size & Forecast by End Use

- Market Size & Forecast by Resin

- Market Size & Forecast by Coating Technology

- Market Size & Forecast by Curing Mechanism

- Market Size & Forecast by Functional Performance

- Market Size & Forecast by Substrate

- Market Size & Forecast by Application Method

- Middle East & Africa Paints & Coatings Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume

- Market Size & Forecast by End Use

- Market Size & Forecast by Resin

- Market Size & Forecast by Coating Technology

- Market Size & Forecast by Curing Mechanism

- Market Size & Forecast by Functional Performance

- Market Size & Forecast by Substrate

- Market Size & Forecast by Application Method

- Country wise Paints & Coatings Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume

- Market Size & Forecast by End Use

- Market Size & Forecast by Resin

- Market Size & Forecast by Coating Technology

- Market Size & Forecast by Curing Mechanism

- Market Size & Forecast by Functional Performance

- Market Size & Forecast by Substrate

- Market Size & Forecast by Application Method

- Decorative Coatings

Countries Analyzed in the Syllogist Global Research Portfolio: China, Japan, India, South Korea, Australia, Indonesia, Thailand, Vietnam, Malaysia, Philippines, Taiwan, Singapore, Bangladesh, Pakistan, Sri-Lanka, Nepal, Myanmar, Cambodia, Laos, New Zealand, Germany, United Kingdom, France, Italy, Spain, The Netherlands, Belgium, Switzerland, Austria, Sweden, Norway, Denmark, Finland, Poland, Czechia, Hungary, Romania, Greece, Portugal, Ireland, Russia, Ukraine, United States, Canada, Mexico, Brazil, Argentina, Chile, Colombia, Peru, Turkey, Saudi Arabia, United Arab Emirates, Qatar, Kuwait, Oman, Bahrain, Israel, Egypt, South Africa

- Pricing Analysis

- Overview of Pricing Structures

- Average Selling Price Trends by Resin and End Use

- Cost Benchmark

- Historical Price Evolution

- Forecast Pricing Curve

- Factors Influencing Price:

- Regional Pricing Differentiation

- Competition Outlook

- Market Concentration and Fragmentation Level

- Company Market Shares (Top 10 Producers)

- Competitive Strategies

- Benchmarking Matrix

- Recent Developments: Partnerships, M&A, and Policy-Driven Expansions

- Cost Structure & Margin Analysis

- Average Cost per Liter

- Profitability and Margin Distribution Along the Value Chain

- Sensitivity Analysis: How Feedstock Price and Policy Incentives Impact Margin

- Cost Reduction Opportunities through Process Optimization

- Business Models & Strategic Insights

- Sales & Distribution Channel Analysis

- Overview of Go-to-Market Channels

- Channel Share by Region

- Distribution Strategies by Leading Players

- Strategic Recommendations & Roadmap

- Competitors’ Strategic Initiatives

- Future Outlook (Next 5–10 Years, Emerging Players, Success Factors)

- Strategic Recommendations

- Technology Advancements to Watch

- Market Acceleration Roadmap

- Short-Term

- Mid-Term

- Long-Term

- Tailored Recommendations for:

- Producers

- Feedstock Suppliers

- Policymakers / Regulators

- Investors

- Recommendations on Key Success Factors

- Feedstock Security

- Technology Partnerships

- Policy Alignment

- Supply Chain Integration

- Investor Confidence