Market Definition

The India Pesticide Market comprises a wide range of crop protection chemicals and biological solutions used to control insects, weeds, fungi, nematodes, and other crop-damaging organisms across agricultural, horticultural, plantation, and commercial crop systems. The market includes insecticides, herbicides, fungicides, bio-pesticides, plant growth regulators (PGRs), and fumigants, offered in various formulations such as EC, SC, WG, WP, SL, GR, and dust-based formats.

Pesticides play a critical role in ensuring crop yield stability, food security, export competitiveness, and farm income sustainability in India. With over 140 million hectares of arable land and rising pressure on productivity per hectare, crop protection inputs remain central to India’s agricultural modernization strategy.

Over the past two years, the India pesticide industry has been influenced by erratic monsoons, pest outbreaks (such as fall armyworm and pink bollworm), shifts in cropping patterns, expansion of horticulture acreage, export demand for generic technicals, and regulatory scrutiny from the Central Insecticides Board (CIB&RC). Volatility in raw material imports (particularly from China), fluctuations in technical-grade prices, and tightening environmental and residue regulations have also shaped pricing and margin structures.

Market Insights

Demand for pesticides in India is structurally aligned with cropping intensity, pest pressure cycles, MSP-driven crop shifts, export-oriented agriculture, and the expansion of high-value crops such as fruits, vegetables, spices, and cotton.

States such as Maharashtra, Uttar Pradesh, Punjab, Haryana, Telangana, Andhra Pradesh, Gujarat, Rajasthan, Madhya Pradesh, and Karnataka account for significant pesticide consumption, driven by cotton, paddy, wheat, soybean, sugarcane, and horticulture cultivation.

Between 2021–2023, raw material price volatility, supply chain disruptions from China, and inventory corrections impacted manufacturer margins. However, strong domestic agricultural demand and rising technical exports supported overall industry stability. By 2024–2025, improved supply normalization and increased domestic manufacturing capacity under the “China+1” diversification strategy restored growth momentum.

The industry is increasingly shaped by:

- Shift toward higher-value patented and specialty molecules

- Rapid growth in bio-pesticides and residue-compliant formulations

- Increasing adoption of combination products (dual/triple mixtures)

- Expansion of contract manufacturing for global agrochemical players

- Rising penetration of branded generics in Tier-2 and Tier-3 districts

- Digital agri-advisory and precision spraying adoption

Unlike mature Western markets that are predominantly replacement-driven and highly regulated, India remains a volume-growth market with increasing sophistication in formulation technology and export-oriented technical production.

Industry projections indicate that the India Pesticide Market will grow steadily between 2027 and 2031, supported by acreage expansion in horticulture, rising farm mechanization, improved farmer awareness, export growth, and increasing penetration of crop protection in under-served regions.

Market Dynamics: Drivers

Key growth drivers in India include:

- Rising food demand and need for yield enhancement

- Increasing pest resistance and changing pest dynamics

- Expansion of horticulture and high-value cash crops

- Government focus on doubling farmer income

- Export growth in technical-grade pesticides

- Shift from unorganized to branded, regulated formulations

- Growing awareness of integrated pest management (IPM)

- Adoption of drone-based spraying and precision agriculture

Government schemes promoting agricultural productivity, crop diversification, and export competitiveness are significantly boosting demand for crop protection inputs across both staple and commercial crops.

Increased farmer awareness regarding crop loss prevention and yield optimization is driving greater adoption of advanced and combination formulations.

Market Dynamics: Challenges

Despite strong structural demand, the industry faces several challenges:

- Raw material dependency on China for key intermediates

- Regulatory scrutiny and potential bans on certain molecules

- Price volatility in technical-grade chemicals

- Increasing environmental and residue compliance standards

- Monsoon variability impacting seasonal demand

- Intense competition from regional and unorganized players

- Inventory fluctuations at distributor and retailer levels

- Credit risk in rural distribution networks

Additionally, regulatory uncertainty around certain older molecules and periodic government intervention in pricing or bans can impact long-term portfolio planning.

Market Segmentation

By Crop Type

- Cereals & Grains (Rice, Wheat, Maize)

- Oilseeds & Pulses (Soybean, Mustard, Gram)

- Cotton

- Sugarcane

- Fruits & Vegetables

- Plantation Crops (Tea, Coffee, Rubber)

- Spices & Others

By Formulation Type

- EC (Emulsifiable Concentrate)

- SC (Suspension Concentrate)

- WG (Water Dispersible Granules)

- WP (Wettable Powder)

- SL (Soluble Liquid)

- GR (Granules)

- Others

By Type

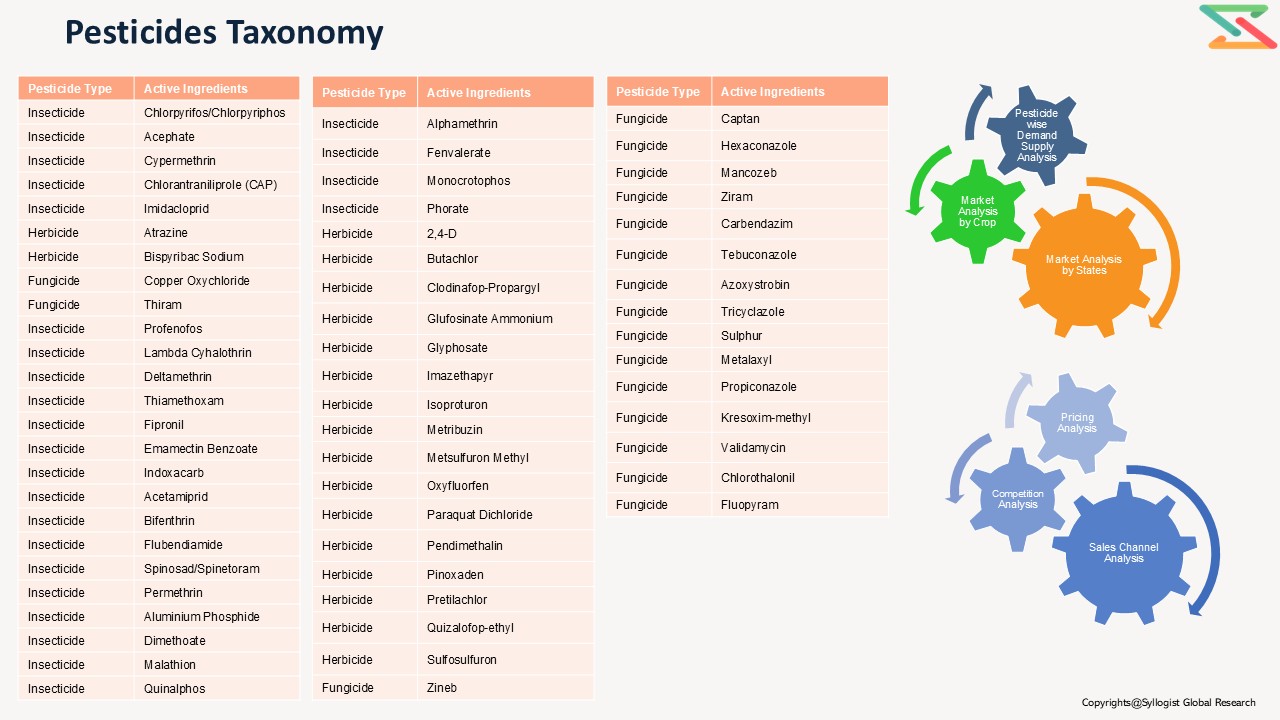

Chemical Pesticides: Acephate, Cypermethrin, Chlorantraniliprole (CAP), Imidacloprid, Atrazine, Bispyribac Sodium, Copper Oxychloride, Thiram, Profenofos, Lambda Cyhalothrin, Deltamethrin, Thiamethoxam, Fipronil, Emamectin Benzoate, Indoxacarb, Acetamiprid, Bifenthrin, Flubendiamide, Spinosad/Spinetoram, Permethrin, Aluminium Phosphide, Dimethoate, Malathion, Quinalphos, Alphamethrin, Fenvalerate, Monocrotophos, Phorate, 2,4-D, Butachlor, Clodinafop-Propargyl, Glufosinate Ammonium, Glyphosate, Imazethapyr, Isoproturon, Metribuzin, Metsulfuron Methyl, Oxyfluorfen, Paraquat Dichloride, Pendimethalin, Pinoxaden, Pretilachlor, Quizalofop-ethyl, Sulfosulfuron, Zineb, Captan, Hexaconazole, Mancozeb, Ziram, Carbendazim, Tebuconazole, Azoxystrobin, Tricyclazole, Sulphur, Metalaxyl, Propiconazole, Kresoxim-methyl, Validamycin, Chlorothalonil, Fluopyram

Biopesticides: Ampelomyces Quisqualis, Beauveria bassiana, Metarhizium anisopliae, Metarhizium rileyi, Lecanicillium lecanii, Purpureocillium lilacinum, Pochonia chlamydosporia, Trichoderma harzianum, Trichoderma viride, Trichoderma asperellum, Trichoderma atroviride, Bacillus subtilis, Bacillus firmus, Lysinibacillus sphaericus, Bacillus thuringiensis var. kurstaki, Bacillus thuringiensis var. israelensis, Bacillus thuringiensis var. galleriae, Bacillus amyloliquefaciens, Pseudomonas fluorescens, Streptomyces lydicus, Helicoverpa armigera NPV, Spodoptera litura NPV

By Application Method

- Foliar Spray

- Soil Treatment

- Seed Treatment

- Drone-Based Spraying

- Drip / Chemigation

By Sales Channel

- Distributor / Dealer Network (Rural Retail Model)

- Direct Institutional Sales

- Contract Manufacturing / Export Channel

- Online / Agri-Digital Platforms

By Market Structure

- Domestic Consumption

- Technical Exports

- Formulation Exports

- Branded Generics

- Patented / Specialty Segment

All market revenues are presented in USD, with volumes expressed in metric tons (technical) and formulation volume (MT) where applicable.

Historical Year: 2021–2024

Base Year: 2025

Estimated Year: 2026

Forecast Period: 2027–2031

Key Questions this Study Will Answer

- What are the key market statistics and forecasts (market size by value & volume, molecule-level shares, formulation mix) for the India Pesticide Market?

- What are the state-wise demand patterns, crop-wise consumption intensity, and seasonal trends shaping growth?

- How are regulatory changes, molecule bans, and environmental compliance reshaping portfolio strategies?

- Who are the leading competitors, and how do they benchmark across technical manufacturing capacity, distribution reach, export orientation, and pricing strategy?

- What insights emerge from interviews with distributors, agri-input retailers, large farmers, contract manufacturers, and export-oriented producers conducted during the study?

- What white-space opportunities exist across bio-pesticides, specialty molecules, combination products, and backward integration into key intermediates?

- Executive Summary

- India Pesticide Market Snapshot (Value & Volume)

- Key Growth Drivers & Structural Shifts

- Segment Highlights (Insecticides, Herbicides, Fungicides)

- Top Molecules by Value & Volume

- Crop-wise & State-wise Demand Hotspots

- Supply Landscape Overview

- Competitive Landscape Summary

- Key Risks & Regulatory Sensitivities

- Strategic Opportunities & Investment Outlook

- Study Scope, Definitions & Methodology

- Scope of the Study

- Market Definitions (AI, Technical, Formulation, Pack Size)

- Units & Conversion Methodology (MT AI to Formulation Volume)

- Market Sizing Framework

- Demand-Side Modelling (Crop Area × Incidence × Dose × Adoption × Sprays)

- Supply-Side Modelling (Production + Imports − Exports ± Inventory)

- Channel Validation & Brand Mapping

- Forecasting Methodology

- Data Validation & Confidence Scoring

- Regulatory & Policy Landscape

- Regulatory Structure in India

- Registration & Licensing Framework

- Compliance Requirements & Label Restrictions

- Banned/Restricted Molecules Overview

- Impact of Regulatory Changes on Market Structure

- Quality Control & Enforcement Environment

- Market Dynamics

- Drivers

- Challenges

- Opportunities

- Market Trends & Developments

- India Chlorpyrifos/Chlorpyriphos Market Outlook

- Demand Supply Analysis

- Market Size & Forecast, by Value & Volume

- Market Size & Forecast, by Crop

- Market Size & Forecast, by State

- Market Size & Forecast, by Formulation

- Market Size & Forecast, by Type

- Market Size & Forecast, by Source (Domestic Vs. Import)

- Market Size & Forecast, by Sales Channel

Similar in-depth analysis will be conducted for all 61 chemical pesticide active ingredients as well as for 22 biopesticide active ingredient, ensuring consistent coverage across demand–supply dynamics, market size (value and volume), formulation splits, crop-wise and state-wise segmentation, and competitive landscape.

Chemical Pesticides: Acephate, Cypermethrin, Chlorantraniliprole (CAP), Imidacloprid, Atrazine, Bispyribac Sodium, Copper Oxychloride, Thiram, Profenofos, Lambda Cyhalothrin, Deltamethrin, Thiamethoxam, Fipronil, Emamectin Benzoate, Indoxacarb, Acetamiprid, Bifenthrin, Flubendiamide, Spinosad/Spinetoram, Permethrin, Aluminium Phosphide, Dimethoate, Malathion, Quinalphos, Alphamethrin, Fenvalerate, Monocrotophos, Phorate, 2,4-D, Butachlor, Clodinafop-Propargyl, Glufosinate Ammonium, Glyphosate, Imazethapyr, Isoproturon, Metribuzin, Metsulfuron Methyl, Oxyfluorfen, Paraquat Dichloride, Pendimethalin, Pinoxaden, Pretilachlor, Quizalofop-ethyl, Sulfosulfuron, Zineb, Captan, Hexaconazole, Mancozeb, Ziram, Carbendazim, Tebuconazole, Azoxystrobin, Tricyclazole, Sulphur, Metalaxyl, Propiconazole, Kresoxim-methyl, Validamycin, Chlorothalonil, Fluopyram

Biopesticides: Ampelomyces Quisqualis, Beauveria bassiana, Metarhizium anisopliae, Metarhizium rileyi, Lecanicillium lecanii, Purpureocillium lilacinum, Pochonia chlamydosporia, Trichoderma harzianum, Trichoderma viride, Trichoderma asperellum, Trichoderma atroviride, Bacillus subtilis, Bacillus firmus, Lysinibacillus sphaericus, Bacillus thuringiensis var. kurstaki, Bacillus thuringiensis var. israelensis, Bacillus thuringiensis var. galleriae, Bacillus amyloliquefaciens, Pseudomonas fluorescens, Streptomyces lydicus, Helicoverpa armigera NPV, Spodoptera litura NPV

- Pricing Analysis

- Sales Channel Analysis

- Competitive Landscape

- Strategic Recommendations

- Portfolio Optimization Strategy

- State Expansion Strategy

- Crop-Focused Bundling Strategy

- Manufacturing & Sourcing Strategy

- Channel & Brand Strategy