Market Definition

The Global Petrochemical Feedstock Diversification Market encompassing Coal-to-Chemicals and Gas-to-Chemicals pathways encompasses the industrial processes, facility infrastructure, technology licenses, catalytic systems, and integrated production complexes through which coal and natural gas are converted into the fundamental chemical building blocks, intermediates, and finished chemical products that constitute the feedstock inputs and finished outputs of the global petrochemical industry, providing alternatives to the naphtha-based and crude oil-derived feedstock streams that have historically dominated the production of olefins, aromatics, methanol, ammonia, and synthesis gas in conventional petroleum refinery-integrated petrochemical operations. The product and process scope of this market includes coal-to-methanol complexes that gasify coal through entrained-flow, fluidized-bed, or fixed-bed gasification reactors using oxygen and steam to produce synthesis gas, which is subsequently cleaned, conditioned, and converted over copper-zinc-alumina catalysts into methanol for use as a direct chemical feedstock or as an intermediate in downstream methanol-to-olefins and methanol-to-propylene conversion trains producing ethylene and propylene as the primary polyolefin feedstocks for polyethylene and polypropylene production, coal-to-olefins integrated complexes combining coal gasification, synthesis gas conditioning, methanol synthesis, and methanol-to-olefins conversion in a single production system as an alternative to naphtha steam cracking for polyolefin production in coal-rich economies with limited access to competitively priced natural gas or petroleum feedstocks, coal-to-ethylene glycol facilities converting coal-derived synthesis gas through dimethyl oxalate synthesis and hydrogenation routes into monoethylene glycol for polyester fiber and polyethylene terephthalate resin production, coal-to-aromatics complexes producing benzene, toluene, and xylene from coal-derived synthesis gas through methanol-to-aromatics or coal direct liquefaction and hydrocracking pathways for use in polyester, nylon, polystyrene, and synthetic rubber production chains, coal-to-ammonia and urea facilities utilizing coal gasification to generate the hydrogen feedstock for Haber-Bosch ammonia synthesis and subsequent urea manufacturing for fertilizer and chemical production applications in coal-endowed economies where natural gas-based ammonia production economics are unfavorable, gas-to-chemicals facilities converting natural gas through steam methane reforming, autothermal reforming, or oxidative coupling to produce methanol, ammonia, hydrogen, synthesis gas, acetylene, and higher hydrocarbon chemical intermediates as primary petrochemical feedstocks or finished chemical products, gas-to-olefins pathways utilizing methane dehydroaromatization, oxidative coupling of methane, or natural gas-to-methanol-to-olefins conversion routes to produce ethylene and propylene from natural gas feedstocks as alternatives to traditional naphtha or ethane steam cracking, gas-to-methanol production utilizing associated gas, stranded gas, and pipeline natural gas as feedstocks for large-scale or modular methanol synthesis plants supplying the fuel methanol, methanol-to-olefins, dimethyl ether, methyl tertiary-butyl ether, acetic acid, and formaldehyde markets, and the integration of both coal-to-chemicals and gas-to-chemicals conversion pathways with carbon capture and storage, green hydrogen co-feeding, and biomass co-gasification technologies that reduce the lifecycle greenhouse gas intensity of feedstock-diversified chemical production and enable the production of low-carbon chemicals qualifying for emerging sustainable chemistry premium markets. The technology landscape within this market spans established commercial gasification technologies including entrained-flow oxygen-blown gasifiers from multiple technology providers, fixed-bed dry-ash and slagging gasifiers deployed in high-sulfur coal applications, fluidized-bed gasifiers for high-moisture and high-ash coal feedstocks, and proprietary advanced gasification systems incorporating plasma-assisted ignition, pressurized operation, and integrated gas cooling and cleaning innovations, as well as the downstream methanol synthesis, methanol-to-olefins, methanol-to-propylene, dimethyl ether, and coal-to-ethylene glycol conversion process technologies operated under proprietary catalyst systems and reactor design licenses whose performance characteristics determine the product yield, energy efficiency, water consumption, and capital cost competitiveness of coal-to-chemicals and gas-to-chemicals production complexes. The value chain of this market extends from coal mining companies and natural gas producers supplying the primary feedstocks, industrial gas companies providing the oxygen and nitrogen utilities essential for gasification operations, engineering procurement and construction contractors designing and building large-scale conversion complexes, technology licensors supplying gasification and downstream conversion process designs and catalysts, equipment manufacturers supplying gasification reactors, gas cleanup systems, synthesis loop vessels, and separation columns, and the chemical producers, polymer manufacturers, fertilizer producers, and fuel blenders whose offtake agreements and long-term supply contracts define the revenue structure and investment economics of coal-to-chemicals and gas-to-chemicals production facilities operating across China, India, the Middle East, the United States, Russia, and Central Asia.

Market Insights

The global petrochemical feedstock diversification market encompassing coal-to-chemicals and gas-to-chemicals pathways is operating with a complex and regionally differentiated commercial dynamic in 2026, shaped by the intersection of China’s dominant and continuing investment in coal chemical production capacity as a strategic energy and chemical security priority, the competitive pressure on gas-to-chemicals investments generated by the global expansion of liquefied natural gas trade and the availability of low-cost associated gas feedstocks in multiple producing regions, the intensifying environmental and carbon regulatory scrutiny of coal-based chemical production whose greenhouse gas intensity substantially exceeds petroleum-derived and natural gas-derived chemical production alternatives, and the emerging commercial interest in hybridized coal and gas conversion pathways integrating carbon capture and storage, green hydrogen co-feeding, and biomass co-processing to reduce the emissions intensity of feedstock-diversified chemical production toward levels compatible with evolving low-carbon chemistry market requirements. The global petrochemical feedstock diversification market covering coal-to-chemicals and gas-to-chemicals was valued at approximately USD 142 billion in 2025 and is projected to expand at a compound annual growth rate of 5 percent through 2036, reaching approximately USD 240 billion by the end of the forecast period, a trajectory reflecting the sustained but selectively moderating growth of coal-to-chemicals production capacity in China as the primary market volume driver, the expanding commercial deployment of gas-to-chemicals facilities across Middle Eastern, North American, and Central Asian natural gas-rich economies, and the progressive emergence of low-carbon integrated chemical production complexes combining fossil feedstock conversion with carbon management technologies. The competitive landscape of this market is structured around a small number of large state-owned chemical and energy corporations in China that dominate global coal-to-chemicals production capacity, major integrated energy companies and national oil companies in the Middle East and Russia that anchor the gas-to-chemicals segment of the market, a cohort of technology licensors and catalyst developers whose proprietary gasification, methanol synthesis, methanol-to-olefins, and gas conversion process technologies are the essential intellectual property foundation of the industry, and the large engineering procurement and construction contractors whose project execution capability determines the capital cost and schedule performance of billion-dollar scale chemical complex construction programs.

A defining commercial and strategic development that has shaped the trajectory of the coal-to-chemicals segment of the feedstock diversification market over the preceding decade and continues to be the primary structural driver of market volume is the massive and sustained investment by Chinese state-owned and private chemical enterprises in inland coal chemical production capacity as a strategic industrial policy response to China’s abundant domestic coal reserves, the geographic concentration of those reserves in water-scarce interior provinces remote from coastal petroleum import infrastructure, and the strategic imperative of reducing Chinese chemical industry dependence on imported naphtha and petroleum feedstocks whose availability and pricing are subject to international crude oil market dynamics beyond domestic policy control. China’s coal-to-olefins and coal-to-methanol industries have grown from demonstration-scale pilot operations in the early 2000s to globally significant production capacities representing substantial fractions of domestic ethylene, propylene, and methanol production, with the technology proven at commercial scale through the operation of dozens of large integrated coal chemical complexes whose operational experience has enabled progressive improvements in energy efficiency, water consumption, catalyst life, and production cost that have progressively improved the competitive economics of coal-derived chemicals relative to petroleum-derived alternatives in the domestic market. The evolution of the Chinese coal chemical industry’s investment focus from pure capacity expansion toward the development of higher-value product integration, including the production of specialty polymers, engineering plastics, synthetic rubber, and coal-to-ethylene glycol for the polyester textile and packaging industries, reflects the maturation of the sector from a bulk commodity chemical feedstock replacement strategy toward a broader industrial value chain development objective that is progressively integrating coal chemical production into the downstream consumer goods and advanced materials manufacturing industries that constitute a growing share of Chinese industrial output and export value.

The gas-to-chemicals segment of the petrochemical feedstock diversification market is experiencing active commercial investment and project development activity across multiple geographic contexts where the combination of abundant and competitively priced natural gas feedstocks, limited naphtha supply or high petroleum product import costs, and strategic chemical industry development objectives is creating favorable economic conditions for gas-based chemical production relative to oil-derived alternatives. In the Middle East, the major natural gas-producing economies of Saudi Arabia, Qatar, the United Arab Emirates, and Iran have built globally significant gas-to-chemicals industries centered on methanol and ammonia production from associated gas and pipeline gas feedstocks, with the competitive feedstock cost advantage of Middle Eastern gas-to-chemicals producers relative to petroleum-based European and Asian competitors enabling the export of cost-competitive methanol, ammonia, urea, and polyolefins to global markets through well-developed marine export infrastructure. The United States gas-to-chemicals investment wave that accompanied the shale gas revolution from approximately 2012 onward delivered a substantial expansion of ethane-based ethylene cracking capacity and propane dehydrogenation facilities that utilize shale gas-derived liquids as competitively priced chemical feedstocks, demonstrating the commercial model for large-scale gas-to-chemicals investment in a developed economy context where feedstock cost advantage relative to naphtha cracking provided a structural competitive edge in polyethylene and polypropylene production that attracted multi-billion USD investments from domestic and international chemical companies. Central Asia, and specifically Uzbekistan, Turkmenistan, and Kazakhstan, represents an emerging and commercially active region for gas-to-chemicals investment, where large gas reserves, limited domestic petrochemical production, geographic remoteness from crude oil import infrastructure, and the strategic industrial development objectives of national governments are combining to drive feasibility study and project development activity for methanol, polypropylene, and polyethylene production facilities based on domestic natural gas feedstocks.

From a regional perspective, Asia-Pacific, and China in particular, represents the overwhelmingly dominant market for coal-to-chemicals production capacity and investment by any measure of production volume, facility count, capital expenditure, or technology deployment, reflecting the unique combination of large domestic coal reserves, limited conventional oil and gas resources relative to chemical industry feedstock requirements, a large and rapidly growing domestic chemical and polymer consumption market, and an industrial policy framework that has consistently prioritized the development of domestic chemical production capability from non-petroleum feedstocks as a national energy and industrial security objective. India represents the most significant near-term growth market for coal-to-chemicals investment outside China, with the Indian government’s ambition to substantially increase domestic chemical production capacity and reduce chemical import dependence creating policy support for coal gasification-based chemical production in coal-rich states where the resource endowment and infrastructure conditions are favorable for large integrated coal chemical complexes. The Middle East represents the dominant regional market for gas-to-chemicals production capacity by volume and competitive significance in global methanol and ammonia trade, with the low-cost feedstock position of Middle Eastern gas-to-chemicals producers providing a structural export competitiveness advantage in global petrochemical markets that is expected to sustain Middle Eastern gas chemical production investment through the forecast period notwithstanding the growing decarbonization pressure on fossil-based chemical production in European and North American consumer markets. Russia and Central Asia represent a combined regional market for gas-to-chemicals investment whose scale and pace of development is determined by the access of gas-rich national economies to technology, engineering execution capability, and export market connections that are being progressively re-configured by the geopolitical disruptions to Russian energy trade following the 2022 conflict and by the growing commercial engagement of Chinese technology and engineering companies in Central Asian chemical project development.

Key Drivers

Energy and Chemical Feedstock Security Imperatives Driving Strategic Investment in Domestic Non-Petroleum Chemical Production Pathways Across Coal and Gas-Rich Economies

The most structurally consequential and politically durable demand driver for petrochemical feedstock diversification investment in both coal-to-chemicals and gas-to-chemicals pathways is the fundamental energy and industrial security imperative of coal and gas-endowed national economies to develop domestic chemical production capability from their indigenous hydrocarbon resources, reducing the strategic vulnerability created by dependence on imported petroleum feedstocks whose availability, pricing, and supply chain integrity are subject to geopolitical disruption, international market volatility, and the foreign policy leverage of crude oil-producing nations whose export decisions are not determined by the energy security interests of importing countries. The energy security argument for petrochemical feedstock diversification is most powerfully expressed in China, where the national strategic calculus of developing coal-to-chemicals and gas-to-chemicals capacity reflects the assessment that a chemical industry overwhelmingly dependent on imported naphtha from Middle Eastern, Russian, and West African crude oil suppliers represents an unacceptable strategic vulnerability in the context of potential supply disruption scenarios arising from maritime chokepoint interdiction, sanctions regimes, or geopolitical conflict that could simultaneously interrupt crude oil supply and restrict access to petroleum-derived chemical feedstocks. The translation of this energy security imperative into sustained capital investment in coal-to-chemicals complexes has been reinforced by the industrial policy framework of the Chinese government, which has directed state-owned enterprises and provided fiscal and financial incentives for private sector investment in coal chemical production capacity as a component of broader strategic resource development and industrial upgrading programs, creating a policy-driven investment momentum that has proven resilient to short-term economic cycle fluctuations, crude oil price movements, and international criticism of the carbon intensity of coal-based chemical production. In natural gas-endowed economies including Qatar, Saudi Arabia, Russia, Uzbekistan, and the United States, the gas-to-chemicals feedstock diversification imperative operates through a market economics mechanism rather than primarily through energy security policy, as the structural competitive advantage of low-cost domestic natural gas feedstock relative to imported naphtha creates a commercial incentive for gas-to-chemicals investment that attracts private and state-owned capital to methanol, ammonia, polyethylene, and polypropylene production projects whose competitiveness in global chemical markets rests on the feedstock cost differential that gas-endowed locations enjoy relative to petroleum-feedstock-dependent competitors in naphtha-importing economies.

Growing Domestic Demand for Petrochemicals and Polymers in Emerging Economies Creating Commercial Pull for Feedstock-Diversified Local Chemical Production Serving Expanding Consumption Markets

The rapid and structurally sustained growth of domestic chemical and polymer consumption in China, India, Southeast Asia, and other emerging economies whose per-capita chemical consumption is converging toward developed economy levels from a low base is creating a powerful commercial demand driver for feedstock-diversified chemical production that complements and reinforces the energy security policy driver by providing a large and growing domestic market that feedstock-diversified chemical producers can serve without the export market access and competitiveness challenges that constrain the commercial economics of production facilities in locations with inferior logistical connections to global chemical trade infrastructure. The chemical and polymer consumption growth trajectory of China, India, and Southeast Asian economies is driven by the progressive industrialization and urbanization of large population bases whose rising incomes are generating expanding demand for packaged consumer goods requiring polyethylene and polypropylene packaging films, polyester textiles and bottles from ethylene glycol and polyethylene terephthalate production, construction materials from polyvinyl chloride and engineering polymer production, automotive and electronics components from specialty polymer and chemical production, and agricultural inputs from ammonia and urea fertilizer production that supports the food security requirements of large and growing populations. The domestic market pull for chemical production investment in coal and gas-endowed emerging economies is particularly powerful because the combination of feedstock cost advantage from indigenous coal and gas resources and proximity to large and growing domestic consumption markets creates a two-sided competitive advantage relative to imported chemical products from geographically remote producers that must absorb international shipping costs, currency exchange risk, and supply chain logistics complexity in addition to feedstock and conversion cost burdens. Government industrial development programs in India, Uzbekistan, and several Southeast Asian economies that are currently net importers of methanol, ammonia, polyethylene, and polypropylene are actively evaluating feedstock-diversified domestic chemical production investments as a mechanism for simultaneously developing the domestic chemical industry, reducing the foreign exchange expenditure associated with chemical imports, and creating industrial employment in regions where coal and gas resource endowments provide the feedstock foundation for competitive chemical production facilities.

Key Challenges

High Greenhouse Gas Intensity of Coal-to-Chemicals Production Pathways and the Growing Carbon Regulatory and Market Access Risk for Coal-Derived Chemical Products in Decarbonizing Consumer Markets

The most consequential long-term structural challenge confronting the coal-to-chemicals segment of the petrochemical feedstock diversification market is the exceptionally high lifecycle greenhouse gas intensity of coal-based chemical production pathways relative to both petroleum-derived and natural gas-derived chemical production alternatives, a carbon intensity disadvantage that is generating progressively more material commercial and regulatory risk for coal chemical producers as the decarbonization policies of major chemical-consuming economies advance from voluntary commitments toward binding regulatory frameworks that assign carbon costs to the embedded emissions of imported goods and that restrict market access for high-carbon-intensity products in regulated markets. The carbon dioxide emissions associated with coal-to-chemicals production arise from multiple stages of the conversion process including the partial combustion of coal carbon during gasification that releases carbon dioxide within the process, the combustion of coal for the steam and power utilities supporting the gasification and downstream conversion operations, and the release of carbon dioxide stripped from synthesis gas during acid gas removal cleaning steps that must be vented unless captured and permanently stored, collectively producing lifecycle carbon intensities per tonne of chemical product that can be multiple times higher than the equivalent metric for natural gas-derived production and substantially higher than for petroleum naphtha-derived production using conventional steam cracking technology. The European Union Carbon Border Adjustment Mechanism, which entered its transitional phase in 2023 and is advancing toward full implementation with financial obligations for importers of carbon-intensive goods including chemicals and fertilizers, represents the most commercially significant near-term regulatory mechanism through which the carbon intensity disadvantage of coal-to-chemicals production is being converted into a direct financial penalty on products sold in European markets, and whose progressive expansion to cover a broader range of chemical product categories will systematically erode the landed cost competitiveness of coal-derived chemicals in the world’s largest and most sophisticated chemical import market. The commercial response of leading coal chemical producers to this carbon intensity challenge, encompassing investment in carbon capture and storage to sequester the carbon dioxide co-produced during coal gasification, green hydrogen co-feeding to reduce coal consumption per unit of chemical output, and integration of renewable electricity into chemical facility utility systems to reduce coal combustion for power generation, represents a capital-intensive and technically complex adaptation pathway whose cost and timeline create a near-term competitive disadvantage relative to natural gas-based chemical producers whose lower starting carbon intensity requires less abatement investment to achieve equivalent lifecycle carbon performance.

Exceptional Capital Expenditure Intensity of Large-Scale Chemical Conversion Complexes and the Extended Development and Financing Timelines That Create Investment Risk in Volatile Feedstock and Product Markets

A structurally significant and persistent commercial challenge limiting the pace and scope of petrochemical feedstock diversification investment in both coal-to-chemicals and gas-to-chemicals pathways is the extraordinary capital expenditure intensity of large-scale chemical conversion complexes, whose gasification trains, air separation units, synthesis gas conditioning and cleaning systems, methanol synthesis and methanol-to-olefins conversion reactors, product separation and purification columns, utilities, offsites, and supporting infrastructure collectively require capital investments in the multi-billion USD range per project for commercial-scale facilities, creating long development timelines, complex multi-source financing structures, and extended payback periods that expose project developers and investors to prolonged and compounding exposure to the coal and natural gas feedstock price volatility, chemical product market price cycles, and regulatory framework changes that can materially alter project economics between the front-end engineering study stage and the commercial production ramp-up that typically occurs five to eight years after initial project sanction. The capital cost estimation and construction schedule management challenges associated with mega-scale coal-to-chemicals and gas-to-chemicals complexes have historically proven more demanding than initially projected, with several flagship projects experiencing cost overruns and schedule delays that significantly exceeded the contingency allowances incorporated in the original investment approval basis and that required additional equity and debt financing at unfavorable terms during construction, creating precedent-setting adverse investor experiences that have elevated the risk premiums required by debt and equity providers in subsequent project financing processes and that have increased the due diligence rigor applied by engineering procurement and construction contractors to project scope definition and contract risk allocation. The financing structure of large coal-to-chemicals and gas-to-chemicals projects, which in many cases combines state-owned enterprise equity with policy bank lending at subsidized interest rates, commercial bank project financing, and in some gas-to-chemicals contexts international bond market capital raising, requires the alignment of multiple financing parties with differing risk tolerances, return requirements, security structures, and regulatory compliance obligations across jurisdictions that may have conflicting legal frameworks governing the rights of secured creditors in project finance distress scenarios, creating transaction complexity that extends financing close timelines and adds legal and advisory cost to project development programs whose feasibility study and permitting costs alone can reach hundreds of millions of USD for the largest integrated chemical complex projects.

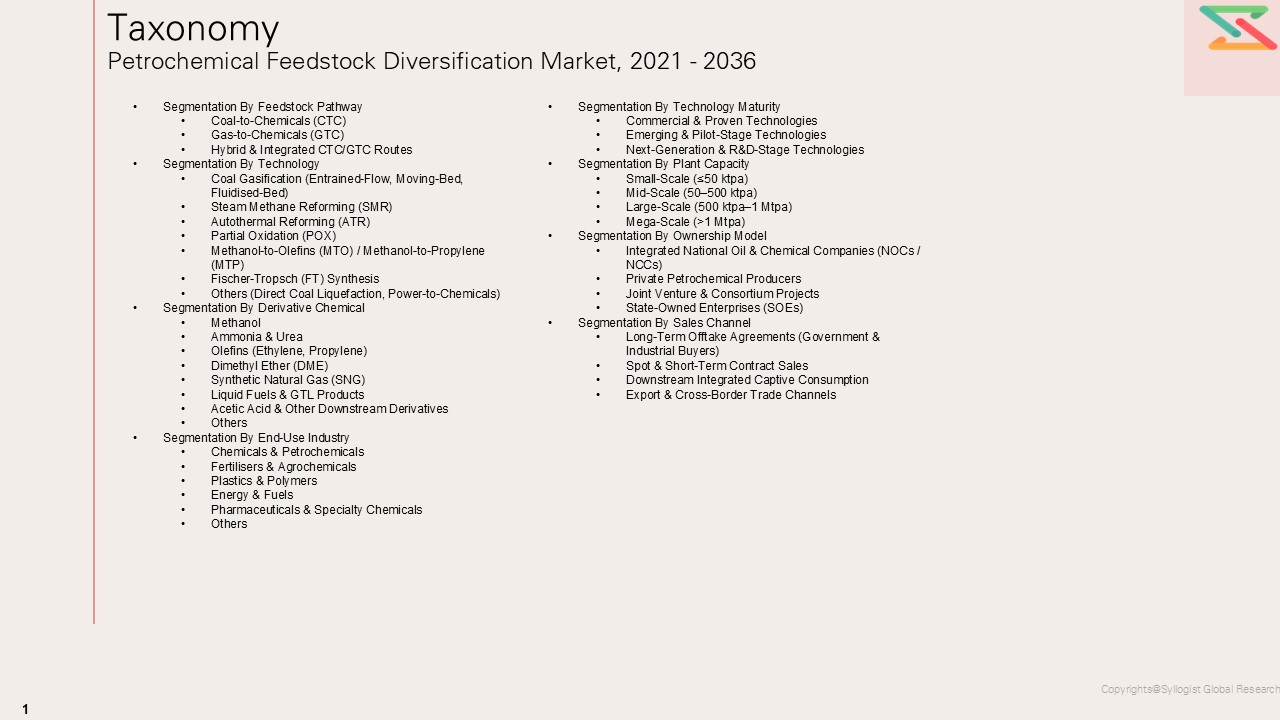

Market Segmentation

- Segmentation By Feedstock Type

- Hard Coal (Bituminous and Anthracite)

- Lignite and Sub-Bituminous Coal

- Pipeline Natural Gas

- Associated Gas from Oil Production

- Shale Gas and Tight Gas

- Coalbed Methane

- Liquefied Natural Gas (LNG) Regasification Streams

- Hybrid Coal and Natural Gas Co-Feed

- Others

- Segmentation By Conversion Pathway

- Coal-to-Methanol (CTM)

- Coal-to-Olefins (CTO) via Methanol-to-Olefins

- Coal-to-Propylene (CTP) via Methanol-to-Propylene

- Coal-to-Ethylene Glycol (CTEG)

- Coal-to-Aromatics (CTA)

- Coal-to-Ammonia and Urea

- Coal-to-Dimethyl Ether (DME)

- Gas-to-Methanol (GTM)

- Gas-to-Olefins (GTO) via Methanol-to-Olefins

- Gas-to-Ammonia and Urea

- Oxidative Coupling of Methane (OCM) to Ethylene

- Methane Dehydroaromatization (MDA)

- Gas-to-Hydrogen and Synthesis Gas

- Others

- Segmentation By Gasification Technology

- Entrained-Flow Oxygen-Blown Gasification

- Fixed-Bed Dry-Ash Gasification

- Fixed-Bed Slagging Gasification

- Fluidized-Bed Gasification

- Steam Methane Reforming (SMR)

- Autothermal Reforming (ATR)

- Partial Oxidation (PDX)

- Plasma-Assisted Gasification

- Others

- Segmentation By Primary Chemical Product

- Methanol

- Ethylene

- Propylene

- Monoethylene Glycol (MEG)

- Benzene, Toluene, and Xylene (BTX) Aromatics

- Ammonia

- Urea

- Dimethyl Ether (DME)

- Hydrogen

- Synthesis Gas (Syngas)

- Acetylene

- Others

- Segmentation By Downstream Application

- Polyethylene and Polypropylene Production

- Polyethylene Terephthalate (PET) and Polyester

- Fertilizer and Agricultural Chemicals

- Methanol Fuel and Fuel Blending

- Synthetic Rubber and Elastomers

- Acetic Acid and Derivatives

- Formaldehyde and Resins

- Engineering Plastics and Specialty Polymers

- Solvents and Chemical Intermediates

- Others

- Segmentation By Carbon Management Integration

- Conventional Production Without Carbon Capture

- Partial Carbon Capture at Synthesis Gas Cleaning Stage

- Full Carbon Capture and Geological Storage (CCS) Integration

- Green Hydrogen Co-Feed to Reduce Carbon Intensity

- Biomass Co-Gasification for Biogenic Carbon Offset

- Carbon Dioxide Utilization (Urea, Methanol, Carbonates)

- Others

- Segmentation By Facility Scale

- Large-Scale Integrated Complexes (Above 1 Million Tonnes per Year Output)

- Mid-Scale Production Facilities (300,000 to 1 Million Tonnes per Year)

- Small and Modular Conversion Units (Below 300,000 Tonnes per Year)

- Segmentation By Ownership Structure

- State-Owned Enterprise (SOE) Operated Facilities

- Private Sector Chemical Company Projects

- Joint Venture (Domestic and International Partners)

- Integrated Energy Company Chemical Divisions

- Independent Project Developer Structures

- Others

- Segmentation By Region

- Asia-Pacific (China, India, Southeast Asia)

- Middle East (Saudi Arabia, Qatar, UAE, Iran)

- North America (United States, Canada)

- Russia and Central Asia

- Europe

- Africa and Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2036

Key Questions this Study Will Answer

- What is the projected global market valuation for petrochemical feedstock diversification across coal-to-chemicals and gas-to-chemicals pathways through 2036, segmented by feedstock type, conversion pathway, primary chemical product, downstream application, carbon management integration, and region, and which conversion pathways and geographic markets are expected to generate the highest incremental revenue and production capacity growth across the forecast period?

- How is the Chinese coal-to-chemicals industry evolving in terms of technology upgrading, product mix sophistication, energy efficiency improvement, water consumption reduction, and carbon intensity management as the industry transitions from first-generation capacity expansion toward higher-value product integration and low-carbon production adaptation, and what are the implications of this industry maturation trajectory for the global competitive positioning of Chinese coal-derived chemical producers relative to natural gas-based and petroleum-based chemical competitors in domestic and export markets?

- What are the projected capital expenditure commitments, project development pipelines, technology license award activity, and first production timelines for coal-to-chemicals and gas-to-chemicals investments across India, Central Asia, the Middle East, and North America over the forecast period, and how are the feedstock cost structures, domestic market demand growth trajectories, and industrial policy support frameworks in each regional market influencing investment decision timelines and facility scale choices by project developers?

- How is the European Union Carbon Border Adjustment Mechanism, alongside emerging equivalent carbon import pricing frameworks in other major chemical-consuming economies, affecting the landed cost competitiveness and market access prospects of coal-to-chemicals and gas-to-chemicals derived products in regulated markets, and what integration of carbon capture and storage, green hydrogen co-feeding, and biomass co-processing with existing and planned coal-to-chemicals facilities is technically feasible and economically achievable within timeframes relevant to the CBAM implementation schedule?

- What are the technology performance benchmarks, capital cost trajectories, energy and water consumption profiles, and catalyst lifetime and selectivity characteristics of the leading methanol-to-olefins, coal-to-ethylene glycol, gas-to-ammonia, and oxidative coupling of methane technology platforms competing for project licensing awards in the major coal-to-chemicals and gas-to-chemicals investment markets, and how are the technology licensing strategies, catalyst supply models, and process performance guarantees of competing technology providers influencing technology selection decisions by project developers across different regional market contexts?

- Who are the leading coal-to-chemicals and gas-to-chemicals technology licensors, gasification technology providers, catalyst manufacturers, large-scale engineering procurement and construction contractors, state-owned chemical enterprise project developers, and independent chemical project developers currently defining the competitive landscape of the global petrochemical feedstock diversification market, and what are their respective technology portfolio strategies, geographic project development priorities, carbon management integration roadmaps, and downstream product market positioning approaches for advancing feedstock-diversified chemical production through the forecast horizon?

- Product Definition

- Scope of the Study

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework (Feedstock Pathway, Derivative, Region, Technology Maturity)

- Key Research Assumptions & Limitations

- Secondary Research

- Industry Publications, Petrochemical Association Reports & Company Press Releases

- Government Energy & Industrial Policy Data (IEA, EIA, CPCIF, EC DG ENERGY, etc.)

- Coal & Gas Feedstock Production, Trade & Consumption Statistics

- Petrochemical Plant Capacity, Commissioning & Capital Project Databases

- Primary Research Design & Execution

- In-depth Interviews with CTC/GTC Plant Operators, Feedstock Procurement Heads & Licensing Engineers

- Surveys with Petrochemical Producers, EPC Contractors & Technology Licensors

- Expert Panel Validation

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Bottom-Up & Top-Down Reconciliation

- Plant Capacity, Utilisation Rate & Derivative Output-Based Market Sizing Model

- Feedstock Price Sensitivity & Substitution Model for CTC vs GTC Economics

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Technology & Innovation Highlights

- Manufacturing Economics & Unit Economics Summary

- Average Plant CAPEX & OPEX Benchmarks (CTC vs GTC)

- Feedstock Cost Competitiveness & Margin Analysis by Route

- Coal-to-Chemicals vs Gas-to-Chemicals Revenue Model Summary

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Geographic & Regional Trends

- Risk Assessment Framework

- Geopolitical & Trade Policy Risk

- Coal & Natural Gas Price Volatility Risk

- Environmental & Carbon Regulation Risk (Emissions, ETS, Carbon Border Adjustment)

- Financial / Market Risk

- Water Scarcity & Environmental Compliance Risk for Coal-Based Processes

- Energy Transition & Low-Carbon Feedstock Substitution Risk

- Technology Obsolescence & Licensing Risk

- Regulatory Framework & Policy Standards

- Global Petrochemical Feedstock Diversification Market Economics

- Manufacturing Economics & Unit Economics Framework

- Capital Expenditure (CAPEX) Structure

- Operating Expenditure (OPEX) Structure

- Revenue Model & Monetisation Levers

- Capacity Utilisation & Throughput Economics

- Payback Period & Return on Investment (ROI) Analysis

- Total Cost of Production vs Naphtha-Based & Crude Oil-Derived Feedstock Economics

- Raw Material & Input Cost Analysis

- Metallurgical & Thermal Coal Price Trends (USD/tonne, 2021–2035)

- Natural Gas & LNG Feedstock Price Dynamics (Henry Hub, TTF, NBP, Asian Spot)

- Syngas Production Cost Structure: Gasification vs Steam Methane Reforming (SMR)

- Water & Utilities Cost Structure in CTC & GTC Processes

- Catalyst, Reagent & Chemical Additives Cost Analysis

- Carbon Capture, Utilisation & Storage (CCUS) Cost Integration

- Impact of Scale, Integration & Co-product Credits on Feedstock Economics

- Plant-Level Economics by Technology Route

- Coal Gasification to Methanol, Olefins (CTO/MTO) & Ammonia Economics

- Coal-to-Dimethyl Ether (DME), Synthetic Natural Gas (SNG) & Liquid Fuels Economics

- Gas-to-Methanol, GTL & Ammonia/Urea Economics

- Gas-to-Olefins (GTO) via Methanol-to-Olefins (MTO) Economics

- Integrated Polyolefin & Downstream Derivatives Economics

- Regulatory & Standards Compliance Economics

- Emissions Regulation & Carbon Pricing Compliance Cost Benchmarks

- Water Treatment, Effluent & Solid Waste Management Compliance Costs

- Health, Safety & Environmental (HSE) Standards Compliance Costs

- Manufacturing Economics & Unit Economics Framework

- Global Petrochemical Feedstock Diversification Market Outlook

- Market Size & Forecast by Value (USD Billion, 2021–2036)

- Market Size & Forecast by Feedstock Pathway

- Coal-to-Chemicals (CTC)

- Gas-to-Chemicals (GTC)

- Hybrid & Integrated CTC/GTC Routes

- Market Size & Forecast by Technology

- Coal Gasification (Entrained-Flow, Moving-Bed, Fluidised-Bed)

- Steam Methane Reforming (SMR)

- Autothermal Reforming (ATR)

- Partial Oxidation (POX)

- Methanol-to-Olefins (MTO) / Methanol-to-Propylene (MTP)

- Fischer-Tropsch (FT) Synthesis

- Others (Direct Coal Liquefaction, Power-to-Chemicals)

- Market Size & Forecast by Derivative Chemical

- Methanol

- Ammonia & Urea

- Olefins (Ethylene, Propylene)

- Dimethyl Ether (DME)

- Synthetic Natural Gas (SNG)

- Liquid Fuels & GTL Products

- Acetic Acid & Other Downstream Derivatives

- Others

- Market Size & Forecast by End-Use Industry

- Chemicals & Petrochemicals

- Fertilisers & Agrochemicals

- Plastics & Polymers

- Energy & Fuels

- Pharmaceuticals & Specialty Chemicals

- Others

- Market Size & Forecast by Technology Maturity

- Commercial & Proven Technologies

- Emerging & Pilot-Stage Technologies

- Next-Generation & R&D-Stage Technologies

- Market Size & Forecast by Plant Capacity

- Small-Scale (≤50 ktpa)

- Mid-Scale (50–500 ktpa)

- Large-Scale (500 ktpa–1 Mtpa)

- Mega-Scale (>1 Mtpa)

- Market Size & Forecast by Ownership Model

- Integrated National Oil & Chemical Companies (NOCs / NCCs)

- Private Petrochemical Producers

- Joint Venture & Consortium Projects

- State-Owned Enterprises (SOEs)

- Market Size & Forecast by Sales Channel

- Long-Term Offtake Agreements (Government & Industrial Buyers)

- Spot & Short-Term Contract Sales

- Downstream Integrated Captive Consumption

- Export & Cross-Border Trade Channels

- Asia-Pacific Petrochemical Feedstock Diversification Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Feedstock Pathway

- By Technology

- By Derivative Chemical

- By End-Use Industry

- By Technology Maturity

- By Plant Capacity

- By Ownership Model

- By Sales Channel

- Key Demand Drivers (APAC-Specific)

- Competitive Landscape (APAC)

- Market Size & Forecast

- Europe Petrochemical Feedstock Diversification Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Feedstock Pathway

- By Technology

- By Derivative Chemical

- By End-Use Industry

- By Technology Maturity

- By Plant Capacity

- By Ownership Model

- By Sales Channel

- Key Demand Drivers (Europe-Specific)

- Competitive Landscape (Europe)

- Market Size & Forecast

- North America Petrochemical Feedstock Diversification Market Outlook

- Market Overview & Strategic Importance

- Market Size & Forecast

- By Value (2020–2035)

- By Feedstock Pathway

- By Technology

- By Derivative Chemical

- By End-Use Industry

- By Technology Maturity

- By Plant Capacity

- By Ownership Model

- By Sales Channel

- Key Demand Drivers (North America-Specific)

- Competitive Landscape (North America)

- Latin America Petrochemical Feedstock Diversification Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Feedstock Pathway

- By Technology

- By Derivative Chemical

- By End-Use Industry

- By Technology Maturity

- By Plant Capacity

- By Ownership Model

- By Sales Channel

- Key Demand Drivers (LATAM-Specific)

- Competitive Landscape (Latin America)

- Market Size & Forecast

- Middle East & Africa Petrochemical Feedstock Diversification Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Feedstock Pathway

- By Technology

- By Derivative Chemical

- By End-Use Industry

- By Technology Maturity

- By Plant Capacity

- By Ownership Model

- By Sales Channel

- Key Demand Drivers (MEA-Specific)

- Competitive Landscape (MEA)

- Market Size & Forecast

- Country-Wise Petrochemical Feedstock Diversification Market Outlook

- Market Size & Forecast by Country

- By Value

- By Feedstock Pathway

- By Technology

- By Derivative Chemical

- By End-Use Industry

- By Technology Maturity

- By Plant Capacity

- By Ownership Model

- By Sales Channel

- Market Size & Forecast by Country

- Countries Covered: China, India, United States, Russia, Australia, Germany, South Africa, Indonesia, Japan, South Korea, Qatar, Saudi Arabia, Iran, Canada, Brazil, Poland, Ukraine, United Kingdom, Turkey, Nigeria

- Technology Landscape & Innovation Analysis

- Petrochemical Feedstock Diversification Technology Maturity Assessment

- Emerging & Disruptive Technologies in CTC & GTC

- Digital Technologies in Plant Operations, Process Optimisation & Predictive Maintenance

- Carbon Capture, Utilisation & Storage (CCUS) Integration with CTC & GTC Plants

- Green Hydrogen & Power-to-Chemicals as Emerging Feedstock Diversification Vectors

- Technology Readiness & Commercialisation Matrix – Key CTC & GTC Technologies

- Patent Landscape Analysis

- R&D Investment Benchmarking

- Value Chain & Supply Chain Analysis

- Petrochemical Feedstock Diversification Value Chain Mapping

- Supply Chain Concentration & Dependency Analysis

- Key Supplier Mapping by Feedstock Route & Technology Programme

- Supplier Risk Heat Map

- Make vs Buy Strategy Trends Among CTC & GTC Plant Developers

- Pricing Analysis

- Feedstock & Derivative Chemical Pricing Dynamics & Mechanisms

- Pricing by Feedstock Pathway, Technology Route & Derivative Chemical

- Total Cost of Production (TCOP) Analysis – Including Feedstock, Utilities & Carbon Costs

- CTC vs GTC vs Naphtha-Based Pricing Benchmarks

- Premium Derivatives Pricing & Value Proposition vs Conventional Routes

- Sustainability & Environmental Stewardship

- Environmental & Sustainability Landscape in Feedstock Diversification

- Carbon Footprint Benchmarking Across CTC & GTC Technologies

- CCUS Integration Roadmap for Coal- & Gas-Based Chemical Producers

- Green & Low-Carbon Methanol & Ammonia Production Pathways

- Water Consumption, Effluent Management & Circular Economy in CTC Plants

- ESG Reporting & Lifecycle Assessment (LCA) in CTC & GTC Operations

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level: Global Leaders vs Regional Players

- Top 5 Petrochemical Feedstock Diversification Company Market Revenue Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis by Technology & Region

- Competitive Intensity Map by Feedstock Pathway & Region

- Player Classification

- Tier-1 Global Integrated Chemical & Energy Companies

- Tier-2 Regional & Specialist CTC/GTC Technology Developers & Plant Operators

- Technology Licensors & EPC Contractors

- Emerging & Disruptive Players

- Competitive Analysis Frameworks

- Market Share Analysis by Technology Route & Geography

- R&D Intensity Benchmarking

- Licensing & Offtake Revenue Comparison

- Geographic Revenue Exposure Comparison

- Company Profiles

- Company Overview, HQ & Organisational Structure

- CTC/GTC Products, Technologies & Services Portfolio

- Revenue Breakdown

- Key Plant Programmes, Licensing Agreements & Industrial Deployments

- Manufacturing Footprint & Key Facilities

- Recent Developments (M&A, Partnerships, New Plants, Financial Results)

- SWOT Analysis

- Strategic Focus: Feedstock Diversification, Low-Carbon Routes & Downstream Integration

- Market Structure & Concentration

- Strategic Output

- Market Opportunity Matrix

- High-Value Opportunity Quadrant Analysis

- Addressable Market by Feedstock Pathway, Technology & Region

- Time-to-Revenue Assessment by Opportunity

- White Space Opportunity Analysis

- Underserved Derivative Chemical & End-Use Sector Gaps

- Geographic Markets with Low CTC/GTC Penetration

- Technology Gaps with High Commercialisation Potential

- Customer Segment Unmet Needs

- Market Opportunity Matrix

- Strategic Recommendations

- Product Portfolio & Innovation Strategy

- Technology & Digitalisation Strategy

- Plant Footprint & Capacity Expansion Strategy

- Downstream Integration & Derivative Diversification Strategy

- Pricing & Commercial Strategy

- Sustainability, Carbon Management & Regulatory Compliance Strategy

- Supply Chain & Feedstock Sourcing Strategy

- Partnership, M&A & Expansion Strategy

- Regional Growth Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-Term (2025–2028)

- Mid-Term (2029–2032)

- Long-Term (2033–2036)