Market Definition

The India School Market comprises the full ecosystem of institutions and services delivering K–12 education across government schools, government-aided schools, and private schools, spanning primary, upper primary, secondary, and higher secondary levels. It includes school infrastructure and operations (classrooms, labs, libraries, transport, safety), academic delivery (curriculum, textbooks, assessments), digital learning tools (smart classrooms, LMS, devices, content), and support services (after-school tutoring, teacher training, school management systems, vocational modules). The school sector is a backbone of India’s human-capital pipeline, directly shaping literacy, employability, and long-term economic productivity. Over the past two years, the India school ecosystem has been significantly influenced by NEP 2020 rollout momentum, post-pandemic learning recovery programs, accelerated digitization, and renewed focus on foundational literacy & numeracy, alongside widening debates around affordability, learning outcomes, and public–private delivery models.

Market Insights

India school market is undergoing a structural shift from “enrolment-focused” expansion to outcomes-focused improvement. While enrolment stabilization has matured in many states, policy and funding are increasingly targeted toward learning recovery, foundational learning, teacher capacity building, and measurable competencies. The “quality gap” between institutions, especially across rural vs urban and government vs private, continues to drive demand for supplementary education (tuitions, test-prep, bridge courses), hybrid learning models, and school improvement programs (teacher training, remedial learning kits, assessment platforms).

Digitization is no longer restricted to smart boards in premium private schools; it is expanding through low-cost digital content, mobile-first learning, LMS adoption, and school administration software (ERP/SIS), especially where schools and state systems seek better attendance tracking, fee management, and student performance monitoring. However, adoption remains uneven due to device access, connectivity constraints, and teacher readiness, resulting in strong demand for assisted/managed digital classrooms, vernacular content, and teacher enablement solutions rather than purely “tech-first” rollouts.

From a demand standpoint, the market remains supported by India’s large school-age population, rapid urbanization, and strong household willingness to invest in education, particularly in English-medium education, STEM skill-building, competitive exam readiness, and holistic development (sports, arts, coding). At the same time, affordability pressure is reshaping private-school pricing and pushing growth of budget private schools, low-fee chains, and blended learning models that reduce delivery costs while improving outcomes.

Industry projections indicate that the India school ecosystem will expand at a steady pace through 2028–2035, driven by continued education spending, policy-driven reforms, growing demand for private and semi-private education models, and increasing adoption of technology-led learning and administration systems. Growth is expected to be stronger in Tier-II/Tier-III cities and aspirational districts, where school modernization, digital initiatives, and private-school penetration are rising from a lower base.

Regulatory and policy initiatives are reshaping competitive dynamics: NEP-aligned curriculum transformation, competency-based assessment, early childhood education integration (pre-primary), teacher training mandates, safety compliance, and school infrastructure norms are pushing institutions to upgrade systems and partner with solution providers. However, the sector remains exposed to operational constraints like uneven state-level execution, teacher shortages in specific subjects, fee regulation uncertainty in some states, and significant disparities in learning outcomes.

Market Dynamics: Drivers

Key drivers of the India school market include rising household expenditure on education, increasing preference for private schooling and English-medium instruction, and growing demand for high-quality learning outcomes and career-linked skills. Policy frameworks such as NEP implementation, foundational literacy & numeracy missions, and school infrastructure modernization programs are boosting institutional spending on teacher capacity, assessment tools, and digital resources. The expansion of edtech enablement inside schools (smart classrooms, LMS, digital content, analytics-driven assessments) and growth of supplementary learning (tutoring/test prep) further accelerate market momentum, especially in competitive academic segments.

Market Dynamics: Challenges

The India school market faces challenges such as wide learning-outcome disparities, infrastructure gaps (especially in rural/remote regions), and constraints in teacher availability, training quality, and subject expertise. Adoption of digital learning is limited by device access, connectivity reliability, and classroom execution readiness, often leading to low utilization after initial deployment. Regulatory uncertainty in areas such as fee controls, affiliation norms, and compliance mandates can pressure private school economics. Additionally, fragmented procurement, long sales cycles (especially in government tenders), and uneven budget allocation can delay implementation of modernization programs. Quality assurance issues (content quality, vendor capability variance) remain a persistent risk in digital and supplementary education categories.

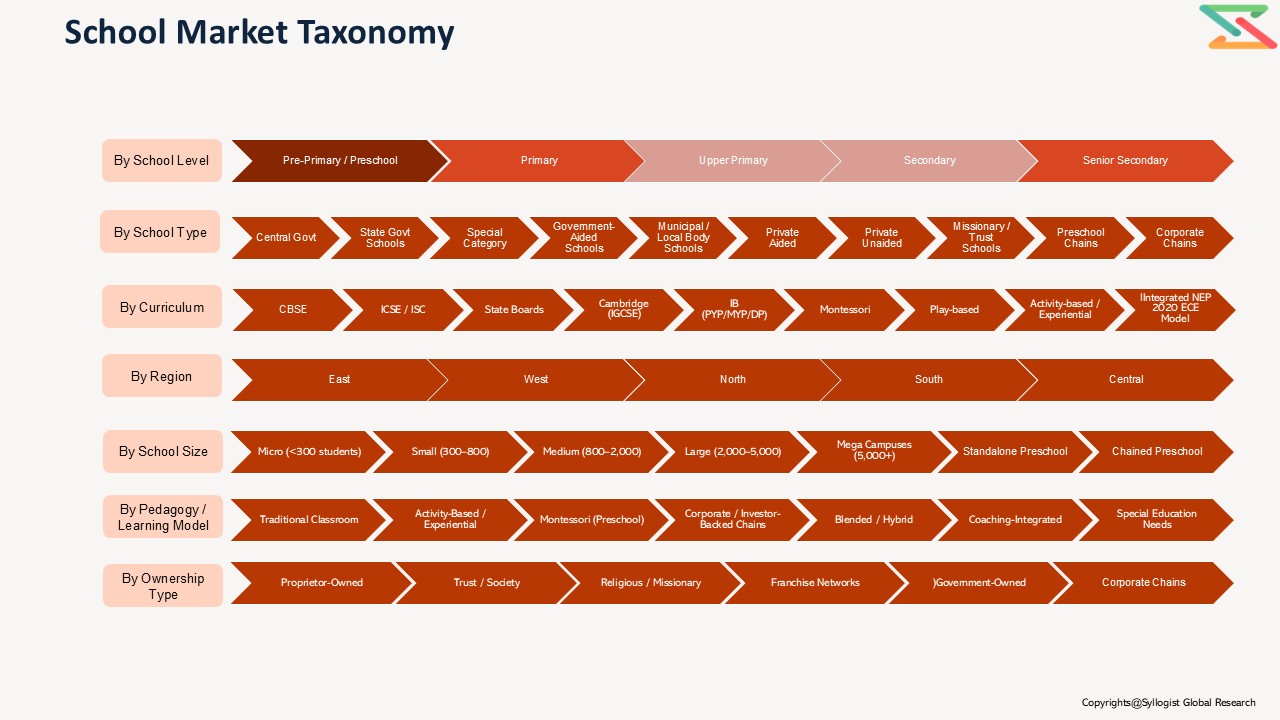

Market Segmentation

Based on School Type, the India School Market is segmented into:

- Government Schools

- Government-Aided Schools

- Private Unaided Schools

- School Chains & Trust-Run Institutions

- International & Premium Schools (IB/IGCSE/ICSE premium)

Based on Education Level:

- Pre-Primary / Early Childhood (ECE)

- Primary (Grades 1–5)

- Upper Primary (Grades 6–8)

- Secondary (Grades 9–10)

- Higher Secondary (Grades 11–12)

Based on Offering / Spend Category:

- Core Academics (Curriculum, Textbooks, Assessments)

- Supplementary Education (Tutoring, Test Prep, Remedial Learning)

- Digital Learning (Smart Classroom, LMS, Devices, Digital Content)

- School Administration & ERP (SIS, Attendance, Fee, Transport, HR)

- Infrastructure & Facilities (Classrooms, Labs, Libraries, Sports, Safety)

- Teacher Training & Professional Development

- Student Services (Transport, Meals, Counseling, Special Education)

Based on Curriculum / Board Affiliation:

- State Boards

- CBSE

- ICSE/ISC

- International Boards (IB/IGCSE and others)

Based on Delivery Mode:

- Traditional (Offline)

- Hybrid (Offline + Digital Support)

- Digital-First / Assisted Digital Classrooms

Based on Geography:

- North, West, South, East, Central, North-East

- Urban vs Rural

- Tier-I, Tier-II, Tier-III/Tier-IV cities

Based on Procurement / Payment Source:

- Government Budget / Tenders

- Household Out-of-Pocket Spend

- CSR/NGO-funded Programs

- Institutional Partnerships (Publishers/Edtech/Service Providers)

All market revenues are presented in USD, with volumes expressed in number of schools, student enrolments, teacher counts, and solution penetration metrics

Historical Year: 2021–2025 | Base Year: 2026 | Estimated Year: 2027 | Forecast Period: 2028–2031

Key Questions this Study Will Answer

- What are the key market statistics and forecasts for the India School Market (number of schools, enrolments, spend by category, penetration of digital solutions, growth trends)?

- How do dynamics vary by school type, board affiliation, education level, and geography?

- What are the most important policy, regulatory, and funding developments shaping India’s schooling ecosystem over 2026–2035?

- Which segments are expanding fastest, budget private schools, school chains, hybrid learning models, supplementary education, digital administration, teacher training, etc.?

- Who are the major competitors and stakeholders, and how do they compete on pricing, distribution, outcomes, and implementation capability?

- What insights emerge from primary research regarding adoption barriers, willingness-to-pay, and unmet needs?

- Introduction And Research Framework

- Product & Market Definition

- Scope Of Study (Preschool, Primary, Upper Primary, Secondary, Sr. Secondary)

- Market Taxonomy

- Research Methodology

- Assumptions & Data Sources

- India School Market Overview

- Evolution Of India’s Education System

- NEP 2020 Impact Overview (ECCE, Foundational Literacy, 5+3+3+4)

- School Density, Enrollment & GER Across Levels

- Public Vs Private School Dynamics

- Key Trends Shaping The Indian School Market

- Regulatory Landscape (RTE, Fee Regulation Acts, Board Regulations)

- India Pre-Primary / Preschool Market Outlook

- Market Structure & Ecosystem

- Market Size & Forecast

- By Value & Volume

- By Type

- Standalone Preschools

- Chained Preschools (Franchise-led)

- Preschool Sections Within K–12 Schools

- By Region

- By School Size

- Fee Structure Analysis (Premium, Mid, Budget)

- Curriculum Models (Montessori, Play-based, NEP ECE)

- Parent Decision Criteria & Trends

- Regional Demand Split (Tier-1/2/3 & Rural)

- Preschool Infrastructure & Service Requirements

- India Primary School Market Outlook

- Market Size & Forecast

- By Value & Volume

- By Ownership

- By Curriculum

- B School Size

- By Pedagogy

- By Region

- Enrollment & Teacher Distribution

- Fee Analysis (Urban vs Rural)

- Curriculum & Pedagogical Practices

- Learning Outcomes & NEP 2020 Foundational Literacy Mandate

- Infrastructure Requirements (ICT, Labs, Classrooms)

- Regional & Socioeconomic Segmentation

- Procurement Behaviour

- Market Size & Forecast

- India Upper Primary/Middle School Market Outlook

- Market Size & Forecast

- By Value & Volume

- By Ownership

- By Curriculum

- B School Size

- By Pedagogy

- By Region

- Transition from Foundational to Preparatory Stage (NEP 2020)

- Curriculum Depth & Subject Expansion

- Fee Evolution & Household Spending Patterns

- Adoption of Digital Learning, Smart Classrooms & Assessments

- School Infrastructure & Facility Needs

- Market Size & Forecast

- India Secondary School Market Outlook

- Market Size & Forecast

- By Value & Volume

- By Ownership

- By Curriculum

- B School Size

- By Pedagogy

- By Region

- High-Stakes Examination Ecosystem & Coaching Integration

- Board-Wise Segmentation: CBSE, ICSE, State Board

- Infrastructure Requirements (Labs, ICT, Vocational Skills Setup)

- Teacher Capability & Subject Specialisation

- Fee Bands & Urban-Rural Split

- Digital & Hybrid Learning Adoption

- Regulatory Environment (Assessment Reforms)

- Market Size & Forecast

- India Senior Secondary School Market Outlook

- Market Size & Forecast

- By Value & Volume

- By Ownership

- By Curriculum

- B School Size

- By Pedagogy

- By Region

- Subject Streams (Science, Commerce, Humanities)

- Coaching-Integrated School Models (NEET/JEE/CLAT/IPMAT)

- Infrastructure: Science Labs, Skill Hubs, AI/Robotics Labs

- Curriculum Reforms under NEP (Choice-based credits)

- Market Size & Forecast

- Market Dynamics (Specific to Schools)

- Drivers

- Challenges

- Trends

- Regional Hotspots

- Opportunity Mapping

- Opportunity Assessment For Stakeholders

- Opportunities for EdTech Players

- Opportunities for Curriculum Providers & Publishers

- Opportunities in Assessments & Teacher Training

- Opportunities in School Infrastructure & ICT

- Investment Opportunities in School Chains & PPP Models

- Competitive Landscape

- Analysis of Top School Chains

- Regional Leaders

- Detailed Benchmarking Analysis

- Detailed School Profiles

- Strategic Recommendations

- Go-to-Market Models for Vendors

- Expansion Strategy for School Chains

- Entry Strategy for International Boards

- Policy Alignment & NEP Implementation Roadmap

- Future of India’s School Market (2035 Vision)