Market Definition

The semiconductor recycling and circular supply chain market refers to a regenerative industrial system designed to replace the traditional linear “take-make-dispose” model with a closed-loop approach focused on minimizing waste and maximizing resource utility throughout the chip lifecycle. This framework encompasses the systematic recovery of high-value materials—such as silicon, gallium, gold, and rare earth elements—from manufacturing scrap and end-of-life electronics, while simultaneously integrating design-for-circularity principles. It involves the coordination of diverse stakeholders across the value chain, from raw material suppliers and foundries to specialized electronics recyclers, to extend product lifespans through reuse, refurbishment, and advanced chemical or physical reclamation processes.

Market Insights

As of early 2026, the global semiconductor recycling and circularity market is experiencing a period of high-velocity growth, reaching an estimated valuation of USD 21.44 billion. This represents a significant year-over-year increase from 2025, sustained by a robust compound annual growth rate (CAGR) of approximately 15.5%. The expansion is primarily driven by the “resource paradox” of the semiconductor industry: while chip sizes continue to shrink, the total volume of chips produced is surging to meet the demands of global AI infrastructure and automotive electrification, creating an unprecedented volume of manufacturing byproducts and electronic waste.

Geographically, the Asia-Pacific region remains the dominant hub, commanding more than half of the global market share. This concentration is anchored by the presence of major foundry ecosystems in Taiwan, South Korea, and China, where manufacturers like TSMC and Samsung have pioneered on-site wafer reclamation and chemical recycling programs to lower operational costs. Meanwhile, North America and Europe are rapidly scaling their domestic recycling capabilities, fueled by government incentives such as the U.S. CHIPS Act and the EU Circular Electronics Initiative, which prioritize supply chain sovereignty and the reduction of “embedded carbon” in high-tech manufacturing.

The “AI-boom” is a critical catalyst for the current market landscape, as the rapid deployment of high-performance GPUs and memory chips in data centers has accelerated the obsolescence of legacy hardware. This has created a steady stream of high-value decommissioned assets that are rich in critical minerals. Furthermore, the automotive sector has emerged as a primary end-user for recycled materials, as modern electric vehicles (EVs) can contain over 3,000 chips. Manufacturers are increasingly adopting “circular sourcing” strategies to secure a stable supply of power semiconductors and sensors while shielding themselves from the volatility of primary mining markets.

From a technological standpoint, 2026 has seen a shift from basic mechanical recycling toward advanced “molecular-level” recovery. Emerging chemical vapor deposition (CVD) reclamation and specialized electrochemical separation techniques are now allowing for the high-purity recovery of compound semiconductor materials like Silicon Carbide (SiC) and Gallium Nitride (GaN). This technological maturation is transforming recycling from a mere waste-management obligation into a strategic revenue stream, as “certified second-hand chips” and reclaimed high-purity substrates begin to find a secondary market in non-critical industrial and IoT applications.

Key Drivers

Critical Mineral Scarcity and Geopolitical Resilience

The primary driver of the circular supply chain is the escalating scarcity and concentrated geographical control of critical raw materials such as lithium, cobalt, germanium, and gallium. Ongoing geopolitical tensions and restrictive trade measures have highlighted the vulnerability of a linear supply model that relies on primary mining. By establishing circular loops, countries can create a “secondary mine” within their own borders, significantly reducing dependence on volatile international markets. As of 2026, this strategy of resource independence is no longer just a sustainability goal but a national security priority for major semiconductor-producing nations.

Regulatory Mandates and Corporate ESG Targets

Tightening global environmental regulations, such as the EU Digital Product Passport and updated WEEE (Waste Electrical and Electronic Equipment) directives, are forcing manufacturers to take responsibility for the entire lifecycle of their products. These mandates require greater transparency in material tracking and higher thresholds for recycled content in new electronics. Simultaneously, leading semiconductor firms have committed to ambitious net-zero targets for 2030 and 2040. Achieving these goals necessitates a radical shift toward circularity to mitigate the high energy and water intensity associated with primary silicon refining and chemical processing.

Key Challenges

High Technical Complexity and Reclamation Costs A major challenge facing the market is the sheer technical difficulty of separating and purifying the complex layers of sophisticated materials used in modern integrated circuits. Chips are composed of microscopic layers of silicon, precious metals, and rare earth elements that are blended intricately during manufacturing. Recovering these materials with the “ultra-pure” quality required for re-entry into the semiconductor fabrication process is a high-cost endeavor. In 2026, while recovery is economically viable for large-scale wafer scrap, the process remains financially problematic for the highly fragmented waste stream of small-form-factor consumer electronics like smartphones.

Lack of Standardized Global Frameworks and Data Transparency The global and highly fragmented nature of the semiconductor supply network poses a significant barrier to standardizing circular practices. There is currently a lack of a definitive, cross-border framework for the certification of reclaimed materials and the handling of hazardous e-waste. Furthermore, concerns regarding intellectual property and data security often hinder the transparency needed for effective circularity. Manufacturers are often hesitant to share detailed component data required for automated disassembly and recycling, fearing that “design-for-circularity” could expose proprietary architectures to competitors or bad actors in the secondary market.

Market Segmentation

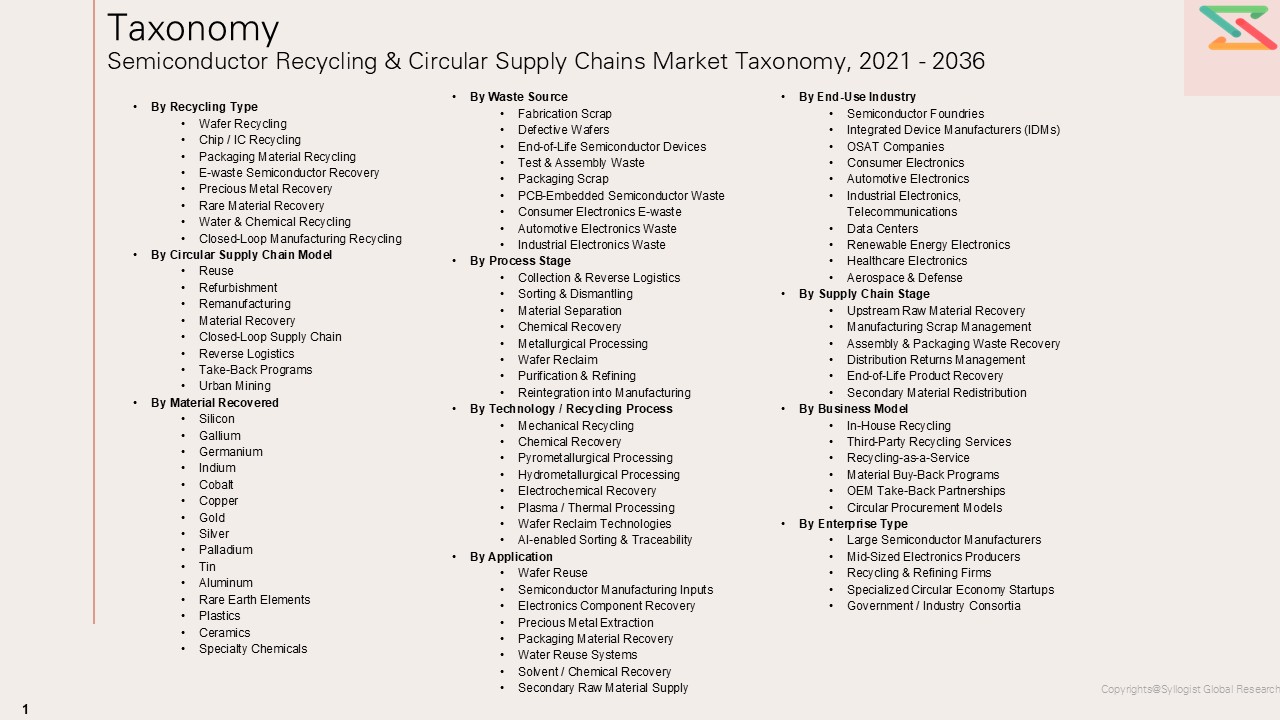

- By Recycling Type

- Wafer Recycling

- Chip / IC Recycling

- Packaging Material Recycling

- E-waste Semiconductor Recovery

- Precious Metal Recovery

- Rare Material Recovery

- Water & Chemical Recycling

- Closed-Loop Manufacturing Recycling

- By Circular Supply Chain Model

- Reuse

- Refurbishment

- Remanufacturing

- Material Recovery

- Closed-Loop Supply Chain

- Reverse Logistics

- Take-Back Programs

- Urban Mining

- By Material Recovered

- Silicon

- Gallium

- Germanium

- Indium

- Cobalt

- Copper

- Gold

- Silver

- Palladium

- Tin

- Aluminum

- Rare Earth Elements

- Plastics

- Ceramics

- Specialty Chemicals

- By Waste Source

- Fabrication Scrap

- Defective Wafers

- End-of-Life Semiconductor Devices

- Test & Assembly Waste

- Packaging Scrap

- PCB-Embedded Semiconductor Waste

- Consumer Electronics E-waste

- Automotive Electronics Waste

- Industrial Electronics Waste

- By Process Stage

- Collection & Reverse Logistics

- Sorting & Dismantling

- Material Separation

- Chemical Recovery

- Metallurgical Processing

- Wafer Reclaim

- Purification & Refining

- Reintegration into Manufacturing

- By Technology / Recycling Process

- Mechanical Recycling

- Chemical Recovery

- Pyrometallurgical Processing

- Hydrometallurgical Processing

- Electrochemical Recovery

- Plasma / Thermal Processing

- Wafer Reclaim Technologies

- AI-enabled Sorting & Traceability

- By Application

- Wafer Reuse

- Semiconductor Manufacturing Inputs

- Electronics Component Recovery

- Precious Metal Extraction

- Packaging Material Recovery

- Water Reuse Systems

- Solvent / Chemical Recovery

- Secondary Raw Material Supply

- By End-Use Industry

- Semiconductor Foundries

- Integrated Device Manufacturers (IDMs)

- OSAT Companies

- Consumer Electronics

- Automotive Electronics

- Industrial Electronics, Telecommunications

- Data Centers

- Renewable Energy Electronics

- Healthcare Electronics

- Aerospace & Defense

- By Supply Chain Stage

- Upstream Raw Material Recovery

- Manufacturing Scrap Management

- Assembly & Packaging Waste Recovery

- Distribution Returns Management

- End-of-Life Product Recovery

- Secondary Material Redistribution

- By Business Model

- In-House Recycling

- Third-Party Recycling Services

- Recycling-as-a-Service

- Material Buy-Back Programs

- OEM Take-Back Partnerships

- Circular Procurement Models

- By Enterprise Type

- Large Semiconductor Manufacturers

- Mid-Sized Electronics Producers

- Recycling & Refining Firms

- Specialized Circular Economy Startup

- Government / Industry Consortia

All market revenues are presented in USD

Historical Year: 2021–2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027–2036

Key Questions this Study Will Answer

- What is the projected market valuation and growth rate (CAGR) for the RaaS model through 2031? This provides the quantitative baseline required for long-term strategic planning and capital allocation across various industrial sectors.

- How does the transition from CapEx to OpEx models specifically lower the entry barriers for Small and Medium Enterprises (SMEs)? The study will evaluate how subscription-based pricing democratizes access to advanced automation and accelerates adoption in previously underserved markets.

- Which industrial segments (e.g., logistics, healthcare, or agriculture) are poised for the highest RaaS adoption rates? Identifying these high-velocity sectors allows providers to tailor their hardware and software stacks to meet specific operational demands.

- What are the primary technological enablers, such as 5G, Edge Computing, and Agentic AI, that are making RaaS scalable in 2026? This question focuses on the infrastructure required to manage large-scale, cloud-connected robotic fleets with minimal latency.

- Who are the dominant market incumbents and emerging startups, and what are their unique value propositions? A detailed competitive analysis will reveal market share concentration and the service models (e.g., pay-per-pick vs. monthly subscription) that are currently winning.

- What are the most significant legal, cybersecurity, and data governance risks associated with third-party robotic management? This analysis provides a framework for mitigating risks related to data breaches, industrial espionage, and liability in autonomous environments.

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Consumer & Demand Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Geographic & Regional Trends

- Risk Assessment Framework

- Political / Geopolitical Risk

- Fuel & Component Supply Risk

- Environmental and Regulatory Risk

- Financial / Market Risk

- Regulatory Framework & Standards

- Global Semiconductor Recycling & Circular Supply Chains Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Recycling Type

- Wafer Recycling

- Chip / IC Recycling

- Packaging Material Recycling

- E-waste Semiconductor Recovery

- Precious Metal Recovery

- Rare Material Recovery

- Water & Chemical Recycling

- Closed-Loop Manufacturing Recycling

- Market Size & Forecast by Circular Supply Chain Model

- Reuse

- Refurbishment

- Remanufacturing

- Material Recovery

- Closed-Loop Supply Chain

- Reverse Logistics

- Take-Back Programs

- Urban Mining

- Market Size & Forecast by Material Recovered

- Silicon

- Gallium

- Germanium

- Indium

- Cobalt

- Copper

- Gold

- Silver

- Palladium

- Tin

- Aluminum

- Rare Earth Elements

- Plastics

- Ceramics

- Specialty Chemicals

- Market Size & Forecast by Waste Source

- Fabrication Scrap

- Defective Wafers

- End-of-Life Semiconductor Devices

- Test & Assembly Waste

- Packaging Scrap

- PCB-Embedded Semiconductor Waste

- Consumer Electronics E-waste

- Automotive Electronics Waste

- Industrial Electronics Waste

- Market Size & Forecast by Process Stage

- Collection & Reverse Logistics

- Sorting & Dismantling

- Material Separation

- Chemical Recovery

- Metallurgical Processing

- Wafer Reclaim

- Purification & Refining

- Reintegration into Manufacturing

- Market Size & Forecast by Technology / Recycling Process

- Mechanical Recycling

- Chemical Recovery

- Pyrometallurgical Processing

- Hydrometallurgical Processing

- Electrochemical Recovery

- Plasma / Thermal Processing

- Wafer Reclaim Technologies

- AI-enabled Sorting & Traceability

- Market Size & Forecast by Application

- Wafer Reuse

- Semiconductor Manufacturing Inputs

- Electronics Component Recovery

- Precious Metal Extraction

- Packaging Material Recovery

- Water Reuse Systems

- Solvent / Chemical Recovery

- Secondary Raw Material Supply

- Asia-Pacific Semiconductor Recycling & Circular Supply Chains Market Outlook

- Market Size & Forecast

- By Value

- By Recycling Type

- By Circular Supply Chain Model

- By Material Recovered

- By Waste Source

- By Process Stage

- By Technology / Recycling Process

- By Application

- By End-Use Industry

- By Supply Chain Stage

- By Business Model

- By Enterprise Type

- Market Size & Forecast

- Europe Semiconductor Recycling & Circular Supply Chains Market Outlook

- Market Size & Forecast

- By Value

- By Recycling Type

- By Circular Supply Chain Model

- By Material Recovered

- By Waste Source

- By Process Stage

- By Technology / Recycling Process

- By Application

- By End-Use Industry

- By Supply Chain Stage

- By Business Model

- By Enterprise Type

- Market Size & Forecast

- North America Semiconductor Recycling & Circular Supply Chains Market Outlook

- Market Size & Forecast

- By Value

- By Recycling Type

- By Circular Supply Chain Model

- By Material Recovered

- By Waste Source

- By Process Stage

- By Technology / Recycling Process

- By Application

- By End-Use Industry

- By Supply Chain Stage

- By Business Model

- By Enterprise Type

- Market Size & Forecast

- Latin America Semiconductor Recycling & Circular Supply Chains Market Outlook

- Market Size & Forecast

- By Value

- By Recycling Type

- By Circular Supply Chain Model

- By Material Recovered

- By Waste Source

- By Process Stage

- By Technology / Recycling Process

- By Application

- By End-Use Industry

- By Supply Chain Stage

- By Business Model

- By Enterprise Type

- Market Size & Forecast

- Middle East & Africa Semiconductor Recycling & Circular Supply Chains Market Outlook

- Market Size & Forecast

- By Value

- By Recycling Type

- By Circular Supply Chain Model

- By Material Recovered

- By Waste Source

- By Process Stage

- By Technology / Recycling Process

- By Application

- By End-Use Industry

- By Supply Chain Stage

- By Business Model

- By Enterprise Type

- Market Size & Forecast

- Country Wise* Semiconductor Recycling & Circular Supply Chains Market Outlook

- Market Size & Forecast

- By Value

- By Recycling Type

- By Circular Supply Chain Model

- By Material Recovered

- By Waste Source

- By Process Stage

- By Technology / Recycling Process

- By Application

- By End-Use Industry

- By Supply Chain Stage

- By Business Model

- By Enterprise Type

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Germany, United Kingdom, France, Italy, Spain, Netherlands, Switzerland, China, Japan, India, South Korea, Australia, Brazil, Mexico, Saudi Arabia, South Africa, UAE

- Technology Landscape & Innovation Analysis

- Value Chain & Supply Chain Analysis

- Pricing Analysis

- Sustainability & Energy Efficiency

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented Vs Consolidated)

- Top 5 Players Market Share

- HHI (Herfindahl–Hirschman Index) Concentration Analysis

- Competitive Intensity Map

- Player Classification

- Market Leaders

- Strong Challengers

- Specialist / Niche Players

- Emerging Players

- Regional Players

- Competitive Analysis Frameworks

- Market Share Analysis

- Company Profile

- Company Overview & HQ

- Products & Solutions Portfolio

- Overall Revenue & Segmental Revenue

- Geographic Presence

- Recent Developments (M&A, Launches, Partnerships)

- SWOT Analysis

- Strategic Focus Areas

- Competitive Positioning Map

- Market Structure & Concentration

- Strategic Output

- Market Opportunity Matrix

- White Space Opportunity Analysis

- Strategic Recommendations

- Raw Material Recovery & Feedstock Strategy

- Closed-Loop Supply Chain Strategy

- Technology & Innovation Strategy

- Partnerships & Ecosystem Strategy

- Regional Expansion Strategy

- Cost & Commercial Strategy

- ESG & Regulatory Strategy

- Risk Management Strategy

- Investment & Long-Term Growth Strategy

- Strategic Priority Matrix & Roadmap

- Near-term (2025–2028)

- Mid-term (2029–2032)

- Long-term (2033–2036)