Market Definition

The Global Smart Parcel Locker Networks Market encompasses the design, manufacturing, software development, installation, operation, and lifecycle management of electronically controlled, network-connected unattended parcel reception and dispatch stations that enable the contactless deposit, retrieval, and reverse logistics processing of parcels and packages by couriers, consumers, retailers, and logistics operators without requiring the physical presence of a recipient or sender at the moment of handoff, providing a shared infrastructure solution to the first-attempt delivery failure, missed delivery, and last-mile logistics inefficiency challenges that constrain the profitability and consumer satisfaction performance of e-commerce fulfillment and parcel delivery networks operating at scale across urban, suburban, and rural deployment environments. The product and system scope of this market includes outdoor and indoor multi-compartment automated parcel locker stations incorporating electronically actuated compartment locking mechanisms, touchscreen or mobile device-controlled user interfaces, optical barcode and two-dimensional code scanning systems, near field communication and Bluetooth reader modules for contactless access authentication, integrated parcel condition and temperature monitoring sensors, remote management and diagnostics connectivity, and modular compartment size configurations allowing simultaneous storage of parcels ranging from small envelope-sized packages to large appliance-sized freight shipments within a single locker station footprint, refrigerated and temperature-controlled parcel locker units incorporating active cooling and heating systems that maintain defined temperature zones for the storage and collection of perishable grocery items, fresh meal delivery orders, pharmaceutical products requiring cold chain continuity, and frozen food shipments whose quality and safety integrity depend on uninterrupted temperature control from dispatch facility to consumer collection, high-security parcel locker configurations incorporating surveillance cameras, tamper detection sensors, biometric authentication options, and reinforced compartment construction for the storage of high-value electronics, pharmaceutical controlled substances, financial documents, and government-issued identity and travel documents requiring enhanced security assurance, carrier-agnostic open-network locker systems that accept parcel deposits from multiple competing courier companies and e-commerce operators through standardized application programming interfaces and universal access credential systems, enabling shared infrastructure utilization that improves location economics compared with operator-proprietary closed locker networks, automated parcel locker management software platforms encompassing network operations management, compartment inventory optimization, dynamic compartment size allocation, predictive maintenance scheduling, consumer notification and collection journey management, carrier integration middleware, and analytics dashboards delivering utilization performance, carrier service level, and consumer experience metrics to network operators and logistics service clients, return logistics processing locker systems that enable consumers to deposit return parcels at locker stations for collection by courier drivers without requiring consumer presence at home or in-store return interactions, and the emerging category of smart parcel lockers integrated with autonomous delivery robot and drone landing infrastructure enabling fully automated end-to-end delivery from warehouse dispatch to consumer collection without human courier involvement in the terminal delivery stage. The technology landscape within this market spans basic electronically controlled locker stations with proprietary access code systems at the entry tier, through connected multi-carrier locker systems with mobile application integration and cloud-based network management at the mainstream commercial tier, to advanced locker platforms incorporating artificial intelligence-based compartment allocation optimization, machine learning-driven predictive maintenance, computer vision parcel condition assessment, and integration with urban autonomous delivery ecosystems at the premium innovation tier. The value chain of this market extends from electronic hardware component suppliers providing microcontrollers, locking actuators, display panels, connectivity modules, and sensor systems, through locker station enclosure and mechanical assembly manufacturers, software platform developers, systems integrators deploying and commissioning locker networks, telecommunications infrastructure providers supporting locker station connectivity, property and real estate operators hosting locker installations at residential buildings, retail locations, transit hubs, petrol stations, grocery stores, and public spaces, parcel network operators and e-commerce logistics companies deploying locker networks as last-mile delivery infrastructure, and the residential consumers, small business recipients, and public sector agencies whose collection behavior and service satisfaction define the commercial performance and network value of smart parcel locker installations globally.

Market Insights

The global smart parcel locker networks market is experiencing a period of accelerating commercial deployment and strategic investment in 2026, driven by the structural growth of e-commerce parcel volumes that are straining the capacity and economics of conventional home delivery courier networks, the progressive adoption of out-of-home delivery as a consumer behavior norm in European, Asian, and North American markets where parcel locker convenience and collection flexibility have demonstrated the ability to convert initial trial users into habitual out-of-home delivery customers, and the intensifying logistics operator demand for capital-efficient last-mile delivery infrastructure that can absorb growing parcel volumes at lower cost per delivery than adding proportional numbers of human couriers to increasingly congested and operationally expensive urban delivery operations. The global smart parcel locker networks market was valued at approximately USD 1.8 billion in 2025 and is projected to expand at a compound annual growth rate of 14 percent through 2036, reaching approximately USD 7.8 billion by the end of the forecast period, a trajectory underpinned by the expansion of parcel locker installation density in established markets across Germany, Japan, South Korea, and the Nordic countries toward the network coverage levels at which locker availability within walking distance of the majority of the served population generates the habitual adoption rates that establish out-of-home delivery as the default rather than the alternative delivery mode for a growing proportion of e-commerce parcel volume. The competitive landscape of the market encompasses national postal operators deploying proprietary locker networks as a strategic modernization of their parcel delivery infrastructure, major e-commerce platform operators investing in owned or partnered locker networks to reduce last-mile delivery dependency on third-party couriers, dedicated parcel locker technology companies providing network-as-a-service platform models to logistics clients, automated locker hardware manufacturers serving the global market with modular and customizable station product ranges, and the growing ecosystem of property technology companies, retail chains, petrol station operators, and transit authorities whose real estate hosting relationships with locker network operators are defining the geographic coverage and consumer accessibility of parcel locker infrastructure across urban and suburban geographies.

A defining commercial and technological trend reshaping the competitive dynamics and customer value proposition of the smart parcel locker market is the progressive transition from closed carrier-proprietary locker networks, in which individual courier companies operate dedicated locker infrastructure accessible only to their own delivery drivers and customers, toward open carrier-agnostic network models in which a single locker installation accepts parcel deposits from multiple competing carriers and e-commerce platforms through standardized integration interfaces, enabling the shared utilization of locker infrastructure across the full breadth of the local parcel delivery market and substantially improving the unit economics of locker station investment by distributing fixed capital and operating costs across a larger and more diverse throughput volume. The carrier-agnostic open network model delivers a superior consumer experience relative to carrier-specific alternatives by enabling recipients to collect parcels from any participating carrier at a single familiar locker location rather than maintaining separate collection relationships with multiple carrier-specific locker networks across their local geography, a convenience consolidation advantage that research across multiple European and Asian markets has demonstrated translates into measurably higher repeat collection rates and consumer net promoter scores compared with single-carrier locker experiences. The commercial infrastructure of open locker networks requires the development of standardized carrier integration application programming interfaces, neutral network operator business models that charge carriers a per-parcel deposit fee while maintaining carrier independence, universal consumer notification and collection workflow platforms that handle multi-carrier parcel status communication through a single consumer-facing application, and regulatory frameworks that in some European markets are being developed to mandate open access to publicly funded locker infrastructure as a condition of government co-investment in national locker network coverage expansion programs, collectively creating the technical and commercial ecosystem within which carrier-agnostic open locker networks are displacing carrier-proprietary alternatives as the dominant deployment model in the most commercially mature parcel locker markets globally.

The refrigerated and temperature-controlled parcel locker segment represents the most commercially dynamic and highest-value-growth category within the smart parcel locker market, driven by the intersection of accelerating consumer adoption of online grocery shopping and fresh meal kit delivery services whose cold chain continuity requirements from dispatch to consumer collection cannot be satisfied by ambient temperature lockers, the post-pandemic structural shift in consumer willingness to purchase perishable food, pharmaceutical, and health and beauty products through online channels that has created a large and growing addressable market for temperature-controlled unattended delivery solutions, and the operational and financial limitations of time-window home delivery for perishables whose narrow acceptable delivery windows, high failed delivery rates, and elevated per-delivery courier cost structure are creating strong commercial demand for temperature-controlled locker alternatives that enable flexible collection at consumer-convenient times without imposing time window constraints on recipients or logistics operators. The technical specifications required for temperature-controlled parcel lockers, including compressor-based active refrigeration systems maintaining precise temperature zones across ambient, chilled, and frozen compartments simultaneously within a single outdoor locker enclosure, weatherproofed construction capable of maintaining specified internal temperatures across the full range of ambient outdoor temperature and humidity conditions experienced in deployment locations, energy management systems optimizing cooling system operation for minimum electricity consumption without compromising temperature zone integrity, and remote temperature monitoring and alarm systems ensuring cold chain compliance documentation for pharmaceutical and food safety regulatory purposes, represent substantial engineering complexity relative to ambient locker stations and are driving significant product development investment among premium locker manufacturers competing for the growing refrigerated locker deployment programs of grocery retailers, meal kit companies, pharmaceutical distributors, and parcel network operators serving the perishables delivery market.

From a regional perspective, Europe represents the most commercially mature and densely deployed regional market for smart parcel locker networks, led by Germany, Poland, the United Kingdom, the Nordic countries, and the Baltic states where the combination of high e-commerce penetration, dense urban populations, strong consumer acceptance of out-of-home delivery, and in several cases government-supported national locker network development programs has created locker network coverage densities that are approaching the point of ubiquitous accessibility for the majority of the urban and suburban population. Germany’s national parcel locker network operated by its postal incumbent represents one of the world’s largest and most utilized locker networks by installation count, consumer registration, and parcel throughput, providing a commercially validated proof of concept for the mass-market out-of-home delivery model that is being referenced by logistics operators and national postal services in other European markets developing their own network expansion strategies. Asia-Pacific represents the largest regional market for parcel locker installations by total unit count, driven by the extraordinary e-commerce parcel volumes generated by the Chinese, Japanese, South Korean, and Southeast Asian markets whose combination of high urban residential density, strong digital consumer engagement, and the geographic concentration of apartment dwelling populations in multi-story residential buildings creates exceptionally favorable conditions for parcel locker deployment economics and consumer adoption. North America represents the most significant near-term growth opportunity for smart parcel locker network expansion relative to current market penetration, as the United States and Canada have historically lower parcel locker adoption relative to European and Asian markets despite comparable e-commerce parcel volumes, creating a structural underpenetration gap that major e-commerce operators, postal services, and dedicated locker network companies are actively addressing through accelerated deployment programs targeting residential multifamily complexes, grocery retail chains, transit hub locations, and petrol station convenience store networks across major metropolitan areas.

Key Drivers

Structural Growth of E-Commerce Parcel Volumes and the Escalating Last-Mile Delivery Cost and Failed Delivery Rate Pressures Driving Logistics Operator Investment in Locker Infrastructure

The most structurally powerful and commercially immediate demand driver for smart parcel locker network investment is the sustained and accelerating growth of e-commerce parcel volumes that is creating a fundamental mismatch between the capacity, cost structure, and operational flexibility of conventional home delivery courier networks and the service level, delivery cost, and first-attempt success rate performance that both e-commerce operators and their customers expect at acceptable delivery charges, a mismatch whose resolution requires the deployment of alternative delivery infrastructure capable of absorbing growing parcel volumes at lower cost per delivery without degrading the consumer experience that drives e-commerce repurchase and customer lifetime value. The economics of conventional last-mile home delivery are being progressively eroded by the combination of urban traffic congestion increasing courier vehicle dwell time and reducing deliveries per shift, rising courier labor costs driven by minimum wage legislation and logistics labor market competition, the high proportion of residential delivery attempts that fail on the first attempt due to recipient absence during business hours generating costly and operationally disruptive redelivery cycles, the carbon emission and traffic impact of the growing fleet of delivery vehicles required to serve expanding e-commerce parcel volumes that is attracting regulatory restriction in an increasing number of European cities, and the competitive pricing pressure from e-commerce platforms offering free delivery that compresses the per-delivery revenue available to logistics operators below the fully loaded cost of individual home delivery attempts in mature urban markets. Smart parcel locker networks address each dimension of this last-mile economics challenge by enabling courier drivers to deposit multiple parcels at a single locker station stop rather than making individual residential delivery attempts, dramatically increasing the number of parcels deposited per vehicle shift and reducing the cost per delivery; by eliminating failed first-attempt deliveries entirely for the parcel volume routed through lockers, removing the largest single source of avoidable cost in conventional courier operations; and by enabling the consolidation of delivery vehicle trips to locker stations during off-peak hours that reduces urban congestion impact and supports the regulatory compliance requirements of emission-controlled urban delivery zones. The financial significance of these cost reduction benefits to major logistics operators whose scale of parcel delivery operations translates locker-enabled efficiency improvements into hundreds of millions of USD of annual operating cost savings at full deployment scale is driving the capital investment commitments and strategic partnership structures with locker technology providers that are financing the rapid expansion of parcel locker installation density in major metropolitan markets.

Changing Consumer Delivery Preferences and the Growing Adoption of Flexible Out-of-Home Collection as a Convenience-Driven Alternative to Constrained Home Delivery Time Windows

The second major structural demand driver reshaping the trajectory of smart parcel locker network investment is the documented and accelerating shift in consumer delivery preference from time-constrained home delivery toward flexible out-of-home collection at conveniently located parcel locker stations, a behavioral transition that in markets with sufficient locker network density is generating habitual adoption patterns among a growing proportion of active e-commerce shoppers who have experienced the convenience of collection at a time and location of their choosing and who are actively selecting out-of-home delivery options at checkout when locker locations within acceptable proximity of their home or commute route are offered. Consumer research across multiple European and Asian markets where parcel locker networks have achieved meaningful density consistently identifies the combination of collection flexibility, delivery reliability, and elimination of the failed delivery frustration experience as the primary motivators for consumer adoption of parcel locker collection, preferences that are particularly strongly expressed among younger demographic cohorts, urban apartment dwellers, active commuters passing transit hub locker locations, and remote workers who value the security of a guaranteed successful delivery over the uncertain prospect of being available at home during a specified delivery window. The growth of proximity-based parcel locker adoption is creating a network effect dynamic in which each incremental improvement in locker network density across a metropolitan area increases the proportion of the local population for whom a conveniently located locker is accessible, generating additional consumer adoption that increases average locker throughput, which in turn improves the per-station unit economics that support further network density investment in a self-reinforcing cycle that has been observed in mature markets including Germany, Japan, and South Korea where out-of-home delivery market share has reached levels that structurally reduce the home delivery volume proportion of total parcel throughput. The integration of parcel locker collection into the native checkout and delivery selection interfaces of major e-commerce platforms, which present locker location options with real-time compartment availability information alongside home delivery alternatives during the purchase flow, is significantly accelerating consumer adoption by embedding the locker collection option at the moment of delivery decision rather than requiring consumers to proactively seek out locker alternatives, and the data emerging from markets where this checkout-integrated locker selection has been deployed shows a substantial proportion of eligible consumers selecting locker delivery when the nearest available location is within their acceptable proximity threshold, providing logistics operators with strong commercial evidence for continued investment in locker network density expansion.

Key Challenges

Real Estate Availability and Hosting Partner Economics Creating Deployment Bottlenecks and Limiting Locker Network Coverage Density in Key Urban and Suburban Markets

The most operationally significant challenge constraining the pace and geographic comprehensiveness of smart parcel locker network deployment is the difficulty of securing suitable real estate locations at commercially viable hosting terms across the range of location types, including residential building lobbies, retail forecourts, transit station premises, petrol station sites, and public footpath locations, whose coverage is required to achieve the locker accessibility density at which a sufficient proportion of the served population can reach a locker within their acceptable walking or travel distance to drive habitual out-of-home delivery adoption at the market share levels required for locker network unit economics to reach commercial sustainability. The real estate challenge is multidimensional, encompassing the physical space availability constraint in high-density urban environments where the footprint required for a multi-compartment locker station with sufficient capacity for the local parcel throughput volume may not be available within the interior floor area of candidate hosting properties or on the exterior footpath area adjacent to candidate retail premises, the electrical supply and connectivity infrastructure requirement that not all candidate hosting locations can readily satisfy for the power and network connectivity that outdoor locker installations require, and the commercial terms negotiation complexity that arises when locker network operators seek hosting agreements with property owners, retail chains, transit authorities, and municipal governments who each have distinct property valuation, liability, maintenance responsibility, and revenue sharing frameworks that must be individually negotiated and managed at the scale of a national locker deployment program covering hundreds or thousands of installation sites. The economics of locker hosting arrangements are particularly challenging in the high-value urban real estate markets where locker network coverage density is most needed for consumer adoption, as the opportunity cost of allocating lobby or forecourt space to a parcel locker station rather than to revenue-generating retail or hospitality uses is higher in prime urban locations than in suburban or rural contexts, requiring locker network operators to either offer hosting fees that improve the economics of the hosting arrangement for property owners or to develop property partnership models in which the locker installation provides demonstrable value to the host property by improving resident or customer satisfaction, reducing package theft liability, or supporting sustainable delivery accreditation objectives that are commercially valued by the hosting property’s own customers or tenants. The emergence of building-integrated locker infrastructure standards in new residential construction projects, driven by progressive building code requirements in several European and Asian jurisdictions that mandate the provision of parcel reception facilities meeting defined technical specifications in new multifamily residential buildings, represents a partial but structurally important solution to the hosting challenge by embedding locker infrastructure into the construction economics of new buildings rather than requiring retrospective negotiation of hosting agreements in existing built environments.

Consumer Awareness, Behavioral Adoption Barriers, and the Investment Required to Establish Habitual Out-of-Home Delivery Usage at Commercially Viable Market Share Levels

A structurally significant commercial challenge limiting the speed at which smart parcel locker networks achieve the consumer adoption rates and average station utilization levels required for commercial network economics to reach viability is the persistence of consumer behavioral inertia toward home delivery as the default e-commerce delivery mode, combined with awareness gaps about locker network locations and service capabilities and the friction associated with the initial registration, application download, and first collection experience that new locker users must navigate before the convenience advantages of out-of-home delivery become apparent through personal experience. Consumer research in markets where parcel locker networks exist but have not yet achieved high adoption rates consistently identifies a substantial proportion of active e-commerce shoppers who are aware that parcel lockers exist but have never used them, citing reasons including uncertainty about how the collection process works, concern about compartment size adequacy for their typical parcel dimensions, unfamiliarity with the nearest locker location, and a preference for the perceived convenience of home delivery that persists until a negative home delivery experience such as a failed delivery, parcel theft, or time window inconvenience motivates a trial of the locker alternative. Overcoming this behavioral adoption barrier requires sustained consumer communication investment by both locker network operators and the e-commerce platforms and logistics companies whose delivery networks route parcels through locker infrastructure, encompassing awareness campaigns promoting locker locations and service capabilities, frictionless locker selection integration within e-commerce checkout flows that presents locker alternatives with proximity information and real-time availability, incentive structures offering delivery fee discounts or loyalty program rewards for locker selection that improve the economic attractiveness of out-of-home delivery relative to home delivery for cost-sensitive consumers, and service recovery programs that rapidly and generously resolve the collection difficulties and technical issues that early adopters encounter in initial locker interactions and that, if handled poorly, generate negative word-of-mouth that suppresses adoption in the broader consumer population. The consumer adoption investment required to drive locker network utilization from the low rates typical of newly installed networks toward the commercially sustainable throughput levels that justify continued network expansion is a significant near-term cost burden for locker network operators that compresses margins during the market development phase and requires patient capital whose return timeline is measured in years rather than months, creating a financial profile that favors well-capitalized operators with long investment horizons over smaller entrants whose financial resources may be insufficient to sustain the consumer adoption investment required to achieve network density and utilization economics in competitive metropolitan markets where established operators have already begun the adoption development process.

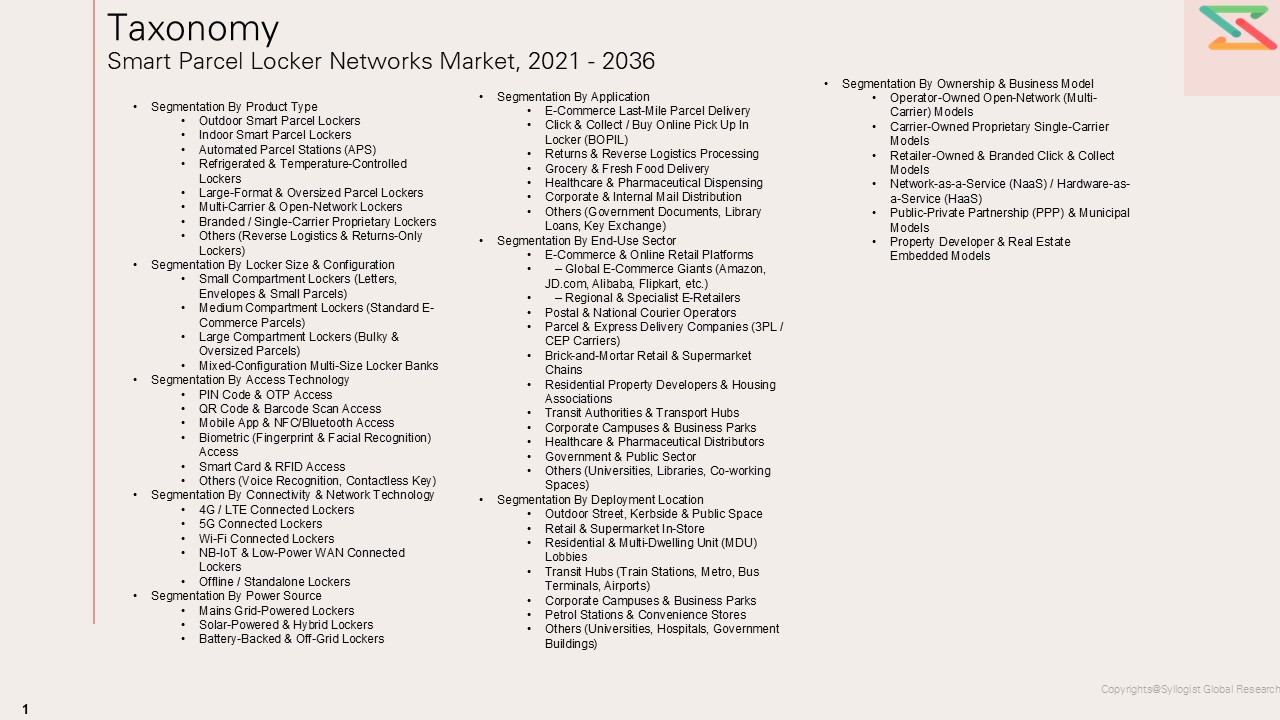

Market Segmentation

- Segmentation By Locker Type

- Ambient Temperature Standard Parcel Lockers

- Refrigerated and Temperature-Controlled Lockers

- Frozen Compartment Parcel Lockers

- Multi-Zone Temperature (Ambient, Chilled, and Frozen) Lockers

- High-Security and High-Value Parcel Lockers

- Returns Processing and Reverse Logistics Lockers

- Automated Parcel Lockers with Robotic Internal Handling

- Autonomous Delivery Robot and Drone-Compatible Locker Stations

- Others

- Segmentation By Network Model

- Carrier-Proprietary Closed Network Lockers

- Open Carrier-Agnostic Multi-Operator Network Lockers

- Retailer and Brand-Owned Dedicated Locker Networks

- Postal Operator National Locker Networks

- Third-Party Independent Locker Network Operator Platforms

- Public-Private Partnership Municipal Locker Networks

- Others

- Segmentation By Installation Location

- Residential Multifamily Building Lobbies

- Grocery and Supermarket In-Store and Forecourt

- Petrol Station and Convenience Store Sites

- Rail and Metro Station Concourses

- Bus Terminal and Transport Hub Locations

- Shopping Mall and Retail Park Premises

- University and Campus Facilities

- Healthcare and Hospital Sites

- Workplace and Office Building Lobbies

- Public Footpath and Street Furniture Locations

- Suburban and Rural Community Hubs

- Others

- Segmentation By Compartment Size Configuration

- Small Compartments (Envelopes and Small Parcels)

- Medium Compartments (Standard E-Commerce Parcels)

- Large Compartments (Oversized and Bulky Parcels)

- Extra-Large Compartments (Appliances and Large Freight)

- Mixed Multi-Size Configuration Stations

- Segmentation By Access and Authentication Technology

- PIN Code and One-Time Password Access

- QR Code and Barcode Scanner Access

- Near Field Communication (NFC) and RFID Card Access

- Mobile Application Bluetooth and Wi-Fi Access

- Biometric Fingerprint and Facial Recognition Access

- Multi-Factor Authentication Systems

- Others

- Segmentation By End-Use Application

- E-Commerce and General Parcel Delivery

- Fresh Grocery and Perishable Food Delivery

- Pharmacy and Healthcare Product Delivery

- Meal Kit and Prepared Food Delivery

- Consumer Electronics and High-Value Goods

- Document and Government Credential Distribution

- E-Commerce Returns and Reverse Logistics

- Click-and-Collect Retail Fulfillment

- Peer-to-Peer Parcel Exchange

- Others

- Segmentation By End User

- National Postal Operators and Universal Service Providers

- E-Commerce Platform Operators

- Third-Party Logistics and Courier Companies

- Grocery and Quick Commerce Retailers

- Pharmaceutical and Healthcare Distributors

- Real Estate Developers and Property Managers

- Municipal Governments and Urban Authorities

- Others

- Segmentation By Component

- Locker Hardware and Enclosure Systems

- Electronic Locking and Actuation Mechanisms

- Touchscreen and User Interface Hardware

- Connectivity and IoT Communication Modules

- Network Management and Operations Software

- Consumer Mobile Application Platforms

- Carrier Integration Middleware and APIs

- Analytics and Business Intelligence Platforms

- Installation, Maintenance, and Field Services

- Others

- Segmentation By Region

- Europe

- Asia-Pacific

- North America

- Latin America

- Middle East and Africa

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2036

Key Questions this Study Will Answer

- What is the projected global market valuation and installation count for smart parcel locker networks through 2036, segmented by locker type, network model, installation location, end-use application, component, and region, and which product categories and geographic markets are expected to generate the highest incremental revenue and network expansion growth across the forecast period?

- How is the transition from carrier-proprietary closed locker networks to open carrier-agnostic multi-operator network models reshaping the competitive landscape, business model economics, and infrastructure investment strategies of parcel locker network operators, and what carrier integration standards, neutral platform commercial structures, and regulatory open-access frameworks are most effectively accelerating this transition in the most commercially mature European and Asian parcel locker markets?

- What is the commercial trajectory and technical development roadmap of refrigerated and temperature-controlled parcel locker deployment serving online grocery, fresh meal delivery, pharmaceutical, and perishables e-commerce fulfillment applications, and how are the engineering specifications, energy management requirements, cold chain compliance documentation capabilities, and total cost of ownership characteristics of leading temperature-controlled locker platforms evolving to serve the growing commercial demand from grocery retailers, meal kit operators, and pharmaceutical distributors?

- What is the consumer behavioral adoption curve for out-of-home parcel locker collection across different demographic segments, e-commerce purchase frequency cohorts, and proximity threshold sensitivity profiles in North America, Europe, and Asia-Pacific, and what checkout integration, incentive structure, consumer communication, and first-experience quality design strategies are most effectively converting aware but non-adopting consumers into habitual locker collection users in markets where network density is already sufficient to enable broad adoption?

- How are the real estate hosting partner economics, building code integration requirements for new residential and commercial construction, municipal public space allocation frameworks, and urban logistics sustainability policy incentives in leading metropolitan markets evolving to reduce the location scarcity and hosting term negotiation challenges that constrain parcel locker network density expansion, and what property technology, building integration, and public infrastructure partnership models are most effectively accelerating locker deployment in the highest-priority urban coverage gaps?

- Who are the leading smart parcel locker hardware manufacturers, network management software platform developers, national postal operator locker network operators, dedicated third-party locker network companies, and e-commerce platform logistics innovators currently defining the competitive landscape of the global smart parcel locker networks market, and what are their respective product portfolio strategies, network expansion investment plans, carrier partnership structures, temperature-controlled product development roadmaps, and autonomous delivery integration strategies for advancing parcel locker network coverage and service capability through the forecast horizon?

- Product Definition

- Scope of the Study

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Industry Publications, Logistics & Postal Association Reports & Press Releases

- Government Urban Planning, Smart City & Last-Mile Delivery Policy Data (USDOT, EC, MoUD, etc.)

- Smart Parcel Locker Deployment, Network Density & Utilisation Rate Statistics

- E-Commerce Order Volume, Failed Delivery & Returns Rate Databases

- Primary Research Design & Execution

- In-depth Interviews with Locker Network Operators, E-Commerce Platforms, Postal Operators & Property Developers

- Surveys with Retailers, Third-Party Logistics (3PL) Providers, Municipal Bodies & End Consumers

- Expert Panel Validation

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Bottom-Up & Top-Down Reconciliation

- Locker Unit Deployment, Network Coverage & Parcel Volume-Based Market Sizing Model

- Failed Delivery Cost Reduction & Consumer Convenience Adoption Rate-Driven Demand Model

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Technology & Innovation Highlights

- Network Economics & Unit Economics Summary

- Average Locker Unit CAPEX & OPEX Benchmarks

- Operator vs Carrier Margin & Profitability Analysis

- Outdoor, Indoor & Automated Parcel Station (APS) Revenue Model Summary

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Geographic & Regional Trends

- Risk Assessment Framework

- Geopolitical & Trade Policy Risk

- Hardware Component, Electronics & Steel Supply Chain Volatility Risk

- Vandalism, Theft & Physical Security Risk

- Financial / Market Risk

- Cybersecurity, Data Privacy & Digital Access Risk

- Real Estate, Site Access & Municipal Permitting Risk

- Consumer Adoption, Behavioural Change & Awareness Risk

- Regulatory Framework & Policy Standards

- Global Smart Parcel Locker Networks Market Economics

- Network Economics & Unit Economics Framework

- Capital Expenditure (CAPEX) Structure

- Operating Expenditure (OPEX) Structure

- Revenue Model & Monetisation Levers

- Network Utilisation, Parcel Throughput & Dwell Time Economics

- Payback Period & Return on Investment (ROI) Analysis

- Total Cost of Ownership (TCO) vs Home Delivery & Collection Point Alternatives

- Hardware & Infrastructure Cost Analysis

- Locker Cabinet, Module & Enclosure Manufacturing Cost Trends (USD/unit, 2021–2035)

- Electronic Locking, Access Control & Biometric Authentication Cost Dynamics

- Display Screen, Touch Interface & User Terminal Cost Benchmarks

- Connectivity & Communication Module (4G/5G, Wi-Fi, NB-IoT) Cost Analysis

- Power Supply, Solar Panel & Backup Battery Infrastructure Cost Structure

- CCTV, Sensor Suite & Physical Security Hardware Cost Analysis

- Impact of Network Scale, Standardisation & Modular Design on Unit Economics

- Software, Platform & Operations Economics

- Locker Management System (LMS) & Cloud Platform Licensing Cost Structure

- Carrier & E-Commerce Platform Integration & API Development Economics

- Consumer App, Notification & PIN/QR Code Access System Cost Analysis

- Predictive Maintenance, Remote Diagnostics & Field Service Operations Economics

- Returns Processing & Reverse Logistics Integration Economics

- Network-as-a-Service (NaaS) vs Owned-Network Commercial Model Comparison

- Site Acquisition & Deployment Economics

- Outdoor Street & Kerbside Deployment Cost Benchmarks

- Retail, Supermarket & Shopping Mall In-Store Deployment Economics

- Residential Apartment Complex & Multi-Dwelling Unit (MDU) Deployment Costs

- Transit Hub, Train Station, Metro & Airport Deployment Cost Analysis

- Corporate Campus & Business Park Deployment Economics

- Network Economics & Unit Economics Framework

- Global Smart Parcel Locker Networks Market Outlook

- Market Size & Forecast by Value (USD Billion, 2021–2036)

- Market Size & Forecast by Volume (Number of Locker Units & Network Locations)

- Market Size & Forecast by Product Type

- Outdoor Smart Parcel Lockers

- Indoor Smart Parcel Lockers

- Automated Parcel Stations (APS)

- Refrigerated & Temperature-Controlled Lockers

- Large-Format & Oversized Parcel Lockers

- Multi-Carrier & Open-Network Lockers

- Branded / Single-Carrier Proprietary Lockers

- Others (Reverse Logistics & Returns-Only Lockers)

- Market Size & Forecast by Locker Size & Configuration

- Small Compartment Lockers (Letters, Envelopes & Small Parcels)

- Medium Compartment Lockers (Standard E-Commerce Parcels)

- Large Compartment Lockers (Bulky & Oversized Parcels)

- Mixed-Configuration Multi-Size Locker Banks

- Market Size & Forecast by Access Technology

- PIN Code & OTP Access

- QR Code & Barcode Scan Access

- Mobile App & NFC/Bluetooth Access

- Biometric (Fingerprint & Facial Recognition) Access

- Smart Card & RFID Access

- Others (Voice Recognition, Contactless Key)

- Market Size & Forecast by Connectivity & Network Technology

- 4G / LTE Connected Lockers

- 5G Connected Lockers

- Wi-Fi Connected Lockers

- NB-IoT & Low-Power WAN Connected Lockers

- Offline / Standalone Lockers

- Market Size & Forecast by Power Source

- Mains Grid-Powered Lockers

- Solar-Powered & Hybrid Lockers

- Battery-Backed & Off-Grid Lockers

- Market Size & Forecast by Application

- E-Commerce Last-Mile Parcel Delivery

- Click & Collect / Buy Online Pick Up In Locker (BOPIL)

- Returns & Reverse Logistics Processing

- Grocery & Fresh Food Delivery

- Healthcare & Pharmaceutical Dispensing

- Corporate & Internal Mail Distribution

- Others (Government Documents, Library Loans, Key Exchange)

- Market Size & Forecast by End-Use Sector

- E-Commerce & Online Retail Platforms

- – Global E-Commerce Giants (Amazon, JD.com, Alibaba, Flipkart, etc.)

- – Regional & Specialist E-Retailers

- Postal & National Courier Operators

- Parcel & Express Delivery Companies (3PL / CEP Carriers)

- Brick-and-Mortar Retail & Supermarket Chains

- Residential Property Developers & Housing Associations

- Transit Authorities & Transport Hubs

- Corporate Campuses & Business Parks

- Healthcare & Pharmaceutical Distributors

- Government & Public Sector

- Others (Universities, Libraries, Co-working Spaces)

- Market Size & Forecast by Deployment Location

- Outdoor Street, Kerbside & Public Space

- Retail & Supermarket In-Store

- Residential & Multi-Dwelling Unit (MDU) Lobbies

- Transit Hubs (Train Stations, Metro, Bus Terminals, Airports)

- Corporate Campuses & Business Parks

- Petrol Stations & Convenience Stores

- Others (Universities, Hospitals, Government Buildings)

- Market Size & Forecast by Ownership & Business Model

- Operator-Owned Open-Network (Multi-Carrier) Models

- Carrier-Owned Proprietary Single-Carrier Models

- Retailer-Owned & Branded Click & Collect Models

- Network-as-a-Service (NaaS) / Hardware-as-a-Service (HaaS)

- Public-Private Partnership (PPP) & Municipal Models

- Property Developer & Real Estate Embedded Models

- Asia-Pacific Smart Parcel Locker Networks Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Volume (Locker Units & Network Locations)

- By Product Type

- By Locker Size & Configuration

- By Access Technology

- By Connectivity & Network Technology

- By Power Source

- By Application

- By End-Use Sector

- By Deployment Location

- By Ownership & Business Model

- Key Demand Drivers (APAC-Specific)

- Competitive Landscape (APAC)

- Market Size & Forecast

- Europe Smart Parcel Locker Networks Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Volume (Locker Units & Network Locations)

- By Product Type

- By Locker Size & Configuration

- By Access Technology

- By Connectivity & Network Technology

- By Power Source

- By Application

- By End-Use Sector

- By Deployment Location

- By Ownership & Business Model

- Key Demand Drivers (Europe-Specific)

- Competitive Landscape (Europe)

- Market Size & Forecast

- North America Smart Parcel Locker Networks Market Outlook

- Market Overview & Strategic Importance

- Market Size & Forecast

- By Value (2020–2035)

- By Volume (Locker Units & Network Locations)

- By Product Type

- By Locker Size & Configuration

- By Access Technology

- By Connectivity & Network Technology

- By Power Source

- By Application

- By End-Use Sector

- By Deployment Location

- By Ownership & Business Model

- Key Demand Drivers (North America-Specific)

- Competitive Landscape (North America)

- Latin America Smart Parcel Locker Networks Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Volume (Locker Units & Network Locations)

- By Product Type

- By Locker Size & Configuration

- By Access Technology

- By Connectivity & Network Technology

- By Power Source

- By Application

- By End-Use Sector

- By Deployment Location

- By Ownership & Business Model

- Key Demand Drivers (LATAM-Specific)

- Competitive Landscape (Latin America)

- Market Size & Forecast

- Middle East & Africa Smart Parcel Locker Networks Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Volume (Locker Units & Network Locations)

- By Product Type

- By Locker Size & Configuration

- By Access Technology

- By Connectivity & Network Technology

- By Power Source

- By Application

- By End-Use Sector

- By Deployment Location

- By Ownership & Business Model

- Key Demand Drivers (MEA-Specific)

- Competitive Landscape (MEA)

- Market Size & Forecast

- Country-Wise Smart Parcel Locker Networks Market Outlook

- Market Size & Forecast by Country

- By Value

- By Volume (Locker Units & Network Locations)

- By Product Type

- By Locker Size & Configuration

- By Access Technology

- By Connectivity & Network Technology

- By Power Source

- By Application

- By End-Use Sector

- By Deployment Location

- By Ownership & Business Model

- Market Size & Forecast by Country

- Countries Covered: United States, Canada, Brazil, Mexico, Germany, United Kingdom, France, Netherlands, Poland, Sweden, China, Japan, South Korea, India, Australia, Singapore, UAE, Saudi Arabia, South Africa, Turkey

- Technology Landscape & Innovation Analysis

- Smart Parcel Locker Technology Maturity Assessment

- Emerging & Disruptive Technologies in Locker Hardware, Access Control & Network Management

- AI, Computer Vision & Predictive Analytics in Locker Network Optimisation & Demand Forecasting

- IoT, Remote Monitoring & Predictive Maintenance in Smart Locker Operations

- Biometric Authentication, Contactless Access & Digital Identity Integration

- Refrigerated & Temperature-Controlled Locker Technology for Grocery & Pharma Delivery

- Robotics & Automated Parcel Sorting Integration with Smart Locker Networks

- Technology Readiness & Commercialisation Matrix – Key Smart Locker Technologies

- Patent Landscape Analysis

- R&D Investment Benchmarking

- Value Chain & Supply Chain Analysis

- Smart Parcel Locker Networks Value Chain Mapping

- Supply Chain Concentration & Dependency Analysis

- Key Supplier Mapping by Component Category & Technology Programme

- Locker Cabinet & Enclosure Manufacturers

- Electronic Locking & Access Control Suppliers

- Display, Touch Screen & Terminal Manufacturers

- Connectivity Module & IoT Component Suppliers

- Software Platform & LMS Developers

- Installation, Field Service & Maintenance Providers

- Supplier Risk Heat Map

- Make vs Buy Strategy Trends Among Network Operators, Carriers & E-Commerce Platforms

- Pricing Analysis

- Smart Parcel Locker Network Pricing Dynamics & Mechanisms

- Hardware Pricing by Locker Type, Configuration & Access Technology

- Software & Platform Licensing Pricing Models (SaaS, Per-Transaction, Per-Locker)

- Network Deployment & Installation Pricing by Location Type & Geography

- Per-Parcel Transaction Fee Benchmarks Across Carrier & Operator Models

- NaaS / HaaS vs Owned-Network Pricing & Value Proposition

- Open-Network vs Proprietary Carrier Locker Pricing Benchmarks

- Sustainability & Environmental Stewardship

- Environmental & Sustainability Landscape in Smart Parcel Locker Networks

- Carbon Footprint Benchmarking: Smart Locker Networks vs Home Delivery & Failed Delivery Trips

- Solar-Powered & Low-Energy Locker Design & Green Infrastructure Roadmap

- Recyclable Materials, Circular Economy & End-of-Life Locker Hardware Management

- Urban Congestion Reduction & Air Quality Impact of Consolidated Parcel Delivery via Lockers

- ESG Reporting & Lifecycle Assessment (LCA) in Smart Locker Network Operations

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level: Global Network Operators vs Regional Players

- Top 5 Smart Parcel Locker Network Operators Market Revenue & Network Size Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis by Product Type & Region

- Competitive Intensity Map by Application Segment & Deployment Location

- Player Classification

- Tier-1 Global Integrated Parcel Locker Network Operators & Postal Giants

- Tier-2 Regional & Specialist Smart Locker Hardware Manufacturers & Network Operators

- Software Platform Providers, Systems Integrators & Technology Enablers

- Emerging & Disruptive Players

- Competitive Analysis Frameworks

- Market Share Analysis by Network Size, Locker Units & Geography

- R&D Intensity Benchmarking

- Carrier Integration Breadth & Open-Network Coverage Comparison

- Geographic Revenue Exposure Comparison

- Company Profiles

- Company Overview, HQ & Organisational Structure

- Smart Locker Products, Platforms & Services Portfolio

- Revenue Breakdown

- Key Network Deployments, Carrier Partnerships & Location Coverage

- Manufacturing Footprint & Key Facilities

- Recent Developments (M&A, Partnerships, Network Expansions, Financial Results)

- SWOT Analysis

- Strategic Focus: Network Density, Multi-Carrier Integration, Open-Platform & International Expansion

- Market Structure & Concentration

- Strategic Output

- Market Opportunity Matrix

- High-Value Opportunity Quadrant Analysis

- Addressable Market by Product Type, Application & Region

- Time-to-Revenue Assessment by Opportunity

- White Space Opportunity Analysis

- Underserved Deployment Location & Application Segment Gaps

- Geographic Markets with Low Smart Locker Penetration & High Failed Delivery Rates

- Technology Gaps with High Commercialisation Potential

- Customer Segment Unmet Needs (Retailers, Carriers, Property Developers & Municipalities)

- Market Opportunity Matrix

- Strategic Recommendations

- Product Portfolio & Innovation Strategy

- Technology & Digitalisation Strategy

- Network Footprint & Locker Deployment Expansion Strategy

- Open-Network, Multi-Carrier Integration & Platform Ecosystem Growth Strategy

- Click & Collect, Returns & Reverse Logistics Channel Growth Strategy

- Pricing & Commercial Strategy

- Sustainability & Regulatory Compliance Strategy

- Supply Chain & Hardware Sourcing Strategy

- Partnership, M&A & Expansion Strategy

- Regional Growth Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-Term (2025–2028)

- Mid-Term (2029–2032)

- Long-Term (2033–2036)