Market Definition

The Specialty Fluorochemicals for Semiconductors market refers to the global industrial and specialty chemicals sector involved in the production, purification, formulation, and supply of fluorine-based chemical compounds specifically engineered to meet the extreme purity, reactivity, and performance standards demanded by semiconductor fabrication, advanced packaging, and compound semiconductor manufacturing processes. The market is structurally defined by three principal product categories: fluorinated etch gases and plasma process chemicals, including nitrogen trifluoride, sulfur hexafluoride, hexafluoroethane, octafluoropropane, tetrafluoromethane, and fluorine gas, which are deployed as selective etchants and chamber cleaning agents in plasma-enhanced processes during front-end-of-line patterning and dielectric layer formation; fluorinated lithography chemicals and photoresist ancillaries, encompassing perfluoropolyether-based immersion fluids, fluorinated top coat polymers, fluorine-containing photoacid generators, and fluorinated co-solvents used in extreme ultraviolet and deep ultraviolet lithography to achieve sub-nanometer patterning precision; and fluorinated specialty solvents, surface treatment agents, and polishing compounds including hydrofluoric acid ultra-high-purity grades, fluorinated cleaning solvents, ammonium fluoride solutions, and fluoropolymer-based chemical mechanical planarization formulations used across wafer cleaning, surface passivation, and back-end processing steps. As a foundational input to chipmaking at the most technologically demanding nodes, specialty fluorochemicals are indispensable to the production of logic processors, memory devices, advanced analog chips, power semiconductors, and photonic integrated circuits. The market dynamics are profoundly influenced by the accelerating migration to gate-all-around transistor architectures, the expansion of extreme ultraviolet lithography adoption, the proliferation of three-dimensional NAND stacking, and the strategic geopolitical imperative driving governments across the United States, Europe, Japan, South Korea, and China to secure domestic supply chains for critical semiconductor process materials.

Global Specialty Fluorochemicals for Semiconductors Market Insights

As of early 2026, the global specialty fluorochemicals for semiconductors market is valued at approximately USD 3.8 billion, operating through a period of structurally supported expansion with a projected compound annual growth rate of 8.4 percent through 2033. The market structure is moderately concentrated, anchored by a small group of vertically integrated global specialty chemical leaders including Kanto Denka Kogyo, Resonac, Solvay, Air Products and Chemicals, Linde, and Stella Chemifa, who collectively control the dominant share of semiconductor-grade fluorine derivative supply capacity. Fluorinated etch and plasma process gases represent the largest product segment by volume and value, accounting for the majority of total market consumption by virtue of their ubiquitous deployment across plasma etch, chemical vapor deposition chamber cleaning, and atomic layer etching process steps that are repeated hundreds of times per wafer in advanced node logic and memory fabrication. While isolated supply disruptions in etch gas supply chains periodically affected chipmaker procurement confidence during 2023 and 2024 following export restriction actions by key producing nations, the underlying structural demand fundamentals entering 2026 are strongly positive, driven by the global expansion of leading-edge semiconductor fabrication capacity at foundries, the accelerating adoption of extreme ultraviolet lithography tools, and the increasing chemical consumption intensity per wafer that advanced three-dimensional device architectures impose on process chemical requirements relative to previous generation planar device structures.

Current Producing Countries and Regional Concentration

Japan remains the undisputed technological and supply chain leader in specialty fluorochemicals for semiconductors, commanding the dominant position in the production of ultra-high-purity fluorine gas, nitrogen trifluoride, semiconductor-grade hydrofluoric acid, and fluorinated photoresist ancillaries by virtue of decades of co-development relationships between Japanese specialty chemical producers and the leading Japanese, Korean, and Taiwanese semiconductor equipment manufacturers and chipmakers whose process specifications have shaped the purity, stability, and packaging standards that define the global semiconductor chemical supply chain. South Korea has emerged as the second most strategically significant production hub, with Korean fluorochemical producers advancing domestic supply capability for nitrogen trifluoride and specialty etch gas mixtures following the 2019 export control episode involving Japanese fluorochemical exports, which catalyzed aggressive domestic capacity investment by Korean conglomerates and government co-funded material development programs. The United States maintains significant capacity in bulk fluorine chemistry, fluorinated specialty solvents, and advanced lithography chemical formulations, with domestic producers benefiting from the policy stimulus of the CHIPS and Science Act which has elevated domestic semiconductor material supply chain security as a national industrial priority. China represents the most consequential variable in the near-term supply landscape, as Chinese fluorochemical producers have substantially expanded capacity in hydrogen fluoride, ammonium fluoride, and some fluorinated etch gas categories while simultaneously being subject to targeted export restrictions on certain fluorochemical precursors by international trading partners, creating both an expanding domestic Chinese market and a complex geopolitical trade dynamic affecting global supply balance. Europe, led by Belgium and Germany, contributes specialty fluorinated solvent formulation and fluoropolymer process chemistry capability, with European producers increasingly benefiting from the European Chips Act investment in securing locally sourced semiconductor process material supply for European fab expansion programs.

Current and Emerging Production Technologies

The current industrial standard for semiconductor-grade nitrogen trifluoride production is electrochemical fluorination of ammonia in anhydrous hydrogen fluoride media, a process that achieves the ultra-high-purity specifications demanded by chipmakers only through multi-stage distillation, adsorption purification, and rigorous in-line analytical monitoring using specialized gas chromatography and trace moisture analyzers capable of detecting impurities at parts-per-trillion concentration levels. Ultra-high-purity hydrofluoric acid production relies on high-temperature reaction of fluorspar with sulfuric acid followed by multi-pass fractional distillation and sophisticated trace metal removal using ion exchange chromatography and sub-boiling distillation techniques to achieve the metal impurity profiles below one part per billion that advanced silicon wafer and compound semiconductor process steps require. Emerging production technologies advancing toward pilot and early commercial scale in 2026 include direct fluorine synthesis routes using electrochemical fluorine generation cells that eliminate the need for imported elemental fluorine by generating fluorine on-site adjacent to downstream fluorination reactors, substantially reducing transportation hazard and supply chain dependency; plasma-driven fluorine chemistry platforms that enable the synthesis of previously inaccessible fluorinated etch gas compositions with superior etch selectivity and lower global warming potential than legacy perfluorocarbon etch chemistries; and molecular distillation technologies adapted from pharmaceutical processing that achieve sub-parts-per-trillion metallic impurity removal in semiconductor-grade solvents and cleaning agents supporting the requirements of gate-all-around and buried power rail device architectures at the most advanced logic nodes. Digital twin simulation of fluorination reactor environments and artificial intelligence-assisted real-time purity monitoring are being deployed by leading producers to reduce batch-to-batch quality variability, accelerate new product qualification timelines with chipmaker customers, and optimize energy consumption in the energy-intensive electrolytic and cryogenic separation steps that dominate the operating cost structure of specialty fluorochemical production.

Market Hotspots and Opportunity Analysis

The most significant near-term growth hotspots for specialty fluorochemicals in the semiconductor sector are concentrated at the intersection of leading-edge logic node transitions, memory architecture advancement, and new fab capacity construction across Taiwan, South Korea, the United States, Japan, and the expanding European and Indian semiconductor manufacturing footprints that are collectively creating a multi-year wave of greenfield and brownfield fab investment whose process chemical consumption requirements will structurally expand addressable demand across all specialty fluorochemical product categories. The most commercially compelling emerging opportunity lies in fluorinated chemistries specifically formulated for high numerical aperture extreme ultraviolet lithography, the next-generation patterning tool whose adoption at the most advanced logic foundries is creating entirely new requirements for fluorinated photoresist top coat polymers, immersion hood materials, and defect-suppressing fluorinated rinse formulations that do not yet exist at commercial scale and whose development represents a high-margin, high-barrier-to-entry specialty chemical opportunity for the limited number of producers with the photoresist chemistry expertise and semiconductor customer qualification relationships required to navigate the multi-year co-development and adoption approval process. A further structural growth vector is the rapid expansion of compound semiconductor fabrication for silicon carbide and gallium nitride power devices and gallium arsenide and indium phosphide photonic and radio frequency devices, which consumes a distinct and high-value portfolio of fluorinated etch gases, surface treatment chemicals, and polishing formulations whose process chemistry requirements differ substantially from silicon wafer processing and whose growing production volumes across dedicated compound semiconductor fabs are creating a diversified demand stream that supplements the cyclically variable logic and memory chip investment cycle. For strategic investors, the integration of low-global-warming-potential fluorinated etch gas alternatives into chipmaker process specifications, driven by voluntary net-zero commitments and regulatory pressure on perfluorocarbon emissions from semiconductor fabs, represents a technology transition opportunity whose timeline and commercial scale are becoming increasingly defined by chipmaker sustainability roadmaps and regulatory emission reporting frameworks.

Accelerating Adoption of Advanced Semiconductor Node Architectures and the Escalating Process Chemical Intensity per Wafer at Gate-All-Around and Extreme Ultraviolet Lithography Nodes

The dominant structural demand driver for specialty fluorochemicals in the semiconductor sector is the relentless progression of the integrated circuit industry toward smaller feature sizes and more complex three-dimensional device architectures whose fabrication process sequences require substantially greater quantities and more diverse compositions of fluorinated etch gases, cleaning chemicals, and lithography ancillaries per wafer processed than the preceding generations of planar and FinFET transistor technologies they are replacing. Gate-all-around nanosheet transistor fabrication, which entered high-volume production at the most advanced foundries beginning with the two-nanometer class node in 2025, demands the precise selective etching of alternating silicon and silicon-germanium nanosheet stacks within nanometer-scale three-dimensional channel regions using highly selective fluorinated atomic layer etching chemistries and atomic layer deposition chamber cleaning gas sequences whose chemical consumption per transistor substantially exceeds that of FinFET patterning at equivalent transistor density. The adoption of high numerical aperture extreme ultraviolet lithography tools, which entered commercial deployment at the most technologically advanced logic foundries during 2025 and 2026, is creating new demand for fluorinated immersion hood materials, top coat polymers, and defect suppression chemistries specifically formulated for the optical environment of these instruments and not previously required at lower numerical aperture extreme ultraviolet exposures. The structural expansion of three-dimensional NAND flash memory stack heights, which have exceeded 300 layers in the most advanced commercial products in 2026 and whose continued progression toward 400 and beyond will require correspondingly deeper and more selective high-aspect-ratio etch processes consuming growing volumes of fluorinated etch gas mixtures per memory die, is providing a complementary and partially independent demand driver for fluorinated process chemicals that supplements the logic chip-driven demand and partially offsets the cyclical capital expenditure variability of the memory semiconductor investment cycle. The cumulative effect of these architectural transitions is that the volume of specialty fluorochemicals consumed per wafer of advanced semiconductor manufacturing output is increasing in each new process generation, creating a structural demand growth dynamic that operates independently of wafer volume growth and that ensures sustained expansion in specialty fluorochemical consumption even in periods of flat or declining unit semiconductor production.

Geopolitical Supply Chain Restructuring and the Strategic Imperative for Semiconductor-Producing Nations to Secure Domestic and Allied Specialty Chemical Supply

The second major structural demand driver reshaping the trajectory and investment landscape of the specialty fluorochemicals for semiconductors market is the fundamental reorganization of global semiconductor material supply chains that has been set in motion by the geopolitical tensions, export restriction actions, and national industrial security assessments of the past several years, which have collectively elevated specialty fluorochemicals from a procurement category managed primarily on price and quality criteria to a strategic supply chain vulnerability whose domestic availability has become a national security priority for the United States, European Union, Japan, South Korea, and China simultaneously. The 2019 Japanese export controls on semiconductor-grade fluorinated resins, hydrogen fluoride, and fluorinated polyimides targeting Korean chipmakers, followed by subsequent actions involving Chinese producers of gallium and germanium fluoride precursors and United States restrictions on the export of certain fluorochemical technology to Chinese entities, have demonstrated that semiconductor-grade specialty fluorochemicals can be deployed as instruments of geopolitical leverage with immediate and severe consequences for the chipmakers dependent on the restricted supply sources, galvanizing government and corporate investment in domestic fluorochemical production capacity, alternative supplier qualification, and inventory buffer strategies that are collectively expanding the addressable procurement pool and geographic supply base for specialty fluorochemicals beyond the historically concentrated Japanese and Korean sources. The CHIPS and Science Act in the United States, the European Chips Act, Japan’s semiconductor industry revival programs, South Korea’s semiconductor material supply chain resilience investment initiatives, and India’s emerging semiconductor program are each explicitly addressing specialty chemical supply security as a component of their semiconductor industry support frameworks, deploying government grants, preferential procurement mechanisms, co-investment instruments, and research and development subsidies that are catalyzing private sector investment in domestic specialty fluorochemical production capacity that would not be commercially justified on market economics alone. This supply chain restructuring dynamic is creating new production capacity investments across multiple geographies simultaneously, generating a sustained multi-year capital expenditure cycle in specialty fluorochemical production infrastructure whose scale and urgency are driven by geopolitical imperatives rather than normal commodity market investment triggers, providing a demand floor for specialty fluorochemical capacity investment that is substantially less cyclical than the semiconductor equipment investment cycle that historically governed fluorochemical demand growth.

Exceptional Purity Qualification Requirements and the Protracted Chipmaker Approval Processes That Create High Barriers to New Supplier Entry and Product Substitution

The most consequential structural challenge governing the competitive dynamics and new entrant economics of the specialty fluorochemicals for semiconductors market is the extraordinary technical and commercial burden associated with achieving and maintaining chipmaker qualification approval for specialty fluorochemical products at the purity, consistency, and supply reliability specifications that advanced semiconductor process nodes demand, a qualification burden whose multi-year duration, deep resource requirements, and outcome uncertainty create formidable barriers to entry for new suppliers and to product substitution even when incumbent suppliers face cost or supply disadvantage. Advanced semiconductor fabrication processes are extraordinarily sensitive to chemical impurities at trace levels that are analytically challenging to characterize and whose effects on device yield, gate dielectric integrity, contact resistance, and long-term device reliability must be demonstrated to be within acceptable bounds through extensive wafer-level process integration testing conducted in the chipmaker’s own manufacturing environment with its specific tool set, process sequence, and substrate materials, a testing process that cannot be compressed below a minimum timeline determined by the statistical sample sizes required for meaningful yield and reliability data and that at leading-edge nodes can require 18 to 36 months from initial sample submission to final qualification approval. The qualification infrastructure that specialty fluorochemical suppliers must maintain to support chipmaker approval processes includes dedicated analytical laboratories equipped with inductively coupled plasma mass spectrometry, trace gas impurity analyzers, particle counter systems, and materials characterization instruments capable of measuring impurity profiles at the parts-per-trillion levels that advanced node process specifications require, the development and validation of proprietary analytical test methods meeting the measurement uncertainty requirements of chipmaker quality management systems, the establishment of traceability chains linking production batch analytical results to primary reference standards, and the commitment to production process freeze conditions under which no manufacturing process change can be implemented without formal notification and requalification approval from qualified chipmaker customers. These qualification demands collectively create a supply chain inertia that, while technically justified by the genuine process sensitivity of advanced semiconductor manufacturing to chemical variability, substantially limits the competitive flexibility of chipmakers in diversifying their specialty fluorochemical supply base and constrains the pace at which geopolitically motivated supply chain diversification objectives can be achieved in practice despite the strategic urgency assigned to them by national industrial policy frameworks.

Stringent Environmental Regulation of High-Global-Warming-Potential Fluorinated Process Gases and the Technology Transition Cost Burden of Low-GWP Alternative Qualification

A structurally significant and commercially complex challenge confronting both specialty fluorochemical producers and their semiconductor manufacturing customers is the accelerating tightening of environmental regulations governing the atmospheric emission of high-global-warming-potential perfluorocarbon and hydrofluorocarbon process gases that constitute a substantial fraction of the specialty fluorochemical portfolio deployed in plasma etch and chemical vapor deposition chamber cleaning applications across semiconductor fabs, regulations whose implementation is imposing concurrent cost burdens of emissions abatement system capital investment on chipmakers, low-global-warming-potential alternative chemistry development investment on fluorochemical producers, and multi-year process requalification programs at chipmakers that create technology transition timelines whose duration and resource requirements compete with the parallel demands of node migration and capacity expansion. The perfluorocarbon etch gases tetrafluoromethane, hexafluoroethane, and octafluoropropane, along with sulfur hexafluoride used in silicon etching and chamber cleaning applications, carry global warming potentials thousands of times higher than carbon dioxide on a 100-year basis, and their aggregate emission from semiconductor manufacturing operations has attracted regulatory attention under voluntary industry emission reduction agreements, mandatory greenhouse gas reporting requirements in the United States, European Union, Japan, South Korea, and Taiwan, and the evolving framework of the European Fluorinated Greenhouse Gas Regulation whose periodic revision process is progressively restricting the use and placing stricter emission management requirements on high-global-warming-potential fluorinated gas applications. The development of low-global-warming-potential alternative etch chemistry solutions, encompassing fluorinated sulfur compounds such as sulfuryl fluoride and sulfur tetrafluoride, unsaturated fluorocarbon compounds, and nitrogen fluoride mixtures whose global warming potential is substantially below that of legacy perfluorocarbon gases while achieving comparable or superior etch selectivity, process window, and chamber cleaning performance, requires multi-year synthetic chemistry development, toxicology and environmental fate assessment, handling and storage system engineering, and most significantly the same protracted chipmaker process integration qualification cycle whose duration and resource requirements are the primary barrier to all specialty fluorochemical product transitions in semiconductor manufacturing environments. The commercial consequence for specialty fluorochemical producers is a transition investment cycle in which the development and qualification cost of low-global-warming-potential alternatives must be absorbed ahead of the commercial revenue that qualified chipmaker adoption generates, creating a capital and resource demand that is particularly burdensome for smaller specialty chemical producers competing against the research and development capacity of larger integrated fluorine chemistry companies with broader product portfolios across which transition development costs can be distributed.

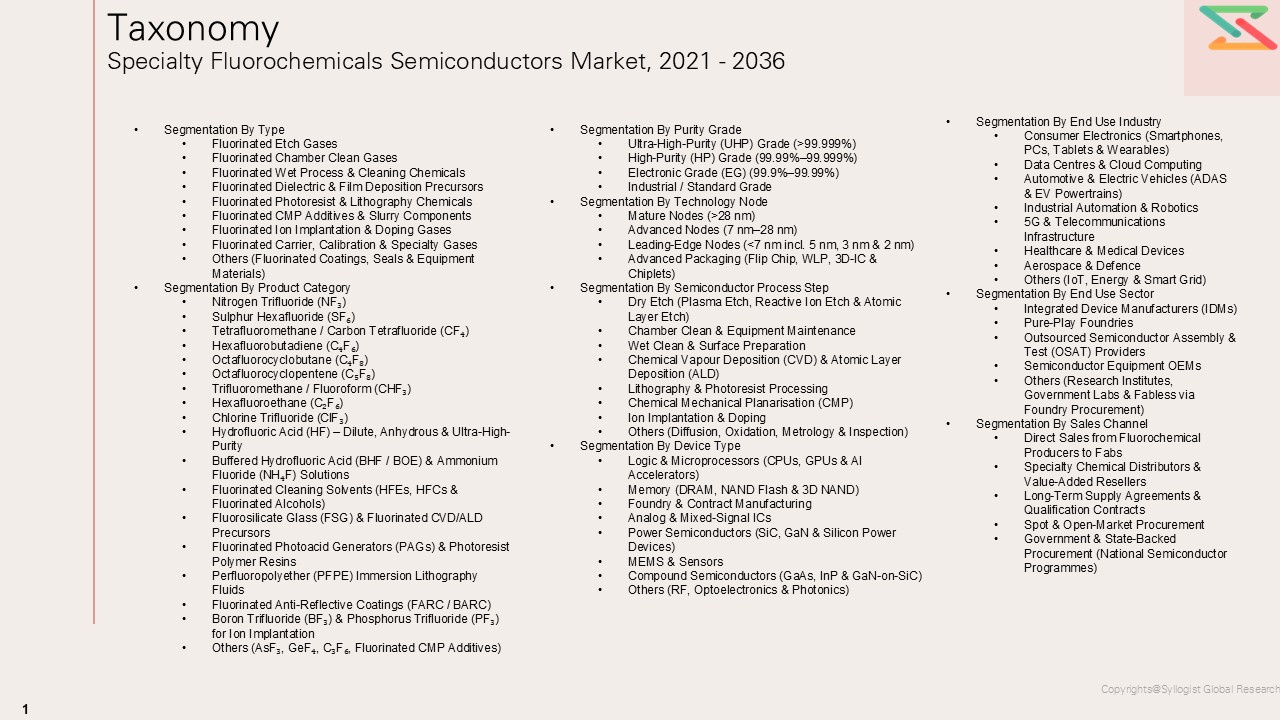

Market Segmentation

- Segmentation By Product Type

- Nitrogen Trifluoride (NF3)

- Sulfur Hexafluoride (SF6)

- Hexafluoroethane (C2F6)

- Octafluoropropane (C3F8)

- Tetrafluoromethane (CF4)

- Fluorine Gas (F2)

- Ultra-High-Purity Hydrofluoric Acid (HF)

- Ammonium Fluoride and Buffered Oxide Etch Solutions

- Fluorinated Photoresist Ancillaries and Top Coat Polymers

- Perfluoropolyether Immersion Fluids

- Low-Global-Warming-Potential Fluorinated Etch Gases

- Fluorinated Specialty Solvents and Cleaning Agents

- Others

- Segmentation By Application

- Plasma Etch and Dry Etch Processes

- Chemical Vapor Deposition Chamber Cleaning

- Atomic Layer Etch (ALE)

- Atomic Layer Deposition (ALD)

- Immersion and Extreme Ultraviolet (EUV) Lithography

- Wafer Cleaning and Surface Preparation

- Chemical Mechanical Planarization (CMP)

- Diffusion and Ion Implantation

- Advanced Packaging and Interconnect Processing

- Others

- Segmentation By Semiconductor Device Type

- Logic and Microprocessor (Leading-Edge Nodes)

- DRAM Memory

- NAND Flash Memory (3D NAND)

- Power Semiconductors (SiC and GaN)

- Analog and Mixed-Signal ICs

- Radio Frequency and Photonic Devices (GaAs, InP)

- Microelectromechanical Systems (MEMS)

- Others

- Segmentation By Purity Grade

- Electronic Grade (EG) – Standard Semiconductor

- Ultra-High-Purity (UHP) – Advanced Node

- Extreme Purity (EP) – Sub-2nm and EUV Applications

- Research and Development Grade

- Segmentation By End User

- Leading-Edge Logic Foundries

- Integrated Device Manufacturers (IDMs)

- Memory Chip Manufacturers

- Power Semiconductor Fabs

- Compound Semiconductor and Photonic Device Manufacturers

- Semiconductor Equipment Manufacturers

- Advanced Packaging Houses

- Others

- Segmentation By Sales Channel

- Direct Long-Term Supply Agreements with Chipmakers

- Specialty Gas and Chemical Distributors

- On-Site Gas Generation and Supply Systems

- Bulk Cylinder and Isotainer Supply

- Others

- Segmentation By Region

- Asia-Pacific (Taiwan, South Korea, Japan, China)

- North America (United States)

- Europe (Netherlands, Germany, Ireland, Belgium)

- Rest of World (India, Israel, Singapore)

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2036

Key Questions this Study Will Answer

- What is the projected global market valuation for specialty fluorochemicals for semiconductors through 2036, segmented by product type, application, semiconductor device type, purity grade, end user, and region, and which product categories and geographic markets are expected to generate the highest incremental revenue and volume growth across the forecast period?

- How is the transition from FinFET to gate-all-around nanosheet transistor architectures and the progressive adoption of high numerical aperture extreme ultraviolet lithography at leading logic foundries reshaping the per-wafer consumption volumes, product composition requirements, and purity specifications of specialty fluorochemicals, and what new fluorinated chemistry categories are being created by these architectural transitions that do not currently exist at commercial scale?

- What are the current supply chain concentration risks and geopolitical exposure profiles of the global specialty fluorochemicals for semiconductors market, and how are the CHIPS and Science Act, European Chips Act, Japan semiconductor material revival programs, and South Korean material supply resilience initiatives translating into tangible new production capacity investments, supplier qualification programs, and strategic inventory buffer strategies by chipmakers and fluorochemical producers?

- Which low-global-warming-potential fluorinated etch gas alternatives are most advanced in chipmaker process integration qualification programs, and what are the projected commercial deployment timelines, performance parity benchmarks, and cost premium trajectories for qualified low-global-warming-potential alternatives relative to the legacy perfluorocarbon and sulfur hexafluoride etch chemistries they are designed to replace across plasma etch and chamber cleaning applications?

- How are the growing compound semiconductor fabrication markets for silicon carbide power devices, gallium nitride radio frequency and power devices, and indium phosphide photonic integrated circuits creating differentiated specialty fluorochemical demand requirements that are distinct from the silicon wafer process chemistry portfolio, and what production capacity, product development, and customer qualification investments are leading fluorochemical suppliers making to address this structurally growing and high-margin demand segment?

- Who are the leading specialty fluorochemical producers, ultra-high-purity gas suppliers, fluorinated lithography chemical developers, semiconductor-grade acid and solvent manufacturers, and on-site fluorine generation system providers currently defining the competitive landscape of the global specialty fluorochemicals for semiconductors market, and what are their respective product portfolio strategies, purity grade roadmaps, low-global-warming-potential transition investment programs, and geographic capacity expansion plans for serving the growing semiconductor manufacturing footprints of the United States, Europe, India, and Japan through the forecast horizon?

- Introduction (Product Definition, Taxonomy and Research Methodology)

- Executive Summary

- Global Specialty Fluorochemicals for Semiconductors Demand Supply Analysis

- Global Specialty Fluorochemicals for Semiconductors Market Assessment, 2021-2036

- Market Size & Forecast by Value

- Market Size & Forecast by Volume

- Market Size & Forecast by Type

- Fluorinated Etch Gases

- Fluorinated Chamber Clean Gases

- Fluorinated Wet Process & Cleaning Chemicals

- Fluorinated Dielectric & Film Deposition Precursors

- Fluorinated Photoresist & Lithography Chemicals

- Fluorinated CMP Additives & Slurry Components

- Fluorinated Ion Implantation & Doping Gases

- Fluorinated Carrier, Calibration & Specialty Gases

- Others (Fluorinated Coatings, Seals & Equipment Materials)

- Market Size & Forecast by Product Category

- Nitrogen Trifluoride (NF₃)

- Sulphur Hexafluoride (SF₆)

- Tetrafluoromethane / Carbon Tetrafluoride (CF₄)

- Hexafluorobutadiene (C₄F₆)

- Octafluorocyclobutane (C₄F₈)

- Octafluorocyclopentene (C₅F₈)

- Trifluoromethane / Fluoroform (CHF₃)

- Hexafluoroethane (C₂F₆)

- Chlorine Trifluoride (ClF₃)

- Hydrofluoric Acid (HF) – Dilute, Anhydrous & Ultra-High-Purity

- Buffered Hydrofluoric Acid (BHF / BOE) & Ammonium Fluoride (NH₄F) Solutions

- Fluorinated Cleaning Solvents (HFEs, HFCs & Fluorinated Alcohols)

- Fluorosilicate Glass (FSG) & Fluorinated CVD/ALD Precursors

- Fluorinated Photoacid Generators (PAGs) & Photoresist Polymer Resins

- Perfluoropolyether (PFPE) Immersion Lithography Fluids

- Fluorinated Anti-Reflective Coatings (FARC / BARC)

- Boron Trifluoride (BF₃) & Phosphorus Trifluoride (PF₃) for Ion Implantation

- Others (AsF₃, GeF₄, C₃F₆, Fluorinated CMP Additives)

- Market Size & Forecast by Purity Grade

- Ultra-High-Purity (UHP) Grade (>99.999%)

- High-Purity (HP) Grade (99.99%–99.999%)

- Electronic Grade (EG) (99.9%–99.99%)

- Industrial / Standard Grade

- Market Size & Forecast by Technology Node

- Mature Nodes (>28 nm)

- Advanced Nodes (7 nm–28 nm)

- Leading-Edge Nodes (<7 nm incl. 5 nm, 3 nm & 2 nm)

- Advanced Packaging (Flip Chip, WLP, 3D-IC & Chiplets)

- Market Size & Forecast by Semiconductor Process Step

- Dry Etch (Plasma Etch, Reactive Ion Etch & Atomic Layer Etch)

- Chamber Clean & Equipment Maintenance

- Wet Clean & Surface Preparation

- Chemical Vapour Deposition (CVD) & Atomic Layer Deposition (ALD)

- Lithography & Photoresist Processing

- Chemical Mechanical Planarisation (CMP)

- Ion Implantation & Doping

- Others (Diffusion, Oxidation, Metrology & Inspection)

- Market Size & Forecast by Device Type

- Logic & Microprocessors (CPUs, GPUs & AI Accelerators)

- Memory (DRAM, NAND Flash & 3D NAND)

- Foundry & Contract Manufacturing

- Analog & Mixed-Signal ICs

- Power Semiconductors (SiC, GaN & Silicon Power Devices)

- MEMS & Sensors

- Compound Semiconductors (GaAs, InP & GaN-on-SiC)

- Others (RF, Optoelectronics & Photonics)

- Market Size & Forecast by End Use Industry

- Consumer Electronics (Smartphones, PCs, Tablets & Wearables)

- Data Centres & Cloud Computing

- Automotive & Electric Vehicles (ADAS & EV Powertrains)

- Industrial Automation & Robotics

- 5G & Telecommunications Infrastructure

- Healthcare & Medical Devices

- Aerospace & Defence

- Others (IoT, Energy & Smart Grid)

- Market Size & Forecast by End Use Sector

- Integrated Device Manufacturers (IDMs)

- Pure-Play Foundries

- Outsourced Semiconductor Assembly & Test (OSAT) Providers

- Semiconductor Equipment OEMs

- Others (Research Institutes, Government Labs & Fabless via Foundry Procurement)

- Market Size & Forecast by Sales Channel

- Direct Sales from Fluorochemical Producers to Fabs

- Specialty Chemical Distributors & Value-Added Resellers

- Long-Term Supply Agreements & Qualification Contracts

- Spot & Open-Market Procurement

- Government & State-Backed Procurement (National Semiconductor Programmes)

- Asia-Pacific Specialty Fluorochemicals for Semiconductors Market Assessment, 2021-2036

- Market Size & Forecast

- By Value

By Volume - By Type

- By Product Category

- By Purity Grade

- By Semiconductor Process Step

- By Device Type

- By End Use Industry

- By Sales Channel

- By Country (Market Share of Leading 5-6 Countries)

- By Value

- Market Size & Forecast

- North America Specialty Fluorochemicals for Semiconductors Market Assessment, 2021-2036

- Market Size & Forecast

- By Value

By Volume - By Type

- By Product Category

- By Purity Grade

- By Semiconductor Process Step

- By Device Type

- By End Use Industry

- By Sales Channel

- By Country (Market Share of Leading 5-6 Countries)

- By Value

- Market Size & Forecast

- Europe Specialty Fluorochemicals for Semiconductors Market Assessment, 2021-2036

- Market Size & Forecast

- By Value

By Volume - By Type

- By Product Category

- By Purity Grade

- By Semiconductor Process Step

- By Device Type

- By End Use Industry

- By Sales Channel

- By Country (Market Share of Leading 5-6 Countries)

- By Value

- Market Size & Forecast

- South America Specialty Fluorochemicals for Semiconductors Market Assessment, 2021-2036

- Market Size & Forecast

- By Value

By Volume - By Type

- By Product Category

- By Purity Grade

- By Semiconductor Process Step

- By Device Type

- By End Use Industry

- By Sales Channel

- By Country (Market Share of Leading 5-6 Countries)

- By Value

- Market Size & Forecast

- Middle East & Africa Specialty Fluorochemicals for Semiconductors Market Assessment, 2021-2036

- Market Size & Forecast

- By Value

By Volume - By Type

- By Product Category

- By Purity Grade

- By Semiconductor Process Step

- By Device Type

- By End Use Industry

- By Sales Channel

- By Country (Market Share of Leading 5-6 Countries)

- By Value

- Market Size & Forecast

- White Space & Emerging Investment Hotspot

- Market White Space Opportunities

- Underserved Low-GWP & PFAS-Compliant Alternative Fluorochemical Categories

- Geographic Markets with Low Domestic Supply & High Import Dependency (India, SE Asia, Europe)

- Technology Gaps in ALD/ALE Precursors for Sub-5 nm & EUV Lithography Nodes

- Unmet Demand in Advanced Packaging & 3D-IC Fluorochemical Supply Chains

- Mergers & Acquisitions (M&A)

- Joint Ventures & Strategic Alliances

- Technology & Innovation Hotspots

- Low-GWP Etch & Clean Gas Development Hubs (NF₃, C₄F₆, C₅F₈ Alternatives)

- Ultra-High-Purity HF & Fluoride Salt Synthesis & Purification Innovation Centres

- EUV Lithography Fluorochemical (PAG, PFPE, Fluoropolymer Resin) R&D Clusters

- On-Site / Point-of-Use (POU) Fluorine Generation & Cylinder-Free Delivery Hotspots

- Regional Investment Attractiveness

- Barriers & Risks in Investment

- PFAS Restriction, F-Gas Regulation & Phase-Out Risk for High-GWP Fluorinated Gases

- Concentrated Upstream Fluorspar & HF Supply Chain (China Dependency)

- Long UHP Qualification Cycles & Single-Source Dependency Risk for Advanced Node Fabs

- IP Fragmentation & Licensing Complexity in Novel Low-GWP Fluorochemical Compositions

- Market White Space Opportunities

- Value Chain Analysis

- Raw Material Sourcing & Suppliers

- Key Raw Materials & Inputs

- Fluorospar (CaF₂) Mining & Primary HF Producers

- Electrofluorination & Specialty Fluorine Compound Synthesisers

- High-Purity Fluoride Salt Producers (NH₄F, KF, AlF₃)

- Fluorinated Solvent & Specialty Organic Fluorochemical Synthesisers

- Cylinder, Bulk Container & Safe Delivery System (SDS) Providers

- Supplier Landscape & Concentration

- Pricing Trends & Volatility

- Dependence on Imports vs Domestic Availability

- Manufacturing & Purification

- Fluorochemical Synthesis, Distillation & Purification Process Steps

- UHP Filtration, Moisture Removal & Metallic Impurity Control

- Batch Certification, Purity Testing & Analytical QC Protocols

- Packaging: Lecture Bottles, High-Pressure Cylinders & Bulk Tanks

- Distribution & Logistics

- Specialty Fluorochemical Distributor & Value-Added Reseller Networks

- Hazardous Goods, Corrosive & Toxic Gas Shipping Compliance (ADR, IATA, IMDG)

- Cold-Chain & Inert-Atmosphere Handling for Moisture-Sensitive Products

- Marketing & Sales Channels

- Value Addition & Profitability across Chain

- Emerging Trends & Disruptions

- On-Site / Point-of-Use (POU) Fluorine Generation Replacing Cylinder Supply

- Circular Economy, Fluorine Recovery & Recycling from Fab Exhaust Streams

- Digital Supply Chain Platforms & Predictive Procurement for UHP Chemicals

- Raw Material Sourcing & Suppliers

- Pricing Analysis

- Historical Vs Projected Pricing Analysis

- Demand-Supply Impact on Prices

- Application-wise Pricing Differences

- UHP Grade vs Electronic Grade vs Industrial Grade Price Benchmarks

- Etch Gas Pricing (NF₃, SF₆, C₄F₆, C₄F₈ & CHF₃ Comparative Benchmarks)

- Low-GWP Alternative Chemistry Price Premium vs Legacy High-GWP Fluorinated Gas

- Wet Chemical (HF, BHF) vs Specialty Lithography Fluorochemical Pricing

- Impact of Tariffs, Taxes, and Trade Policies

- Fluorspar & HF Import Tariffs & China Supply Chain Decoupling Impact

- F-Gas Carbon Tax, Emission Trading Scheme (ETS) & Abatement Cost Pass-Through

- Export Controls & Semiconductor Supply Chain Geopolitical Pricing Effects

- Key Player Pricing Strategies

- Technology Landscape

- Key Existing Technologies

- Plasma Etch & Reactive Ion Etch (RIE) Gas Chemistry (CF₄, CHF₃, SF₆, NF₃)

- Remote Plasma Chamber Clean with NF₃

- Wet HF & BHF Silicon Oxide Etching & Surface Preparation

- Spiro-OMeTAD-Class Fluorinated CVD Dielectric Precursors (FSG, Fluorinated TEOS)

- ArF Excimer Laser Photoresist & Fluoropolymer-Based Lithography Chemicals

- Standard EVA & Butyl Rubber Fluorochemical-Assisted Encapsulation

- Emerging & Next-gen Technologies

- Atomic Layer Etch (ALE) Fluorochemistry for Sub-5 nm Precision Patterning

- Low-GWP Etch Gases: C₄F₆, C₅F₈ & Novel Unsaturated Fluorocarbon Alternatives

- High-NA EUV Lithography: Fluorinated PAG, Fluoropolymer Resin & Pellicle Coating Needs

- Advanced ALD Fluorinated Precursors for High-k & Low-k Dielectric Films

- 3D-IC & Advanced Packaging Fluorochemical Requirements (TSV Etch, Underfill, Encapsulation)

- On-Site F₂ Generation & Point-of-Use (POU) Purification Eliminating Cylinder Logistics

- AI-Driven Process Optimisation & Digital Twin Models for Fluorochemical Consumption Forecasting

- Strategic Insights

- Future Technology Roadmap

- Opportunities for Differentiation via Technology

- Risks of Obsolescence & Barriers to Adoption

- PFAS Phase-Out Timeline & Impact on Existing Fluorochemical Product Portfolios

- Scale-Up & UHP Qualification Challenges for Novel Low-GWP Etch Gas Alternatives

- Geopolitical Supply Chain Restructuring & Domestic Fluorochemical Capacity Build-Out

- Key Existing Technologies

- Policy & Regulatory Landscape

- Competition Outlook (Leading 10 Companies)

- Competition Benchmarking

- Market Share Analysis by Product Type, Purity Grade & Geography

- R&D Intensity & Patent Portfolio Benchmarking

- Technology Node Qualification Breadth & Fab Customer Status Comparison

- Product Portfolio Breadth: Full-Stack Fluorochemical Supply vs Specialist Producers

- Market Leaders Vs New Entrants

- Established Global Fluorochemical Giants (Integrated Producers with Captive HF Supply)

- Regional Specialty Gas & Chemical Producers Entering Semiconductor-Grade Markets

- Start-ups & Technology Spin-Outs Commercialising Novel Low-GWP & POU Fluorine Solutions

- Competition Benchmarking

- Strategic Recommendations