Market Size, Growth Outlook, Key Drivers, and Challenges

The global syngas market is on a strong growth path, with one recent estimate placing demand at 290.91 million metric normal cubic meters per hour in 2025, rising to 552.65 million metric normal cubic meters per hour by 2031, implying a CAGR of 11.29% over 2026–2031. The growth story is being driven by syngas’s central role as an intermediate for hydrogen, methanol, ammonia, refining, and synthetic fuels, as well as by rising interest in cleaner fuel alternatives and wider government support for clean-energy and carbon-management initiatives. At the same time, the market remains constrained by high capital intensity, feedstock-price volatility, project complexity, carbon-emissions pressure on coal-linked routes, and the fact that many newer low-carbon pathways still need scale-up before they can compete with established fossil-based systems on cost and reliability. In practical terms, syngas demand is benefiting from decarbonization-linked industrial transition, but the market is simultaneously being forced to move from purely low-cost production toward lower-carbon, more flexible, and more integrated production models.

Feedstock Landscape: What Is Established, What Is Emerging, and What Has Future Potential

In feedstock terms, coal, natural gas, petroleum coke, and other liquid hydrocarbons such as naphtha/heavy oils remain the most established commercial syngas inputs today. Coal and petcoke are especially important where gasification is tied to chemicals, power, or heavy industrial chains, while natural gas dominates reforming-led pathways such as SMR and ATR. Biomass has moved beyond theory and is already used commercially in smaller and medium-scale gasification settings, though it is still less mature and less globally scaled than coal- and gas-based routes. Municipal solid waste / refuse-derived fuel and industrial or hazardous waste are better classified as emerging-to-demonstration feedstocks: they are technically proven in selected waste-to-syngas and gasification projects, but deployment remains more limited because feedstock heterogeneity, cleanup complexity, and project economics are harder to standardize. At the far end of the maturity curve, CO2 + green hydrogen / e-fuels pathways represent the clearest future-potential route. These pathways are gaining strategic relevance because they align with low-carbon fuel and circular-carbon systems, but they remain constrained by electrolyzer economics, renewable-power availability, and the need for new reactor and catalyst optimization. So, in maturity terms, the market today is led by coal, natural gas, petcoke, and liquid hydrocarbons; biomass sits in the early-commercial to scaling phase; waste-based feedstocks are emerging and project-specific; and CO2-derived synthetic syngas pathways remain the most important long-term opportunity rather than a fully scaled mainstream route.

Production Technology Maturity: Established Routes vs Pilot and Future Routes

On the production side, the most commercially established syngas technologies today are Steam Methane Reforming (SMR), Partial Oxidation (POX), Autothermal Reforming (ATR), and coal gasification. SMR remains the dominant gas-based route, especially for hydrogen-rich syngas from natural gas, while ATR is increasingly relevant where carbon capture integration and large-scale low-emission hydrogen or ammonia projects are being considered. POX is established in heavy feedstock and high-purity syngas applications, and coal gasification remains a major route in coal-rich chemical economies. Biomass gasification is further along than most emerging routes and can be considered early-commercial to scaling, especially in smaller and mid-scale systems, but it is still not as globally standardized as fossil routes. Plasma gasification, dry reforming, tri-reforming, sorption-enhanced reforming, catalytic gasification, and underground coal gasification are less mature overall and are better viewed across pilot, demonstration, or niche pre-commercial stages depending on the exact configuration. Dry reforming and tri-reforming are strategically attractive because they can utilize CO2 and improve carbon efficiency, but they are still limited by catalyst durability, heat management, and scale economics. Sorption-enhanced and catalytic gasification concepts show promise in process intensification and efficiency improvement, yet they have not displaced conventional routes commercially. Underground coal gasification has long been discussed as a future resource-conversion pathway, but commercial penetration remains limited because of environmental, groundwater, and project-control concerns. In short, SMR, ATR, POX, and coal gasification are the mature backbone of the current market; biomass gasification is the most advanced alternative route; and most CO2-linked or process-intensified reforming concepts remain in pilot, demo, or selective niche deployment.

End-Use Structure: Established Demand Centers and Emerging Growth Pockets

By end use, the most established and commercially important syngas outlets remain methanol, ammonia, hydrogen, refining, and synthetic fuels/value-chain intermediates such as oxo chemicals and alcohols. Hydrogen is particularly important because syngas remains a major intermediate in conventional hydrogen production, while ammonia and methanol continue to anchor large captive syngas demand in chemicals and fertilizers. Refining also remains a durable demand base because hydrogen-rich syngas supports upgrading and desulfurization-linked needs. Fischer–Tropsch fuels, Synthetic Natural Gas (SNG), DME, and steel/metallurgical applications are all strategically significant but vary more by geography, policy support, and feedstock economics. Fischer–Tropsch pathways attract attention because of their relevance to synthetic fuels and sustainable aviation fuel platforms, but they are still more selective and project-driven than methanol or ammonia. Power generation and IGCC have long been important syngas-linked applications, but their future attractiveness depends heavily on local fuel economics, carbon rules, and competition from renewables plus storage. Fuel cells and distributed energy represent a smaller but future-oriented outlet, especially where decentralized low-carbon systems and cleaner gaseous fuels become more valuable. Overall, current syngas demand is most firmly anchored in hydrogen, ammonia, methanol, and refining, while FT fuels, DME, SNG, steel decarbonization routes, and distributed-energy applications represent the more strategic long-term growth pockets.

Technology Analysis and Future Roadmap

From a broader technology-analysis perspective, the syngas industry today is still dominated by a commercially proven landscape built around reforming and gasification. Existing licensors and technology providers are strongest in SMR, ATR, POX, and large-scale gasification systems, with mature route selection usually determined by feedstock type, required H2/CO ratio, desired downstream product, plant scale, and carbon-management strategy. In general, gasification routes offer wide feedstock flexibility, especially for coal, petcoke, and certain waste streams, while reforming routes remain stronger for natural-gas-based hydrogen and ammonia systems. Efficiency, carbon intensity, and operating profile differ materially by route: conventional fossil-based routes remain cost-competitive and operationally robust, but they are more exposed to future carbon constraints, whereas ATR with carbon capture, biomass-to-syngas, and CO2-utilization routes are increasingly attractive in low-emission project design. Looking ahead, the roadmap is clearly moving toward low-carbon syngas technologies, especially biomass-to-syngas evolution, waste-to-syngas pathways, CO2 utilization routes, electrified reforming, green-hydrogen blending with carbon sources, carbon-capture-integrated systems, and modular/decentralized configurations. AI and digital control are also becoming more relevant for process optimization, predictive maintenance, and tighter control of feed variability and reactor performance. In maturity terms, the current market is still led by commercial fossil-based reforming and gasification, while biomass and some waste routes are scaling, and electrified, CO2-derived, and modular low-carbon syngas systems remain mostly in the pilot-to-pre-commercial corridor. The long-term direction is clear: future competitiveness will depend not only on making syngas efficiently, but on making it with lower carbon intensity, wider feedstock flexibility, stronger digital control, and better compatibility with downstream net-zero fuel and chemical systems.

Market Segmentation

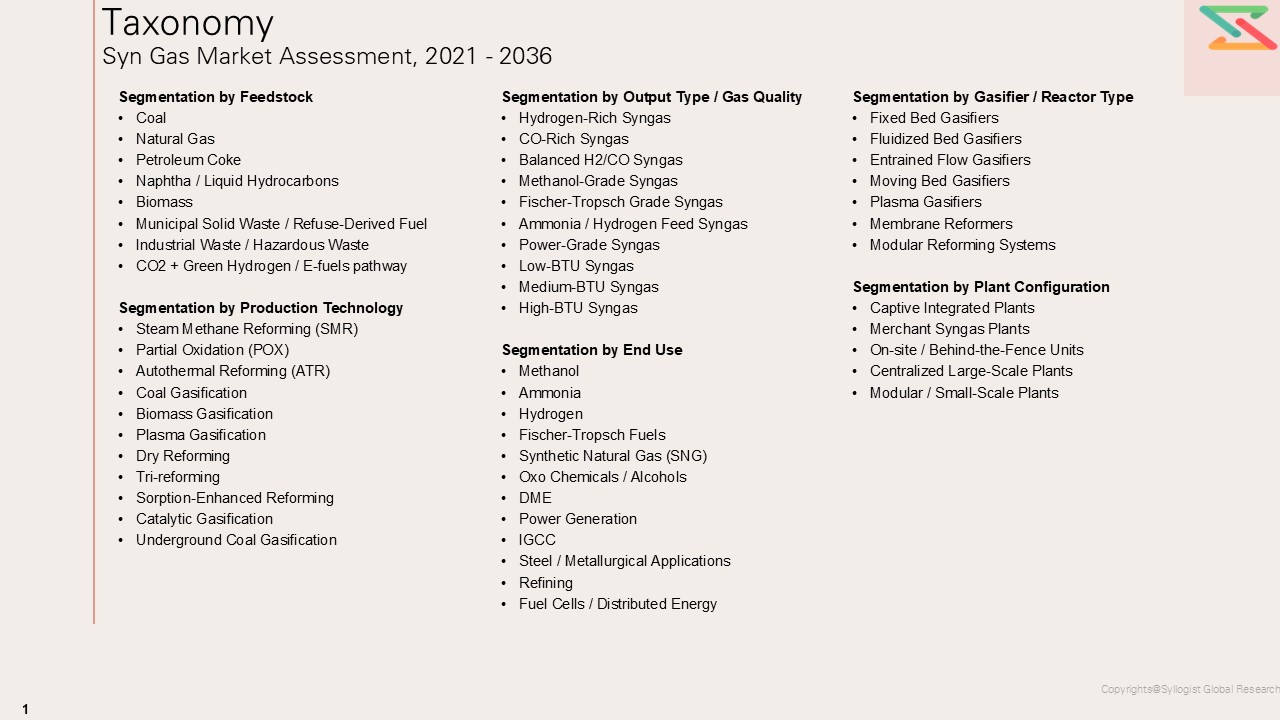

- Segmentation by Feedstock

- Coal

- Natural Gas

- Petroleum Coke

- Naphtha / Liquid Hydrocarbons

- Biomass

- Municipal Solid Waste / Refuse-Derived Fuel

- Industrial Waste / Hazardous Waste

- CO2 + Green Hydrogen / E-fuels pathway

- Segmentation by Production Technology

- Steam Methane Reforming (SMR)

- Partial Oxidation (POX)

- Autothermal Reforming (ATR)

- Coal Gasification

- Biomass Gasification

- Plasma Gasification

- Dry Reforming

- Tri-reforming

- Sorption-Enhanced Reforming

- Catalytic Gasification

- Underground Coal Gasification

- Segmentation by Output Type / Gas Quality

- Hydrogen-Rich Syngas

- CO-Rich Syngas

- Balanced H2/CO Syngas

- Methanol-Grade Syngas

- Fischer-Tropsch Grade Syngas

- Ammonia / Hydrogen Feed Syngas

- Power-Grade Syngas

- Low-BTU Syngas

- Medium-BTU Syngas

- High-BTU Syngas

- Segmentation by End Use

- Methanol

- Ammonia

- Hydrogen

- Fischer-Tropsch Fuels

- Synthetic Natural Gas (SNG)

- Oxo Chemicals / Alcohols

- DME

- Power Generation

- IGCC

- Steel / Metallurgical Applications

- Refining

- Fuel Cells / Distributed Energy

- Segmentation by Gasifier / Reactor Type

- Fixed Bed Gasifiers

- Fluidized Bed Gasifiers

- Entrained Flow Gasifiers

- Moving Bed Gasifiers

- Plasma Gasifiers

- Membrane Reformers

- Modular Reforming Systems

- Segmentation by Plant Configuration

- Captive Integrated Plants

- Merchant Syngas Plants

- On-site / Behind-the-Fence Units

- Centralized Large-Scale Plants

- Modular / Small-Scale Plants

- Market Definition and Scope

- Syngas Definition

- Composition Range and Quality Parameters

- Scope By Merchant Vs Captive Syngas

- Scope By Conventional Vs Low-Carbon Syngas

- Key Assumptions and Exclusions

- Executive Summary

- Market Snapshot

- Key Findings

- Technology Shift Highlights

- Feedstock Transition Outlook

- Strategic Opportunity Map

- Product Overview and Industry Structure

- What Syngas is and Why It Matters

- Syngas Value Chain

- Role Of Syngas in Chemicals, Fuels, Power, And Hydrogen

- Captive Vs Merchant Market Structure

- Integrated Vs Standalone Syngas Plants

- Research Methodology

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Risk Assessment Framework

- Political / Geopolitical Risk

- Raw Material Supply Risk

- Environmental and Regulatory Risk

- Financial / Market Risk

- Regulatory Framework & Standards

- Global Policy and Mandate Overview

- Transportation and Storage Regulations

- Sustainability and GHG Reduction Standards

- Environmental & Liability Considerations

- Global Syn Gas Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume

- Market Size & Forecast by Feedstock

- Coal

- Natural Gas

- Petroleum Coke

- Naphtha / Liquid Hydrocarbons

- Biomass

- Municipal Solid Waste / Refuse-Derived Fuel

- Industrial Waste / Hazardous Waste

- CO2 + Green Hydrogen / E-fuels pathway

- Market Size & Forecast by Production Technology

- Steam Methane Reforming (SMR)

- Partial Oxidation (POX)

- Autothermal Reforming (ATR)

- Coal Gasification

- Biomass Gasification

- Plasma Gasification

- Dry Reforming

- Tri-reforming

- Sorption-Enhanced Reforming

- Catalytic Gasification

- Underground Coal Gasification

- Market Size & Forecast by Gasifier / Reactor Type

- Fixed Bed Gasifiers

- Fluidized Bed Gasifiers

- Entrained Flow Gasifiers

- Moving Bed Gasifiers

- Plasma Gasifiers

- Membrane Reformers

- Modular Reforming Systems

- Market Size & Forecast by Output Type / Gas Quality

- Hydrogen-Rich Syngas

- CO-Rich Syngas

- Balanced H2/CO Syngas

- Methanol-Grade Syngas

- Fischer-Tropsch Grade Syngas

- Ammonia / Hydrogen Feed Syngas

- Power-Grade Syngas

- Low-BTU Syngas

- Medium-BTU Syngas

- High-BTU Syngas

- Market Size & Forecast by End Use

- Methanol

- Ammonia

- Hydrogen

- Fischer-Tropsch Fuels

- Synthetic Natural Gas (SNG)

- Oxo Chemicals / Alcohols

- DME

- Power Generation

- IGCC

- Steel / Metallurgical Applications

- Refining

- Fuel Cells / Distributed Energy

- Market Size & Forecast by Plant Configuration

- Captive Integrated Plants

- Merchant Syngas Plants

- On-site / Behind-the-Fence Units

- Centralized Large-Scale Plants

- Modular / Small-Scale Plants

- Market Size & Forecast by Region

- North America

- Europe

- Asia-Pacific

- Middle East & Africa

- South America

- Asia-Pacific Syn Gas Market Outlook

- Market Size & Forecast by Value & Volume

- Market Size & Forecast by Feedstock

- Market Size & Forecast by Production Technology

- Market Size & Forecast by Output Type / Gas Quality

- Market Size & Forecast by End Use

- Market Size & Forecast by Gasifier / Reactor Type

- Market Size & Forecast by Plant Configuration

- Europe Syn Gas Market Outlook

- Market Size & Forecast by Value & Volume

- Market Size & Forecast by Feedstock

- Market Size & Forecast by Production Technology

- Market Size & Forecast by Output Type / Gas Quality

- Market Size & Forecast by End Use

- Market Size & Forecast by Gasifier / Reactor Type

- Market Size & Forecast by Plant Configuration

- North America Syn Gas Market Outlook

- Market Size & Forecast by Value & Volume

- Market Size & Forecast by Feedstock

- Market Size & Forecast by Production Technology

- Market Size & Forecast by Output Type / Gas Quality

- Market Size & Forecast by End Use

- Market Size & Forecast by Gasifier / Reactor Type

- Market Size & Forecast by Plant Configuration

- Latin America Syn Gas Market Outlook

- Market Size & Forecast by Value & Volume

- Market Size & Forecast by Feedstock

- Market Size & Forecast by Production Technology

- Market Size & Forecast by Output Type / Gas Quality

- Market Size & Forecast by End Use

- Market Size & Forecast by Gasifier / Reactor Type

- Market Size & Forecast by Plant Configuration

- Middle East & Africa Syn Gas Market Outlook

- Market Size & Forecast by Value & Volume

- Market Size & Forecast by Feedstock

- Market Size & Forecast by Production Technology

- Market Size & Forecast by Output Type / Gas Quality

- Market Size & Forecast by End Use

- Market Size & Forecast by Gasifier / Reactor Type

- Market Size & Forecast by Plant Configuration

- Country wise Syn Gas Market Outlook

- Market Size & Forecast by Value & Volume

- Market Size & Forecast by Feedstock

- Market Size & Forecast by Production Technology

- Market Size & Forecast by Output Type / Gas Quality

- Market Size & Forecast by End Use

- Market Size & Forecast by Gasifier / Reactor Type

- Market Size & Forecast by Plant Configuration

Countries Analyzed in the Syllogist Global Research Portfolio: China, India, Japan, South Korea, Indonesia, Australia, United States, Canada, Mexico, Germany, United Kingdom, France, Italy, Spain, Netherlands, Saudi Arabia, Qatar, Brazil, South Africa, Russia

- Syn Gas Market Technology Analysis

- Existing Technology Landscape

- Commercially Established Syngas Technologies

- Technology Readiness by Route

- Leading Licensors and Technology Providers

- Typical Operating Conditions

- Feedstock Compatibility by Technology

- Efficiency Comparison Across Technologies

- Carbon Intensity by Route

- Flexibility and Scale Comparison

- Future Technology Roadmap

- Low-Carbon Syngas Technologies

- Biomass-To-Syngas Evolution

- Waste-To-Syngas Pathways

- CO2 Utilization Routes

- Electrified Reforming

- Green Hydrogen Blending with Carbon Sources

- AI / Digital Control in Gasification and Reforming

- Carbon Capture Integrated Syngas Systems

- Modular And Decentralized Systems

- Technology Maturity Outlook: Current, Pilot, Demo, Pre-Commercial

- Raw Material Analysis: Existing and Future Feedstock Outlook

- Existing Feedstock Landscape

- Feedstock Availability by Region

- Price Competitiveness by Feedstock

- Carbon Intensity by Feedstock

- Feedstock Suitability by End Use

- Future Feedstock Transition Outlook

- Role of Biomass Residues

- Role of Waste Streams

- Role of Pet coke in Heavy Industry

- Natural Gas Vs Coal Vs Biomass Economics

- Future Role of CO2-Derived Carbon Feedstock

- Feedstock-to-Technology Suitability Matrix

- Coal Vs Gasification Routes

- Natural Gas Vs Reforming Routes

- Biomass Vs Gasifier Types

- Waste Feedstocks Vs Advanced Gasification

- Pet coke Vs POX/Gasification

- Best-Fit Technology by Feedstock Quality

- Best-Fit End Use by Syngas Composition

- Capex Analysis

- Capex by technology route

- Capex by plant scale

- Capex by feedstock type

- Brownfield vs greenfield economics

- Syngas cleanup and conditioning Capex

- Carbon capture integration Capex

- Compression / storage / balance-of-plant costs

- Regional Capex comparison

- Sensitivity to materials and EPC costs

- OpEx Analysis

- Feedstock Cost Contribution

- Utility Cost Contribution

- Catalyst And Consumables

- Labor And Maintenance

- Oxygen Supply Economics

- Ash / Slag / Waste Handling

- Carbon Compliance Cost

- Water Use and Treatment Cost

- Delivered Syngas Cost Comparison

- Techno-Economic Comparison

- SMR vs ATR vs POX

- Coal gasification vs biomass gasification

- Conventional vs low-carbon syngas

- Large-scale vs modular systems

- Captive vs merchant economics

- Cost per Nm3 / cost per GJ / cost per ton downstream output

- Breakeven feedstock analysis

- Sensitivity to gas, coal, power, and carbon prices

- Carbon and Sustainability Benchmarking

- Carbon Footprint by Route

- Water Intensity by Route

- Waste Generation by Route

- Carbon Capture Compatibility

- Lifecycle Emissions Comparison

- Blue Vs Gray Vs Green-Linked Syngas Pathways

- ESG Attractiveness by Technology

- Syngas Cleanup and Conditioning Analysis

- Sulfur Removal

- Tar Removal

- Particulate Removal

- CO2 Removal

- Shift Conversion

- Methanation

- Acid Gas Removal

- Compression And Purification

- Impact of Cleanup Costs on Downstream Viability

- Downstream Value Chain Analysis

- Syngas To Methanol

- Syngas To Ammonia / Hydrogen

- Syngas To FT Fuels

- Syngas To SNG

- Syngas To Chemicals

- Syngas To Power

- Downstream Margin Comparison

- Most Attractive Downstream Pathways by Region

- Application Attractiveness / Margin Pool Analysis

- Best Downstream Use by Feedstock

- Best Downstream Use by Region

- High-Growth Application Pockets

- High-Margin Application Pockets

- Demand Risk Vs Return Comparison

- Strategic Attractiveness Matrix

- Policy, Regulation, and Carbon Framework

- Carbon Pricing Implications

- Emission Standards

- Waste-To-Energy Regulations

- Renewable Fuels Incentives

- Hydrogen Economy Policies

- CCS Incentives

- Biofuel Blending Mandates

- Country-Level Policy Comparison

- Future of Syngas: Strategic Outlook

- Role In Low-Carbon Fuels

- Role In Hydrogen Economy

- Role In Circular Carbon Systems

- Role In Waste Valorization

- Impact Of Electrification on Syngas Demand

- Can Syngas Remain Relevant in a Net-Zero Economy?

- Regional Winners and Losers

- Future Investment Hotspots

- Competitive Landscape

- Major Syngas Producers

- Technology Licensors

- EPC Companies

- Gasifier/Reformer Suppliers

- Integrated Chemical Players

- Strategic Partnerships

- Capacity Expansions

- M&A and Joint Ventures

- Country / Regional Opportunity Assessment

- Feedstock-Rich Countries

- Coal-Based Opportunity Markets

- Gas-Rich Opportunity Markets

- Biomass-Rich Opportunity Markets

- Waste-To-Syngas Opportunity Regions

- Policy-Supported Low-Carbon Markets

- Country Attractiveness Index

- Scenario Analysis

- Base Case

- Low-Carbon Transition Case

- High Gas Price Case

- High Carbon Price Case

- Biomass / Waste Breakthrough Case

- Hydrogen Substitution Risk Case

- Strategic Recommendations

- Best Technology-Route Opportunities

- Best Feedstock-Route Combinations

- Best End-Use Pockets

- Capex-Light Vs Scale-Heavy Strategies

- Regional Entry Priorities

- Investment Risk Mitigation