Market Definition

The Global Synthetic Fuels from Natural Gas Market encompasses the industrial processes, technologies, facilities, and commercial value chains through which natural gas is chemically converted into liquid or gaseous synthetic hydrocarbon fuels and fuel blendstocks that substitute for or supplement conventionally refined petroleum-derived transportation fuels, aviation fuels, marine bunker fuels, and industrial energy carriers, utilizing natural gas as the primary carbon and hydrogen feedstock in thermochemical, catalytic, and reforming conversion pathways that produce synthesis gas as an intermediate product and subsequently upgrade it into finished synthetic fuel products with defined composition, combustion, and emissions characteristics. The product scope of this market encompasses gas-to-liquids facilities producing synthetic crude oil and finished distillate products including synthetic diesel, synthetic jet fuel, synthetic naphtha, and synthetic lubricant base oils through Fischer-Tropsch synthesis using iron-based or cobalt-based catalysts operating at elevated temperature and pressure conditions in fixed-bed, slurry-bed, or microchannel reactor configurations, methanol-to-gasoline and methanol-to-olefins conversion processes that route natural gas through methanol synthesis as a chemical intermediate before catalytic conversion into gasoline blendstocks or olefinic feedstocks for further refining, dimethyl ether synthesis from natural gas-derived synthesis gas for use as a diesel substitute in heavy transport and off-road equipment applications, synthetic natural gas production through methanation of natural gas-derived synthesis gas for grid injection or replacement of conventional pipeline gas, gas-to-liquids based synthetic paraffinic kerosene certified as a sustainable aviation fuel blendstock under international aviation fuel certification standards, and the integration of natural gas conversion pathways with carbon capture and storage systems to produce low-carbon or near-zero-carbon synthetic fuels by capturing and permanently sequestering the carbon dioxide co-produced during synthesis gas generation and Fischer-Tropsch or methanol synthesis reactions. The technology landscape within this market spans conventional steam methane reforming and autothermal reforming for synthesis gas production, partial oxidation processes using oxygen-blown or air-blown gasification reactors adapted for natural gas feedstock, advanced compact reforming reactor systems developed for smaller-scale modular gas-to-liquids applications including associated gas monetization at remote oil field locations, membrane reactor systems integrating reforming and hydrogen separation in a single process unit to improve conversion efficiency and reduce capital cost, microreactor and structured reactor systems enabling intensified process configurations with superior heat transfer and catalyst utilization characteristics, and the downstream Fischer-Tropsch wax hydrocracking, product fractionation, and blending infrastructure required to convert raw Fischer-Tropsch synthesis products into finished fuel specifications meeting international quality and emissions standards. The value chain of this market extends from natural gas producers and pipeline transmission companies supplying feedstock gas at the plant gate through oxygen plant suppliers providing the industrial oxygen required for partial oxidation and autothermal reforming processes, synthesis gas generation equipment manufacturers, Fischer-Tropsch and methanol synthesis reactor and catalyst suppliers, product upgrading and hydrocracking unit designers and builders, large-scale engineering procurement and construction contractors executing gas-to-liquids facility projects, product blending and quality certification infrastructure operators, and the aviation fuel wholesalers, road transportation fuel distributors, marine bunker fuel suppliers, and industrial energy buyers whose offtake agreements underpin the commercial viability of synthetic fuel production facilities operating across the natural gas-rich producing regions of the Middle East, Central Asia, Africa, North America, and the Asia-Pacific basin.

Market Insights

The global synthetic fuels from natural gas market is experiencing a period of renewed strategic interest and carefully calibrated investment in 2026, driven by the intersection of energy security imperatives that are elevating the strategic value of domestically convertible gaseous hydrocarbon resources into transportable liquid fuel forms, the progressive tightening of aviation and marine fuel decarbonization requirements that are creating regulatory demand for low-carbon synthetic fuel blendstocks certifiable under international standards, and the persistent challenge of monetizing stranded and associated natural gas resources in remote or infrastructure-deficient locations where gas-to-liquids conversion offers a compelling value proposition relative to pipeline export, liquefaction, or flaring alternatives. The global synthetic fuels from natural gas market was valued at approximately USD 38 billion in 2025 and is projected to expand at a compound annual growth rate of 7 percent through 2036, reaching approximately USD 79 billion by the end of the forecast period, a trajectory reflecting the structural demand for high-quality synthetic distillate fuels from aviation and marine transport sectors facing regulatory pressure to reduce particulate and sulfur dioxide emissions, the monetization imperative for the large global inventory of stranded and associated natural gas whose conversion to synthetic liquid fuels enables transportation to market without pipeline or liquefaction infrastructure investment, and the growing interest of energy companies in integrating carbon capture and storage with natural gas conversion to produce low-carbon synthetic fuels whose lifecycle greenhouse gas intensity qualifies for regulatory credits and voluntary carbon market premiums. The competitive landscape of the market is structured around a small number of large integrated energy companies that operate commercial-scale gas-to-liquids facilities with multi-decade operational track records, a growing cohort of technology developers and engineering companies promoting advanced compact and modular gas-to-liquids reactor systems targeting smaller-scale and remote associated gas conversion applications, specialist Fischer-Tropsch catalyst developers whose proprietary catalyst formulations differentiate the product selectivity, thermal stability, and operational lifetime of gas-to-liquids process trains, and the engineering procurement and construction contractors with the multi-billion USD project execution capability required to deliver large-scale gas-to-liquids facilities within defined cost and schedule parameters.

A defining trend reshaping the commercial and technology landscape of the synthetic fuels from natural gas market is the progressive development and certification of gas-to-liquids-based synthetic paraffinic kerosene as an approved sustainable aviation fuel pathway under the ASTM D7566 standard and equivalent international aviation fuel certification frameworks, creating an aviation fuel market entry point for synthetic kerosene produced from natural gas that offers the ultra-low aromatic content, near-zero sulfur specification, and consistent combustion quality characteristics that distinguish Fischer-Tropsch synthetic aviation fuel from conventionally refined jet fuel and that are generating active procurement interest from major international airlines committed to sustainable aviation fuel adoption targets under the International Air Transport Association’s net-zero carbon emissions by 2050 commitment. The aviation fuel application for gas-to-liquids synthetic paraffinic kerosene is commercially significant because it provides a price premium pathway relative to commodity synthetic diesel markets, as sustainable aviation fuel commands premiums above conventional jet fuel pricing in markets where airlines face mandatory sustainable aviation fuel blending obligations or where voluntary corporate sustainability commitments and passenger willingness to contribute to sustainable aviation fuel purchase funds are generating supplementary revenue streams that improve the commercial economics of gas-to-liquids aviation fuel production relative to the conventional distillate markets that have historically been the primary revenue driver for large commercial gas-to-liquids facilities. The certification of natural gas-based synthetic paraffinic kerosene as a sustainable aviation fuel blendstock under pathways that incorporate lifecycle carbon accounting incorporating the emissions intensity of the natural gas feedstock production and conversion process is creating a market segmentation within gas-to-liquids aviation fuel between standard synthetic kerosene produced from conventional natural gas and low-carbon synthetic kerosene produced from natural gas conversion integrated with carbon capture and storage systems, with the latter commanding substantially higher sustainable aviation fuel premium pricing in markets where regulatory frameworks assign carbon intensity reduction credits based on lifecycle greenhouse gas performance rather than feedstock type alone.

The associated and stranded natural gas monetization driver for gas-to-liquids investment continues to represent the most commercially compelling near-term application context for compact and modular gas-to-liquids technology development, as the global inventory of natural gas resources that cannot be economically transported to market through pipeline or liquefied natural gas infrastructure due to their remote location, small reservoir size, complex ownership structure, or inadequate supporting infrastructure represents a large and geographically distributed feedstock opportunity for small-scale and modular gas-to-liquids conversion systems that can be deployed at the production site, operated with minimal local workforce, and transported by road or sea between locations as gas availability evolves over field production life cycles. The environmental imperative to eliminate routine natural gas flaring at oil field locations, which wastes a globally significant volume of associated gas annually while generating greenhouse gas and black carbon emissions with documented public health and climate impacts, is creating regulatory pressure and commercial incentive for operators to adopt gas-to-liquids or other associated gas utilization technologies that convert what would otherwise be a flared waste stream into marketable synthetic liquid fuel products that can be transported by truck or barge to local or regional fuel markets without requiring the pipeline infrastructure whose construction cost would be prohibitive for small and scattered associated gas volumes. The development of compact modular gas-to-liquids reactor systems by technology developers targeting this associated gas monetization opportunity has produced a generation of containerized and skid-mounted Fischer-Tropsch and methanol synthesis systems in the thousands of barrels per day capacity range that are demonstrating deployability advantages over conventional large-scale gas-to-liquids facilities and whose unit economics, while not yet competitive with large-scale facilities at equivalent feedstock cost, are approaching commercial viability in remote locations where the alternative to gas-to-liquids conversion is flaring or venting and where the synthetic fuel product commands premium pricing relative to infrastructure-constrained local markets.

From a regional perspective, the Middle East represents the most commercially significant regional market for large-scale conventional gas-to-liquids production by installed capacity, housing the world’s largest operational gas-to-liquids facilities whose production of synthetic diesel, naphtha, and base oil feedstocks from low-cost Qatari natural gas has established the commercial proof of concept for large integrated gas-to-liquids operations and whose operational cost structure and product quality track record provides the commercial benchmark against which competing technology and project concepts are evaluated by energy company project developers and their investment banking advisors. Africa, and specifically South Africa and emerging associated gas monetization opportunities in Nigeria, Angola, Mozambique, and Tanzania, represents a market of significant near-term project development interest where the combination of large gas resource inventories, limited pipeline export options, domestic fuel supply deficit conditions, and operator obligation to eliminate routine flaring is creating active project feasibility study activity for both large-scale gas-to-liquids facilities targeting export fuel markets and smaller-scale associated gas conversion systems addressing domestic fuel supply and flare elimination objectives. North America represents the most dynamic market for advanced compact and modular gas-to-liquids technology demonstration and early commercial deployment, driven by the large inventory of associated gas at Permian Basin and Bakken formation oil production sites that is subject to flaring reduction regulatory requirements and whose conversion to synthetic liquid fuels through small-scale gas-to-liquids systems represents an economically attractive alternative to pipeline gathering infrastructure investment for the smallest and most remote production locations. Asia-Pacific, led by Australia, Malaysia, and the major liquefied natural gas-producing nations of Southeast Asia, represents a growing market for gas-to-liquids investment driven by the strategic interest of national oil companies in diversifying natural gas monetization pathways beyond liquefied natural gas export and in developing domestic synthetic fuel production capability for aviation, marine, and industrial energy security purposes.

Key Drivers

Aviation and Marine Sector Decarbonization Regulations Creating Structural Demand for Low-Carbon Synthetic Fuel Blendstocks Producible from Natural Gas Conversion Pathways

The most commercially consequential near-term demand driver for synthetic fuels from natural gas is the progressive implementation of mandatory sustainable aviation fuel blending obligations and marine fuel carbon intensity reduction requirements across major aviation and shipping markets, regulations that are creating structural and growing demand for synthetic fuel blendstocks whose production from natural gas conversion can meet defined lifecycle carbon intensity thresholds and whose combustion performance characteristics are equal to or superior to conventionally refined petroleum fuels in critical applications where fuel quality consistency, energy density, and compatibility with existing engine and fuel system infrastructure are non-negotiable operational requirements. The European Union ReFuelEU Aviation regulation, which mandates progressive sustainable aviation fuel blending percentages in aviation fuel uplifted at European airports escalating from 2 percent in 2025 to 70 percent by 2050, creates a large and growing guaranteed off-take market for sustainable aviation fuel produced from approved pathways including Fischer-Tropsch synthetic paraffinic kerosene derived from natural gas conversion, provided the feedstock and conversion process meets the lifecycle greenhouse gas reduction threshold relative to conventional jet fuel that is specified in the regulatory carbon accounting methodology. The United States Inflation Reduction Act sustainable aviation fuel tax credit, which provides production incentives scaled to the lifecycle carbon intensity reduction of qualifying sustainable aviation fuel relative to conventional jet fuel on a well-to-wing basis, creates a financial incentive for the development of gas-to-liquids aviation fuel production integrated with carbon capture and storage systems whose lifecycle carbon intensity performance can achieve the reduction levels required to qualify for the maximum credit tier and whose USD per gallon production economics are materially improved by the credit value to a level approaching commercial competitiveness with conventionally refined jet fuel in premium sustainable aviation fuel markets. The International Maritime Organization’s Carbon Intensity Indicator framework and its FuelEU Maritime equivalent in the European Union, which impose progressive reductions in shipping sector greenhouse gas emissions intensity and create financial incentives for early adoption of low-carbon alternative marine fuels, are driving interest in synthetic diesel and dimethyl ether produced from natural gas conversion as near-term marine fuel alternatives whose energy density, engine compatibility, and infrastructure familiarity advantages over hydrogen and ammonia-based alternative fuels make them commercially attractive transitional solutions for ship operators seeking to reduce fuel carbon intensity within existing engine and bunkering infrastructure constraints. The commercial pipeline of aviation and marine synthetic fuel offtake agreements being actively negotiated between synthetic fuel producers, airlines, and shipping companies is providing project developers with the revenue visibility required to advance gas-to-liquids facility projects toward final investment decision in markets where regulatory blending mandates and sustainable fuel premium pricing structures are sufficiently mature to support project financing at acceptable cost of capital levels.

Energy Security Imperatives and the Strategic Value of Converting Domestic Natural Gas Resources into Liquid Transportation Fuels Reducing Dependence on Crude Oil Imports

The intensification of energy security concerns across major energy-importing economies following repeated supply chain disruptions, geopolitical conflicts affecting crude oil and petroleum product trade flows, and the growing strategic awareness among national governments of the vulnerability of transportation fuel supply chains dependent on politically concentrated crude oil production sources is generating a powerful and durable policy-driven demand driver for synthetic fuels from natural gas investment in countries and regions possessing natural gas resources that can substitute for crude oil import dependence through domestic conversion to synthetic liquid transportation fuels. The energy security argument for gas-to-liquids investment is particularly compelling in natural gas-rich nations that simultaneously import significant volumes of refined petroleum products, where the gap between domestic natural gas resource abundance and petroleum product import dependency represents both an economic inefficiency and a strategic vulnerability that gas-to-liquids investment can address by capturing the value-add of fuel conversion domestically rather than exporting gas and re-importing refined products through potentially disrupted international supply chains. In the Asia-Pacific region, Japan, South Korea, and several Southeast Asian economies whose energy security strategies have been materially affected by the volatility of global liquefied natural gas and crude oil markets are evaluating synthetic fuel production from natural gas as a component of diversified energy supply portfolios that reduce dependence on any single import supply source or fuel type, with government energy agencies actively supporting feasibility studies and pilot programs for gas-to-liquids technologies that could contribute to domestic synthetic fuel production capability at commercially meaningful scale. The strategic premium assigned to domestic synthetic fuel production capability by national energy security planners is supporting policy frameworks including investment incentives, preferential procurement of domestically produced synthetic fuels for government vehicle and equipment fleets, military aviation and logistics fuel diversification programs, and strategic synthetic fuel reserve development that collectively improve the commercial economics of gas-to-liquids investment beyond what unsubsidized market economics alone would support, providing the policy uplift required to close the economic gap between gas-to-liquids production costs and conventional refined fuel market prices in strategic application contexts. The long-duration and capital-intensive nature of gas-to-liquids facility investments, whose 20 to 30 year operational lifespans span multiple crude oil price cycles, makes the energy security policy framework a particularly important commercial enabler as the stable and predictable demand signal provided by long-term government offtake commitments or mandated blending obligations reduces the revenue risk that otherwise constrains private sector investment in large-scale gas-to-liquids facilities in markets where short-term commodity price fluctuations create uncertainty about the commercial competitiveness of synthetic fuel production relative to refined petroleum product alternatives.

Key Challenges

High Capital Expenditure Intensity of Gas-to-Liquids Facilities and the Vulnerability of Project Economics to Natural Gas Feedstock Cost and Crude Oil Price Fluctuations

The most persistent structural challenge limiting investment in synthetic fuels from natural gas is the exceptionally high capital expenditure intensity of commercial-scale gas-to-liquids facilities, whose synthesis gas generation, Fischer-Tropsch reactor systems, product upgrading and fractionation infrastructure, utilities, offsites, and ancillary process units collectively require multi-billion USD capital investments that expose project developers and their financing institutions to extended construction periods, significant engineering cost uncertainty, and a commercialization timeline that requires sustained favorable feedstock and product price differentials across a multi-decade operational life to generate acceptable returns on invested capital. The capital cost intensity of gas-to-liquids projects reflects the complexity of the three-stage process conversion sequence from natural gas feedstock through synthesis gas generation to Fischer-Tropsch synthesis and product upgrading, each of which requires large-scale specialized process equipment operating at elevated temperature and pressure conditions that demands high-specification materials of construction, extensive instrumentation and control systems, large heat integration networks, and safety system infrastructure whose combined engineering scope and equipment procurement lead time drives construction costs and schedules that have historically proven difficult to control within original project budget and completion date estimates. The commercial economics of gas-to-liquids facilities are structurally sensitive to the spread between natural gas feedstock acquisition cost and synthetic crude oil or finished product sale price, a spread that narrows substantially during periods of low crude oil prices or high natural gas prices and that has historically been the primary cause of gas-to-liquids facility operational impairment and project cancellation, as the inability to achieve a sufficient price differential between the feedstock and product sides of the conversion process eliminates the operating margin required to service the capital cost of the facility and generate a commercial return on investment. The transition of the energy sector toward renewable electricity and low-carbon fuel alternatives over the forecast period introduces an additional long-term demand risk for synthetic fuel producers, as the potential substitution of synthetic hydrocarbons by electrofuels, green hydrogen, and battery electric vehicles in transportation markets that currently represent the primary offtake channel for gas-to-liquids synthetic diesel and naphtha could reduce the addressable market for natural gas-derived synthetic fuels and erode the long-term price realizations available to gas-to-liquids facilities whose capital investments require decades of revenue generation to recover.

Lifecycle Carbon Intensity Constraints and the Challenge of Qualifying Natural Gas-Derived Synthetic Fuels Under Increasingly Stringent Low-Carbon Fuel Standards

A structurally significant commercial challenge limiting the market development potential of synthetic fuels from natural gas in the growing regulatory and voluntary sustainability-driven fuel market segments is the inherent carbon intensity of natural gas as a fossil fuel feedstock whose combustion-derived carbon dioxide emissions are released into the atmosphere either during the synthesis gas generation step within the gas-to-liquids process or upon combustion of the finished synthetic fuel product by the end user, resulting in a well-to-wheel lifecycle greenhouse gas intensity for conventionally produced gas-to-liquids synthetic fuels that is comparable to or in some process configurations higher than the lifecycle intensity of conventionally refined petroleum fuels and that therefore does not qualify for the carbon intensity reduction credits and sustainable fuel premium pricing mechanisms that are becoming the primary commercial revenue enhancement pathway for synthetic fuel producers in regulated aviation and marine fuel markets. The lifecycle carbon accounting framework applied to synthetic fuels from natural gas under the regulatory methodologies of the European Union ReFuelEU Aviation regulation, the United States Inflation Reduction Act sustainable aviation fuel tax credit, the International Civil Aviation Organization’s Carbon Offsetting and Reduction Scheme for International Aviation, and the International Maritime Organization’s greenhouse gas reduction framework all assess the carbon intensity of the feedstock extraction, processing, transmission, conversion, and product combustion stages on a well-to-wake or well-to-wheel basis, and the results of these lifecycle assessments for conventionally produced gas-to-liquids synthetic fuels typically show insufficient lifecycle carbon intensity reduction relative to the petroleum fuel baseline to qualify for the highest sustainable fuel incentive tiers that are necessary to generate the premium revenue required for commercially viable project economics in competitive sustainable fuel markets. The integration of carbon capture and storage with gas-to-liquids facilities, which captures the carbon dioxide co-produced during steam methane reforming or autothermal reforming synthesis gas generation and permanently sequesters it in geological formations, represents the primary technical pathway to achieving the lifecycle carbon intensity reduction required to qualify gas-to-liquids synthetic fuels for premium sustainable fuel market incentives and certifications, but introduces additional capital cost for carbon dioxide capture, compression, transport, and injection infrastructure and requires access to suitable geological storage formations in proximity to the gas-to-liquids facility whose availability is geographically constrained and whose permitting and development timeline adds complexity and cost to integrated gas-to-liquids and carbon capture and storage project execution. The potential for future regulatory tightening of the lifecycle carbon intensity reduction thresholds required for sustainable fuel qualification, driven by the progressive escalation of climate policy ambition and the increasing competitiveness of electrofuel alternatives whose lifecycle carbon intensity can approach zero when produced from renewable electricity and green hydrogen, creates a long-term regulatory risk for gas-to-liquids synthetic fuel producers whose current investments in carbon capture and storage integration may prove insufficient to maintain sustainable fuel qualification as regulatory standards evolve over the multi-decade operational life of gas-to-liquids facilities commissioned during the forecast period.

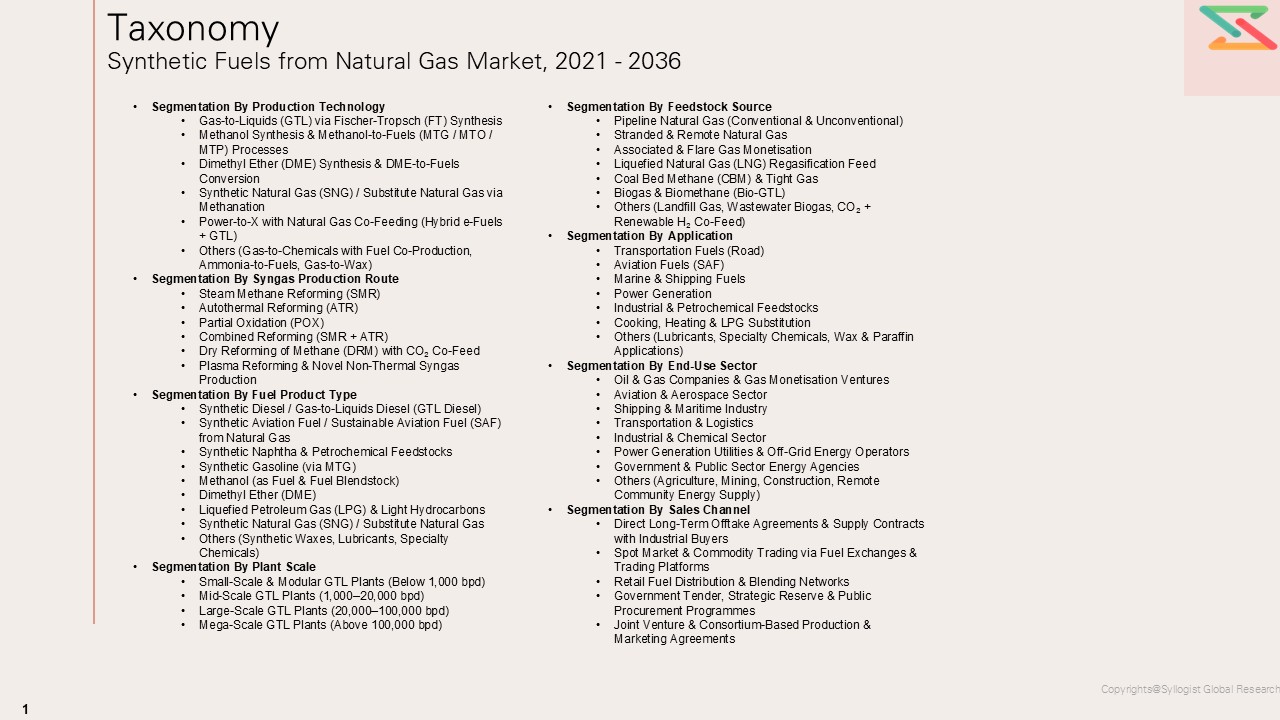

Market Segmentation

- Segmentation By Conversion Process Technology

- Fischer-Tropsch Synthesis via Steam Methane Reforming

- Fischer-Tropsch Synthesis via Autothermal Reforming

- Fischer-Tropsch Synthesis via Partial Oxidation

- Methanol-to-Gasoline (MTG) Conversion

- Methanol-to-Olefins and Olefins-to-Fuels (MTO-OTF)

- Dimethyl Ether (DME) Synthesis from Synthesis Gas

- Compact and Modular Microchannel Fischer-Tropsch Systems

- Integrated Gas-to-Liquids with Carbon Capture and Storage

- Others

- Segmentation By Synthetic Fuel Product

- Synthetic Diesel and Middle Distillate Blendstocks

- Synthetic Paraffinic Kerosene (Aviation Fuel Blendstock)

- Synthetic Naphtha and Gasoline Blendstocks

- Synthetic Lubricant Base Oils and Waxes

- Dimethyl Ether (DME) Fuel

- Synthetic Methanol for Fuel Applications

- Synthetic Natural Gas (SNG) for Grid Injection

- Fischer-Tropsch Crude (Syncrude) for Refinery Integration

- Others

- Segmentation By Feedstock Type

- Pipeline Natural Gas

- Associated Gas from Oil Production Fields

- Stranded and Remote Natural Gas Reserves

- Liquefied Natural Gas (LNG) Regasification Streams

- Coalbed Methane and Tight Gas

- Biomethane and Renewable Natural Gas (Hybrid Pathways)

- Others

- Segmentation By Facility Scale

- Large-Scale Integrated Gas-to-Liquids Plants (Above 30,000 bpd)

- Mid-Scale Gas-to-Liquids Facilities (5,000 to 30,000 bpd)

- Small-Scale Modular Gas-to-Liquids Systems (500 to 5,000 bpd)

- Micro-Scale and Containerized Gas-to-Liquids Units (Below 500 bpd)

- Segmentation By End-Use Application

- Aviation Fuel (Sustainable Aviation Fuel Blending)

- Road Transportation Diesel and Gasoline Blending

- Marine Bunker Fuel and Shipping Sector Supply

- Military and Defense Aviation and Ground Fuel

- Off-Road Heavy Equipment and Mining Fuel

- Industrial Process Energy and Chemical Feedstocks

- Power Generation Fuel

- Others

- Segmentation By Fischer-Tropsch Catalyst Type

- Cobalt-Based Low-Temperature Fischer-Tropsch Catalysts

- Iron-Based High-Temperature Fischer-Tropsch Catalysts

- Iron-Based Low-Temperature Fischer-Tropsch Catalysts

- Proprietary and Promoted Advanced Fischer-Tropsch Catalysts

- Others

- Segmentation By Carbon Management Integration

- Conventional Gas-to-Liquids Without Carbon Capture

- Gas-to-Liquids with Post-Combustion Carbon Capture

- Gas-to-Liquids with Pre-Combustion Carbon Capture

- Gas-to-Liquids with Geological Carbon Dioxide Storage

- Gas-to-Liquids with Enhanced Oil Recovery Carbon Dioxide Utilization

- Others

- Segmentation By Sales Channel and Offtake Mechanism

- Long-Term Offtake Agreements with Aviation Fuel Wholesalers

- Marine Bunker Fuel Supply Contracts

- Road Fuel Blending and Distribution Agreements

- Government Strategic Reserve and Military Procurement

- Sustainable Aviation Fuel Mandate Compliance Supply

- Voluntary Corporate Sustainable Fuel Procurement Programs

- Spot Market and Commodity Exchange Sales

- Others

- Segmentation By Region

- Middle East

- Africa

- North America

- Asia-Pacific

- Europe

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2036

Key Questions this Study Will Answer

- What is the projected global market valuation for synthetic fuels from natural gas through 2036, segmented by conversion process technology, synthetic fuel product type, feedstock category, facility scale, end-use application, and region, and which product categories and geographic markets are expected to generate the highest incremental revenue and production volume growth across the forecast period?

- How are the European Union ReFuelEU Aviation regulation, the United States Inflation Reduction Act sustainable aviation fuel tax credit, and the International Civil Aviation Organization Carbon Offsetting and Reduction Scheme for International Aviation shaping the development of a premium offtake market for gas-to-liquids synthetic paraffinic kerosene, and what lifecycle carbon intensity integration with carbon capture and storage is required for natural gas-derived synthetic aviation fuel to qualify for the maximum available regulatory incentive tiers in the major regulated aviation fuel markets through the forecast period?

- What is the current commercial and technical readiness of compact and modular gas-to-liquids reactor systems targeting associated and stranded natural gas monetization applications, and how are the capital cost trajectories, product yield structures, operational reliability records, and deployment logistics of leading modular gas-to-liquids technology platforms evolving toward the commercial viability thresholds required for widespread adoption at oil field flare reduction and remote gas monetization project sites across Africa, North America, the Middle East, and Asia-Pacific?

- How are the capital expenditure cost benchmarks, engineering procurement and construction contractor execution capacity, and project financing structures for large-scale gas-to-liquids facilities evolving relative to the historical project cost and schedule overrun experience of first-generation commercial gas-to-liquids projects, and what technology maturation, project delivery model innovation, and risk allocation framework developments are enabling project developers and financing institutions to advance new large-scale gas-to-liquids investments toward final investment decision with greater cost and schedule certainty than was achievable in prior project development cycles?

- What is the competitive positioning of natural gas-derived synthetic fuels relative to electrofuels produced from renewable electricity and green hydrogen, biomass-derived synthetic fuels produced through biomass gasification and Fischer-Tropsch synthesis, and direct renewable energy pathways in the sustainable aviation fuel, marine alternative fuel, and low-carbon road transportation fuel markets, and at what carbon price levels, renewable energy cost trajectories, and regulatory carbon intensity threshold evolutions does the commercial competitiveness of gas-to-liquids synthetic fuels with integrated carbon capture and storage improve or deteriorate relative to these competing low-carbon fuel production pathways?

- Who are the leading gas-to-liquids technology licensors, Fischer-Tropsch catalyst developers, large-scale engineering procurement and construction contractors, integrated energy company project developers, and compact modular gas-to-liquids technology companies currently defining the competitive landscape of the global synthetic fuels from natural gas market, and what are their respective technology platform differentiation strategies, project reference portfolios, carbon capture and storage integration roadmaps, sustainable aviation fuel certification programs, and regional market development priorities for advancing natural gas-derived synthetic fuel production toward the commercially significant scale required to contribute meaningfully to aviation, marine, and industrial sector decarbonization through the forecast horizon?

- Product Definition

- Scope of the Study

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Industry Publications, Gas Processing & Synthetic Fuel OEM Reports, Chemical Engineering Journals & Press Releases

- Government Energy, Environment & Trade Authority Data (IEA, EIA, IHS Markit, IRENA, DOE, EC DG ENER, METI, etc.)

- Synthetic Fuel Production Capacity, Plant Investment & Output Volume Statistics

- Natural Gas Producer, GTL Operator & Synthetic Fuel Offtaker Procurement & Capacity Databases

- Primary Research Design & Execution

- In-depth Interviews with Synthetic Fuel Plant Developers, Gas Processing OEM Executives, Catalyst Suppliers & Downstream Fuel Offtakers

- Surveys with Natural Gas Producers, Petrochemical Companies, Refinery Operators, Shipping Lines & Aviation Fuel Buyers

- Expert Panel Validation

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Bottom-Up & Top-Down Reconciliation

- Natural Gas Feedstock Availability, Plant Capacity Expansion & Synthetic Fuel Demand-Driven Market Sizing Model

- Technology Cost Reduction Learning Curve, Carbon Policy Incentive & Competing Fuel Price Adjustment Framework

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Technology & Innovation Highlights

- Plant Economics & Unit Economics Summary

- Average Plant CAPEX & OPEX Benchmarks

- GTL vs MTG vs ATR-Based Synthetic Fuel Plant Margin & Profitability Analysis

- Fischer-Tropsch (FT), Methanol-to-Fuels & Dimethyl Ether (DME) Revenue Model Summary

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Geographic & Regional Trends

- Risk Assessment Framework

- Geopolitical & Natural Gas Supply Security, Price Volatility & Feedstock Availability Risk

- Carbon Policy & Emissions Regulation Risk: Carbon Pricing, Fuel Standards & Low-Carbon Fuel Mandates

- Technology Readiness, Catalyst Deactivation & Plant Reliability Risk

- Capital Cost Overrun & Project Execution Risk for Large-Scale GTL Plants

- Competing Low-Carbon Fuel Technologies (Green Hydrogen, Electro-Fuels, Biofuels) Substitution Risk

- Downstream Fuel Price Risk: Synthetic Fuel vs Crude Oil-Derived Fuel Price Parity

- Financial / Project Financing, Offtake Contract Bankability & Long-Term Revenue Certainty Risk

- Regulatory Framework & Policy Standards

- Global Synthetic Fuels from Natural Gas Market Economics

- Plant Development & Manufacturing Economics Framework

- Capital Expenditure (CAPEX) Structure

- Operating Expenditure (OPEX) Structure

- Revenue Model & Monetisation Levers (Synthetic Fuel Sales, By-Product Sales, Carbon Credit Revenue, LPG & Naphtha Co-Products)

- Capacity Utilisation & Plant Throughput Economics

- Payback Period & Return on Investment (ROI) Analysis

- Total Cost of Production vs Conventional Petroleum-Derived Fuels, Bio-Based Fuels & Electro-Fuels

- Feedstock & Process Input Cost Analysis

- Natural Gas Feedstock Price Trends & Basis Differentials by Region (USD/MMBtu, 2021–2035)

- Syngas Production: Steam Methane Reforming (SMR), Autothermal Reforming (ATR) & Partial Oxidation (POX) Cost Dynamics

- Fischer-Tropsch (FT) Catalyst (Cobalt, Iron) Procurement, Activation & Replacement Cost Structure

- Methanol Synthesis Catalyst, DME Catalyst & Zeolite MTG/MTO Catalyst Cost Analysis

- Oxygen Supply: Air Separation Unit (ASU) & Cryogenic Oxygen Plant Capital & Operating Cost Structure

- CO₂ Capture, Utilisation & Storage (CCUS) Cost Integration into Synthetic Fuel Plant Economics

- Energy & Utilities Cost Structure in Synthetic Fuel Plant Operations

- Impact of Stranded Gas Monetisation, Flare Gas Recovery & Associated Gas Utilisation on Feedstock Economics

- Product Upgrading, Refining & Distribution Economics

- Hydrocracking, Hydrotreating & Product Fractionation Cost Structure

- Synthetic Fuel Blending, Quality Certification & Product Specification Compliance Cost Economics

- Pipeline, Storage & Terminal Distribution Infrastructure Cost Analysis

- Export Logistics, Shipping & Marine Fuel Bunkering Economics for GTL Products

- Regulatory & Standards Compliance Economics

- Synthetic Fuel Quality, Safety & Environmental Standards Compliance Cost Benchmarks (ASTM, EN, ICAO, ISO, EPA, EU Fuel Quality Directive, etc.)

- Plant Environmental Permitting, EIA & Emissions Compliance Cost Structure

- Carbon Intensity Certification, Low-Carbon Fuel Standard (LCFS) & Renewable Fuel Standard (RFS) Compliance Cost Analysis

- Global Synthetic Fuels from Natural Gas Market Outlook

- Market Size & Forecast by Value (USD Billion, 2021–2036)

- Market Size & Forecast by Volume (Million Tonnes per Annum, 2021–2036)

- Market Size & Forecast by Production Technology

- Gas-to-Liquids (GTL) via Fischer-Tropsch (FT) Synthesis

- Cobalt-Catalysed Low-Temperature Fischer-Tropsch (LTFT)

- Iron-Catalysed High-Temperature Fischer-Tropsch (HTFT)

- Microchannel & Compact FT Reactor Technology

- Methanol Synthesis & Methanol-to-Fuels (MTG / MTO / MTP) Processes

- Conventional High-Pressure Methanol Synthesis (ICI / Lurgi Process)

- Methanol-to-Gasoline (MTG) via ExxonMobil / Haldor Topsøe Technology

- Methanol-to-Olefins (MTO) & Methanol-to-Propylene (MTP) for Synthetic Fuel Precursors

- Dimethyl Ether (DME) Synthesis & DME-to-Fuels Conversion

- Direct DME Synthesis (Single-Step) from Syngas

- Two-Step DME Production via Methanol Dehydration

- Synthetic Natural Gas (SNG) / Substitute Natural Gas via Methanation

- Power-to-X with Natural Gas Co-Feeding (Hybrid e-Fuels + GTL)

- Others (Gas-to-Chemicals with Fuel Co-Production, Ammonia-to-Fuels, Gas-to-Wax)

- Gas-to-Liquids (GTL) via Fischer-Tropsch (FT) Synthesis

- Market Size & Forecast by Syngas Production Route

- Steam Methane Reforming (SMR)

- Autothermal Reforming (ATR)

- Partial Oxidation (POX)

- Combined Reforming (SMR + ATR)

- Dry Reforming of Methane (DRM) with CO₂ Co-Feed

- Plasma Reforming & Novel Non-Thermal Syngas Production

- Market Size & Forecast by Fuel Product Type

- Synthetic Diesel / Gas-to-Liquids Diesel (GTL Diesel)

- Synthetic Aviation Fuel / Sustainable Aviation Fuel (SAF) from Natural Gas

- Synthetic Naphtha & Petrochemical Feedstocks

- Synthetic Gasoline (via MTG)

- Methanol (as Fuel & Fuel Blendstock)

- Dimethyl Ether (DME)

- Liquefied Petroleum Gas (LPG) & Light Hydrocarbons

- Synthetic Natural Gas (SNG) / Substitute Natural Gas

- Others (Synthetic Waxes, Lubricants, Specialty Chemicals)

- Market Size & Forecast by Plant Scale

- Small-Scale & Modular GTL Plants (Below 1,000 bpd)

- Mid-Scale GTL Plants (1,000–20,000 bpd)

- Large-Scale GTL Plants (20,000–100,000 bpd)

- Mega-Scale GTL Plants (Above 100,000 bpd)

- Market Size & Forecast by Feedstock Source

- Pipeline Natural Gas (Conventional & Unconventional)

- Stranded & Remote Natural Gas

- Associated & Flare Gas Monetisation

- Liquefied Natural Gas (LNG) Regasification Feed

- Coal Bed Methane (CBM) & Tight Gas

- Biogas & Biomethane (Bio-GTL)

- Others (Landfill Gas, Wastewater Biogas, CO₂ + Renewable H₂ Co-Feed)

- Market Size & Forecast by Application

- Transportation Fuels (Road)

- Synthetic Diesel for Heavy-Duty Trucks & Commercial Vehicles

- Synthetic Gasoline & Blendstocks for Passenger Vehicles

- Aviation Fuels (SAF)

- Drop-In Synthetic SAF for Commercial Aviation (ASTM D7566 Compliant)

- Military & Defence Aviation Synthetic Fuel Supply

- Marine & Shipping Fuels

- GTL-Based IMO-Compliant Marine Diesel & Bunker Fuel

- Methanol & DME as Alternative Marine Fuels

- Power Generation

- Gas Turbine, Reciprocating Engine & Combined Heat & Power (CHP) Synthetic Fuel Supply

- Off-Grid & Remote Power Generation Using Modular GTL Fuel

- Industrial & Petrochemical Feedstocks

- Synthetic Naphtha for Steam Cracking & Olefin Production

- Methanol as Chemical Feedstock (Formaldehyde, Acetic Acid, Olefins)

- Cooking, Heating & LPG Substitution

- Others (Lubricants, Specialty Chemicals, Wax & Paraffin Applications)

- Transportation Fuels (Road)

- Market Size & Forecast by End-Use Sector

- Oil & Gas Companies & Gas Monetisation Ventures

- Global Integrated Oil & Gas Majors with GTL Operations (Shell, Sasol, ExxonMobil, Qatar Petroleum / QatarEnergy, etc.)

- National Oil Companies (NOCs) & State-Owned Gas Monetisation Entities

- Independent Gas Producers & Stranded Gas Monetisation Ventures

- Aviation & Aerospace Sector

- Commercial Airlines & SAF Procurement Programmes (IATA Member Airlines)

- Airport Authorities & Aviation Fuel Infrastructure Operators

- Shipping & Maritime Industry

- Global Container Shipping Lines, Bulk Carrier & Tanker Operators

- Marine Fuel Bunkering & LNG/Methanol Bunkering Terminal Operators

- Transportation & Logistics

- Truck Fleet Operators, Logistics Providers & Road Freight Companies

- Government & Municipal Fleet Operators

- Industrial & Chemical Sector

- Petrochemical Companies, Refinery Operators & Specialty Chemical Manufacturers

- Industrial Gas & Fertiliser Producers Using Methanol & Syngas Co-Products

- Power Generation Utilities & Off-Grid Energy Operators

- Government & Public Sector Energy Agencies

- Others (Agriculture, Mining, Construction, Remote Community Energy Supply)

- Oil & Gas Companies & Gas Monetisation Ventures

- Market Size & Forecast by Sales Channel

- Direct Long-Term Offtake Agreements & Supply Contracts with Industrial Buyers

- Spot Market & Commodity Trading via Fuel Exchanges & Trading Platforms

- Retail Fuel Distribution & Blending Networks

- Government Tender, Strategic Reserve & Public Procurement Programmes

- Joint Venture & Consortium-Based Production & Marketing Agreements

- Asia-Pacific Synthetic Fuels from Natural Gas Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Volume (Million Tonnes per Annum)

- By Production Technology

- By Syngas Production Route

- By Fuel Product Type

- By Plant Scale

- By Feedstock Source

- By Application

- By End-Use Sector

- By Sales Channel

- Key Demand Drivers (APAC-Specific)

- Competitive Landscape (APAC)

- Europe Synthetic Fuels from Natural Gas Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Volume (Million Tonnes per Annum)

- By Production Technology

- By Syngas Production Route

- By Fuel Product Type

- By Plant Scale

- By Feedstock Source

- By Application

- By End-Use Sector

- By Sales Channel

- Key Demand Drivers (Europe-Specific)

- Competitive Landscape (Europe)

- North America Synthetic Fuels from Natural Gas Market Outlook

- Market Overview & Strategic Importance

- Market Size & Forecast

- By Value (2020–2035)

- By Volume (Million Tonnes per Annum)

- By Production Technology

- By Syngas Production Route

- By Fuel Product Type

- By Plant Scale

- By Feedstock Source

- By Application

- By End-Use Sector

- By Sales Channel

- Key Demand Drivers (North America-Specific)

- Competitive Landscape (North America)

- Latin America Synthetic Fuels from Natural Gas Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Volume (Million Tonnes per Annum)

- By Production Technology

- By Syngas Production Route

- By Fuel Product Type

- By Plant Scale

- By Feedstock Source

- By Application

- By End-Use Sector

- By Sales Channel

- Key Demand Drivers (LATAM-Specific)

- Competitive Landscape (LATAM)

- Middle East & Africa Synthetic Fuels from Natural Gas Market Outlook

- Market Size & Forecast

- By Value (2020–2035)

- By Volume (Million Tonnes per Annum)

- By Production Technology

- By Syngas Production Route

- By Fuel Product Type

- By Plant Scale

- By Feedstock Source

- By Application

- By End-Use Sector

- By Sales Channel

- Key Demand Drivers (MEA-Specific)

- Competitive Landscape (MEA)

- Country-Wise Synthetic Fuels from Natural Gas Market Outlook

- Market Size & Forecast by Country

- By Value

- By Volume (Million Tonnes per Annum)

- By Production Technology

- By Syngas Production Route

- By Fuel Product Type

- By Plant Scale

- By Feedstock Source

- By Application

- By End-Use Sector

- By Sales Channel

- Market Size & Forecast by Country

- Market Size & Forecast

- Market Size & Forecast

- Market Size & Forecast

- Market Size & Forecast

- Plant Development & Manufacturing Economics Framework

Countries Covered: Qatar, South Africa, United States, Canada, Russia, Australia, China, Saudi Arabia, United Arab Emirates, Nigeria, Norway, Netherlands, Germany, United Kingdom, Japan, South Korea, India, Indonesia, Brazil, Kazakhstan

- Technology Landscape & Innovation Analysis

- Synthetic Fuel from Natural Gas Technology Maturity Assessment

- Emerging & Disruptive Technologies in Gas-to-Liquids & Gas-to-Fuels Conversion

- Next-Generation Fischer-Tropsch Catalyst Development: High-Activity Cobalt, Bimetallic & Nanostructured Catalysts for Improved Selectivity & Longevity

- Modular & Compact GTL Technology: Microchannel Reactors, 3D-Printed Process Equipment & Containerised Small-Scale GTL Systems

- Autothermal Reforming (ATR) with Integrated CO₂ Capture: Low-Carbon Blue Synthetic Fuel Production Pathway

- Methanol & DME Technology Advances: Low-Temperature Synthesis, Electrocatalytic CO₂ Co-Conversion & Novel Reactor Concepts

- Hybrid Power-to-X + GTL: Green Hydrogen Co-Feed with Natural Gas Syngas for Near-Zero Carbon Synthetic Fuel Production

- AI-Driven Process Optimisation, Digital Twin & Predictive Catalyst Management for GTL Plant Operations

- Technology Readiness & Commercialisation Matrix – Key Synthetic Fuel from Natural Gas Technologies

- Patent Landscape Analysis

- R&D Investment Benchmarking

- Value Chain & Supply Chain Analysis

- Synthetic Fuels from Natural Gas Value Chain Mapping

- Supply Chain Concentration & Dependency Analysis

- Key Supplier Mapping by Component & Technology Programme

- Natural Gas Feedstock Producer & Pipeline / LNG Infrastructure Supplier Mapping

- Syngas Reformer, Reactor & Pressure Vessel Fabricator Mapping

- Fischer-Tropsch, Methanol & DME Catalyst Manufacturer Mapping

- Air Separation Unit (ASU), Cryogenic Equipment & Gas Processing OEM Mapping

- Product Upgrading, Hydrocracker & Fractionation Unit Equipment Supplier Mapping

- Supplier Risk Heat Map

- Make vs Buy Strategy Trends Among Synthetic Fuel Plant Developers & Gas Processing Companies

- Pricing Analysis

- Synthetic Fuel from Natural Gas Pricing Dynamics & Mechanisms

- Pricing by Production Technology, Fuel Product Type, Plant Scale & Feedstock Source

- Total Cost of Production (TCOP) Analysis – Including Feedstock, CAPEX Amortisation, OPEX, Catalyst, Logistics & Carbon Compliance Costs (USD/barrel & USD/tonne)

- GTL vs MTG vs DME vs SNG Pricing Trends & Benchmarks by Region

- Synthetic Fuel vs Petroleum-Derived Fuel vs Biofuel vs Electro-Fuel Pricing Parity & Value Proposition

- Sustainability & Environmental Stewardship

- Environmental & Sustainability Landscape in Synthetic Fuel from Natural Gas Production

- Lifecycle GHG Emissions & Carbon Intensity Benchmarking: GTL vs Petroleum Diesel vs Biofuel vs Electro-Fuel (gCO₂e/MJ)

- Blue Synthetic Fuel Pathway: CCUS Integration, Carbon Intensity Reduction & Low-Carbon Fuel Standard Eligibility

- Methane Slip, Flaring Elimination & Associated Gas Monetisation’s Contribution to Upstream Emission Reduction

- Water Consumption, Effluent Management & Air Quality Impact Assessment for GTL Plant Operations

- ESG Reporting & Lifecycle Assessment (LCA) in Synthetic Fuel from Natural Gas Plant Operations

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level: Global Energy Majors & National Oil Companies vs Technology Licensors & Modular GTL Startups

- Top 5 Synthetic Fuel from Natural Gas Companies Market Revenue & Production Capacity Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis by Production Technology, Fuel Product Type & Region

- Competitive Intensity Map by Segment & Region

- Player Classification

- Tier-1 Global Integrated Gas-to-Liquids & Synthetic Fuel Producers (Shell GTL, Sasol, QatarEnergy / Pearl GTL, ExxonMobil, etc.)

- Tier-2 Technology Licensors, Process Engineering Firms & Catalyst Suppliers (Haldor Topsøe / Topsoe, Johnson Matthey, Velocys, INFRA Technology, CompactGTL, etc.)

- Emerging Modular GTL & Small-Scale Synthetic Fuel Technology Developers & Stranded Gas Monetisation Startups

- Emerging & Disruptive Players

- Competitive Analysis Frameworks

- Market Share Analysis by Production Technology, Fuel Product Type & Geography

- R&D Intensity & Catalyst & Process Technology Portfolio Benchmarking

- Technology Licensing Agreement Portfolio, Offtake Contract & Long-Term Supply Agreement Comparison

- Geographic Revenue Exposure & Plant Operating Footprint Comparison

- Company Profiles

- Company Overview, HQ & Organisational Structure

- Synthetic Fuel Production Technology, Process Licence & Fuel Product Portfolio

- Revenue Breakdown

- Key GTL Plant Operations, Technology Licensing Programmes & Offtake Agreements

- Manufacturing Footprint, Plant Locations & Key Facilities

- Recent Developments (M&A, Partnerships, New Projects, Technology Qualifications, Financial Results)

- SWOT Analysis

- Strategic Focus: Production Cost Reduction, CCUS Integration for Blue Synthetic Fuels, Modular GTL Commercialisation & SAF Market Expansion

- Strategic Output

- Market Opportunity Matrix

- High-Value Opportunity Quadrant Analysis

- Addressable Market by Production Technology, Fuel Product Type & Region

- Time-to-Revenue Assessment by Opportunity

- White Space Opportunity Analysis

- Underserved Feedstock Source, Fuel Product Category & Application Segment Gaps

- Geographic Markets with Stranded Gas Resources & Low Synthetic Fuel Penetration

- Technology, Plant Scale & Carbon Intensity Gaps with High Commercialisation Potential

- Customer Segment Unmet Needs

- Strategic Recommendations

- Product Portfolio & Fuel Product Innovation Strategy

- Technology Platform, Catalyst Development & Process Efficiency Strategy

- Plant Development, Capacity Expansion & Modular GTL Scale-Up Strategy

- Offtake Agreement, End-Use Market Penetration & Channel Growth Strategy

- Pricing, Carbon Revenue Optimisation & Commercial Strategy

- Sustainability, CCUS Integration & Low-Carbon Fuel Standard Compliance Strategy

- Feedstock Supply Chain, Stranded Gas Monetisation & Sourcing Strategy

- Partnership, M&A & Technology Licensing Expansion Strategy

- Regional Growth & Export Market Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-Term (2025–2028)

- Mid-Term (2029–2032)

- Long-Term (2033–2036)

- Market Opportunity Matrix

- Market Structure & Concentration