Market Definition

Textile chemicals are specialized organic and inorganic compounds applied at various stages of the fabric manufacturing process, from fiber pre-treatment and dyeing to final finishing, to impart specific aesthetic, functional, and performance attributes. These substances act as the secret sauce of the industry, transforming raw, abrasive fibers into soft, vibrant, and durable materials. By manipulating the physical and chemical properties of a substrate, these chemicals enable essential characteristics such as moisture wicking, flame retardancy, UV protection, and wrinkle resistance, while also ensuring that colors remain vibrant and resistant to fading.

Market Insights

The global textile chemicals market is currently navigating a period of significant structural transformation, driven by a convergence of regulatory pressure and shifting consumer values. As of 2026, the industry is moving away from its historically heavy environmental footprint toward a model defined by clean chemistry. This shift is not merely a branding exercise but a fundamental realignment of the supply chain, as manufacturers increasingly adopt closed-loop systems and bio-synthetic alternatives to traditional petroleum-based processing agents.

Sustainability has transitioned from a niche preference to a mandatory operational standard. Industry players are aggressively phasing out hazardous substances like perfluorinated compounds (PFCs) and certain phthalates in favor of biodegradable surfactants and plant-derived finishing agents. This green pivot is heavily reinforced by global certifications such as ZDHC (Zero Discharge of Hazardous Chemicals), which are now essential for any chemical provider looking to maintain contracts with major international apparel brands.

One of the most impactful technological shifts is the rapid adoption of digital textile printing and low-liquor ratio dyeing machines. These innovations significantly reduce the volume of auxiliary chemicals and water required per kilogram of fabric. Consequently, the demand for high-performance, specialized inks and pre-treatment chemicals is surging, while traditional bulk commodity chemicals are seeing a relative stagnation in market share.

While the fashion apparel segment remains the largest consumer of textile chemicals, the most resilient growth is occurring in the technical textiles sector. Chemicals engineered for smart functionalities, such as antimicrobial properties for healthcare, flame retardancy for construction, and high-tenacity coatings for the automotive industry, are commanding higher margins. This diversification provides a critical buffer for chemical manufacturers against the volatility of the fast-fashion retail cycle.

The Asia-Pacific region remains the primary engine of the market, but the China Plus One strategy is actively reshaping sourcing patterns. While China retains its lead in sophisticated chemical manufacturing and infrastructure, there is a marked increase in chemical consumption and production capacity in India, Vietnam, and Bangladesh. This geographic broadening is forcing global chemical giants to establish more localized R&D and technical support centers to better serve these emerging textile clusters.

Key Drivers

The global textile chemicals market in 2026 is primarily driven by the surging demand for technical textiles across the automotive, healthcare, and construction industries. As these sectors require fabrics with specialized functional properties, such as flame retardancy, antimicrobial resistance, and high-performance durability, chemical manufacturers are shifting away from commodity products toward high-value, R&D-intensive specialty formulations. This growth is further accelerated by the rapid adoption of digital textile printing and green chemistry. With global brands facing pressure to reduce their environmental footprint, there is a massive transition toward bio-based enzymes and water-borne finishes that significantly lower water and energy consumption compared to traditional dyeing methods, making clean chemistry a core competitive advantage.

Key Challenges

The industry faces significant hurdles, most notably the increasingly stringent global regulatory landscape and the persistent volatility of raw material prices. Regulations such as the EU’s Ecodesign for Sustainable Products Regulation (ESPR) and strict Zero Liquid Discharge (ZLD) norms in manufacturing hubs like India and China have imposed heavy compliance costs and required massive investments in advanced effluent treatment. These financial pressures are compounded by the unpredictable pricing of petrochemical feedstocks, which remain sensitive to ongoing geopolitical tensions. This combination of high operational costs and a global overcapacity in basic chemicals is squeezing profit margins, forcing many smaller players to consolidate or exit the market entirely in favor of more resilient, specialty-focused companies.

Simultaneously, the industry is facing a massive hurdle in the form of tightening environmental regulations and the PFAS-free transition. Global regulators, particularly in the EU and North America, are imposing strict mandates on the chemical composition of tires to reduce microplastic shedding (tire-wear particles) and eliminate forever chemicals from the manufacturing process. This has triggered an expensive R&D race to find viable, high-performance alternatives that do not compromise the tire’s safety or longevity. Additionally, the move toward Extended Producer Responsibility (EPR) laws requires manufacturers to take greater financial and operational ownership of tire recycling and end-of-life disposal. For many players, the high CAPEX required to overhaul legacy production lines into sustainable, circular-economy-ready facilities remains a formidable barrier to maintaining competitiveness.

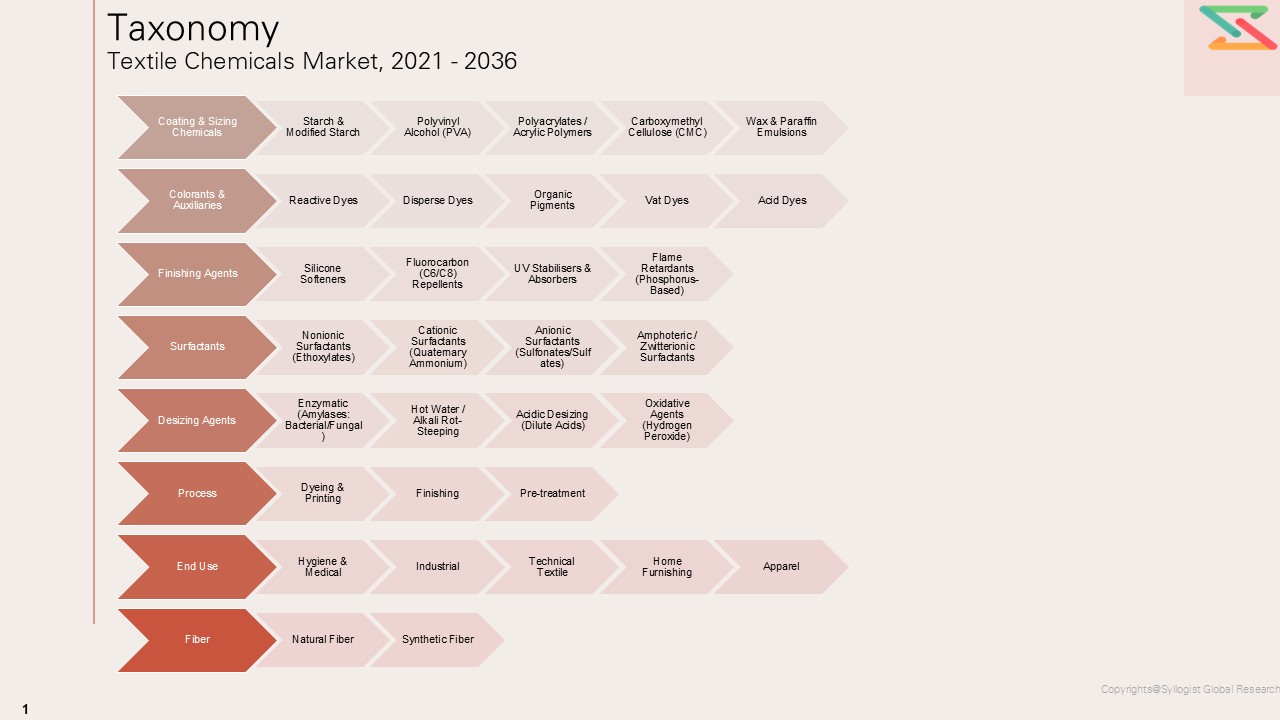

Market Segmentation

- Segmentation By Type

- Coating & sizing chemicals

- Starch & modified starch

- Polyvinyl alcohol (PVA)

- Polyacrylates / acrylic polymers

- Carboxymethyl cellulose (CMC)

- Wax & paraffin emulsions

- Colorants & Auxiliaries

- Reactive dyes

- Disperse dyes

- Acid dyes

- Vat dyes

- Organic Pigments

- Finishing Agents

- Silicone Softeners

- Fluorocarbon (C6/C8) Repellents

- Flame Retardants (Phosphorus-Based)

- Flame Retardants (Phosphorus-Based)

- UV Stabilisers & Absorbers

- Surfactants

- Nonionic Surfactants (Ethoxylates)

- Anionic Surfactants (Sulfonates/Sulfates)

- Cationic Surfactants (Quaternary Ammonium)

- Amphoteric / Zwitterionic Surfactants

- Desizing Agents

- Enzymatic (Amylases: Bacterial/Fungal)

- Oxidative Agents (Hydrogen Peroxide)

- Acidic Desizing (Dilute Acids)

- Hot Water / Alkali Rot-Steeping

- Segmentation By Process

- Pre-treatment

- Finishing

- Dyeing & Printing

- Segmentation By End Use

- Apparel

- Home Furnishing

- Industrial

- Technical Textile

- Hygiene & Medical

- Segmentation By Fiber

- Synthetic Fiber

- Natural Fiber

- Coating & sizing chemicals

All market revenues are presented in USD and volume in tons

Historical Year: 2021–2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027–2036

Key Questions this Study Will Answer

- What are the critical market metrics and forward-looking projections for the Global Textile Chemicals Market, including revenue size, volume consumption, and average selling prices, with performance segmentation across Product Type (Coating & Sizing Chemicals, Colorants & Dyeing Auxiliaries, Finishing Agents, Surfactants, Desizing Agents, Bleaching Agents, Specialty Textile Chemicals), Fiber Type (Cotton, Polyester, Nylon, Wool, Viscose, Blends, Others), Process Stage (Pre-treatment, Dyeing, Printing, Finishing), Application (Apparel, Home Textiles, Technical Textiles, Industrial Textiles), Functionality (Softening, Water Repellency, Flame Retardancy, Anti-microbial, Wrinkle Resistance, UV Protection, Anti-static), Form (Liquid, Powder, Paste), and End-Use Industry (Fashion & Apparel, Home Furnishing, Automotive Textiles, Medical Textiles, Protective Textiles, Sportswear, Others)?

- How do supply–demand fundamentals vary across key regions and major textile manufacturing hubs, and what role do textile production volumes, apparel exports, synthetic fiber consumption, fast-fashion demand, technical textile expansion, sustainability mandates, wastewater discharge norms, and restricted substance regulations play in shaping regional competitiveness, alongside local manufacturing capability in formulation chemistry, dye-fixation technologies, specialty finishing, enzyme processing, and downstream distribution networks, as well as procurement structures across large textile mills, dye houses, garment exporters, contract processors, distributors, and specialty chemical traders?

- In what ways are raw material and energy price volatility and lead-time constraints for petrochemical intermediates, surfactants, solvents, caustic soda, hydrogen peroxide, dyestuff intermediates, silicone-based agents, fluorine-free repellents, resins, enzymes, and specialty additives influencing production costs, pricing strategies, supplier margins, delivery schedules, and profitability, especially for high-performance finishing chemicals, eco-friendly processing agents, low-VOC formulations, ZDHC-compliant products, and sustainable bio-based textile chemical solutions?

- Who are the leading global and regional textile chemical manufacturers, auxiliary suppliers, dye and finishing chemical companies, and distribution partners, and how do they benchmark across product performance, shade consistency, wash fastness, chemical efficiency, compatibility with multiple fibers, sustainability profile, regulatory compliance, price competitiveness, brand strength, and portfolio breadth, across standalone chemical supply versus value-added offerings such as technical application support, lab-to-bulk scale-up assistance, process optimization, on-site troubleshooting, wastewater reduction solutions, and compliance advisory services?

- What strategic insights emerge from primary discussions with textile mills, dye houses, apparel manufacturers, chemical formulators, distributors, exporters, and technical textile producers regarding demand shifts toward sustainable processing chemicals, water-saving dyeing auxiliaries, fluorine-free repellents, bio-based softeners, digital printing chemicals, multifunctional finishes, and compliance-ready formulations, along with key purchase criteria such as price competitiveness, performance consistency, regulatory acceptance, ease of processing, fabric compatibility, environmental footprint, supply reliability, and technical service support?

- Executive Summary

- Key Findings & Headline Numbers

- Market Snapshot by Segment & Region

- Top Trends Shaping the Next 5 Years

- Strategic Recommendations for Stakeholders

- Research Methodology & Scope

- Report Scope, Definitions & Inclusions & Exclusions

- Primary & Secondary Research Approach

- Market Estimation & Forecasting Methodology

- Data Validation & Triangulation Process

- Assumptions, Limitations & Currency Basis

- Industry Overview & Value Chain Analysis

- Introduction To Textile Chemicals — Types & Functions

- End-To-End Value Chain: Raw Materials → Textile Mill → Brand → Consumer

- Textile Manufacturing Process & Chemical Touchpoints

- Key Raw Material Inputs & Supply Dependencies

- Distribution Channels & Go-To-Market Models

- Market Dynamics

- Market Dynamics (Drivers, Restraints, Opportunities, Challenges, Porter’s Five Forces Analysis, PESTLE Analysis)

- Market Trends & Developments

- Risk Assessment Framework

- Political / Geopolitical Risk

- Feedstock Supply Risk

- Environmental and Regulatory Risk

- Financial / Market Risk

- Regulatory Framework & Standards

- Global Regulatory Overview: REACH, ZDHC MRSL, Bluesign, OEKO-TEX

- PFAS & Fluorochemical Phaseout: EU & US Timelines

- Effluent & Wastewater Discharge Norms by Region

- Sustainability Certifications & Their Market Impact

- Green Chemistry, Bio-Based Alternatives & Circular Economy

- ESG Disclosure Requirements for Chemical Suppliers

- Technology Trends & Innovation Landscape

- Nanotechnology Applications in Textile Finishing

- Digital & Inkjet Printing Chemical Systems

- Smart & Functional Textiles: Conductive, Responsive, Self-Cleaning

- Bio-Enzymatic Processes Replacing Conventional Chemicals

- AI & Process Optimisation in Chemical Application

- Patent Landscape & R&D Investment Analysis

- Supply Chain & Raw Material Analysis

- Key Petrochemical & Bio-Based Feedstock Mapping

- Price Trend Analysis: Crude Oil, Ethylene, Starch, Silicone

- Supply Chain Risk Assessment: Concentration, Disruption

- China+1 And Nearshoring Impact on Chemical Supply

- Logistics, Packaging & Distribution Cost Structure

- Global Textile Chemicals Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume

- Market Size & Forecast by Type

- Coating & Sizing Chemicals

- Starch & Modified Starch

- Polyvinyl Alcohol (PVA)

- Polyacrylates / Acrylic Polymers

- Carboxymethyl Cellulose (CMC)

- Wax & Paraffin Emulsions

- Colorants & Auxiliaries

- Reactive Dyes

- Disperse Dyes

- Acid Dyes

- Vat Dyes

- Organic Pigments

- Finishing Agents

- Silicone Softeners

- Fluorocarbon (C6/C8) Repellents

- Flame Retardants (Phosphorus-Based)

- UV Stabilisers & Absorbers

- Surfactants

- Nonionic Surfactants (Ethoxylates)

- Anionic Surfactants (Sulfonates/Sulfates)

- Cationic Surfactants (Quaternary Ammonium)

- Amphoteric / Zwitterionic Surfactants

- Desizing Agents

- Enzymatic (Amylases: Bacterial/Fungal)

- Oxidative Agents (Hydrogen Peroxide)

- Acidic Desizing (Dilute Acids)

- Hot Water / Alkali Rot-Steeping

- Coating & Sizing Chemicals

- Market Size & Forecast by Process

- Pre-treatment

- Finishing

- Dyeing & Printing

- Market Size & Forecast by End Use

- Apparel

- Home Furnishing

- Industrial

- Technical Textile

- Hygiene & Medical

- Market Size & Forecast by Fiber

- Synthetic Fiber

- Natural Fiber

- Asia-Pacific Passenger Car Tires Market Outlook

- Market Size & Forecast

- By Value

- By Volume

- By Type

- By Process

- By End Use

- By Fiber

- Market Size & Forecast

- Europe Passenger Car Tires Market Outlook

- Market Size & Forecast

- By Value

- By Volume

- By Type

- By Process

- By End Use

- By Fiber

- Market Size & Forecast

- North America Passenger Car Tires Market Outlook

- Market Size & Forecast

- By Value

- By Volume

- By Type

- By Process

- By End Use

- By Fiber

- Market Size & Forecast

- Latin America Passenger Car Tires Market Outlook

- Market Size & Forecast

- By Value

- By Volume

- By Type

- By Process

- By End Use

- By Fiber

- Market Size & Forecast

- Middle East & Africa Passenger Car Tires Market Outlook

- Market Size & Forecast

- By Value

- By Volume

- By Type

- By Process

- By End Use

- By Fiber

- Market Size & Forecast

- Country Wise* Passenger Car Tires Market Outlook

- Market Size & Forecast

- By Value

- By Volume

- By Type

- By Process

- By End Use

- By Fiber

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, China, Germany, United Kingdom, Japan, Australia, France, The Netherlands, Singapore, India, Canada, Brazil, South Korea, UAE, Sweden, Ireland, Malaysia, Indonesia, Italy, Poland, Mexico, South Africa, Saudi Arabia, Finland, Thailand, Chile, Norway, Kenya, Vietnam, Qatar

- Trade Flow Analysis

- Major Tire Exporting Countries

- Major Tire Importing Countries

- Tariff & Trade Barrier Analysis

- Pricing Analysis

- Historical Price Trends by Product Segment

- Price Driver and Cost Structure Analysis

- Sustainability Premium and Green Chemistry Pricing

- Raw Material Analysis

- Investment Landscape & Strategic Opportunities

- White Space & Unmet Demand Analysis

- High-Growth Niches: Bio-Based, Functional, Digital Print Chemicals

- Greenfield Vs Brownfield Investment Considerations

- Venture & PE Activity in Sustainable Textile Chemistry

- Strategic Partnerships & Licensing Models

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented Vs Consolidated)

- Top 5 Players Market Share

- HHI (Herfindahl–Hirschman Index) Concentration Analysis

- Competitive Intensity Map

- Player Classification

- Market Leaders

- Strong Challengers

- Specialist / Niche Players

- Emerging Players

- Regional Players

- Competitive Analysis Frameworks

- Market Share Analysis

- Company Profile

- Company Overview & HQ

- Products & Solutions Portfolio

- Revenue & Cooling Segment Revenue

- Geographic Presence

- Recent Developments (M&A, Launches, Partnerships)

- SWOT Analysis

- Strategic Focus Areas

- Competitive Positioning Map

- Market Structure & Concentration

- Strategic Recommendations

- Portfolio & Product Strategy

- Innovation & Sustainability

- Commercial & Supply Chain

- Strategic Priority Matrix & Roadmap

- Near-term (2025–2028)

- Mid-term (2029–2032)

- Long-term (2023–2036)