Market Definition

The Vinyl Acetate Monomer (VAM) market comprises a critical segment of the global petrochemical and acetyl value chain, encompassing production, distribution, and downstream integration of VAM into performance polymers and specialty chemical derivatives. VAM is primarily produced through the reaction of ethylene and acetic acid in the presence of oxygen, serving as a foundational intermediate for polyvinyl acetate (PVAc), polyvinyl alcohol (PVOH), ethylene vinyl acetate (EVA), and vinyl acetate ethylene (VAE) emulsions.

VAM plays a central role in enabling high-performance adhesives, coatings, construction chemicals, packaging films, solar encapsulants, textile finishes, and industrial binders. It supports key industries including construction, packaging, automotive, textiles, paper & pulp, consumer goods, and renewable energy.

Over the past two years, the global VAM industry has undergone structural adjustments driven by feedstock volatility (ethylene and acetic acid), supply-demand imbalances in Asia, capacity rationalization in mature markets, and rising demand for specialty emulsions and EVA used in solar panel encapsulation. The sector has also been influenced by energy cost fluctuations, trade realignments, and environmental compliance pressures impacting plant operations and expansion decisions.

Market Insights

Global demand for VAM has been shaped by construction activity, packaging growth, solar module installations, and expanding adhesive consumption. During 2021–2022, tight supply conditions and feedstock cost inflation led to pricing volatility across major regions. Asia-Pacific remained the dominant production and consumption hub, supported by large downstream derivative capacity.

Between 2023 and 2025, the market experienced normalization in operating rates as new capacities came online and supply chains stabilized. However, demand from EVA (solar encapsulants), VAE emulsions for construction, and water-based adhesive systems remained structurally strong. The increasing preference for low-VOC, water-based formulations further strengthened VAM’s strategic position in coatings and adhesives.

Sustainability considerations are increasingly shaping the VAM ecosystem. Manufacturers are investing in energy-efficient reactor technologies, catalyst improvements, emission control systems, and carbon footprint optimization. Integration into acetic acid and ethylene supply chains remains a key competitive differentiator, while selective investments in downstream derivative integration enhance margin stability.

Industry projections indicate that the global VAM market will expand at a steady CAGR between 2027 and 2031, supported by infrastructure development in Asia-Pacific, growth in renewable energy installations, packaging expansion, and rising industrial adhesive consumption. Emerging markets in Southeast Asia, the Middle East, and Latin America are witnessing increasing import demand and downstream capacity additions.

Regulatory frameworks, particularly environmental emission norms, VOC regulations, and carbon reporting standards, are influencing plant modernization and compliance investments. At the same time, the industry remains sensitive to feedstock price fluctuations, energy costs, high capital intensity, and geopolitical trade dynamics.

Market Dynamics: Drivers

Construction growth, infrastructure expansion, and urbanization remain primary drivers of VAM demand, particularly through VAE emulsions and adhesive systems. The rapid growth of solar energy installations has significantly increased EVA consumption, creating incremental pull-through demand for VAM.

Packaging demand growth, especially flexible packaging and paperboard coatings, is supporting PVAc and PVOH usage. Additionally, the shift toward environmentally compliant, water-based adhesives and coatings is reinforcing structural demand. Automotive lightweighting and industrial binder applications further contribute to steady consumption growth.

Regional industrialization, expansion of downstream polymer capacity, and integration strategies by large chemical producers are strengthening long-term demand fundamentals.

Market Dynamics: Challenges

The VAM industry faces structural challenges including feedstock dependency on ethylene and acetic acid, both of which are subject to crude oil and natural gas price volatility. Margin compression risks arise during periods of feedstock inflation or derivative oversupply.

Environmental compliance costs, energy intensity, and emission control investments increase capital and operational expenditures. Capacity additions in Asia can create periodic oversupply cycles, exerting downward pressure on pricing.

Trade barriers, anti-dumping duties, and logistical disruptions also impact regional arbitrage dynamics. Additionally, competition from alternative chemistries or substitute adhesive technologies can influence demand in select applications.

Maintaining integration, operational efficiency, and derivative diversification remains essential to preserving profitability across market cycles.

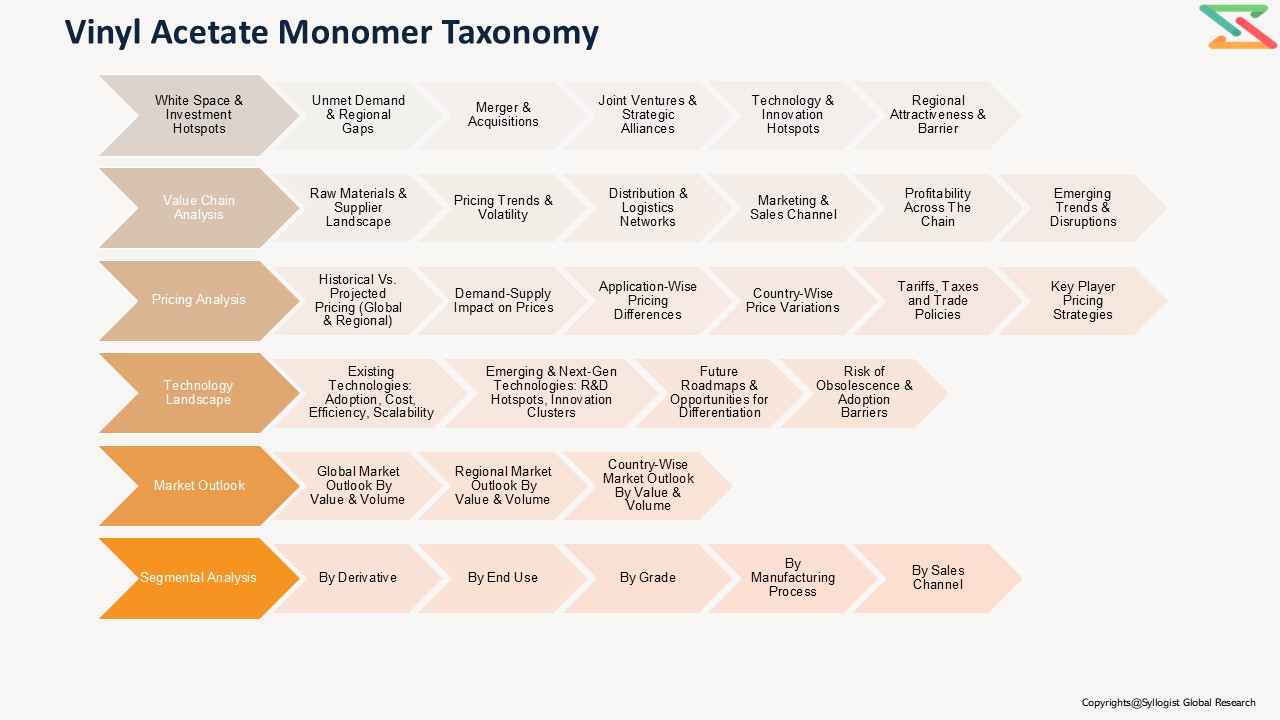

Market Segmentation

- By Derivative

- Polyvinyl Acetate

- Polyvinyl Alcohol

- Ethylene Vinyl Acetate

- Ethylene Vinyl Alcohol

- VAE Emulsions (Vinyl Acetate Ethylene Emulsions)

- Other Derivatives

- Vinyl Acetate Copolymers

- Specialty Polymers

- Acrylic Modifiers

- By End Use

- Construction

- Adhesives

- Sealants

- Cement Modifiers

- Insulation

- Packaging

- Flexible Packaging

- Barrier Films

- Carton Adhesives

- Automotive

- Interior Foams (EVA) Adhesives

- Adhesives

- Wire & Cable Insulation

- Textiles

- Sizing Agents

- Coatings

- Renewable Energy

- Solar Module Encapsulants (EVA)

- Consumer Goods

- Footwear

- Furniture Adhesives

- By Grade / Purity

- Industrial Grade

- High Purity Grade

- By Manufacturing Process

- Ethylene-Based Route

- Acetylene-Based Route

- By Sales Channel

- Direct Sales (Long-Term Contracts)

- Spot Market

- Distributors

- By Integration Level

- Integrated Producers (Ethylene + Acetic Acid + VAM + Derivatives)

- Merchant Producers

- By Market Structure

- Captive

- Merchant

- By Region

- Asia-Pacific

- Europe

- North America

- Latin America

- Middle East & Africa

- Construction

All market revenues are presented in USD, with production volumes expressed in metric tons and operating rates expressed as percentage capacity utilization.

Historical Year: 2021–2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027–2031

Key Questions this Study Will Answer

- What are the key market statistics and forecasts (market size by value and volume, derivative split, regional growth trends) for the Global VAM Market?

- What are the region-wise supply-demand balances, trade flows, and feedstock linkages?

- How are feedstock volatility, energy pricing, and regulatory mandates shaping profitability?

- Who are the leading producers, and how do they benchmark across integration depth, cost position, derivative portfolio, and regional footprint?

- What insights emerge from interviews with producers, derivative manufacturers, traders, and downstream end-users conducted during the market assessment?

- Executive Summary

- Market Snapshot (Value & Volume)

- Key Insights & Strategic Takeaways

- Demand Outlook by Region & Application

- Supply & Capacity Overview

- Pricing & Margin Highlights

- Key Regulatory & Risk Themes

- Introduction & Scope

- Study Objectives

- Product Definition & Scope Coverage

- Market Segmentation Framework

- Geographic Coverage

- Base Year & Forecast Period

- Assumptions & Limitations

- Research Methodology

- Research Approach (Primary + Secondary + Modelling)

- Market Sizing Methodology (Top-down & Bottom-up)

- Demand Modelling Approach (Derivative Linkage Method)

- Supply-Side Validation (Capacity & Utilization Mapping)

- Forecast Methodology & Scenario Building

- Data Triangulation Framework

- Industry Overview & Value Chain Analysis

- VAM in the Acetyl Chain

- Manufacturing Process Overview

- Feedstock Linkages (Acetic Acid, Ethylene)

- Cost Structure Overview

- Value Chain Mapping (Upstream to Downstream)

- Margin Distribution Across Value Chain

- Demand Supply Analysis (Regional and for 30+ Countries)

- Production

- Imports

- Exports

- Domestic Demand

- Demand Supply Analysis

- Market Dynamics

- Growth Drivers

- Industry Challenges

- Emerging Trends

- Substitution & Competitive Chemistries

- Porter’s Five Forces Analysis

- Global Vinyl Acetate Monomer Market Outlook, 2021-2031

- Market Size & Forecast by Value & by Volume

- Market Size & Forecast by Derivative

- Polyvinyl Acetate

- Polyvinyl Alcohol

- Ethylene Vinyl Acetate

- Ethylene Vinyl Alcohol

- VAE Emulsions (Vinyl Acetate Ethylene Emulsions)

- Other Derivatives

- Vinyl Acetate Copolymers

- Specialty Polymers

- Acrylic Modifiers

- Market Size & Forecast by End Use

- Construction

- Adhesives

- Sealants

- Cement Modifiers

- Insulation

- Packaging

- Flexible Packaging

- Barrier Films

- Carton Adhesives

- Automotive

- Interior Foams (EVA) Adhesives

- Adhesives

- Wire & Cable Insulation

- Textiles

- Sizing Agents

- Coatings

- Renewable Energy

- Solar Module Encapsulants (EVA)

- Consumer Goods

- Footwear

- Furniture Adhesives

- Market Size & Forecast by Grade / Purity

- Industrial Grade

- High Purity Grade

- By Manufacturing Process

- Ethylene-Based Route

- Acetylene-Based Route

- By Sales Channel

- Direct Sales (Long-Term Contracts)

- Spot Market

- Distributors

- By Integration Level

- Integrated Producers (Ethylene + Acetic Acid + VAM + Derivatives)

- Merchant Producers

- By Market Structure

- Captive

- Merchant

- By Region

- Asia-Pacific

- Europe

- North America

- Latin America

- Middle East & Africa

- Construction

Note: A consistent level of detail and data granularity will be provided across all 5 regions and 33 countries covered in the report

- Policy & Regulatory Landscape

- Global Regulatory Framework Overview

- Chemical Registration Regimes

- Hazard Classification Standards

- Environmental Regulations Impacting VAM

- VOC Emission Norms

- Industrial Air Emission Standards

- Wastewater Discharge Compliance

- Carbon Emission and ESG Policies

- Occupational Health & Safety Regulations

- Worker Exposure Limits

- Handling And Storage Standards

- Hazard Labeling Requirements

- Chemical Registration & Compliance

- Reach (Europe)

- TSCA (USA)

- China Chemical Regulations

- India Chemical Management Rules

- Other Asia-Pacific Frameworks

- Trade Policies & Tariff Structure

- Import/Export Duties

- Anti-Dumping Cases (If applicable)

- Free Trade Agreements Affecting VAM Flows

- Sustainability & ESG Policies

- Low-Carbon Production Initiatives

- Bio-Based Alternatives & Green Chemistry Trends

- Corporate Sustainability Mandates

- Regulatory Risk Assessment

- Impact on Capacity Expansions

- Cost Escalation Due To Compliance

- Policy-Driven Market Shifts

- Supply-Side Analysis

- Global Installed Capacity (By Company, Region, Country)

- Plant-Level Database (Capacity, Location, Technology, Start-Up Year)

- Operating Rates and Utilization Trends

- Captive Vs Merchant Supply Mapping

- Planned Expansions, Debottlenecks, And New Projects

- Producer Cost Curve (Indicative Ranking by Region/Feedstock Advantage)

- Logistics And Trade Lane Economics (Indicative)

- Trade Analysis

- Global Trade Overview (Exports/Imports by Region)

- Key Exporting Countries and Their Competitiveness

- Key Importing Countries and Demand Gap

- Trade Routes and Pricing Benchmarks (CFR/FOB Concepts)

- Tariffs, Duties, and Non-Tariff Barriers (High-Level)

- Trade Disruption Scenarios (Shipping, Geopolitics, Outages)

- Pricing Analysis and Margin Dynamics

- Price Benchmarks and Regional Price Formation

- Historical Price Trend Analysis (VAM)

- Feedstock Linkages

- Acetic Acid

- Ethylene

- VAM Spread Analysis (VAM Vs Feedstocks)

- Contract Vs Spot Pricing Mechanisms

- Price Forecast Methodology and Scenarios

- Sensitivity: Oil, Gas, Ethylene Chain, Acetic Chain Shocks

- Competitive Landscape

- Competitive Overview and Market Shares (Global + Regional)

- Producer Profiles (For Each Major Player)

- Company Overview and Strategy

- VAM Capacity & Plant Locations

- Integration (Ethylene/Acetic Acid)

- Cost Position and Operating Footprint

- Derivative Integration (PVAc, VAE, PVOH, EVA)

- Recent Developments (Expansions, Shutdowns, Partnerships)

- Competitive Benchmarking Matrix

- Scale, Integration, Geographic Reach, Customer Mix, Pricing Power

- Distributor/Trader Landscape

- Downstream & Customer Landscape

- Major downstream producers (PVAc, VAE, PVOH, EVA)

- Key End-Use Industries and Major Customers (Top 50)

- Procurement Behaviour: Contract Length, Pricing Terms, Quality Requirements

- Substitution Analysis (Alternative Chemistries and Switching Costs)

- Customer Decision Factors (Performance, Compliance, Cost, Supply Security)

- Sustainability, and EHS Landscape

- EHS Profile and Handling Requirements

- VOC Regulations and Implications for Adhesives/Coatings

- REACH/TSCA And Regional Compliance Themes

- Sustainability Trends

- Water-Based Formulations

- Bio-Based Routes and Low-Carbon Initiatives

- Impact Assessment on Demand and Product Positioning

- Strategic Analysis and Opportunity Mapping

- White Space Opportunities by Region and Application

- Import Substitution Opportunities (Country-Specific)

- Integration Opportunities (Acetic Acid/Ethylene, Derivatives)

- Go-To-Market Strategy Options

- Merchant Sales Strategy

- Contracting And Key Account Strategy

- Distribution Strategy

- Risk Assessment and Mitigation Strategies

- Investment Attractiveness and Scenario Outcomes

- Strategic Recommendations

- For VAM Producers

- For Downstream Derivative Manufacturers

- For Traders/Distributors

- For Investors and New Entrants

- For Policymakers/Industry Bodies

- Global Regulatory Framework Overview