Market Definition

A water infrastructure digital twin is a continuously synchronised, physics-informed virtual replica of a physical water system, encompassing drinking water treatment and distribution networks, wastewater collection and treatment infrastructure, stormwater management systems, irrigation canals, desalination plants, and large-scale water resource management assets such as reservoirs, dams, and inter-basin transfer schemes, that integrates real-time sensor data, hydraulic simulation models, asset management records, geospatial information, and operational history into a single, dynamic computational environment. Unlike static simulation models or geographic information systems that represent infrastructure at a fixed point in time, a water infrastructure digital twin is a living model: it ingests continuous data streams from supervisory control and data acquisition (SCADA) systems, advanced metering infrastructure (AMI), pressure and flow sensors, water quality monitors, structural health monitoring arrays, and weather and climate feeds to maintain a state of the system that mirrors physical reality with a latency typically measured in seconds to minutes. The market spans the full digital twin capability stack from foundational data integration and hydraulic model calibration through to advanced predictive analytics, real-time operational optimisation, scenario planning, and autonomous control recommendation. Core technical components include hydraulic and hydrodynamic simulation engines (EPANET, InfoWorks, WaterGEMS, MIKE FLOOD, DHI), IoT sensor networks and edge computing nodes for real-time data ingestion, cloud and hybrid-cloud computing infrastructure for model execution and storage, AI and machine learning engines for anomaly detection, demand forecasting, and predictive asset maintenance, cybersecurity frameworks for operational technology (OT) network protection, digital twin platform software (Bentley iTwin, Siemens Xcelerator, Esri ArcGIS, IBM Maximo, Autodesk Tandem), and the professional services layer encompassing system integration, model calibration, training, and managed operations. The market is defined across four principal application domains: water distribution digital twins for network operations, pressure management, and leakage reduction; wastewater and sewer digital twins for collection system hydraulics, combined sewer overflow prediction, and treatment process optimisation; stormwater and flood digital twins for real-time flood inundation modelling and emergency response; and water resource digital twins for catchment hydrology, reservoir operations, and climate-adaptive planning.

Market Insights

The most consequential structural shift reshaping the global water infrastructure digital twins market in 2026 is the transition from proof-of-concept and pilot deployments, which dominated the 2019–2023 period and were overwhelmingly driven by technology vendor-led demonstration projects with limited operational integration, to enterprise-scale, operationally embedded deployments in which digital twins are functioning as the primary decision-support infrastructure for large municipal and regional water utilities managing tens of thousands of kilometres of pipe network, tens of millions of customer connections, and water systems handling billions of litres per day. This operational maturity transition is being driven by three convergent factors: the accumulation of sufficient real-world performance evidence from early-adopter utilities, Thames Water, Southern Water, Anglian Water, Singapore PUB, Melbourne Water, Copenhagen Wastewater Services, and DC Water among them, to give conservative utility management boards the evidence base required to commit to full-network digital twin investments; the commoditisation of IoT sensor hardware and cloud computing unit costs to levels that make continuous real-time monitoring economically viable even for secondary distribution networks previously considered instrumentation-uneconomical; and the mounting financial and regulatory pressure from non-revenue water losses, energy cost escalation, and tightening regulatory water quality and environmental compliance requirements that make the quantifiable operating savings from digital twin deployment, typically 15–30% reduction in non-revenue water, 10–25% reduction in energy costs, and 20–40% improvement in asset maintenance cost efficiency, impossible for utility management to defer when alternative capital investment options are similarly constrained.

Geographically, the competitive and investment landscape for water infrastructure digital twins is developing on markedly different trajectories shaped by utility scale, regulatory environment, and the maturity of the underlying data and sensor infrastructure. The United Kingdom remains the most advanced regulatory market globally: Ofwat’s Price Review 2024 (PR24) settlement framework has embedded digital resilience investment, customer outcome commitments, and total expenditure efficiency targets that water companies can demonstrably achieve most cost-effectively through digital twin deployment, creating a direct regulatory-financial incentive structure with no equivalent in most other national markets. The Environment Agency’s enhanced storm overflow monitoring requirements, mandating event duration monitoring on all storm overflows by 2025, creating a real-time data layer that feeds directly into digital twin wastewater network models, provide an additional UK-specific catalyst. In North America, the Infrastructure Investment and Jobs Act (IIJA) allocation of USD 55 billion for water infrastructure modernisation through 2031, combined with the EPA’s Lead and Copper Rule Revisions and the Safe Drinking Water Act compliance requirements, is driving the largest wave of water utility capital investment in a generation and creating a procurement environment in which digital twin capabilities are increasingly embedded within broader capital programme delivery frameworks rather than procured as standalone technology. Singapore’s PUB (Public Utilities Board) represents the most comprehensively integrated national water digital twin programme globally, having deployed a real-time hydraulic digital twin of its entire potable water distribution network, a stormwater drainage digital twin covering the island’s complete catchment system, and a used-water reclamation digital twin integrating treatment process and collection network models, positioning Singapore as the global reference implementation that utility executives from across Asia, the Middle East, and Australasia are using as a benchmark and procurement template.

The primary structural growth catalyst for the global water infrastructure digital twins market is the deepening global water stress crisis, a combination of physical water scarcity, ageing infrastructure, population growth, climate variability, and escalating water quality regulation, that is creating a procurement environment in which water utilities have no viable alternative to deploying advanced digital intelligence to maintain service reliability, regulatory compliance, and financial sustainability with constrained capital budgets. The American Water Works Association (AWWA) estimates that the United States water and wastewater sector requires USD 625 billion in infrastructure investment over the next 20 years; the European Commission’s Water Blueprint identifies EUR 500+ billion in water infrastructure investment needs across EU member states through 2035; and the OECD’s Global Water Outlook projects that 40% of the global population will live in areas of severe water stress by 2050. Against this backdrop, digital twins offer water utilities a uniquely capital-efficient pathway to extending the useful life of existing assets through predictive maintenance, reducing operational expenditure through AI-driven process optimisation, cutting the catastrophic costs of unplanned pipe bursts and treatment failures through early detection, and achieving regulatory compliance outcomes without the full capital cost of physical infrastructure replacement. The market is further reinforced by the structural shift of major hydraulic simulation and GIS software vendors, Bentley Systems, Xylem (formerly Innovyze), DHI, Esri, Siemens Digital Industries, and IBM, from perpetual licence models toward subscription-based, cloud-hosted platform models that lower the barrier to continuous model maintenance and create recurring revenue streams that are aligned with the operational rather than capital procurement cycles of water utilities, fundamentally changing the procurement conversation from a capital expenditure item to an operational expenditure decision.

Key Drivers

- The foundational demand accelerator for water infrastructure digital twins is the structural deterioration of water distribution and wastewater infrastructure across the developed world combined with the catastrophic cost of undetected failures, a dynamic that makes the risk-reduction and asset intelligence value of digital twins increasingly non-discretionary for utilities managing ageing networks under tightening regulatory scrutiny. In the United States, the ASCE Infrastructure Report Card gives drinking water infrastructure a grade of C-, with an estimated 6 billion gallons of treated drinking water lost daily through leaking pipes, representing approximately 14–18% of all water entering distribution, at an economic cost of USD 2.6 billion annually in wasted treatment chemical, energy, and abstraction costs. In the UK, Ofwat’s enforcement actions against Southern Water, Thames Water, and Yorkshire Water for illegal sewage discharges, culminating in record fines of up to GBP 90 million per utility, have demonstrated that the regulatory and reputational cost of infrastructure failures is no longer absorbable within conventional operating margins, creating a board-level imperative to deploy digital intelligence that provides advance warning of network hydraulic stress, sewer surcharging risk, and treatment process exceedance before regulatory breach events occur. The financial calculus is increasingly clear: leading utilities deploying full-network digital twins report leakage reduction savings of USD 15–45 million per year for networks serving 1 million+ connections, energy optimisation savings of USD 5–15 million per year through pump scheduling and treatment process optimisation, and avoided capital expenditure of USD 30-80 million per decade through data-driven asset prioritisation that replaces costly condition assessment programmes with continuous structural health monitoring, payback periods of 2–4 years that meet the investment criteria of even the most conservative utility finance committees.

- The second structural driver is the AI and IoT technology maturation wave that is simultaneously expanding the analytical power available within digital twin platforms and dramatically reducing the unit cost of the sensor infrastructure required to achieve real-time network visibility at the granularity needed for operational digital twins. In AI, the deployment of foundation model architectures for time-series anomaly detection, trained on multi-year SCADA and AMI data streams from tens of thousands of sensors across multiple utility networkshas produced demand forecasting models that achieve 48-hour water demand prediction accuracy of 97–99% across daily, weekly, and seasonal demand cycles, pipe burst probability models that provide 72-hour advance warning for 85–90% of significant mains failures when trained on sufficient historical break and pressure transient data, and treatment process control models that reduce chemical dosing variability by 30–50% while maintaining compliance with turbidity, pH, and disinfection residual regulatory thresholds. The combination of these AI capabilities with real-time digital twin hydraulic state estimation creates a ‘living network intelligence’ layer that transforms reactive, crew-dispatched utility operations into proactive, predictive field force management. In IoT, the unit cost of pressure loggers, flow meters, and water quality sensors has declined 40–60% over the period 2020–2026 as chip-on-board sensor integration and LPWAN (LoRaWAN, NB-IoT) communication protocols have commoditised previously expensive point monitoring, enabling utilities to achieve sensor coverage densities of one device per 300–500 pipe connections in district metering areas where previously economic deployment thresholds required one device per 2,000–5,000 connections, fundamentally expanding the real-time observability of distribution networks that forms the data backbone of operational digital twin functionality.

- The third critical driver is the convergence of climate change-driven extreme weather events and regulatory tightening that is creating an acute and growing market for real-time flood and stormwater digital twins as an emergency management and long-term climate adaptation investment. The financial toll of urban flooding has escalated dramatically: Swiss Re estimates global insured flood losses have increased at 5–7% per annum over the past decade driven by a combination of more intense precipitation events and expanding urban impervious surface coverage, with single urban flood events in cities including Houston, Zhengzhou, Dubai, and Auckland generating insured losses of USD 5–20 billion per event. In this context, real-time stormwater and flood digital twins, which integrate weather radar precipitation nowcasting, real-time sewer and drainage network hydraulic modelling, surface flood inundation mapping, and emergency operations centre alerting into a unified operational platform, are transitioning from aspirational smart city initiatives to operationally essential public safety infrastructure. The EU Floods Directive and the UK National Flood and Coastal Erosion Risk Management Strategy both require local flood authorities and drainage boards to develop Flood Risk Management Plans that are increasingly informed by dynamic digital twin models, creating a regulatory pull that complements the operational and financial drivers. The insurance industry is beginning to price this capability into infrastructure resilience ratings: Zurich Insurance, Swiss Re, and Aon have published frameworks for climate risk disclosures that explicitly reference real-time flood modelling capability as a key indicator of infrastructure resilience, creating a financial market signal that complements the regulatory and operational drivers in incentivising water authority digital twin investment.

Key Challenges

- The most structurally significant challenge constraining the global water infrastructure digital twins market is the profound data quality, completeness, and accessibility gap that prevents most water utilities from constructing a digital twin of sufficient fidelity to deliver the operational and predictive performance benefits that vendor demonstrations promise. A functional hydraulic digital twin of a water distribution network requires, at minimum: a geometrically accurate and topologically connected GIS pipe network model covering 95%+ of pipe connectivity; attributed asset data including pipe material, age, diameter, roughness, and condition scores for the majority of the network; calibrated demand patterns derived from AMI smart meter data or zonal flow metering; pressure and flow boundary conditions from operational monitoring; and a hydraulic simulation engine capable of real-time extended period simulation. In practice, a survey of 150+ utilities conducted by the International Water Association in 2024 found that fewer than 25% of utilities in lower-income nations and fewer than 55% of utilities in high-income OECD nations possess GIS network models of sufficient completeness and accuracy to serve as a viable digital twin foundation without a multi-year data remediation programme. The data remediation investment required to bring a network model to digital twin readiness, typically USD 2–12 million for a utility serving 500,000–2 million connections, depending on existing data maturity, is often larger than the digital twin platform investment itself, creating a hidden total cost of ownership that is systematically underestimated in vendor-led business case development. Furthermore, the siloed organisational structure of most water utilities, in which operational technology (SCADA), geographic information systems, asset management, financial, and customer data are maintained in separate departmental systems by separate teams with limited data governance frameworks, creates integration complexity that extends digital twin implementation timelines from the 12–18 months promised in vendor demonstrations to 3–5 years in practice for full-network enterprise deployments, substantially eroding the financial returns modelled in procurement business cases.

- A parallel and increasingly prominent challenge is the cybersecurity vulnerability that real-time digital twin deployment introduces into water critical national infrastructure, and the regulatory, procurement, and operational complexity this creates for utilities and their technology vendors. Water infrastructure digital twins require bidirectional data connectivity between operational technology (OT) networks, which control physical treatment processes, pump stations, and distribution control valves, and information technology (IT) cloud platforms hosting simulation models, AI analytics, and external data feeds. This OT-IT integration creates attack surface exposure that is categorically different from the air-gapped SCADA environments that characterise most legacy water utility control architectures. The US Cybersecurity and Infrastructure Security Agency (CISA) has classified water infrastructure as one of sixteen critical infrastructure sectors and has issued multiple advisories following demonstrated cyber intrusions into water utility SCADA systems, including the 2021 Oldsmar, Florida municipal water system attack in which an operator’s remote access terminal was compromised and sodium hydroxide levels were briefly adjusted to dangerous concentrations. The 2024 American Water Works Company cyberattack, which forced the largest US investor-owned water utility to disconnect customer-facing systems and disrupted operations across multiple states, demonstrated that even well-resourced utilities with mature IT organisations are vulnerable to cyber incidents that can translate to operational disruption. For digital twin deployments, the consequence of a successful cyberattack is amplified: a compromised digital twin that feeds falsified sensor data to AI-driven control systems could enable manipulation of physical infrastructure at scale in ways that no individual SCADA terminal attack could achieve. Addressing this challenge requires purpose-built OT cybersecurity architecture, data diodes, unidirectional security gateways, network segmentation, and zero-trust access frameworks, that add USD 500,000–3 million to digital twin implementation costs and require specialist OT cybersecurity expertise that is in critically short supply globally.

Market Segmentation

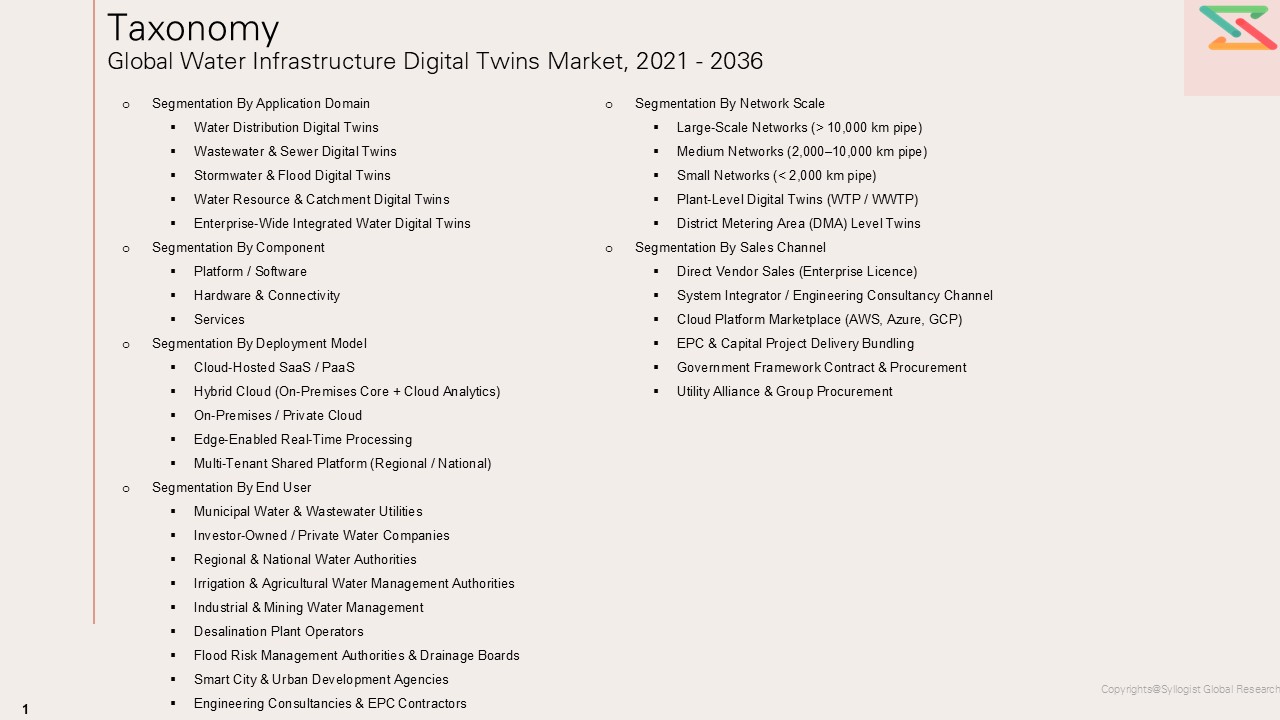

- Segmentation by Application Domain

- Water Distribution Digital Twins

- Leakage Detection & Non-Revenue Water Reduction

- Pressure Zone Management & Optimisation

- Demand Forecasting & Supply-Demand Balancing

- Water Quality Monitoring & Contamination Tracing

- Pipe Burst Prediction & Asset Prioritisation

- Hydraulic Network Modelling & Calibration

- Wastewater & Sewer Digital Twins

- Collection System Hydraulic Modelling

- Combined Sewer Overflow (CSO) Prediction & Control

- Wastewater Treatment Process Optimisation

- Energy Efficiency & Chemical Dosing Optimisation

- Biogas & Energy Recovery Optimisation

- Sewer Condition Assessment & Rehabilitation Planning

- Stormwater & Flood Digital Twins

- Real-Time Flood Inundation Mapping

- Urban Drainage Network Hydraulic Modelling

- Flood Early Warning & Emergency Response

- Climate Scenario Planning & Flood Risk Assessment

- Sustainable Urban Drainage System (SuDS) Modelling

- Water Resource & Catchment Digital Twins

- Reservoir Operations & Yield Optimisation

- Catchment Hydrology & Water Quality Modelling

- Irrigation Network Management

- Desalination Plant Digital Twins

- Inter-Basin Transfer System Management

- Enterprise-Wide Integrated Water Digital Twins

- Water Distribution Digital Twins

- Segmentation by Component

- Platform / Software

- Hydraulic & Hydrodynamic Simulation Engines

- Digital Twin Platform & Integration Middleware

- AI / ML Analytics & Predictive Modelling

- GIS & Spatial Analytics

- Asset Management Integration (EAM / CMMS)

- Cybersecurity & OT Network Protection

- Visualisation, Dashboarding & Reporting

- Hardware & Connectivity

- IoT Sensors (Pressure, Flow, Water Quality)

- Advanced Metering Infrastructure (AMI / Smart Meters)

- SCADA / ADMS Integration Systems

- Edge Computing Nodes & RTUs

- LPWAN Communication Networks (LoRaWAN, NB-IoT, 5G)

- Data Historian & Time-Series Databases

- Services

- System Integration & Implementation

- Hydraulic Model Build & Calibration

- Data Remediation & GIS Network Cleansing

- Training & Change Management

- Managed Services & Ongoing Model Maintenance

- Consulting & Strategic Advisory

- Segmentation by Deployment Model

- Cloud-Hosted (SaaS / PaaS)

- Hybrid Cloud (On-Premises Core + Cloud Analytics)

- On-Premises / Private Cloud

- Edge-Enabled Real-Time Processing

- Multi-Tenant Shared Platform (Regional / National)

- Segmentation by End User

- Municipal Water & Wastewater Utilities

- Large Metropolitan Utilities (1M+ connections)

- Medium Municipal Utilities (100K-1M connections)

- Small & Rural Utilities (< 100K connections)

- Investor-Owned / Private Water Companies

- Regional & National Water Authorities

- Irrigation & Agricultural Water Management Authorities

- Industrial & Mining Water Management

- Desalination Plant Operators

- Flood Risk Management Authorities & Drainage Boards

- Smart City & Urban Development Agencies

- Engineering Consultancies & EPC Contractors

- Municipal Water & Wastewater Utilities

- Segmentation by Network Scale

- Large-Scale Networks (> 10,000 km pipe)

- Medium Networks (2,000 – 10,000 km pipe)

- Small Networks (< 2,000 km pipe)

- Plant-Level Digital Twins (WTP / WWTP)

- District Metering Area (DMA) Level Twins

- Segmentation by Sales Channel

- Direct Vendor Sales (Enterprise Licence)

- System Integrator / Consulting Channel

- Cloud Platform Marketplace (AWS, Azure, GCP)

- EPC & Capital Project Delivery Bundling

- Government Framework Contract & Procurement

- Utility Alliance & Group Procurement

- Platform / Software

All market revenues are presented in USD and encompass platform software, hardware, connectivity, and professional services components

Historical Year: 2021–2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027–2036

Key Questions this Study Will Answer

- What are the critical market metrics and forward-looking projections for the Global Water Infrastructure Digital Twins Market, including total revenue (platform software, hardware/IoT, connectivity, and professional services), average contract value by utility scale, and total cost of ownership benchmarking, segmented across Application Domain (Water Distribution, Wastewater & Sewer, Stormwater & Flood, Water Resource & Catchment, Enterprise-Integrated), Component (Platform/Software, Hardware & Connectivity, Services), Deployment Model (Cloud SaaS, Hybrid, On-Premises, Edge, Multi-Tenant), End User (Municipal utility size tiers, Private water companies, Irrigation authorities, Industrial, Flood risk authorities), Network Scale (Large, Medium, Small, Plant-level, DMA-level), and Sales Channel (Direct, System Integrator, Cloud Marketplace, EPC Bundled, Government Framework, Utility Alliance)?

- How do market penetration rates, procurement velocity, and digital twin capability maturity vary across key geographies, the United Kingdom (Ofwat PR24 regulatory driver, Environment Agency overflow monitoring mandate), North America (IIJA USD 55B water investment, EPA Lead & Copper Rule, state-level PFAS compliance), Singapore (PUB enterprise national twin reference model), Australia (National Water Grid, urban utility AMI density), the European Union (EU Water Framework Directive, Floods Directive, Water Blueprint), the Middle East (desalination-dependent national water strategies in Saudi Arabia, UAE, and Israel), and Asia Pacific (rapid urbanisation, industrial water stress, national digital infrastructure programmes in Japan and South Korea), and what regulatory mandates, utility consolidation trends, infrastructure investment cycles, and competitive vendor dynamics shape adoption in each regional market?

- In what ways are data quality constraints, legacy GIS completeness gaps, OT-IT integration complexity, organisational data silos, hydraulic model calibration challenges, sensor network density limitations, SCADA protocol heterogeneity, and OT cybersecurity architecture requirements influencing digital twin implementation timelines, total cost of ownership relative to vendor business case projections, the selection of platform architecture (cloud vs. hybrid vs. on-premises), the sequencing of digital twin capability deployment (distribution first vs. wastewater first vs. enterprise-integrated), and the ultimate operational performance, measured by non-revenue water reduction, asset failure prediction accuracy, energy cost savings, and regulatory compliance improvement, achieved by utilities that have completed enterprise-scale deployments relative to pre-deployment business case projections?

- Who are the leading global digital twin platform vendors, hydraulic simulation software providers, IoT and AMI hardware suppliers, system integrators, and specialist AI analytics developers serving the water infrastructure sector, and how do they benchmark across key competitive dimensions including hydraulic model engine performance (network size supported, simulation speed, calibration tooling), AI analytics capability (demand forecast accuracy, pipe burst prediction lead time and precision recall performance), IoT sensor integration breadth and real-time data latency, cloud platform architecture and data security certifications (ISO 27001, SOC 2, OT-specific IEC 62443), deployment track record by utility scale and network type, OT cybersecurity integration capability, pricing model and total cost of ownership per connection per year, and partner ecosystem depth for system integration and managed services delivery?

- What strategic insights emerge from primary discussions with utility chief digital officers, asset management directors, operational technology managers, network operations leads, and capital delivery programme managers, as well as digital twin platform vendors, hydraulic engineering consultancies, IoT infrastructure providers, OT cybersecurity specialists, and water sector regulators, regarding utilities’ actual versus projected savings from deployed digital twins, the minimum sensor density and data quality thresholds required to achieve operationally meaningful hydraulic state estimation, the critical success factors distinguishing utilities that have achieved measurable operational ROI from digital twins within 18 months of deployment from those still in prolonged calibration and optimisation phases, the evolving competitive boundary between established hydraulic simulation vendors (Xylem Innovyze, Bentley, DHI) and cloud-native AI platform entrants (Fracta, Fathom, Autodesk, IBM), the role of regulatory investment incentives versus genuine operational conviction in driving procurement decisions, and the technology investment roadmap priorities that will most effectively close the capability gap between current digital twin deployments and the autonomous, self-calibrating, AI-driven water network intelligence that represents the long-term vision of the sector?

- Market Overview

- Product Overview

- Research Methodology

- Executive Summary

- Market Dynamics

- Market Dynamics (Drivers, Restraints, Opportunities, Challenges, Porter’s Five Forces Analysis, PESTLE Analysis)

- Market Trends & Developments

- Risk Assessment Framework

- Regulatory & Compliance Risk

- Data Quality & Legacy Infrastructure Risk

- OT Cybersecurity & Operational Risk

- Technology Adoption & Change Management Risk

- Regulatory Framework & Standards

- Global Regulatory Overview

- Key Regulations & Mandates by Region

- UK: Ofwat PR24 Settlement

- UK: Environment Agency Storm Overflow Monitoring Mandate (2025)

- UK: National Flood & Coastal Erosion Risk Management Strategy

- USA: Infrastructure Investment & Jobs Act (IIJA)

- USA: EPA Lead & Copper Rule Revisions

- USA: Safe Drinking Water Act

- USA: America’s Water Infrastructure Act (AWIA) Risk & Resilience Assessments

- EU: Water Framework Directive (WFD)

- EU: Floods Directive

- EU: Urban Wastewater Treatment Directive (Revised)

- EU: Water Blueprint

- Australia: National Water Grid Authority

- Singapore: PUB Smart Water Grid & Digital Twin Mandate

- Middle East: National Water Strategies (Saudi Vision 2030, UAE Water Security Strategy)

- Water Quality, Safety & Environmental Standards

- WHO Drinking Water Quality Guidelines

- ISO 24510

- ISO 24518

- EN 805

- EPA National Primary Drinking Water Regulations (NPDWRs)

- Digital Infrastructure & Cybersecurity Standards

- IEC 62443

- NIST Cybersecurity Framework

- CISA Water & Wastewater Sector Cybersecurity Guidelines

- ISO/IEC 27001

- SOC 2 Type II

- IEC 61968

- Digital Twin & Simulation Standards

- ISO 23247

- ASCE/EWRI Standards for Hydraulic Modelling

- BS 8632

- ISO 55000

- Regulatory Impact on Market

- Global Water Infrastructure Digital Twins Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Revenue Stream (Platform, Hardware, Services)

- Market Size & Forecast by Application Domain

- Water Distribution Digital Twins

- Leakage Detection & Non-Revenue Water (NRW) Reduction

- Pressure Zone Management & Optimisation

- Demand Forecasting & Supply-Demand Balancing

- Water Quality Monitoring & Contamination Tracing

- Pipe Burst Prediction & Asset Prioritisation

- Hydraulic Network Modelling & Continuous Calibration

- District Metering Area (DMA) Digital Twin Management

- Wastewater & Sewer Digital Twins

- Collection System Hydraulic Modelling

- Combined Sewer Overflow (CSO) Prediction & Control

- Wastewater Treatment Process Optimisation

- Energy Efficiency & Chemical Dosing Optimisation

- Biogas Production & Energy Recovery Optimisation

- Sewer Condition Assessment & Rehabilitation Planning

- Nutrient Removal Process Digital Twin

- Stormwater & Flood Digital Twins

- Real-Time Flood Inundation Mapping & Alerting

- Urban Drainage Network Hydraulic Modelling

- Flood Early Warning System Integration

- Climate Scenario Planning & Flood Risk Assessment

- Sustainable Urban Drainage System (SuDS) Modelling

- Coastal Flood & Tidal Surge Digital Twins

- Water Resource & Catchment Digital Twins

- Reservoir Operations & Yield Optimisation

- Catchment Hydrology & Water Quality Modelling

- Irrigation Network Management & Demand Efficiency

- Desalination Plant Process Digital Twins

- Inter-Basin Transfer System Management

- Groundwater & Aquifer Management Digital Twins

- Enterprise-Wide Integrated Water Digital Twins

- Full-Cycle Water Systems Integration (Supply to Treatment to Return)

- Corporate Asset Performance Management & Capital Planning

- Regulatory Compliance Reporting & Evidence Generation

- Market Size & Forecast by Component

- Platform / Software

- Hydraulic & Hydrodynamic Simulation Engines

- Digital Twin Platform & Integration Middleware

- AI / ML Analytics & Predictive Modelling Engines

- GIS & Spatial Analytics Platform

- Asset Management Integration (EAM / CMMS / ERP)

- Cybersecurity & OT Network Protection Software

- Visualisation, Dashboarding & Reporting Tools

- Data Historian & Time-Series Database

- Hardware & Connectivity

- IoT Pressure & Flow Sensors

- Water Quality Monitoring Sensors (Online & In-Situ)

- Advanced Metering Infrastructure (AMI) / Smart Meters

- SCADA & ADMS Integration Systems & Gateways

- Edge Computing Nodes & Remote Terminal Units (RTUs)

- LPWAN Communication Networks (LoRaWAN, NB-IoT, Sigfox)

- 5G Private Network Infrastructure for Water OT

- Structural Health Monitoring Sensors (Acoustic, Vibration)

- Services

- System Integration & Digital Twin Implementation

- Hydraulic Model Build, Calibration & Validation

- Data Remediation & GIS Network Cleansing

- IoT Network Design & Sensor Deployment

- OT Cybersecurity Assessment & Architecture

- Training, Change Management & Capability Building

- Managed Services & Ongoing Model Maintenance

- Strategic Advisory & Business Case Development

- Platform / Software

- Market Size & Forecast by Deployment Model

- Cloud-Hosted SaaS / PaaS

- Hybrid Cloud (On-Premises Core + Cloud Analytics)

- On-Premises / Private Cloud

- Edge-Enabled Real-Time Processing

- Multi-Tenant Shared Platform (Regional / National)

- Market Size & Forecast by End User

- Municipal Water & Wastewater Utilities

- Large Metropolitan Utilities (1M+ connections)

- Medium Municipal Utilities (100K–1M connections)

- Small & Rural Utilities (< 100K connections)

- Investor-Owned / Private Water Companies

- Regional & National Water Authorities

- Irrigation & Agricultural Water Management Authorities

- Industrial & Mining Water Management

- Desalination Plant Operators

- Flood Risk Management Authorities & Drainage Boards

- Smart City & Urban Development Agencies

- Engineering Consultancies & EPC Contractors

- Municipal Water & Wastewater Utilities

- Market Size & Forecast by Network Scale

- Large-Scale Networks (> 10,000 km pipe)

- Medium Networks (2,000–10,000 km pipe)

- Small Networks (< 2,000 km pipe)

- Plant-Level Digital Twins (WTP / WWTP)

- District Metering Area (DMA) Level Twins

- Market Size & Forecast by Sales Channel

- Direct Vendor Sales (Enterprise Licence)

- System Integrator / Engineering Consultancy Channel

- Cloud Platform Marketplace (AWS, Azure, GCP)

- EPC & Capital Project Delivery Bundling

- Government Framework Contract & Procurement

- Utility Alliance & Group Procurement

- Market Size & Forecast by Region

- North America

- Europe

- Asia-Pacific

- Middle East & Africa

- Latin America

- Water Distribution Digital Twins

- Asia-Pacific Water Infrastructure Digital Twins Market Outlook

- Market Size & Forecast

- By Value

- By Application Domain

- By Component

- By Deployment Model

- By End User

- By Network Scale

- By Sales Channel

- Market Size & Forecast

- Europe Water Infrastructure Digital Twins Market Outlook

- Market Size & Forecast

- By Value

- By Application Domain

- By Component

- By Deployment Model

- By End User

- By Network Scale

- By Sales Channel

- Market Size & Forecast

- North America Water Infrastructure Digital Twins Market Outlook

- Market Size & Forecast

- By Value

- By Application Domain

- By Component

- By Deployment Model

- By End User

- By Network Scale

- By Sales Channel

- Market Size & Forecast

- Latin America Water Infrastructure Digital Twins Market Outlook

- Market Size & Forecast

- By Value

- By Application Domain

- By Component

- By Deployment Model

- By End User

- By Network Scale

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Water Infrastructure Digital Twins Market Outlook

- Market Size & Forecast

- By Value

- By Application Domain

- By Component

- By Deployment Model

- By End User

- By Network Scale

- By Sales Channel

- Market Size & Forecast

- Country Wise* Water Infrastructure Digital Twins Market Outlook

- Market Size & Forecast

- By Value

- By Application Domain

- By Component

- By Deployment Model

- By End User

- By Network Scale

- By Sales Channel

- *Countries Analyzed in the Syllogist Global Research Portfolio: United Kingdom, United States, Singapore, Australia, Netherlands, Germany, France, Denmark, Sweden, Norway, Spain, Italy, Belgium, Canada, Japan, South Korea, India, China, UAE, Saudi Arabia, Israel, South Africa, Brazil, Mexico, New Zealand, Poland, Portugal, Austria, Switzerland, Finland

- Technology Analysis

- Digital Twin Capability Maturity Model — Level 1 to Level 5

- Level 1: Static Model (GIS / Hydraulic Simulation Only)

- Level 2: Connected Model (Real-Time SCADA / AMI Integration)

- Level 3: Operational Twin (Continuous State Estimation & Alerting)

- Level 4: Predictive Twin (AI-Driven Failure Prediction & Optimisation)

- Level 5: Autonomous Twin (Self-Calibrating, Closed-Loop Control)

- Hydraulic & Hydrodynamic Simulation Technology

- EPANET 2.2 — Open-Source Distribution Network Modelling

- Xylem Innovyze InfoWorks WS Pro & ICM — Integrated Catchment Modelling

- Bentley WaterGEMS & WaterSight — Cloud-Native Distribution Twin

- DHI MIKE+ — Integrated Urban Water Modelling Suite

- Siemens PSS SINCAL — Network Analysis & Planning

- Esri ArcGIS Water Utility Network — GIS-Centric Hydraulic Integration

- Real-Time Extended Period Simulation (EPS) Engine Performance

- Model Calibration Methodologies — Genetic Algorithm, Gradient-Based, Ensemble

- AI & Machine Learning Technology for Water Digital Twins

- Demand Forecasting — LSTM, Transformer, Prophet Models

- Pipe Burst & Failure Prediction — Survival Analysis, Random Forest, XGBoost

- Anomaly Detection — Isolation Forest, Autoencoders, Statistical Process Control

- Pressure Transient Analysis for Leak Localisation — AI Signal Processing

- Water Quality Prediction — Disinfection Residual, Turbidity, PFAS Forecasting

- Treatment Process Optimisation — Reinforcement Learning for Chemical Dosing

- Foundation Models & Transfer Learning for Multi-Utility Generalisation

- IoT & Sensor Technology

- Pressure Sensor Technology — Piezoelectric, Strain Gauge, MEMS

- Acoustic Leak Detection Sensors — Correlating Loggers, Fixed Hydrophones

- Online Water Quality Analysers — TOC, Turbidity, Chlorine, pH, Nitrate

- Smart Metering Technology — AMI Architecture, Data Communication Protocols

- LPWAN Protocol Comparison — LoRaWAN vs NB-IoT vs Sigfox for Water

- 5G Private Network Applications for Real-Time OT Data Streaming

- Edge Computing Architecture for Low-Latency Sensor Data Processing

- Data Integration & Platform Technology

- OT-IT Convergence Architecture — Data Diodes, Unidirectional Gateways

- SCADA Protocol Integration — Modbus, DNP3, IEC 60870, OPC-UA

- Digital Twin Middleware — API Architecture, Event Streaming (Kafka)

- Time-Series Database Technology — InfluxDB, TimescaleDB, OSIsoft PI

- Cloud Data Lake Architecture for Multi-Source Water Data Integration

- Digital Thread — Linking Design, Construction & Operational Data

- OT Cybersecurity Technology

- Network Segmentation — Purdue Model & Zero-Trust for Water OT

- Unidirectional Security Gateways — Waterfall, Owl Cyber Defense

- OT Security Monitoring — Claroty, Dragos, Nozomi Networks for Water

- Vulnerability Assessment for Water SCADA & Digital Twin Platforms

- Incident Response Planning for Water OT Cyberattack Scenarios

- Emerging Technologies & Innovation Pipeline

- Generative AI for Hydraulic Model Synthesis & Scenario Generation

- Digital Twin Interoperability — Open Standards & API Federation

- Quantum-Accelerated Hydraulic Simulation for Large Network Optimisation

- Satellite & UAV Remote Sensing Integration for Catchment Monitoring

- Drone-Based Pipe Condition Assessment & Digital Twin Data Capture

- Augmented Reality (AR) Field Interface for Digital Twin Maintenance

- Blockchain for Water Data Provenance & Regulatory Evidence Chain

- Digital Twin Capability Maturity Model — Level 1 to Level 5

- Value Chain & Supply Chain Analysis

- Water Data Generation Layer (Sensors, Meters, SCADA)

- Data Transmission & Connectivity Infrastructure

- Data Integration & Management (Historian, Data Lake, Middleware)

- Hydraulic Simulation & Digital Twin Core Platform

- AI Analytics & Predictive Intelligence Layer

- Visualisation, Alerting & Control Interface Layer

- Professional Services & System Integration

- End-User Utility Operations & Asset Management

- Ecosystem Map

- Supply Chain Analysis

- Sensor & Hardware Component Supply — Semiconductor & MEMS Dependency

- Hydraulic Simulation Software IP Concentration

- Cloud Hyperscaler Dependency — AWS, Azure, GCP for SaaS Platforms

- Data Science & Hydraulic Engineering Talent Supply Constraints

- OT Cybersecurity Specialist Shortage in Water Sector

- Supply Chain Risk — IoT Hardware Geopolitical Exposure

- Trade Flow Analysis

- Software Licensing Export — US & European Simulation Platform Dominance

- IoT Hardware Trade Flows — Asian Manufacturing, Western Deployment

- Managed Services Offshoring & Nearshoring Dynamics

- Open-Source Ecosystem vs Proprietary Software Trade-Offs

- Pricing Analysis

- Platform Software Pricing Models

- Perpetual Licence vs Annual Subscription (SaaS) — Market Transition

- Per-Connection Pricing (USD / Connection / Year) by Utility Scale

- Per-Node or Per-Pipe-km Pricing Models

- Tiered Capability Pricing — Basic Hydraulic vs Full AI Analytics

- Enterprise Site Licence vs Modular Capability Bundling

- Hardware & IoT Sensor Pricing

- Pressure Logger Unit Cost Trajectory (USD / Device) 2020–2030

- Online Water Quality Analyser Pricing by Parameter

- Smart Meter AMI System Cost Per Connection

- Edge Computing Node & Gateway Pricing

- Professional Services Pricing

- System Integration Day Rate Benchmarking by Geography

- Hydraulic Model Build Cost — Per km of Network

- Data Remediation Cost Per Connection

- Managed Service Annual Fee as % of Total Implementation Cost

- Total Cost of Ownership Modelling

- 5-Year TCO at Small, Medium, and Large Utility Scale

- TCO Sensitivity to Data Maturity Starting Point

- ROI Modelling — NRW Savings, Energy, Maintenance, Compliance

- Payback Period Analysis by Utility Type & Network Complexity

- Pricing Tier Analysis

- Entry-Level / DMA-Scale Deployment

- Zone-Level Distribution Twin

- Full-Network Enterprise Digital Twin

- Enterprise-Integrated Multi-Domain Twin

- Platform Software Pricing Models

- Sustainability, Resilience & ESG Considerations

- Climate Resilience Planning — Digital Twin Role in Adaptation

- Energy Consumption Reduction — Pump Optimisation & Treatment Efficiency

- Chemical Usage Reduction — Disinfection Optimisation & Environmental Benefit

- Water Loss Reduction — NRW & Environmental Impact Quantification

- Carbon Footprint of Digital Twin Infrastructure (Cloud Compute Emissions)

- ESG Reporting Frameworks for Water Utility Digital Investment

- TCFD — Physical & Transition Risk Disclosure for Water Infrastructure

- GRI 303 — Water & Effluent Disclosure

- UN SDG 6 — Clean Water & Sanitation — Digital Twin Contribution Metrics

- Science Based Targets for Nature (SBTn) — Water Stewardship

- Circular Water Economy — Digital Twin Support for Resource Recovery

- Social Value & Water Equity — Digital Deployment in Underserved Utilities

- Go-to-Market & Distribution

- Sales Channel Overview

- Direct Enterprise Sales — Platform Vendor to Large Utility

- System Integrator & Engineering Consultancy Channel

- Cloud Marketplace Listings — AWS, Microsoft Azure, GCP

- EPC & Capital Programme Delivery Bundling

- Government Framework & Crown Commercial Service (UK) Procurement

- Utility Alliance & Consortium Group Procurement

- Partner Ecosystem Strategies

- Technology Alliance Partnerships — IoT + Platform + AI

- Reseller & Value-Added Reseller (VAR) Channel for SME Utilities

- Academic & National Laboratory Research Partnerships

- Utility Procurement Decision Dynamics

- Capital vs Operating Expenditure Framing for Digital Twin Investment

- Regulatory Incentive Structures — Ofwat, IIJA, EU Cohesion Fund

- Utility Board & C-Suite Decision Criteria

- Proof of Concept to Enterprise Scale-Up Pathway

- Customer Success & Retention Strategies

- Continuous Model Calibration & Platform Update SLAs

- ROI Reporting & Value Demonstration Frameworks

- User Community & Knowledge Sharing Networks

- Sales Channel Overview

- Competitive Landscape

- Market Structure & Concentration

- Market Fragmentation — Hydraulic Simulation Incumbents vs Cloud-Native Entrants

- Top 10 Players by Revenue & Utility Deployment Count

- HHI Concentration Analysis by Component & Geography

- Competitive Intensity Map — Application Domain vs Region

- Player Classification

- Hydraulic Simulation Incumbents

- Xylem (Innovyze) — InfoWorks, ICM, IWLive

- Bentley Systems — WaterGEMS, WaterSight, iTwin

- DHI — MIKE+, MIKE FLOOD, MIKE URBAN+

- Esri — ArcGIS Water Utility Network

- Autodesk — InfoDrainage, Tandem Digital Twin

- Industrial Platform & OT Vendors

- Siemens Digital Industries — Xcelerator, SIWA Water Suite

- IBM — Maximo Application Suite, Environmental Intelligence

- Schneider Electric — EcoStruxure for Water & Wastewater

- ABB — AbilityTM Water Asset Management

- Emerson — DeltaV Digital Twin for Water Treatment

- Cloud-Native AI & Analytics Platforms

- Fracta — AI Pipe Failure Prediction

- Fathom — Global Flood & Water Risk Modelling

- Wychwood Water Systems — Operational Insight Platform

- WaterBit — IoT Platform for Agricultural Water

- Hive Systems — Stormwater Real-Time Intelligence

- IoT Hardware & AMI Platform Vendors

- Sensus (Xylem) — Smart Meters & AMI

- Itron — Advanced Metering Infrastructure

- Mueller Water Products — Mi.Net AMI Platform

- Radcom / Echologics — Acoustic Leak Detection

- Inflowmatix — Pressure Analytics & Leak Detection

- Specialist Flood & Stormwater Platforms

- Innovyze (Xylem) — InfoWorks ICM Stormwater

- HR Wallingford — Flood Modeller Suite

- JBA Consulting — Flood Risk Modelling

- KWR Water Research Institute — Digital Twin R&D

- System Integrators & Implementation Partners

- WSP Global — Water Digital Programme Delivery

- Jacobs Engineering — Digital Water Solutions

- Stantec — Water & Digital Infrastructure

- Mott MacDonald — Digital Water & SCADA Integration

- Black & Veatch — Smart Utility Digital Transformation

- Emerging & Regional Players

- Hydraulic Simulation Incumbents

- Market Structure & Concentration

- Competitive Analysis Frameworks

- Market Share Analysis by Revenue & Deployments

- Company Profile

- Company Overview & HQ

- Digital Twin Product Portfolio — Application Domain Coverage

- Simulation Engine & AI Analytics Capability

- Deployment Track Record — Utility Scale & Network Type

- Revenue & Water Digital Segment Revenue

- Cloud Platform Architecture & Security Certification

- IoT & AMI Integration Breadth

- OT Cybersecurity Integration Capability

- Partner Ecosystem & System Integration Depth

- Recent Developments (Acquisitions, Product Launches, Contracts)

- SWOT Analysis

- Technology Roadmap — AI, Autonomy & Interoperability

- Competitive Positioning Map (Simulation Depth vs AI Analytics vs Scale)

- Patent Landscape Analysis — Hydraulic AI, Leak Detection, Water Quality

- Investment & Ecosystem Financing Landscape

- Utility Capital Programme Investment in Digital Twin (2025–2036)

- Vendor R&D Investment — AI, IoT, Platform Architecture

- Government Grant & Stimulus Programmes

- UK: Ofwat Innovation Fund — Digital & Data Projects

- UK: Innovate UK Water Technology Challenge Fund

- USA: IIJA Water Infrastructure Grants — Digital Eligibility

- EU: Horizon Europe — Water4All Partnership & Digital Water Projects

- EU: Cohesion Fund & ERDF — Smart Water Grants

- Australia: National Water Grid Authority Digital Investment

- Singapore: PUB R&D Grant Programme

- Venture Capital & Private Equity Activity (2020–2026)

- AI Water Analytics Funding Rounds — Fracta, Fathom, Wychwood, Others

- IoT Water Technology VC Activity

- Water Sector Digital Infrastructure PE Investment

- Strategic M&A Activity

- Xylem Acquisition of Innovyze (2022) — Strategic Rationale & Market Impact

- Bentley Systems Digital Twin Acquisitions — Velocity, Sensemetrics

- Siemens & ABB Water Digital Acquisitions

- Emerging M&A Targets — AI Analytics, IoT, OT Cybersecurity

- Project Pipeline — Major Digital Twin Tenders & Deployments (2025–2030)

- Strategic Recommendations

- For Water Digital Twin Platform Vendors

- Application Domain Priority & Product Roadmap Strategy

- AI Analytics Capability Deepening — From Alerting to Autonomous Control

- Open Standards & Interoperability — API-First Platform Architecture

- OT Cybersecurity Integration as Competitive Differentiator

- SME Utility Market Entry — Modular, Low-Barrier Deployment Models

- Emerging Market Strategy — India, Southeast Asia, Latin America

- M&A, Partnership & Ecosystem Building Strategy

- For IoT Sensor & Hardware Vendors

- Sensor Cost Reduction Roadmap — MEMS & Chip-on-Board Integration

- LPWAN Protocol Selection & Certification Strategy

- Digital Twin Data Format & API Compatibility Standards

- OT Security by Design for Water-Deployed IoT Hardware

- For Engineering Consultancies & System Integrators

- Digital Twin Delivery Methodology — Data-First Implementation Approach

- Hydraulic Model Quality Assurance & Calibration Standards

- OT Cybersecurity Competency Development & Certification

- Managed Services & Long-Term Model Maintenance Business Models

- Alliance Strategy with Platform Vendors & IoT Suppliers

- For Water Utilities — Large Metropolitan & Regional

- For Water Utilities — Small & Medium

- Entry-Level Digital Twin Pathway — DMA & Zone-Level First

- Shared Platform & Utility Alliance Models to Pool Investment

- Government Grant & Regulatory Incentive Optimisation

- Low-Code / No-Code AI Analytics Adoption for Resource-Constrained Teams

- For Water Digital Twin Platform Vendors

- For Investors & Private Equity

- High-Priority Investment Themes — AI Analytics, OT Security, AMI Integration

- M&A Opportunity Map — Platform vs IoT vs Services

- Geographic Investment Priorities — UK, USA, Singapore, Middle East

- Risk-Return Analysis by Technology Maturity Stage

- Key Risks — Data Quality Gap, Cyber Liability, Platform Concentration

- For Governments & Regulators

- Regulatory Incentive Design for Digital Twin Investment (Ofwat PR Model)

- Minimum Data Standards for Water Network GIS & SCADA Completeness

- National Digital Water Programme Design — Singapore PUB as Template

- OT Cybersecurity Minimum Standards for Water Critical Infrastructure

- Public Procurement Frameworks — Digital Twin Capability Requirements

- R&D Grant Programme Design — AI, IoT & Open-Standards Innovation

- White Space & Opportunity Analysis

- Unmet Needs — Small Utility, Agricultural Water, Groundwater Digital Twins

- Emerging Business Models — Digital Twin-as-a-Service, Per-Connection SaaS

- Technology White Spaces — Autonomous Self-Calibrating Twins, AR Field Interface

- Geographic White Spaces — Sub-Saharan Africa, South Asia, Southeast Asia

- Strategic Priority Matrix & Roadmap

- Near-term (2025–2028) — Enterprise Rollout & AI Maturation

- Mid-term (2029–2032) — Autonomous Operations & Standard Interoperability

- Long-term (2033–2036) — Climate-Adaptive Integrated Water Intelligence