Market Definition

The Global Water Pumps Market comprises a broad range of mechanical and electro-mechanical pumping systems designed for the movement, circulation, and pressurization of water across residential, agricultural, commercial, industrial, municipal, and infrastructure applications. The market includes centrifugal pumps (end-suction, split-case, multistage, vertical turbine, submersible), positive displacement pumps, booster systems, sewage & drainage pumps, solar pumps, smart pumps, and integrated pumping solutions.

Water pumps play a critical role in irrigation, groundwater extraction, municipal water supply, wastewater treatment, flood control, desalination, building services, industrial process water circulation, cooling systems, and fire protection systems. These systems are essential for ensuring water security, agricultural productivity, sanitation infrastructure, and industrial continuity.

Over the past two years, the global water pumps industry has been significantly influenced by infrastructure investments, urbanization, climate variability, rising energy efficiency regulations, groundwater depletion concerns, renewable-powered pumping expansion, and increasing adoption of smart monitoring technologies. Volatility in raw material prices (cast iron, stainless steel, copper, motors), supply chain constraints, and fluctuations in construction cycles have also shaped industry dynamics.

Market Insights

Global demand for water pumps has been strongly shaped by increasing urbanization, agricultural modernization, expansion of water and wastewater infrastructure, industrial growth, and rising focus on water reuse and desalination.

A key driver has been the global push toward energy-efficient pumping systems, supported by tightening motor efficiency standards (IE3/IE4), sustainability mandates, and rising electricity costs. The transition from conventional pumps to variable frequency drive (VFD)-integrated smart pumping systems has accelerated adoption across municipal and industrial sectors.

Between 2021–2023, fluctuations in steel, copper, motor components, and freight costs impacted pricing cycles and margins. However, by 2024–2025, improved supply chain normalization and higher infrastructure spending restored market momentum.

The industry is increasingly shaped by:

- Smart pumps with IoT-enabled monitoring

- Predictive maintenance systems

- Solar-powered irrigation pumps

- High-efficiency hydraulics and optimized impeller designs

- Modular and skid-mounted pumping systems

Industry projections indicate that the Global Water Pumps Market will grow at a steady CAGR of 6.18% between 2026 and 2035, supported by expanding irrigation coverage, wastewater treatment capacity upgrades, desalination investments, and rapid infrastructure growth in Asia-Pacific, the Middle East, and parts of Africa.

North America and Europe remain technology-driven markets focused on efficiency upgrades and replacement demand, while emerging markets are witnessing first-time installations and rapid penetration.

Market Dynamics: Drivers

The primary growth drivers include:

- Rising global water demand due to urbanization and population growth

- Agricultural mechanization and irrigation expansion

- Infrastructure modernization programs (smart cities, rural water schemes)

- Industrial process water management requirements

- Wastewater treatment and reuse mandates

- Increasing energy efficiency standards

- Growth in solar-powered and off-grid pumping solutions

- Climate variability and flood management investments

Government investments in water security, groundwater management policies, desalination projects, and rural electrification programs are significantly boosting pump demand in developing economies.

The increasing integration of digital monitoring, remote diagnostics, and automation in pumping systems is enhancing lifecycle value and driving premium product adoption.

Market Dynamics: Challenges

Despite strong demand fundamentals, the industry faces several challenges:

- Raw material price volatility (steel, castings, copper windings)

- Energy price fluctuations affecting operating costs

- Groundwater regulation restrictions in certain regions

- Intense competition from low-cost manufacturers

- Project execution delays in public infrastructure

- High initial CAPEX for large industrial pumping systems

- Supply chain dependencies for motors, VFDs, and electronics

Additionally, climate risks and water scarcity regulations can alter irrigation patterns, impacting demand in specific regions. Replacement cycles in mature markets also depend on capital expenditure budgets and infrastructure renewal timelines.

Market Segmentation

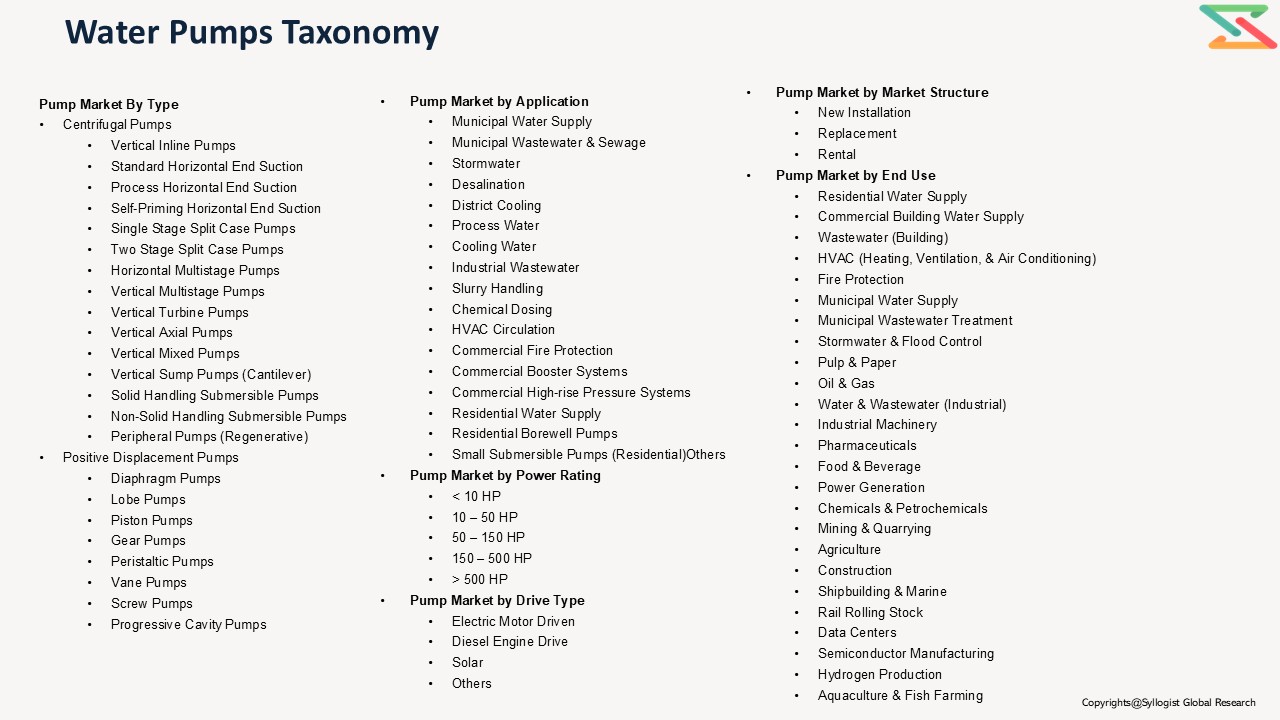

By Type

- Centrifugal Pumps

- Vertical Inline Pumps

- Standard Horizontal End Suction

- Process Horizontal End Suction

- Self-Priming Horizontal End Suction

- Single Stage Split Case Pumps

- Two Stage Split Case Pumps

- Horizontal Multistage Pumps

- Vertical Multistage Pumps

- Vertical Turbine Pumps

- Vertical Axial Pumps

- Vertical Mixed Pumps

- Vertical Sump Pumps (Cantilever)

- Solid Handling Submersible Pumps

- Non-Solid Handling Submersible Pumps

- Peripheral Pumps (Regenerative)

- Positive Displacement Pumps

- Diaphragm Pumps

- Lobe Pumps

- Piston Pumps

- Gear Pumps

- Peristaltic Pumps

- Vane Pumps

- Screw Pumps

- Progressive Cavity Pumps

By Application

- Municipal Water Supply

- Municipal Wastewater & Sewage

- Stormwater

- Desalination

- District Cooling

- Process Water

- Cooling Water

- Industrial Wastewater

- Slurry Handling

- Chemical Dosing

- HVAC Circulation

- Commercial Fire Protection

- Commercial Booster Systems

- Commercial High-rise Pressure Systems

- Residential Water Supply

- Residential Borewell Pumps

- Small Submersible Pumps (Residential)

- Others

By End Use

- Residential Water Supply

- Commercial Building Water Supply

- Wastewater (Building)

- HVAC (Heating, Ventilation, & Air Conditioning)

- Fire Protection

- Municipal Water Supply

- Municipal Wastewater Treatment

- Stormwater & Flood Control

- Pulp & Paper

- Oil & Gas

- Water & Wastewater (Industrial)

- Industrial Machinery

- Pharmaceuticals

- Food & Beverage

- Power Generation

- Chemicals & Petrochemicals

- Mining & Quarrying

- Agriculture

- Construction

- Shipbuilding & Marine

- Rail Rolling Stock

- Data Centers

- Semiconductor Manufacturing

- Hydrogen Production

- Aquaculture & Fish Farming

By Power Rating

- < 10 HP

- 10 – 50 HP

- 50 – 150 HP

- 150 – 500 HP

- > 500 HP

By Drive Type

- Electric Motor Driven

- Diesel Engine Drive

- Solar

- Others

By Market Structure

- New Installation

- Replacement

- Rental

All market revenues are presented in USD, with volumes expressed in million units.

Historical Year: 2021–2024

Base Year: 2025

Estimated Year: 2026

Forecast Period: 2027–2031

Key Questions this Study Will Answer

- What are the key market statistics and forecasts (market size by value & volume, product shares, efficiency trends) for the Global Water Pumps Market?

- What are the regional demand patterns, infrastructure investments, irrigation trends, and regulatory impacts shaping growth?

- How are energy efficiency mandates, smart pumping technologies, and digitalization transforming the industry?

- Who are the leading competitors, and how do they benchmark across product portfolio, capacity, regional presence, technology innovation, and pricing?

- What insights emerge from EPC contractor interviews, irrigation equipment distributors, municipal authorities, and industrial end-users conducted during the study?

- What are the white-space opportunities across solar pumps, desalination, wastewater reuse, and digital monitoring systems?

- Market Foundations & Dynamics

- Introduction

- Product Overview

- Value Chain Analysis

- Research Methodology

- Executive Summary

- Major Trends Shaping the Market

- Short-Term vs. Long-Term Opportunities

- Scenario Planning (Base, Optimistic, Conservative)

- Sensitivity Analysis

- Identification of Regional Growth Hotspots

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Introduction

- Market Ecosystem & Value Chain

- Overview of Value Chain Participants

- Raw Material Suppliers (Castings, Forgings, Motors, Seals, Bearings)

- Component Manufacturers (Impellers, Shafts, Casings)

- Motor & Drive Manufacturers (Electric Motors, VFDs, Controllers)

- Technology Providers (Hydraulics Design, IoT Monitoring, Efficiency Optimization)

- Distribution Channels (Dealers, EPC Contractors, OEM Direct Sales)

- Service & Aftermarket Providers

- Flow of Value & Material Through the Chain

- Value Addition & Margins at Each Stage

- Integration Trends (OEM Integration into Motors, Controls & Service)

- Impact of Vertical Integration

- Mapping of Roles & Interdependencies

- Market Trends & Developments

- White Space Analysis

- Demand Supply Analysis

- Demand–Supply Gaps (Capacity Constraints, Import Dependency)

- Unmet Needs (High-Efficiency Pumps, Corrosion-Resistant Materials)

- Risk Assessment Framework

- Political / Geopolitical Risk (Import Duties, Trade Policies)

- Operational Risk (Supply Chain Disruptions, Power Costs)

- Environmental Risk (Energy Efficiency Norms, Emission Standards)

- Financial Risk (Commodity Price Volatility, CAPEX Intensity)

- Regulatory Framework & Standards (Energy Efficiency, IS/ISO Standards)

- Regulatory & Standards Overview

- Energy Efficiency Regulations & Compliance

- Safety & Quality Standards

- Environmental Compliance Norms

- Local Country Regulations (Import Norms, Certification Requirements)

- Testing & Certification Requirements

- Technology Landscape

- Hydraulic Design Optimization

- Energy-Efficient Pump Technologies

- Automation & Smart Pumping Systems (IoT, SCADA Integration)

- Variable Frequency Drives (VFD) Integration

- Advanced Materials & Corrosion Protection

- Future Outlook (AI-Based Monitoring, Predictive Maintenance)

- Global Water Pumps Market Outlook

- Market Size by Value & Volume

- Market Size by Pump Type

- Centrifugal Pumps

- Vertical Inline Pumps

- Standard Horizontal End Suction

- Process Horizontal End Suction

- Self-Priming Horizontal End Suction

- Single Stage Split Case Pumps

- Two Stage Split Case Pumps

- Horizontal Multistage Pumps

- Vertical Multistage Pumps

- Vertical Turbine Pumps

- Vertical Axial Pumps

- Vertical Mixed Pumps

- Vertical Sump Pumps (Cantilever)

- Solid Handling Submersible Pumps

- Non-Solid Handling Submersible Pumps

- Peripheral Pumps (Regenerative)

- Positive Displacement Pumps

- Diaphragm Pumps

- Lobe Pumps

- Piston Pumps

- Gear Pumps

- Peristaltic Pumps

- Vane Pumps

- Screw Pumps

- Progressive Cavity Pumps

- Market Size by Application

- Municipal Water Supply

- Municipal Wastewater & Sewage

- Stormwater

- Desalination

- District Cooling

- Process Water

- Cooling Water

- Industrial Wastewater

- Slurry Handling

- Chemical Dosing

- HVAC Circulation

- Commercial Fire Protection

- Commercial Booster Systems

- Commercial High-rise Pressure Systems

- Residential Water Supply

- Residential Borewell Pumps

- Small Submersible Pumps (Residential)Others

- Market Share by End Use

- Residential Water Supply

- Commercial Building Water Supply

- Wastewater (Building)

- HVAC (Heating, Ventilation, & Air Conditioning)

- Fire Protection

- Municipal Water Supply

- Municipal Wastewater Treatment

- Stormwater & Flood Control

- Pulp & Paper

- Oil & Gas

- Water & Wastewater (Industrial)

- Industrial Machinery

- Pharmaceuticals

- Food & Beverage

- Power Generation

- Chemicals & Petrochemicals

- Mining & Quarrying

- Agriculture

- Construction

- Shipbuilding & Marine

- Rail Rolling Stock

- Data Centers

- Semiconductor Manufacturing

- Hydrogen Production

- Aquaculture & Fish Farming

- Market Share by Power Rating

- < 10 HP

- 10 – 50 HP

- 50 – 150 HP

- 150 – 500 HP

- > 500 HP

- Market Share by Drive Type

- Electric Motor Driven

- Diesel Engine Drive

- Solar

- Others

- Market Share by Market Structure

- New Installation

- Replacement

- Rental

- Centrifugal Pumps

- Regional Analysis (Similar detailed analysis as presented in Chapter 6 will be provided individually for all five regions)

- Country Analysis (Similar detailed analysis as presented in Chapter 6 will be provided individually for 50 countries)

- Pricing Analysis

- Overview of Pricing Structures (Per Unit, Per HP, Per System)

- Price Trends by Pump Type

- Historical and Forecast Pricing

- Factors Influencing Price

- Raw Material Availability

- Energy Costs

- Logistics

- Regulatory Burden

- R&D & Certification Costs

- Regional Pricing Differentiation

- Cost Structure & Margin Analysis

- Detailed Cost Breakdown (Castings, Motors, Assembly, Testing)

- Average Cost per Stage

- Profitability & Margin Distribution

- Sensitivity Analysis (Steel Prices, Copper Prices, Energy Costs)

- Cost Reduction Opportunities (Localization, Automation, Design Optimization)

- Competition Outlook

- Market Concentration vs Fragmentation

- Company Market Shares

- Competitive Strategies

- Capacity Expansion

- Product Diversification

- Service & Aftermarket Expansion

- Technology Collaborations

- Benchmarking Matrix (Technology vs Price vs Service Network)

- Recent Developments (M&A, New Plants, Partnerships)

- Business Models & Strategic Insights

- Integrated Pump Manufacturers

- EPC-Focused Manufacturers

- Dealer-Driven Distribution Models

- Service & AMC-Driven Models

- SWOT of Leading Business Models

- Sales & Distribution Channel Analysis

- GTM Channels (Dealers, EPCs, Direct Industrial Sales)

- Channel Share by Region

- Typical Channel Flow Diagram (Manufacturer → Distributor → Contractor → End User)

- Sales Process & Customer Engagement

- Distribution Strategy of Leading Players

- Emerging Trends (Digital Sales, Predictive Service Contracts)

- Strategic Recommendations & Roadmap

- Competitor Strategic Initiatives

- Future Outlook (2024–2029)

- Strategic Recommendations for Stakeholders

- Adoption Roadmap for High-Efficiency Pumps

- Tailored Recommendations (OEMs, EPCs, Utilities, Industrial Buyers)

- Key Success Factors (Efficiency, Service Depth, Cost Competitiveness)