Global Robotic Warehouse Automation Market By Robot Type, By Technology, By Function, By Warehouse Type, By End Use Industry, By Region, Competition, Forecast & Opportunities, 2021-2036F

Market Definition

The Global Robotic Warehouse Automation Market encompasses the design, manufacture, integration, and operation of robotic hardware, software, and AI systems deployed within warehouse and distribution center environments to automate goods receiving, storage, order picking, sorting, packing, and dispatch operations, including autonomous mobile robots, goods-to-person robotic storage and retrieval systems, articulated robotic picking arms, automated guided vehicles, robotic palletizing and depalletizing systems, sortation robots, and associated warehouse management software, procured by e-commerce operators, third-party logistics providers, retailers, manufacturers, and food and beverage distributors globally.

Market Insights

The global robotic warehouse automation market is experiencing a sustained investment acceleration that is fundamentally transforming the operational architecture, workforce model, and competitive differentiation calculus of warehouse and distribution center operations across virtually every major supply chain intensive industry, as the combination of persistent labor market tightness in warehouse locations, escalating order fulfillment speed expectations from e-commerce consumers, and demonstrable return on investment evidence from early adopter automation deployments creates a convergent set of investment drivers that are broadening robotic automation adoption from the largest logistics network operators toward mid-market warehousing, regional distribution, and specialized storage operations. The market was valued at approximately USD 28.6 billion in 2025 and is projected to expand at a compound annual growth rate of 16.8% through 2034, as the technology maturity of autonomous mobile robots, AI-powered robotic picking, and goods-to-person retrieval systems continues improving order picking accuracy, throughput consistency, and operational uptime performance toward benchmarks that justify large-scale warehouse automation investment across a broader range of facility types, throughput volumes, and SKU complexity profiles than first-generation automation solutions could address.

Autonomous mobile robot systems deployed in goods-to-person order fulfillment configurations represent the largest and fastest-growing technology category within the robotic warehouse automation market, having established their commercial dominance in e-commerce and omnichannel retail distribution center environments where their combination of rapid deployment without structural facility modification, flexible task reassignment capability, incremental scalability through fleet size expansion, and demonstrated fifty to seventy percent improvement in picker productivity relative to manual goods-to-person walking operations create compelling return on investment cases that warehouse operators across multiple industries are acting upon at increasing scale. The goods-to-person architecture enabled by autonomous mobile robots and robotic storage and retrieval systems is simultaneously improving inventory accuracy, reducing order cycle time variability, decreasing picking error rates, and improving warehouse space utilization through high-density storage configurations that physical human access constraints previously made impractical in large-scale distribution environments.

AI-powered robotic piece picking, which deploys articulated robot arms equipped with advanced computer vision, tactile sensing, and machine learning-based grasp planning to autonomously pick individual items from totes, shelves, and conveyors for order fulfillment, is advancing from early commercial deployment in controlled SKU environments toward broader applicability across diverse product types, irregular packaging formats, and high-variety fashion, grocery, and pharmaceutical picking applications that were previously beyond the reliable grasp capability of first-generation picking robots. The improvement of robotic picking system capability to handle the product variety and packaging format diversity characteristic of general merchandise and grocery order fulfillment is expanding the addressable automation opportunity from the structured SKU environments of pharmaceuticals, spare parts, and standardized consumer goods toward the full range of warehouse order picking tasks that currently represent the largest labor cost and operational bottleneck in distribution center operations globally. Food and beverage distribution is emerging as a high-priority automation investment category, driven by the combination of cold storage labor challenges, food safety compliance requirements, and high-throughput case picking volume economics that make automated case handling and palletizing systems particularly compelling for ambient and chilled food distribution operations.

North America is the largest regional market for robotic warehouse automation, reflecting the high labor costs of United States and Canadian warehouse markets, the scale of e-commerce fulfillment network investment by major retail and marketplace operators, the maturity of the warehouse automation technology vendor and systems integrator ecosystem, and the active deployment programs of major third-party logistics providers investing in automation to improve service capability and cost competitiveness across their distribution network footprints. Europe represents the second largest regional market, characterized by high labor cost environments in Germany, the Netherlands, France, and Scandinavia that create strong economic justification for warehouse automation investment, a sophisticated food and consumer goods supply chain infrastructure requiring high throughput automation, and a growing regulatory focus on warehouse worker ergonomics that incentivizes automated solutions for physically demanding manual handling tasks. Asia-Pacific is the fastest-growing regional market, anchored by the massive warehouse automation investment programs of Chinese e-commerce platforms, the rapidly expanding automation adoption of Japanese food and pharmaceutical distributors, and the growing third-party logistics automation investment across South Korea, Australia, and Southeast Asian markets.

Key Drivers

Structural Warehouse Labor Shortages, Rising Wage Costs, and High Workforce Turnover Compelling Sustained Investment in Robotic Automation as the Scalable Alternative to Labor-Dependent Operations

Persistent labor shortages across warehouse and distribution center operations in North America, Europe, and parts of Asia-Pacific, driven by declining working-age population growth, competition from higher-wage service sector employers, and the physically demanding and repetitive nature of warehouse picking and packing tasks that generates high voluntary attrition rates, are compelling logistics operators to invest in robotic automation as the only operationally scalable and financially sustainable long-term response to workforce availability and cost challenges that wage increases and recruitment incentives alone cannot structurally resolve. The compound impact of annual warehouse labor wage inflation, recruitment and training cost accumulation from high turnover, and the operational throughput variability of human-staffed operations during peak demand periods is accelerating the payback period calculations for warehouse automation investment across a growing range of facility sizes and throughput volumes.

E-Commerce Growth and Omnichannel Fulfillment Complexity Driving Warehouse Throughput, Speed, and Accuracy Requirements That Systematically Exceed Human-Operated Fulfillment Capabilities

The sustained growth of e-commerce order volumes, the proliferation of SKU counts across online assortments, and the shortening of expected delivery windows from two-day to same-day that major marketplace and direct-to-consumer operators are progressively implementing are collectively imposing warehouse throughput, order accuracy, and operational consistency requirements that human-staffed order picking operations cannot reliably achieve at scale during peak demand periods without automation support. The simultaneous management of direct-to-consumer unit picking, retail store replenishment case picking, and marketplace order fulfillment from shared omnichannel distribution infrastructure creates operational complexity and demand variability that robotic automation systems handle with greater consistency and scalability than the manual workforce sizing and scheduling flexibility available to warehouse operators managing seasonal and promotional demand surges.

AI and Computer Vision Technology Maturation Expanding Robotic Picking Capability to Diverse Product Types and Accelerating Deployment Feasibility Across Previously Unautomatable Warehouse Tasks

Progressive advances in deep learning-based computer vision, 3D object recognition, tactile force feedback sensing, and AI grasp planning algorithms are systematically expanding the range of product types, packaging formats, and pick-from configurations that robotic picking systems can handle reliably at commercial production speeds, reducing the SKU complexity and product variety constraints that previously limited robotic picking deployment to structured environments with controlled product presentation and limited format variability. The improvement of robotic picking system capability to learn new product types rapidly through few-shot learning and self-supervised training approaches is accelerating deployment feasibility assessment timelines for warehouse operators evaluating automation across diverse product catalogs, reducing the integration cost and timeline barriers that had constrained broader adoption beyond specialized picking applications in pharmaceuticals, spare parts, and standardized consumer goods categories.

Key Challenges

High Capital Investment Requirements and Long Payback Periods for Full Warehouse Automation Programs Creating Adoption Barriers Among Mid-Market and Smaller Distribution Operators

Comprehensive warehouse automation programs encompassing autonomous mobile robot fleets, goods-to-person storage and retrieval systems, robotic picking stations, automated conveyor and sortation infrastructure, and integrated warehouse management software represent capital investments that can reach tens or hundreds of millions of dollars for large distribution center deployments, creating financial access barriers for mid-market and regional logistics operators whose capital budgets, financing capacity, and multi-year payback requirements restrict automation investment to incremental robotics additions rather than transformative full-facility automation architectures. The concentration of warehouse automation return on investment justification in high-volume, high-throughput facilities means that smaller facilities with lower order volumes and less predictable demand patterns face less favorable automation economics that extend payback periods beyond the investment horizon preferences of cost-of-capital-constrained operators.

System Integration Complexity, WMS Compatibility Requirements, and Extended Implementation Timelines Creating Operational Risk and Productivity Disruption During Automation Transition Periods

Deploying robotic warehouse automation within operational distribution environments requires deep integration with existing warehouse management systems, enterprise resource planning platforms, transportation management systems, and order management interfaces whose varying data standards, API architectures, and operational logic create substantial systems integration complexity that extends implementation timelines, introduces operational disruption risk during transition periods, and generates customization costs that can materially elevate total automation program investment above capital equipment purchase prices. The challenge of maintaining continuous warehouse throughput and order fulfillment service levels during the commissioning, testing, and operational handover phases of large automation deployments requires careful phasing planning, parallel operation of manual and automated processes, and intensive technical resource commitment that creates implementation risk for operators whose operational continuity obligations during the transition period limit the pace and scale of automation cutover.

Robotic System Flexibility Limitations and Difficulty Handling Unstructured Environments, Damaged Packaging, and Unexpected Product Presentation Scenarios Constraining Autonomous Operation Reliability

Robotic warehouse automation systems are engineered for optimal performance within defined operational parameters encompassing expected product presentation formats, packaging condition standards, conveyance configurations, and environmental conditions, and their operational reliability degrades when encountering scenarios outside design envelopes including severely damaged packaging, novel product types not present in training datasets, unusual stacking configurations, foreign object contamination, or environmental variations such as lighting fluctuation, temperature extremes, and floor surface irregularities that affect robot navigation and sensing performance. The residual requirement for human exception handling of edge cases, system recovery from robot faults, and maintenance oversight of automated equipment means that fully autonomous warehouse operation without human staffing remains an aspirational rather than operationally achievable objective at current technology maturity levels for most product variety and operational complexity profiles.

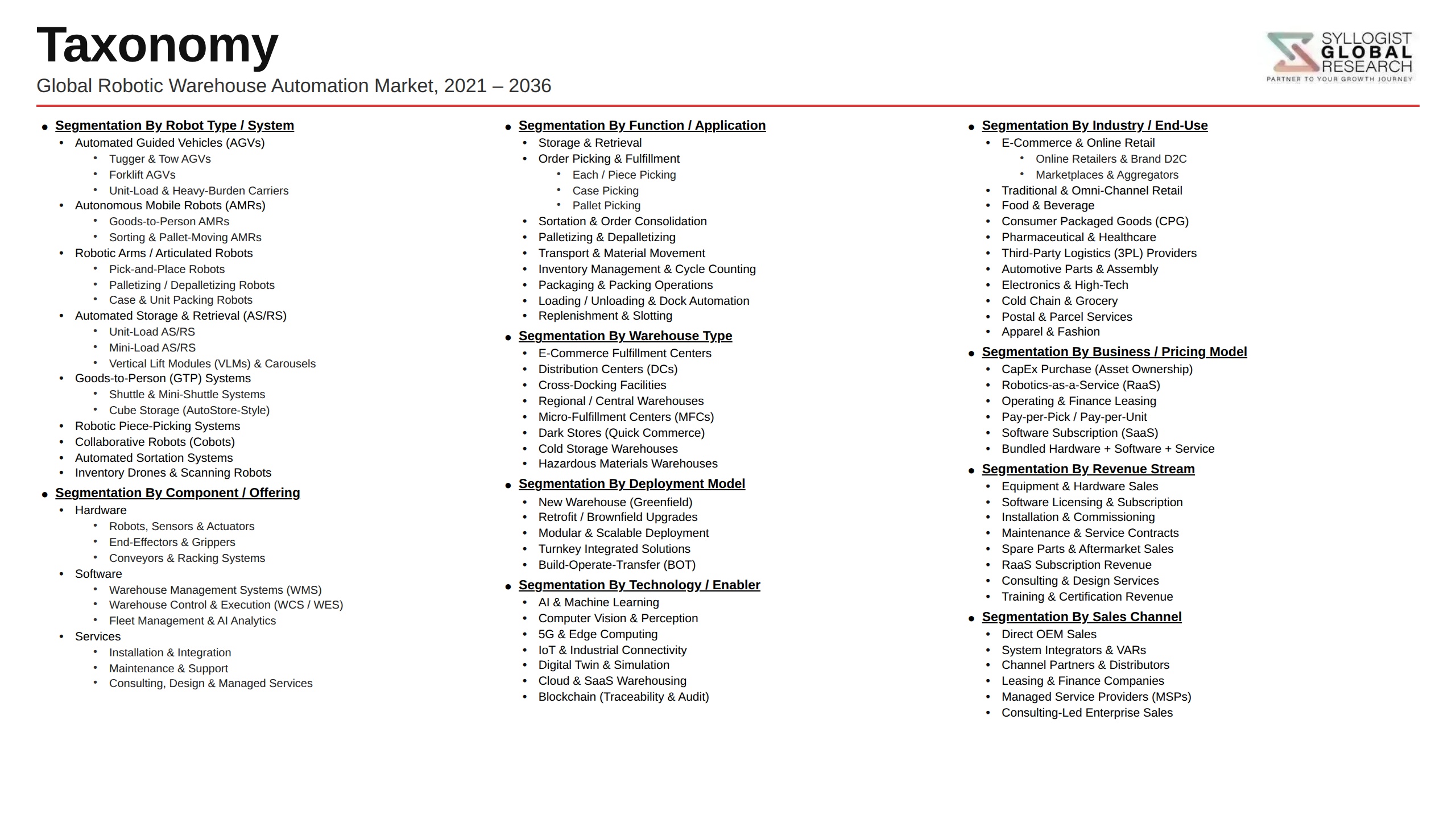

Market Segmentation

- Segmentation By Robot Type

- Autonomous Mobile Robots and Automated Guided Vehicles

- Goods-to-Person Robotic Storage and Retrieval Systems

- Robotic Picking and Piece-Picking Arms

- Robotic Palletizing and Depalletizing Systems

- Sortation and Cross-Belt Robots

- Robotic Packing and Void-Fill Systems

- Others

- Segmentation By Technology

- AI and Computer Vision-Guided Picking Systems

- SLAM-Based Robot Navigation and Mapping

- Goods-to-Person Shuttle and Crane Systems

- Conveyor, Sorter, and Material Handling Automation

- Warehouse Management and Robot Fleet Software

- IoT Sensors and Real-Time Location Systems

- Others

- Segmentation By Function

- Receiving and Inbound Sortation

- Storage and Inventory Management

- Order Picking and Fulfillment

- Packing and Dispatch Preparation

- Returns Processing and Restocking

- Yard Management and Loading Automation

- Others

- Segmentation By Warehouse Type

- E-Commerce and Omnichannel Fulfillment Centers

- Third-Party Logistics Distribution Warehouses

- Grocery and Cold Chain Distribution Centers

- Pharmaceutical and Healthcare Warehouses

- Manufacturing Inbound and Finished Goods Warehouses

- Retail Store Replenishment Distribution Centers

- Others

- Segmentation By End Use Industry

- E-Commerce and Online Retail

- Food, Grocery, and Beverage Distribution

- Third-Party Logistics and Contract Logistics

- Pharmaceutical and Healthcare

- Fashion and Apparel

- Automotive and Industrial Parts

- Consumer Electronics

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global robotic warehouse automation market valuation in 2025, projected through 2034, segmented by robot type, function, and end use industry, enabling automation technology vendors, systems integrators, logistics operators, and investors to identify the highest-growth robotic systems categories and most commercially significant warehouse automation adoption opportunities across the global market?

- How are autonomous mobile robot goods-to-person picking systems, AI-powered piece picking robots, and robotic palletizing and sortation systems comparing in terms of deployment maturity, addressable application breadth, return on investment performance, and total cost of ownership across e-commerce, grocery, pharmaceutical, and general merchandise distribution center environments at different throughput scales?

- Which warehouse automation application segments, specifically e-commerce fulfillment order picking, grocery cold chain automation, pharmaceutical dispensing, returns processing, and case picking for retail replenishment, are generating the highest capital investment volumes and fastest adoption growth through 2034, and what operational performance improvements and labor cost reduction outcomes are commercially deployed systems achieving in verified installations?

- How is the competitive landscape structured among autonomous mobile robot platform developers, goods-to-person system vendors, robotic picking technology providers, and full warehouse automation systems integrators, and what technology differentiation, software platform development, systems integration capability, fleet management service, and customer reference ecosystem strategies are enabling leading vendors to win large enterprise automation programs?

- What capital cost barriers, systems integration complexity challenges, warehouse management system compatibility requirements, and implementation timeline risks are most significantly constraining warehouse automation adoption among mid-market and regional distribution operators, and what modular deployment architectures, Robotics-as-a-Service financing models, and standardized integration frameworks are vendors and operators developing to lower adoption barriers for smaller facilities?

- How are AI computer vision advances, few-shot product learning capabilities, improved grasp planning algorithms, and multi-modal sensing technologies expanding the range of product types, packaging formats, and pick-from configurations addressable by robotic picking systems, and what capability milestones are required for robotic piece picking to achieve reliable autonomous performance across the full SKU variety of general merchandise and grocery distribution environments?

- Which regional robotic warehouse automation markets, specifically North America, Europe, and Asia-Pacific, are expected to generate the highest incremental investment growth through 2034, and what combinations of warehouse labor cost levels, e-commerce fulfillment volume growth, food and pharmaceutical distribution automation investment, third-party logistics sector automation programs, and domestic automation technology ecosystem development are defining regional market growth trajectories and competitive dynamics?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- High Upfront Capital Cost, Long Payback Period & ROI Uncertainty Risk

- System Integration Complexity, Legacy WMS Incompatibility & Implementation Delay Risk

- Robot Downtime, Component Failure & Operational Disruption Risk

- Cybersecurity, Connected Fleet Vulnerability & Data Breach Risk

- Workforce Displacement, Change Management & Reskilling Cost Risk

- Technology Obsolescence, Rapid Innovation Cycle & Platform Lock-In Risk

- Regulatory Framework & Standards

- ISO 3691-4, ANSI/ITSDF B56.5 & Safety Standards for Industrial Automated Guided Vehicles & AMRs

- ISO 10218, ISO/TS 15066 & Collaborative Robot Safety Standards for Warehouse Cobot Deployments

- EU Machinery Regulation (2023/1230), CE Marking & Type Approval Standards for Warehouse Automation Equipment

- OSHA 1910.217, ANSI/RIA R15.06 & US Warehouse Robot & Automated Machinery Safety Regulatory Frameworks

- IEC 62443, NIST Cybersecurity Framework & Industrial IoT Security Standards for Connected Warehouse Systems

- Fire Safety, Sprinkler System & Building Code Standards for High-Bay Automated Storage & Retrieval Facilities

- Global Robotic Warehouse Automation Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Number of Robot Units & Automated Systems Deployed)

- Market Size & Forecast by System Type

- Autonomous Mobile Robots (AMRs) & Goods-to-Person (GTP) Systems

- Automated Guided Vehicles (AGVs) & Laser-Guided Tugger Trains

- Automated Storage & Retrieval Systems (AS/RS): Unit Load, Mini-Load & Shuttle Systems

- Goods-to-Person Piece-Picking Robots (Robotic Arms & Gantry Picking Systems)

- Robotic Palletising & Depalletising Systems

- Robotic Sortation Systems (Crossbelt, Pop-Up Wheel & Bomb Bay Sorters)

- Collaborative Robots (Cobots) for Pick-Assist, Packing & Intralogistics

- Automated Conveyor, Accumulation & Tilt-Tray Sortation Systems

- Robotic Put-Walls, Pocket Sorters & Batch-Pick Fulfilment Systems

- Warehouse Management System (WMS) & Fleet Orchestration Software

- Market Size & Forecast by Technology

- AI, Machine Learning & Computer Vision-Enabled Warehouse Robots

- SLAM-Based Navigation, LiDAR & 3D Sensor Technology for AMR & AGV Guidance

- Robotic Grasping, Bin-Picking & Dexterous Manipulation Technology

- Digital Twin & Simulation Technology for Warehouse Automation Design & Optimisation

- IoT, Edge Computing & Real-Time Data Analytics for Warehouse Fleet Management

- Cloud-Based WMS, API Integration & ERP Connectivity Platforms

- Market Size & Forecast by Warehouse Function

- Inbound Receiving, Unloading & Depalletising Automation

- Storage, Slotting & Automated Inventory Management

- Order Picking, Piece Picking & Batch Fulfilment Automation

- Sorting, Routing & Divert Automation

- Packing, Void Fill & Label Application Automation

- Outbound Palletising, Loading & Despatch Automation

- Returns Processing & Reverse Logistics Automation

- Market Size & Forecast by Deployment Type

- Greenfield Automated Warehouse & Fulfilment Centre

- Brownfield Retrofit & Partial Automation of Existing Facilities

- Micro-Fulfilment Centre (MFC) & Dark Store Automation

- Robotics-as-a-Service (RaaS) Flexible Deployment Model

- Market Size & Forecast by Application

- E-Commerce & Omnichannel Retail Fulfilment

- Grocery, Food & Beverage Distribution & Fulfilment

- Third-Party Logistics (3PL) & Contract Logistics

- Pharmaceutical, Healthcare & Cold Chain Warehousing

- Automotive Parts & Manufacturing Component Distribution

- Apparel, Fashion & Footwear Fulfilment

- Industrial, Building Materials & Heavy Goods Distribution

- Market Size & Forecast by End-User

- E-Commerce Retailers & Online Marketplaces

- Brick-and-Mortar Retailers & Grocery Chains

- Third-Party Logistics (3PL) & Freight Forwarders

- Manufacturers & Industrial Distributors

- Pharmaceutical & Healthcare Distributors

- Postal & Parcel Carrier Operators

- Market Size & Forecast by Sales Channel

- Direct OEM & Robot Manufacturer Sales

- System Integrator & Turnkey Automation Project Channel

- Robotics-as-a-Service (RaaS) & Subscription Channel

- Value-Added Reseller, Distributor & Channel Partner

- North America Robotic Warehouse Automation Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Robot Units & Automated Systems Deployed)

- By System Type

- By Technology

- By Warehouse Function

- By Deployment Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Robotic Warehouse Automation Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Robot Units & Automated Systems Deployed)

- By System Type

- By Technology

- By Warehouse Function

- By Deployment Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Robotic Warehouse Automation Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Robot Units & Automated Systems Deployed)

- By System Type

- By Technology

- By Warehouse Function

- By Deployment Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Robotic Warehouse Automation Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Robot Units & Automated Systems Deployed)

- By System Type

- By Technology

- By Warehouse Function

- By Deployment Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Robotic Warehouse Automation Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Robot Units & Automated Systems Deployed)

- By System Type

- By Technology

- By Warehouse Function

- By Deployment Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Robotic Warehouse Automation Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Robot Units & Automated Systems Deployed)

- By System Type

- By Technology

- By Warehouse Function

- By Deployment Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Germany, France, United Kingdom, Netherlands, Sweden, Denmark, Spain, Italy, Japan, China, South Korea, Australia, Singapore, India, Brazil, Mexico, Saudi Arabia, UAE, South Africa

- Technology Landscape & Innovation Analysis

- AMR Goods-to-Person Technology Deep-Dive: Shelf-Carrying, Tote-Lifting & Drive-Under Architectures, Fleet Density & Pick Rate Benchmarking

- Robotic Piece-Picking Technology: Suction Cup, Multi-Fingered Gripper, Soft Robotic Hand & AI Vision-Guided Bin-Picking Advances

- AS/RS Shuttle Technology: Single-Level, Multi-Level, Cube Storage (Autostore) & Vertical Lift Module (VLM) Comparison

- AI Warehouse Management, Task Orchestration & Multi-Robot Fleet Coordination Technology

- Humanoid & Bipedal Warehouse Robot Technology: Emergence, Capability Assessment & Commercial Readiness Timeline

- Digital Twin & Physics Simulation Technology for Warehouse Automation Design, Commissioning & Ongoing Optimisation

- Voice, Wearable & Vision Picking Technology as Hybrid Human-Robot Workflow Augmentation

- Patent & IP Landscape in Robotic Warehouse Automation Technologies

- Value Chain & Supply Chain Analysis

- Robot Hardware: Actuator, Motor, LiDAR Sensor, Camera & Structural Component Manufacturing Supply Chain

- Conveyor, Sorter, Racking, Shelving & Mechanical System Manufacturing Supply Chain

- Computing, Edge AI, Vision System & Electronics Supply Chain for Warehouse Robots

- WMS, Fleet Management & Warehouse Orchestration Software Development Supply Chain

- System Integration, Site Engineering, Civil Works & Facility Preparation Supply Chain

- Commissioning, Testing, Training & Go-Live Support Supply Chain

- Field Service, Preventive Maintenance, Spare Parts & Aftermarket Support Channel

- Pricing Analysis

- Robotic Warehouse Automation System Capital Cost (Capex) Analysis by System Type & Deployment Scale

- AMR & AS/RS Total Cost of Ownership (TCO): Hardware, Software, Maintenance & Integration Cost Breakdown

- ROI & Payback Period Analysis: Labour Saving, Throughput Gain & Error Reduction Value Analysis

- RaaS Subscription Pricing vs. Outright Purchase Cost Comparison for Robotic Warehouse Systems

- System Integration, WMS Licence & Ongoing Software Support Cost Structure Analysis

- Price Trend Analysis: Impact of Robot Hardware Cost Reduction, AI Commoditisation & Scale Economics

- Sustainability & Environmental Analysis

- Energy Consumption of Automated Warehouses vs. Conventional Operations: PUE, HVAC & Lighting Reduction Analysis

- Battery Technology, Charging Infrastructure & Energy Efficiency of AMR & AGV Fleet Operations

- Warehouse Space Optimisation, Building Footprint Reduction & Sustainable Site Design Enabled by Automation

- Workforce Safety Improvement, Ergonomic Injury Reduction & Human-Robot Collaboration Wellbeing Standards

- ESG Reporting, Responsible Automation & Circular Economy for Warehouse Robot Hardware

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by System Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by System Type, Application & Geography

- Player Classification

- Integrated Warehouse Automation System Providers (Full-Suite, AS/RS & Turnkey)

- Specialist AMR & Goods-to-Person Robot Manufacturers

- Robotic Piece-Picking & Bin-Picking System Specialists

- Conveyor, Sorter & Mechanical Material Handling System Specialists

- WMS, Fleet Orchestration & Warehouse Software Platform Providers

- System Integrators & Automation Project Delivery Specialists

- Competitive Analysis Frameworks

- Market Share Analysis by System Type, Application & Region

- Company Profile

- Company Overview & Headquarters

- Robotic Warehouse Automation Products & System Portfolio

- Key Customer Relationships & Reference Warehouse Deployments

- Manufacturing Footprint & Production Capacity

- Revenue (Warehouse Automation Segment) & Order Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Project Wins, Product Launches, Capacity Expansion)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Breadth vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By System Type, Warehouse Function, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing, Integration Capability & Operational Excellence Strategy

- Geographic Expansion & Vertical Market Entry Strategy

- Customer, End-User & System Integrator Engagement Strategy

- Partnership, M&A & Warehouse Automation Ecosystem Strategy

- Sustainability, Energy Efficiency & Responsible Automation Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output