India Servers Market By Server Type, By Component, By Processor Architecture, By Form Factor, By End Use Industry, By Deployment Model, By Region, Competition, Forecast & Opportunities, 2021-2036F

Market Definition

The India Servers Market encompasses the procurement, deployment, and management of rack-mount, tower, blade, and high-density server systems incorporating central processing units, graphics processing units, memory, storage, and networking components, utilized for enterprise data processing, cloud computing infrastructure, artificial intelligence training and inference, high-performance computing, web hosting, database management, telecommunications network functions, and edge computing applications across commercial, government, financial, telecommunications, and technology sector organizations operating within India.

Market Insights

The India servers market is entering a period of structurally elevated growth, driven by the simultaneous acceleration of hyperscale data center investment by global and domestic cloud service providers, the rapid scaling of artificial intelligence infrastructure procurement by technology enterprises and government digital initiatives, the ongoing digitalization of Indian banking, financial services, manufacturing, and public sector organizations, and India’s emergence as a strategically preferred data center destination for multinational corporations diversifying their Asia-Pacific cloud infrastructure footprint. The market was valued at approximately USD 4.2 billion in 2025 and is projected to expand at a compound annual growth rate of 16.3% through 2034, as India’s digital economy transformation, sovereign artificial intelligence ambitions, and its growing role as a global technology services hub collectively generate server infrastructure investment requirements at a scale and pace that the market has not previously experienced across its development trajectory.

The hyperscale and cloud segment is the most powerful growth engine within the India servers market, as global hyperscale operators including Amazon Web Services, Microsoft Azure, and Google Cloud have committed to substantial multi-year data center capacity expansion programs across Indian metros, driven by the scale of India’s enterprise cloud adoption market, data localization regulatory requirements mandating in-country data processing for sensitive financial and personal information, and India’s attractiveness as a low-latency serving location for the rapidly growing Southeast Asian digital economy. Domestic cloud service providers are simultaneously expanding their data center footprints to capture enterprise cloud migration demand from Indian mid-market and public sector organizations that prefer locally operated infrastructure for compliance, latency, and data sovereignty reasons, reinforcing server procurement volumes across both hyperscale and commercial data center operator customer segments.

Artificial intelligence infrastructure investment is reshaping the composition of India’s server procurement market at an accelerating pace, as technology companies, financial institutions, telecommunications operators, and government agencies invest in graphics processing unit-dense AI training clusters and inference server deployments to develop and deploy large language models, computer vision systems, fraud detection platforms, and enterprise AI applications tailored to Indian language, regulatory, and business context requirements. The Indian government’s IndiaAI mission, which encompasses a national AI compute infrastructure program targeting the deployment of a substantial sovereign graphics processing unit cluster accessible to Indian startups, research institutions, and government agencies, is directly generating public sector server procurement demand while simultaneously stimulating private sector AI infrastructure investment by establishing the national policy framework and co-investment commitments that underpin India’s AI capability development ambitions. The growing concentration of global capability centers and technology delivery centers in India, operated by multinational corporations managing enterprise infrastructure for their global operations from Indian locations, is further expanding the installed server base across hyper-urban technology corridor locations in Bangalore, Hyderabad, Pune, Chennai, and the National Capital Region.

Maharashtra and the Mumbai Metropolitan Region, Karnataka centered on Bangalore, and Telangana centered on Hyderabad collectively account for the dominant share of India’s data center server infrastructure by installed capacity, supported by reliable power supply, strong fiber connectivity infrastructure, concentration of technology sector enterprise customers, and established ecosystems of data center operators, systems integrators, and technology service providers. Chennai and the National Capital Region are registering accelerating data center investment that is progressively expanding geographic distribution of server infrastructure beyond the traditional western and southern India concentration. Tier-2 cities including Pune, Ahmedabad, Kolkata, and Kochi are attracting growing data center investment driven by lower land and power costs, improving connectivity infrastructure, and government industrial policy incentives supporting data center development outside established metro locations.

Key Drivers

Hyperscale Data Center Capacity Expansion and Global Cloud Provider Infrastructure Investment Establishing India as a Priority Asia-Pacific Server Procurement Market

Committed capital expenditure by global hyperscale operators for India data center expansion, combined with growing domestic cloud service provider capacity investment, is establishing a structurally elevated and multi-year server procurement cycle that represents a qualitative shift in India’s server market scale relative to its historical trajectory. Data localization mandates under India’s Digital Personal Data Protection Act, Reserve Bank of India requirements for financial data storage within India, and regulatory frameworks governing health data, telecommunications records, and government data processing are reinforcing hyperscale and enterprise infrastructure investment by compelling multinational corporations and regulated industry operators to maintain in-country server infrastructure for compliance purposes, expanding the non-discretionary component of India server procurement beyond growth-driven capacity expansion alone.

National Artificial Intelligence Policy Ambitions and Enterprise AI Adoption Creating Rapidly Expanding Demand for GPU-Dense Server Infrastructure and High-Performance Computing Capacity Across India

India’s government-backed IndiaAI mission, private technology sector artificial intelligence investment, and the rapid adoption of AI-powered applications across banking, financial services, telecommunications, e-commerce, and healthcare industries are generating procurement demand for graphics processing unit-equipped servers and high-performance computing infrastructure that is transforming the composition of India’s server market toward higher average unit values and more compute-intensive configurations. The strategic imperative for India to develop sovereign artificial intelligence capabilities in Indian languages, cultural contexts, and domain-specific knowledge areas is motivating public sector AI compute infrastructure investment that supplements private sector demand, while the commercial AI services opportunity accessible to India’s large technology services industry is incentivizing enterprise investment in AI training and inference server infrastructure at an accelerating pace.

Digital India Transformation, Banking Sector Technology Modernization, and 5G Network Infrastructure Rollout Generating Broad-Based Enterprise and Telecommunications Server Procurement Growth

The ongoing digital transformation of India’s banking and financial services sector, driven by Reserve Bank of India technology investment mandates, competitive pressure from digital-native payment and lending platforms, and the expansion of financial inclusion through technology-enabled services reaching previously unbanked populations, is generating sustained server infrastructure investment among private and public sector banks, non-banking financial companies, insurance providers, and payment processors upgrading their core banking systems, fraud detection platforms, and customer-facing digital application infrastructure. Simultaneously, the nationwide 5G network deployment by Reliance Jio, Bharti Airtel, and Vodafone Idea is driving substantial telecommunications sector server procurement for radio access network virtualization, mobile edge computing nodes, and network function virtualization infrastructure that replaces proprietary telecommunications hardware with software-defined workloads running on commodity server platforms.

Key Challenges

Power Infrastructure Reliability Constraints and High Commercial Electricity Tariffs Elevating Data Center Operating Costs and Complicating Large-Scale Server Infrastructure Deployment Across Indian Locations

Despite significant improvements in grid infrastructure quality across major Indian cities, power supply reliability, power quality consistency, and commercial electricity tariff competitiveness remain material challenges for data center operators deploying large-scale server infrastructure across Indian locations, where grid outage frequency, voltage fluctuation sensitivity of high-density server equipment, and electricity costs substantially exceeding those of competing data center locations in Singapore, Malaysia, and the United Arab Emirates constrain the economics of server infrastructure deployment relative to regional alternative locations. The substantial capital expenditure required for uninterruptible power supply systems, diesel generator backup capacity, and power conditioning infrastructure to maintain the continuous availability standards required by hyperscale and enterprise data center operations adds significant cost that reduces the economic attractiveness of Indian data center locations for cost-sensitive server deployment programs.

Import Duty Structures on Server Hardware and Component Supply Chain Concentration Elevating Procurement Costs and Extending Delivery Lead Times for Indian Enterprise and Data Center Customers

India’s import duty structure on server hardware, components, and associated equipment increases the landed cost of server systems procured by Indian enterprises and data center operators relative to customers in duty-exempt or lower-tariff jurisdictions, reducing the purchasing power of capital budgets allocated to server infrastructure investment and creating cost competitiveness challenges for India-based service delivery relative to offshore locations. The geographic concentration of server manufacturing and component production in Taiwan, China, and Southeast Asia creates supply chain vulnerability and extended delivery lead time exposure that complicates capacity planning for rapidly scaling data center operators and enterprise technology teams managing server refresh cycles against accelerating digital transformation program timelines that cannot accommodate supply chain disruption delays.

Shortage of Specialized Data Center Engineering Talent and Advanced Server Infrastructure Management Expertise Constraining the Operational Efficiency of India’s Rapidly Expanding Server Deployment Base

The rapid expansion of India’s data center server infrastructure is outpacing the development of the specialized engineering workforce required for data center design, server infrastructure deployment, hyperscale operations management, and advanced server performance optimization, creating talent scarcity in critical roles including data center mechanical and electrical engineering, server hardware reliability engineering, storage and networking infrastructure management, and cloud infrastructure operations that extends project timelines, elevates personnel costs, and limits the operational sophistication achievable at newly commissioned data center facilities. The concentration of available data center engineering expertise in established technology corridor cities is further constraining the pace at which server infrastructure can be deployed and professionally operated in emerging tier-2 data center markets where talent availability is more limited.

Market Segmentation

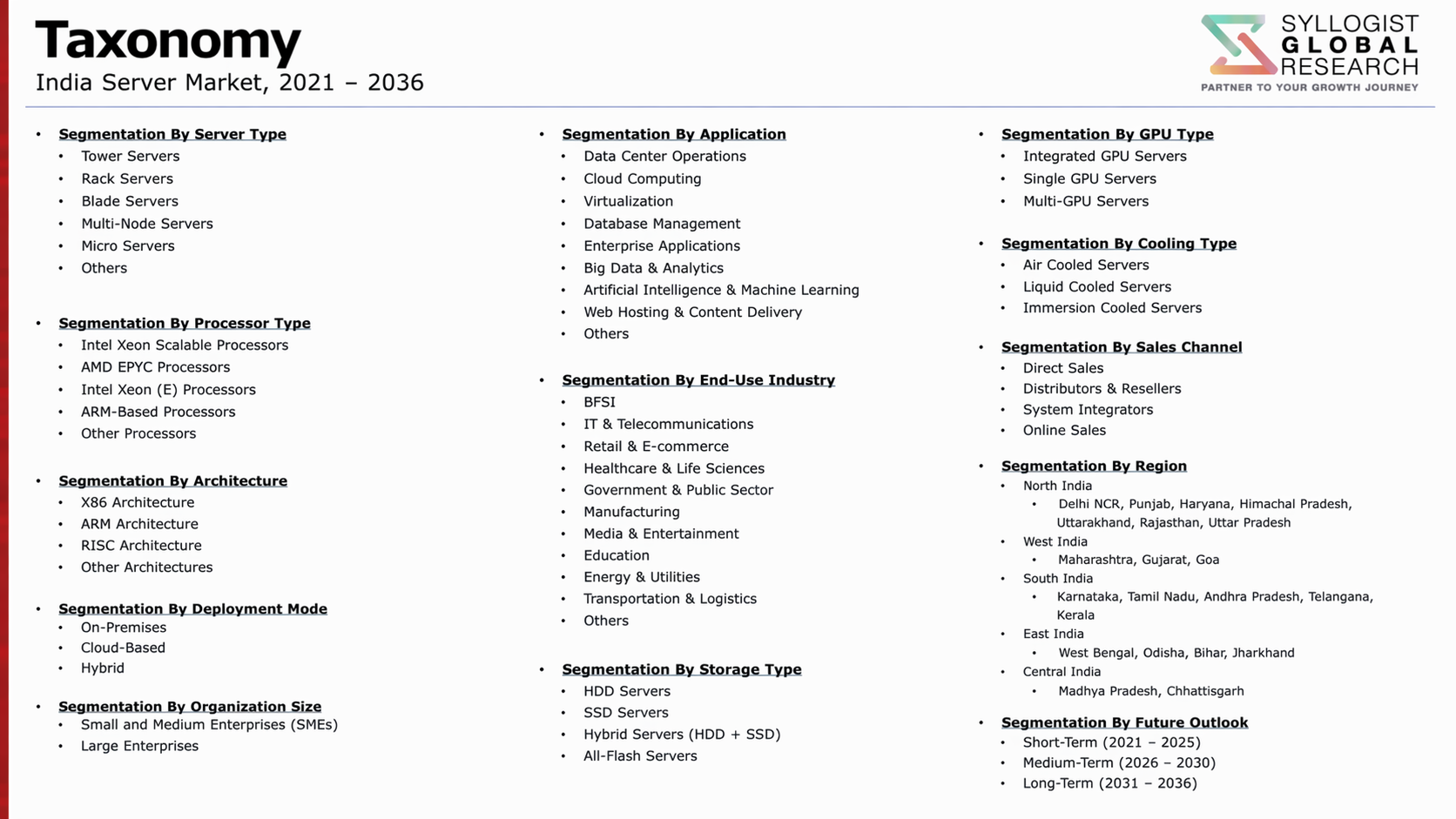

- Segmentation By Server Type

- Tower Servers

- Rack-Mount Servers

- Blade Servers

- High-Density and Hyperscale Servers

- GPU-Accelerated AI and HPC Servers

- Edge Servers

- Others

- Segmentation By Component

- Central Processing Units and Server Processors

- Graphics Processing Units and AI Accelerators

- Server Memory and RAM

- Server Storage (SSD, HDD, NVMe)

- Networking and Interface Cards

- Power Supply and Cooling Systems

- Others

- Segmentation By Processor Architecture

- x86 Architecture Servers

- ARM Architecture Servers

- RISC and SPARC Architecture Servers

- Others

- Segmentation By Form Factor

- 1U and 2U Rack Servers

- 4U and Above High-Density Rack Servers

- Blade Server Chassis and Modules

- Tower and Pedestal Form Factors

- Micro and Ultra-Dense Form Factors

- Segmentation By End Use Industry

- Banking, Financial Services, and Insurance

- Information Technology and Technology Services

- Telecommunications and Network Operators

- Government and Public Sector

- Healthcare and Life Sciences

- Retail and E-Commerce

- Manufacturing and Industrial

- Education and Research

- Others

- Segmentation By Deployment Model

- On-Premises Enterprise Data Centers

- Colocation and Third-Party Data Centers

- Hyperscale Cloud Provider Data Centers

- Edge and Distributed Computing Deployments

- Government and Sovereign Cloud Infrastructure

- Segmentation By Region

- North India (National Capital Region, Uttar Pradesh)

- West India (Maharashtra, Gujarat)

- South India (Karnataka, Telangana, Tamil Nadu)

- East India (West Bengal, Odisha)

- Central India

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total India servers market valuation in 2025, projected through 2034, segmented by server type, component, and end use industry, enabling server manufacturers, systems integrators, and technology investors to identify the highest-growth product configurations and most durable procurement demand opportunities across India’s rapidly expanding server infrastructure landscape?

- How are global hyperscale operator data center expansion commitments, domestic cloud service provider capacity investment, and data localization regulatory requirements collectively shaping the scale, geographic distribution, and server configuration preferences of India’s hyperscale and commercial data center server procurement market through 2034?

- What role is the Indian government’s IndiaAI mission, combined with private technology sector AI investment and enterprise AI application adoption across banking, telecommunications, and e-commerce, playing in accelerating GPU-accelerated server procurement and reshaping the average unit value and configuration complexity of India’s server market composition through 2034?

- How is the competitive landscape structured among global server original equipment manufacturers, domestic systems integrators, and white-box server assemblers competing for India server procurement, and what localization investment, channel partnership, service capability development, and government procurement qualification strategies are enabling suppliers to capture share across hyperscale, enterprise, and public sector customer segments?

- What power infrastructure reliability challenges, commercial electricity tariff competitiveness constraints, import duty cost impacts, and component supply chain lead time risks are most significantly affecting the economics and deployment pace of large-scale server infrastructure investment in India, and what mitigation strategies are data center operators and enterprise technology teams employing to manage these structural market constraints?

- Which emerging tier-2 data center markets including Pune, Ahmedabad, Chennai, Kolkata, and Kochi are expected to generate the most significant incremental server infrastructure investment through 2034, and what combinations of land cost advantages, government incentive programs, improving power and connectivity infrastructure, and enterprise customer proximity are driving data center development and server procurement activity in each location?

- How are the 5G network virtualization rollout, banking sector core technology modernization programs, digital government infrastructure expansion under Digital India initiatives, and the growth of global capability centers in India collectively shaping enterprise and telecommunications sector server procurement priorities, refresh cycle timelines, and technology specification requirements across the forecast period through 2034?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Import Dependency, Foreign Exchange Volatility & Customs Duty Escalation Risk for Server Hardware

- Power Infrastructure Reliability, Grid Stability & Cooling Cost Risk for Indian Data Centres

- Cybersecurity, Data Localisation Compliance & IT Act Regulatory Risk

- Skilled Talent Availability, Data Centre Operations Expertise & Workforce Retention Risk

- Technology Obsolescence, AI Workload Transition & Rapid Server Refresh Cycle Risk

- Regulatory Framework & Standards

- Digital Personal Data Protection (DPDP) Act 2023, Data Localisation Policy & IT Act Compliance for Server Infrastructure

- MeitY Data Centre Policy Framework, National Data Centre & Cloud Policy & Government Cloud (GI Cloud) Standards

- BIS Compulsory Registration Order (CRO), Quality Control Orders & STQC Certification for IT & Server Hardware

- Make in India, PLI Scheme for IT Hardware & Domestic Server Manufacturing Incentive Frameworks

- Energy Conservation Building Code (ECBC), Bureau of Energy Efficiency (BEE) & Green Data Centre Standards

- E-Waste Management Rules, EPR Framework & RoHS-Equivalent Standards for Server Hardware in India

- India Server Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Units Shipped)

- Market Size & Forecast by Server Type

- Rack Servers

- Tower Servers

- Blade Servers

- High-Density & Micro Servers

- Modular & Composable Infrastructure Servers

- GPU Servers & AI Accelerated Computing Platforms

- Edge Servers & Ruggedised Edge Computing Platforms

- High-Performance Computing (HPC) & Research Computing Nodes

- Arm-Based & Alternative Architecture Servers

- Market Size & Forecast by Processor Architecture

- x86 (Intel Xeon & AMD EPYC) Processor-Based Servers

- Arm-Based (Ampere, AWS Graviton & Nvidia Grace) Processor Servers

- GPU-Accelerated (Nvidia H-Series, AMD Instinct & Intel Gaudi) Server Platforms

- FPGA-Accelerated & SmartNIC-Integrated Server Platforms

- Custom ASIC & Domain-Specific Accelerator Server Platforms

- Market Size & Forecast by Memory & Storage Configuration

- DDR4 DRAM Memory-Based Servers

- DDR5 & HBM (High Bandwidth Memory) Servers

- NVMe SSD & All-Flash Storage Servers

- CXL (Compute Express Link) Memory-Pooling & Composable Memory Servers

- Market Size & Forecast by Deployment Model

- On-Premises Enterprise & Corporate Data Centre Servers

- Hyperscale & Cloud Service Provider (CSP) Data Centre Servers

- Colocation & Third-Party Data Centre Hosted Servers

- Government & NIC Data Centre Servers

- Edge & Near-Edge Deployment Servers

- Market Size & Forecast by Application

- AI Training & Inference Workloads

- Cloud Computing, Virtualisation & Software-Defined Infrastructure

- Enterprise Applications (ERP, CRM, Databases & Business Intelligence)

- High-Performance Computing (HPC), Research & Simulation

- Big Data Analytics, Data Warehousing & Data Lakehouse Workloads

- Telecom Network Function Virtualisation (NFV) & 5G Core Infrastructure

- Edge Computing, IoT Data Processing & Real-Time Analytics

- Storage, Backup & Disaster Recovery Infrastructure

- E-Governance, Digital India & Public Sector IT Infrastructure

- Market Size & Forecast by End-User

- Hyperscale Cloud Service Providers & Internet Companies

- BFSI (Banking, Financial Services & Insurance)

- IT & IT-Enabled Services (ITeS) & Software Companies

- Government & Public Sector Organisations

- Telecommunications & Network Operators

- Manufacturing, Automotive & Industrial Companies

- Healthcare, Pharma & Life Sciences Organisations

- Education, Research Institutions & National Laboratories

- Retail, E-Commerce & Media Companies

- Small & Medium-Sized Enterprises (SMEs)

- Market Size & Forecast by Sales Channel

- Direct OEM & Server Manufacturer Sales

- National Distributor & Value-Added Reseller (VAR) Channel

- Systems Integrator & Managed Service Provider (MSP) Channel

- Government Procurement (GeM Portal, NICSI & DGS&D Tender) Channel

- Online & E-Commerce Channel

- Domestically Assembled & Make in India Server Channel

- North India Server Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Shipped)

- By Server Type

- By Processor Architecture

- By Deployment Model

- By Application

- By End-User

- By State

- By Sales Channel

- Market Size & Forecast

- South India Server Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Shipped)

- By Server Type

- By Processor Architecture

- By Deployment Model

- By Application

- By End-User

- By State

- By Sales Channel

- Market Size & Forecast

- West India Server Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Shipped)

- By Server Type

- By Processor Architecture

- By Deployment Model

- By Application

- By End-User

- By State

- By Sales Channel

- Market Size & Forecast

- East India Server Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Shipped)

- By Server Type

- By Processor Architecture

- By Deployment Model

- By Application

- By End-User

- By State

- By Sales Channel

- Market Size & Forecast

- Central India Server Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Shipped)

- By Server Type

- By Processor Architecture

- By Deployment Model

- By Application

- By End-User

- By State

- By Sales Channel

- Market Size & Forecast

- State-Wise* India Server Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Shipped)

- By Server Type

- By Processor Architecture

- By Deployment Model

- By Application

- By End-User

- By State

- By Sales Channel

- Market Size & Forecast

- *States & Union Territories Analyzed in the Syllogist India Research Portfolio: Maharashtra, Delhi NCT, Karnataka, Tamil Nadu, Telangana, Gujarat, Uttar Pradesh, West Bengal, Andhra Pradesh, Rajasthan, Haryana, Kerala, Madhya Pradesh, Punjab, Odisha

- Technology Landscape & Innovation Analysis

- AI Server & GPU Cluster Technology Adoption in India: Hyperscaler Build-Out, National AI Mission & Enterprise AI Infrastructure

- Next-Generation Processor Technology Adoption in India: Intel Xeon 6, AMD EPYC Turin & Arm-Based Server Roadmaps

- India Data Centre Cooling Technology: Air Cooling, Liquid Cooling & Free Cooling Adoption in Tropical Climate Conditions

- Open Compute Project (OCP) & ODM White-Box Server Adoption by Indian Hyperscalers & Large Enterprises

- Edge Computing Server Technology: Deployment Models for India’s Smart Cities, 5G Rollout & Rural Connectivity

- Make in India Server Assembly & Domestic Manufacturing Technology: PLI-Driven Local Production Capabilities

- Hybrid Cloud & HCI (Hyper-Converged Infrastructure) Technology Adoption in Indian Enterprises

- Patent & IP Landscape in Server Technologies Relevant to India

- Value Chain & Supply Chain Analysis

- Global Server Component Import Supply Chain: Processors, DRAM, NAND & Key Hardware Components Sourced for India

- Domestic Server Assembly, System Integration & PLI-Incentivised Manufacturing Supply Chain

- PCB, Motherboard, Power Supply & Chassis Local Sourcing & Import Dependency Analysis

- Data Centre Infrastructure: UPS, PDU, Cooling & Rack Equipment Supply Chain in India

- National Distributor, Regional VAR & Tier-2 City Reseller Supply Chain

- Systems Integrator, MSP & Government Channel Supply Chain

- Aftermarket Support, AMC, Spare Parts & Warranty Service Supply Chain

- Pricing Analysis

- Average Selling Price (ASP) Analysis by Server Type & Processor Architecture in India

- Impact of Import Duties, GST & Currency Fluctuation on India Server Pricing

- AI GPU Server & HPC Node Pricing vs. Equivalent Cloud Infrastructure Cost Analysis in India

- On-Premises vs. Cloud vs. Colocation Total Cost of Ownership (TCO) Comparison for Indian Enterprises

- Government & Public Sector Server Procurement Pricing: GeM Rates, L1 Tender Dynamics & Rate Contract Analysis

- Domestically Assembled vs. Imported Server Price Premium & PLI Incentive Impact Analysis

- Sustainability & Environmental Analysis

- India Data Centre Energy Consumption, Power Usage Effectiveness (PUE) Benchmarking & Energy Efficiency Standards

- Renewable Energy Procurement for Indian Data Centres: Solar, Wind PPA & REC Frameworks

- Water Consumption & Cooling Water Management in Indian Data Centres: Challenges of Hot & Humid Climate Conditions

- E-Waste Management Rules 2022, Extended Producer Responsibility (EPR) & Server Hardware Disposal in India

- Green Data Centre Certification (IGBC, GRIHA & BEE Star Rating) & Sustainable IT Infrastructure in India

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Server Type & Segment)

- Top 10 Players Market Share in India

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Server Type, Application & Region

- Player Classification

- Global OEM Server Brands with India Sales & Support Operations

- Domestic & India-Assembled Server Manufacturers (PLI & Make in India Players)

- AI & GPU Server Specialist Providers in India

- National Systems Integrators & IT Infrastructure Solution Providers

- Regional Distributors, VARs & Channel Partners Serving Indian Markets

- Managed Service Providers (MSPs) & Colocation Operators in India

- Competitive Analysis Frameworks

- Market Share Analysis by Server Type, Application & Region in India

- Company Profile

- Company Overview & India Operations Headquarters

- Server Products & Technology Portfolio Available in India

- Key Customer Relationships & Reference Deployments in India

- India Manufacturing, Assembly & Service Footprint

- India Revenue (Server Segment) & Order Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, Channel Agreements & M&A Activity in India

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches in India)

- SWOT Analysis

- Strategic Focus Areas & India Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration in India)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Server Type, Processor Architecture, Application, End-User & Region

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy for India

- Manufacturing, Localisation & PLI Strategy for India

- Geographic Expansion & Tier-2/Tier-3 City Penetration Strategy

- Customer & End-User Engagement Strategy for India

- Channel, Partnership & Ecosystem Strategy for India

- Government & Public Sector Engagement Strategy

- Sustainability & Green IT Strategy for India

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output