Market Definition

The Global Space Manufacturing and Orbital Infrastructure Market encompasses the design, development, fabrication, deployment, and commercial operation of space-based manufacturing facilities, orbital platforms, in-space assembly systems, satellite servicing infrastructure, commercial space stations, orbital transfer vehicles, and associated on-orbit and terrestrial support services. The market includes microgravity materials processing, on-orbit fabrication of pharmaceutical and advanced material products, in-space propellant depots, orbital debris remediation systems, and commercial habitat modules procured by national space agencies, commercial operators, defense establishments, pharmaceutical developers, and advanced materials manufacturers globally.

Market Insights

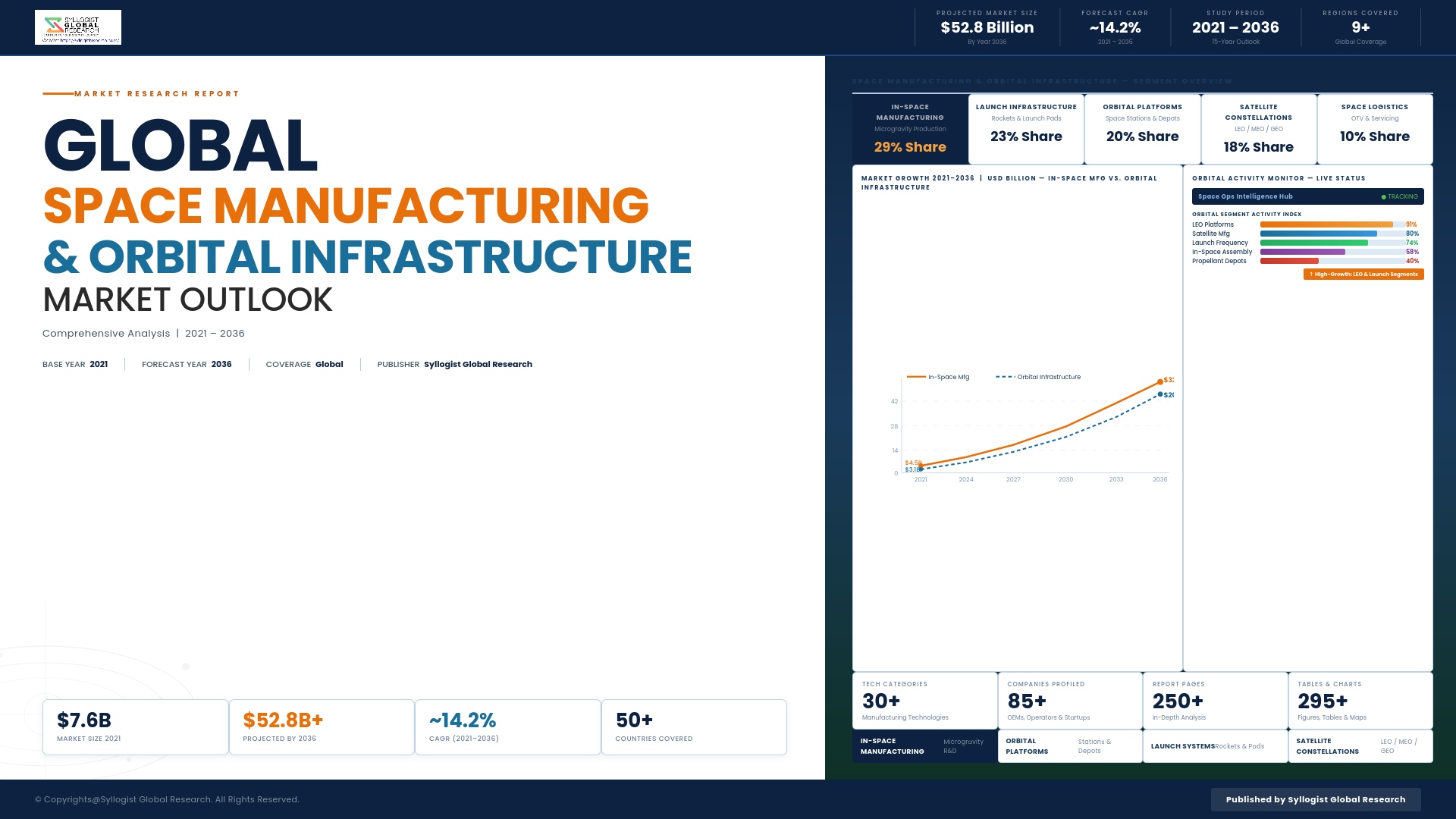

The global space manufacturing and orbital infrastructure market is entering an unprecedented phase of commercial expansion, propelled by declining launch costs, maturing in-space propulsion technologies, growing governmental and private investment in sustained orbital presence, and the emergence of viable commercial use cases for microgravity manufacturing across pharmaceuticals, semiconductor fabrication, and advanced materials synthesis. The market was valued at approximately USD 5.8 billion in 2025 and is projected to reach USD 31.4 billion by 2034, advancing at a compound annual growth rate of 20.6% through the forecast period, as orbital manufacturing transitions from experimental demonstration to commercially scalable operations underpinned by reusable launch systems, autonomous in-orbit assembly architectures, and expanding commercial space station programs.

The structural foundation supporting this growth rests on the convergence of three enabling transitions: the dramatic reduction in orbital access costs achieved through reusable launch vehicle development, the maturation of robotic in-space assembly and servicing capabilities, and validated commercial demand for pharmaceutical protein crystals, fiber optic preforms, and semiconductor structures manufactured in microgravity conditions that cannot be replicated in terrestrial production environments. These transitions collectively redefine orbital manufacturing from a government-funded scientific endeavor into a commercially self-sustaining industrial activity with defensible economic returns across multiple product categories. National space agency investment remains a critical demand anchor, with programs in the United States, Europe, Japan, China, and India allocating substantial funding to orbital infrastructure development encompassing next-generation space stations, in-space transportation architectures, and lunar gateway platforms that create durable multi-year procurement pipelines for orbital platform developers, launch service providers, and on-orbit servicing operators.

The commercial sector is simultaneously accelerating investment in orbital manufacturing facilities, propellant depot infrastructure, and satellite servicing platforms, with venture capital and strategic corporate financing flowing into in-space manufacturing ventures and commercial space station developers at a pace reflecting growing investor confidence in near-term revenue generation from orbital industrial operations. Asia-Pacific is projected to record the highest regional compound annual growth rate through 2034, driven by China’s space station expansion and commercial orbital manufacturing programs, India’s emerging launch and orbital services sector, and Japan’s investment in in-space assembly and servicing technologies. North America maintains its position as the largest absolute revenue contributor, anchored by commercial station transition programs, defense orbital infrastructure procurement, and the leading concentration of private space manufacturing ventures globally. Europe represents the third major regional market, with coordinated agency and national programs across Germany, France, Italy, and Luxembourg accelerating investment in orbital manufacturing and in-space transportation capabilities.

Key Drivers

Declining Launch Costs and Reusable Vehicle Economics Unlocking Commercial Viability of Orbital Manufacturing at Scale

The dramatic reduction in payload delivery costs to low Earth orbit achieved through reusable launch vehicle development has fundamentally transformed the commercial economics of orbital manufacturing and infrastructure deployment, reducing the per-kilogram launch cost barrier that previously confined space manufacturing to government-funded scientific programs and enabling commercial operators to develop financially viable business cases for orbital pharmaceutical production, advanced materials synthesis, and in-space infrastructure. Continued vehicle reuse improvements and increasing launch cadence across multiple competing providers are expected to sustain this cost reduction trajectory through the forecast period, further expanding the addressable commercial market for orbital manufacturing facilities and infrastructure platforms beyond historically accessible segments.

Validated Commercial Demand for Microgravity-Derived Products in Pharmaceutical and Advanced Materials Applications Generating Durable Revenue Incentives for Orbital Investment

The confirmation of commercially viable demand for pharmaceutical protein crystals, fiber optic preforms, and semiconductor structures whose quality characteristics in microgravity manufacturing conditions materially exceed terrestrially produced equivalents is generating durable revenue incentives for orbital manufacturing investment, providing the commercial foundation necessary to attract institutional capital beyond government-funded research programs. Clinical validation of superior pharmaceutical products manufactured in microgravity, combined with early commercial agreements between orbital platform operators and life sciences developers, is establishing revenue-generating precedent that is reshaping investor risk assessment of commercial space manufacturing and accelerating private capital deployment into orbital manufacturing infrastructure at commercially meaningful scale.

Government Space Station Transition Programs and Commercial Orbital Infrastructure Procurement Creating Foundational Demand Across the Orbital Services Value Chain

The planned transition from the International Space Station to commercially operated successors, supported by dedicated national agency funding commitments, is establishing a government-backed commercial orbital infrastructure market that provides the anchor tenancy and procurement revenue streams necessary to justify the capital expenditure of commercial space station construction and long-duration operation. These transition programs create multi-billion dollar procurement opportunities across habitat modules, life support systems, power generation infrastructure, in-space transportation, and on-orbit servicing capabilities, generating sustained demand across the orbital infrastructure supply chain while simultaneously providing the operational framework within which commercial manufacturing, research, and crew habitation activities can scale toward sustained economic viability.

Key Challenges

Extreme Capital Expenditure Requirements and Extended Payback Timelines Constraining Commercial Investment in Orbital Manufacturing Infrastructure

The development, launch, and commissioning of orbital manufacturing facilities and commercial space stations requires capital expenditure of a scale and risk profile that substantially exceeds conventional infrastructure project financing norms, with extended payback timelines, technology risk, and regulatory uncertainty creating significant barriers to institutional debt and equity financing outside government-backed programs. The absence of established insurance frameworks for on-orbit manufacturing assets, combined with the technical complexity of maintaining continuous operational capability across multi-year deployment horizons in the space environment, constrains the pool of commercially viable project sponsors and limits the pace of private capital deployment into orbital manufacturing infrastructure relative to the market projected growth trajectory.

In-Space Regulatory Governance Gaps, Orbital Debris Liability Frameworks, and Spectrum Allocation Constraints Complicating Commercial Orbital Operations

The absence of comprehensive international regulatory frameworks governing commercial manufacturing activities in orbit, combined with unresolved liability allocation for orbital debris generated by commercial platforms and intensifying competition for spectrum and orbital slot resources, creates compliance complexity and operational risk that complicates commercial orbital infrastructure development and imposes regulatory uncertainty on investment decisions spanning multi-decade asset lifecycles. National licensing frameworks for commercial space activities vary substantially across jurisdictions, creating fragmented regulatory environments for multinational orbital manufacturing ventures, while the accelerating proliferation of satellites in low Earth orbit intensifies congestion risks and collision probability for orbital manufacturing platforms operating in increasingly contested altitude bands.

Technological Maturity Gaps in Autonomous In-Space Assembly, On-Orbit Manufacturing Process Control, and Long-Duration Life Support Engineering Limiting Commercial Scalability

The commercial scalability of orbital manufacturing and infrastructure operations is constrained by limited maturity of autonomous in-space assembly systems, on-orbit process control for precision manufacturing applications, closed-loop life support engineering for extended commercial crew habitation, and in-space propellant transfer technologies that are prerequisite capabilities for economically viable orbital industrial operations at commercially meaningful scale. The transition from government-operated research platforms employing highly trained crews to commercially operated manufacturing facilities requiring reliable, cost-efficient, and largely autonomous operational performance demands technology readiness levels that current in-space systems have not consistently demonstrated outside controlled research environments, creating a commercialization gap that limits near-term revenue generation relative to market projections.

Market Segmentation

- Segmentation By Manufacturing Type

- Pharmaceutical and Biopharmaceutical Manufacturing

- Advanced Materials and Fiber Optics Production

- Semiconductor and Electronics Fabrication

- Additive Manufacturing and In-Orbit 3D Printing

- Others

- Segmentation By Orbital Segment

- Low Earth Orbit (LEO) Platforms and Facilities

- Medium Earth Orbit (MEO) Infrastructure

- Geostationary and Geosynchronous Orbit (GEO) Platforms

- Cislunar and Lunar Orbit Infrastructure

- Others

- Segmentation By Platform

- Commercial Space Stations and Habitat Modules

- Free-Flying Manufacturing Modules

- Satellite Servicing and Propellant Refueling Depots

- Orbital Transfer Vehicles and Space Tugs

- In-Space Assembly and Construction Platforms

- Others

- Segmentation By Application

- Pharmaceutical and Life Sciences Manufacturing

- Advanced Materials and Specialty Chemicals Synthesis

- Space Infrastructure Assembly and Maintenance

- Satellite Servicing and Life Extension

- Scientific Research and Technology Demonstration

- Commercial Habitation and Space Tourism

- Others

- Segmentation By Component

- Manufacturing Process Equipment and Bioreactors

- Habitat and Closed-Loop Life Support Systems

- Power Generation and Distribution Systems

- Propulsion and Orbital Maneuvering Systems

- Robotics and Autonomous Assembly Systems

- Communications and Data Management Systems

- Others

- Segmentation By End User

- National Space Agencies

- Commercial Space Station Operators

- Pharmaceutical and Life Sciences Companies

- Advanced Materials and Electronics Manufacturers

- Defense and Intelligence Organizations

- Academic and Research Institutions

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Space Manufacturing and Orbital Infrastructure Market in 2025, projected through 2034, disaggregated by manufacturing type and orbital segment, enabling investors, commercial operators, and government procurement planners to identify highest-growth segments and most durable revenue opportunities across the evolving orbital industrial landscape?

- How are national space agencies and commercial operators structuring investment across pharmaceutical manufacturing, advanced materials synthesis, and space infrastructure assembly applications, and which orbital platform categories are defining the technical and commercial benchmarks shaping global space manufacturing market architecture through 2034?

- What regulatory, liability, and orbital debris governance frameworks are shaping commercial orbital infrastructure development timelines, and how are leading platform developers managing compliance complexity across multiple jurisdictions while maintaining investment certainty necessary to justify capital commitments with multi-decade payback horizons?

- Which orbital manufacturing platform segments, including commercial space stations, free-flying modules, and satellite servicing depots, are generating the highest growth rates through 2034, and what in-space assembly, propulsion, and process control technologies are most critical to commercial performance leadership in each platform category?

- How is the competitive landscape structured among launch service providers, orbital platform developers, in-space manufacturing ventures, and satellite servicing operators, and what partnership, acquisition, and anchor tenancy strategies are enabling new entrants to secure commercial viability against established contractors in the orbital infrastructure market?

- What are the most significant technology readiness gaps affecting commercial scalability of orbital manufacturing operations, and how are platform developers and government programs addressing autonomous assembly, on-orbit process control, and life support engineering challenges within commercial deployment and certification frameworks?

- Which regional space markets, specifically Asia-Pacific, North America, and Europe, are expected to generate the most substantial incremental orbital infrastructure investment through 2034, and what governmental, commercial, and industrial base factors are driving capability development priorities and supplier selection in each regional market?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Launch Failure, Orbital Debris Collision & In-Space Infrastructure Loss Risk

- Sovereign Regulation, Space Traffic Management & Orbital Slot Allocation Risk

- Dual-Use Technology, Export Control (ITAR/EAR) & Militarisation of Space Risk

- Technology Maturity, In-Space Assembly Complexity & Long-Duration Operational Reliability Risk

- Financing, Long Gestation Period, Revenue Uncertainty & Stranded Asset Risk in Orbital Infrastructure

- Regulatory Framework & Standards

- Outer Space Treaty, Moon Agreement & International Space Law Framework Governing In-Space Manufacturing & Orbital Infrastructure

- National Space Legislation, Commercial Space Launch Authorisation & Orbital Slot Licensing Regulations

- Space Traffic Management (STM), Conjunction Analysis & Active Debris Removal Regulatory Frameworks

- Export Control Regimes: ITAR, EAR & Wassenaar Arrangement Provisions for Space Manufacturing Technology

- Space Sustainability Guidelines: UN COPUOS, ITU Frequency Coordination & Long-Term Sustainability of Outer Space Activities Framework

- Global Space Manufacturing & Orbital Infrastructure Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Number of Platforms, Facilities & Orbital Assets Deployed)

- Market Size & Forecast by Infrastructure Type

- Commercial Space Stations & Crewed Orbital Habitats

- In-Space Manufacturing Facilities & Microgravity Processing Platforms

- On-Orbit Servicing, Assembly & Manufacturing (OSAM) Platforms

- Orbital Logistics Hubs, Propellant Depots & In-Space Transfer Nodes

- Space-Based Solar Power (SBSP) Generation & Transmission Infrastructure

- Lunar Gateway, Cislunar Infrastructure & Deep Space Staging Nodes

- On-Orbit 3D Printing, Fabrication & Structural Assembly Facilities

- Space Debris Removal, Active Debris Mitigation & Orbital Remediation Infrastructure

- Reusable Launch Vehicle (RLV) Ground Support & Orbital Return Infrastructure

- Market Size & Forecast by Technology

- Microgravity-Enabled Materials Processing, Crystal Growth & Additive Manufacturing Technology

- On-Orbit Robotics, Autonomous Assembly & Rendezvous and Proximity Operations (RPO) Technology

- Closed-Loop Life Support, Regenerative Environmental Control & Habitat Technology

- Space-Based Solar Power (SBSP) Photovoltaic Array, Wireless Power Transmission & Rectenna Technology

- In-Situ Resource Utilisation (ISRU), Propellant Production & Orbital Refuelling Technology

- Cryogenic Propellant Storage, Long-Duration Space Logistics & In-Space Transportation Technology

- Advanced Materials: Radiation-Hardened, Ultra-Lightweight Structural & Smart Materials for Orbital Environments

- AI, Digital Twin, Autonomous Operations & Mission Management Technology for Orbital Infrastructure

- Market Size & Forecast by Orbit Type

- Low Earth Orbit (LEO)

- Medium Earth Orbit (MEO)

- Geostationary Earth Orbit (GEO)

- Highly Elliptical Orbit (HEO)

- Cislunar & Lunar Orbit

- Interplanetary & Deep Space

- Market Size & Forecast by Manufacturing Output

- Pharmaceutical & Biological Products Manufactured in Microgravity

- Advanced Semiconductor, Optical Fibre & Crystal Products

- Structural Components & In-Space Fabricated Satellite Parts

- Propellant & In-Space Resource Derived Materials

- Energy (Space-Based Solar Power Transmitted to Earth)

- Market Size & Forecast by Application

- Commercial Space Station Operations & Microgravity Research

- Satellite Servicing, Life Extension & On-Orbit Refuelling

- Space-Based Manufacturing & High-Value Product Production

- Space-Based Solar Power Generation & Terrestrial Energy Transmission

- Cislunar & Lunar Surface Infrastructure Support

- Space Tourism, Crew Transportation & Commercial Habitation

- Space Debris Remediation & Orbital Environment Management

- Market Size & Forecast by End-User

- Government Space Agencies & National Defense Organisations

- Commercial Satellite Operators & Space Services Providers

- Pharmaceutical, Biotechnology & Life Sciences Companies

- Advanced Materials, Semiconductor & Industrial Manufacturing Companies

- Energy Companies & Space-Based Solar Power Developers

- Space Tourism & Commercial Spaceflight Operators

- Market Size & Forecast by Sales Channel

- Government Contract, Cost-Plus Program & National Space Agency Procurement

- Commercial Launch & Space Services Contract

- Public-Private Partnership (PPP) & NASA/ESA Commercial Development Programs

- Direct Commercial Development, Private Investment & Venture-Backed Space Ventures

- North America Space Manufacturing & Orbital Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Platforms, Facilities & Orbital Assets Deployed)

- By Infrastructure Type

- By Technology

- By Orbit Type

- By Manufacturing Output

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Space Manufacturing & Orbital Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Platforms, Facilities & Orbital Assets Deployed)

- By Infrastructure Type

- By Technology

- By Orbit Type

- By Manufacturing Output

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Space Manufacturing & Orbital Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Platforms, Facilities & Orbital Assets Deployed)

- By Infrastructure Type

- By Technology

- By Orbit Type

- By Manufacturing Output

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Space Manufacturing & Orbital Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Platforms, Facilities & Orbital Assets Deployed)

- By Infrastructure Type

- By Technology

- By Orbit Type

- By Manufacturing Output

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Space Manufacturing & Orbital Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Platforms, Facilities & Orbital Assets Deployed)

- By Infrastructure Type

- By Technology

- By Orbit Type

- By Manufacturing Output

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Space Manufacturing & Orbital Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Platforms, Facilities & Orbital Assets Deployed)

- By Infrastructure Type

- By Technology

- By Orbit Type

- By Manufacturing Output

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Norway, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Technology Landscape & Innovation Analysis

- Microgravity Materials Processing, Additive Manufacturing & In-Space Production Technology Deep-Dive

- On-Orbit Robotics, Autonomous Assembly & Rendezvous and Proximity Operations (RPO) Technology

- Closed-Loop Life Support, Environmental Control & Crew Habitation System Technology

- Space-Based Solar Power (SBSP) Array, Wireless Power Transmission & Ground Receiver Technology

- In-Situ Resource Utilisation (ISRU), Propellant Extraction & Orbital Refuelling Technology

- Advanced Structural Materials, Radiation Shielding & Thermal Management Technology for Orbital Environments

- AI, Digital Twin, Autonomous Operations & Mission Management Platform Technology

- Patent & IP Landscape in Space Manufacturing & Orbital Infrastructure Technologies

- Value Chain & Supply Chain Analysis

- Launch Vehicle, Heavy-Lift Rocket & Orbital Delivery Supply Chain

- Spacecraft Bus, Habitat Module & Structural Assembly Manufacturing Supply Chain

- Propulsion, Power Systems & Energy Storage Supply Chain for Orbital Platforms

- Sensors, Avionics, Robotics & On-Orbit Servicing Equipment Supply Chain

- Prime Space Systems Integrator, Contractor & OEM Procurement Landscape

- Government Space Agency, Commercial Operator & Research Institution End-User Channel

- In-Space Manufactured Product Downstream Distribution & Commercialisation Channel

- Pricing Analysis

- Launch Cost per Kilogram to Orbit: Historical Trend, Current Benchmarks & Forecast by Vehicle Class

- Commercial Space Station Module & Habitat Capital Cost and per-Seat, per-Rack Pricing Analysis

- On-Orbit Servicing, Assembly & Manufacturing (OSAM) Platform Capital and Mission Cost Analysis

- In-Space Manufactured Product Pricing: Pharmaceutical, Crystal, Fibre & Structural Component Price Benchmarks

- Space-Based Solar Power (SBSP) Levelised Cost of Energy (LCOE) & Transmission Cost Analysis

- Total Orbital Infrastructure Project Economics: Capital Expenditure, Revenue Model & Return on Investment Analysis

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Orbital Infrastructure: Launch Carbon Footprint, Propellant Emissions & In-Space Energy Consumption

- Space Debris Generation, Orbital Environment Sustainability & Active Debris Removal Contribution

- Space-Based Solar Power (SBSP) as a Climate Solution: Carbon Abatement Potential & Energy Transition Contribution

- Circular Economy, Platform Servicing, Life Extension & End-of-Life Deorbit for Orbital Infrastructure

- Regulatory-Driven Sustainability, UN Long-Term Sustainability Guidelines & Space ESG Disclosure Frameworks

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Infrastructure Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Infrastructure Type, Technology & Geography

- Player Classification

- Integrated Space Systems Primes & Full-Spectrum Orbital Infrastructure Developers

- Commercial Space Station & Habitat Module Manufacturers

- On-Orbit Servicing, Assembly & Manufacturing (OSAM) Technology Providers

- Launch Vehicle Manufacturers & Heavy-Lift Orbital Delivery Providers

- In-Space Manufacturing, Microgravity Research & Payload Service Providers

- Space-Based Solar Power (SBSP) Technology Developers

- AI, Digital Twin & Autonomous Operations Platform Providers for Orbital Systems

- Government-Owned Space Agencies, National Laboratories & Research Institutes

- Competitive Analysis Frameworks

- Market Share Analysis by Infrastructure Type, Technology & Region

- Company Profile

- Company Overview & Headquarters

- Space Manufacturing & Orbital Infrastructure Products & Technology Portfolio

- Key Customer Relationships & Reference Mission Installations

- Manufacturing Footprint & Production Capacity

- Revenue (Space Manufacturing & Orbital Infrastructure Segment) & Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Market Opportunity Analysis

- Strategic Output

- Market Opportunity Matrix: By Infrastructure Type, Technology, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Output

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)