Rapid Digital Commerce Expansion Driving Demand Amid Unit-Economics and Operational Challenges

The GCC last mile delivery market is emerging as one of the region’s most dynamic digital-commerce infrastructure segments, with the market valued at USD 17.13 billion and projected to grow at a CAGR of 9.67% during 2026–2031. This growth is being driven by the continued expansion of e-commerce marketplaces, food delivery platforms, grocery and quick-commerce models, rising smartphone penetration, digital payment adoption, and a strong consumer preference for convenience-led fulfillment. Urban concentration in cities such as Riyadh, Jeddah, Dubai, Abu Dhabi, Doha, Kuwait City, Muscat, and Manama makes dense delivery networks increasingly viable, while retailer investments in dark stores, micro-fulfillment centers, and omnichannel retail are further accelerating market development. At the same time, the market is not without friction points. High delivery costs, rider productivity pressure, traffic congestion, fragmented merchant density outside top urban clusters, and the challenge of balancing fast delivery expectations with sustainable unit economics remain key restraints. Labor dependence, volatile fuel and fleet costs, and competition-led price discounting can further compress profitability. However, significant opportunities remain in EV-based fleets, hyperlocal delivery expansion, pharmacy and healthcare logistics, subscription-based delivery ecosystems, route optimization technologies, and white-label logistics services for SMEs and mid-sized merchants seeking outsourced last mile capabilities.

Regulatory Framework Shaping the GCC Last Mile Delivery Ecosystem: Gig Worker Protection, Licensing Compliance, and Sustainability Policies

The GCC regulatory environment is becoming more important as last mile delivery evolves from a convenience-driven service into a structured logistics sub-sector. Labor regulations for gig workers are receiving greater scrutiny, particularly around rider welfare, sponsorship structures, contract transparency, working hours, insurance, and heat-exposure protections, especially in markets with a large outsourced or freelancer-led rider base. Delivery licensing requirements are also becoming more formalized, with municipalities and transport authorities increasingly emphasizing commercial permits, food handling compliance, vehicle registration, and courier operating approvals. Traffic regulations remain a critical operating consideration, especially for two-wheeler fleets navigating dense urban areas where road safety, parking enforcement, and delivery-zone access can directly affect delivery productivity. EV adoption policies are gradually gaining relevance as GCC governments promote sustainability agendas, low-emission mobility, and green urban logistics; this creates long-term potential for electric bikes, scooters, and compact delivery fleets, especially in dense metro zones. Food delivery regulations are equally influential, as restaurant aggregators and delivery operators must comply with food safety, packaging, storage, handling, and temperature integrity requirements. Over time, regulation is likely to push the market toward better formalization, stronger fleet compliance, more structured platform operations, and a gradual shift away from purely informal or loosely managed last mile networks.

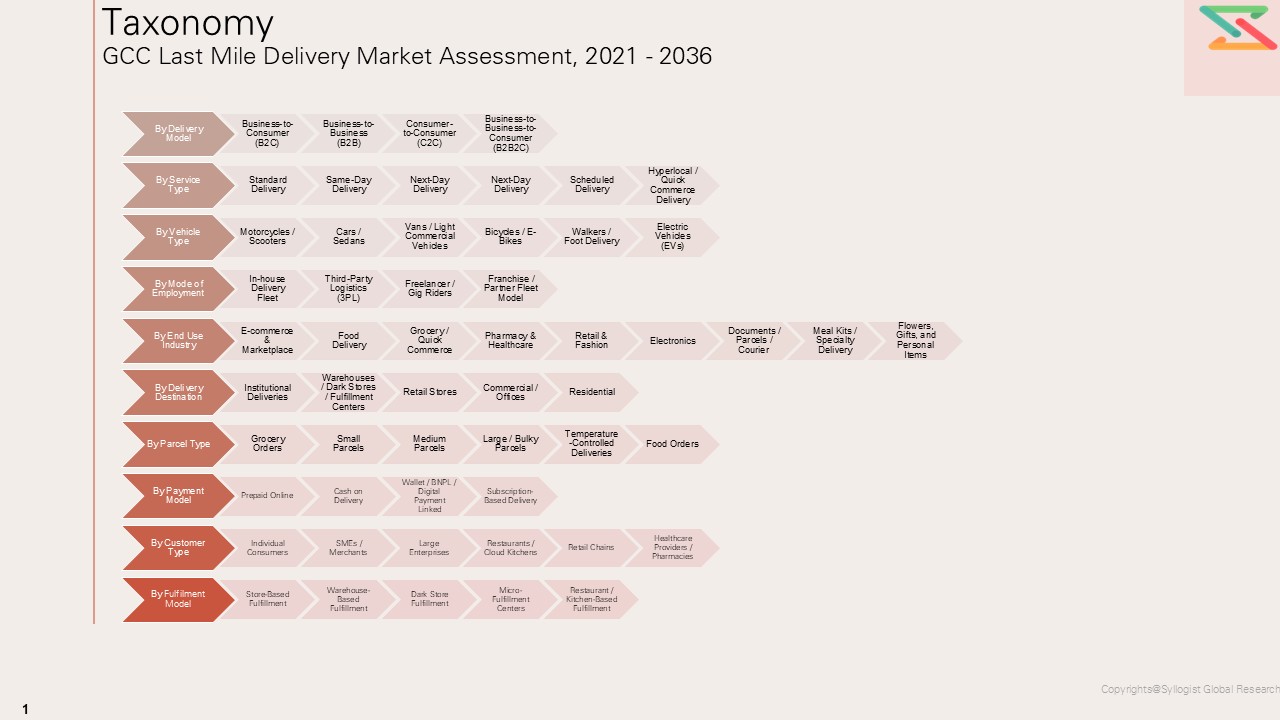

Segment Insights Across Delivery Model, Service Type, Vehicle, Employment, End Use, Destination, Parcel, Payment, Customer, and Fulfilment

By delivery model, Business-to-Consumer (B2C) remains the largest segment because the GCC last mile market is fundamentally anchored in consumer-facing e-commerce, food delivery, grocery, and retail transactions, while Business-to-Business-to-Consumer (B2B2C) is likely the fastest-growing as platforms, merchants, marketplaces, and third-party fulfilment players become more interconnected.

By service type, Standard Delivery continues to hold the largest share due to its broad use across general parcel and non-urgent retail logistics, whereas Hyperlocal / Quick Commerce Delivery is the fastest-growing as consumers increasingly expect rapid grocery, pharmacy, and convenience-item fulfilment.

By vehicle type, Motorcycles / Scooters dominate because they offer the best balance of speed, manoeuvrability, and cost efficiency in dense urban delivery environments, while Electric Vehicles (EVs) are expected to be the fastest-growing segment as sustainability agendas and operating-cost optimization gain traction.

By mode of employment, Third-Party Logistics (3PL) and outsourced fleet structures remain the largest because many platforms and merchants prefer asset-light operations, while Freelancer / Gig Riders are the fastest-growing due to the flexibility they provide in handling peak demand and fluctuating order volumes.

By end-use industry, Food Delivery remains the largest segment given its high order frequency and daily-use nature, while Grocery / Quick Commerce is the fastest-growing as dark-store-led convenience models scale rapidly across GCC cities.

By delivery destination, Residential leads because the majority of last mile demand is home-directed, while Warehouses / Dark Stores / fulfilment Centers are the fastest-growing linked destination nodes as the backend of urban logistics becomes more distributed.

By parcel type, Food Orders account for the largest share because of their high-frequency nature, while Temperature-Controlled Deliveries are likely the fastest-growing as healthcare, premium grocery, and specialty food delivery expand.

By payment model, Prepaid Online is the largest segment as digital payment adoption deepens across the GCC, while Wallet / BNPL / Digital Payment Linked models are the fastest-growing due to platform integration and fintech ecosystem expansion.

By customer type, Individual Consumers dominate because consumer ordering remains the core market engine, while SMEs / Merchants are among the fastest-growing user groups as smaller sellers increasingly rely on platform-led and outsourced. By fulfilment model, Store-Based Fulfilment remains the largest due to legacy retail and restaurant networks, while Dark Store Fulfilment and Micro-fulfilment Centers are the fastest-growing as speed-led delivery models become more central to competitive differentiation.

Unit Economics of GCC Last Mile Delivery: Balancing Delivery Fees, Rider Compensation, and Platform Monetization Strategies

Pricing in the GCC last mile delivery market is shaped by a delicate balance between customer acquisition, order density, service-level commitments, and rider economics. Delivery fee structures vary widely depending on distance, speed, order value, urban density, and platform strategy, but increasingly, fees are used as a strategic lever rather than a pure cost recovery mechanism. Platforms often subsidize delivery to drive frequency, improve user retention, or gain market share in highly competitive cities. Cost per delivery is influenced by rider productivity, route density, idle time, traffic conditions, fuel or vehicle operating expenses, failed delivery attempts, and the complexity of the final drop. Rider compensation is one of the most sensitive components of the cost stack, particularly where the market depends on gig fleets, incentive-based structures, and surge-led dispatching. Platform commissions from merchants remain a major revenue stream, especially in food delivery and marketplace-led models, but excessive commission pressure can create merchant dissatisfaction and encourage direct-order alternatives. Merchant fees, subscription models, and logistics service bundles are increasingly being redesigned to improve platform monetization without weakening merchant retention. Over time, the strongest operators will be those that move from growth-at-all-costs delivery economics toward more disciplined, density-led, and technology-supported unit economics.

Technology-Led Differentiation in GCC Last Mile Delivery: AI Dispatching, Route Optimization, and Dark Store Fulfilment Transforming Operational Efficiency

Technology is becoming the main differentiator in GCC last mile delivery, particularly as platforms compete on speed, reliability, rider efficiency, and customer experience. Route optimization tools are increasingly critical in dense urban markets where traffic variability, building access complexity, and order clustering directly influence delivery times and cost per order. AI dispatching is allowing platforms to allocate orders more dynamically based on rider location, merchant preparation time, traffic patterns, service priority, and order pooling logic, helping improve both operational efficiency and customer satisfaction. Delivery tracking has evolved from a convenience feature into a baseline expectation, with real-time visibility, predictive ETA systems, and proactive delay notifications now central to platform trust. Dark store technology is reshaping high-frequency delivery models by improving inventory visibility, order batching, picking speed, and localized fulfilment performance, especially for grocery and convenience-led segments. Autonomous delivery remains an emerging rather than mainstream theme, but it holds long-term relevance in controlled campuses, premium districts, and low-complexity delivery zones where robotics, drone pilots, and semi-automated systems may gradually become viable. As the market matures, technology will increasingly determine who can sustain fast delivery promises without eroding margins.

Competitive Landscape of GCC Last Mile Delivery: Platform Ecosystems, Strategic Partnerships, and Operational Scale Driving Market Leadership

The GCC last mile delivery market is highly competitive and increasingly defined by platform specialization, ecosystem control, and fulfilment partnerships rather than by simple fleet size alone. Market share is concentrated among a mix of food-delivery leaders, regional super-app players, e-commerce platforms, and parcel/logistics operators, each approaching the market with a different strategic logic. Talabat and HungerStation are deeply entrenched in food-led daily frequency demand, while Deliveroo competes through premium restaurant partnerships, branded service experience, and selective urban density. Careem benefits from ecosystem adjacency through mobility, payments, and broader app-based services, while Jahez has built strong positioning in Saudi Arabia’s food and digital ordering landscape. Noon and Amazon are leveraging their commerce ecosystems to build stronger parcel, grocery, and marketplace-linked last mile capabilities, with fulfilment integration becoming a major strategic advantage. Aramex and DHL bring parcel, express, and B2B logistics depth, particularly in structured courier and cross-border connected networks, while players such as Jeeny can play more selectively where mobility and on-demand infrastructure intersect. Pricing strategies remain aggressive in contested verticals, especially food and quick commerce, where free delivery, subscriptions, merchant promotions, and loyalty-led offers are frequently used to gain frequency and defend retention. Partnerships and M&A are likely to remain important as platforms seek merchant exclusivity, dark-store scale, fulfillment reach, and operational density. Over time, the competitive edge will increasingly shift toward players that can combine strong consumer engagement, efficient rider utilization, merchant monetization, and scalable backend logistics rather than relying only on discount-led growth.

Market Segmentation

- Segmentation by Delivery Model

- Business-to-Consumer (B2C)

- Business-to-Business (B2B)

- Consumer-to-Consumer (C2C)

- Business-to-Business-to-Consumer (B2B2C)

- Segmentation by Service Type

- Standard Delivery

- Same-Day Delivery

- Next-Day Delivery

- Express / On-Demand Delivery

- Scheduled Delivery

- Hyperlocal / Quick Commerce Delivery

- Segmentation by Vehicle Type

- Motorcycles / Scooters

- Cars / Sedans

- Vans / Light Commercial Vehicles

- Bicycles / E-Bikes

- Walkers / Foot Delivery

- Electric Vehicles (EVs)

- Segmentation by Mode of Employment

- In-house Delivery Fleet

- Third-Party Logistics (3PL)

- Freelancer / Gig Riders

- Franchise / Partner Fleet Model

- Segmentation by End Use Industry

- E-commerce & Marketplace

- Food Delivery

- Grocery / Quick Commerce

- Pharmacy & Healthcare

- Retail & Fashion

- Electronics

- Documents / Parcels / Courier

- Meal Kits / Specialty Delivery

- Flowers, Gifts, and Personal Items

- Segmentation by Delivery Destination

- Residential

- Commercial / Offices

- Retail Stores

- Warehouses / Dark Stores / Fulfilment Centers

- Institutional Deliveries

- Segmentation by Parcel Type

- Food Orders

- Grocery Orders

- Small Parcels

- Medium Parcels

- Large / Bulky Parcels

- Temperature-Controlled Deliveries

- Segmentation by Payment Model

- Prepaid Online

- Cash on Delivery

- Wallet / BNPL / Digital Payment Linked

- Subscription-Based Delivery

- Segmentation by Customer Type

- Individual Consumers

- SMEs / Merchants

- Large Enterprises

- Restaurants / Cloud Kitchens

- Retail Chains

- Healthcare Providers / Pharmacies

- Segmentation by Fulfilment Model

- Store-Based fulfilment

- Warehouse-Based fulfilment

- Dark Store fulfilment

- Micro-fulfilment Centers

- Restaurant / Kitchen-Based fulfilment

- Market Foundations & Dynamics

- Market Taxonomy

- Research Methodology

- Executive Summary

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Ecosystem & Value Chain

- Evolution of Last Mile Delivery

- Logistics Value Chain

- Role of E-commerce, Food Delivery, and Quick Commerce

- Market Structure in GCC

- Marketplace Platforms

- Logistics Operators

- Merchant Partners

- Dark Stores / Micro Fulfilment

- Payment Platforms

- Market Trends & Developments

- Investment Hotspots

- Unmet Needs and White Market Spaces

- Investment and Funding Trends

- Venture Capital Investments

- Startup Ecosystem

- Strategic Partnerships

- Market Consolidation

- Risk Assessment Framework

- Political / Geopolitical Risk

- Regulatory Risk

- Financial / Market Risk

- Regulatory Framework & Standards

- Labor Regulations for Gig Workers

- Delivery Licensing Requirements

- Traffic Regulations

- EV Adoption Policies

- Food Delivery Regulations

- GCC Last Mile Delivery Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Number of Deliveries)

- Market Size & Forecast by Delivery Model

- Business-to-Consumer (B2C)

- Business-to-Business (B2B)

- Consumer-to-Consumer (C2C)

- Business-to-Business-to-Consumer (B2B2C)

- Market Size & Forecast by Service Type

- Standard Delivery

- Same-Day Delivery

- Next-Day Delivery

- Express / On-Demand Delivery

- Scheduled Delivery

- Hyperlocal / Quick Commerce Delivery

- Market Size & Forecast by Vehicle Type

- Motorcycles / Scooters

- Cars / Sedans

- Vans / Light Commercial Vehicles

- Bicycles / E-Bikes

- Walkers / Foot Delivery

- Electric Vehicles (EVs)

- Market Size & Forecast by Mode of Employment

- In-house Delivery Fleet

- Third-Party Logistics (3PL)

- Freelancer / Gig Riders

- Franchise / Partner Fleet Model

- Market Size & Forecast by End Use Industry

- E-commerce & Marketplace

- Food Delivery

- Grocery / Quick Commerce

- Pharmacy & Healthcare

- Retail & Fashion

- Electronics

- Documents / Parcels / Courier

- Meal Kits / Specialty Delivery

- Flowers, Gifts, and Personal Items

- Market Size & Forecast by Delivery Destination

- Residential

- Commercial / Offices

- Retail Stores

- Warehouses / Dark Stores / Fulfillment Centers

- Institutional Deliveries

- Market Size & Forecast by Parcel Type

- Food Orders

- Grocery Orders

- Small Parcels

- Medium Parcels

- Large / Bulky Parcels

- Temperature-Controlled Deliveries

- Market Size & Forecast by Payment Model

- Prepaid Online

- Cash on Delivery

- Wallet / BNPL / Digital Payment Linked

- Subscription-Based Delivery

- Market Size & Forecast by Customer Type

- Individual Consumers

- SMEs / Merchants

- Large Enterprises

- Restaurants / Cloud Kitchens

- Retail Chains

- Healthcare Providers / Pharmacies

- Market Size & Forecast by Fulfilment Model

- Store-Based fulfilment

- Warehouse-Based fulfilment

- Dark Store fulfilment

- Micro-fulfilment Centers

- Restaurant / Kitchen-Based fulfilment

- Saudi Arabia Last Mile Delivery Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Number of Deliveries)

- Market Size & Forecast by Delivery Model

- Market Size & Forecast by Service Type

- Market Size & Forecast by Vehicle Type

- Market Size & Forecast by Mode of Employment

- Market Size & Forecast by End Use Industry

- Market Size & Forecast by Delivery Destination

- Market Size & Forecast by Parcel Type

- Market Size & Forecast by Payment Model

- Market Size & Forecast by Customer Type

- Market Size & Forecast by Fulfilment Model

- UAE Last Mile Delivery Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Number of Deliveries)

- Market Size & Forecast by Delivery Model

- Market Size & Forecast by Service Type

- Market Size & Forecast by Vehicle Type

- Market Size & Forecast by Mode of Employment

- Market Size & Forecast by End Use Industry

- Market Size & Forecast by Delivery Destination

- Market Size & Forecast by Parcel Type

- Market Size & Forecast by Payment Model

- Market Size & Forecast by Customer Type

- Market Size & Forecast by Fulfilment Model

- Qatar Last Mile Delivery Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Number of Deliveries)

- Market Size & Forecast by Delivery Model

- Market Size & Forecast by Service Type

- Market Size & Forecast by Vehicle Type

- Market Size & Forecast by Mode of Employment

- Market Size & Forecast by End Use Industry

- Market Size & Forecast by Delivery Destination

- Market Size & Forecast by Parcel Type

- Market Size & Forecast by Payment Model

- Market Size & Forecast by Customer Type

- Market Size & Forecast by Fulfilment Model

- Kuwait Last Mile Delivery Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Number of Deliveries)

- Market Size & Forecast by Delivery Model

- Market Size & Forecast by Service Type

- Market Size & Forecast by Vehicle Type

- Market Size & Forecast by Mode of Employment

- Market Size & Forecast by End Use Industry

- Market Size & Forecast by Delivery Destination

- Market Size & Forecast by Parcel Type

- Market Size & Forecast by Payment Model

- Market Size & Forecast by Customer Type

- Market Size & Forecast by Fulfilment Model

- Oman Last Mile Delivery Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Number of Deliveries)

- Market Size & Forecast by Delivery Model

- Market Size & Forecast by Service Type

- Market Size & Forecast by Vehicle Type

- Market Size & Forecast by Mode of Employment

- Market Size & Forecast by End Use Industry

- Market Size & Forecast by Delivery Destination

- Market Size & Forecast by Parcel Type

- Market Size & Forecast by Payment Model

- Market Size & Forecast by Customer Type

- Market Size & Forecast by Fulfilment Model

- Bahrain Last Mile Delivery Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Number of Deliveries)

- Market Size & Forecast by Delivery Model

- Market Size & Forecast by Service Type

- Market Size & Forecast by Vehicle Type

- Market Size & Forecast by Mode of Employment

- Market Size & Forecast by End Use Industry

- Market Size & Forecast by Delivery Destination

- Market Size & Forecast by Parcel Type

- Market Size & Forecast by Payment Model

- Market Size & Forecast by Customer Type

- Market Size & Forecast by Fulfilment Model

- Pricing and Cost Structure

- Delivery Fee Structure

- Cost per Delivery

- Rider Compensation

- Platform Commission

- Merchant Fees

- Operational Metrics Benchmarking

- Orders per Rider per Day

- Average Delivery Time

- Cost per Delivery

- Rider Productivity

- Fleet Utilization

- Technology Landscape

- Route Optimization

- AI Dispatching

- Delivery Tracking

- Dark Store Technology

- Autonomous Delivery

- Competitive Landscape

- Market Share Analysis

- Platform Strategies

- Pricing Strategies

- Partnerships and M&A

- Key Players:

- Talabat

- Deliveroo

- Careem

- Noon

- Amazon

- Aramex

- DHL

- Jeeny

- Jahez

- HungerStation

- Rider Economics

- Average Rider Income

- Incentive Models

- Cost Per Order

- Strategic Recommendations & Roadmap

- Competitors’ Strategic Initiatives

- Future Outlook (Next 5–10 Years, Emerging Players, Success Factors)

- Strategic Recommendations

- Market Acceleration Roadmap

- Short-Term

- Mid-Term

- Long-Term

- Tailored Recommendations for:

- Producers

- Raw Material Suppliers

- Policymakers / Regulators

- Recommendations on Key Success Factors

- Raw Material Security

- Policy Alignment

- Supply Chain Integration

- Market Acceleration Roadmap