Market Definition

The data center automation and monitoring market is defined by the integration of software solutions and intelligent systems designed to manage, track, and execute routine data center workflows with minimal human intervention. This market encompasses a broad range of technologies, including Data Center Infrastructure Management (DCIM), automated provisioning tools, and real-time telemetry systems that monitor environmental factors (power, cooling) and hardware performance (servers, networking). By automating tasks such as load balancing, patch management, and capacity planning, the market enables organizations to transition from reactive maintenance to a proactive, software-defined operational model that maximizes uptime and resource utilization.

Market Insights

The Transition from Rule-Based Scripting to AI-Driven Autonomous Operations The market is currently undergoing a fundamental shift as traditional rule-based automation is replaced by AI and Machine Learning (ML) models capable of autonomous decision-making. By 2026, it is projected that over 60% of IT organizations will employ AI-enabled predictive automation to manage network domains. Unlike older systems that required manual scripts for every scenario, modern AI-driven controllers can analyze real-time telemetry to predict equipment failures and initiate self-healing protocols before an outage occurs. This evolution significantly reduces human error, the leading cause of data center downtime, and allows operators to manage increasingly complex, high-density environments without a proportional increase in headcount.

Rising Rack Densities and the Critical Role of Thermal Automation The explosion of generative AI and Large Language Models (LLMs) has pushed data center rack densities from a traditional 8 kW to upwards of 30–100 kW. This shift has made manual cooling management obsolete, driving a surge in automated liquid-cooling loops and microfluidic monitoring systems. Monitoring solutions are no longer just tracking up/down status; they are now deeply integrated with cooling infrastructure to dynamically rebalance workloads across the floor to avoid thermal hotspots. By 2026, the demand for sophisticated thermal automation is expected to be a primary growth driver, particularly for hyperscalers and colocation providers hosting power-hungry AI training clusters.

Edge Computing Proliferation and the Need for Distributed Monitoring As data generation moves closer to the source via 5G and IoT, the Edge has become a vital segment of the automation market. Unlike centralized facilities, edge data centers are often unmanned and geographically dispersed, necessitating a lights-out management approach. This has birthed a new sub-sector for decentralized monitoring software that provides a unified single pane of glass view across thousands of remote nodes. Market data suggests that the edge data center segment will grow at a CAGR of over 17% through 2026, with automation software playing the role of the virtual onsite technician, handling everything from remote security biometrics to localized power optimization.

Sustainability Mandates as a Commercial Catalyst for Automation Environmental, Social, and Governance (ESG) regulations are transforming automation from an operational luxury into a compliance necessity. With data centers consuming nearly 2% of global electricity, automated Energy Management Systems (EMS) are being deployed to hit aggressive Power Usage Effectiveness (PUE) targets. Advanced monitoring tools now provide real-time carbon footprint tracking and automate the shifting of non-critical workloads to hours when renewable energy is most available on the grid. By 2026, Green Automation will be a key differentiator in the market, as enterprises favor providers that can offer automated, auditable reports on energy efficiency to satisfy both regulators and eco-conscious investors.

Key Drivers

The Surge of Generative AI and High-Density Power Demands: The shift from traditional cloud workloads to Generative AI and Large Language Model (LLM) training has caused rack power densities to skyrocket from 10 kW to over 50–100 kW. Manual monitoring of such intense thermal environments is no longer feasible. This has driven a massive adoption of AI-integrated cooling automation, where software dynamically adjusts liquid cooling loops and airflow in real-time to prevent thermal runaway. Without these automated systems, the risk of hardware failure in high-density AI clusters becomes unmanageably high.

Proliferation of Lights-Out Edge Data Centers: As 5G and IoT applications require lower latency, data processing is moving to the edge, smaller, decentralized facilities located closer to the end-user. These sites are often unmanned and geographically dispersed, making physical maintenance costly and inefficient. The necessity for remote, autonomous management, where software handles everything from biometric security to patch management without a human on-site, is a massive driver for the specialized edge-scale automation software market.

Key Challenges

The Brownfield Integration Gap and Legacy Debt: While new greenfield data centers are built with automation in mind, a significant portion of the global infrastructure consists of older brownfield facilities. Integrating modern, AI-driven automation platforms with legacy hardware and siloed proprietary systems remains a major hurdle. Many organizations find themselves stuck with islands of automation where new software cannot communicate with older power distribution units (PDUs) or cooling chillers, leading to inconsistent data and manual workarounds.

Cyber-Physical Security Vulnerabilities: As data centers become more automated, the attack surface for cyber threats shifts from just data to the physical infrastructure itself. A single vulnerability in an automation script or a hijacked administrative account could allow a malicious actor to remotely shut down cooling systems or manipulate power loads, potentially causing physical damage to hardware. Securing these automated control planes against sophisticated state-sponsored or ransomware attacks is currently one of the most complex technical challenges facing the industry.

Market Segmentation

Data Center Automation Market

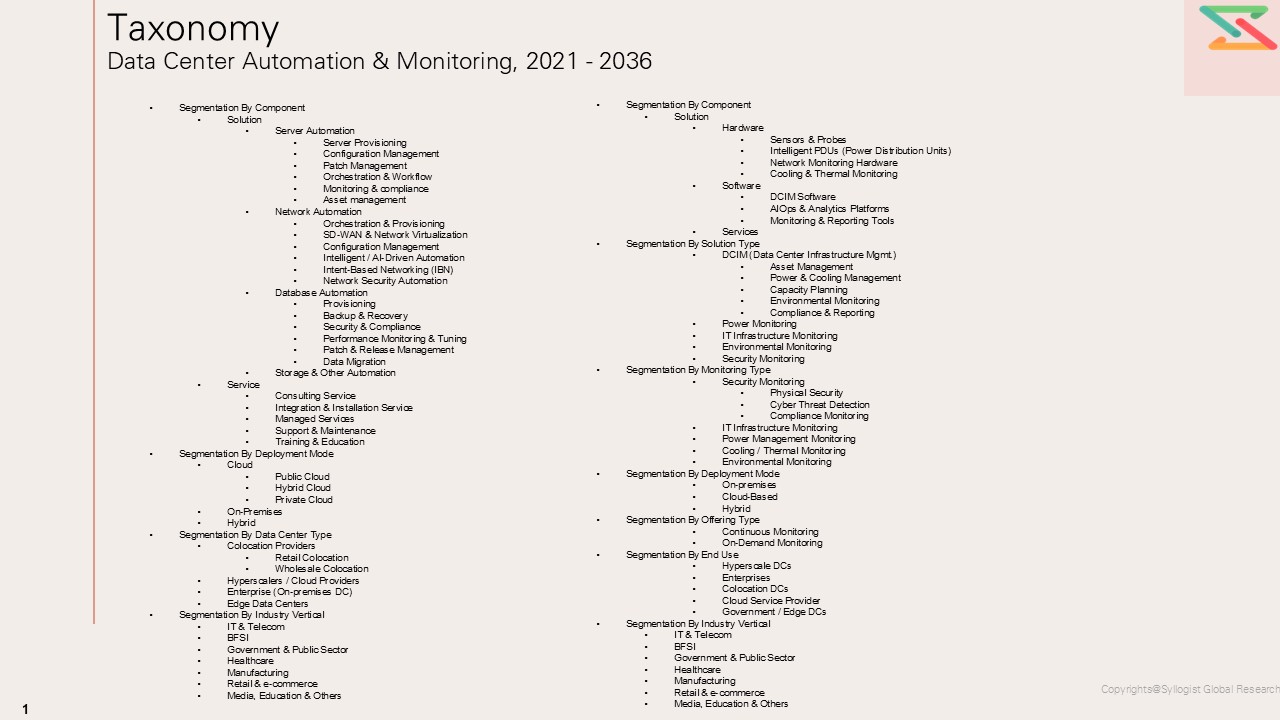

- Segmentation By Component

- Solution

- Server Automation

- Server Provisioning

- Configuration Management

- Patch Management

- Orchestration & Workflow

- Monitoring & compliance

- Asset management

- Network Automation

- Orchestration & Provisioning

- SD-WAN & Network Virtualization

- Configuration Management

- Intelligent / AI-Driven Automation

- Intent-Based Networking (IBN)

- Network Security Automation

- Database Automation

- Provisioning

- Backup & Recovery

- Security & Compliance

- Performance Monitoring & Tuning

- Patch & Release Management

- Data Migration

- Storage & Other Automation

- Server Automation

- Service

- Consulting Service

- Integration & Installation Service

- Managed Services

- Support & Maintenance

- Training & Education

- Segmentation By Deployment Mode

- Cloud

- Public Cloud

- Hybrid Cloud

- Private Cloud

- On-Premises

- Hybrid

- Cloud

- Segmentation By Data Center Type

- Colocation Providers

- Retail Colocation

- Wholesale Colocation

- Hyperscalers / Cloud Providers

- Enterprise (On-premises DC)

- Edge Data Centers

- Colocation Providers

- Segmentation By Industry Vertical

- IT & Telecom

- BFSI

- Government & Public Sector

- Healthcare

- Manufacturing

- Retail & e-commerce

- Media, Education & Others

- Solution

Data Center Monitoring Market

- Segmentation By Component

- Solution

- Hardware

- Sensors & Probes

- Intelligent PDUs (Power Distribution Units)

- Network Monitoring Hardware

- Cooling & Thermal Monitoring

- Software

- DCIM Software

- AIOps & Analytics Platforms

- Monitoring & Reporting Tools

- Services

- Hardware

- Segmentation By Solution Type

- DCIM (Data Center Infrastructure Mgmt.)

- Asset Management

- Power & Cooling Management

- Capacity Planning

- Environmental Monitoring

- Compliance & Reporting

- Power Monitoring

- IT Infrastructure Monitoring

- Environmental Monitoring

- Security Monitoring

- DCIM (Data Center Infrastructure Mgmt.)

- Segmentation By Monitoring Type

- Security Monitoring

- Physical Security

- Cyber Threat Detection

- Compliance Monitoring

- IT Infrastructure Monitoring

- Power Management Monitoring

- Cooling / Thermal Monitoring

- Environmental Monitoring

- Security Monitoring

- Segmentation By Deployment Mode

- On-premises

- Cloud-Based

- Hybrid

- Segmentation By Offering Type

- Continuous Monitoring

- On-Demand Monitoring

- Segmentation By End Use

- Hyperscale DCs

- Enterprises

- Colocation DCs

- Cloud Service Provider

- Government / Edge DCs

- Segmentation By Industry Vertical

- IT & Telecom

- BFSI

- Government & Public Sector

- Healthcare

- Manufacturing

- Retail & e-commerce

- Media, Education & Others

- Solution

All market revenues are presented in USD

Historical Year: 2021–2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027–2036

Key Questions this Study Will Answer

- What are the critical market metrics and forward-looking projections for the Global Data Center Automation & Monitoring Market, including revenue size, deployment volume, and average spend per site / rack / MW, with performance segmentation across Solution Type (DCIM, Infrastructure Monitoring, Network Monitoring, Server & Storage Monitoring, Power Monitoring, Cooling Monitoring, AIOps / Predictive Analytics, Workflow & Orchestration Automation), Component (Software, Hardware, Services), Deployment Model (On-Premises, Cloud-Based, Hybrid), Data Center Type (Enterprise, Colocation, Hyperscale, Edge, Telecom), Tier Classification (Tier I, Tier II, Tier III, Tier IV), Application (Asset Tracking, Capacity Planning, Incident Management, Energy Optimization, Thermal Management, Security Monitoring, Remote Infrastructure Management), and End-Use Industry (BFSI, IT & Telecom, Government, Healthcare, Retail & E-commerce, Manufacturing, Media & Entertainment)?

- How do supply–demand fundamentals vary across key regions and major data center hubs, and what role do hyperscale expansion, colocation growth, edge deployments, AI and high-density computing workloads, uptime requirements, sustainability mandates, power availability constraints, and cybersecurity regulations play in shaping regional competitiveness, alongside local capability in software development, systems integration, sensor and controller deployment, BMS/DCIM interoperability, cloud observability, and downstream service ecosystems, as well as procurement structures across direct enterprise contracts, colocation operator agreements, hyperscaler framework contracts, channel partners, managed service providers, and value-added resellers?

- In what ways are software licensing costs, semiconductor and sensor pricing, server/network equipment lead times, cloud infrastructure expenses, and energy price volatility influencing deployment costs, pricing strategies, vendor margins, implementation timelines, and profitability, especially for AI-enabled monitoring platforms, real-time analytics solutions, predictive maintenance tools, digital twin-based optimization systems, and automated power and cooling management platforms?

- Who are the leading global and regional data center automation, monitoring, and observability vendors, infrastructure management platform providers, and system integrators, and how do they benchmark across scalability, interoperability, monitoring accuracy, analytics capability, automation depth, response time, cybersecurity resilience, ease of integration, dashboard usability, price competitiveness, and portfolio breadth across standalone software offerings versus value-added solutions such as remote monitoring services, predictive maintenance, workflow automation, incident remediation, SLA management, consulting, and integration support?

- What strategic insights emerge from primary discussions with data center operators, hyperscalers, colocation providers, enterprise IT teams, facility managers, system integrators, and monitoring platform vendors regarding demand shifts toward AI-driven observability, centralized command-center visibility, autonomous incident response, predictive maintenance, remote site management, liquid-cooling monitoring, and energy-efficiency optimization, along with key purchase criteria such as reliability, interoperability with legacy systems, cybersecurity, real-time visibility, scalability, ease of deployment, total cost of ownership, and vendor support quality?

- Executive summary

- Industry 360° Synopsis (Historical + Forecast)

- Key Market Facts

- Size Highlights

- Inflection Points at a Glance

- Key Findings & Headline Metrics

- TAM / SAM / SOM Analysis

- CXO Perspectives & Strategic Imperatives

- Industry 360° Synopsis (Historical + Forecast)

- Research Methodology

- Market Definition & Scope

- Research Design & Data Sources

- Data Modelling & Estimation Approach

- Forecast Model & Base Year Assumptions

- Research Limitations & Caveats

- Abbreviations, Currency Conventions & Exchange Rates

- Market Background & Evolution

- History of Data Center Automation (1990 → Present)

- Market Structure & Taxonomy

- Data Center Market Overview (Broader Context)

- Macro Trends Driving Automation Adoption

- Industry Structure

- Industry Ecosystem Map

- Supply Chain Analysis

- Pricing Models & Cost Structure Analysis

- Market Concentration & Fragmentation

- Technology Landscape & Innovation Trends

- Core Technology Pillars

- Virtualization & Containerization

- Software-Defined Infrastructure (SDI)

- Infrastructure As Code (IaC)

- Orchestration & Workflow Automation

- Data Center Infrastructure Management (DCIM)

- Emerging & Disruptive Technologies

- AI & ML In DC Automation (AiOps)

- Intent-Based Networking (IBN)

- Digital Twin Technology

- Edge Computing Automation

- Autonomous/Self-Driving Data Centers

- Liquid Cooling & Thermal Automation

- Value Chain & Industry Ecosystem Analysis

- Value Chain Stages

- Hardware & Component Suppliers

- Automation Software Developers

- System Integrators & Consultants

- Cloud & Managed Service Providers

- End-User Organizations

- Value Chain Economics

- Profit Margin Analysis by Chain Stage

- Cost Structure Analysis

- Value Addition at Each Stage

- Key Disruptions in The Value Chain

- Partnership & Collaboration Landscape

- Hyperscale–Automation Vendor Alliances

- OEM & Reseller Channel Analysis

- Open-Source Community Dynamics

- Market Dynamics

- Value Chain Stages

- Core Technology Pillars

- Market Dynamics (Drivers, Restraints, Opportunities, Challenges, Porter’s Five Forces Analysis, PESTLE Analysis)

- Market Trends & Developments

- Risk Assessment Framework

- Regulatory Environment, Compliance & ESG Analysis

- Regulatory Landscape

- Global Data Protection & Privacy Regulations

- Cybersecurity Frameworks & Mandates

- Industry-Specific Compliance Drivers

- Data Sovereignty & Localization Requirements

- Regulatory Bodies by Region

- ESG & Sustainability Analysis

- Energy Efficiency Automation

- Carbon Neutrality & Renewable Energy Integration

- Water Usage & Cooling Automation

- ESG Reporting & Carbon Tracking Automation

- Circular Economy Practices

- Regulatory Landscape

- Global Data Center Automation Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Component

- Solution

- Server Automation

- Server Provisioning

- Configuration Management

- Patch Management

- Orchestration & Workflow

- Monitoring & compliance

- Asset management

- Network Automation

- Orchestration & Provisioning

- SD-WAN & Network Virtualization

- Configuration Management

- Intelligent / AI-Driven Automation

- Intent-Based Networking (IBN)

- Network Security Automation

- Database Automation

- Provisioning

- Backup & Recovery

- Security & Compliance

- Performance Monitoring & Tuning

- Patch & Release Management

- Data Migration

- Storage & Other Automation

- Server Automation

- Service

- Consulting Service

- Integration & Installation Service

- Managed Services

- Support & Maintenance

- Training & Education

- Solution

- Market Size & Forecast by Deployment Mode

- Cloud

- Public Cloud

- Hybrid Cloud

- Private Cloud

- On-Premises

- Hybrid

- Cloud

- Market Size & Forecast by Data Center Type

- Colocation Providers

- Retail Colocation

- Wholesale Colocation

- Hyperscalers / Cloud Providers

- Enterprise (On-premises DC)

- Edge Data Centers

- Colocation Providers

- Market Size & Forecast by Industry Vertical

- IT & Telecom

- BFSI

- Government & Public Sector

- Healthcare

- Manufacturing

- Retail & e-commerce

- Media, Education & Others

- Global Data Center Monitoring Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Component

- Solution

- Hardware

- Sensors & Probes

- Intelligent PDUs (Power Distribution Units)

- Network Monitoring Hardware

- Cooling & Thermal Monitoring

- Software

- DCIM Software

- AIOps & Analytics Platforms

- Monitoring & Reporting Tools

- Services

- Hardware

- Solution

- Market Size & Forecast by Solution Type

- DCIM (Data Center Infrastructure Mgmt.)

- Asset Management

- Power & Cooling Management

- Capacity Planning

- Environmental Monitoring

- Compliance & Reporting

- Power Monitoring

- IT Infrastructure Monitoring

- Environmental Monitoring

- Security Monitoring

- DCIM (Data Center Infrastructure Mgmt.)

- Market Size & Forecast by Monitoring Type

- Security Monitoring

- Physical Security

- Cyber Threat Detection

- Compliance Monitoring

- IT Infrastructure Monitoring

- Power Management Monitoring

- Cooling / Thermal Monitoring

- Environmental Monitoring

- Security Monitoring

- Market Size & Forecast by Deployment Mode

- On-premises

- Cloud-Based

- Hybrid

- Market Size & Forecast by Offering Type

- Continuous Monitoring

- On-Demand Monitoring

- Market Size & Forecast by End Use

- Hyperscale DCs

- Enterprises

- Colocation DCs

- Cloud Service Provider

- Government / Edge DCs

- Market Size & Forecast by Industry Vertical

- IT & Telecom

- BFSI

- Government & Public Sector

- Healthcare

- Manufacturing

- Retail & e-commerce

- Media, Education & Others

- Asia-Pacific Data Center Automation Market Outlook

- Market Size & Forecast

- By Value

- By Component

- By Deployment Mode

- By Data Center Type

- By Industry Vertical

- Market Size & Forecast

- Asia-Pacific Data Center Monitoring Market Outlook

- Market Size & Forecast

- By Value

- By Component

- By Solution Type

- By Monitoring Type

- By Deployment Mode

- By Offering Type

- By End Use

- By Industry Vertical

- Market Size & Forecast

- North America Data Center Automation Market Outlook

- Market Size & Forecast

- By Value

- By Component

- By Deployment Mode

- By Data Center Type

- By Industry Vertical

- Market Size & Forecast

- North America Data Center Monitoring Market Outlook

- Market Size & Forecast

- By Value

- By Component

- By Solution Type

- By Monitoring Type

- By Deployment Mode

- By Offering Type

- By End Use

- By Industry Vertical

- Market Size & Forecast

- Europe Data Center Automation Market Outlook

- Market Size & Forecast

- By Value

- By Component

- By Deployment Mode

- By Data Center Type

- By Industry Vertical

- Market Size & Forecast

- Europe Data Center Monitoring Market Outlook

- Market Size & Forecast

- By Value

- By Component

- By Solution Type

- By Monitoring Type

- By Deployment Mode

- By Offering Type

- By End Use

- By Industry Vertical

- Market Size & Forecast

- Latin America Data Center Automation Market Outlook

- Market Size & Forecast

- By Value

- By Component

- By Deployment Mode

- By Data Center Type

- By Industry Vertical

- Market Size & Forecast

- Latin America Data Center Monitoring Market Outlook

- Market Size & Forecast

- By Value

- By Component

- By Solution Type

- By Monitoring Type

- By Deployment Mode

- By Offering Type

- By End Use

- By Industry Vertical

- Market Size & Forecast

- Middle East & Africa Data Center Automation Market Outlook

- Market Size & Forecast

- By Value

- By Component

- By Deployment Mode

- By Data Center Type

- By Industry Vertical

- Market Size & Forecast

- Middle East & Africa Data Center Monitoring Market Outlook

- Market Size & Forecast

- By Value

- By Component

- By Solution Type

- By Monitoring Type

- By Deployment Mode

- By Offering Type

- By End Use

- By Industry Vertical

- Market Size & Forecast

- Country Wise* Data Center Automation Market Outlook

- Market Size & Forecast

- By Value

- By Component

- By Deployment Mode

- By Data Center Type

- By Industry Vertical

- Market Size & Forecast

- Country Wise* Data Center Monitoring Market Outlook

- Market Size & Forecast

- By Value

- By Component

- By Solution Type

- By Monitoring Type

- By Deployment Mode

- By Offering Type

- By End Use

- By Industry Vertical

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, China, Germany, United Kingdom, Japan, Australia, France, The Netherlands, Singapore, India, Canada, Brazil, South Korea, UAE, Sweden, Ireland, Malaysia, Indonesia, Italy, Poland, Mexico, South Africa, Saudi Arabia, Finland, Thailand, Chile, Norway, Kenya, Vietnam, Qatar

- Strategic Outlook, Growth Opportunities & Recommendations

- Growth Opportunity Analysis

- High-Potential Countries & Geographies

- High-Potential Segments

- White-Space & Adjacency Analysis

- Total Addressable Opportunity By 2030

- Strategic Recommendations

- For Automation Vendors & Software Developers

- For System Integrators & Service Providers

- For Enterprises & End-User Organizations

- For Investors

- Future Outlook & Scenario Analysis

- Base / Bull / Bear Case Forecasts

- Disruptive Scenario

- Trend Convergence Map

- Key Uncertainties & Risk Factors to Monitor

- Growth Opportunity Analysis

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented Vs Consolidated)

- Top 5 Players Market Share

- HHI (Herfindahl–Hirschman Index) Concentration Analysis

- Competitive Intensity Map

- Player Classification

- Market Leaders

- Strong Challengers

- Specialist / Niche Players

- Emerging Players

- Regional Players

- Competitive Analysis Frameworks

- Market Share Analysis

- Company Profile

- Company Overview & HQ

- Products & Solutions Portfolio

- Revenue & Cooling Segment Revenue

- Geographic Presence

- Recent Developments (M&A, Launches, Partnerships)

- SWOT Analysis

- Strategic Focus Areas

- Competitive Positioning Map

- Market Structure & Concentration