Market Definition

Passenger Car Tires are engineered, multi-component toroidal structures, primarily composed of natural and synthetic rubber, carbon black, steel cords, and specialized chemical accelerators, designed specifically for use on light-duty vehicles such as sedans, hatchbacks, SUVs, and crossovers. Unlike commercial or heavy-duty tires, they are optimized for a balance of high-speed stability, ride comfort (noise, vibration, and harshness), and fuel efficiency. The market is bifurcated into Original Equipment (OE), where tires are supplied directly to automakers, and the Aftermarket (Replacement) segment, which remains the larger revenue driver due to the recurring nature of tire wear and the increasing average age of the global vehicle population.

Market Insights

The most significant structural shift in the market is the rapid EV-ready transformation of tire design. As of 2026, the proliferation of Electric Vehicles (EVs) has forced a redesign of the traditional tire architecture to manage the unique stresses of instant torque and the significant weight of battery packs, which can increase a vehicle’s mass by up to 30%. Manufacturers are now deploying high-load capacity (HL) tires that feature reinforced sidewalls and specialized tread patterns designed to minimize the electric hum and reduce rolling resistance. This segment is growing at a CAGR of over 10%, as the efficiency of a tire now directly correlates with a vehicle’s usable battery range.

A second major trend is the Premiumization of the tire profile, driven by the global dominance of SUVs and Crossover Utility Vehicles (CUVs). These body styles have shifted consumer demand toward larger rim sizes, typically 18 inches and above, which command significantly higher profit margins than legacy 15 or 16-inch tires. This shift is not merely aesthetic; larger tires are necessary to maintain stability and braking performance for vehicles with a higher center of gravity. Consequently, tire manufacturers are focusing their R&D on ultra-high-performance (UHP) compounds that provide superior grip without sacrificing the longevity that consumers in the replacement market expect.

Sustainability is no longer a niche marketing tool but a core operational requirement. In response to increasing environmental mandates and the impending PFAS bans in major markets, the industry is aggressively integrating circular materials into mass-market products. Leading players are now substituting petroleum-derived oils and synthetic rubbers with bio-sourced alternatives, such as rice husk silica, dandelion-derived rubber, and recycled PET from plastic bottles. This Green Tire movement aims to reduce the carbon footprint of production by 25% or more by 2030, aligning with the broader net-zero commitments of the global automotive supply chain.

The digitalization of the Contact Patch is giving rise to the Smart Tire ecosystem. Integrated sensors that provide real-time telemetry on tire pressure, temperature, and tread depth are transitioning from high-end fleet applications to the general passenger car market. These systems are increasingly integrated with the vehicle’s Advanced Driver Assistance Systems (ADAS) to adjust stability control and braking parameters based on real-time friction data. Simultaneously, the procurement landscape is being disrupted by a shift toward E-commerce and Click-and-Fit models, where digital platforms and mobile installation services are capturing a larger share of the aftermarket from traditional brick-and-mortar retail hubs.

Key Drivers

The rapid acceleration of Electric Vehicle (EV) adoption is a primary catalyst reshaping the tire industry in 2026. Because EVs are significantly heavier due to their battery packs and deliver instant torque, they place unique mechanical stresses on the contact patch that traditional internal combustion engine (ICE) tires are not equipped to handle. Consequently, there is a surging demand for specialized EV-ready tires featuring reinforced sidewalls for high-load capacity and advanced rubber compounds designed for ultra-low rolling resistance. This segment is growing at a CAGR of over 10%, as these tires are critical for maximizing battery range and ensuring a quiet cabin experience, effectively turning the shift toward electrification into a high-value growth engine for manufacturers.

Another dominant driver is the global Premiumization of the vehicle fleet, characterized by the overwhelming consumer preference for SUVs and Crossovers. These larger vehicle profiles have shifted the market volume away from smaller rim sizes toward 18-inch-plus diameters, which command significantly higher price points and profit margins. This trend is particularly visible in emerging economies like India and China, where the burgeoning middle class views larger, more robust tires as a status and safety symbol. By focusing on these high-performance, larger-diameter products, tire manufacturers are successfully increasing their average selling price (ASP), offsetting the rising costs of raw materials and logistics while catering to a market that prioritizes durability and aesthetic presence.

Key Challenges

- The passenger car tire market is currently navigating a period of significant structural pressure, particularly regarding the volatility of raw material supply chains and the surging costs of essential inputs. Manufacturers are grappling with the unpredictable pricing of natural rubber, synthetic rubber, and carbon black, materials that are highly sensitive to geopolitical instability and fluctuating oil prices. In 2026, the industry is also facing a tightening supply of specialized additives due to Force Majeure events and shifting trade policies, which often force manufacturers into localized near-shoring strategies. These disruptions not only squeeze profit margins but also complicate long-term production planning, especially for high-volume OE (Original Equipment) contracts where pricing is often locked in months in advance.

- Simultaneously, the industry is facing a massive hurdle in the form of tightening environmental regulations and the PFAS-free transition. Global regulators, particularly in the EU and North America, are imposing strict mandates on the chemical composition of tires to reduce microplastic shedding (tire-wear particles) and eliminate forever chemicals from the manufacturing process. This has triggered an expensive R&D race to find viable, high-performance alternatives that do not compromise the tire’s safety or longevity. Additionally, the move toward Extended Producer Responsibility (EPR) laws requires manufacturers to take greater financial and operational ownership of tire recycling and end-of-life disposal. For many players, the high CAPEX required to overhaul legacy production lines into sustainable, circular-economy-ready facilities remains a formidable barrier to maintaining competitiveness.

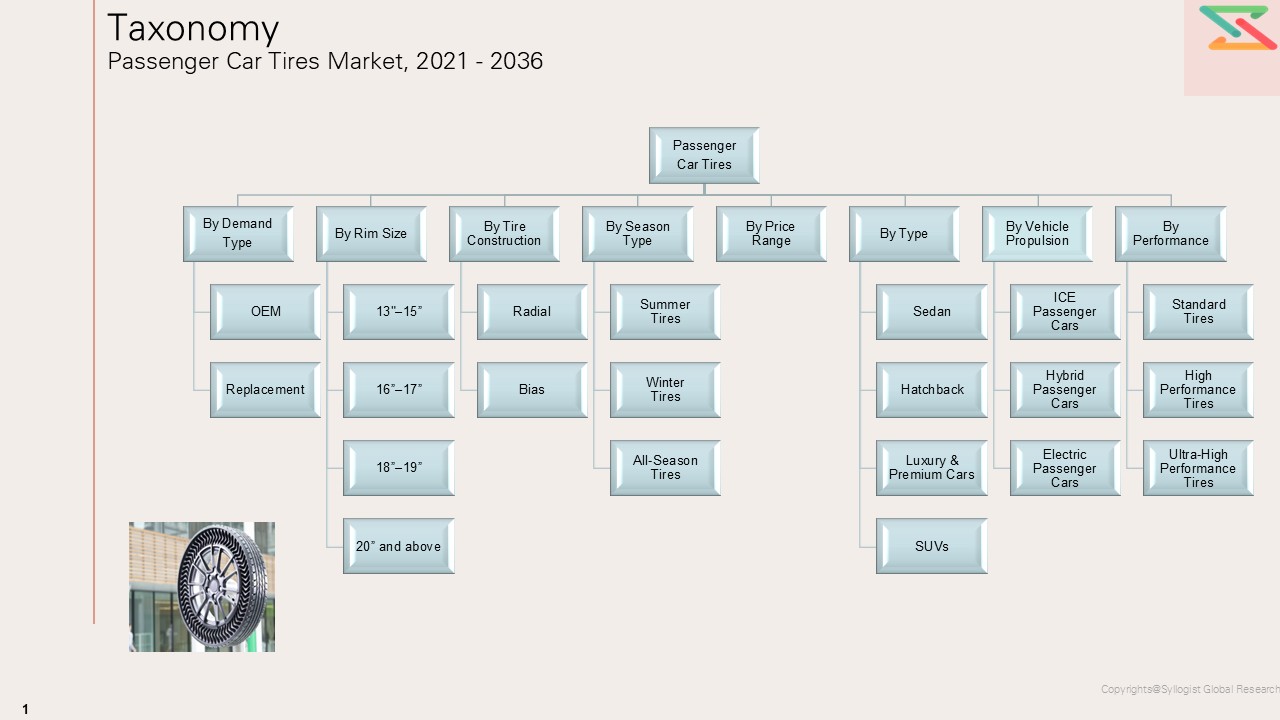

Market Segmentation

- Segmentation by Demand Type

- OEM

- Replacement

- Segmentation by Rim Size

- 13–15

- 16–17

- 18–19

- 20 and above

- Segmentation by Tire Construction

- Radial

- Bias

- Segmentation by Season Type

- Summer Tires

- Winter Tires

- All-Season Tires

- Segmentation by Type

- Sedan

- Hatchback

- Luxury & Premium Cars

- SUVs

- Segmentation by Vehicle Propulsion

- ICE Passenger Cars

- Hybrid Passenger Cars

- Electric Passenger Cars

- Segmentation by Performance

- Standard Tires

- High Performance Tires

- Ultra-High-Performance Tires

All market revenues are presented in USD and volume in units

Historical Year: 2021–2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027–2036

Key Questions this Study Will Answer

- What are the critical market metrics and forward-looking projections for the Global Passenger Car Tire Market, including revenue size, volume sales, and average selling prices, with performance segmentation across Tire Type (Summer, Winter, All-Season, Performance, Touring, Run-Flat), Demand Category (OEM vs. Replacement), Rim Size (Up to 15, 16–18, 19–21, Above 21), Tire Construction (Radial vs. Bias), Vehicle Class (Hatchback, Sedan, SUV, Crossover, Luxury Cars), Price Segment (Budget, Mid-Range, Premium), Sales Channel (Authorized Dealers, Independent Retailers, Online, OEM Dealerships), and Seasonality/Application (On-road, High-performance, All-weather, Fuel-efficient / Low Rolling Resistance)?

- How do supply–demand fundamentals vary across key regions and major automotive markets, and what role do passenger vehicle production, vehicle parc growth, replacement cycles, miles driven, premiumization trends, EV adoption, and regulatory standards for safety and fuel efficiency play in shaping regional competitiveness, alongside local manufacturing capability in tire compounding, tread design, curing, reinforcement materials integration, and downstream distribution networks, as well as procurement structures across OEM supply contracts, replacement market distributors, dealer networks, and e-commerce platforms?

- In what ways are raw material and energy price volatility and lead-time constraints (Natural rubber, synthetic rubber, carbon black, steel cord, textile reinforcements, silica, petrochemical derivatives, and specialty additives) influencing production costs, pricing strategies, supplier margins, delivery schedules, and profitability, especially for premium tires, EV-specific tires, ultra-high-performance tires, and sustainable / low-rolling-resistance product lines?

- Who are the leading global and regional passenger car tire manufacturers, private-label suppliers, and distribution players, and how do they benchmark across durability, tread life, rolling resistance, wet and dry grip, noise performance, fuel efficiency, price competitiveness, brand strength, regulatory compliance, and portfolio breadth across standalone tire supply versus value-added offerings such as warranty programs, fitment services, digital tire monitoring, roadside assistance, and dealer support solutions?

- What strategic insights emerge from primary discussions with tire manufacturers, OEMs, replacement dealers, distributors, fleet-linked service providers, and automotive aftermarket participants regarding demand shifts toward larger rim-size tires, EV-compatible tire specifications, seasonal tire adoption patterns, regional sourcing strategies, inventory and lead-time management, and key purchase criteria such as price competitiveness, brand trust, fuel efficiency, safety performance, ride comfort, durability, and supply assurance?

- Market Overview

- Product Overview

- Research Methodology

- Executive Summary

- Market Dynamics

- Market Dynamics (Drivers, Restraints, Opportunities, Challenges, Porter’s Five Forces Analysis, PESTLE Analysis)

- Market Trends & Developments

- Risk Assessment Framework

- Political / Geopolitical Risk

- Feedstock Supply Risk

- Environmental and Regulatory Risk

- Financial / Market Risk

- Regulatory Framework & Standards

- Global Regulatory Overview

- Key Regulations by Region

- EU: EU Tire Labeling Regulation (2020/740)

- USA: FMVSS 139, UTQG (Uniform Tire Quality Grading)

- China: GB Standards, CCC certification

- India: BIS standards, AIS-142

- Japan: JATMA standards

- Tire Labeling & Rating Systems

- Fuel Efficiency Rating

- Wet Grip Rating

- Noise Emission Rating

- Environmental Regulations

- Tire Microplastic Regulations

- End-Of-Life Tire (ELT) Recycling Mandates

- VOC Emissions from Tire Manufacturing

- EV-Specific Tire Standards

- Load Index Requirements for EV Weight

- Low Rolling Resistance Mandates

- Noise Reduction Requirements

- Safety & Performance Standards

- Unece Regulation 30 & 117

- Iso Tire Standards

- Regulatory Impact Analysis: Opportunities & Threats

- Global Passenger Car Tires Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume

- Market Size & Forecast by Demand Type

- OEM

- Replacement

- Market Size & Forecast by Rim Size

- 13″–15”

- 16”–17”

- 18”–19”

- 20” and above

- Market Size & Forecast by Tire Construction

- Radial

- Bias

- Market Size & Forecast by Season Type

- Summer Tires

- Winter Tires

- All-Season Tires

- Market Size & Forecast by Type

- Sedan

- Hatchback

- Luxury & Premium Cars

- SUVs

- Market Size & Forecast by Vehicle Propulsion

- ICE Passenger Cars

- Hybrid Passenger Cars

- Electric Passenger Cars

- Market Size & Forecast by Performance

- Standard Tires

- High Performance Tires

- Ultra-High-Performance Tires

- Asia-Pacific Passenger Car Tires Market Outlook

- Market Size & Forecast

- By Value

- By Volume

- By Demand Type

- By Rim Size

- By Tire Construction

- By Season Type

- By Type

- By Vehicle Propulsion

- By Performance

- Market Size & Forecast

- Europe Passenger Car Tires Market Outlook

- Market Size & Forecast

- By Value

- By Volume

- By Demand Type

- By Rim Size

- By Tire Construction

- By Season Type

- By Type

- By Vehicle Propulsion

- By Performance

- Market Size & Forecast

- North America Passenger Car Tires Market Outlook

- Market Size & Forecast

- By Value

- By Volume

- By Demand Type

- By Rim Size

- By Tire Construction

- By Season Type

- By Type

- By Vehicle Propulsion

- By Performance

- Market Size & Forecast

- Latin America Passenger Car Tires Market Outlook

- Market Size & Forecast

- By Value

- By Volume

- By Demand Type

- By Rim Size

- By Tire Construction

- By Season Type

- By Type

- By Vehicle Propulsion

- By Performance

- Market Size & Forecast

- Middle East & Africa Passenger Car Tires Market Outlook

- Market Size & Forecast

- By Value

- By Volume

- By Demand Type

- By Rim Size

- By Tire Construction

- By Season Type

- By Type

- By Vehicle Propulsion Tires

- By Performance

- Market Size & Forecast

- Country Wise* Passenger Car Tires Market Outlook

- Market Size & Forecast

- By Value

- By Volume

- By Demand Type

- By Rim Size

- By Tire Construction

- By Season Type

- By Type

- By Vehicle Propulsion

- By Performance

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, China, Germany, United Kingdom, Japan, Australia, France, The Netherlands, Singapore, India, Canada, Brazil, South Korea, UAE, Sweden, Ireland, Malaysia, Indonesia, Italy, Poland, Mexico, South Africa, Saudi Arabia, Finland, Thailand, Chile, Norway, Kenya, Vietnam, Qatar

- Technology & Innovation Analysis

- Tire Technology Evolution

- Smart & Connected Tires

- Airless / Non-Pneumatic Tires (NPT)

- Sustainable Tire Technologies

- Tire Compound & Material Innovation

- Manufacturing Technology

- Automation & Robotics in Tire Manufacturing

- AI-Based Quality Control

- 3D Printing in Tire Prototyping

- Industry 4.0 Adoption in Tire Plants

- Value Chain & Supply Chain Analysis

- Raw Material Suppliers

- Tire Manufacturers

- Distributors & Wholesalers

- Retailers & Fitment Centers

- OEM Supply Chain

- End Users (Consumers)

- Ecosystem Map

- Supply Chain Analysis

- Natural Rubber Supply (Southeast Asia Dependency)

- Synthetic Rubber & Petrochemical Inputs

- Carbon Black Supply Chain

- Steel Cord & Textile Cord

- Supply Chain Risk & Disruption Analysis

- Trade Flow Analysis

- Major Tire Exporting Countries

- Major Tire Importing Countries

- Tariff & Trade Barrier Analysis

- Raw Material Analysis

- Natural Rubber

- Global Production & Supply Dynamics

- Key Producing Countries (Thailand, Indonesia, Vietnam)

- Price Trend Analysis

- Supply Risk & Alternative Sourcing

- Synthetic Rubber

- Styrene-Butadiene Rubber (SBR)

- Butadiene Rubber (BR)

- Key Producers & Price Trends

- Petrochemical Feedstock Dependency

- Carbon Black

- Role in Tire Performance

- Price Trends & Supply Dynamics

- Recovered / Recycled Carbon Black (RCB) Emergence

- Silica

- Growing Use as Carbon Black Replacement

- Performance Benefits (Rolling Resistance, Wet Grip)

- Key Silica Suppliers

- Steel Cord & Textile Reinforcement

- Steel Cord for Belts & Bead

- Polyester, Nylon, Aramid Fiber Usage

- Key Suppliers

- Raw Material Cost Structure

- % Breakdown of Raw Material in Tire Cost

- Sensitivity Analysis, Impact of Rubber Price on Tire Pricing

- Natural Rubber

- Pricing Analysis

- Average Selling Price by Tier

- Premium Tier Pricing

- Mid-Tier Pricing

- Value / Economy Tier Pricing

- Price Trend Analysis (2021–2036)

- Sales & Distribution Channel Analysis

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented Vs Consolidated)

- Top 5 Players Market Share

- HHI (Herfindahl–Hirschman Index) Concentration Analysis

- Competitive Intensity Map

- Player Classification

- Market Leaders

- Strong Challengers

- Specialist / Niche Players

- Emerging Players

- Regional Players

- Competitive Analysis Frameworks

- Market Share Analysis

- Company Profile

- Company Overview & HQ

- Products & Solutions Portfolio

- Revenue & Cooling Segment Revenue

- Geographic Presence

- Recent Developments (M&A, Launches, Partnerships)

- SWOT Analysis

- Strategic Focus Areas

- Competitive Positioning Map

- Market Structure & Concentration

- Strategic Recommendations

- For Tire Manufacturers

- Product & Technology Strategy

- Ev Tire Portfolio Prioritization

- Sustainability & Circular Economy Strategy

- Geographic Expansion Priorities

- M&A & Partnership Strategy

- For OEMs & Automakers

- EV Tire Specification & Homologation Strategy

- Tire Supplier Diversification

- Sustainable Tire Procurement Commitments

- For Aftermarket & Retail Players

- E-Commerce & Omnichannel Strategy

- Private Label Tire Strategy

- Tire-As-A-Service (Taas) Opportunity

- For Investors & Private Equity

- High-Priority Investment Themes

- Smart Tire & Sustainable Material Startups

- Geographic Investment Priorities

- Risk Considerations

- Strategic Priority Matrix & Roadmap

- Near-term (2025–2028)

- Mid-term (2029–2032)

- Long-term (2023–2036)

- For Tire Manufacturers