Market Definition

The Global Advanced Battery Chemicals Market encompasses the production, processing, and supply of high-purity cathode active materials, anode active materials, electrolyte solvents and salts, binders, separators, conductive additives, and electrolyte additives used in the manufacturing of lithium-ion, solid-state, sodium-ion, lithium-sulfur, and next-generation electrochemical energy storage cells. The market includes battery-grade lithium carbonate, lithium hydroxide, cobalt sulfate, nickel sulfate, manganese compounds, graphite, silicon anode precursors, and fluorinated electrolyte chemicals procured by battery cell manufacturers, electric vehicle producers, stationary energy storage system developers, and consumer electronics companies globally.

Market Insights

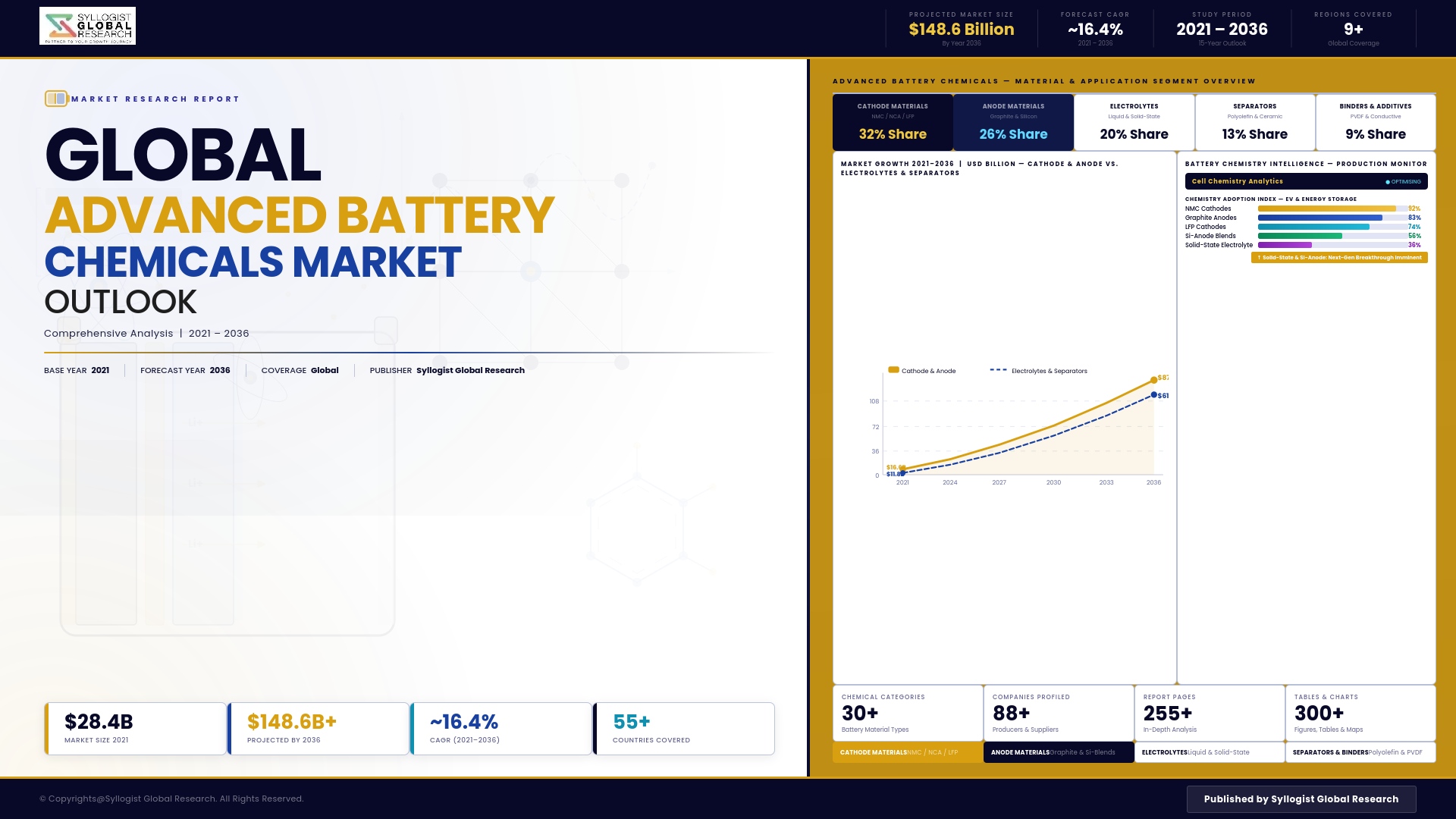

The global advanced battery chemicals market is experiencing an era of unprecedented investment and structural expansion, driven by the simultaneous acceleration of electric vehicle adoption across all major automotive markets, the rapid scaling of grid-scale stationary energy storage deployment supporting renewable power integration, and the intensifying geopolitical imperative among major economies to establish domestically resilient battery chemical supply chains that reduce strategic dependence on geographically concentrated raw material processing and refining infrastructure. The market was valued at approximately USD 38.7 billion in 2025 and is projected to reach USD 134.5 billion by 2034, advancing at a compound annual growth rate of 14.8% through the forecast period, as battery cell manufacturing capacity expands at an unprecedented pace across North America, Europe, and Asia-Pacific, each requiring continuous high-volume procurement of battery-grade chemical inputs at quality and consistency specifications that demand advanced processing capabilities beyond conventional industrial chemical production standards.

Cathode active materials represent the largest and most strategically consequential segment within the battery chemicals market, with lithium nickel manganese cobalt oxide and lithium iron phosphate formulations dominating current battery cell production volumes and their respective upstream precursor chemical supply chains generating the highest revenue intensity and the greatest geopolitical supply security scrutiny among battery manufacturers, automotive OEMs, and government procurement agencies seeking to reduce China-dependent supply chain concentration risk. The ongoing chemistry evolution within the cathode materials segment, including the progressive shift toward higher nickel content formulations offering superior energy density, the expanding market penetration of lithium iron phosphate driven by its lower cost and superior thermal stability for applications where energy density is a secondary priority, and the accelerating development of manganese-rich and sodium-ion alternatives, is generating continuous product reformulation demand and process chemistry investment requirements across the cathode chemical supply chain that sustain revenue growth above underlying volume expansion rates. Electrolyte chemistry innovation is simultaneously emerging as a critical performance and safety differentiation axis, with fluorinated solvent formulations, lithium bis(fluorosulfonyl)imide salt systems, and multifunctional additive packages enabling higher charge rate capability, extended cycle life, and improved low-temperature performance that translate directly into competitive differentiation for battery cell manufacturers competing for premium electric vehicle platform supply contracts.

The solid-state battery segment represents the highest-potential transformational opportunity within the advanced battery chemicals landscape over the forecast period, with ceramic and sulfide solid electrolyte materials, lithium metal anode processing chemicals, and interface compatibility coating chemistries constituting entirely new chemical supply categories whose commercial scale development is receiving concentrated investment from battery developers, chemical companies, and automotive OEM venture programs simultaneously. Anode material innovation, particularly the integration of silicon-dominant and silicon-graphite composite materials offering substantially higher lithium intercalation capacity than conventional graphite, is generating growing demand for silicon anode precursor chemicals and surface treatment agents capable of managing the volumetric expansion challenges that have historically constrained silicon anode commercial deployment. Asia-Pacific, led by China, South Korea, and Japan, maintains dominant market share in battery chemical production, processing, and supply, anchored by the regional concentration of battery cell manufacturing and the established chemical processing infrastructure servicing it. North America and Europe are investing aggressively in domestic battery chemical production capacity through industrial policy incentives, with the United States Inflation Reduction Act and European Union Battery Regulation creating regulatory demand pull for regionally sourced battery chemical supply that is reshaping global investment flows and supply chain architecture through the forecast period.

Key Drivers

Accelerating Global Electric Vehicle Production and Battery Cell Manufacturing Capacity Expansion Generating Sustained High-Volume Demand for Advanced Battery Chemical Inputs Across All Chemistries

The unprecedented scaling of electric vehicle production across China, Europe, and North America, combined with the parallel construction of battery cell gigafactory capacity across all three regions at volumes that will collectively represent a multi-fold increase in global battery chemical consumption relative to 2023 baseline levels, is generating structural long-term demand for cathode active materials, electrolyte systems, anode materials, and functional additives that is compelling battery chemical producers to execute major capacity expansion programs while simultaneously managing the chemistry evolution requirements driven by battery cell manufacturer specification upgrades toward higher energy density and faster charging formulations. This demand acceleration is creating favorable pricing environments and supply agreement structures for battery chemical producers able to demonstrate the quality consistency, supply security, and technical development support that automotive-qualified battery manufacturers require.

Government Industrial Policy Incentives and Domestic Battery Supply Chain Localization Mandates Driving Greenfield Battery Chemical Production Investment Across North America and Europe

The United States Inflation Reduction Act advanced manufacturing production credits, domestic content requirements for electric vehicle tax credit eligibility, and Department of Energy battery materials grant programs are collectively generating the largest government-backed investment mobilization in North American battery chemical production infrastructure in the sector’s history, compelling battery chemical producers, mining companies, and chemical manufacturers to accelerate domestic refining and processing capacity deployment that would not be financially justified under purely commercial market economics at current battery chemical price levels. Parallel industrial policy frameworks in the European Union, the United Kingdom, Canada, Australia, and India are creating a globally distributed battery chemical investment cycle that is fundamentally reshaping the geographic supply chain architecture of the industry beyond the Asia-Pacific concentration that has characterized it historically.

Battery Chemistry Innovation and Next-Generation Cell Architecture Development Creating Continuous New Specification Chemical Supply Opportunities Across Cathode, Anode, and Electrolyte Material Categories

The rapid pace of battery chemistry advancement, encompassing the commercialization of high-nickel cathode formulations, silicon anode integration, solid electrolyte material development, sodium-ion cell chemistry scale-up, and lithium-sulfur architecture progression, is generating continuous demand for new and reformulated battery chemical products whose performance specifications, purity requirements, and processing characteristics differ materially from established commercial chemistries, creating persistent product development and qualification investment cycles that sustain revenue growth and margin opportunity for battery chemical producers capable of advancing alongside battery cell developer technology roadmaps rather than supplying commoditized chemical inputs to static specifications.

Key Challenges

Critical Mineral Supply Concentration, Geopolitical Resource Nationalism, and Lithium, Cobalt, and Nickel Price Volatility Creating Procurement Security and Cost Management Challenges Across the Supply Chain

The global advanced battery chemicals industry confronts a fundamental supply security challenge arising from the extreme geographic concentration of lithium, cobalt, nickel, manganese, and natural graphite mining and primary processing across a small number of countries where resource nationalism policies, export restriction implementation, royalty regime changes, and geopolitical tension create procurement risk profiles of a magnitude that is driving battery manufacturers and automotive OEMs to require multi-source supply qualification, strategic inventory buffer programs, and long-term offtake agreements as standard procurement risk management practices. Commodity price volatility across lithium carbonate, cobalt, and nickel sulfate, which have demonstrated extreme price amplitude cycles in recent years, creates battery chemical cost planning challenges that propagate through battery cell cost structures into electric vehicle total cost of ownership economics and consumer pricing decisions.

Battery Chemical Purity and Consistency Requirements, Quality Certification Complexity, and Automotive-Grade Qualification Timelines Constraining New Supplier Market Entry and Capacity Ramp Speed

The quality specifications governing battery chemicals for automotive-grade lithium-ion cell applications demand trace impurity control at parts-per-million levels, particle size distribution precision, moisture content management, and batch-to-batch consistency standards that represent substantially more demanding production and quality assurance requirements than industrial chemical manufacturing norms, creating high barriers to new supplier qualification that involve multi-year testing, certification, and production validation programs before commercial supply volumes can be approved by battery cell manufacturer quality systems. The length and cost of automotive-grade battery chemical qualification processes mean that new capacity additions, whether from greenfield producers or established chemical companies entering battery materials, require long lead times between facility commissioning and meaningful commercial revenue generation, constraining the pace at which new supply can respond to demand growth and price incentives.

Spent Battery Chemical Recovery Infrastructure Immaturity, Recycling Economics Uncertainty, and Regulatory Compliance Complexity Constraining Circular Economy Material Flow Integration

The long-term sustainability and resource security of the advanced battery chemicals industry depends critically on the development of economically viable closed-loop recycling systems capable of recovering high-purity lithium, cobalt, nickel, and manganese from end-of-life battery cells at unit economics competitive with primary mining and processing, but the immaturity of commercial-scale spent battery collection infrastructure, the variability of incoming battery chemistry and physical condition across recycling feedstock streams, and the technical complexity of hydrometallurgical and pyrometallurgical processing at commercially viable recovery rates and purity specifications are creating recycling economics that remain challenging outside favorable regulatory subsidy frameworks, constraining the pace of circular material flow integration into primary battery chemical supply chains.

Market Segmentation

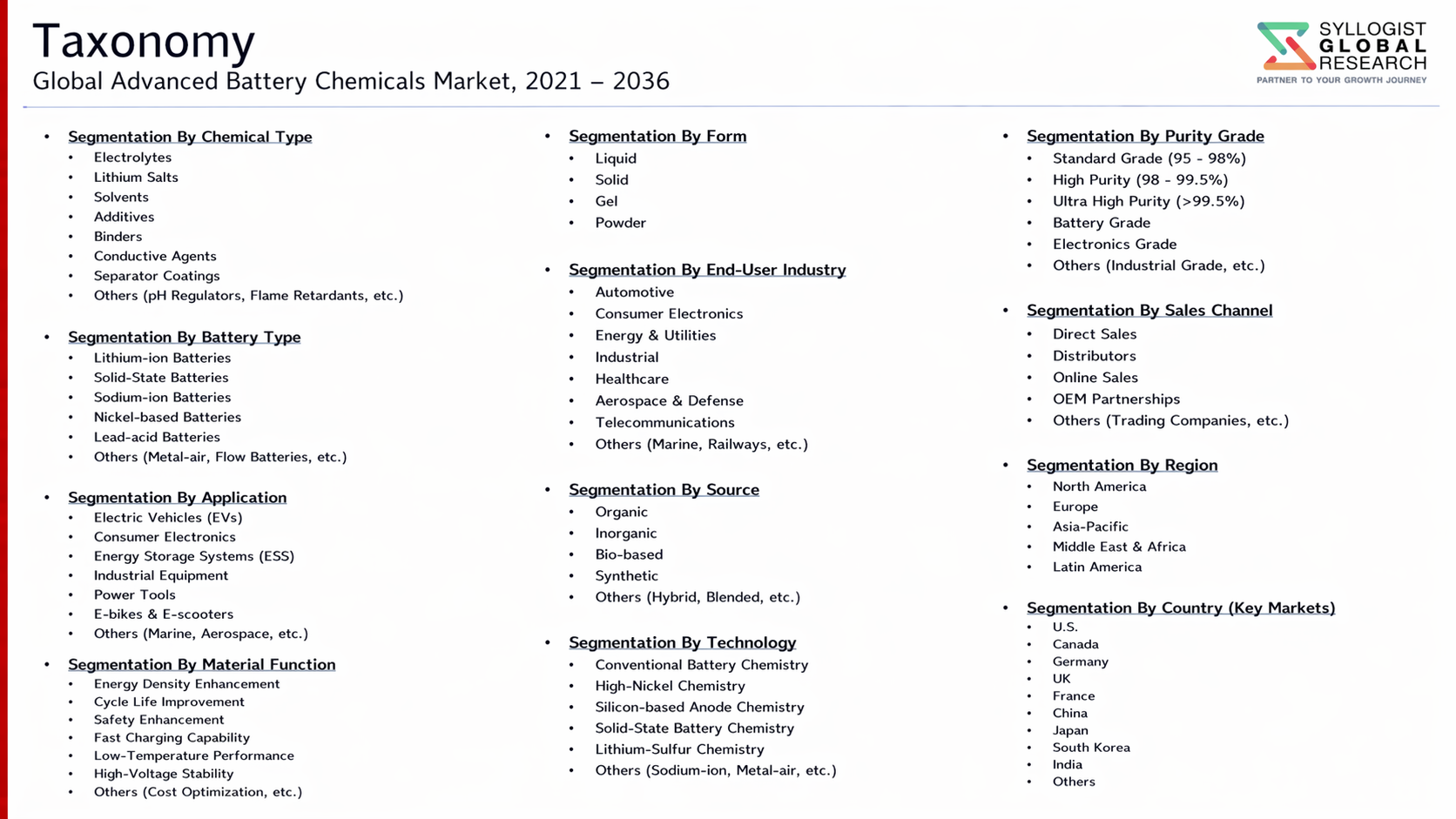

- Segmentation By Chemical Type

- Cathode Active Materials (NMC, NCA, LFP, LCO, LMNO)

- Anode Active Materials (Graphite, Silicon, Lithium Metal)

- Electrolyte Solvents and Lithium Salt Systems

- Electrolyte Functional Additives

- Binders and Conductive Carbon Additives

- Separator Coatings and Surface Treatment Chemicals

- Solid Electrolyte Materials (Oxide, Sulfide, Polymer)

- Others

- Segmentation By Battery Type

- Lithium-Ion Batteries (NMC and NCA Chemistry)

- Lithium Iron Phosphate (LFP) Batteries

- Solid-State Batteries

- Sodium-Ion Batteries

- Lithium-Sulfur Batteries

- Lithium-Metal and Next-Generation Anode Batteries

- Others

- Segmentation By Application

- Electric Vehicle Battery Packs

- Grid-Scale Stationary Energy Storage Systems

- Consumer Electronics and Portable Devices

- Industrial and Heavy Equipment Energy Storage

- Aerospace and Defense Energy Storage

- Marine and Off-Highway Vehicle Electrification

- Others

- Segmentation By End User

- Battery Cell Manufacturers and Gigafactory Operators

- Electric Vehicle Original Equipment Manufacturers

- Stationary Energy Storage System Integrators

- Consumer Electronics Manufacturers

- Battery Recycling and Second-Life Processing Companies

- Research Institutions and Battery Development Laboratories

- Others

- Segmentation By Purity Grade

- Automotive-Grade Battery Chemicals (Highest Purity)

- Industrial-Grade Battery Chemicals

- Research and Development Grade Chemicals

- Segmentation By Distribution Channel

- Direct Supply Agreements with Battery Cell Manufacturers

- Chemical Distributor and Trading Company Networks

- Spot Market and Exchange-Based Procurement

- Long-Term Offtake and Strategic Partnership Agreements

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Advanced Battery Chemicals Market in 2025, projected through 2034, disaggregated by chemical type, battery type, and application, enabling battery manufacturers, chemical producers, mining companies, and investors to identify the highest-growth material categories and most durable revenue opportunities across the battery chemical value chain?

- How are cathode active material chemistry transitions, including the shift toward higher-nickel NMC formulations and expanding LFP adoption, reshaping upstream precursor chemical demand volumes and specifications, and which cathode chemistry trajectories are expected to define the largest procurement volumes and highest per-kilogram value segments through 2034?

- What impact are the United States Inflation Reduction Act domestic content requirements, European Union Battery Regulation sourcing mandates, and allied nation industrial policy frameworks having on battery chemical supply chain geographic restructuring, greenfield investment decisions, and the competitive positioning of non-Asian battery chemical producers through the forecast period?

- Which advanced battery chemical segments, including solid electrolyte materials, silicon anode precursors, and high-voltage electrolyte additive systems, are generating the highest technology development investment and near-term commercialization momentum, and what qualification timelines and performance benchmarks are defining their integration into next-generation battery cell platform programs?

- How is the competitive landscape structured among established Asian battery chemical producers, emerging Western chemical manufacturers, mining company downstream integration initiatives, and battery recycling feedstock providers, and what technology, capacity, and customer partnership strategies are enabling leading participants to secure long-term supply agreements with automotive-qualified battery cell manufacturers?

- What critical mineral supply concentration risks, price volatility dynamics, and export restriction frameworks across lithium, cobalt, nickel, and graphite are shaping battery chemical procurement strategy for automotive OEMs and battery manufacturers, and how are supply chain diversification, strategic inventory, and recycled material integration programs being structured to manage these risks?

- Which regional battery chemical markets, specifically Asia-Pacific, North America, and Europe, are expected to generate the most substantial production capacity investment and demand growth through 2034, and what electric vehicle production trajectories, gigafactory buildout programs, and industrial policy incentive frameworks are driving chemical supply chain investment decisions in each region?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Raw Material Supply, Critical Mineral Concentration & Geopolitical Risk

- Battery Chemistry Disruption, Technology Obsolescence & Transition Risk

- Regulatory, Safety Compliance & Environmental Permitting Risk

- Quality Control, Battery Performance & Thermal Runaway Risk

- Capital Investment, Gigafactory Offtake & Demand Volatility Risk

- Regulatory Framework & Standards

- Critical Mineral Sourcing, Responsible Mining & Conflict Mineral Compliance Policy Frameworks

- Battery Passport, Traceability & Digital Product Identification Standards

- Battery Material Safety, REACH, TSCA & Chemical Registration Requirements

- End-of-Life, Recycling, Extended Producer Responsibility & Circular Economy Regulations

- Green Finance, ESG Disclosure & Sustainable Battery Manufacturing Procurement Standards

- Global Advanced Battery Chemicals Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Kilotons)

- Market Size & Forecast by Chemical Type

- Cathode Active Materials (LFP, NMC, NCA, LCO, LMO & High-Nickel Chemistries)

- Anode Active Materials (Natural Graphite, Synthetic Graphite, Silicon & Silicon-Oxide Composites)

- Electrolyte Solutions, Lithium Salts (LiPF6, LiFSI, LiTFSI) & Carbonate Solvents

- Separator Materials (Polyolefin, Ceramic-Coated & Non-Woven Separators)

- Binders, Conductive Additives & Current Collector Foils

- Solid-State Electrolytes (Sulphide, Oxide & Polymer-Based)

- Precursor Materials (Nickel Sulphate, Cobalt Sulphate, Manganese Sulphate & Lithium Hydroxide)

- Sodium-Ion Battery Active Materials (Prussian Blue, Polyanionic & Layered Oxide Chemistries)

- Next-Generation Chemistries (Lithium Metal, Lithium Sulphur & Silicon-Dominant Anodes)

- Market Size & Forecast by Battery Type

- Lithium Iron Phosphate (LFP) Batteries

- Nickel Manganese Cobalt (NMC & NCM) Batteries

- Nickel Cobalt Aluminium (NCA) Batteries

- Lithium Cobalt Oxide (LCO) & Lithium Manganese Oxide (LMO) Batteries

- Sodium-Ion Batteries

- Solid-State Lithium Batteries

- Lithium Sulphur & Lithium Air Batteries

- Lead-Acid & Advanced Lead-Carbon Batteries

- Flow Batteries (Vanadium Redox, Zinc-Bromine & Iron-Air Chemistries)

- Market Size & Forecast by Form

- Powder, Granule & Pelletised Solid Materials

- Liquid Electrolyte & Solvent Blends

- Film, Foil & Coated Sheet Materials

- Slurry, Paste & Coating Formulations

- Gel, Polymer & Solid-State Composite Materials

- Market Size & Forecast by Manufacturing Process

- Co-Precipitation & Hydroxide Precursor Synthesis

- Solid-State Calcination & Sintering Process

- Sol-Gel & Spray Pyrolysis Process

- Electrochemical & Hydrothermal Synthesis

- Market Size & Forecast by Application

- Electric Vehicle (Passenger Cars, Commercial Vehicles & Two-Wheelers) Batteries

- Stationary Energy Storage & Grid-Scale Battery Systems

- Consumer Electronics (Smartphones, Laptops & Wearables) Batteries

- Industrial, Material Handling & Forklift Batteries

- Power Tools, Medical Devices & Specialty Batteries

- Aerospace, Defence & Marine Batteries

- Market Size & Forecast by End-User

- Battery Cell Manufacturers & Gigafactory Operators

- Electric Vehicle OEMs with In-House Cell Production

- Energy Storage System Integrators & Utility Operators

- Consumer Electronics & Device Manufacturers

- Industrial Equipment & Speciality Battery Pack Assemblers

- Market Size & Forecast by Sales Channel

- Direct Long-Term Offtake & Gigafactory Supply Contract

- Distributor, Trading & Spot Market Sales

- Joint Venture, Strategic Alliance & Integrated Supply

- Tolling, Contract Manufacturing & Custom Formulation Services

- North America Advanced Battery Chemicals Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotons)

- By Chemical Type

- By Battery Type

- By Form

- By Manufacturing Process

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Advanced Battery Chemicals Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotons)

- By Chemical Type

- By Battery Type

- By Form

- By Manufacturing Process

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Advanced Battery Chemicals Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotons)

- By Chemical Type

- By Battery Type

- By Form

- By Manufacturing Process

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Advanced Battery Chemicals Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotons)

- By Chemical Type

- By Battery Type

- By Form

- By Manufacturing Process

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Advanced Battery Chemicals Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotons)

- By Chemical Type

- By Battery Type

- By Form

- By Manufacturing Process

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Advanced Battery Chemicals Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotons)

- By Chemical Type

- By Battery Type

- By Form

- By Manufacturing Process

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

*Countries Analysed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Norway, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Technology Landscape & Innovation Analysis

- Cathode Active Material Technology Deep-Dive (LFP, NMC, NCA, High-Nickel & Cobalt-Free Chemistries)

- Anode Active Material Technology (Graphite, Silicon-Dominant & Lithium Metal Anodes)

- Electrolyte, Salt & Solvent Technology for Next-Generation Liquid Electrolytes

- Solid-State Electrolyte & All-Solid-State Battery Material Technology

- Separator, Binder & Conductive Additive Technology

- Battery Precursor, Critical Mineral Refining & Upstream Processing Technology

- Battery Recycling, Black Mass Processing & Secondary Material Recovery Technology

- Patent & IP Landscape in Advanced Battery Chemical Technologies

- Value Chain & Supply Chain Analysis

- Lithium, Nickel, Cobalt, Manganese & Graphite Mining and Refining Supply Chain

- Cathode & Anode Active Material Manufacturing Supply Chain

- Electrolyte, Salt, Solvent & Separator Production Supply Chain

- Precursor & Intermediate Chemical Supply Chain

- Battery Cell Manufacturer, Gigafactory & OEM Procurement Landscape

- Electric Vehicle, Energy Storage & Consumer Electronics Offtake Channel

- Battery Recycling, Black Mass Trading & Circular Supply Loop

- Pricing Analysis

- Cathode Active Material (LFP, NMC, NCA) Pricing and Cost Structure Analysis

- Anode Active Material (Graphite & Silicon) Pricing and Margin Analysis

- Electrolyte, Lithium Salt & Solvent Pricing and Raw Material Cost Pass-Through Analysis

- Critical Mineral & Precursor Pricing Trend and Volatility Analysis

- Battery Chemical Long-Term Offtake Contract, Indexation & Pricing Structure Analysis

- Total Battery Pack Chemical Cost Economics: Cost per kWh & Learning Curve Analysis

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Advanced Battery Chemicals: Carbon Footprint, Energy Intensity & Water Footprint Across Chemistry Routes

- Carbon Neutrality & Net Zero Contribution: Pathway to Low-Carbon Battery Manufacturing and Green Chemical Production

- Responsible Sourcing, Critical Mineral Due Diligence & Conflict-Free Supply Chain Contribution

- Environmental Compliance, Hazardous Chemical Management & Water Discharge Consideration in Battery Chemical Production

- Regulatory-Driven Sustainability, Battery Passport, SDG 7 (Affordable Energy) & SDG 12 (Responsible Consumption) Alignment & Green Finance Eligibility

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Chemical Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Chemical Type, Battery Type & Geography

- Player Classification

- Integrated Battery Material & Critical Mineral Companies

- Specialist Cathode Active Material Producers

- Anode Material, Graphite & Silicon Technology Providers

- Electrolyte, Salt & Solvent Chemical Manufacturers

- Separator, Binder & Conductive Additive Suppliers

- Solid-State Electrolyte & Next-Generation Chemistry Innovators

- Battery Recyclers & Black Mass Processing Companies

- Precursor, Intermediate & Custom Chemical Tolling Specialists

- Competitive Analysis Frameworks

- Market Share Analysis by Chemical Type, Battery Type & Region

- Company Profile

- Company Overview & Headquarters

- Advanced Battery Chemical Products & Technology Portfolio

- Key Customer Relationships & Reference Gigafactory Supply Contracts

- Manufacturing Footprint & Production Capacity

- Revenue (Battery Chemical Segment) & Order Book

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Chemical Type, Battery Type, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Output

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)