Market Definition

The Global Automotive Brake Systems Market encompasses the design, manufacturing, supply, and aftermarket servicing of hydraulic disc brakes, drum brakes, anti-lock braking systems, electronic stability control systems, regenerative braking systems, electromechanical brake-by-wire architectures, and integrated brake control modules deployed across passenger cars, light commercial vehicles, heavy commercial vehicles, motorcycles, and off-highway equipment. The market includes brake calipers, rotors, pads, master cylinders, brake boosters, electronic control units, and hydraulic actuation hardware procured by original equipment manufacturers, aftermarket distributors, fleet operators, and vehicle service providers globally.

Market Insights

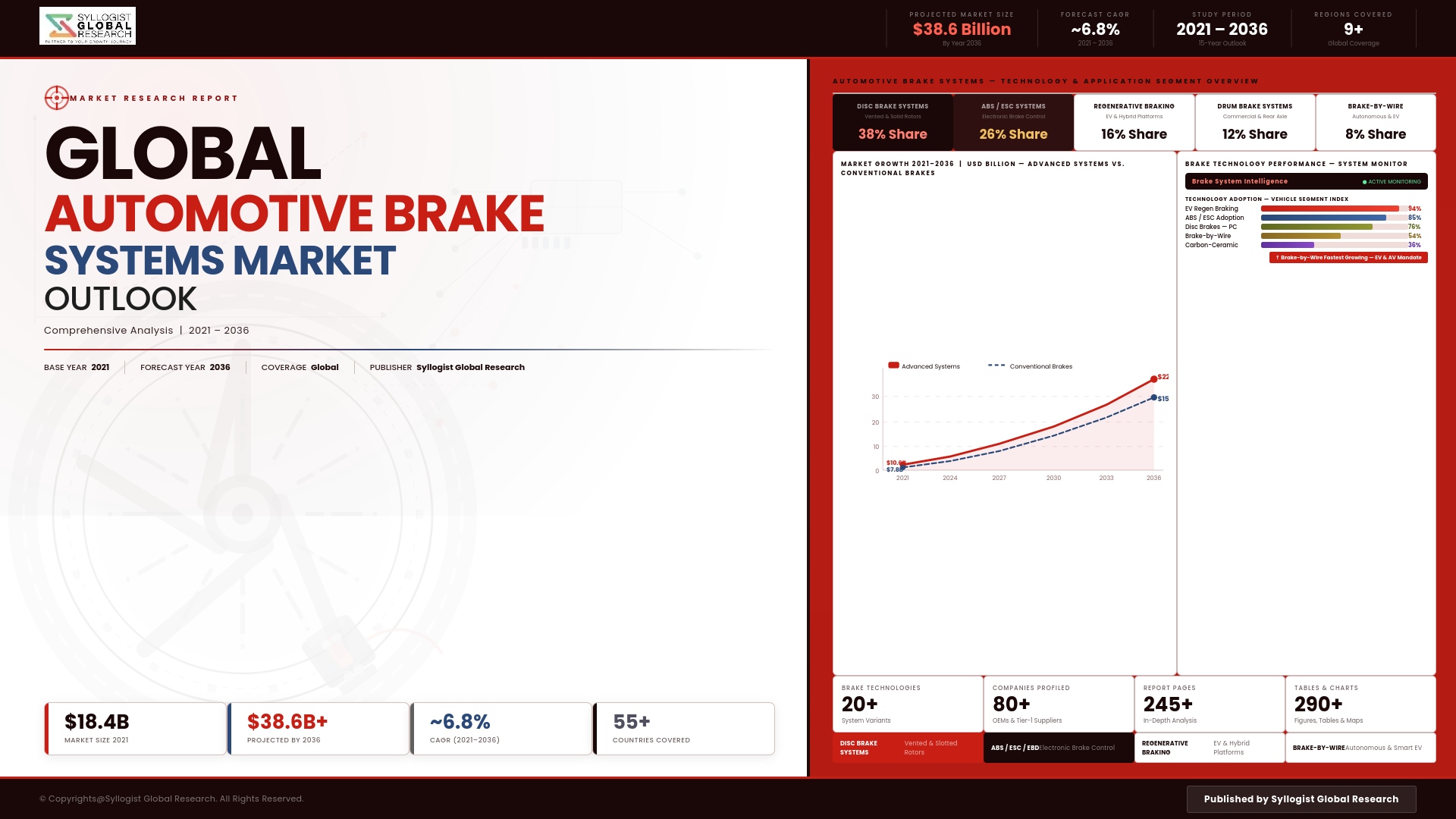

The global automotive brake systems market is navigating a period of simultaneous technological reinvention and steady volume-driven growth, propelled by expanding global vehicle production, progressively stringent vehicle safety regulations mandating advanced braking system integration across new vehicle categories and emerging markets, and the structural transformation of braking architecture driven by electric vehicle adoption that is displacing conventional vacuum-assisted hydraulic systems in favor of electromechanical and regenerative braking configurations. The market was valued at approximately USD 29.8 billion in 2025 and is projected to reach USD 46.2 billion by 2034, advancing at a compound annual growth rate of 5.0% through the forecast period, as global vehicle production recovery, EV-specific brake system demand, and mandatory advanced driver assistance system integration requirements collectively sustain multi-year revenue growth across both original equipment and aftermarket brake system supply segments.

The most consequential technology transition reshaping the global brake systems landscape is the rapid proliferation of regenerative braking architectures within battery electric and hybrid electric vehicle platforms, where the fundamental energy recovery requirement of electrified powertrains demands brake-by-wire and integrated regenerative-friction blending systems capable of seamlessly coordinating electric motor deceleration torque with conventional friction braking actuation to deliver transparent pedal feel and regulatory stopping distance compliance across the full deceleration range. This architectural shift is generating entirely new component demand categories including electromechanical caliper actuators, high-voltage brake control electronics, and sophisticated integrated brake control modules that represent substantially higher per-vehicle content value compared with the vacuum-assisted hydraulic systems they replace, driving average selling price elevation across the brake system supply chain even as unit volume growth remains moderate. The regenerative braking segment is simultaneously creating technical differentiation opportunity for brake system suppliers capable of delivering the software-defined brake blending algorithms and electromechanical actuator precision necessary to meet the stringent pedal feel, noise-vibration-harshness, and energy recovery efficiency specifications demanded by premium and volume electric vehicle platform programs.

Advanced driver assistance system integration is generating a second major growth vector within the brake system market, as automatic emergency braking, adaptive cruise control, and autonomous emergency braking functions require brake systems with electronically controlled hydraulic actuation response times, pressure modulation precision, and fail-safe redundancy architectures that exceed the capabilities of conventional brake hardware designed for human-initiated deceleration inputs. Mandatory automatic emergency braking requirements across the European Union, the United States, China, and increasingly across emerging market regulatory frameworks are creating volume demand for electronically integrated brake systems across vehicle categories and price points where such capabilities were previously limited to premium vehicle segments. The Asia-Pacific region is projected to record the highest compound annual growth rate through 2034, anchored by vehicle production growth in India, Southeast Asia, and continued expansion in China, combined with regulatory safety requirement upgrades progressively mandating anti-lock braking and electronic stability control systems across commercial vehicle and two-wheeler categories that represent large volume opportunities in these markets. North America and Europe maintain substantial market shares driven by high vehicle safety standard compliance requirements, strong aftermarket replacement demand from large installed vehicle fleets, and the leading concentration of electric vehicle adoption generating premium brake system content opportunity.

Key Drivers

Electric Vehicle Platform Proliferation and Regenerative Braking Architecture Requirements Driving Substantial Brake System Content Value Elevation and New Component Category Demand

The accelerating global transition toward battery electric and hybrid electric vehicle platforms is fundamentally restructuring brake system content requirements, replacing conventional vacuum booster and hydraulic master cylinder architectures with electromechanical brake-by-wire systems, integrated regenerative-friction blending control modules, and electrically actuated caliper systems that deliver substantially higher per-vehicle revenue to brake system suppliers while demanding new engineering capabilities in software-defined brake blending, electromechanical actuator precision, and high-voltage electronics integration. As electric vehicle production volumes scale across both premium and mainstream vehicle segments in China, Europe, and North America, the aggregate shift in brake system architecture is generating a structural revenue mix improvement within the brake system supply chain that is sustaining market value growth at rates meaningfully exceeding underlying vehicle production volume growth across the forecast period.

Mandatory Advanced Driver Assistance System Regulations and Automatic Emergency Braking Mandates Expanding Electronically Integrated Brake System Requirements Across Vehicle Categories

The progressive global implementation of mandatory automatic emergency braking, electronic stability control, and autonomous emergency braking regulatory requirements across passenger cars, light commercial vehicles, and heavy trucks is generating durable volume demand for electronically actuated brake systems with the rapid response times, pressure modulation precision, and control system integration architectures required to support ADAS function execution across the full operating speed and load range of regulated vehicle categories. Regulatory mandates in the European Union, the United States National Highway Traffic Safety Administration framework, Chinese national vehicle safety standards, and progressively across Asian and Latin American regulatory regimes are extending advanced brake system integration requirements to vehicle price segments and categories where such capabilities were previously absent, substantially expanding the addressable market for electronically integrated brake system hardware and control software.

Rising Global Vehicle Parc Expansion and Growing Aftermarket Replacement Demand Across Emerging Markets Generating Sustained Brake Component Revenue Independent of New Vehicle Production Cycles

The continued expansion of the global vehicle parc, particularly across rapidly motorizing emerging markets in India, Southeast Asia, Africa, and Latin America where vehicle ownership rates remain substantially below developed market levels, is generating a structurally growing aftermarket brake component replacement demand base that provides revenue stability through new vehicle production cycle downturns and supports sustained multi-year volume growth in brake pad, rotor, caliper, and hydraulic system replacement parts. The aftermarket brake segment benefits from non-discretionary replacement demand characteristics driven by safety-critical component wear cycles, regulatory vehicle inspection requirements mandating minimum brake performance standards, and consumer safety awareness that prioritizes brake system maintenance across vehicle ownership demographics, creating a demand profile substantially less cyclical than original equipment brake system supply revenues.

Key Challenges

Brake-by-Wire and Electromechanical System Development Complexity, Functional Safety Certification Requirements, and Fail-Safe Redundancy Architecture Costs Constraining Technology Transition Economics

The transition from conventional hydraulic brake architectures to electromechanical brake-by-wire systems required for electric vehicle and advanced autonomous driving platform integration demands engineering investment in functional safety architecture compliance with ISO 26262 automotive safety integrity level requirements, redundant actuation pathway design, and software validation programs of a complexity and cost that substantially exceed the development economics of the hydraulic brake systems they replace, creating non-recurring engineering cost burdens that challenge the financial returns of brake system suppliers whose historical product portfolios have been optimized around hydraulic component manufacturing competencies rather than electromechanical system development and automotive-grade software validation capabilities. Achieving the fail-operational system architecture required for autonomous vehicle brake applications adds further redundancy and cost requirements that elevate brake system development investment to levels demanding substantial revenue scale to justify.

Brake Dust and Particulate Emission Regulations Creating Material and Design Constraints on Friction Material Formulation and Brake System Architecture Development Programs

Emerging regulatory frameworks governing non-exhaust particulate emissions from brake friction materials, led by the European Union Euro 7 regulation introducing mandatory brake dust emission limits for the first time, are compelling brake pad and friction material developers to reformulate compound chemistries away from copper and other metallic constituents that contribute to regulated particulate emissions, imposing material science development costs, friction performance recertification requirements, and supply chain transition obligations across brake pad manufacturing operations that add complexity and investment requirements to brake system development programs simultaneously managing the broader technology transition toward electromechanical architectures. Achieving compliant low-emission friction material performance across the full brake temperature, load, and environmental operating range while maintaining stopping distance performance and pad wear life required by vehicle homologation standards represents a non-trivial materials engineering challenge with meaningful development cost and timeline implications.

Raw Material Price Volatility, Steel and Specialty Alloy Supply Chain Disruption, and Cost Inflation Pressuring Brake System Supplier Margins Across Original Equipment and Aftermarket Channels

Brake system manufacturing relies on steel stampings, grey cast iron rotors and drums, copper-containing friction materials, aluminium caliper castings, and specialty electronic components whose procurement costs are subject to commodity market volatility, supply chain disruption, and energy cost inflation that collectively compress brake system supplier operating margins when raw material cost increases cannot be recovered through customer price adjustments within the contractually constrained pricing frameworks governing original equipment supply agreements with automotive manufacturers. The aftermarket channel, while offering greater pricing flexibility than OEM supply contracts, faces margin pressure from low-cost import competition across brake pad and rotor categories where product differentiation is limited, creating a dual-channel margin compression dynamic that challenges brake system supplier profitability during commodity price escalation cycles.

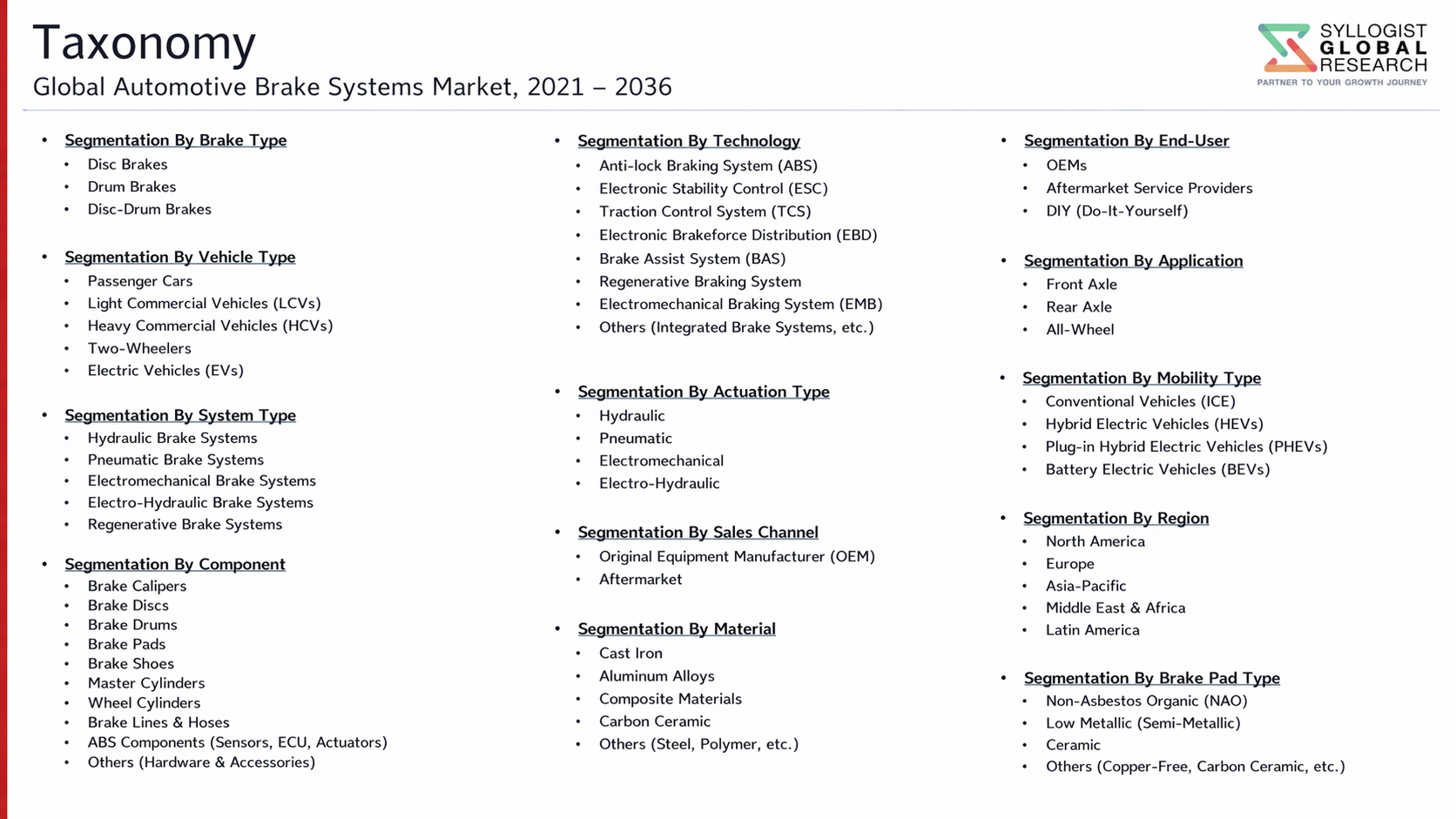

Market Segmentation

- Segmentation By System Type

- Hydraulic Disc Brake Systems

- Hydraulic Drum Brake Systems

- Anti-Lock Braking Systems (ABS)

- Electronic Stability Control (ESC) and Traction Control Systems

- Regenerative Braking Systems

- Electromechanical Brake-by-Wire Systems

- Integrated Brake Control and ADAS Actuation Systems

- Others

- Segmentation By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles and Trucks

- Buses and Coaches

- Two-Wheelers and Motorcycles

- Off-Highway and Agricultural Vehicles

- Electric and Hybrid Electric Vehicles

- Others

- Segmentation By Technology

- Conventional Hydraulic Brake Technology

- Electronic Brake Force Distribution (EBD)

- Brake Assist Systems (BAS)

- Autonomous Emergency Braking (AEB)

- Regenerative and Blended Braking Technology

- Electromechanical and Brake-by-Wire Technology

- Others

- Segmentation By Component

- Brake Calipers and Caliper Actuation Hardware

- Brake Rotors and Discs

- Brake Pads and Friction Materials

- Drum Brakes and Brake Shoes

- Master Cylinders and Brake Boosters

- Electronic Control Units and Hydraulic Modulator Assemblies

- Brake Lines, Hoses, and Fluid Systems

- Others

- Segmentation By Sales Channel

- Original Equipment Manufacturer (OEM) Supply

- Independent Aftermarket Distribution

- Authorized Dealer and OEM Aftersales Network

- Online Retail and E-Commerce Platforms

- Segmentation By End User

- Passenger Vehicle Owners and Individual Consumers

- Commercial Fleet Operators

- Automotive OEM Assembly Plants

- Independent Repair and Service Workshops

- Authorized Dealer Service Centers

- Government and Municipal Fleet Authorities

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Automotive Brake Systems Market in 2025, projected through 2034, disaggregated by system type, vehicle type, and technology, enabling OEM suppliers, aftermarket distributors, and investors to identify the highest-growth segments and most durable revenue opportunities across the evolving brake system technology landscape?

- How is the rapid proliferation of electric and hybrid vehicle platforms reshaping brake system architecture requirements, and which regenerative braking, brake-by-wire, and integrated control module technologies are capturing the largest OEM content share and defining the performance benchmarks shaping brake system procurement competitiveness through 2034?

- What impact are mandatory automatic emergency braking, electronic stability control, and autonomous emergency braking regulatory requirements across the European Union, the United States, China, and emerging markets having on brake system integration specifications, average content value per vehicle, and addressable market expansion across previously unregulated vehicle categories?

- Which brake system segments, including electromechanical brake-by-wire, regenerative braking integration, and ADAS-compatible hydraulic actuation systems, are generating the highest OEM revenue growth through 2034, and what functional safety certification, fail-safe redundancy, and software integration capabilities are most critical to supplier platform selection?

- How is the competitive landscape structured among global brake system Tier 1 suppliers, regional component manufacturers, and emerging electromechanical brake technology developers, and what technology investment, electrification transition, and customer partnership strategies are enabling leading suppliers to defend and expand market positions across OEM and aftermarket channels?

- What challenges do brake dust emission regulations, low-emission friction material reformulation requirements, and raw material cost volatility present to brake system suppliers across OEM and aftermarket channels, and how are manufacturers addressing friction compound development, supply chain resilience, and margin protection strategies within constrained OEM pricing frameworks?

- Which regional automotive brake system markets, specifically Asia-Pacific, North America, and Europe, are expected to generate the most substantial incremental revenue growth through 2034, and what vehicle production trajectories, EV adoption rates, safety regulation implementation timelines, and aftermarket fleet size dynamics are shaping demand and supplier selection in each region?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Raw Material Price Volatility: Friction Material, Steel, Cast Iron & Copper Alternative Sourcing Risk

- EV Transition Impact: Reduced Friction Brake Wear, Regenerative Braking Cannibalisation & Aftermarket Volume Erosion Risk

- Stringent Brake Dust & Particulate Emission Regulation Compliance Risk Across Key Markets

- OEM Platform Consolidation, Single-Source Brake System Award & Tier 1 Supplier Revenue Concentration Risk

- Counterfeit Brake Components, Grey Market Penetration & Safety Liability Risk in Aftermarket Channels

- Regulatory Framework & Standards

- UN Regulation No. 13 & UN Regulation No. 13-H: Heavy Vehicle & Passenger Car Braking Performance Standards

- FMVSS 105, FMVSS 121 & FMVSS 135: US Federal Motor Vehicle Safety Standards for Hydraulic, Air & Passenger Car Brake Systems

- Euro 7 Brake Particle Emission Regulation: Particle Number (PN) & Mass Emission Limits for Brake Wear Particulates

- ISO 26262 Functional Safety Standard for Brake-by-Wire, Electronic Brake Control & ADAS-Integrated Braking Systems

- RoHS, REACH & Copper-Free Brake Pad Legislation: California AB 2762, Washington State SB 6557 & Global Hazardous Material Restrictions for Friction Materials

- Global Automotive Brake Systems Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Number of Units & Sets)

- Market Size & Forecast by System Type

- Disc Brake System

- Drum Brake System

- Anti-Lock Braking System (ABS)

- Electronic Stability Control (ESC) & Traction Control System (TCS)

- Electronic Parking Brake (EPB) System

- Regenerative Braking System

- Brake-by-Wire (BBW) System: Electro-Hydraulic & Electro-Mechanical

- Integrated Braking System (IBS) for ADAS & Autonomous Vehicle Applications

- Market Size & Forecast by Component

- Brake Caliper: Fixed, Floating & Electric Parking Brake Caliper

- Brake Disc & Rotor: Cast Iron, Carbon Ceramic & Composite Disc

- Brake Pad & Friction Material: NAO, Low-Metallic, Semi-Metallic & Ceramic Pad

- Brake Drum & Brake Shoe Assembly

- Brake Master Cylinder & Hydraulic Booster

- Electronic Brake Control Module (EBCM), ABS & ESC ECU

- Electric Brake Booster (EBB) & Integrated Brake Unit (IBU)

- Brake Lines, Hoses & Hydraulic Fluid

- Market Size & Forecast by Actuation Technology

- Hydraulic Brake Actuation

- Pneumatic & Air Brake Actuation

- Electro-Hydraulic Brake (EHB) Actuation

- Electro-Mechanical Brake (EMB) & Brake-by-Wire Actuation

- Regenerative & Blended Braking Actuation for Electrified Vehicles

- Market Size & Forecast by Vehicle Type

- Passenger Cars & Light Duty Vehicles

- Light Commercial Vehicles (LCV) & Vans

- Medium & Heavy Commercial Vehicles (MHCV): Trucks & Buses

- Off-Highway, Construction & Agricultural Vehicles

- Two-Wheelers & Three-Wheelers

- Battery Electric Vehicles (BEV)

- Plug-in Hybrid Electric Vehicles (PHEV) & Hybrid Electric Vehicles (HEV)

- Market Size & Forecast by Sales Channel

- Original Equipment Manufacturer (OEM) Channel

- Original Equipment Service (OES) Aftermarket Channel

- Independent Aftermarket (IAM) Channel

- E-Commerce & Online Retail Aftermarket Channel

- Market Size & Forecast by Application

- Conventional Internal Combustion Engine (ICE) Vehicle Braking

- Electrified Vehicle Braking: BEV, PHEV & HEV Integrated Regenerative & Friction Braking

- ADAS-Integrated Automatic Emergency Braking (AEB) & Collision Avoidance

- Autonomous & Highly Automated Vehicle Brake-by-Wire & Redundant Braking

- High-Performance, Sports & Premium Vehicle Braking

- Market Size & Forecast by End-User

- Passenger Vehicle OEMs & Tier 1 Automotive Suppliers

- Commercial Vehicle OEMs & Fleet Operators

- Independent Workshop, Garage & Service Centre Operators

- Specialist Performance, Motorsport & Aftermarket Retrofit Customers

- North America Automotive Brake Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Units & Sets)

- By System Type

- By Component

- By Actuation Technology

- By Vehicle Type

- By Sales Channel

- By Application

- By End-User

- By Country

- Market Size & Forecast

- Europe Automotive Brake Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Units & Sets)

- By System Type

- By Component

- By Actuation Technology

- By Vehicle Type

- By Sales Channel

- By Application

- By End-User

- By Country

- Market Size & Forecast

- Asia-Pacific Automotive Brake Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Units & Sets)

- By System Type

- By Component

- By Actuation Technology

- By Vehicle Type

- By Sales Channel

- By Application

- By End-User

- By Country

- Market Size & Forecast

- Latin America Automotive Brake Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Units & Sets)

- By System Type

- By Component

- By Actuation Technology

- By Vehicle Type

- By Sales Channel

- By Application

- By End-User

- By Country

- Market Size & Forecast

- Middle East & Africa Automotive Brake Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Units & Sets)

- By System Type

- By Component

- By Actuation Technology

- By Vehicle Type

- By Sales Channel

- By Application

- By End-User

- By Country

- Market Size & Forecast

- Country-Wise* Automotive Brake Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Units & Sets)

- By System Type

- By Component

- By Actuation Technology

- By Vehicle Type

- By Sales Channel

- By Application

- By End-User

- By Country

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Norway, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Technology Landscape & Innovation Analysis

- Brake-by-Wire (BBW), Electro-Mechanical Brake (EMB) & Integrated Brake Unit (IBU) Technology Deep-Dive

- Regenerative Braking, Blended Braking Control & Energy Recovery Optimisation Technology for EVs and PHEVs

- Copper-Free & Low-Emission Friction Material: NAO, Ceramic & Bio-Based Friction Compound Development Technology

- Carbon Ceramic & Advanced Composite Brake Disc Technology for Performance & Weight Reduction Applications

- Automatic Emergency Braking (AEB), Predictive Braking & ADAS-Integrated Brake Control Technology

- Electric Brake Booster (EBB), Integrated Brake System & Electrohydraulic Control Unit Technology

- Brake Condition Monitoring, Wear Sensing & Predictive Maintenance Technology for Connected Vehicles

- Patent & IP Landscape in Automotive Brake System, Friction Material & Brake-by-Wire Technologies

- Value Chain & Supply Chain Analysis

- Friction Material, Brake Pad & Brake Lining Raw Material & Manufacturing Supply Chain

- Cast Iron, Aluminium & Carbon Ceramic Brake Disc & Drum Manufacturing Supply Chain

- Brake Caliper, Hydraulic & Electric Parking Brake Caliper Casting & Assembly Supply Chain

- Brake Master Cylinder, Hydraulic Booster & Integrated Brake Unit Assembly Supply Chain

- Electronic Brake Control Module (EBCM), ABS & ESC ECU & Power Electronics Supply Chain

- OEM Tier 1 System Integrator, Vehicle Manufacturer & OES Aftermarket Channel

- Independent Aftermarket (IAM) Distributor, Retailer & E-Commerce Channel

- Pricing Analysis

- OEM Brake System & Subsystem Unit Pricing Analysis by System Type & Vehicle Segment

- Brake Pad & Friction Material Pricing: NAO, Semi-Metallic, Ceramic & Low-Metallic Tier Benchmarking

- Brake Disc & Rotor Pricing: Cast Iron, Coated & Carbon Ceramic Product Tier Analysis

- Brake-by-Wire & Integrated Brake System Incremental Cost vs. Conventional Hydraulic System Benchmarking

- Aftermarket Pricing Analysis: OES vs. IAM vs. E-Commerce Channel Price Positioning by Component & Vehicle Segment

- Total Cost of Ownership (TCO) Analysis: Brake System Replacement Frequency, Aftermarket Revenue Cycle & EV Impact on Friction Component Demand

- Sustainability & Environmental Analysis

- Brake Wear Particle & Non-Exhaust Emission (NEE) Reduction: Copper-Free Pad Adoption, Low-Dust Friction Material & Euro 7 Compliance Roadmap

- Regenerative Braking & Friction Brake Usage Reduction in EVs: Lifecycle Wear Material Saving & Particulate Emission Abatement Quantification

- Lifecycle Assessment (LCA) of Brake System Components: Raw Material Extraction, Manufacturing Energy & End-of-Life Recyclability

- Circular Economy in Brake Manufacturing: Cast Iron Disc Recycling, Friction Material Waste Management & Remanufactured Component Programs

- Regulatory-Driven Sustainability: Euro 7 NEE Limits, RoHS & REACH Compliance, Conflict Mineral Reporting & Brake System ESG Disclosure Frameworks

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by System Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by System Type, Component & Geography

- Player Classification

- Integrated Brake System Tier 1 Suppliers: Full-System OEM Development & Supply

- Specialist Friction Material & Brake Pad Manufacturers

- Brake Disc, Drum & Rotor Manufacturers

- Brake Caliper & Hydraulic Component Specialists

- Electronic Brake Control, ABS, ESC & Brake-by-Wire System Developers

- Electric Brake Booster & Integrated Brake Unit Suppliers for EV Platforms

- Independent Aftermarket (IAM) Brake Component Brands & Distributors

- Carbon Ceramic & High-Performance Brake System Specialists

- Competitive Analysis Frameworks

- Market Share Analysis by System Type, Component & Region

- Company Profile

- Company Overview & Headquarters

- Brake System Products & Technology Portfolio

- Key Customer Relationships & Reference OEM Installations

- Manufacturing Footprint & Production Capacity

- Revenue (Brake Systems Segment) & Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Market Opportunity Analysis

- Strategic Output

- Market Opportunity Matrix: By System Type, Component, Vehicle Type, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Output

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)