Market Definition

The Global Vehicle-to-Grid (V2G) and Vehicle-to-Everything (V2X) Market encompasses the development, deployment, and commercial operation of bidirectional energy transfer systems, wireless and dedicated short-range communication infrastructure, onboard communication units, roadside units, and network management platforms enabling electric vehicles to exchange power with electricity grids and communicate with infrastructure, other vehicles, pedestrians, and cloud networks. The market includes V2G inverters, charging management software, grid integration hardware, V2X chipsets, edge computing modules, and associated cybersecurity and connectivity solutions procured by utilities, automakers, fleet operators, municipalities, and telecommunications providers globally.

Market Insights

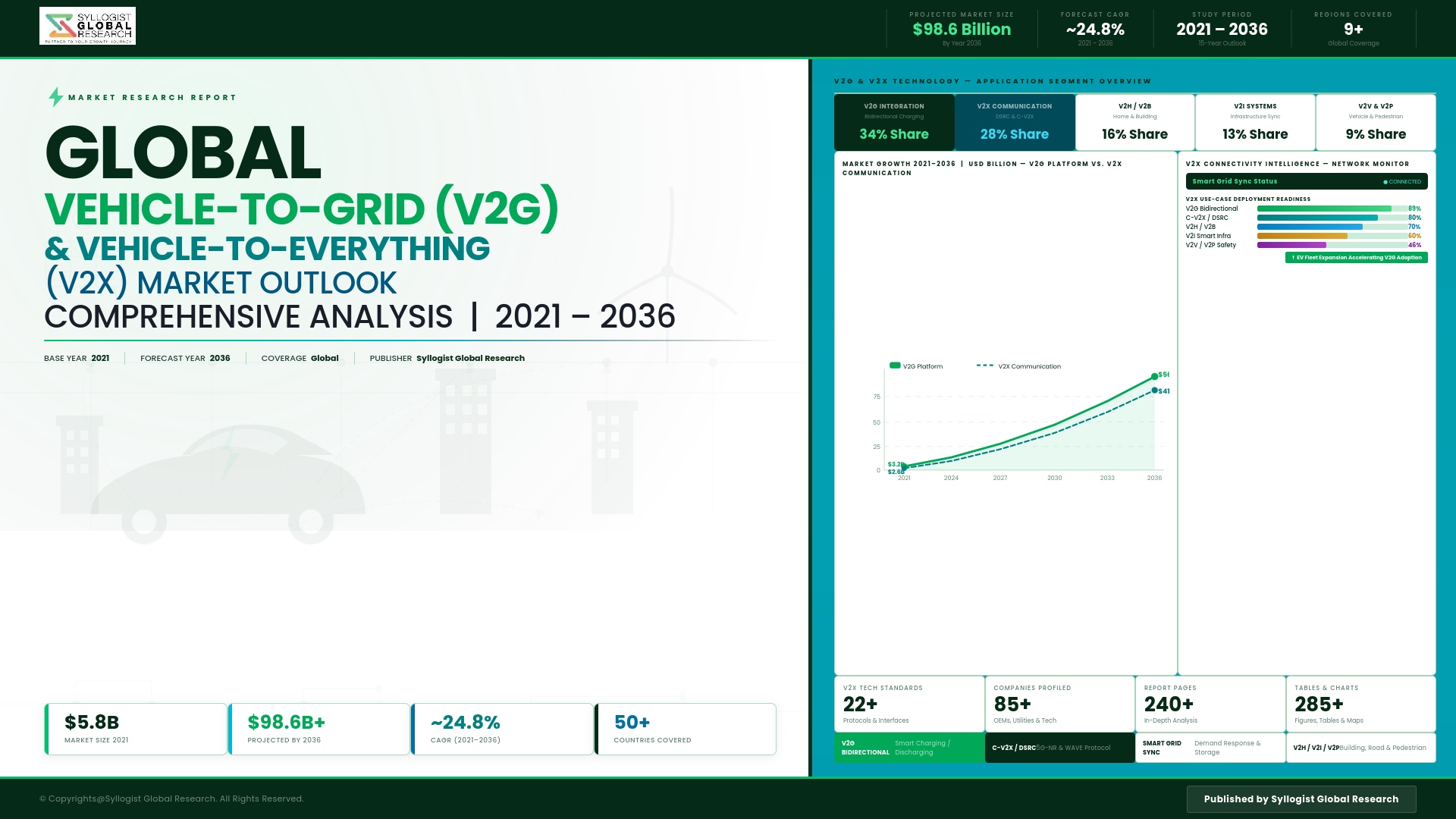

The global V2G and V2X market is entering an accelerated commercialization phase, driven by the rapid scaling of electric vehicle adoption, mounting grid stability challenges arising from intermittent renewable energy integration, and the growing recognition among utilities, policymakers, and automakers that electric vehicle fleets represent a distributed energy asset of transformative grid management potential rather than a unidirectional load burden. The market was valued at approximately USD 8.4 billion in 2025 and is projected to reach USD 74.6 billion by 2034, advancing at a compound annual growth rate of 27.5% through the forecast period, as V2G commercial deployments transition from pilot programs into utility-contracted grid services and V2X communication systems achieve mandatory regulatory status across major automotive markets in North America, Europe, and Asia-Pacific.

The V2G segment is gaining decisive commercial momentum as utilities confront the operational reality of managing grid frequency, voltage stability, and peak demand response across networks increasingly dominated by variable solar and wind generation resources, where the dispatchable stored energy capacity of aggregated electric vehicle fleets offers a commercially scalable alternative to dedicated battery storage infrastructure at substantially lower capital cost per unit of controllable capacity. Early commercial V2G deployments across the United Kingdom, the Netherlands, Japan, and the United States have demonstrated measurable grid service revenue streams for participating vehicle owners and fleet operators, with frequency regulation, peak shaving, and demand response applications generating recurring revenue that is beginning to materially improve the total cost of ownership economics for electric vehicle adoption across both private and commercial fleet segments. The aggregation layer, which enables virtual power plant operators and energy service companies to consolidate thousands of individually small V2G-capable vehicle batteries into dispatchable grid service assets of utility-relevant scale, is emerging as a high-value software and platform services market that is attracting substantial investment from energy technology companies, automotive manufacturers, and grid management software developers seeking to establish positions in the bidirectional energy services value chain.

The V2X communication segment is being propelled by regulatory mandates, autonomous vehicle safety architecture requirements, and smart city infrastructure investment programs that collectively establish V2X connectivity as a foundational enabler of both near-term vehicle safety applications and longer-term autonomous mobility deployments. The competition between cellular vehicle-to-everything and dedicated short-range communication technology standards has been substantially resolved in several major markets in favor of cellular architectures leveraging 5G network infrastructure, providing V2X with a commercially scalable deployment pathway aligned with existing telecommunications investment cycles. Asia-Pacific is projected to record the highest regional compound annual growth rate through 2034, underpinned by China’s mandatory V2X deployment programs, aggressive EV adoption targets, and smart city infrastructure investment that is integrating V2X communication into urban mobility management at national scale. Europe represents the second major contributor, with the European Union regulatory framework driving both V2G grid service market development and V2X communication infrastructure deployment across member states. North America is advancing through utility-led V2G pilot expansion and the progressive implementation of V2X communication standards within new vehicle safety regulations.

Key Drivers

Accelerating Electric Vehicle Fleet Expansion and Grid Stability Imperatives Creating Compelling Commercial Case for V2G Bidirectional Energy Services at Utility Scale

The rapid scaling of electric vehicle adoption across consumer, commercial, and fleet segments is simultaneously creating both the distributed battery capacity necessary to make V2G grid services commercially viable at utility-relevant scale and the grid management urgency that is compelling utilities to invest in V2G aggregation infrastructure as a cost-effective alternative to dedicated grid-scale battery storage installations. As EV penetration rates cross critical thresholds in leading markets, the aggregate controllable energy capacity of connected vehicle fleets is becoming large enough to meaningfully influence grid frequency regulation, peak demand management, and renewable energy balancing operations, generating utility procurement interest in V2G platform contracts that create durable multi-year revenue streams for technology developers, aggregation platform operators, and EV charging infrastructure providers serving commercial fleet and residential markets.

Autonomous and Connected Vehicle Safety Architecture Requirements and Regulatory V2X Mandates Establishing Mandatory Communication Infrastructure Deployment Across Major Automotive Markets

The architectural requirements of advanced driver assistance systems and autonomous vehicle platforms for real-time environmental awareness beyond the perception range of onboard sensor suites are driving the integration of V2X communication as a mandatory safety capability within next-generation vehicle platform designs, supported by regulatory mandates in China, the European Union, and progressively in the United States that are establishing V2X communication system installation requirements across new vehicle categories. The convergence of V2X communication with 5G network rollout programs is providing a commercially scalable deployment architecture that leverages existing telecommunications infrastructure investment rather than requiring dedicated roadside hardware deployment at the scale historically required by purely dedicated short-range communication approaches, materially reducing the infrastructure investment barrier to widespread V2X adoption.

Renewable Energy Integration Challenges and Grid Decarbonization Investment Programs Elevating V2G as a Priority Flexibility Resource Within National Energy Transition Policy Frameworks

National energy transition programs targeting high renewable energy penetration are generating structural grid flexibility deficits that are elevating V2G bidirectional charging from a commercially interesting technology demonstration into a policy-prioritized grid resource receiving dedicated regulatory support, favorable tariff structures, and direct government investment in deployment infrastructure. Electricity market regulators across the United Kingdom, Germany, the Netherlands, Japan, and Australia are developing or implementing market frameworks specifically designed to compensate V2G-enabled electric vehicle batteries for grid balancing services, creating the revenue certainty necessary to justify utility and aggregator investment in V2G platform infrastructure and to incentivize EV owners and fleet operators to participate in managed bidirectional charging programs at commercially meaningful scale.

Key Challenges

Battery Degradation Concerns, Warranty Limitations, and Consumer Acceptance Barriers Constraining Widespread Participation in V2G Bidirectional Discharging Programs

The fundamental concern that repeated bidirectional discharge cycles required by V2G grid service participation will accelerate battery degradation, reduce long-term energy storage capacity, and void manufacturer warranty coverage is creating significant consumer and fleet operator reluctance to enroll vehicles in V2G programs, constraining the aggregated capacity available to utility and aggregator platforms below commercially optimal levels despite growing EV adoption rates. Resolving this barrier requires battery management system sophistication capable of demonstrating empirically that optimized V2G dispatch protocols operating within defined state-of-charge and thermal management parameters do not materially accelerate degradation beyond normal usage patterns, alongside automotive manufacturer warranty policy evolution that explicitly accommodates certified V2G program participation without triggering warranty exclusions.

V2X Communication Technology Fragmentation, Standardization Gaps, and Interoperability Complexity Across Cellular and Dedicated Short-Range Communication Architectures Delaying Deployment at Scale

The protracted competition between cellular vehicle-to-everything and dedicated short-range communication technology standards across different regulatory jurisdictions has created vehicle platform and infrastructure investment uncertainty that has delayed automaker integration decisions, fragmented roadside infrastructure procurement, and complicated cross-border vehicle operation in regions where adjacent countries have adopted differing communication architecture mandates. Although cellular architectures have gained regulatory preference in several major markets, the absence of globally harmonized V2X communication standards continues to impose interoperability complexity on multinational automotive platforms, international fleet operations, and cross-border infrastructure deployment programs that require simultaneous support for multiple communication protocols within single vehicle and roadside unit hardware implementations.

Grid Infrastructure Upgrade Requirements, Utility Interconnection Complexity, and Regulatory Tariff Framework Immaturity Constraining Commercial V2G Deployment Timelines and Revenue Certainty

The commercial deployment of V2G services at grid-relevant scale requires utility distribution network upgrades to accommodate bidirectional power flows across residential and commercial charging infrastructure that existing grid interconnection architecture and protection systems were not designed to manage, creating capital investment requirements and regulatory approval timelines that substantially extend V2G deployment schedules beyond technology readiness milestones. The immaturity of electricity market tariff frameworks governing compensation for V2G grid services, including the absence of standardized interconnection agreements, net metering provisions accommodating vehicle discharge, and real-time energy pricing signals accessible to aggregation platforms, creates revenue uncertainty that undermines the business case for V2G infrastructure investment by utilities, charging network operators, and fleet managers contemplating program participation commitments.

Market Segmentation

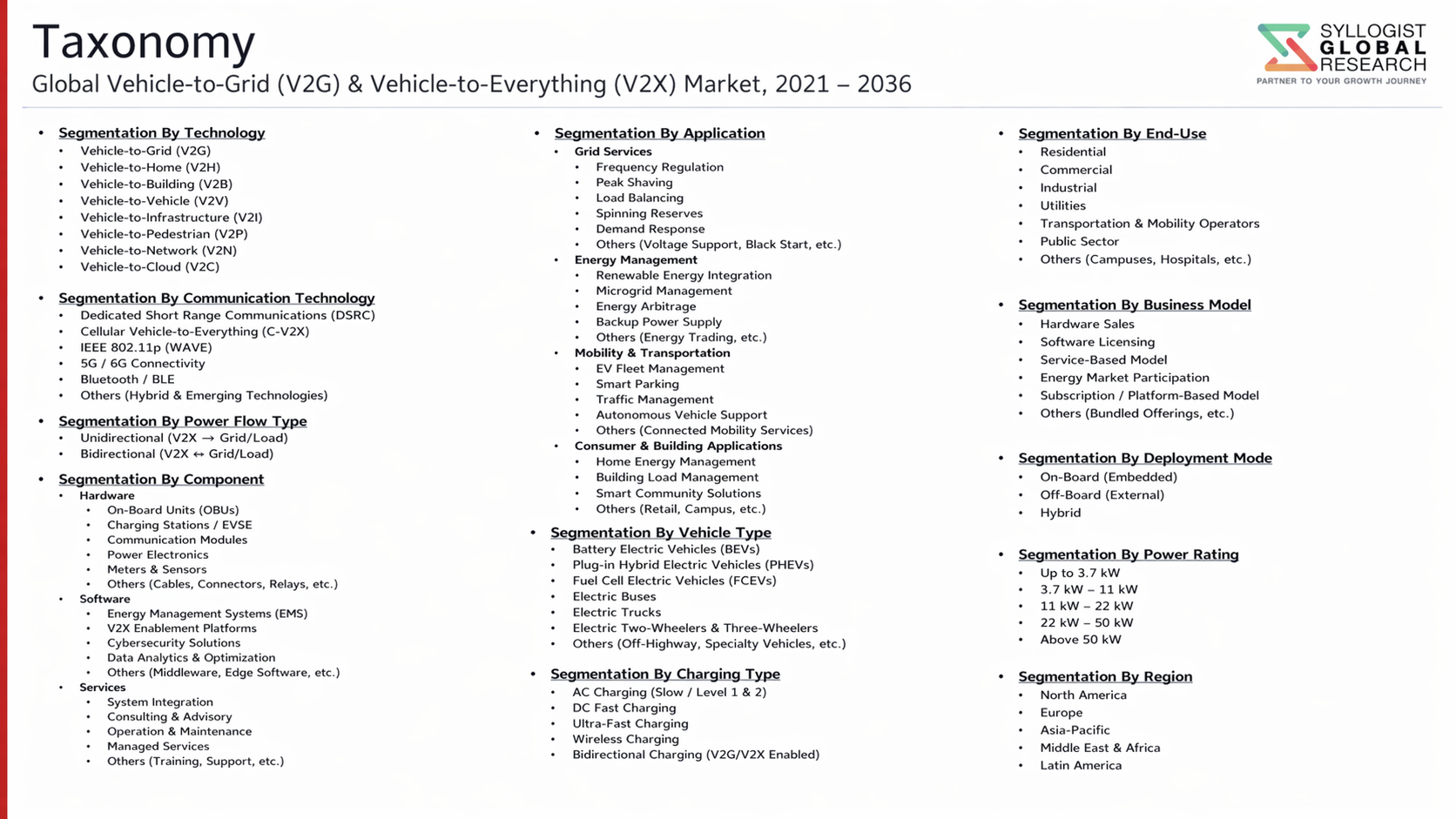

- Segmentation By Technology Type

- Vehicle-to-Grid (V2G) Bidirectional Charging Systems

- Vehicle-to-Home (V2H) Energy Management Systems

- Vehicle-to-Building (V2B) Integration Platforms

- Vehicle-to-Vehicle (V2V) Communication Systems

- Vehicle-to-Infrastructure (V2I) Communication Systems

- Vehicle-to-Pedestrian (V2P) Safety Systems

- Vehicle-to-Network (V2N) Cloud Connectivity Platforms

- Others

- Segmentation By Communication Standard

- Cellular Vehicle-to-Everything (C-V2X) and 5G NR-V2X

- Dedicated Short-Range Communication (DSRC) and IEEE 802.11p

- Combined C-V2X and DSRC Hybrid Architectures

- Others

- Segmentation By Application

- Grid Frequency Regulation and Ancillary Services

- Peak Demand Management and Load Shifting

- Renewable Energy Integration and Balancing

- Autonomous and Connected Vehicle Safety

- Smart Traffic Management and Signal Priority

- Emergency Vehicle and Vulnerable Road User Alerts

- Fleet Energy Management and Optimization

- Others

- Segmentation By Component

- V2G Bidirectional Inverters and Charging Hardware

- Onboard Communication Units (OBU)

- Roadside Units (RSU) and Infrastructure Hardware

- V2X Chipsets and Modems

- Energy Management and Aggregation Software Platforms

- Cybersecurity and Network Management Solutions

- Others

- Segmentation By Vehicle Type

- Battery Electric Vehicles (BEV)

- Plug-in Hybrid Electric Vehicles (PHEV)

- Commercial Electric Trucks and Buses

- Electric Two-Wheelers and Micro-Mobility Vehicles

- Autonomous and Connected Vehicles

- Others

- Segmentation By End User

- Electric Utilities and Grid Operators

- Automotive Original Equipment Manufacturers

- Commercial and Municipal Fleet Operators

- Residential and Commercial Building Owners

- Charging Network and Energy Service Providers

- Smart City and Municipal Authorities

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the V2G and V2X Market in 2025, projected through 2034, disaggregated by technology type, application, and component, enabling utilities, automakers, technology developers, and investors to identify the highest-growth segments and most durable revenue opportunities across the bidirectional energy and connected vehicle communication landscape?

- How are electric utilities, automotive manufacturers, and energy aggregators structuring V2G commercial deployment programs across grid frequency regulation, peak demand management, and renewable integration applications, and which market and tariff frameworks are defining the revenue models and procurement benchmarks shaping V2G platform adoption through 2034?

- What is the current regulatory status of V2X communication mandates across China, the European Union, and the United States, and how are automakers and infrastructure developers navigating the competition between cellular V2X and dedicated short-range communication standards within active vehicle platform development and roadside infrastructure deployment programs?

- Which V2G and V2X application segments, including grid ancillary services, autonomous vehicle safety communication, and fleet energy management, are generating the highest near-term adoption and revenue growth rates, and what technology performance and interoperability capabilities are most critical to platform commercial success through 2034?

- How is the competitive landscape structured among automotive OEMs, energy technology companies, telecommunications providers, and V2G aggregation platform developers, and what partnership, ecosystem integration, and utility contract strategies are enabling leading players to establish durable market positions in the V2G and V2X value chain?

- What battery degradation, warranty, grid interconnection, and regulatory tariff challenges are constraining V2G commercial participation rates, and how are technology developers, automakers, utilities, and policymakers addressing these barriers to expand the pool of grid-eligible EV capacity at commercially and operationally meaningful scale?

- Which regional markets, specifically Asia-Pacific, Europe, and North America, are expected to generate the most substantial incremental V2G and V2X investment through 2034, and what EV adoption trajectories, grid decarbonization mandates, smart city programs, and autonomous vehicle regulatory frameworks are driving technology investment priorities in each region?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Battery Degradation, Warranty Liability & EV Owner Willingness-to-Participate Risk in V2G Programs

- Grid Cybersecurity, Vehicle Network Vulnerability & Data Privacy Risk in V2X-Connected Ecosystems

- Regulatory Fragmentation, Utility Tariff Structure Incompatibility & Grid Code Compliance Risk Across Jurisdictions

- Interoperability, Multi-Standard Complexity & Communication Protocol Fragmentation Risk (OCPP, ISO 15118, DSRC, C-V2X)

- EV Adoption Rate Uncertainty, Fleet Availability for Grid Services & Aggregator Business Model Viability Risk

- Regulatory Framework & Standards

- ISO 15118 Vehicle-to-Grid Communication Interface Standard & Plug-and-Charge (PnC) Protocol Framework

- IEC 61851, SAE J1772, CHAdeMO & Combined Charging System (CCS) Standards Governing V2G Bidirectional Charging Equipment

- ETSI EN 302 663, IEEE 802.11p DSRC, 3GPP C-V2X (LTE-V2X & 5G NR-V2X) & ETSI ITS-G5 Communication Standards for V2X

- Grid Code, Demand Response Program Rules, Virtual Power Plant (VPP) Licensing & Distributed Energy Resource (DER) Integration Regulations

- EV Mandate Policies, Smart Charging Directives & V2G Incentive Frameworks: EU AFIR, US NEVI Program, UK Smart EV Charging Regulations & National EV Strategies

- Global Vehicle-to-Grid (V2G) & Vehicle-to-Everything (V2X) Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Number of V2G-Enabled Units & V2X-Connected Vehicles)

- Market Size & Forecast by Technology

- Vehicle-to-Grid (V2G): Bidirectional Charging & Energy Dispatch to the Grid

- Vehicle-to-Home (V2H): Residential Energy Supply & Home Backup Power

- Vehicle-to-Building (V2B): Commercial & Industrial Facility Energy Management

- Vehicle-to-Load (V2L): Direct Appliance & Equipment Power Delivery from EV Battery

- Vehicle-to-Vehicle (V2V): Inter-Vehicle Communication for Safety & Cooperative Driving

- Vehicle-to-Infrastructure (V2I): Communication with Traffic Management & Road Infrastructure

- Vehicle-to-Network (V2N): Cloud, Cellular & Mobile Network Connectivity for Fleet & Traffic Management

- Vehicle-to-Pedestrian (V2P): Vulnerable Road User Detection & Collision Avoidance Communication

- Market Size & Forecast by Component

- Bidirectional On-Board Charger (OBC) & Power Electronics

- Bidirectional Electric Vehicle Supply Equipment (EVSE) & Charging Station Hardware

- V2X Communication Unit: On-Board Unit (OBU) & Roadside Unit (RSU)

- Energy Management System (EMS), Aggregation Platform & Virtual Power Plant (VPP) Software

- Battery Management System (BMS) with V2G Capability

- Cybersecurity & Authentication Software for V2G and V2X Ecosystems

- Cloud Platform, Data Analytics & Fleet Management Software

- Market Size & Forecast by Communication Technology

- Dedicated Short-Range Communications (DSRC) & IEEE 802.11p

- Cellular Vehicle-to-Everything (C-V2X): LTE-V2X (PC5 & Uu Interface)

- 5G NR-V2X: Ultra-Reliable Low-Latency Communication (URLLC) for Advanced V2X Use Cases

- Wi-Fi & Wireless LAN-Based V2X Communication

- Power Line Communication (PLC) for V2G Charging & ISO 15118 Implementation

- Market Size & Forecast by Charging Standard

- Combined Charging System (CCS) Combo 1 & Combo 2 with ISO 15118 Bidirectional Protocol

- CHAdeMO 3.0 (ChaoJi) Bidirectional Charging Standard

- GB/T 27930 & GB/T 20234 Chinese National Bidirectional Charging Standard

- North American Charging Standard (NACS) with Bidirectional Capability

- Wireless Power Transfer (WPT) & Dynamic Wireless Charging with V2G Capability

- Market Size & Forecast by Vehicle Type

- Battery Electric Vehicles (BEVs): Passenger Cars

- Battery Electric Vehicles (BEVs): Light Commercial Vehicles & Vans

- Battery Electric Vehicles (BEVs): Electric Buses & Coaches

- Battery Electric Vehicles (BEVs): Electric Heavy-Duty Trucks & Freight Vehicles

- Plug-in Hybrid Electric Vehicles (PHEVs)

- Electric Two-Wheelers & Three-Wheelers

- Market Size & Forecast by Application

- Grid Frequency Regulation & Ancillary Services

- Peak Shaving, Load Shifting & Demand Response

- Renewable Energy Integration & Grid Balancing

- Home & Building Energy Self-Sufficiency & Backup Power

- Fleet Depot Energy Management & Commercial V2G Aggregation

- Connected & Autonomous Vehicle (CAV) Safety & Traffic Management

- Smart City, Intelligent Transport System (ITS) & Urban Mobility Management

- Market Size & Forecast by End-User

- Private EV Owners & Residential Consumers

- Commercial Fleet Operators & Last-Mile Delivery Companies

- Public Transport Authorities & Electric Bus Fleet Operators

- Electric Utilities, Grid Operators & Energy Retailers

- Charge Point Operators (CPOs) & Mobility Service Providers

- Smart City Authorities & Intelligent Transport System Operators

- Automotive OEMs & EV Manufacturers

- Market Size & Forecast by Sales Channel

- Automotive OEM Direct Integration & Vehicle-Bundled V2G Solution

- Charge Point Operator (CPO) & EVSE Manufacturer Direct Sales

- Energy Retailer, Utility & Virtual Power Plant (VPP) Aggregator Channel

- Systems Integrator, Smart Building & Energy Management Solution Partner

- North America Vehicle-to-Grid (V2G) & Vehicle-to-Everything (V2X) Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of V2G-Enabled Units & V2X-Connected Vehicles)

- By Technology

- By Component

- By Communication Technology

- By Charging Standard

- By Vehicle Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Vehicle-to-Grid (V2G) & Vehicle-to-Everything (V2X) Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of V2G-Enabled Units & V2X-Connected Vehicles)

- By Technology

- By Component

- By Communication Technology

- By Charging Standard

- By Vehicle Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Vehicle-to-Grid (V2G) & Vehicle-to-Everything (V2X) Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of V2G-Enabled Units & V2X-Connected Vehicles)

- By Technology

- By Component

- By Communication Technology

- By Charging Standard

- By Vehicle Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Vehicle-to-Grid (V2G) & Vehicle-to-Everything (V2X) Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of V2G-Enabled Units & V2X-Connected Vehicles)

- By Technology

- By Component

- By Communication Technology

- By Charging Standard

- By Vehicle Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Vehicle-to-Grid (V2G) & Vehicle-to-Everything (V2X) Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of V2G-Enabled Units & V2X-Connected Vehicles)

- By Technology

- By Component

- By Communication Technology

- By Charging Standard

- By Vehicle Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Vehicle-to-Grid (V2G) & Vehicle-to-Everything (V2X) Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of V2G-Enabled Units & V2X-Connected Vehicles)

- By Technology

- By Component

- By Communication Technology

- By Charging Standard

- By Vehicle Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Norway, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Technology Landscape & Innovation Analysis

- Bidirectional On-Board Charger (OBC), Power Electronics & Inverter Technology Deep-Dive for V2G Applications

- ISO 15118-20 Bidirectional Power Transfer (BPT), Plug-and-Charge (PnC) & Smart Charging Protocol Technology

- 5G NR-V2X, C-V2X & DSRC Communication Technology: Architecture, Latency & Reliability Benchmarking

- Virtual Power Plant (VPP), Aggregation Platform & AI-Driven Energy Management Technology for V2G Fleets

- Battery Management System (BMS) Optimisation, State-of-Health Monitoring & Degradation Mitigation Technology for V2G Cycling

- Wireless Power Transfer (WPT), Dynamic Wireless EV Charging & V2G Integration Technology

- Cybersecurity, PKI Authentication & Secure Communication Architecture for V2G and V2X Ecosystems

- Patent & IP Landscape in V2G Bidirectional Charging & V2X Communication Technologies

- Value Chain & Supply Chain Analysis

- Bidirectional Power Electronics, Semiconductor (SiC & GaN) & OBC Component Manufacturing Supply Chain

- V2X Communication Chipset, On-Board Unit (OBU) & Roadside Unit (RSU) Hardware Supply Chain

- Bidirectional EVSE, Charging Station & Grid Interface Equipment Manufacturing Supply Chain

- Battery Cell, Pack & BMS Supply Chain with V2G Cycle Durability Requirements

- Software Platform, EMS, Aggregation & VPP Technology Developer Supply Chain

- Automotive OEM, EV Integrator & Charge Point Operator End-User Channel

- Energy Retailer, Utility, Grid Operator & Demand Response Aggregator Channel

- Pricing Analysis

- Bidirectional EVSE & V2G Charging Station Hardware Capital Cost Analysis by Power Level & Standard

- Bidirectional OBC & Power Electronics System Cost: Vehicle-Level Incremental Cost vs. Unidirectional Benchmark

- V2X On-Board Unit (OBU) & Roadside Unit (RSU) Hardware Unit Cost Analysis by Communication Technology

- VPP Aggregation Platform, EMS Software & Subscription Pricing Analysis for V2G Fleet Operators

- Revenue Model Analysis: Grid Service Revenue, Frequency Regulation Payment & Demand Response Compensation Benchmarking

- Total Cost of Ownership (TCO) & Payback Period Analysis for V2G-Enabled EV Programs by End-User Segment

- Sustainability & Environmental Analysis

- V2G Contribution to Grid Decarbonisation: Avoided Peaker Plant Capacity, Renewable Curtailment Reduction & CO2 Abatement Quantification

- Battery Lifecycle Impact of V2G Cycling: Accelerated Degradation, Second-Life Battery Utilisation & End-of-Life Management

- V2X-Enabled Traffic Optimisation, Eco-Driving & Vehicle Platooning: Fuel Consumption & Emissions Reduction Contribution

- Circular Economy in V2G Hardware: Bidirectional Charger Recyclability, Critical Material Recovery & Supply Chain Sustainability

- Regulatory-Driven Sustainability: EU Green Deal, IEA Net Zero Scenario, Smart Charging Mandates & EV Grid Integration ESG Disclosure

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Technology & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Technology, Component & Geography

- Player Classification

- Automotive OEMs with Integrated V2G & V2X Technology in Production Vehicles

- Dedicated V2G Bidirectional EVSE & Charging Equipment Manufacturers

- V2X Communication Chipset & On-Board Unit (OBU) Technology Providers

- VPP Aggregation Platform, EMS & Smart Charging Software Vendors

- Charge Point Operators (CPOs) Deploying Bidirectional V2G Infrastructure

- Energy Retailers, Utilities & Grid Operators Running V2G Programs

- Semiconductor Manufacturers Supplying SiC & GaN Power Devices for Bidirectional Applications

- Telecommunications Operators & Infrastructure Providers Supporting C-V2X & 5G V2X Networks

- Competitive Analysis Frameworks

- Market Share Analysis by Technology, Component & Region

- Company Profile

- Company Overview & Headquarters

- V2G & V2X Products & Technology Portfolio

- Key Customer Relationships & Reference Program Installations

- Manufacturing Footprint & Production Capacity

- Revenue (V2G & V2X Segment) & Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Market Opportunity Analysis

- Strategic Output

- Market Opportunity Matrix: By Technology, Component, Vehicle Type, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Output

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)